Copyright © 2008 Pearson Education Canada8-1

Chapter 8

Saving and Investing

8-2

Copyright © 2008 Pearson Education Canada

How Much Do Canadians Save? Most Canadians don’t save enough

Spend more than they earn Tend to have very low or negative

savings rates

8-3

Copyright © 2008 Pearson Education Canada

Four Reasons to Save

1. Emergencies2. Liquidity3. Short-term goals4. Long-term goals

8-4

Copyright © 2008 Pearson Education Canada

1. Save for an Emergency Readily accessible funds

For unexpected expenses E.G. 3 months’ take home pay

Savings account, term deposit, CSB’s

Insurance protection Property Dependants

8-5

Copyright © 2008 Pearson Education Canada

2. Save for Liquidity Needs For unevenness in cash flow To pay for infrequent large

expenses E.G. One months’ take-home pay

Deposit that permits checking

8-6

Copyright © 2008 Pearson Education Canada

3. Save for Short-term Goals Things to be accomplished in next

five years Snowmobile, car, holiday,

computer, home down-payment Low risk securities

With appropriate maturities

8-7

Copyright © 2008 Pearson Education Canada

4. Save for Long-term Goals Typical goals

Enhance financial security Achieve financial independence Achieve comfortable lifestyle during

retirement Start planning early Invest in securities that have

prospects for long-term growth

8-8

Copyright © 2008 Pearson Education Canada

Two Approaches to Saving

1. Pay yourself first Take savings off the top of each

paycheck Before spending anything

2. Pay yourself last Save what is left at the end of each

pay period Not recommended

8-9

Copyright © 2008 Pearson Education Canada

Rules for Saving Set goals Plan Regular contributions

8-10

Copyright © 2008 Pearson Education Canada

Saving Versus Investing Saving

Means not spending Passive approach to wealth

accumulation Little risk but little return

Investing Committing capital to earn a return Active approach to wealth accumulation More risk but more larger return

8-11

Copyright © 2008 Pearson Education Canada

Why Invest? Growth Hobby

8-12

Copyright © 2008 Pearson Education Canada

Two Basic Ways to Invest

1. Debt Lending money

Deposits accounts, bonds, treasury bills, mortgages

2. Equity Acquiring ownership

Business, real estate, jewelry, stocks, gold, silver

8-13

Copyright © 2008 Pearson Education Canada

Investment Objectives Return on investment Current income Liquidity Inflation protection Management effort Tax reduction

8-14

Copyright © 2008 Pearson Education Canada

Forms of Investment Return

1. Income Profit, dividends, interest, rent

2. Capital gain Capital appreciation

Increase in asset value

8-15

Copyright © 2008 Pearson Education Canada

Characteristics of Investments Risk/return trade-off Liquidity Marketability Term Management effort required Income tax treatment

8-16

Copyright © 2008 Pearson Education Canada

Factors Inversely Related to Return on Investment Safety of principal Accessibility of funds Liquidity Inattention to securities

management

8-17

Copyright © 2008 Pearson Education Canada

Investment Risks Inflation risk

Loss of purchasing power Interest rate risk

Inverse relationship Market risk

Price of asset may fall Business risk

Business performs poorly

8-18

Copyright © 2008 Pearson Education Canada

Risk Management Balance investments and other risks

Life cycle risk Older people prefer less risk

Income and risk People with secure income tolerate more

risk

Diversify investments Variety of investments

Spread risk

8-19

Copyright © 2008 Pearson Education Canada

Minimizing Risk Influenced by

Time spent studying investments Knowledge about the future

8-20

Copyright © 2008 Pearson Education Canada

Knowledge Economic conditions in general The specific marketplace

Stock market Bond market Real estate market

Specific stocks and bonds and real estate

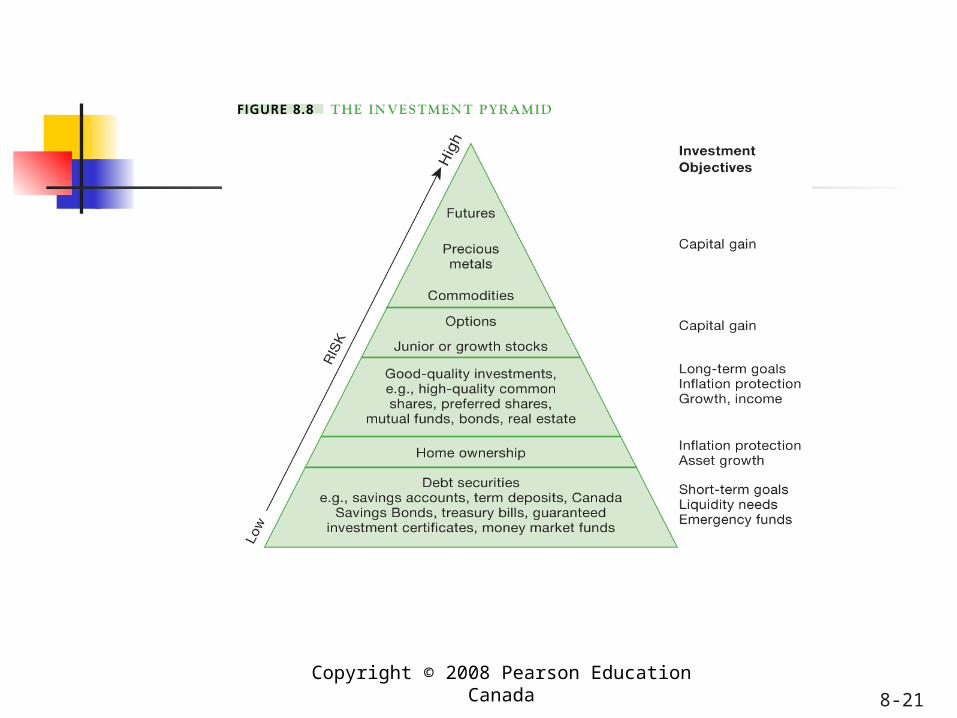

8-21

Copyright © 2008 Pearson Education Canada

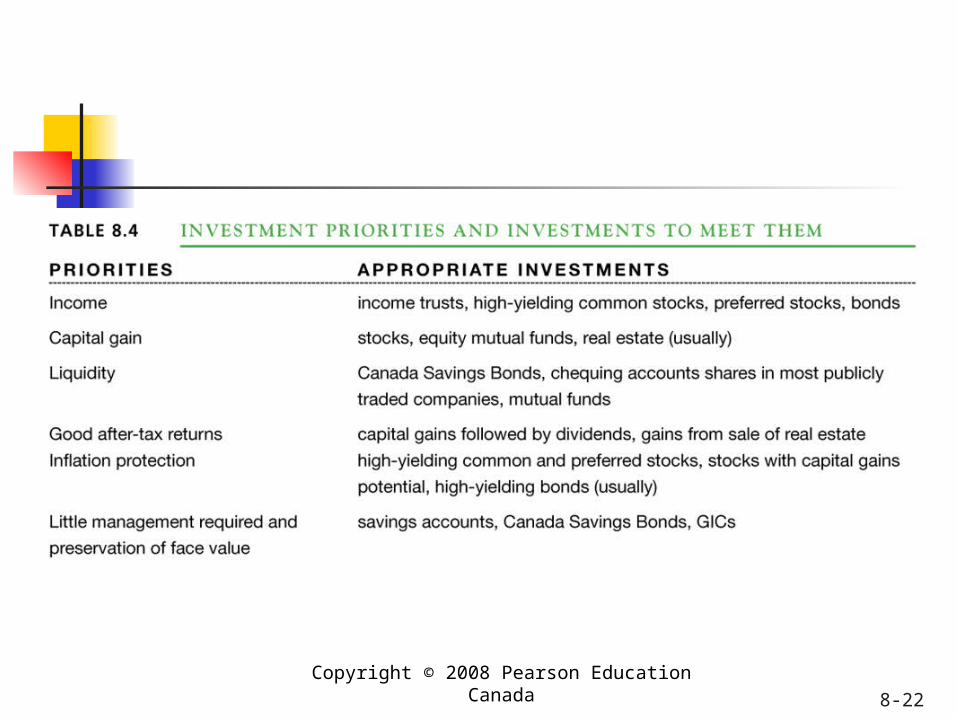

8-22

Copyright © 2008 Pearson Education Canada

8-23

Copyright © 2008 Pearson Education Canada

8-24

Copyright © 2008 Pearson Education Canada