Ord Minnett Research 7 March 2014 Page 1

Ord Minnett Research

Company Review

Strike Energy Limited (STX) A different take on Cooper unconventional gas

Valuation and Recommendation

We initiate coverage of Strike Energy with a Buy recommendation and a risk

adjusted DCF target price of $0.25/share, providing a return of 85/%. Strike Energy

is an oil & gas company with conventional and unconventional interests in Australia

and the USA. The primary value driver is appraisal and development of large scale

coal seam gas (CSG) resources from Australia’s Cooper Basin. The potential for

Southern Cooper CSG to supply near term domestic customers is underscored by

agreements with Orica (ORI.AX, Hold), Orora (ORA.AX, Accumulate) and Austral

Bricks, totalling ~190 PJ over 20 years, with Orica advancing $52m to accelerate

resource definition and production. Near term price catalysts include Eagle Ford

divestment and Cooper CSG pilot well testing.

Key investment points

Well located acreage. Strike has over four million net acres in the Cooper

Basin with an estimated 14.3 tcf of recoverable gas and 54 mmbbl of liquids,

over 10,400 net acres in the Eagle Ford shale and 1,875 net acres in the

Permian Basin, all areas which are receiving significant industry attention.

Initial Cooper Basin results look promising.

Southern Cooper CSG: Strike has high equity interest in and operatorship

of its key Cooper Basin tenement, PEL 96. Southern Cooper CSG is located

at depths of 1,500-2,000 m, deeper than typical Queensland CSG projects

(300-800 m), but shallower than Cooper shale at 2,000-4,000 m. As a result

Strike believes Cooper CSG can be appraised for one quarter of the cost of

shale and deliver higher rates of return on field development.

Domgas focus: Initial development of Strike’s Cooper CSG is aimed at

domgas supply but the resource could feed export projects at a later date.

Strike’s foundation agreement with Orica provides $52m of funding to supply

150 PJ over 20 years from 2017, while agreements with Orora and Austral

Bricks total 42.5 PJ over 10 years, equivalent to 12 PJ/yr for the three firms.

Eagle Ford and Permian Basin shale divestment. Strike’s involvement in

US shale plays has proceeded more slowly than planned, with well problems

delaying derisking and divestment. We expect that divestment of the Eagle

Ford project in 2014 and Permian Basin in 2015 will redeploy capital to the

Southern Cooper in time for initial field development.

Risks: Strike has small conventional reserves, with declining production. It

will require further industry or equity funding to develop its Cooper program.

Key Financials

Year-end June (A$) FY13A FY14E FY15E FY16E FY17E

USD/AUD (average) 1.03 0.90 0.88 0.83 0.80

Brent (US$/bbl) 109 109 102 97 97

Production (mmboe) 0.1 0.1 0.1 0.1 0.1

Revenue ($m) 5 5 6 5 2

EBITDA ($m) 3 -2 -2 -2 -4

Cash costs ($/boe) 56 64 65 75 118

Normalized NPAT ($m) -10 -4 -5 -8 -7

Reported NPAT ($m) -14 -4 2 -10 -7

ROE (%) -22 -7 -6 -5 -5

Cash ($m) 1 9 8 65 53

Debt ($m) 3 5 3 3 23

Capex ($m) 17 7 26 23 29

PER -8.1 -30.0 -28.7 -17.6 -18.2

EV/EBITDA 53.5 -57.7 -70.0 -31.1 -26.5

Source: Iress, Company, Ord Minnett estimates

Last price $0.135

Target price $0.25

Recommendation Buy

Risk Assessment Higher

Oil and Gas

John Young

Senior Oil & Gas Analyst

+61 3 9608 4184

Strike Energy Limited

ASX Code STX

52 week range $0.07 - $0.14

Market Cap (A$m) 95

Shares Outstanding (m) 707

Av Daily Turnover (#) 831,398

ASX All Ordinaries 5,469.8

Net Debt/(Cash) FY13A (A$m) 2

Relative price performance

Source: Iress

Consensus earnings

Cons. OML

Target price $/sh 0.20 0.27

FY14 earnings $m n/a -4

FY15 earnings $m n/a -5

Source: Bloomberg

40

50

60

70

80

90

100

110

120

130

Feb-13 May-13 Aug-13 Nov-13 Feb-14

STX

ASX Small Resources

7 March 2014

Ord Minnett Research 7 March 2014 Page 2

Company Review

Strike Energy Limited

Contents

Executive summary ..................................................................................................................... 3

Valuation and target price ........................................................................................................................................ 3

Simulation and sensitivity analysis ........................................................................................................................... 5

SWOT analysis ......................................................................................................................................................... 6

Risks ......................................................................................................................................................................... 6

Company description ................................................................................................................... 7

Southern Cooper Basin Gas Project ........................................................................................................................ 8

Cooper Basin conventional .................................................................................................................................... 10

USA unconventional: Eagle Ford Shale ................................................................................................................. 10

USA unconventional: Permian Basin ..................................................................................................................... 10

USA conventional ................................................................................................................................................... 11

Carnarvon Basin ..................................................................................................................................................... 11

Kingston Lignite Project .......................................................................................................................................... 11

Key activities ........................................................................................................................................................... 14

Reserves and resources ........................................................................................................................................ 15

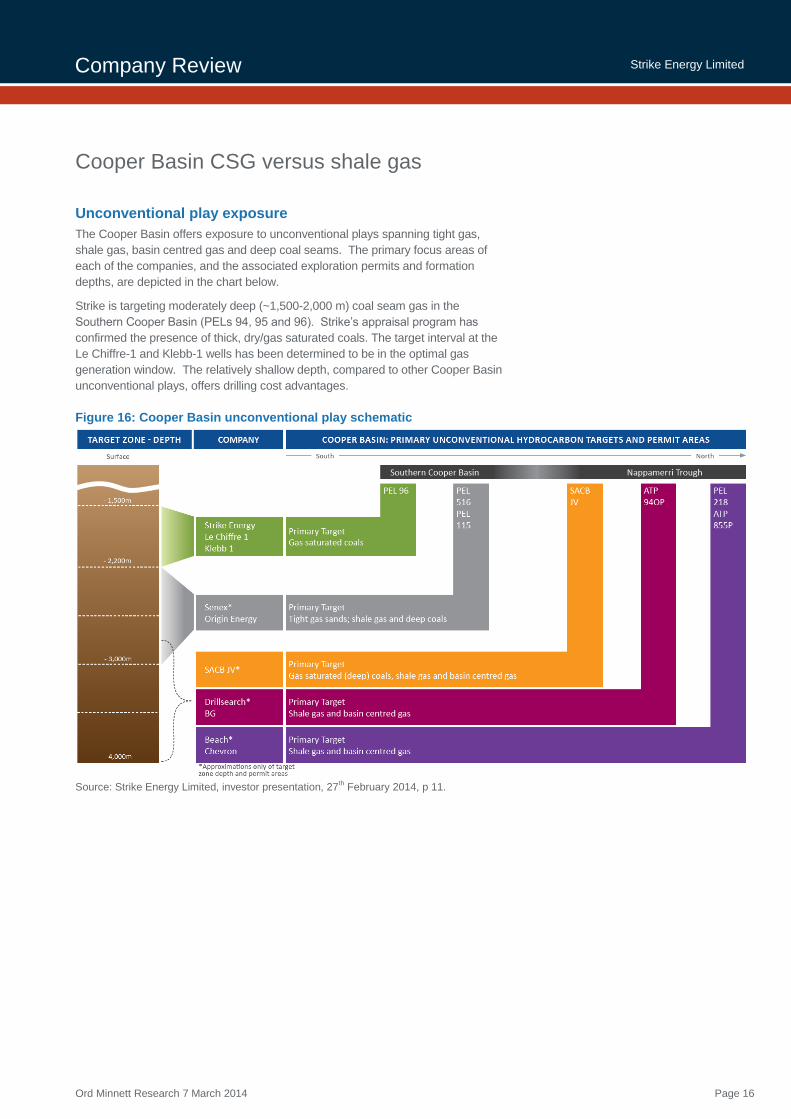

Cooper Basin CSG versus shale gas ........................................................................................ 16

Unconventional play exposure ............................................................................................................................... 16

Technical comparison ............................................................................................................................................ 17

Southern Cooper project development concept ..................................................................................................... 19

Valuation model ......................................................................................................................... 20

Methodology ........................................................................................................................................................... 20

Project assumptions ............................................................................................................................................... 22

Funding requirements ............................................................................................................................................ 23

Valuation model ...................................................................................................................................................... 24

Corporate overview .................................................................................................................... 28

Board ...................................................................................................................................................................... 28

Management ........................................................................................................................................................... 29

Capital structure ..................................................................................................................................................... 30

Appendices ................................................................................................................................ 31

Appendix 1: Tenement summary ........................................................................................................................... 31

Appendix 2: Commodity price assumptions ........................................................................................................... 32

Appendix 3: South Australian coal seam gas potential .......................................................................................... 33

Appendix 4: Eagle Ford shale valuation ................................................................................................................. 35

Ord Minnett Research 7 March 2014 Page 3

Company Review

Strike Energy Limited

Executive summary

Valuation and target price

Investment thesis: Strike offers exposure to appraisal and development of large

scale coal seam gas (CSG) resources from Australia’s Cooper Basin. These

resources, which can be appraised more cheaply than comparable shale programs,

are well located with respect to eastern Australia’s gas market and can be

developed in a time frame suitable for large domestic customers. This potential is

underscored by Orica’s $52m advance to accelerate resource definition and

production and agreements with Orora and Austral Bricks, with demand from the

three firms totalling 12 PJ/yr (equivalent to ~30 mmscfd or ~2 mmboe/yr). Santos,

Beach, Drillsearch, Senex and Origin Energy are also evaluating Cooper Basin

deep coal. Strike has a high equity interest (67%) in and operatorship of its key

Cooper Basin tenement, PEL 96, enabling it to drive the pace and scale of activity.

Valuation and target price: We estimate a base case valuation of $0.21/share as

of 31st December 2013 (at 12% discount rate). Our target price of $0.25 is based

on a 12-month roll-forward of our DCF valuation, with risk factor on Strike’s main

project increasing from 40% to 50% following expected pilot testing progress. This

initiation report should be read in conjunction with our Cooper Basin sector report of

11th September 2013.

Base case: Our base case assumes development of current 2P reserves, together

with a risked value for unconventional prospective resources. Our valuation

assumes a long run Brent oil price of $US90/bbl real, USD/AUD exchange rate of

0.80 and 12% nominal discount rate.

Price catalysts: Near term catalysts include divestment of Strike’s Eagle Ford

shale interest and testing results from the Southern Cooper CSG pilot wells.

Funding: Our modelling indicates Strike will need additional equity funding during

late 2014 to continue to progress appraisal of its Southern Cooper CSG project.

Asset monetization / exit strategy: We expect Strike will divest its US assets and

non-core Australian assets to focus on the potential of its three primary Cooper

Basin tenements (PELs 94, 95 and 96). We expect Strike will retain its current

66.7% interest in the key PEL 96 permit to maintain control of the joint venture and

drive the pace and scale of the Southern Cooper appraisal program. Whilst Strike

may be able to retain its current shareholding in the initial phase of project

development, partial divestment will be required for later, larger scale production.

Table 1: Base case valuation and target price

Source: Ord Minnett analysis. Diluted shares includes assumed future capital raisings.

NPV @ 12.0% WACC $A(m) $A/share %

Production 6 0.01 2.6

Development 22 0.02 10.2

Appraisal 54 0.05 25.3

Exploration 106 0.11 49.2

Corporate costs -37 -0.04 -17.2

Hedging & Investments 0 0.00 0.0

Enterprise Value 150 0.15 70.0

Cash 4 0.00 1.7

Additional Equity 28 0.03 13.0

Debt -7 -0.01 -3.2

Minorities / Other 40 0.04 18.5

Total Equity Valuation - Fully Diluted 215 0.21 100.0

Target price (as of Dec 2014) 251 0.25 116.8

DCF Valuation date: 31-Dec-13. Number of shares (diluted): 1003m

Our valuation includes $35m of additional capital (NPV of $28m), with $15m raised in late 2014 at $0.118/share (based on a 10% discount to the Theoretical ex-rights price, assuming the current share price) and $20m raised in late 2015, also at $0.118/share.

Ord Minnett Research 7 March 2014 Page 4

Company Review

Strike Energy Limited

Table 2: Valuation summary

NPV @ 12.0% WACC Net Unit Risk Risked Risked Unrisked Risked

volume value factor value value value value

Valuation as of 31 Dec 2013 mmboe $US/boe % $A(m) $A/sh $A/sh $A/sh

Projects (DCF model valuation) 147.1 75 0.08 0.14

Louise gas field 0.5 9.20 100 6 0.01 0.01

Eagle Ford Shale 0.0 - 50 20 0.02 0.02

Clearfork conv. 0.0 - 90 2 0.00 0.00

Clearfork shale 0.1 12.60 50 2 0.00 0.00

Southern Cooper CSG Ph1 146.5 0.65 40 46 0.05 0.11

Exploration / Appraisal 3,442.8 112 0.11 1.11

Kingston Lignite 2,144.0 - 10 6 0.01 0.06

Carnarvon permits - - - - - -

S'thn Cooper CSG Ph 2 (PEL96) 310.1 0.65 10 25 0.03 0.25

S'thn Cooper CSG Ph 2 (PEL94/95) 586.5 0.65 10 47 0.05 0.47

Cooper shale gas 402.2 0.65 10 33 0.03 0.33

Cooper (PEL 71/515/575) - - - - - -

Cooper (PPL 210) - - - - - -

Geothermal (GEL 526/527) - - - - - -

Other (corporate, cash, debt, etc) 27 0.03 0.03

Corporate costs 100.0 -37 -0.04 -0.04

Hedging & Investments 100.0 - - -

Franking credits (@ 0 %) 0.0 0 0.00 0.01

Cash 100.0 4 0.00 0.00

Additional Equity 100.0 28 0.03 0.03

Debt 100.0 -7 -0.01 -0.01

Minorities / Other 100.0 40 0.04 0.04

Equity Valuation (diluted) as of Dec 2013 215 0.21 1.30

Equity Valuation @ spot prices @ $US102/bbl real WTI & 0.908 fx 231 0.23

Target price as of Dec 2014 251 0.25

Mkt Cap @ current share price (and undiluted share count) 95 0.135

Total shareholder return (%) 85.2

Number of shares (undiluted) 000,000 706.5

Number of shares (diluted) 000,000 1,003.2

Source: Ord Minnett analysis

Oil price and forex sensitivity: $A/sh Real WTI oil price, $US/bbl Valuation analysis:

$US/$A forex 50 75 100 125 150 175

fx=1.20 0.06 0.17 0.23 0.26 0.29 0.32 Prod'n

fx=1.10 0.06 0.17 0.23 0.26 0.28 0.31 Devel't

fx=1.00 0.06 0.17 0.23 0.25 0.28 0.31 Appr'l

fx=0.90 0.05 0.17 0.23 0.25 0.28 0.30 Expl'n

fx=0.80 0.05 0.17 0.23 0.25 0.27 0.30 Other

fx=0.70 0.04 0.18 0.23 0.25 0.27 0.29

Source: Ord Minnett analysis

Source: Ord Minnett analysis

Ord Minnett Research 7 March 2014 Page 5

Company Review

Strike Energy Limited

Simulation and sensitivity analysis

Monte Carlo simulation calculates the distribution of possible share price outcomes

given the uncertainty in the underlying assumptions. Our simulation analysis

estimates a mean share price of $0.20/share, effectively equal to our base case

valuation of $0.21/share. The distribution is bimodal, reflecting the upside from

shale and Phase 2 of the Southern Cooper CSG resources, which are treated as

discrete variables (i.e. all or nothing). There is an 80% probability the share price

will be above ~$0.06/share and a 20% probability of exceeding ~$0.38/share.

The Tornado chart shows the sensitivity of the valuation to changes in individual

variables, ranking the variables from highest to lowest impact. Our analysis

indicates that the value attributed to Strike’s Cooper shale gas and Southern

Cooper CSG resources have the greatest impact. The oil price impacts value, both

directly through the US unconventional projects and indirectly through the

Australian gas price (reflecting LNG netback pricing).

Figure 1: Monte Carlo simulation

Source: Ord Minnett analysis.

Figure 2: Tornado chart

Source: Ord Minnett analysis.

The bars correspond to the low case (red bar) and high case (blue bar) for each variable.

Due to oil industry convention probabilities are reported as being above a given level. Hence the low case corresponds to a 90% probability of the value being above the low case level and the high case corresponds to a 10% probability of being above the high case level.

The values shown at the end of each bar are the values of the input variables at the low and high cases.

The Monte Carlo simulation method selects values for each of the input assumptions from their probability distributions, calculates the resulting share price, and repeats the process many (in this case 1,000) times.

Ord Minnett Research 7 March 2014 Page 6

Company Review

Strike Energy Limited

SWOT analysis

Strengths

Material acreage positions in good locations (Cooper Basin, South Australia

and Eagle Ford, Texas)

Diversified asset portfolio (regulatory jurisdictions, play types, commodities)

High equity interest in and operatorship of Cooper projects

Near term news flow (Eagle Ford divestment, Cooper drilling)

Low cost appraisal for Southern Cooper CSG (vs. shale)

Weaknesses

Existing production is modest and is declining

Requires funding to progress Cooper CSG program

Lack of control over pace of US projects

Eagle Ford drilling problems potentially impacts divestment value

Opportunities

Divest non-core projects (Carnarvon Basin, Kingston Lignite)

Appraise / divest US unconventional acreage (Eagle Ford, Permian Basin)

Appraise / farm-out Cooper unconventional assets (CSG, shale)

Gas sales option agreements to supply early funding / lock in demand

Supply Australian domgas (and export) markets

Threats

Community opposition to shale exploration and development (particularly

hydraulic fracturing) (although this is unlikely to be a major issue for the

Cooper Basin).

Competition for limited domgas and export markets by other players

Risks

Risks include, but are not limited to, the following factors.

Asset quality (Cooper CSG and shale, Eagle Ford shale)

Cooper gas commercialization

Development costs

Commodity prices

Community opposition / regulatory burden

Investor sentiment towards junior oil & gas companies

Ord Minnett Research 7 March 2014 Page 7

Company Review

Strike Energy Limited

Company description

Strike’s portfolio consists of six projects:

Southern Cooper Basin unconventional gas (South Australia)

Eagle Ford Shale (Texas)

Permian Basin Lower Clearfork Shale (Texas)

USA conventional (Texas and Louisiana)

Carnarvon Basin (offshore Western Australia)

Kingston Lignite (South Australia)

In our view the primary value driver is the Southern Cooper Basin Gas Project.

Existing production, sourced predominantly from the USA conventional assets, is

modest at ~230 boepd.

Table 3: Existing production

Project Production (boepd) % oil

Eaglewood 185 11 Clearfork 34 88 Eagle Ford 18 78 Total 237 27

Source: Ord Minnett estimates from Strike Energy December 2013 quarterly report

Tenement information is summarized in Appendix 1 and key features of each

project are described in the following pages.

Figure 3: Strike Energy project areas

Source: Strike Energy Limited, investor presentation, 27

th February 2014, p 3.

Ord Minnett Research 7 March 2014 Page 8

Company Review

Strike Energy Limited

Southern Cooper Basin Gas Project

Large acreage: Strike has 1.55 million gross acres (~927,000 net acres) in the

southern part of the Cooper Basin. The seven permits have conventional and

unconventional potential from shales, coals and sands and have pipeline access to

south eastern Australia and a potentially fast appraisal and development timeline.

The permit areas are on the southern flanks of the basin, which are less thermally

mature than the centre of the basin, suggesting the permits may contain liquids in

addition to gas and are likely to have lower CO2 levels.

Southern Cooper Gas Project: Strike’s project is targeting coal formations at

depths of 1,500-2,000 m. Coals are the primary oil and gas source rocks in the

Cooper Basin and Strike believes its acreage has the thickest and shallowest

Permian age coals in the basin. The relatively shallow formations should result in

lower drilling costs than the deeper shale and basin centred gas plays being

targeted by other companies in the Patchawarra and Nappamerri troughs further to

the north.

Phase 1 project should deliver ~1800 PJ: Strike is primarily focused on the

“Phase 1 Area” within the PEL 96 permit, which is less than 10 km from the

Moomba to Adelaide Pipeline and contains an estimated 1800 PJ gross

recoverable resource. Strike estimates this is sufficient to supply 25% of NSW’s

energy demand. The proposed pad drilling development concept involves five

“deviated” wells per pad targeting ~50-70 m of net coal thickness across three

zones. Strike previously estimated this would deliver an ex-field cost of $3.00/GJ

excluding royalties, significantly lower than most estimates for shale gas projects.

Orica funding agreement: In July 2013 Strike signed a binding term sheet with

Orica (ASX:ORI, Hold) for a gas supply agreement in which Orica would provide up

to $52.5m in staged payments as partial prepayments for up to 150 PJ of gas over

20 years. In simple terms this is equivalent to $0.35/GJ. Strike retains 66.67% of

the PEL 96 permit and effective control of the PEL 96 joint venture. The gas

subject to the agreement is less than 5% of overall resource within the permit. The

Orica payment will fund pilot test work to establish and contingent resource and

some of the initial development expenditure.

Orora and Austral Bricks gas sales agreements: In January and February 2014

Strike announced gas supply option agreements to supply 30 PJ of gas to Orora

and 12.5 PJ of gas to Austral Bricks respectively. The agreements have the same

key terms, involving a fixed price over a 10 year term from 2017 and the payment of

an option fee to Strike as a gas pre-payment, conditional only on the PEL 96 joint

venture proceeding with a pilot production test project. Orora and Austral can

exercise the supply options when a decision is made by the PEL 96 joint venture to

proceed with project development.

Appraisal program: Initially the PEL 96 joint venture expected to drill three

exploration wells to determine the thickness, continuity and gas content of the coals

in the project area. However, initial results were better than expected, with thicker

coals, and two wells, Le Chiffre 1 and Klebb-1, were sufficient. Completion and

testing of both wells is expected to be undertaken in the June quarter of 2014.

Ord Minnett Research 7 March 2014 Page 9

Company Review

Strike Energy Limited

Figure 4: Cooper Basin permit unconventional focus area

Source: Strike Energy Limited, investor presentation, 27

th February 2014, p 9.

Figure 5: Cooper Basin gas resource

Source: Strike Energy Limited, investor presentation, 27

th February 2014, p 10.

Ord Minnett Research 7 March 2014 Page 10

Company Review

Strike Energy Limited

Cooper Basin conventional

Three of Strike’s seven Cooper Basin permits, PEL 71, 515 and 575, are

prospective for conventional oil & gas. We expect Strike will seek a farm-in partner

to assist in the funding the work program on these permits.

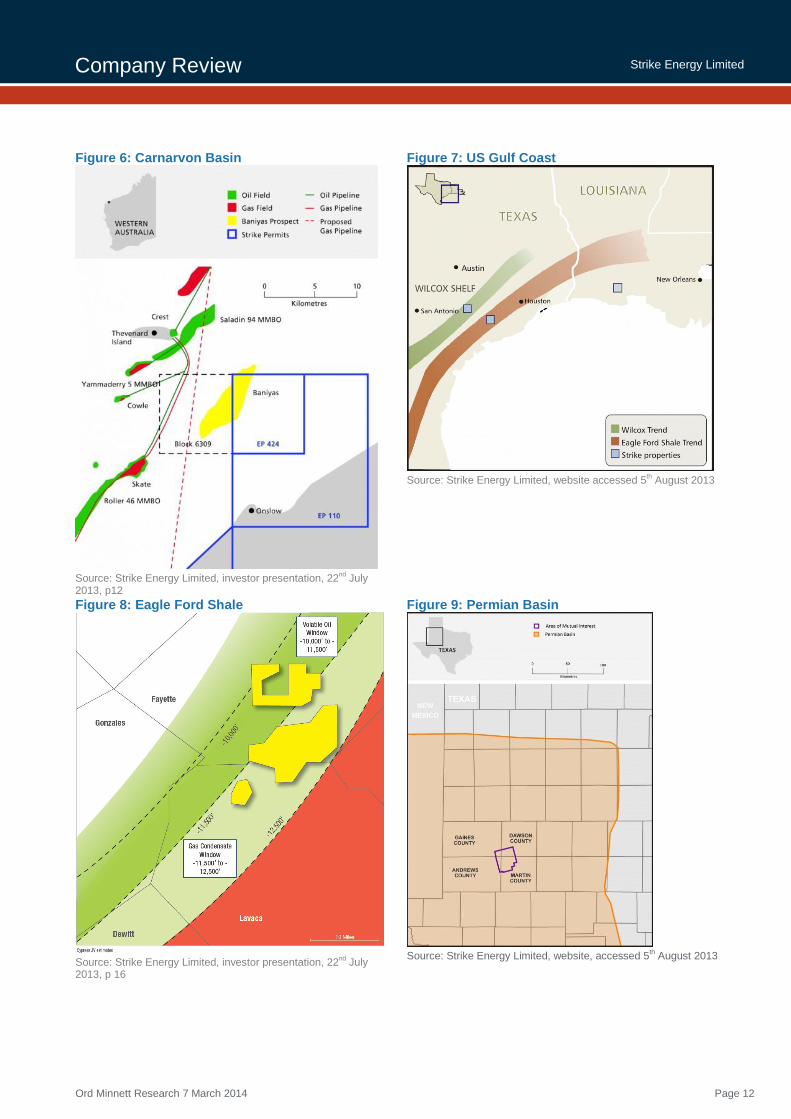

USA unconventional: Eagle Ford Shale

Strike has a 27.5% interest in 41,550 gross acres (10,995 net acres) in the Cypress

Eagle Ford Shale project in Lavaca and Fayette Counties, Texas. The acreage is

on-trend with fields which have demonstrated the north-eastern extension of the

Eagle Ford shale trend in counties to the south west. Approximately 75% of the

acreage is in the gas-condensate window and 25% in the oil window, with the gas-

condensate window typically demonstrating better economics due to high liquids

recovery and strong flow rates.

However, the joint venture has experienced problems with its two Eagle Ford wells.

Given this situation and Strike’s Cooper Basin opportunities we expect Strike will

divest its interest in the Eagle Ford formations during 2014. The joint venture has

engaged corporate advisers to conduct a sale. However, Strike will retain an

interest in the deeper Edwards formation and has farmed out part of its interest in

the Murphy Gas Unit #1 well to be drilled commencing in March. Strike will be free

carried for a 6.875% working interest until casing point.

Commercial production rates are being achieved from Penn Virginia (NYSE: PVA,

not rated) and Magnum Hunter Resources (NYSE: MHR, not rated) in Lavaca

County and from Sanchez Energy (NYSE: SN, not rated) in Fayette County.

Production rates and estimated ultimate recoveries appear to be correlated with

trend window (gas-condensate, oil, etc.), completion horizon and lateral length.

Strike reports recent corporate activity has placed a value of ~$20,000/acre on

nearby producing acreage (Penn Virginia purchased 19,037 contiguous net acres in

Gonzales and Lavaca Counties from Magnum Hunter for $400m in April 2013).

Transactions for early stage acreage have typically been conducted at $US2-

4,000/acre, suggesting Strike may receive ~$20m for its interest.

USA unconventional: Permian Basin

Strike has a 25% interest in the Permian Basin Joint Venture covering a 170,000

acre area of mutual interest (AMI) within the Midland Sub-Basin with Torch Energy,

a privately held Houston-based company. The Joint Venture’s first acquisition, the

MB Clearfork Project, covers 7,500 gross acres (1,875 acres net to Strike) with

existing conventional oil production and reserves and upside from the Lower

Clearfork Shale, estimated to contain original-oil-in-place (OOIP) of 180 kbbl/acre.

The project currently produces ~25-30 boepd net to Strike.

Encouraging results were obtained from the MBCU #16 well drilled in 2012 and the

MBCU #17 well drilled in 2nd

half 2013. The MBCU #17 well was completed in the

Middle Clearfork carbonate zone. A third vertical well is planned to test the Lower

Clearfork Shale section, with drilling expected to commence by the end of March.

Ord Minnett Research 7 March 2014 Page 11

Company Review

Strike Energy Limited

USA conventional

Eaglewood JV (Louise field)

Strike has a 40% working interest in the 704 gross acre (282 net acres) Louise

gas-condensate field in Wharton County, Texas operated by Cypress E&P

Corporation, a private company based in Austin, Texas. The Louise Gardner-

Duncan-1 well, drilled and completed in April 2010, continues to produce gas and

condensate at ~180 boepd net to Strike. The field is in the early stages of natural

decline. The existing 2.5 bcf of 2P reserves (net, after royalties basis) should be

producible from the current well.

MB Clearfork

Strike has a 25% working interest (reducing to 18.75% after project payout) in the

conventional portion of the MB Clearfork project in Texas. No further

development of the conventional resources is planned at this time.

St Landry Canyon

Strike has a 10% working interest in 37,000 gross acres (3,700 net acres) in

onshore Louisiana. The primary targets are deep (18,000 ft, 5,500 m) Wilcox wet

gas prospects (15-30 bbl/mmscf). The first well drilled in August 2011 did not

encounter commercial hydrocarbons. No further exploration is planned at this

time.

Tigre Lagoon

Strike had a 15% working interest in a large (~100 bcf) conventional gas prospect

in onshore Louisiana, but elected not to participate given the cost (~$4m net to

Strike) and risk following 3D seismic analysis. The ~19,000 ft (5,800 m) well is

likely to take six months to drill and cost ~$US20m to drill and a further $14m to

complete.

Carnarvon Basin

Strike has a 44% working interest on average in five permits in the offshore

Carnarvon Basin in Western Australia totalling 1,200 km2 (net to Strike). The WA-

460P permit is adjacent to the WA-384-P permit in which Shell recently drilled the

13.5 tcf Palta gas prospect. Strike had estimated that ~20% of the prospect

extended into Strike’s permit, however the well did not encounter commercial

hydrocarbons and was plugged and abandoned. The permits also include the

small (16 bcf) undeveloped Rivoli gas discovery. A $3.5m sale of four of the

permits (excluding WA-460P) to Torrens Energy Limited (ASX: TEY, not rated)

announced in April 2013 did not proceed. We expect Strike will continue to seek

to divest these permits, or relinquish its interest if divestment is not achieved.

Kingston Lignite Project

Strike has a 100% working interest in a 578 Mt JORC-compliant lignite resource

near Kingston, South Australia in PEL 127 / EL 4576. The resource, discovered

in 1979, is suitable for conventional open cut mining and test work indicates that

the lignite can be gasified to deliver good quality syngas. Approximately $40m (in

today’s dollar terms) has been spent on exploration and appraisal work by

previous owners and Strike. Strike is currently seeking a partner to advance the

project. We believe the project has a high degree of commercial risk and is likely

to face community and environmental opposition.

Ord Minnett Research 7 March 2014 Page 12

Company Review

Strike Energy Limited

Figure 6: Carnarvon Basin

Source: Strike Energy Limited, investor presentation, 22

nd July

2013, p12

Figure 7: US Gulf Coast

Source: Strike Energy Limited, website accessed 5

th August 2013

Figure 8: Eagle Ford Shale

Source: Strike Energy Limited, investor presentation, 22

nd July

2013, p 16

Figure 9: Permian Basin

Source: Strike Energy Limited, website, accessed 5

th August 2013

Ord Minnett Research 7 March 2014 Page 13

Company Review

Strike Energy Limited

Figure 10: Kingston Lignite

Source: Roadmap for Unconventional Gas Projects in South Australian, 12

th December 2012, Chapter 4, pp. 127-128

Figure 11: Kingston Lignite properties

Ord Minnett Research 7 March 2014 Page 14

Company Review

Strike Energy Limited

Key activities

Key activities for the next 18 months involve:

Initial production testing of the two Southern Cooper Basin wells,

Establishing 2P reserves (>200 PJ gross threshold for Stage 1 field

development FID) in the Southern Cooper Basin project, and

Divesting the Eagle Ford shale project.

Figure 12: Near term work program

Source: Strike Energy Limited, investor presentation, 27

th February 2014, p 17.

Figure 13: Southern Cooper development timeline

Source: Strike Energy Limited, investor presentation, 27

th February 2014, p 18.

Ord Minnett Research 7 March 2014 Page 15

Company Review

Strike Energy Limited

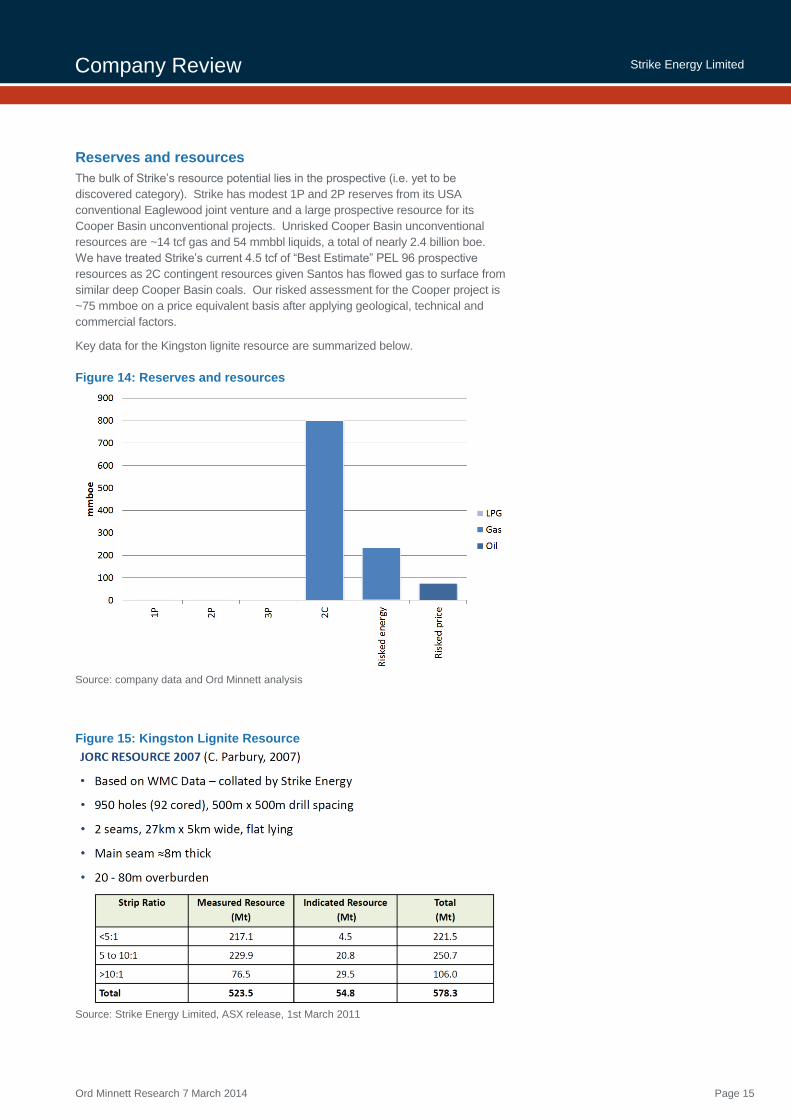

Reserves and resources

The bulk of Strike’s resource potential lies in the prospective (i.e. yet to be

discovered category). Strike has modest 1P and 2P reserves from its USA

conventional Eaglewood joint venture and a large prospective resource for its

Cooper Basin unconventional projects. Unrisked Cooper Basin unconventional

resources are ~14 tcf gas and 54 mmbbl liquids, a total of nearly 2.4 billion boe.

We have treated Strike’s current 4.5 tcf of “Best Estimate” PEL 96 prospective

resources as 2C contingent resources given Santos has flowed gas to surface from

similar deep Cooper Basin coals. Our risked assessment for the Cooper project is

~75 mmboe on a price equivalent basis after applying geological, technical and

commercial factors.

Key data for the Kingston lignite resource are summarized below.

Figure 14: Reserves and resources

Source: company data and Ord Minnett analysis

Figure 15: Kingston Lignite Resource

Source: Strike Energy Limited, ASX release, 1st March 2011

Ord Minnett Research 7 March 2014 Page 16

Company Review

Strike Energy Limited

Cooper Basin CSG versus shale gas

Unconventional play exposure

The Cooper Basin offers exposure to unconventional plays spanning tight gas,

shale gas, basin centred gas and deep coal seams. The primary focus areas of

each of the companies, and the associated exploration permits and formation

depths, are depicted in the chart below.

Strike is targeting moderately deep (~1,500-2,000 m) coal seam gas in the

Southern Cooper Basin (PELs 94, 95 and 96). Strike’s appraisal program has

confirmed the presence of thick, dry/gas saturated coals. The target interval at the

Le Chiffre-1 and Klebb-1 wells has been determined to be in the optimal gas

generation window. The relatively shallow depth, compared to other Cooper Basin

unconventional plays, offers drilling cost advantages.

Figure 16: Cooper Basin unconventional play schematic

Source: Strike Energy Limited, investor presentation, 27

th February 2014, p 11.

Ord Minnett Research 7 March 2014 Page 17

Company Review

Strike Energy Limited

Technical comparison

Strike believes the Southern Cooper coal formations can be appraised and

developed for approximately one quarter of the cost (per unit of gas recovered) of

Cooper shale projects, due to the shallower and less demanding conditions.

Strike’s work suggests that the in-place gas content of Southern Cooper CSG is

similar to Cooper Basin shale at 30-50 bcf/km2. This is significantly higher than the

shallower CSG formations being developed in Queensland’s Surat and Bowen

Basins (at 5-10 bcf/km2).

Our analysis comparative project economics is summarized on the following page.

Figure 17: CSG vs. shale technical comparison

Figure 18: Well productivity comparison

Source: Strike Energy Limited, 2012 AGM presentation, 21

st November 2012, pp. 13-14

Ord Minnett Research 7 March 2014 Page 18

Company Review

Strike Energy Limited

Figure 19: Comparative unrisked NPV per unit of gas

Source: Ord Minnett analysis. 12% nominal discount rate. After tax basis.

Table 4: Comparative cost structure for notional 1000 PJ gas projects

Source: Ord Minnett analysis.

Notes:

- Life cycle costs, real Dec-2013 $ basis.

- Cooper Shale Gas assumes 11 bbl liquids/mmscf raw gas; Cooper Dry Shale Gas assumes zero liquids

- 1000 PJ gas, drilling commences Jan 2014, first gas 2nd

half 2015, plateau from 2019 onwards

- Own gas plant. ~20% CO2 Southern Cooper CSG, 30% Cooper Shale, 5% Bowen CSG

- Shale gas well capex at 30% premium to US analogues

Units Southern Cooper

CSG

Cooper Shale

Gas

Cooper Dry

Shale Gas

Bowen Basin

CSG

Development assumptions

Number of new wells successful - 345 146 146 954

EUR well PJe 2.90 7.30 6.80 1.02

Peak production (6 mth avg) TJe/d 123.3 132.4 123.3 123.3

Well capex per successful well M$A 3.8 15.1 15.1 1.5

Total capex (excluding restoration) M$A 1,839 2,713 2,635 1,771

Performance measures

IRR (after tax) % 19.9 15.8 13.1 18.0

Profitability Index (=1+NPV/PV capex) - 1.3 1.2 1.0 1.2

DCF Payback period years 11.5 11.5 21.5 11.5

NPV/well (unrisked) M$A/well 0.59 0.90 0.23 0.16

NPV/resource (unrisked) $A/GJ 0.20 0.12 0.03 0.16

Cost structure (real Dec-13 $) $A/GJ

Revenue $A/GJ 6.32 7.08 6.31 6.32

Capex $A/GJ 1.66 2.22 2.31 1.58

Cash opex $A/GJ 1.52 1.51 1.46 1.71

Royalties $A/GJ 0.59 0.66 0.57 0.58

Taxes $A/GJ 1.24 1.29 0.92 1.17

Total cost (inc. taxes) $A/GJ 4.42 5.02 4.69 4.45

Net cash (after royalties, before tax) $A/GJ 4.21 4.91 4.28 4.03

NPAT $A/GJ 1.31 1.40 1.05 1.28

Ord Minnett Research 7 March 2014 Page 19

Company Review

Strike Energy Limited

Southern Cooper project development concept

Strike’s planned development concept involves the drilling of five deviated wells

from each drilling pad, with each of the wells intersecting over 50 net metres of

Patchawarra coals, with an expected ultimate recovery of ~3 PJ/well.

This is 50 to 100% more than the 1.5-2.0 PJ of gas that Strike estimates it needs to

recover to break even (based on a $6/GJ price for sales gas delivered into the

MAPS pipeline and drilling and completion costs of $3.5m per well Strike).

Figure 20: Southern Cooper development concept

Source: Strike Energy Limited, investor presentation, 27

th February 2014, p 12

Ord Minnett Research 7 March 2014 Page 20

Company Review

Strike Energy Limited

Valuation model

Methodology

Risk adjusted DCF: We have valued Strike using discounted cash flow analysis for

projects for which sufficient data are available and enterprise value (EV) to area or

EV to resource metrics for exploration prospects and early stage appraisal projects.

We apply a risk factor for each project based on our assessment of the project’s

technical and commercial maturity. We compare resources based on an energy

price equivalent basis, rather than an energy thermal equivalent basis, to better

account for the value differences between liquids and gas prospects.

Simulation model: Our investment model incorporates probability distributions for

key variables (such as reserves, commodity prices and exploration outcomes) and

uses Monte Carlo simulation to quantify the range of share price outcomes.

Long run commodity prices: Our valuation assumes a long run Brent oil price of

$US90/bbl real, USD/AUD exchange rate of 0.80 and 12% nominal discount rate.

We assume the following received price differentials:

Australia: Cooper Basin crude oil: Brent plus $US3/bbl quality and location

premium, less transport; Condensate: North West Shelf Condensate (~95%

of Brent), less transport; LPG: Saudi Contract Price, less processing fee; and

natural gas: ~$A2.90/GJ field gate, increasing to ~$A6.00/GJ from 2015

following the commencement of industry LNG exports.

USA: Crude oil and condensate: Texas (WTI) & Louisiana (LLS), less $US3-

7/bbl transport; NGLs: 33% of crude price; natural gas: Henry Hub:

$US3.20/mmBtu in FY13, rising to $US4.70/mmBtu in real dollar terms by

2017.

The Orica gas prepayment of $52.5m for 150 PJ gas is equivalent to

~$0.35/GJ. Applying a similar multiple to the Orora (30 PJ) and Austral

Bricks (12.5 PJ) gas supply agreements suggests further prepayments of

~$15m.

Fiscal terms: Strike’s Southern Cooper Project will incur a state royalty of 10% and

will pay an effective tax rate of 58% once PRRT (Petroleum Resources Rent Tax)

applies, based on the current corporate income tax rate of 30%. The state royalty is

deductible for PPRT.

Strike’s US projects in Texas incur a mineral owner royalty of 25% of gross

wellhead revenue, plus a state severance tax of 7.5% on gas revenues and 35%

federal income tax. Louisiana projects will incur gross wellhead royalties of 28%,

plus a state severance tax of 12.5% on oil and $US0.16/mscf for gas and NGLs in

addition to federal tax.

Petroleum Resources Rent Tax (PRRT) is levied at 40%. PRRT is deductible for

income tax purposes and is recognised as an income tax under AASB 112 'Income

Taxes'. From 1 July 2012, the existing PRRT regime was extended to all Australian

petroleum production sourced from projects located onshore and in territorial

waters. On transition to the extended PPRT regime, a starting tax base is available

to be deducted against the relevant project profits, giving rise to a potential deferred

tax asset. Strike, unlike other operators in the Cooper Basin, did not apply to the

Minister of Resources and Energy for a combination certificate to treat a list of

petroleum licences as a single project for PRRT purposes, given Strike’s limited

previous expenditure.

Ord Minnett Research 7 March 2014 Page 21

Company Review

Strike Energy Limited

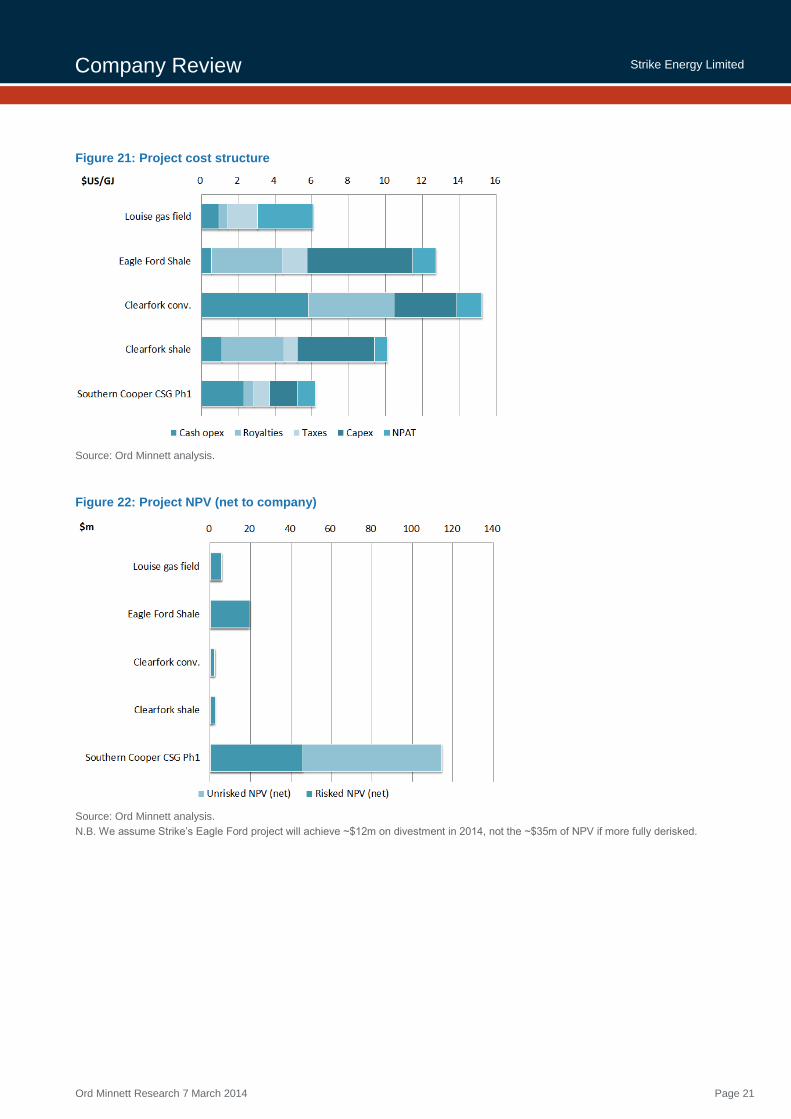

Figure 21: Project cost structure

Source: Ord Minnett analysis.

Figure 22: Project NPV (net to company)

Source: Ord Minnett analysis.

N.B. We assume Strike’s Eagle Ford project will achieve ~$12m on divestment in 2014, not the ~$35m of NPV if more fully derisked.

Ord Minnett Research 7 March 2014 Page 22

Company Review

Strike Energy Limited

Project assumptions

Our primary project assumptions are summarized below. Our valuation of USA

conventional and unconventional projects and Southern Cooper CSG is based on

DCF analysis. Other projects are based on resource or area metrics. We have

valued Strike’s Eagle Ford shale project interest on recent transaction metrics,

described in Appendix 3.

Table 5: Project assumptions

Project Assumptions

USA conventional o Louise gas field: DCF model. 2P reserves produced from single existing well.

o MB Clearfork: DCF model. 1P (PDP) reserves from 19 existing wells.

Eagle Ford shale o DCF model. ~300 gross well sites @ 120 acre spacing (41,550 gross acres) 27.5% STX

o 450-550 kboe/well, 2200 scf/bbl, 1.25 mmBtu/kscf.

o $10m to drill/complete (over-pressured reservoir), ~20% EUR in first year.

o 2 wells CY13, 4-8 wells CY15, full field development CY16+

o Opex k$US6/month/well + $US0.50/mmBtu

o Strike divests 2H CY14. Transaction metric based on $US1,000/acre => $A12m after tax

Permian Basin unconventional

(Clearfork)

o ~190 gross well sites @ 40 acre spacing.

o 125-175 kboe/well, 3600 scf/bbl, 1.4 mmBtu/kscf.

o $2.5m to drill/complete. IP30 ~125 boepd.

o 2 wells CY13, 5-10 wells CY14, full field development CY15+

o Opex k$US6/month/well + $US0.50/mmBtu

o Strike divests CY15 after proof-of-concept is demonstrated.

Southern Cooper CSG

(Phase 1)

o Phase 1 area gross gas resource of 1840 PJ (1227 PJ net to Strike). 70% conversion to 2P

o 5 wells per well pad, 600 acre spacing per pad (120 acres per well).

o $3.5m/well to drill/complete. EUR 2.9 PJ/well (after deducing 12-20% CO2), 2.2 TJ/d IP

o ~$1.00/GJ gas gathering, 3rd

party processing and compression

o ~$1.20/GJ field opex and overheads.

o 2 appraisal wells FY14, 6 pilot wells late CY14, FID Stage 1 field development late CY15.

o Strike retains 66.7% interest.

Southern Cooper CSG (Phase 2+)

o Resource multiple valuation, based on Phase 1 NPV value.

o 21,822 bcf gross per 19th

September 2012 resource estimate less Phase 1 development

o 20% assumed CO2, 50% net interest (PEL 94/95/96), 50% conversion to reserves

o (21,822*(1-0.2)*0.99*1.0551*50%-1,227)*50% = 3,945 PJ * $0.15/GJ * 10% risk = ~$60m.

Cooper Basin shale gas

o Area multiple valuation

o 2,198 km2 gross permit area (PEL 94/95), ~44% average net interest

o Value at $140-550/acre for Cooper Basin shale transactions => $33-132 net.

Kingston Lignite o 587 Mt JORC resource (523.5 Mt Measured, 54.8 Mt Inferred)

o $0.10/t EV/thermal coal resource multiple after adjusting for calorific value (Newcastle

standard thermal coal 6,080 kcal/kg Net As Received (6,300 kcal/kg GAR); Kingston lignite

22.7 MJ/kg (dry basis) = ~2500 kcal/kg GAR).

o 10% risk factor (for technical and commercial maturity, likely community opposition).

Carnarvon Basin o $3.5m upper value based on recent farm-out proposal (which did not complete).

o No value ascribed to WA 460P following the recent Palta-1 outcome (P&A’d).

Source: company data and Ord Minnett estimates

Ord Minnett Research 7 March 2014 Page 23

Company Review

Strike Energy Limited

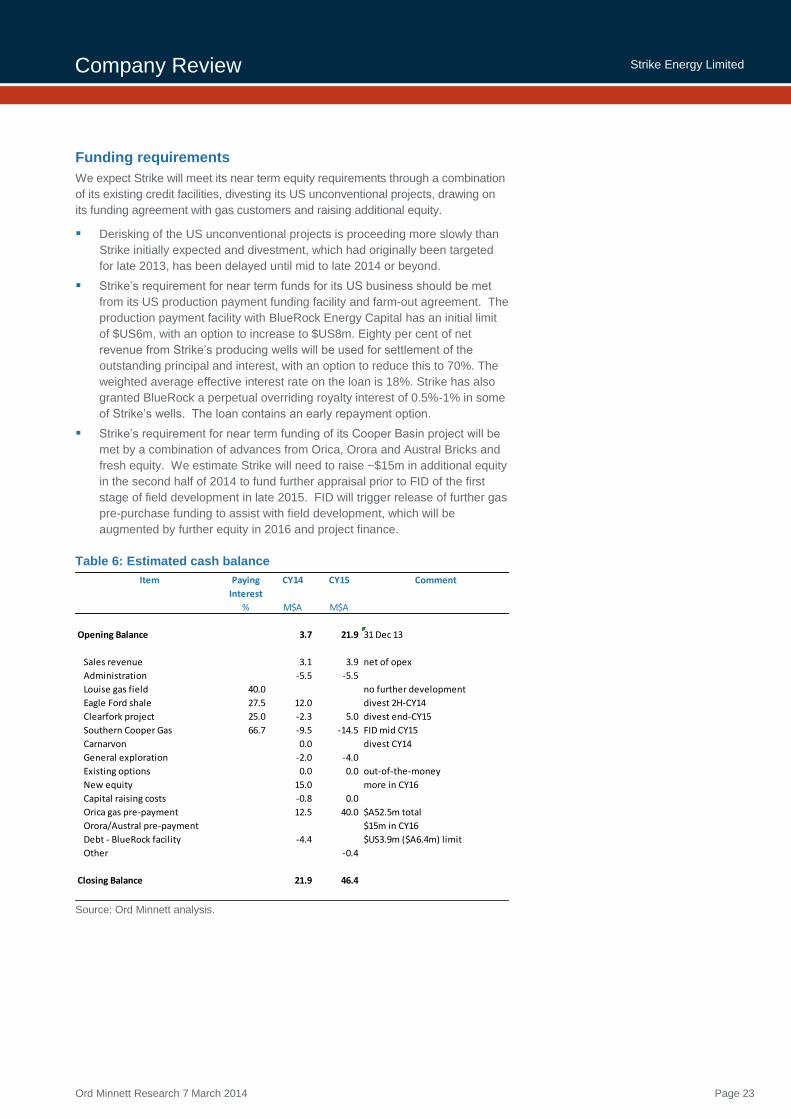

Funding requirements

We expect Strike will meet its near term equity requirements through a combination

of its existing credit facilities, divesting its US unconventional projects, drawing on

its funding agreement with gas customers and raising additional equity.

Derisking of the US unconventional projects is proceeding more slowly than

Strike initially expected and divestment, which had originally been targeted

for late 2013, has been delayed until mid to late 2014 or beyond.

Strike’s requirement for near term funds for its US business should be met

from its US production payment funding facility and farm-out agreement. The

production payment facility with BlueRock Energy Capital has an initial limit

of $US6m, with an option to increase to $US8m. Eighty per cent of net

revenue from Strike’s producing wells will be used for settlement of the

outstanding principal and interest, with an option to reduce this to 70%. The

weighted average effective interest rate on the loan is 18%. Strike has also

granted BlueRock a perpetual overriding royalty interest of 0.5%‐1% in some

of Strike’s wells. The loan contains an early repayment option.

Strike’s requirement for near term funding of its Cooper Basin project will be

met by a combination of advances from Orica, Orora and Austral Bricks and

fresh equity. We estimate Strike will need to raise ~$15m in additional equity

in the second half of 2014 to fund further appraisal prior to FID of the first

stage of field development in late 2015. FID will trigger release of further gas

pre-purchase funding to assist with field development, which will be

augmented by further equity in 2016 and project finance.

Table 6: Estimated cash balance

Source: Ord Minnett analysis.

Item Paying CY14 CY15 Comment

Interest

% M$A M$A

Opening Balance 3.7 21.9 31 Dec 13

Sales revenue 3.1 3.9 net of opex

Administration -5.5 -5.5

Louise gas field 40.0 no further development

Eagle Ford shale 27.5 12.0 divest 2H-CY14

Clearfork project 25.0 -2.3 5.0 divest end-CY15

Southern Cooper Gas 66.7 -9.5 -14.5 FID mid CY15

Carnarvon 0.0 divest CY14

General exploration -2.0 -4.0

Existing options 0.0 0.0 out-of-the-money

New equity 15.0 more in CY16

Capital raising costs -0.8 0.0

Orica gas pre-payment 12.5 40.0 $A52.5m total

Orora/Austral pre-payment $15m in CY16

Debt - BlueRock facility -4.4 $US3.9m ($A6.4m) limit

Other -0.4

Closing Balance 21.9 46.4

Ord Minnett Research 7 March 2014 Page 24

Company Review

Strike Energy Limited

Valuation model

Production

Production declines modestly in the early years due to natural decline from

the Louise gas field, before building strongly from 2017 once Phase 1 of the

Southern Cooper CSG project comes on-line.

Product mix is approximately 20-30% liquids in the early years, and then

effectively 100% gas following start-up of the Southern Cooper CSG project.

Income statement

Revenue is relatively flat at $5-7m in the early years, before growing strongly

from 2017, building to over $200m by 2020.

EBITDA grows strongly from 2017 driven by Southern Cooper CSG

production.

Normalized NPAT is negative in the early years before building from 2017 to

over $70m by 2020.

NPAT is negative in the early years, with impairment of oil and gas assets.

Cash flow statement

Operating cash flow remains negative in the early years, until building

strongly from 2017, to over $100m per year from 2020. “Other operating

cash flow” includes the gas sales agreement prepayments from Orica, Orora

and Austral Bricks.

Capex is substantial, growing from ~$13m in FY14 to over $50m by 2017

and $70m from 2020, associated with Phase 1 development of the Southern

Cooper CSG project.

Other investing items include the assumed divestment of Strike’s Eagle

Ford assets in late 2014 and Permian Basin assets in 2015.

Financing cash flow includes assumed equity raisings in FY15 and FY16

and debt in FY17 and FY18 to develop Phase 1 of the Southern Cooper CSG

project.

Balance sheet

Cash fluctuates due to project development requirements. Cash builds after

2020 once the bulk of the Phase 1 development is completed.

Net debt increases during FY17 and FY18 before being paid down with

increasing operating cash flows late in the decade.

Financial ratios

EBITDA margin rises to ~$18/boe once production commences from the

Southern Cooper Gas project.

Interest cover rises to 6-7 times by around 2020.

Price to earnings ratio drops to ~2.5 times by 2020.

Ord Minnett Research 7 March 2014 Page 25

Company Review

Strike Energy Limited

Production and revenue

Production Sales revenue

PRODUCTION units FY12A FY13A FY14E FY15E FY16E FY17E FY18E FY19E FY20E FY21E

Production by project

Louise gas field mmboe 0.1 0.1 0.1 0.1 0.1 0.1 0.0 0.0 0.0 0.0

Eagle Ford Shale mmboe - 0.0 0.0 0.0 - - - - - -

Clearfork conv. mmboe 0.0 0.0 0.0 0.0 0.0 - - - - -

Clearfork shale mmboe - 0.0 0.0 0.0 0.0 - - - - -

Southern Cooper CSG Ph1 mmboe - - 0.0 0.0 0.0 0.0 1.9 2.7 4.1 4.9

Southern Cooper CSG mmboe - - - - - - - - - -

Cooper Shale Gas mmboe - - - - - - - - - -

Cooper Dry Shale Gas mmboe - - - - - - - - - -

Bowen Basin CSG mmboe - - - - - - - - - -

Tigre Lagoon mmboe - - - - - - - - - -

Total mmboe 0.2 0.1 0.1 0.1 0.1 0.1 2.0 2.7 4.1 4.9

Total production kboed 0.42 0.36 0.31 0.32 0.26 0.14 5.43 7.43 11.22 13.38

Production growth % -14.1 -13.3 2.8 -20.5 -45.0 3,746.2 36.9 51.0 19.3

PRICES & REVENUE nominal $ FY12A FY13A FY14E FY15E FY16E FY17E FY18E FY19E FY20E FY21E

Price markers

Forex (period average) $US/$A 1.03 1.03 0.90 0.88 0.83 0.80 0.80 0.80 0.80 0.80

WTI $US/bbl 95 92 102 96 91 91 93 95 97 100

Brent $US/bbl 113 109 109 102 97 97 99 101 103 105

Nat Gas (Henry Hub) $US/mmBtu 3.0 3.2 3.8 4.4 4.9 5.1 5.2 5.3 5.4 5.5

Nat Gas (NE Australia) $A/GJ 3.9 4.3 5.7 7.1 7.3 7.3 7.5 7.6 7.8 7.9

LNG $US/mmBtu 16.7 16.1 16.2 15.2 14.6 14.5 14.8 15.1 15.4 15.8

Qld average RRP $A/MWh 9 12 16 16 20 20 21 21 22 22

Received prices

Oil $US/bbl 90 88 98 94 89 - - - - -

Condensate $US/bbl 103 98 98 90 86 85 87 89 91 93

Gas $US/mmBtu 3.0 3.2 3.7 3.8 4.2 5.1 5.3 5.6 5.8 6.0

LPG $US/bbl - - - - - - - - - -

LNG $US/t - - - - - - - - - -

Electricity $US/MWh - - - - - - - - - -

Total 28 34 40 43 41 33 31 32 34 35

Revenue

Oil M$A 1 1 2 3 2 - - - - -

Condensate M$A 1 2 1 1 0 0 0 0 0 0

Gas M$A 2 2 2 2 2 2 76 110 174 213

LPG M$A - - - - - - - - - -

LNG M$A - - - - - - - - - -

Electricity M$A - - - - - - - - - -

Total modelled M$A 4 4 5 6 5 2 76 110 174 213

Total reported M$A 5 5 - - - - - - - -

Source: company data and Ord Minnett forecasts $A currency unless otherwise noted. Nominal $ basis. Year ending June.

-

1.0

2.0

3.0

4.0

5.0

6.0

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

mmboe Electricity LNG LPG GasCondensate Oil Act/Target

-

50

100

150

200

250

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

$m Electricity LNG LPG Gas Condensate Oil

Ord Minnett Research 7 March 2014 Page 26

Company Review

Strike Energy Limited

Financial Statements

Earnings Cash flow

INCOME STATEMENT M$A FY12A FY13A FY14E FY15E FY16E FY17E FY18E FY19E FY20E FY21E

Sales revenue 5 5 5 6 5 2 77 110 174 213

Other revenue 1 2 - - - - - - - -

COGS & opex -8 -7 -7 -8 -7 -6 -43 -58 -88 -106

Other 0 3 - - - - - - - -

EBITDA -2 3 -2 -2 -2 -4 34 52 86 107

Depreciation and Amortization -13 -13 -1 -2 -3 -1 -3 -5 -8 -13

EBIT -15 -11 -3 -4 -5 -5 31 46 78 94

Net Interest Expense 0 0 -1 -3 -2 -2 -7 -12 -13 -13

EBT -14 -11 -4 -6 -7 -7 24 35 65 81

Tax expense - 0 -0 1 -1 -0 -0 -0 -18 -24

Minorities / prefered dividends - - - - - - - - - -

Normalized NPAT -14 -10 -4 -5 -8 -7 24 34 46 56

Abnormals -0 -4 - 7 -2 - - - - -

Reported NPAT -14 -14 -4 2 -10 -7 24 34 46 56

Effective tax rate % 0.0 8.4 0.0 41.0 0.0 0.0 0.3 0.2 28.6 30.1

CASH FLOW STATEMENT M$A FY12A FY13A FY14E FY15E FY16E FY17E FY18E FY19E FY20E FY21E

EBITDA -2 3 -2 -2 -2 -4 34 52 86 107

Other operating items (tax, etc) 0 -3 9 5 56 1 -4 -4 -13 -27

Operating cash flow -2 -0 7 3 53 -3 29 47 73 80

PPE capex -0 -0 - - - - - - - -

Exploration capex -22 -10 -0 -4 -4 -4 -4 -4 - -

Development capex -3 -7 -7 -22 -19 -25 -46 -67 -69 -70

Other investing items 0 - 2 12 7 - - - - -

Investing cash flow -25 -17 -5 -14 -16 -29 -50 -71 -69 -70

Inc/(Dec) in Equity 40 - 9 14 19 - - - - -

Inc/(Dec) in Borrowings - 2 2 -2 - 20 32 -11 -11 -11

Dividends paid - - - - - - - - - -

Other financing items -0 - -0 -1 - - - - - -

Financing Cash Flow 40 2 11 10 19 20 32 -11 -11 -11

Net Inc/(Dec) in Cash 13.7 -15.1 12.7 -0.6 56.7 -11.6 11.6 -34.9 -6.8 -1.3

Free cash flow -26.3 -17.5 1.9 -10.9 37.7 -31.6 -20.1 -24.1 4.1 9.5

BALANCE SHEET M$A FY12A FY13A FY14E FY15E FY16E FY17E FY18E FY19E FY20E FY21E

Cash & cash equivalents 17 1 9 8 65 53 65 30 23 22

Other current assets 3 4 4 4 3 3 10 15 18 21

PPE, Exp & Dev 45 46 53 75 86 114 161 227 287 344

Other non-current assets 0 0 0 2 2 2 2 2 8 4

Total Assets 65 51 66 89 156 172 237 274 337 391

Short term debt - 3 1 1 1 5 11 9 7 4

Other current liabilities 4 1 1 1 1 1 4 5 19 36

Long term debt - 0 4 2 2 18 43 35 26 17

Other non-current liabilities 1 0 1 5 7 10 17 28 38 50

Total Liabilities 4 4 7 9 10 34 75 77 90 109

Minorities - - - - - - - - - -

Total Funds Employed 61 47 58 80 146 138 162 196 247 282

Debt - 3 5 3 3 23 54 44 33 22

Net debt -17 1 -4 -5 -62 -31 -10 14 10 0

Source: company data and Ord Minnett forecasts $A currency unless otherwise noted. Nominal $ basis. Year ending June.

-100

-80

-60

-40

-20

-

20

40

60

80

100

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

$m Financing Cash Flow Investing cash flowOperating cash flow Free cash flow

-50

-

50

100

150

200

250

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

$m Sales revenue EBITDA Normalized NPAT Abnormals

Ord Minnett Research 7 March 2014 Page 27

Company Review

Strike Energy Limited

Financial Analysis

Debt Funding

OPERATIONAL METRICS FY12A FY13A FY14E FY15E FY16E FY17E FY18E FY19E FY20E FY21E

EBITDA margin % -34.3 55.6 -44.8 -32.0 -50.2 -188.2 44.0 46.9 49.5 50.2

EBIT margin % -313.5 -232.8 -60.7 -62.4 -106.0 -236.8 40.5 42.1 44.6 44.0

Normalized NPAT margin % -307.1 -222.4 -80.0 -81.3 -163.3 -353.8 31.0 31.3 26.5 26.4

Revenue growth % -2.1 10.9 13.7 -19.0 -55.3 3,542.9 43.8 58.3 22.4

EBITDA growth % -258.6 -189.4 -18.7 27.0 67.5 -951.8 53.3 66.9 24.2

EBIT growth % -27.3 -71.1 16.8 37.6 -0.2 -722.7 49.5 67.8 20.8

Normalized ROA % -22.2 -20.0 -6.2 -5.3 -4.9 -4.3 10.0 12.6 13.7 14.4

Normalized ROE % -23.7 -21.7 -7.0 -5.9 -5.3 -5.4 14.6 17.5 18.7 20.0

VALUATION RATIOS FY12A FY13A FY14E FY15E FY16E FY17E FY18E FY19E FY20E FY21E

Fully diluted shares (end of period) 000,000 614.5 614.5 1,003.2 1,003.2 1,003.2 1,003.2 1,003.2 1,003.2 1,003.2 1,003.2

Weighted fully diluted shares 000,000 434.2 614.5 906.1 1,003.2 1,003.2 1,003.2 1,003.2 1,003.2 1,003.2 1,003.2

Share price (end of period) $/share 0.15 0.07 0.14 0.14 0.14 0.14 0.14 0.14 0.14 0.14

Market Cap M$A 92 45 135 135 135 135 135 135 135 135

Less Net Debt M$A -17 1 -4 -5 -62 -31 -10 14 10 0

Market EV M$A 76 47 132 130 73 105 125 149 145 136

EPS before abnormals c -3.3 -1.7 -0.5 -0.5 -0.8 -0.7 2.4 3.4 4.6 5.6

EPS growth % -49.9 -72.9 4.3 62.8 -3.2 -418.9 45.4 33.8 22.3

PER x -4.1 -8.1 -30.0 -28.7 -17.6 -18.2 5.7 3.9 2.9 2.4

Op Cash flow per share c -0.4 -0.1 0.8 0.3 5.3 -0.3 2.9 4.7 7.3 8.0

Price / Op Cash flow x -37.1 -227.3 17.2 39.7 2.5 -52.4 4.6 2.9 1.9 1.7

EV/EBITDA (n.b. future EV) x -73.8 53.5 -57.7 -70.0 -31.1 -26.5 3.7 2.9 1.7 1.3

LEVERAGE FY12A FY13A FY14E FY15E FY16E FY17E FY18E FY19E FY20E FY21E

Net Debt / Book Equity % -27 3 -6 -7 -43 -22 -6 7 4 0

Net Debt / (ND+Book Equity) % -37 3 -6 -7 -74 -28 -7 6 4 0

Net Debt / Total Assets % -25 2 -5 -6 -40 -18 -4 5 3 0

EBIT Interest cover x - - -3.5 -1.4 -3.0 -2.1 4.3 3.9 5.9 7.1

Debt / Free Cash Flow x - -0.2 2.7 -0.2 0.1 -0.7 -2.7 -1.8 8.0 2.3

MARGIN ANALYSIS real $ FY12A FY13A FY14E FY15E FY16E FY17E FY18E FY19E FY20E FY21E

Revenue/boe $A/boe 41 53 44 48 48 38 35 36 37 37

Opex/boe $A/boe 52 33 64 63 72 110 20 19 19 19

EBITDA margin/boe $A/boe -11 20 -20 -15 -24 -72 15 17 18 19

D&A/boe $A/boe 88 102 7 15 27 18 1 2 2 2

Tax and financing/boe $A/boe -2 -4 9 9 27 44 3 4 7 7

Cash margin % -26 37 -45 -32 -50 -188 44 47 49 50

EBIT margin % -241 -156 -61 -62 -106 -237 40 42 45 44

NPAT margin % -236 -207 -80 38 -205 -354 31 31 26 26

Resource to production ratio years 955.6 1,114.3 1,283.7 1,248.1 1,563.9 2,851.3 73.6 53.0 34.1 28.3

Product mix (liquids % of total) % 13 21 25 30 26 7 0 0 0 0

Source: company data and Ord Minnett forecasts $A currency unless otherwise noted. Nominal $ basis. Year ending June.

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

-

10

20

30

40

50

60

70

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

x$mDebt Net cashNet Debt / (ND+Book Equity) EBIT Interest cover

-

10

20

30

40

50

60

70

-20

-10

-

10

20

30

40

50

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

Cash ->

$mDividends paid Inc/(Dec) in BorrowingsInc/(Dec) in Equity Cash & cash equivalents

Ord Minnett Research 7 March 2014 Page 28

Company Review

Strike Energy Limited

Corporate overview

Board

Mark Carnegie, BA and a BSc (Hons), Chairman

Mark Carnegie has over 30 years’ experience as an entrepreneur, investor and

corporate adviser in New York, London and Sydney. He was a principal of

Carnegie, Wylie & Company before the acquisition by Lazard Limited and was

previously the CEO of Lazard Australia Private Equity Pty Ltd. He established M.H.

Carnegie & Co. Pty Ltd in 2010, a venture capital and private equity firm. Mark is a

Director of Macquarie Radio Network Ltd, Chandler Macleod Group Limited and a

large number of private companies. He was appointed Non-Executive Director on

9th August 2013 and Chairman 19th August 2010

David Wrench, B Eng (Mining) Hons, Managing Director

David Wrench has worked in Australia and North America with Macquarie Bank,

Credit Suisse and Chase Manhattan Bank in the precious metals, base metals and

energy sectors. David was a co-founder and director of CH4 Gas Limited. He was

appointed to the Board on 29 October 1998 and assumed the role of Managing

Director on 1 October 2011.

Tim Clifton, BSc (Hons), Non-Executive Director

Tim Clifton has over 40 years mining and corporate experience as a geologist and

company director. He was appointed to the Board on 13 August 2008 and

appointed Chairman on 19 August 2010. He stood down as Chairman on 11th

September 2013.

Simon Ashton, B Sc (Hons) M Sc MBA, Non-Executive Director

Simon Ashton has over 30 years’ experience in the Australian and international

petroleum and resources industries. He established Western Mining Corporation’s

USA petroleum subsidiary, Greenhill Petroleum, co-founded Strike Energy in 1997

and served as MD until September 2011.

Tim Goyder, Non-Executive Director

Tim Goyder has over 30 years’ experience in the natural resources industry and

has been involved in the formation and management of a number of publicly listed

companies. He is currently the chairman of Chalice Gold Mines Limited and

Liontown Resources Limited, and a director of Uranium Equities Limited. Tim was

appointed a director on 19 August 2010.

David L Baker BA, LL.B (Hons), Non-Executive Director

David Baker is a lawyer with experience in structured debt, utility financing, project

finance and mergers and acquisitions as an adviser, lender and principal in

Australia and Singapore. He was previously Executive Director of Gryphon

Partners, a corporate advisory house focused on the resources industry and a

senior executive in the resources team at Standard Chartered Bank. He conducts

his own corporate advisory business and, in that capacity, provides consulting

services to Strike Energy. David was appointed as a Non-Executive Director on 11

August 2013.

Ord Minnett Research 7 March 2014 Page 29

Company Review

Strike Energy Limited

Management

David Wrench, B Eng (Mining) Hons, Managing Director

As above.

Ben Thomas, B Sc (Petroleum Engineering), Executive Director

Ben Thomas joined Strike in mid-2010 and is the Company’s President of US

Operations. Prior to joining Strike, Ben had over 40 years upstream petroleum

sector experience with Mobil Oil Corporation, Superior Oil Company, Mark

Producing, Edisto Resources and Hall-Houston Oil Company. He was appointed a

Director on 29 September 2011

Sean McGuinness, B Comm, Chief Financial Officer and Company Secretary

Sean McGuinness was previously GM-Finance with the ASX listed Group Lynas

Corporation (LYC.AX, Spe Buy) and prior to that, Chief Accountant with Rank

Group Limited (New Zealand). Sean worked in the UK and US with ConocoPhillips

and in Australia with KPMG and PricewaterhouseCoopers.

Chris Thompson, General Manager - Cooper Basin

Chris Thompson has 20 years of experience in the oil and gas industry with

qualifications in both geology and reservoir engineering. He previously worked for

Oil Company of Australia, Schlumberger, Oil Search, Novus Petroleum, Leed

Petroleum and Origin Energy. He joined Strike in September 2012.

Don Poynton, Manager of Exploration and Environment

Don Poynton joined Strike Energy in 1997 after working for 25 years in technical

and management roles with GSI, Burmah/Woodside, Mesa and WMC Resources.

Rob Weeden, Manager of Geoscience

Rob Weeden has over 30 years’ experience in both the mineral and petroleum

industries, in Australia, the USA and South America. He joined Strike in 1997.

Ord Minnett Research 7 March 2014 Page 30

Company Review

Strike Energy Limited

Capital structure

Shares on

issue:

706,519,664

Options: 20,200,000 @ various dates and various prices

Performance

rights:

-

Convertible

notes:

-

Substantial

shareholders:

M H Carnegie & Co Pty Ltd 8.0%

Ownership: Top 20 shareholders as of 30th

June 2013

Source: Strike Energy Limited, 2013 Annual Report, p 74

Ord Minnett Research 7 March 2014 Page 31

Company Review

Strike Energy Limited

Appendices

Appendix 1: Tenement summary

Source: Ord Minnett, company data

Permit Current Area Expiry Partners Status

Interest gross date

% km2

Cooper/Otway conventional

PEL 71 75.00 4,609

PEL 515 100.00 3,038 -

PEL 575 100.00 3,804 -

ATP 549P - Cypress Block 5.00 540 Australian Gasfields

PPL 210 50.00 BPT

PEL 127 (Otway) 100.00 - Kingston Lignite project

Cooper Basin unconventional

PEL 94 35.00 901 BPT 1 vertical well (Davenport-1)

PEL 95 50.00 1,297 BPT 1 vertical well (Marsden-1)

PEL 96 66.70 2,707 EWC 2 vertical wells late CY13

Carnarvon Basin

EP 110 61.54 attempted divestment 1H CY13

EP 325 44.50 "

EP 424 61.54 "

WA 261P 19.94 Apache Rivoli gas discovery (small)

WA 460P 33.33 Shell Palta-1 next door, P&A'd

USA conventional

Eaglewood JV 40.00 49 Cypress Louise-1 in prod'n, 1.4 mmscfd

St Landry Canyon 10.00 150 West Plum Bob P&A'd 2H CY11

Tigre Lagoon 15.00 3D seismic 2H CY12

USA unconventional

Eagle Landing JV 27.50 157 Torch Bingham-1H 2H CY12

MB Clearfork 25.00 30 Cypress 16 existing conv, core testing

Geothermal / coal

GEL 526 100.00 -

GEL 527 100.00 -

EL 5476 (Mineral) 100.00 - JORC resource (lignite)

Net area km2 13,180

acres 3,255,562

Ord Minnett Research 7 March 2014 Page 32

Company Review

Strike Energy Limited

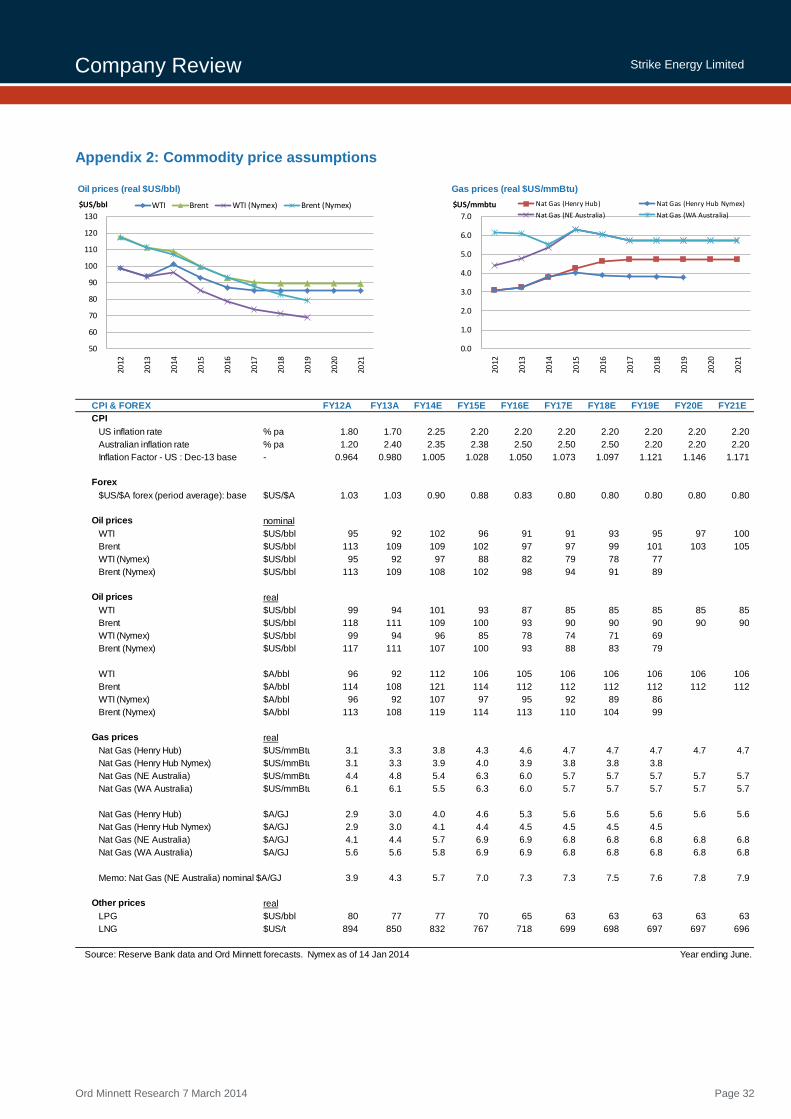

Appendix 2: Commodity price assumptions

Oil prices (real $US/bbl) Gas prices (real $US/mmBtu)

CPI & FOREX FY12A FY13A FY14E FY15E FY16E FY17E FY18E FY19E FY20E FY21E

CPI

US inflation rate % pa 1.80 1.70 2.25 2.20 2.20 2.20 2.20 2.20 2.20 2.20

Australian inflation rate % pa 1.20 2.40 2.35 2.38 2.50 2.50 2.50 2.20 2.20 2.20

Inflation Factor - US : Dec-13 base - 0.964 0.980 1.005 1.028 1.050 1.073 1.097 1.121 1.146 1.171

Forex

$US/$A forex (period average): base $US/$A 1.03 1.03 0.90 0.88 0.83 0.80 0.80 0.80 0.80 0.80

Oil prices nominal

WTI $US/bbl 95 92 102 96 91 91 93 95 97 100

Brent $US/bbl 113 109 109 102 97 97 99 101 103 105

WTI (Nymex) $US/bbl 95 92 97 88 82 79 78 77

Brent (Nymex) $US/bbl 113 109 108 102 98 94 91 89

Oil prices real

WTI $US/bbl 99 94 101 93 87 85 85 85 85 85

Brent $US/bbl 118 111 109 100 93 90 90 90 90 90

WTI (Nymex) $US/bbl 99 94 96 85 78 74 71 69

Brent (Nymex) $US/bbl 117 111 107 100 93 88 83 79

WTI $A/bbl 96 92 112 106 105 106 106 106 106 106

Brent $A/bbl 114 108 121 114 112 112 112 112 112 112

WTI (Nymex) $A/bbl 96 92 107 97 95 92 89 86

Brent (Nymex) $A/bbl 113 108 119 114 113 110 104 99

Gas prices real

Nat Gas (Henry Hub) $US/mmBtu 3.1 3.3 3.8 4.3 4.6 4.7 4.7 4.7 4.7 4.7

Nat Gas (Henry Hub Nymex) $US/mmBtu 3.1 3.3 3.9 4.0 3.9 3.8 3.8 3.8

Nat Gas (NE Australia) $US/mmBtu 4.4 4.8 5.4 6.3 6.0 5.7 5.7 5.7 5.7 5.7

Nat Gas (WA Australia) $US/mmBtu 6.1 6.1 5.5 6.3 6.0 5.7 5.7 5.7 5.7 5.7

Nat Gas (Henry Hub) $A/GJ 2.9 3.0 4.0 4.6 5.3 5.6 5.6 5.6 5.6 5.6

Nat Gas (Henry Hub Nymex) $A/GJ 2.9 3.0 4.1 4.4 4.5 4.5 4.5 4.5

Nat Gas (NE Australia) $A/GJ 4.1 4.4 5.7 6.9 6.9 6.8 6.8 6.8 6.8 6.8

Nat Gas (WA Australia) $A/GJ 5.6 5.6 5.8 6.9 6.9 6.8 6.8 6.8 6.8 6.8

Memo: Nat Gas (NE Australia) nominal $A/GJ 3.9 4.3 5.7 7.0 7.3 7.3 7.5 7.6 7.8 7.9

Other prices real

LPG $US/bbl 80 77 77 70 65 63 63 63 63 63

LNG $US/t 894 850 832 767 718 699 698 697 697 696

Source: Reserve Bank data and Ord Minnett forecasts. Nymex as of 14 Jan 2014 Year ending June.

50

60

70

80

90

100

110

120

130

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

$US/bbl WTI Brent WTI (Nymex) Brent (Nymex)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

$US/mmbtu Nat Gas (Henry Hub) Nat Gas (Henry Hub Nymex)

Nat Gas (NE Australia) Nat Gas (WA Australia)

Ord Minnett Research 7 March 2014 Page 33

Company Review

Strike Energy Limited

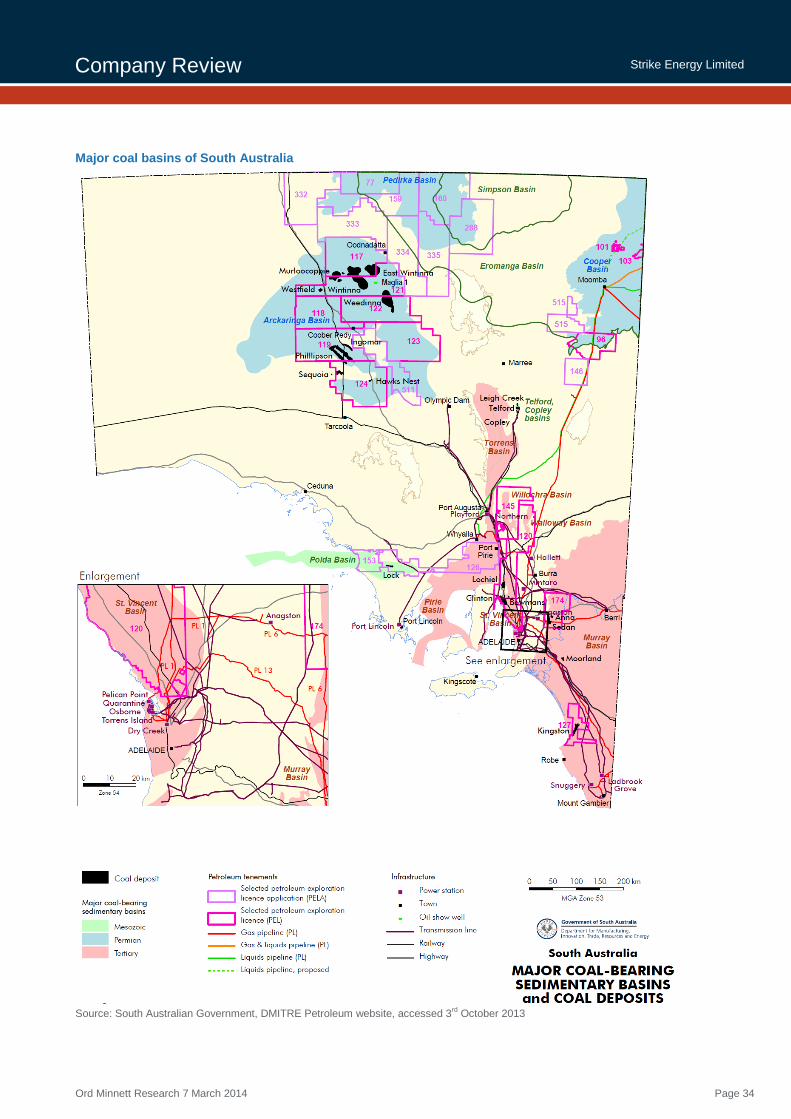

Appendix 3: South Australian coal seam gas potential

Limited existing data: Evaluation of the CSG potential of South Australia is less

advanced than in Queensland. Almost all known coal deposits have been

evaluated for mining potential, but not for coal seam gas. The depth and maturity of

the coal deposits and distance to infrastructure and markets have prevented

economic exploitation of all except the Leigh Creek Coalfield. A collaborative

research project between PIRSA and the Australian School of Petroleum was

established in 2006 to undertake a desktop evaluation of the state’s CSG and UCG

potential. Some seismic, drilling and coal desorption analysis is included in current

company work programs.

Predominantly immature coals: Gas content is a major economic consideration in

assessing CSG potential. As yet there are no desorption measurements of South

Australian coals. The South Australian coals at exploitable depths for CSG are

generally immature and have Vitrinite Reflectance maturities below the 0.8%

threshold needed for significant thermogenic methane production (200–300 scf/t).

Hence South Australian CSG prospects may need a contribution from a biogenic

methane (similar to the Powder River Basin in the USA) to have economic gas

contents.

Permian coals: Extensive and thick Permian coal measures occur in the

Arckaringa, Pedirka and Cooper basins. These deposits are similar in age to proven

eastern Australian CSG producing basins (i.e. Bowen and Surat basins). Coals in

the Pedirka and Arckaringa basins are shallower and less mature for oil and gas

generation (sub-bituminous) than Cooper Basin coals. Coals in the Cooper Basin

are a proven source of conventional oil and gas and occur at depths from 2000–

3500 m (bituminous to anthracite rank). The Patchawarra Formation contains a

major coal seam which forms an important seismic reflector. The Weena Trough in

the southern Cooper Basin, targeted by Strike Energy, contains the shallowest

occurrences of thick Patchawarra Formation sub-bituminous coal seams.

Deep CSG: The deepest CSG production in the USA is from 2500m in the

Piceance Basin and 2000m is generally considered the floor for CSG production

due to cleat closure and permeability reduction at these depths. However Santos

has flowed gas to surface from a fracced Patchawarra coal at ~2900m in the

Moomba 77 well. .

Triassic coals measures are currently being mined at Leigh Creek (the only

operating coal mine in South Australia). This Triassic coal is sub-bituminous in rank,

and is mined at the margins of the Telford Basin, but extends to depths in excess of

1000 m in the basin centre. Jurassic coal measures form a deposit at Lock in the

Polda Basin. Jurassic coals also occur in the deeper parts of the Eromanga Basin in

the Poolowanna and Birkhead formations. Cretaceous coal measures are known

from the Otway Basin (e.g. Eumeralla Formation) and Eromanga Basin (Winton

Formation); the latter is a potential exploration target for CSG.

Tertiary coals are typically low-grade shallow lignites (<100 m deep) that occur in

intracratonic and structurally controlled basins located along Australia’s southern

margin. In South Australia this includes the Pirie-Torrens, St Vincent and Murray

basins. These coals are typically high in moisture, sulphur, sodium and chlorine and

the shallow depth limits reservoir pressure and gas content. Mining some of these

deposits for coal to gas or coal to liquids projects is currently being evaluated.

Eromanga Basin: AGL explored for CSG in PELs 101 and 103 on the Innamincka

Dome in joint venture with Acer Petroleum. Three cored drillholes evaluated the

coals in the Early Cretaceous Winton Formation. A gas kick was recorded on the

mudlog through Winton Formation coals in the Aspen 1 exploration well.

Ord Minnett Research 7 March 2014 Page 34

Company Review

Strike Energy Limited

Major coal basins of South Australia

Source: South Australian Government, DMITRE Petroleum website, accessed 3

rd October 2013

Ord Minnett Research 7 March 2014 Page 35

Company Review

Strike Energy Limited

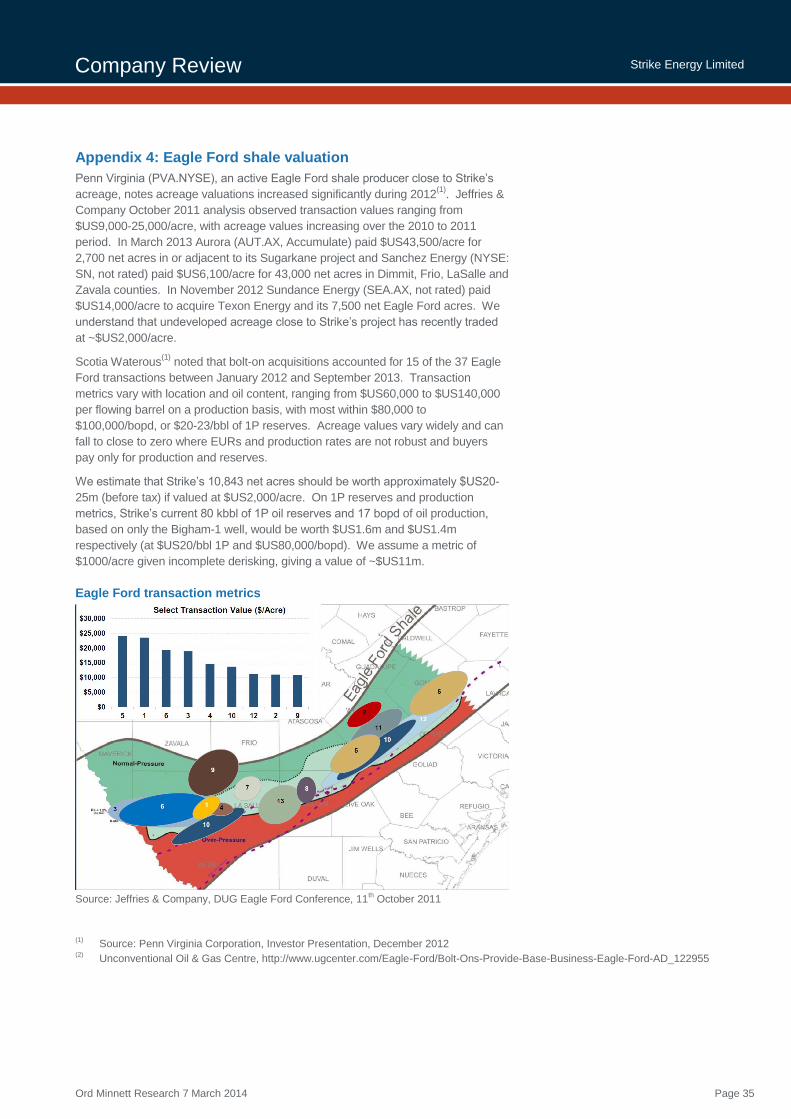

Appendix 4: Eagle Ford shale valuation

Penn Virginia (PVA.NYSE), an active Eagle Ford shale producer close to Strike’s

acreage, notes acreage valuations increased significantly during 2012(1)

. Jeffries &

Company October 2011 analysis observed transaction values ranging from

$US9,000-25,000/acre, with acreage values increasing over the 2010 to 2011

period. In March 2013 Aurora (AUT.AX, Accumulate) paid $US43,500/acre for

2,700 net acres in or adjacent to its Sugarkane project and Sanchez Energy (NYSE:

SN, not rated) paid $US6,100/acre for 43,000 net acres in Dimmit, Frio, LaSalle and

Zavala counties. In November 2012 Sundance Energy (SEA.AX, not rated) paid

$US14,000/acre to acquire Texon Energy and its 7,500 net Eagle Ford acres. We

understand that undeveloped acreage close to Strike’s project has recently traded

at ~$US2,000/acre.

Scotia Waterous(1)

noted that bolt-on acquisitions accounted for 15 of the 37 Eagle

Ford transactions between January 2012 and September 2013. Transaction

metrics vary with location and oil content, ranging from $US60,000 to $US140,000

per flowing barrel on a production basis, with most within $80,000 to

$100,000/bopd, or $20-23/bbl of 1P reserves. Acreage values vary widely and can

fall to close to zero where EURs and production rates are not robust and buyers

pay only for production and reserves.

We estimate that Strike’s 10,843 net acres should be worth approximately $US20-

25m (before tax) if valued at $US2,000/acre. On 1P reserves and production

metrics, Strike’s current 80 kbbl of 1P oil reserves and 17 bopd of oil production,

based on only the Bigham-1 well, would be worth $US1.6m and $US1.4m

respectively (at $US20/bbl 1P and $US80,000/bopd). We assume a metric of

$1000/acre given incomplete derisking, giving a value of ~$US11m.

Eagle Ford transaction metrics

Source: Jeffries & Company, DUG Eagle Ford Conference, 11

th October 2011

(1)

Source: Penn Virginia Corporation, Investor Presentation, December 2012 (2)

Unconventional Oil & Gas Centre, http://www.ugcenter.com/Eagle-Ford/Bolt-Ons-Provide-Base-Business-Eagle-Ford-AD_122955

Ord Minnett Research 7 March 2014 Page 36

Company Review

Strike Energy Limited

Eagle Ford shale project data

Penn Virginia (PVA.NYSE) analysis indicates attractive development economics,

with break-even oil pricing (at a 10% discount rate before tax) of $US50-57/bbl.

Eagle Ford project characteristics and rates of return

Source: Penn Virginia Corporation, Investor Presentation, December 2012

Ord Minnett Research 7 March 2014 Page 37

Company Review

Strike Energy Limited

Please contact your Ord Minnett Adviser for further information on our document.

Research

Tim Smart Head of Research Sydney [email protected]

David Brennan, CFA Senior Resource Analyst Sydney [email protected]

Paresh Patel Senior Research Analyst Sydney [email protected]

John Young Senior Research Analyst Melbourne [email protected]

Brad Dunn Analyst Sydney [email protected]

Nicholas McGarrigle Analyst Sydney [email protected]

Ord Minnett Offices Adelaide Level 11 13 Grenfell Street Adelaide SA 5000 Tel: (08) 8203 2500 Fax: (08) 8203 2525

Brisbane Level 31 10 Eagle St Brisbane QLD 4000 Tel: (07) 3214 5555 Fax: (07) 3214 5550

Buderim Sunshine Coast 1/99 Burnett Street Buderim QLD 4556 Tel: (07) 5430 4444 Fax: (07) 5430 4400

Caloundra, Sunshine Coast 79-81 Bulcock Street Caloundra QLD 4551 Tel: (07) 5491 3100 Fax: (07) 5491 3222

Canberra 101 Northbourne Avenue Canberra ACT 2600 Tel: (02) 6206 1700 Fax: (02) 6206 1720