Download - Concept of Micro credit

7/28/2019 Concept of Micro credit

http://slidepdf.com/reader/full/concept-of-micro-credit 1/16

Page 1 of 16

Abstract

Microcredit – the extension of small loans – gives people who would otherwise not have access

to credit the opportunity to begin or expand businesses or to pursue job-specific training. These

borrowers lack the income, credit history, assets, or security to borrow from other sources.

Although the popularity and success of microcredit in developing countries has been trumpeted

in the media, microcredit is established and growing in the United States and Canada as well. Its

appeal comes from its capacity to provide the means for those who have the ability, drive, and

commitment to overcome the hurdles to self-sufficiency.

In this report, the role of microcredit as a stimulant for economic development is examined

specially in the context of Bangladesh. Firstly, the concept of microcredit, history, an overview

of the general microcredit climate system and classification are described. Second, brief stories

about the Grameen Bank and its Microcredit system known as Grameencredit are focused. Third,

recent development scenario in Asia, Latin America and Africa with the help of micro credit and

examples are provided. Fourth, a summary of the benefits of microcredit as a win-win

proposition for economic development is highlighted. Finally, microcredit in context of

Bangladesh is overviewed with the help of statistical data.

7/28/2019 Concept of Micro credit

http://slidepdf.com/reader/full/concept-of-micro-credit 2/16

Page 2 of 16

Concept of M icrocredit

Microcredit is the extension of very small loans (microloans) to impoverished borrowers who

typically lack collateral, steady employment and a verifiable credit history. It is designed not

only to support entrepreneurship and alleviate poverty, but also in many cases to empower

women and uplift entire communities by extension. In many communities worldwide, indeveloped and developing nations alike, women lack the highly stable employment histories that

traditional lenders tend to require. This reality might result from factors such as leaving the paid

workforce to care for children and elderly relatives. As of 2009 an estimated 74 million men and

women held microloans that totaled US$38 billion.

Grameen Bank reports that repayment success rates are between 95 and 98 per cent. Microcredit

is a division of microfinance, which is the provision of a wider range of financial services,

especially savings accounts, to the poor. Modern microcredit is generally considered to have

originated with the Grameen Bank founded in Bangladesh in 1983. Many traditional banks

subsequently introduced microcredit despite initial misgivings. The United Nations declared2005 the International Year of Microcredit. As of 2012, microcredit is widely used in developing

countries and is presented as having "enormous potential as a tool for poverty alleviation."

Early beginni ngs

Ideas relating to microcredit can be found at various times in modern history. Jonathan

Swift inspired the Irish Loan Funds of the 18th and 19th centuries. In the mid-19th

century,Individualist anarchist Lysander Spooner wrote about the benefits of numerous small

loans for entrepreneurial activities to the poor as a way to alleviate poverty. At about the same

time, but independently to Spooner, Friedrich Wilhelm Raiffeisen founded the first cooperativelending banks to support farmers in rural Germany In the 1950s, Akhtar Hameed Khan began

distributing group-oriented credit in East Pakistan. Khan used the Comilla Model, in which

credit is distributed through community-based initiatives. The project failed due to the over-

involvement of the Pakistani government, and the hierarchies created within communities as

certain members began to exert more control over loans than others.

7/28/2019 Concept of Micro credit

http://slidepdf.com/reader/full/concept-of-micro-credit 3/16

Page 3 of 16

Modern microcredit

Nobel laureate Muhammad Yunus, the founder of Grameen Bank, which is generally considered

the first modern microcredit institution.

The origins of microcredit in its current practical incarnation can be linked to several

organizations founded in Bangladesh, especially the Grameen Bank. The Grameen Bank, which

is generally considered the first modern microcredit institution, was founded in 1983

by Muhammad Yunus. Yunus began the project in a small town called Jobra, using his own

money to deliver small loans at low-interest rates to the rural poor. Grameen Bank was followed

by organizations such as BRAC in 1972 and ASA in 1978. Microcredit reached Latin America

with the establishment of PRODEM in Bolivia in 1986; a bank that later transformed into the

for-profit BancoSol. Microcredit quickly became a popular tool for economic development, with

hundreds of institutions emerging throughout the third world. Though the Grameen Bank was

formed initially as a non-profit organization dependent upon government subsidies, it later

became a corporate entity and was renamed Grameen II in 2002. Muhammad Yunus was

awarded the Nobel Peace Prize in 2006 for his work providing microcredit services to the poor.

In contrast, microloans are usually “character - based” lending, where the personal commitment,

experience, and skills of the applicant are considered along with the quality of the business idea.

Micro lenders often take more time to assist borrowers with business planning and the

application process than commercial lenders, and frequently provide free mentoring after the

loan has been disbursed. Microloans can be at preferential rates. However, micro lenders dorequire a sound business plan to ensure the greatest probability of success and a viable self-

supporting future for the borrower. The only potential downside for microcredit borrowers is the

risk of default, which will set back their creditworthiness even further.

7/28/2019 Concept of Micro credit

http://slidepdf.com/reader/full/concept-of-micro-credit 4/16

Page 4 of 16

Microcredit is truly a win-win proposition for economic development, boosting income and

adding jobs for individuals, diversifying the regional economy while lowering government

support costs and increasing government revenues. The importance of small business to the

health of the economy, especially in difficult times, brings home the potential for microcredit to

assist people in turning challenges into opportunities.

A broad classif ication of microcredit

A) Traditional informal microcredit (such as, moneylender's credit, pawn shops, loans from

friends and relatives, consumer credit in informal market, etc.)

B) Microcredit based on traditional informal groups (such as, tontin, su su, ROSCA, etc.)

C) Activity-based microcredit through conventional or specialized banks (such as, agricultural

credit, livestock credit, fisheries credit, handloom credit, etc.)

D) Rural credit through specialized banks.

E) Cooperative microcredit (cooperative credit, credit union, savings and loan associations,

savings banks, etc.)

F) Consumer microcredit.

G) Bank-NGO partnership based microcredit.

H) Grameen type microcredit or Grameen credit.

I) Other types of NGO microcredit.

J) Other types of non-NGO non-collateralized microcredit.

Whenever I use the word "microcredit" I actually have in mind Grameen type microcredit or

Grameencredit. Not every Grameen type programme has all these features present in the

programme. Some programes are strong in some of the features, while others are strong in some

other features.

7/28/2019 Concept of Micro credit

http://slidepdf.com/reader/full/concept-of-micro-credit 5/16

Page 5 of 16

General features of Grameencredit are

a) It promotes credit as a human right.

b) Its mission is to help the poor families to help themselves to overcome poverty. It is targeted

to the poor, particularly poor women.

c) Most distinctive feature of Grameencredit is that it is not based on any collateral, or legally

enforceable contracts. It is based on "trust", not on legal procedures and system.

d) It is offered for creating self-employment for income-generating activities and housing for the

poor, as opposed to consumption.

e) It was initiated as a challenge to the conventional banking which rejected the poor by

classifying them to be "not creditworthy". As a result it rejected the basic methodology of theconventional banking and created its own methodology.

f) It provides service at the door-step of the poor based on the principle that the people should

not go to the bank, bank should go to the people.

g) In order to obtain loans a borrower must join a group of borrowers.

h) Loans can be received in a continuous sequence. New loan becomes available to a borrower if

her previous loan is repaid.

i) All loans are to be paid back in installments (weekly, or bi-weekly).

j) Simultaneously more than one loan can be received by a borrower.

k)It comes with both obligatory and voluntary savings programmes for the borrowers.

Grameencredit is based on the premise that the poor have skills which remain unutilised or

under-utilised. It is definitely not the lack of skills which make poor people poor. Grameen

believes that the poverty is not created by the poor, it is created by the institutions and policies

which surround them. In order to eliminate poverty all we need to do is to make appropriate

changes in the institutions and policies, and/or create new ones. Grameen believes that charity is

not an answer to poverty. It only helps poverty to continue. It creates dependency and takes away

individual's initiative to break through the wall of poverty. Unleashing of energy and creativity in

each human being is the answer to poverty.

7/28/2019 Concept of Micro credit

http://slidepdf.com/reader/full/concept-of-micro-credit 6/16

Page 6 of 16

Grameen brought credit to the poor, women, the illiterate, and the people who pleaded that they

did not know how to invest money and earn an income. Grameen created a methodology and an

institution around the financial needs of the poor, and created access to credit on reasonable term

enabling the poor to build on their existing skill to earn a better income in each cycle of loans.

Grameen as a Model Communi ty Bank

In 1983 Yunus founded the Grameen Bank, universally cited as the inspiration and model for the

global microcredit movement. His purpose was to improve the lives of millions of poor

Bangladeshis by making small loans to poor women to fund income-generating micro

businesses.

The basis f or the Grameen Bank‟s worldwide renown lies in a number of key characteristics that

are not widely understood.

Most local branches are self-funded by deposits of their local members in taka, the

Bangladesh national currency.

By serving as a depository for its members, Grameen Bank allows the poor to build their

own financial asset base.

The bank extends loans to its members at a maximum interest rate of 20 percent, a

fraction of what many other micro lenders charge.

Operating on a cooperative model, profits are redistributed to the Grameen Bank‟s

owner-members or are invested in community projects.

These features root the Grameen Bank in the community it serves and keep money, including

interest payments, continuously circulating locally to facilitate productive local exchange and

build real community wealth.

Microcredit programs seeking to replicate the Grameen model have spread rapidly across the

globe. Most, however, replicate only the loan feature. Few provide their members with

depository services or replicate the Grameen Bank‟s other defining features, though these

features are central to its commitment to community wealth building.

7/28/2019 Concept of Micro credit

http://slidepdf.com/reader/full/concept-of-micro-credit 7/16

Page 7 of 16

Recent development

Over the past decade, microfinance institutions have adopted innovative ways of providing credit

and savings services to the entrepreneurial poor. Two approaches have been advocated on the

role of credit in poverty reduction. While supporters of the income-generation approach maintainthat credit should be provided mainly to the entrepreneurial poor to enable them to finance

specific private income-generating activities to increase their revenues, proponents of the so-

called new minimalist approach argue that credit progammes would still be helping the poor

fight poverty by giving credit to any poor person who is able to repay a loan without dictating to

that person how and on what the loan should be used. Some studies have pointed out that the

problem of the non-productive use of credit, as advocated by the minimalist approach, lies in the

fact that by consuming rather than investing their loans, the actions of such borrowers, if imitated

by other poor people, could produce a negative impact on the future growth of microcredit.

Several microfinance institutions have succeeded in reaching the poorest of the poor by devisinginnovative strategies. These include the provision of small loans to poor people, especially in

rural areas, at full-cost interest rates, without collateral, that are repayable in frequent

installments. Borrowers are organized into groups, which reduces the risk of default. These are

also effective mechanisms through which to disseminate valuable information on ways to

improve the health, legal rights, sanitation and other relevant concerns of the poor. Above all,

many microcredit programmes have targeted one of the most vulnerable groups in society -

women who live in households that own little or no assets. By providing opportunities for self-

employment, many studies have concluded that these programmes have significantly increased

women's security, autonomy, self-confidence and status within the household.

Asia

Microlending has progressed to the greatest extent in the Asian region. An innovative approach

that has been used successfully by Grameen Bank's credit-delivery system is "peer-group

monitoring" to reduce lending risk, although some studies have suggested that the reason for the

Grameen Bank's high repayment rates is also partly due to the practice of weekly public

meetings - at which attendance is compulsory - for the repayment of loan installments and the

collection of savings. It is reported that the meetings reinforce a culture of discipline, routine

repayments and staff accountability. Not all microfinance institutions use peer-group monitoring.Other institutions such as the Bank Rakyat of Indonesia, which serves 2.5 million clients and 12

million small savers, rely on character references and locally recruited lending agents in place of

physical collateral. Thailand's Bank of Agriculture and Agricultural Cooperatives serves

approximately 1 million micro borrowers and 3.6 million micro-savers. Newcomers such as the

Association for Social Advancement of Bangladesh, with half a million clients, and the People's

Credit Funds of Viet Nam, with more than 200,000 members or clients, are other examples of the

7/28/2019 Concept of Micro credit

http://slidepdf.com/reader/full/concept-of-micro-credit 8/16

Page 8 of 16

potential for growth in the industry. Other institutions such as the Association of Cambodia

Local Economic Development Agencies, Buro-Tangail of Bangladesh, the Self-Employed

Women's Association Bank of India, and Amanah Ikhtiar Malaysia are also reported to be

making good progress.

Latin America

In Latin America, Accion International, a non-profit development agency, and its affiliates was

reported to have disbursed in the past five years $1 billion in loans to poor micro entrepreneurs.

Its first-time loans are between $100 and $200, and the overall repayment rate is above 98 per

cent. Its network of 19 affiliates in Latin America and North America provides $300 million a

year in loans to poor entrepreneurs (56 per cent of whom are women). Since 1987, Accion's

network has grown from 13,000 to more than 285,000 active borrower clients. The six largest

affiliates now provide $1 million per month in loans. Banco Solidario of Bolivia, which hasgrown from a credit-providing non-governmental organization to a fully licensed commercial

bank, provides financial services to 67,000 people, more than one half of the total number of

clients in the entire Bolivian banking system. The Association for the Development of Micro-

Entreprises of the Dominican Republic and Accion Comunitaria del Peru are reported to have

achieved sustainability.

Africa

In West Africa, where microfinance institutions are still in their infancy, a World Bank casestudy of nine microfinance programmes - the Pride, Credit rural and credit mutuel de Guinee;

Credit mutuel du Senegal and Village Banks Nganda of Senegal; Reseau des caisses populaires

and Sahel Action Project de promotion du petit credit rural of Burkina Faso; and Caisses

villageoises du pays dogon and Kafo Jiginew of Mali - concluded that all nine of these

programmes are very much in the mainstream of best practice in the field of microfinance. In

terms of sustainable lending to microentrepreneurs, the study gave high marks to the

programmes on the following basis: all nine programmes are located near their clients and in the

largest catchment areas possible; they use lending technologies that are simple, well-tailored to

the cultural environment and inexpensive for both lender and client; they have employed

effective techniques for obtaining high repayment rates; most include savings, which meet a

critical need of many people, and they price their loans far above commercial lending rates,

though not at full cost recovery.

7/28/2019 Concept of Micro credit

http://slidepdf.com/reader/full/concept-of-micro-credit 9/16

Page 9 of 16

In view of the growing popularity of microfinance institutions, some of which now explore the

possibility of deposit mobilization or leverage commercial capital, it is reported that bank

regulators in such countries as Bolivia, Ghana, Kenya and Peru, and other countries, are creating

laws or special regulations for this new breed of institutions. In Bolivia, it is reported that Banco

Solidario, a private commercial microenterprise bank, is regulated by the Superintendence of

Banks, with the same financial and reporting requirements as traditional banks, but with simpler

loan documentation and risk classification rules. In the case of Bolivia, which seeks to encourage

new micro-financial institutions, it is reported that the Government has begun licensing a new

class of intermediaries, known as private financial funds, subject to the same solvency and

reserve requirements as banks, but with lower minimal capital requirements.

M icrocredit: The Good, the Bad, and the Ugly

For more than twenty years, microcredit has been widely heralded as the remedy for world

poverty. Recent news stories, however, have sullied microcredit‟s glowing reputation with

reports on scandals, exorbitant compensation to managers, skyrocketing interest rates, and

aggressive marketing schemes.

Once praised as a universal panacea, micro lenders are now being widely attacked as predatory

loan sharks. In December 2010, Sheik Hasina Wazed, the prime minister of Bangladesh and

former microcredit advocate, accused microcredit programs of “sucking blood from the poor in

the name of poverty alleviation for more than twenty years, microcredit has been widely

heralded as the remedy for world poverty. Recent news stories, however, have sulliedmicrocredit‟s glowing reputation with reports on scandals, exorbitant compensation to managers,

skyrocketing interest rates, and aggressive marketing schemes.

It turns out there are two very different models of microcredit. As Muhammad Yunus, winner of

the 2006 Nobel Prize, pointed out in his January 15, 2011 New York Times op-ed, one type of

microcredit program is designed to serve the poor; another to maximize financial returns to

program managers and Wall Street investors.

Microfinance is one way of fighting poverty in rural areas, where most of the world‟s poorest

people live. It puts credit, savings, insurance and other basic financial services within the reachof poor people. Through microfinance institutions such as credit unions, financial non-

governmental organizations and even commercial banks, poor people can obtain small loans,

receive money from relatives working abroad and safeguard their savings.

7/28/2019 Concept of Micro credit

http://slidepdf.com/reader/full/concept-of-micro-credit 10/16

Page 10 of 16

It has also changed the perception that poor people are not credit worthy. Records have shown

that, instead, they are a good risk, with higher repayment rates than conventional borrowers. In

some of the most successful microfinance institutions, repayment rates are as high as 98 per cent.

As microfinance has evolved, there has been an increasing recognition of the importance of

savings, often referred to as the “the forgotten half of microfinance”. While credit is important, it

is only one of the many different kinds of financial services that poor people need to improve

their lives.

For example, the Unit Desai of Bank Rakyat Indonesia, which has been one of the most

successful providers of microfinance services in the region, counts more than 28 million savers,

for only three million borrowers. The large financial cooperative networks in West Africa also

have many more savers than borrowers among their members.

The Microcredit Summit Campaign has the ambitious objective of reaching 100 million of the

world‟s poorest families by the year 2005. By the end of 2001, mor e than 2000 microfinance

institutions were involved in the campaign, providing financial services, mostly loans, to almost

55 million individuals or groups. More than 21 million of those clients were women. Although

the amounts involved may be small, the loans, savings and insurance options that microfinance

offers can give millions of rural men and women an opportunity to find their own solutions.

Following benefits of micro credit in economy is visible:

Reduction of Vulnerability

Microcredit programs aid against crises by building household assets for those in need. These

assets can bring in extra profit if they need to because they can be sold. Also, they can be used to

verify credit worthiness when dealing with lending agencies or businessmen. These additional

assets provide more security for families because they are diversified; diversified assets cut the

risks of loss. Furthermore, other aspects such as skills training and female empowerment also

help families cope with crises. Microcredit teaches people to hold their own place in society, thus

allowing the cycle of poverty to stop.

Increased Consumption

Microcredit programs cause an increase in household consumption. A researcher from

Bangladesh found that for over 100 taka (unit of currency in Bangladesh) lent to a female

borrower, their household consumption was raised by 18 taka. Even small increases inconsumption can lead to better health and well being for the entire family. Providing a greater

stability for families has huge long term positive effects for ending poverty cycles within

families.

7/28/2019 Concept of Micro credit

http://slidepdf.com/reader/full/concept-of-micro-credit 11/16

Page 11 of 16

Reduced Income Poverty

Borrowers of Microcredit tend to make more money over time. Once the cycle of poverty stops,

and there is stability in the household, many borrowers go on to make profitable investments and

may be able to lift their entire family out of poverty altogether. On average, 15% of participants

in Bangladesh rise up from poverty after three years of participation. The poorest of the poor will

see a 25% reduction in poverty after the first year. Any rate of reduction of poverty certainly

warrants optimism.

Boosting Self-Esteem

Simply put, participants experience a sense of pride when they create or expand a business

successfully. Many learn new trades or management skills causing them to have a sense of

ownership in what they have accomplished and they feel worthy of a place in society. This boost

in self-esteem causes many women to want to continue being successful, causing a halt in the

cycles of poverty that once surrounded their lives.

Immigrants in action

Microcredit plays an especially important role in enabling immigrants to establish small

businesses, since they face significant obstacles to accessing loans from mainstream financial

institutions, such as language barriers, unfamiliarity with financial norms, and lack of credit

history. Many immigrants turn to self-employment as a means of circumventing the difficulties

they have in finding jobs commensurate with their skills and experience. The potential for

immigrants to be a powerhouse of entrepreneurial activity and job creation is indicated by a

study of immigrant entrepreneurs in New York City in 2000, which found that 36% of New

York‟s population was born outside the US, while foreign-born individuals made up 49% of all

self-employed workers in the city.

7/28/2019 Concept of Micro credit

http://slidepdf.com/reader/full/concept-of-micro-credit 12/16

Page 12 of 16

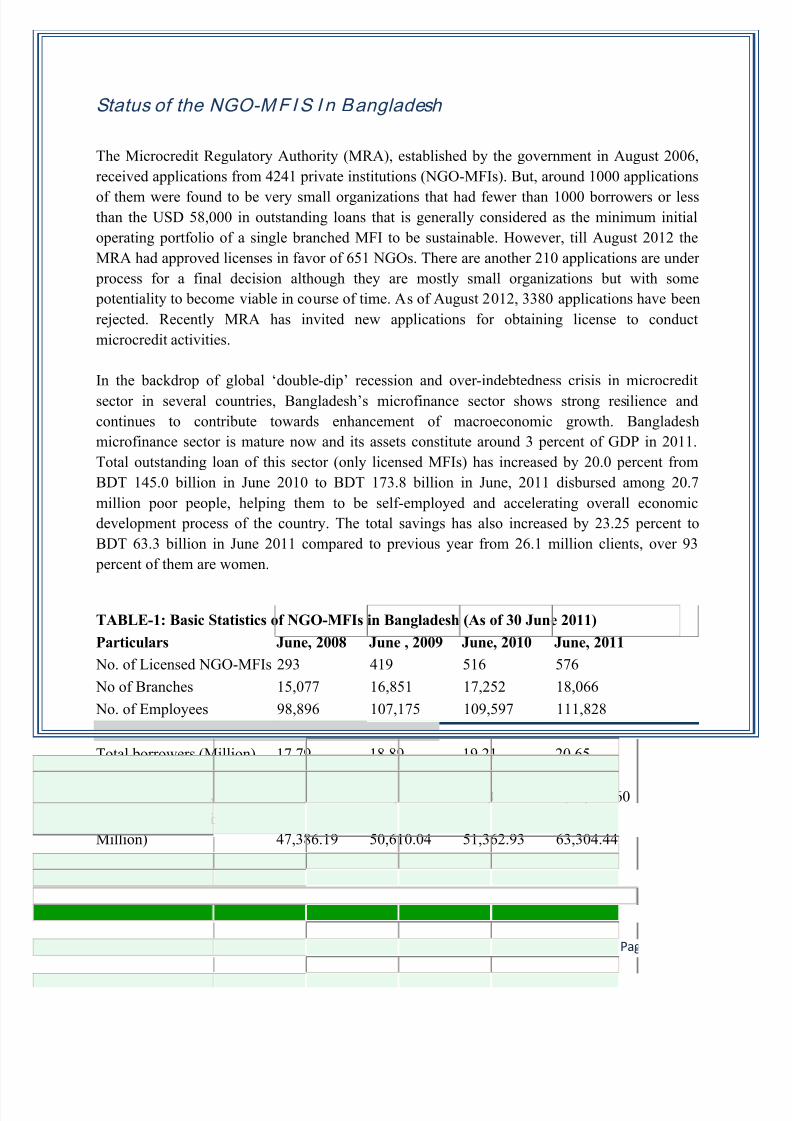

Status of the NGO-MFIS I n Bangladesh

The Microcredit Regulatory Authority (MRA), established by the government in August 2006,

received applications from 4241 private institutions (NGO-MFIs). But, around 1000 applications

of them were found to be very small organizations that had fewer than 1000 borrowers or lessthan the USD 58,000 in outstanding loans that is generally considered as the minimum initial

operating portfolio of a single branched MFI to be sustainable. However, till August 2012 the

MRA had approved licenses in favor of 651 NGOs. There are another 210 applications are under

process for a final decision although they are mostly small organizations but with some

potentiality to become viable in course of time. As of August 2012, 3380 applications have been

rejected. Recently MRA has invited new applications for obtaining license to conduct

microcredit activities.

In the backdrop of global „double-dip‟ recession and over -indebtedness crisis in microcredit

sector in several countries, Bangladesh‟s microfinance sector shows strong resilience and

continues to contribute towards enhancement of macroeconomic growth. Bangladesh

microfinance sector is mature now and its assets constitute around 3 percent of GDP in 2011.

Total outstanding loan of this sector (only licensed MFIs) has increased by 20.0 percent from

BDT 145.0 billion in June 2010 to BDT 173.8 billion in June, 2011 disbursed among 20.7

million poor people, helping them to be self-employed and accelerating overall economic

development process of the country. The total savings has also increased by 23.25 percent to

BDT 63.3 billion in June 2011 compared to previous year from 26.1 million clients, over 93

percent of them are women.

TABLE-1: Basic Statistics of NGO-MFIs in Bangladesh (As of 30 June 2011)

Particulars June, 2008 June , 2009 June, 2010 June, 2011

No. of Licensed NGO-MFIs 293 419 516 576

No of Branches 15,077 16,851 17,252 18,066

No. of Employees 98,896 107,175 109,597 111,828

No. of Clients (Million) 23.45 24.85 25.28 26.08

Total borrowers (Million) 17.79 18.89 19.21 20.65

Amount of Loan

Outstanding (Tk. Million ) 134,680.96 143,134.03 145,022.66 1,73,797.60

Amount of Savings( Tk.

Million) 47,386.19 50,610.04 51,362.93 63,304.44

Source: MRA-MIS Database-2011

7/28/2019 Concept of Micro credit

http://slidepdf.com/reader/full/concept-of-micro-credit 13/16

Page 13 of 16

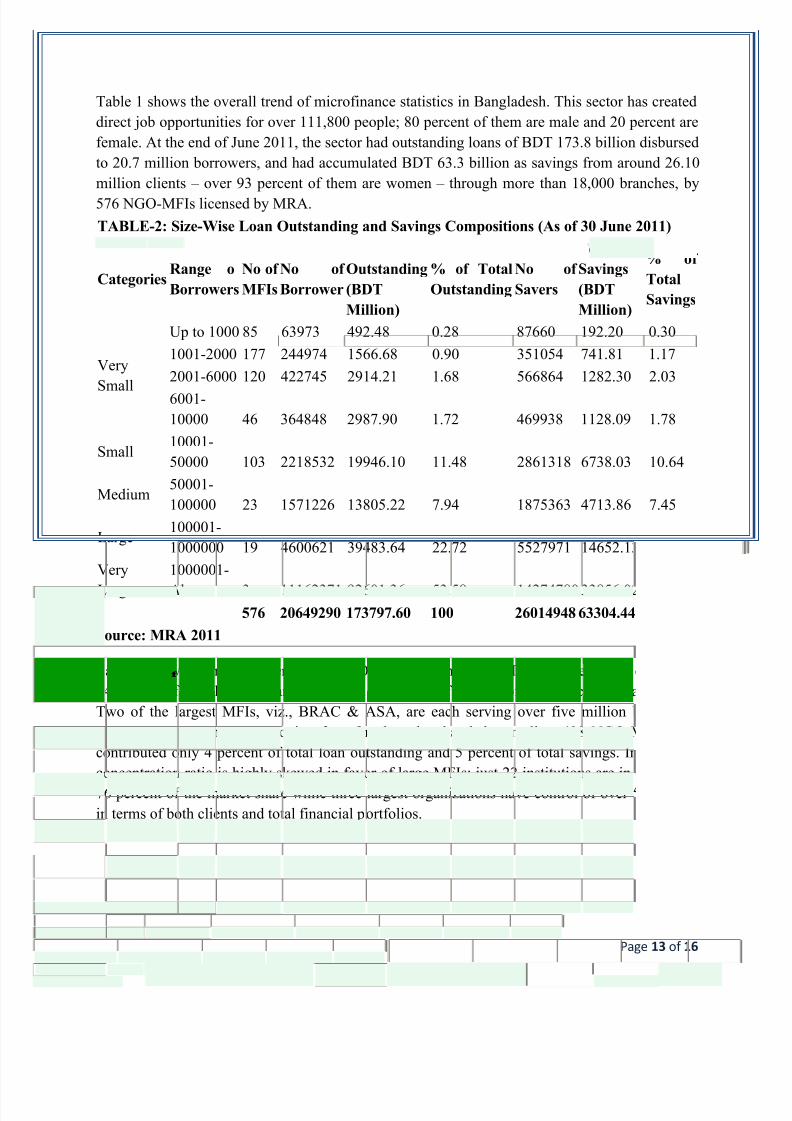

Table 1 shows the overall trend of microfinance statistics in Bangladesh. This sector has created

direct job opportunities for over 111,800 people; 80 percent of them are male and 20 percent are

female. At the end of June 2011, the sector had outstanding loans of BDT 173.8 billion disbursed

to 20.7 million borrowers, and had accumulated BDT 63.3 billion as savings from around 26.10

million clients – over 93 percent of them are women – through more than 18,000 branches, by

576 NGO-MFIs licensed by MRA.

TABLE-2: Size-Wise Loan Outstanding and Savings Compositions (As of 30 June 2011)

Categories Range o

Borrowers

No of

MFIs

No of

Borrower

Total Loan

Outstanding

(BDT

Million)

% of Total

Outstanding

No of

Savers

Total

Savings

(BDT

Million)

% of

Total

Savings

Very

Small

Up to 1000 85 63973 492.48 0.28 87660 192.20 0.30

1001-2000 177 244974 1566.68 0.90 351054 741.81 1.17

2001-6000 120 422745 2914.21 1.68 566864 1282.30 2.03

6001-

10000 46 364848 2987.90 1.72 469938 1128.09 1.78

Small10001-

50000 103 2218532 19946.10 11.48 2861318 6738.03 10.64

Medium50001-

100000 23 1571226 13805.22 7.94 1875363 4713.86 7.45

Large100001-

1000000 19 4600621 39483.64 22.72 5527971 14652.13 23.15

Very

Large

1000001-

Above 3 11162371 92601.36 53.58 14274780 33856.028 53.51576 20649290 173797.60 100 26014948 63304.44 100

Source: MRA 2011

Table 2 shows the market scenario of NGO-MFIs in Bangladesh. The top three MFIs contribute

54 percent of total loan outstanding as well as savings of the microfinance sector in Bangladesh.

Two of the largest MFIs, viz., BRAC & ASA, are each serving over five million borrowers.

There are a few more developing fast. On the other hand the smallest 428 NGO-MFIs have

contributed only 4 percent of total loan outstanding and 5 percent of total savings. Institutional

concentration ratio is highly skewed in favor of large MFIs: just 22 institutions are in control of

76 percent of the market share while three largest organizations have control of over 50 percent

in terms of both clients and total financial portfolios.

7/28/2019 Concept of Micro credit

http://slidepdf.com/reader/full/concept-of-micro-credit 14/16

Page 14 of 16

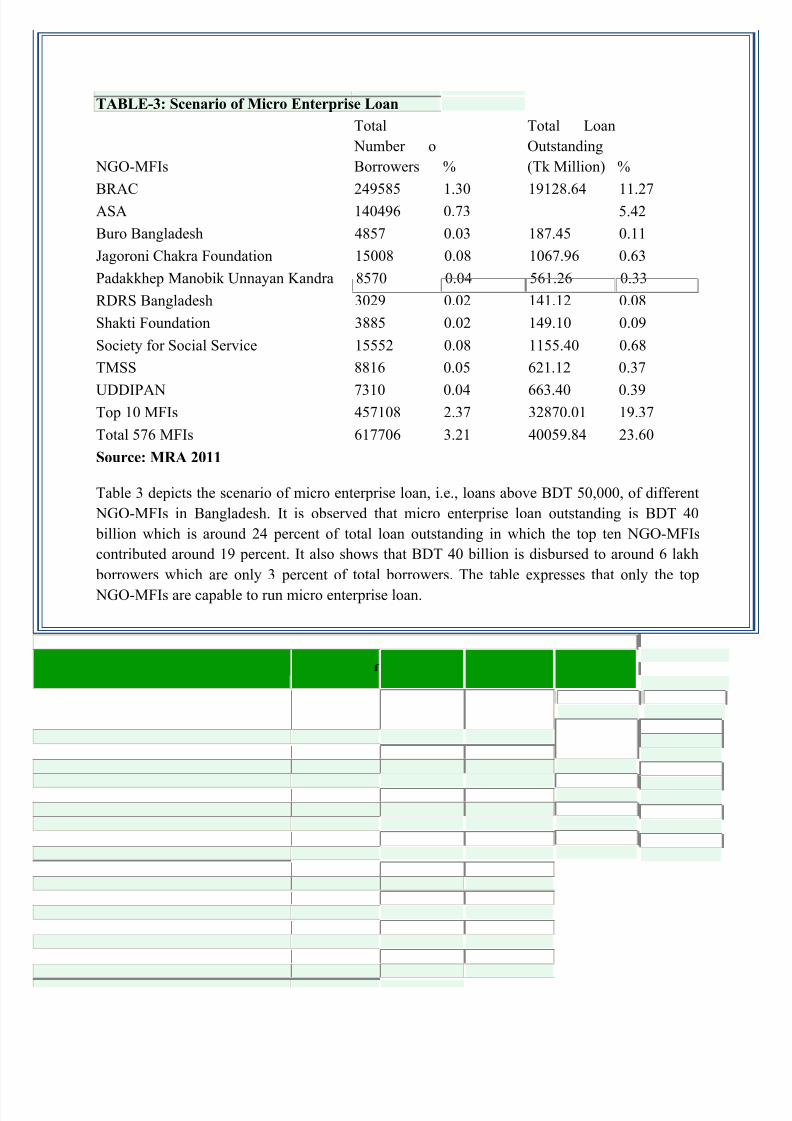

TABLE-3: Scenario of Micro Enterprise Loan

NGO-MFIs

Total

Number o

Borrowers %

Total Loan

Outstanding

(Tk Million) %

BRAC 249585 1.30 19128.64 11.27ASA 140496 0.73 9194.57 5.42

Buro Bangladesh 4857 0.03 187.45 0.11

Jagoroni Chakra Foundation 15008 0.08 1067.96 0.63

Padakkhep Manobik Unnayan Kandra 8570 0.04 561.26 0.33

RDRS Bangladesh 3029 0.02 141.12 0.08

Shakti Foundation 3885 0.02 149.10 0.09

Society for Social Service 15552 0.08 1155.40 0.68

TMSS 8816 0.05 621.12 0.37

UDDIPAN 7310 0.04 663.40 0.39Top 10 MFIs 457108 2.37 32870.01 19.37

Total 576 MFIs 617706 3.21 40059.84 23.60

Source: MRA 2011

Table 3 depicts the scenario of micro enterprise loan, i.e., loans above BDT 50,000, of different

NGO-MFIs in Bangladesh. It is observed that micro enterprise loan outstanding is BDT 40

billion which is around 24 percent of total loan outstanding in which the top ten NGO-MFIs

contributed around 19 percent. It also shows that BDT 40 billion is disbursed to around 6 lakh

borrowers which are only 3 percent of total borrowers. The table expresses that only the top

NGO-MFIs are capable to run micro enterprise loan.

7/28/2019 Concept of Micro credit

http://slidepdf.com/reader/full/concept-of-micro-credit 15/16

Page 15 of 16

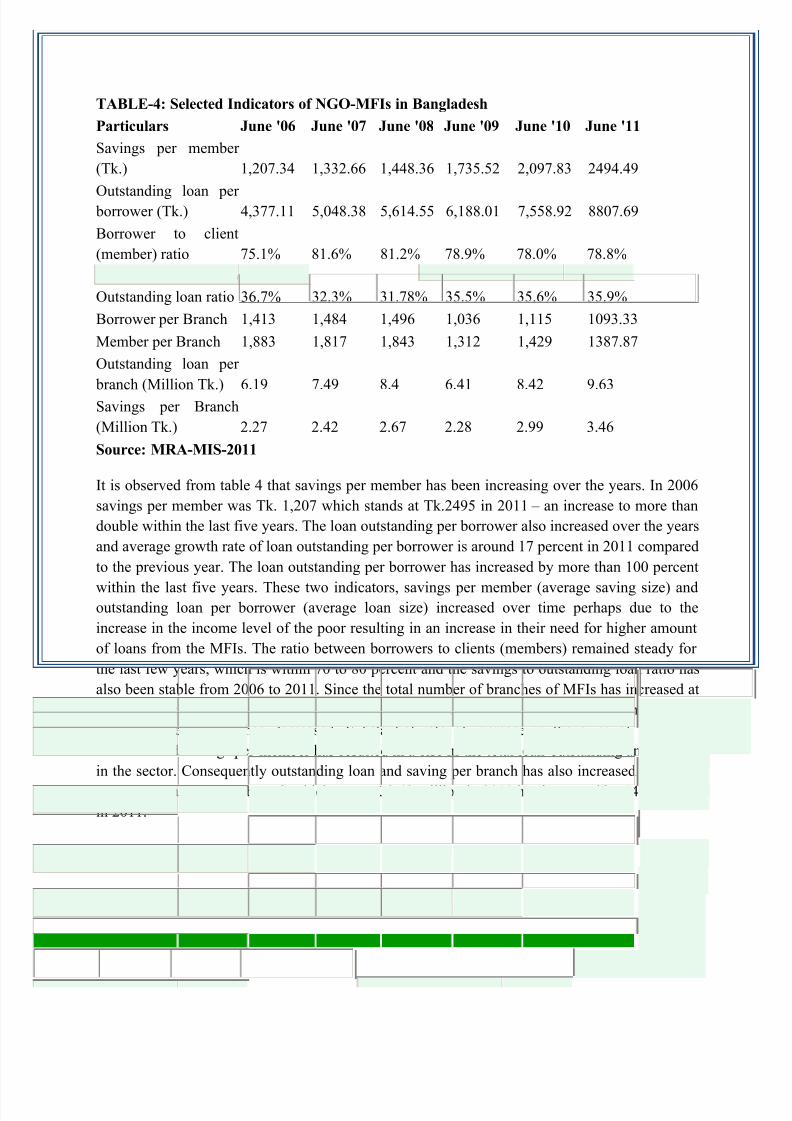

TABLE-4: Selected Indicators of NGO-MFIs in Bangladesh

Particulars June '06 June '07 June '08 June '09 June '10 June '11

Savings per member

(Tk.) 1,207.34 1,332.66 1,448.36 1,735.52 2,097.83 2494.49

Outstanding loan per borrower (Tk.) 4,377.11 5,048.38 5,614.55 6,188.01 7,558.92 8807.69

Borrower to client

(member) ratio 75.1% 81.6% 81.2% 78.9% 78.0% 78.8%

Savings to

Outstanding loan ratio 36.7% 32.3% 31.78% 35.5% 35.6% 35.9%

Borrower per Branch 1,413 1,484 1,496 1,036 1,115 1093.33

Member per Branch 1,883 1,817 1,843 1,312 1,429 1387.87

Outstanding loan per

branch (Million Tk.) 6.19 7.49 8.4 6.41 8.42 9.63

Savings per Branch

(Million Tk.) 2.27 2.42 2.67 2.28 2.99 3.46

Source: MRA-MIS-2011

It is observed from table 4 that savings per member has been increasing over the years. In 2006

savings per member was Tk. 1,207 which stands at Tk.2495 in 2011 – an increase to more than

double within the last five years. The loan outstanding per borrower also increased over the years

and average growth rate of loan outstanding per borrower is around 17 percent in 2011 compared

to the previous year. The loan outstanding per borrower has increased by more than 100 percent

within the last five years. These two indicators, savings per member (average saving size) andoutstanding loan per borrower (average loan size) increased over time perhaps due to the

increase in the income level of the poor resulting in an increase in their need for higher amount

of loans from the MFIs. The ratio between borrowers to clients (members) remained steady for

the last few years, which is within 70 to 80 percent and the savings to outstanding loan ratio has

also been stable from 2006 to 2011. Since the total number of branches of MFIs has increased at

a much higher rate in 2011 compared to the previous year, the number of members and

borrowers per branch has decreased. Substantial rate of increase in the sizes of loans per

borrower and savings per member has resulted in a rise in the total loan outstanding and savings

in the sector. Consequently outstanding loan and saving per branch has also increased. The loan

outstanding amount per branch which was TK 8.42 million in 2010 has increased by 14.4 percent

in 2011.

7/28/2019 Concept of Micro credit

http://slidepdf.com/reader/full/concept-of-micro-credit 16/16

Page 16 of 16

Conclusion

Microcredit is a very effective way for the global economic development. This tool was formed

from very ancient period of human civilization but with the light of Grameen Bank the system

has experienced a whole new way. In this report briefly the microcredit system, benefits and

costs, recent development etc are described. As we live in Bangladesh and we are the proud

introducer of microcredit system, in context of Bangladesh the microcredit related development

is overviewed with the help of reliable statistical data.