Copyright © 2003 by M. Ray Gregg. All rights reserved. 1

Men Women

6 p.m., Monday noon, Monday

6 p.m., Tuesday * 2:00 p.m., Tuesday *

* on ESPN * on ESPNU

Copyright © 2003 by M. Ray Gregg. All rights reserved. 2

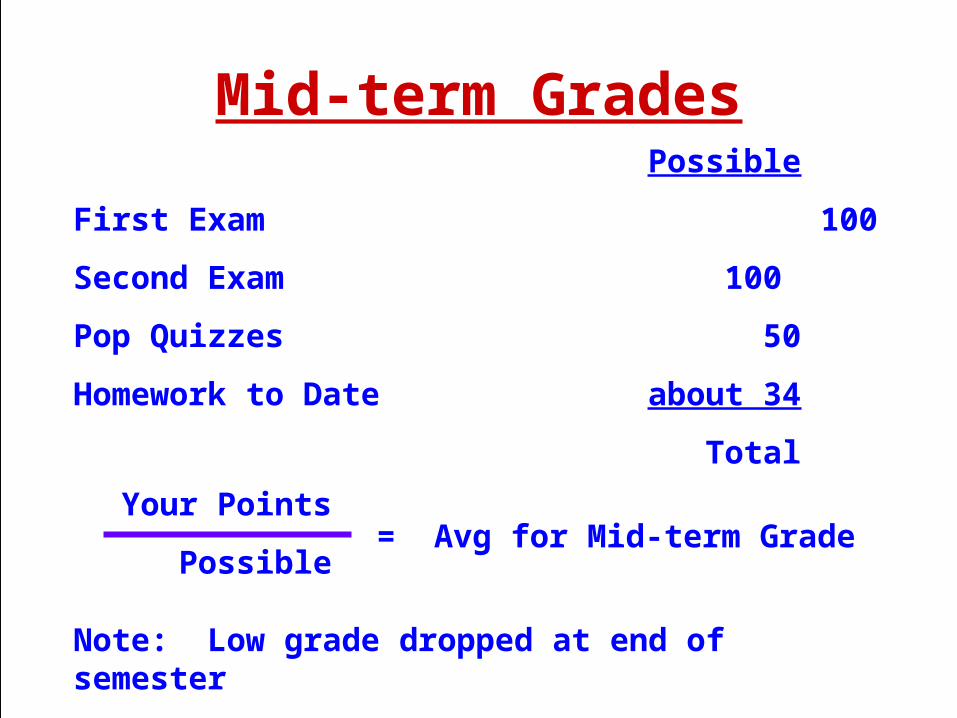

Mid-term GradesMid-term grades will be submitted this week. Shortly thereafter, you will be able to view them on Vision, accessible through the ORU home page.

A printed copy of mid-term grades will be mailed only to the parents of undergraduate dependent students.

Copyright © 2003 by M. Ray Gregg. All rights reserved. 3

Mid-term GradesPossible

First Exam 100

Second Exam 100

Pop Quizzes 50

Homework to Date about 34

Total

Your Points

Possible= Avg for Mid-term Grade

Note: Low grade dropped at end of semester

ManufacturingProcess Cost Accounting

Copyright © 2003 by M. Ray Gregg. All rights reserved. 5

Overview• Which method for which industry?• Similarities and Differences• Allocation of Costs

– Equivalent Units– FIFO vs. Weighted Average– Steps

• Cost of Goods– Finished– Not Finished

Copyright © 2003 by M. Ray Gregg. All rights reserved. 6

ComparisonJob Order Process

Wide variety of distinct products

Homogenous products

Costs accumulated by jobs

Costs accumulated in departments

Unit cost determined by dividing cost of job by # of units

Unit cost determined by dividing process costs of period by units produced during period

Copyright © 2003 by M. Ray Gregg. All rights reserved. 9

ComparisonJob Order Process

Print Shop Publisher

Auto Mechanic Auto Manufacturer

Furniture Upholster Furniture Manufacturer

Copyright © 2003 by M. Ray Gregg. All rights reserved. 11

ComparisonJob Order Process

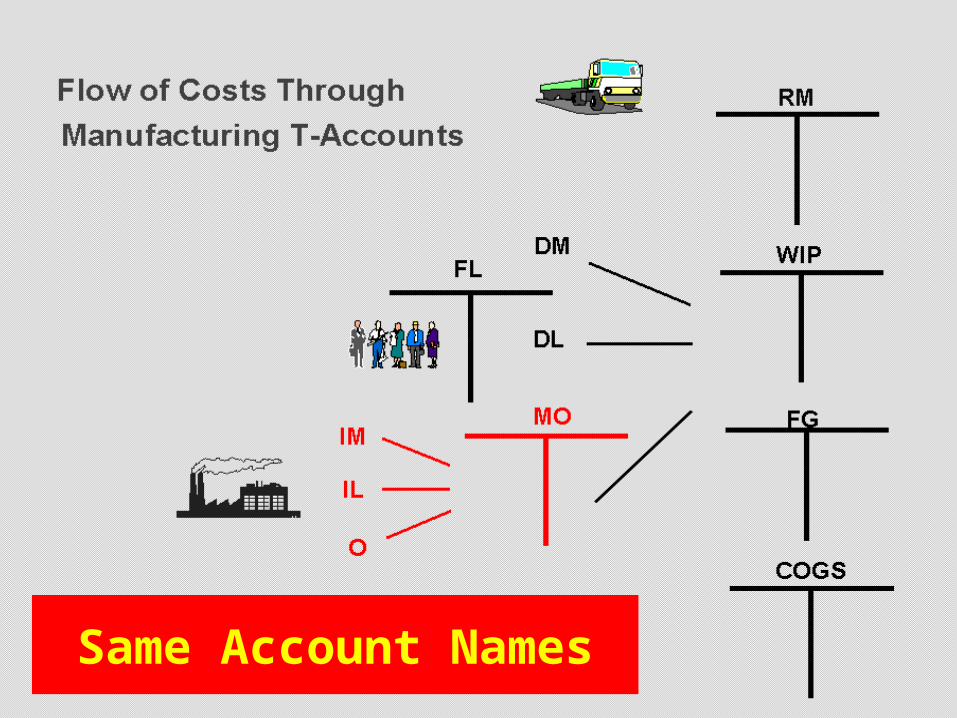

Copyright © 2003 by M. Ray Gregg. All rights reserved. 14Same Account Names

Copyright © 2003 by M. Ray Gregg. All rights reserved. 15

Same Elements of Cost

Copyright © 2003 by M. Ray Gregg. All rights reserved. 16

Different Approachto Finished Goods

Copyright © 2003 by M. Ray Gregg. All rights reserved. 17

Copyright © 2003 by M. Ray Gregg. All rights reserved. 19

WIP - A WIP - B WIP - C

Process CostsAccumulated by Departments

Departments vs.Job Cost Sheets

Copyright © 2003 by M. Ray Gregg. All rights reserved. 21

Copyright © 2003 by M. Ray Gregg. All rights reserved. 22

Equivalent Units of Production

• A measure of productive effort expressed in fully completed units

• Becomes the basis for the allocation of costs

Copyright © 2003 by M. Ray Gregg. All rights reserved. 24

Production Time Line

Conversion Costs Added Throughout the Process

Materials Addedat the Beginningof the Process

Unfinished Units

Beginning Inventory

Copyright © 2003 by M. Ray Gregg. All rights reserved. 26

Production Time LineMaterials Addedat the Beginningof the Process

Goods finished and “transferred

out”

Conversion Costs Added Throughout the Process

Unfinished Units

Beginning Inventory

Copyright © 2003 by M. Ray Gregg. All rights reserved. 27

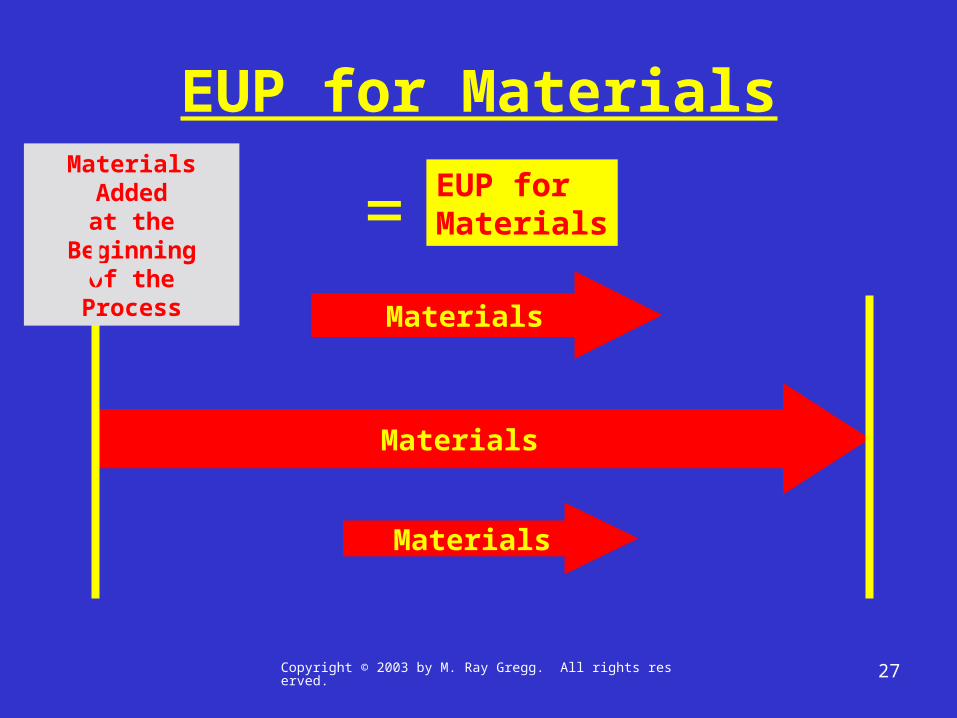

EUP for Materials

Materials

Materials Addedat the Beginningof the Process

Materials

Materials

EUP forMaterials=

Copyright © 2003 by M. Ray Gregg. All rights reserved. 28

EUP for Conversion Costs

Finished

Materials Addedat the Beginningof the Process

Unfinished Units

EUP forConversion Costs

=

Beg Inv

Copyright © 2003 by M. Ray Gregg. All rights reserved. 29

Allocating Process Costs

• FIFO Method– For a long, long time!– Tied for 1st place (with Bonds) for difficulty

• Weighted Average Method– 6th edition – 2003– “It is the method most widely used in practice.” –

W,K,K– “…is simpler than the FIFO method…” – H,H,B pg

862– “But W-A costs per EUP are not as useful for

evaluating the efficiency [for the period] because they are affected by costs incurred [in the previous period].” -- H,H,B pg 865

Copyright © 2003 by M. Ray Gregg. All rights reserved. 30

Allocating Process Costs1. Determine “physical flow” in units2. Determine EUP

• for materials and• for conversion costs

3. Determine unit costs• for materials• for conversion costs• and total

4. Allocate costs incurred to goods• Finished and• Not Finished

Copyright © 2003 by M. Ray Gregg. All rights reserved. 32

IllustrationX Company has several processing departments. Costs charged to Department 1 for February totaled $258,600 as follows:

Work in Process, 2/1Materials $12,000Conversion Costs 9,000 $21,000

Materials added 72,000Labor 103,500Overhead 62,100

Records indicate that 3,000 units were in beginning Work in Process 30% complete as to conversion costs, 18,000 units were started into production, and 4,000 units were in ending work in process 60% complete as to conversion costs. Materials are entered at the beginning of each process.

Instructions: (a) Determine the equivalent units of production and the unit costs for Department 1. (b) Determine the assignment of costs to goods transferred out and in process.

Copyright © 2003 by M. Ray Gregg. All rights reserved. 33

General Ledger

BI - M 12,000 to Dept 2 ???BI - CC 9,000DM 72,000

DL 103,500MO 62,100

258,600Bal ???

Work in Process -- Dept 1

Copyright © 2003 by M. Ray Gregg. All rights reserved. 34

General Ledger

BI - M 12,000 to Dept 2 ???BI - CC 9,000DM 72,000

DL 103,500MO 62,100

258,600Bal ???

Work in Process -- Dept 1

ConversionCosts$165,600

Copyright © 2003 by M. Ray Gregg. All rights reserved. 35

Step 1: Determine physical units

PhysicalUnits

Beg Inv 3,000Started 18,000 Units TO account for 21,000

Finished 17,000Not Finished 4,000 Units ACCOUNTED for 21,000

Step 1: Determine physical units

Copyright © 2003 by M. Ray Gregg. All rights reserved. 37

Determine EUP for M and CC

Step 2: Determine EUP

Direct ConversionMaterials Costs

Finished 17,000 17,000Not Finished 4,000 2,400 Total EUP 21,000 19,400

Equivalent Units

4,000 x 60%

Copyright © 2003 by M. Ray Gregg. All rights reserved. 40

Determine EUP for M and CC

Step 2: Determine EUP

Direct ConversionMaterials Costs

Finished 17,000 17,000Not Finished 4,000 2,400 Total EUP 21,000 19,400

Equivalent Units

Copyright © 2003 by M. Ray Gregg. All rights reserved. 42

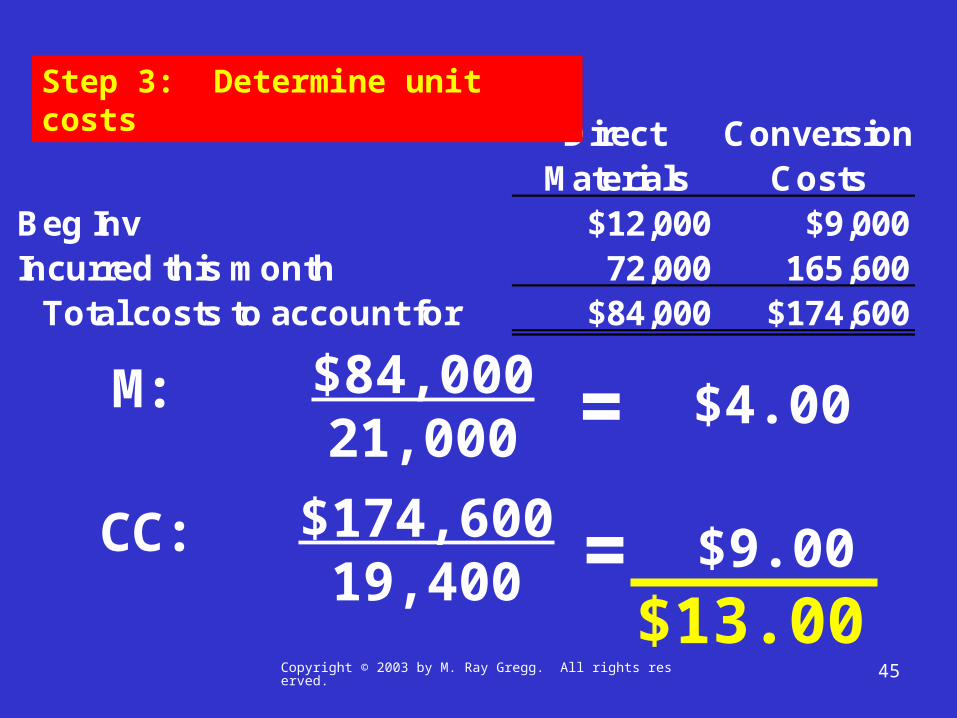

Determine unit costsStep 3: Determine unit costs

Direct ConversionMaterials Costs

Beg Inv $12,000 $9,000Incurred this month 72,000 165,600

Total costs to account for $84,000 $174,600

Copyright © 2003 by M. Ray Gregg. All rights reserved. 43

Determine unit costsDirect Conversion

Materials CostsBeg Inv $12,000 $9,000Incurred this month 72,000 165,600

Total costs to account for $84,000 $174,600

Step 3: Determine unit costs

$84,00021,000 = $4.00M:

Copyright © 2003 by M. Ray Gregg. All rights reserved. 44

Determine unit costsDirect Conversion

Materials CostsBeg Inv $12,000 $9,000Incurred this month 72,000 165,600

Total costs to account for $84,000 $174,600

Step 3: Determine unit costs

$84,00021,000 = $4.00M:

$174,60019,400 = $9.00CC:

Copyright © 2003 by M. Ray Gregg. All rights reserved. 45

Determine unit costsDirect Conversion

Materials CostsBeg Inv $12,000 $9,000Incurred this month 72,000 165,600

Total costs to account for $84,000 $174,600

Step 3: Determine unit costs

$84,00021,000 = $4.00M:

$174,60019,400 = $9.00CC:

$13.00

Copyright © 2003 by M. Ray Gregg. All rights reserved. 46

Determine unit costs

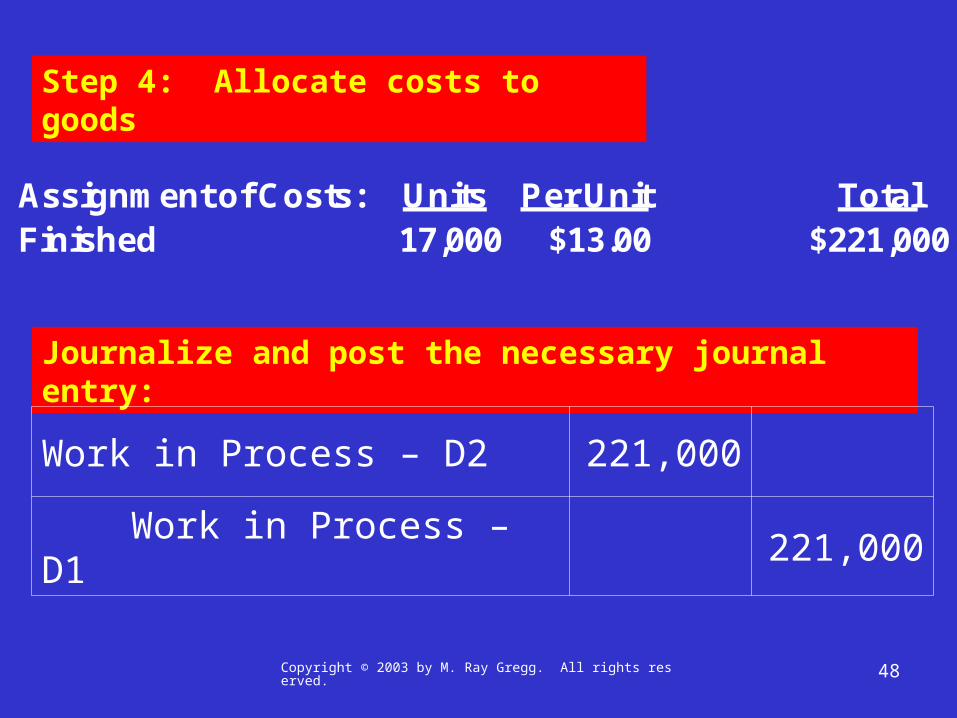

Assignment of Costs: Units Per Unit TotalFinished 17,000 $13.00 $221,000Not Finished Materials 4,000 $4.00 $16,000 CC 2,400 $9.00 21,600 37,600

Total costs accounted for $258,600

Step 4: Allocate costs to goods

Copyright © 2003 by M. Ray Gregg. All rights reserved. 47

Determine unit costs

Assignment of Costs: Units Per Unit TotalFinished 17,000 $13.00 $221,000Not Finished Materials 4,000 $4.00 $16,000 CC 2,400 $9.00 21,600 37,600

Total costs accounted for $258,600

Step 4: Allocate costs to goods

Copyright © 2003 by M. Ray Gregg. All rights reserved. 48

Determine unit costs

Assignment of Costs: Units Per Unit TotalFinished 17,000 $13.00 $221,000Not Finished Materials 4,000 $4.00 $16,000 CC 2,400 $9.00 21,600 37,600

Total costs accounted for $258,600

Step 4: Allocate costs to goods

Journalize and post the necessary journal entry:

Work in Process – D2 221,000

Work in Process – D1 221,000

Copyright © 2003 by M. Ray Gregg. All rights reserved. 49

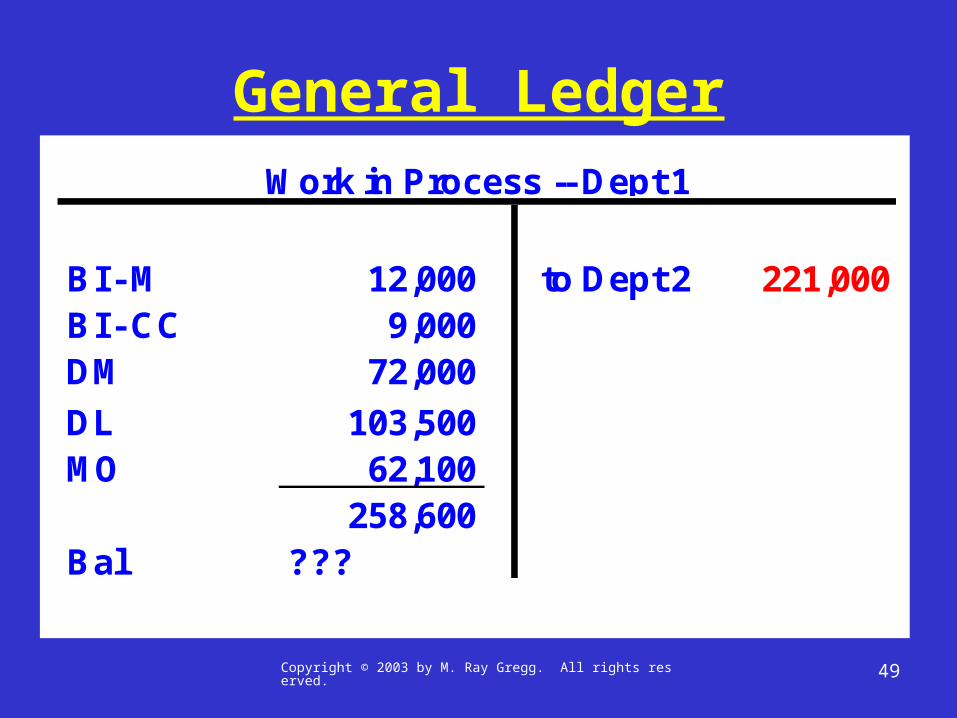

General Ledger

BI - M 12,000 to Dept 2 221,000BI - CC 9,000DM 72,000

DL 103,500MO 62,100

258,600Bal ???

Work in Process -- Dept 1

Copyright © 2003 by M. Ray Gregg. All rights reserved. 50

General Ledger

BI - M 12,000 to Dept 2 221,000BI - CC 9,000DM 72,000

DL 103,500MO 62,100

258,600Bal 37,600

Work in Process -- Dept 1

Copyright © 2003 by M. Ray Gregg. All rights reserved. 51

Determine unit costs

Assignment of Costs: Units Per Unit TotalFinished 17,000 $13.00 $221,000Not Finished Materials 4,000 $4.00 $16,000 CC 2,400 $9.00 21,600 37,600

Total costs accounted for $258,600

Step 4: Allocate costs to goods

Copyright © 2003 by M. Ray Gregg. All rights reserved. 52

Determine unit costs

Assignment of Costs: Units Per Unit TotalFinished 17,000 $13.00 $221,000Not Finished Materials 4,000 $4.00 $16,000 CC 2,400 $9.00 21,600 37,600

Total costs accounted for $258,600

Step 4: Allocate costs to goods

BI - M 12,000 to Dept 2 221,000BI - CC 9,000DM 72,000

DL 103,500MO 62,100

258,600Bal 37,600

Work in Process -- Dept 1

ManufacturingProcess Cost Accounting

Copyright © 2003 by M. Ray Gregg. All rights reserved. 54

Copyright © 2003 by M. Ray Gregg. All rights reserved. 55

Sources• Dell computer logo

– http://www.hubspan.com/partners_tech.asp• Home Construction

– http://www.rtsonline.com/builder-info.asp– http://www.continentalweather.com

• Accounting logos– Ernst & Young

http://www.rgu.ac.uk/abs/undergraduate/page.cfm?pge=4857– Deloitte & Touche

http://www.columbia.edu/cu/finance/report99/fin_statements13.html