Communication

impacting financial

markets

SYstemic Risk TOmography: Signals, Measurements, Transmission Channels, and Policy Interventions

Jørgen Vitting Andersen, Ioannis Vrontos, Petros Dellaportas and Serge Galam

CFE 2013, London – 14-16 December 2013

CFE 2013, London – December, 14 2013

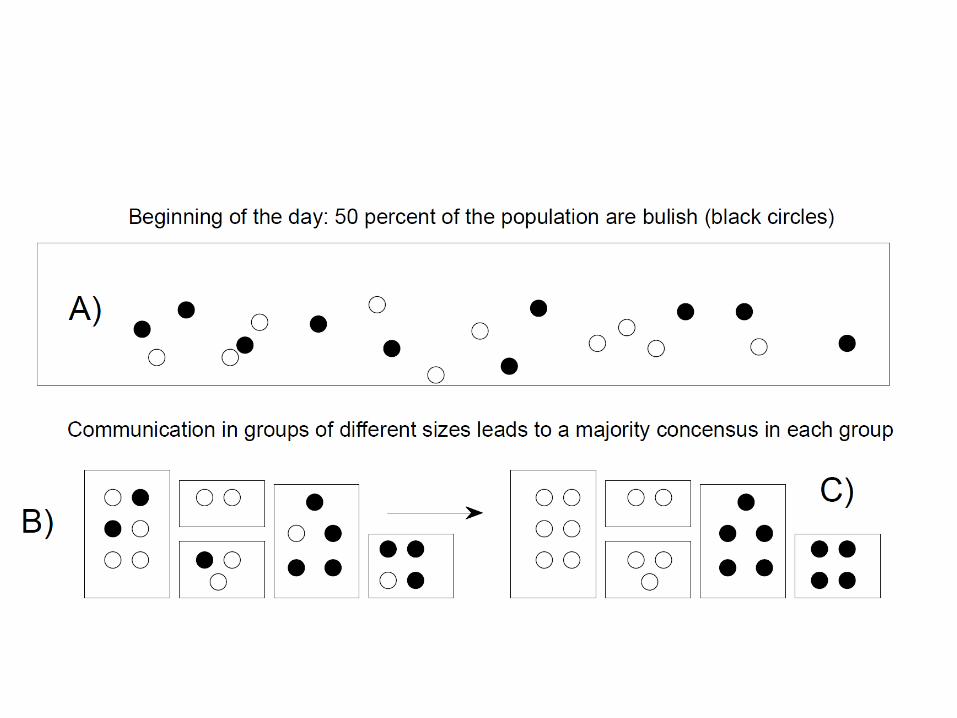

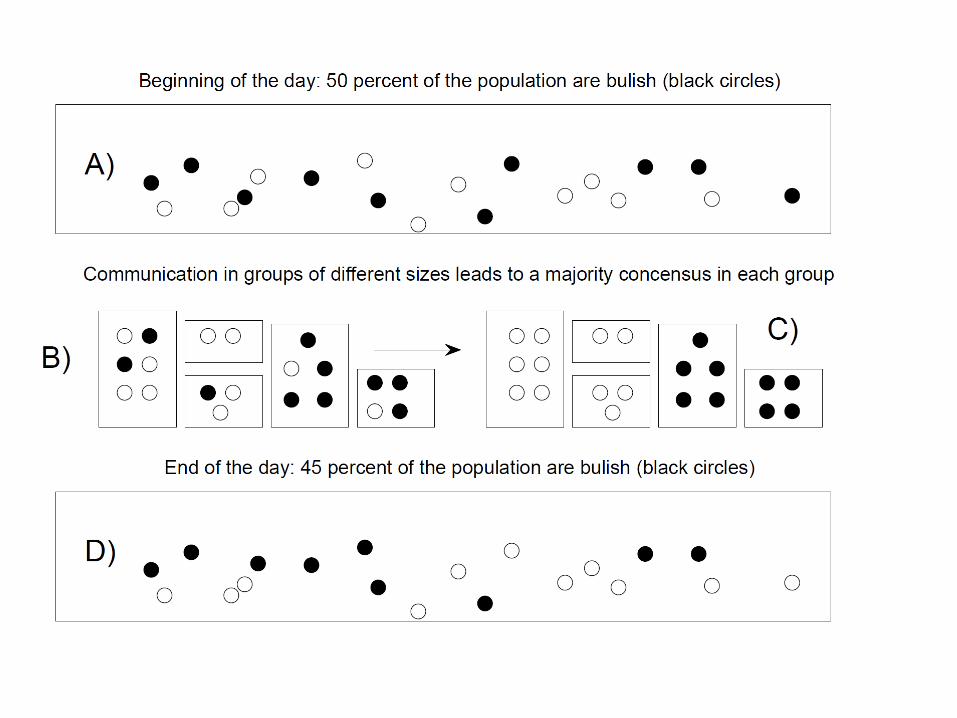

Changing the « bullishness » in a population via communication in subgroups

During the day communication takes place in random subgroups

During the day communication takes place in random subgroups

During the day communication takes place in random subgroups

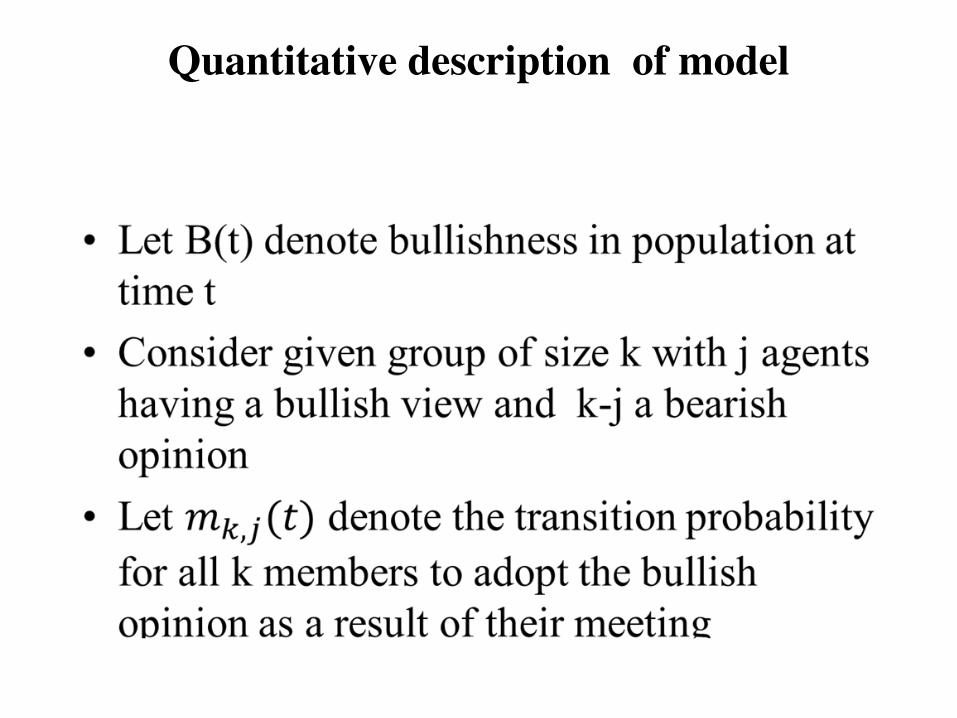

Quantitative description of model

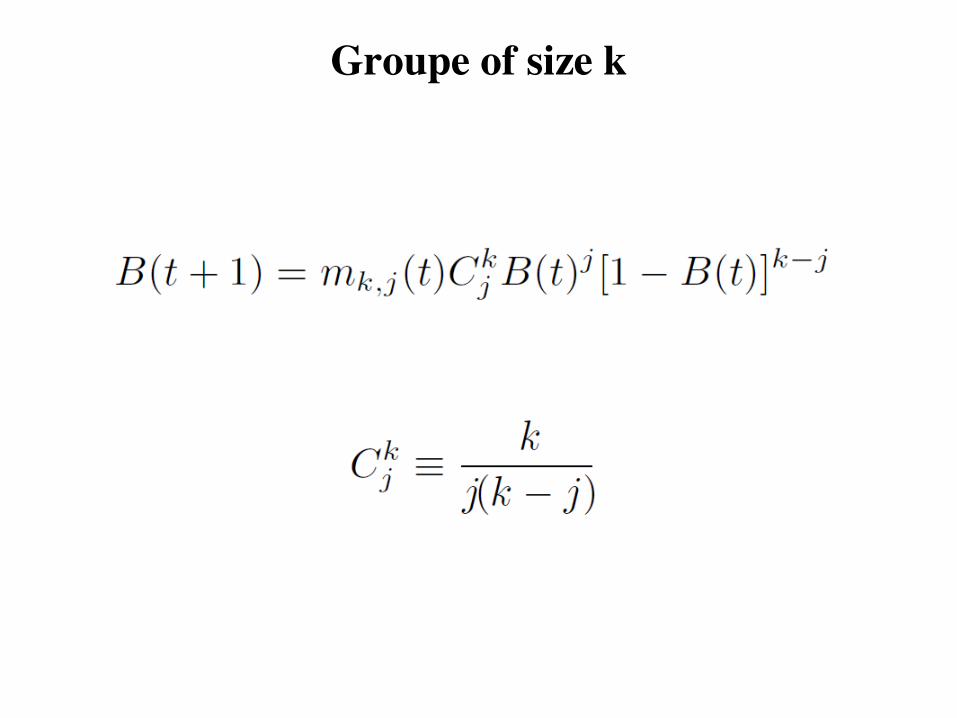

Groupe of size k

Groupes of different sizes

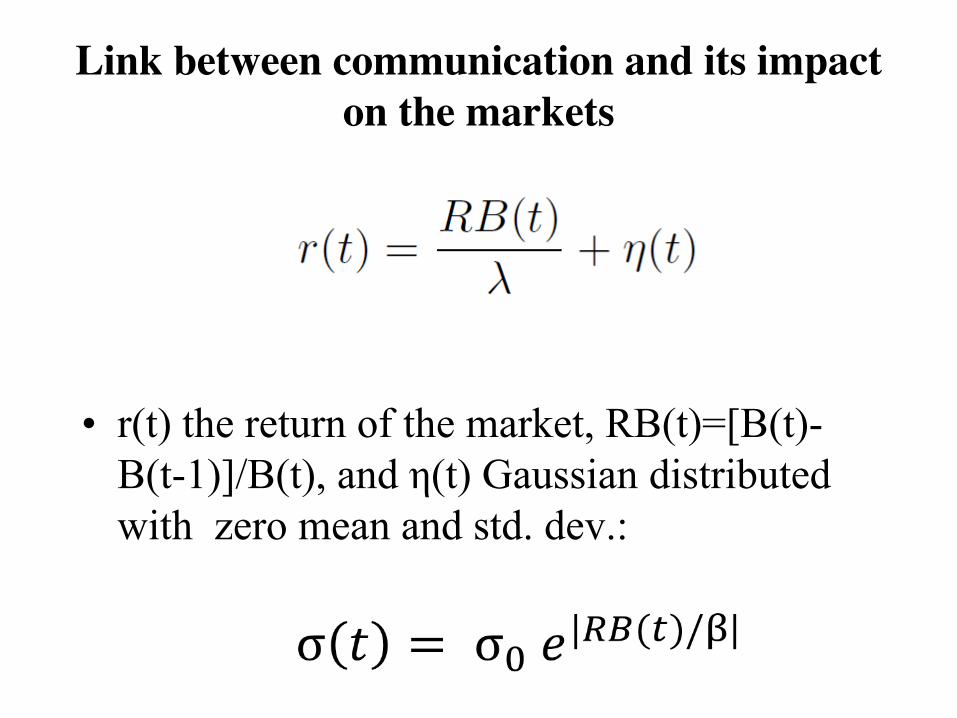

Link between communication and its impact on the markets

• r(t) the return of the market, RB(t)=[B(t)-B(t-1)]/B(t), and η(t) Gaussian distributed with zero mean and std. dev.:

Link between transition probabilities and the market performance

Main results: reproducing stylized facts

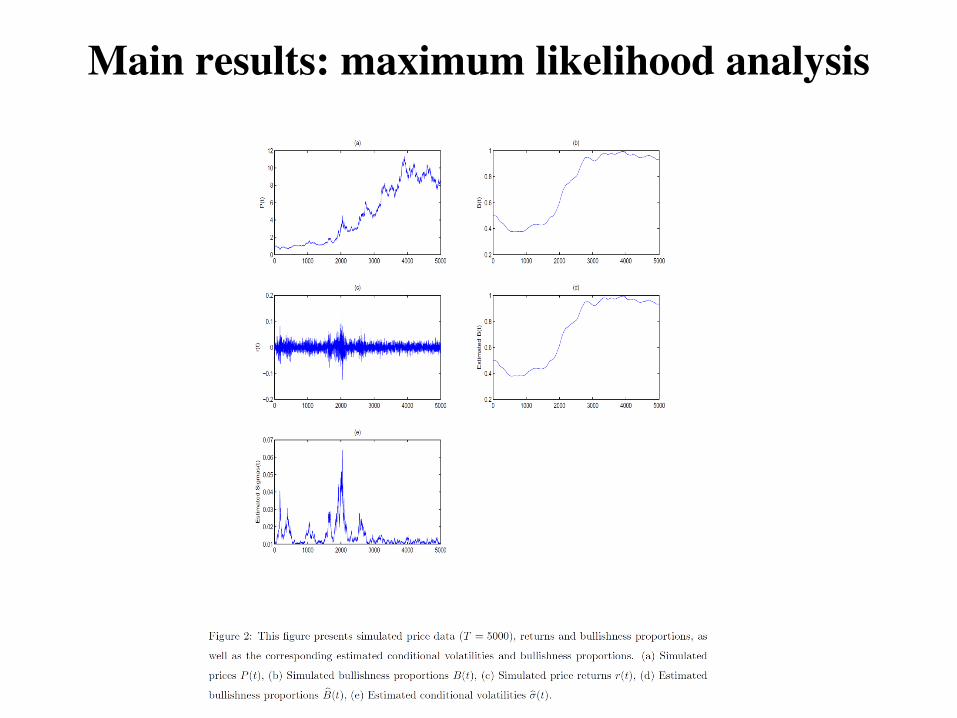

Main results: maximum likelihood analysis

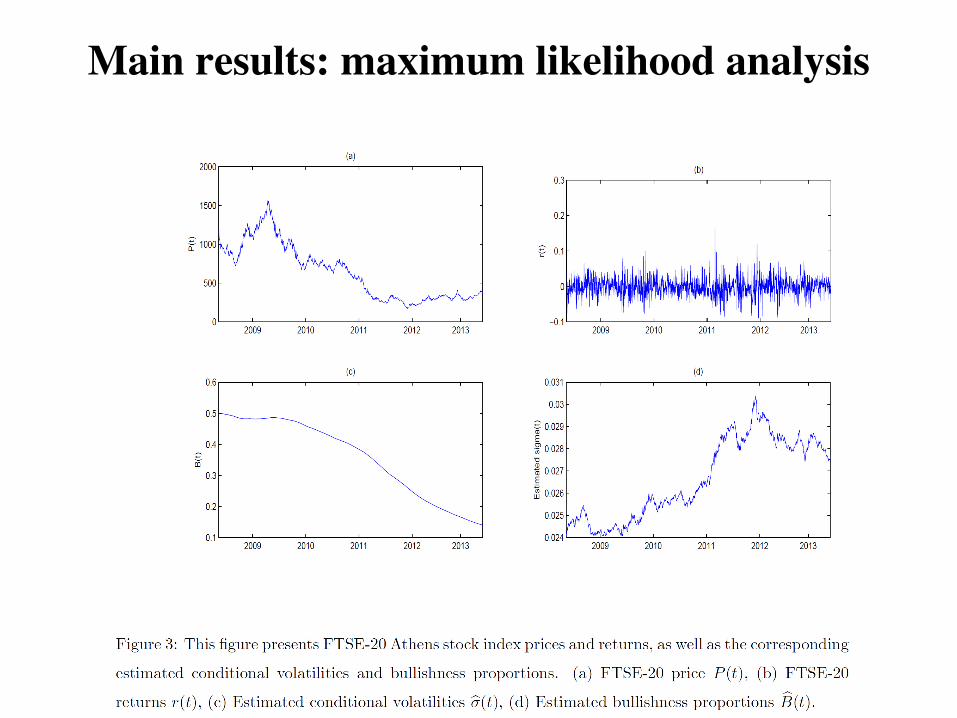

Main results: maximum likelihood analysis

This project has received funding from the European Union’s Seventh Framework Programme for research, technological

development and demonstration under grant agreement n° 320270

www.syrtoproject.eu