1

CommonThreadFootwear:BostonEntryStrategybyMollyDouglas,ArslanMuradi,MahmoudJabari,BhavikShah,andPeterSacco

PeterandLee,theco-foundersofCommonThreadFootwearsitdeepinconversationinthefarcornerofaSomervillecafé.Overcupsofcoffee,theyrevisittheircorebusinessphilosophyofdoingwellbydoinggood.TheirideatolaunchasocialenterprisethatwouldconnectartisanalshoemakersinruralGuatemalawiththeBostonmarkethadprogressedsubstantiallysinceitsconceptionsixmonthsearlierinOctoberof2015.ThepairhadtraveledtoGuatemalatoconfirmproductquality,mappedtheirorganizationalstructure,andhonedinontargetdemographicswithintheBostonmarket.NowinAprilof2016,theyfaceastrategicdecisionwithpotentialtomakeorbreakthecompany’sfuture:howtosuccessfullyenterBoston’sfashionfootwearmarket. PeterandLeegrapplewiththreepotentialmarketentrymodels:(1)partneringwithathirdpartyretailer,(2)establishingabrickandmortarstore,and(3)takingtheirproducttothestreetsinashoetruck.Eachoptionwouldbecomplementedbyaretailwebsite. Theduodiscussestheirlimitedcapitalavailableforhighfront-endinvestmentsandthevalueofpartnershipandsecuringconsistentsales.Theyfeelpressuretomakea“splash”inthelocalfootwearmarketwithaninnovativeentrystrategythatwouldreflecttheuniquenessoftheirproductandappealtotheirtargetcustomers. ThedisappearingsunsetstheurbanskylinealightasLeeapproachesthebarforherfourthcupofcoffee.Itwillbealongnightahead. TheProduct

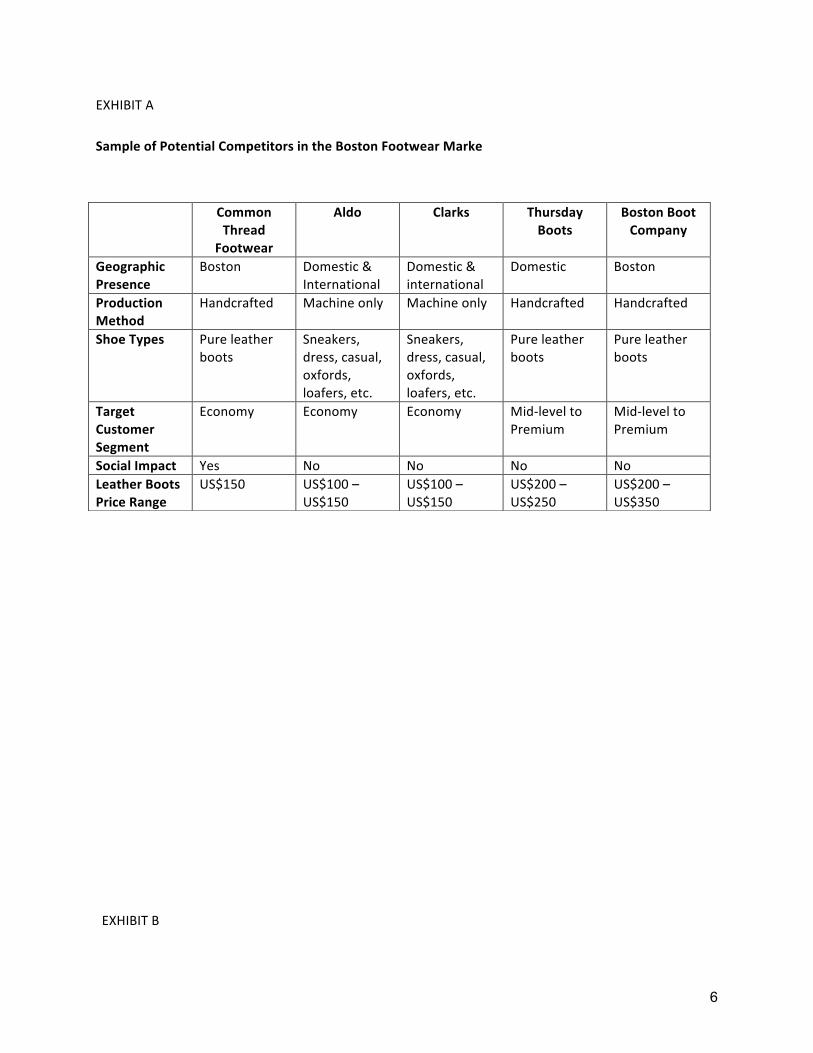

CTFshoes,boots,andsandalsaremadeformenandwomenwithclassicstyle.CTFproductsarehandcrafted,meaningthatnothingmoreindustrialthanasewingmachineisusedinproduction.Allfootwearismadefrom100%full-grainandtop-grainleather.SeveralcobblersintheBostonareabetweenUS$200andUS$300haveappraisedCTFproducts. UniqueValueProposition CTFcombinesquality,fashion,andaffordabilitywithmeaningfulsocialimpact,makingiteasyfortheconsumertochooseshoesthatmaketheworldabetterplace. TheMarket ThegreaterBostonareaisafashionfootwearhub.Reebok,NewBalance,andConversearejustafewoftheindustrygiantsthatcallthiscityhome.PeterandLeedecidedtoentertheBostonmarketafterdeterminingthatnopre-existingcompanyofferedacomparablyholisticuniquevalueproposition.

2

CTF’sgreatestcompetitorswithintheBostonmarketareAldo,Clarks,ThursdayBootsandBostonBootCompany.EachofthesecompaniesincorporatesapartofCTF’suniquevalueproposition,butnoonecompanyoffersthefullpackage.PleasecheckExhibitA. PeterandLeebelievethattheircombinationofquality,affordability,fashion,andsocialimpactsetthemapartfromtheircompetitors.Specifically,CTFproductsarehandmadefromhigherqualitymaterialsthancompetingbrands,andarefarcheaperthanmanycompetingproductsofcomparablequality.PeterandLeesourceproductdesignsdirectlyfromtheirtargetcustomers,ensuringthattheirfootwearremainsontheforefrontofevolvingconsumerpreferences. Finally,theduointendstomarkettheirsocialimpactmissionwithon-producttagsthatrelaythepersonalstoriesofGuatemalancraftsmenanddemonstratecompletefinancialtransparency.“Peopleworkhardfortheirmoney,”saidPeter.“Theyshouldknowitisn’tjustdisappearingintothebackholeoftheworldeconomy.”ThepairdoesnotassumethatcustomerswillchooseCTFproductsonsocialimpactalone,buttheydoexpecttheirdemonstratedbenevolencetoswaycustomersinachoicebetweenaCTFshoeandcomparableproduct. TheCustomer PeterandLeeconvenedtheirfirstfocusgroupontargetdemographicsinMarchatPeter’sgraduateschool,theFletcherSchoolofLawandDiplomacy. PeterandLeereasonedthatPeter’sfellowstudentscouldconstituteonesegmentofCommonThreadFootwear’stargetdemographic,so,overpizzaandatableofshoesamples,twelvegraduatestudentsexaminedanarrayofmen’sandwomen’sleathershoes.Theyreachedconsensusonfourwordsthatdescribedtheproductline:“handmade”,“modernclassic”,“distinctive”,and“character”.Theyalsodiscussedwhatqualitiestheyvaluedmostinanewpairofshoes,andwhataspectsoftheproductlinerequiredadjustmenttomeettheirrequirementsforpurchase. Thefocusgroupconcludedthattheymostvalueddurability,attentiontodetail,andcomfortinanewpairofshoes,and,whiletheyappreciatedtheaestheticandqualityoftheCTFline,theywouldbemorelikelytopurchasetheshoeswiththeadditionofcomfortable,foot-conforminginsoles,linings,andgripoutsoles.PeterandLeeindicatedthattheseadjustmentscouldbemade. WithrespecttoCommonThreadFootwear’svaluepropositionofcombiningqualityandaffordabilitywithmeaningfulsocialimpact,thefocusgroupcommunicatedthatsocialresponsibilitywasnotaprimarysellingpoint.Theydidreason,however,thatsocialimpactmayconstitute“theicingonthecake”thatwoulddifferentiateonecomparablypriced,qualityleathershoefromanother. ThefocusgroupsketchedoutPeterandLee’stargetdemographic,concludingthatthelikeliestcustomersofCTFshoesintheBostonareaareyoung,urbanprofessionalsbetweentheagesof25and39whovaluefashion,arecultivatingdistinctivepersonalstyle,andarewillingtoinvestinshoeswitha

3

“classic,internationaledge”aesthetic.Thesepotentialconsumersaresomewhatsociallyconsciousandwouldappreciatethe“socialimpactinacolorful,far-awayland”elementoftheirCTFshoes.Aftermuchheateddebate,thefocusgroupalsoconcludedthatthesepotentialconsumerswouldbewillingtopayapproximatelyUS$150forapairofCTFshoes. Reflectingontheoutcomeofthefocusgroupsession,Peterfelttheassembledstudentshadfailedtoidentifyasecondlikelyconsumerprofile.Hedescribedthissecondconsumergroupasuppermiddle-class,socially-conscious,classically-styledprofessionalsbetweentheagesof40and59whowanttofeelgoodaboutmakingsociallyresponsiblepurchasesandsignalingtheirresponsibilitytotheirpeersthroughtheirdress. TheEntryModels Model1:ThirdPartyRetailer OnemarketentryoptionthatPeterandLeecontemplatedwasapartnershipwithoneormorethird-partyretailers.ClothingboutiquesarecommonthroughoutthegreaterBostonareaandofferthepotentialbenefitofnegotiatingprice,payment,andinventoryspecificswithstoreowners.Large,corporateretailersarealsoubiquitous,butmorerigidintheircontractrequirementsandmoredifficulttobreakinto.

PeterandLeeweretemptedtopartnerwithoneormorethirdpartyretailersbecausetheybelievedthat:(1)establishedretailerscommandadegreeoflegitimacyandcustomerloyaltythatthenascentCommonThreadFootwearbranddidnot,and(2)consumersprefertocomparesimilarproductsinpersonbeforemakingapurchase.Thisoptionwasalsoattractivebecauseitwouldobviatetheneedforin-storeemployeesandincreasethelikelihoodofconsistentmonth-over-monthsales.

However,pursuingpartnershipwithanynumberofboutiqueorcorporateretailerswouldsignificantlyimpactthecoststructureofCommonThreadFootwearproducts.Asageneralrule,thirdpartyretailersmarkupfootwear100%fromwholesalepurchaseprice.Althoughboutiqueshopsmaybemoreflexiblethancorporateretailerswithrespecttomarkuppercentiles,itwasunlikelythatanyboutiquewouldmarkupCommonThreadFootwearshoestoanythinglessthan80%ofwholesalevalue. IfPeterandLeewantedtheirshoestoretailforUS$150inthird-partystores,theywouldneedtowholesaletheirshoesfornomorethanUS$75.Atthispricepoint,PeterandLeewouldbehardpressedtomakeaprofit.ThepaircouldcompensateforlowprofitmarginsbyincreasingtheirwholesalepricefromUS$75toUS$100,whichwouldinturnincreaseretailpricestoUS$200.However,affordabilitywasakeyfactorintheCTFvalueproposition,andPeterandLeefearedthatretailpricesaboveUS$150couldcompromisetheircomparativeadvantage.Moreover,theduowaswaryofpartneringwithunreliablestoreownersorcedingagencyintheproductdisplayprocess.

4

Model2:BrickandMortar PeterandLeealsoconsideredestablishingabrick-and-mortarretailerinoneofDowntownBoston’strendyshoppinghubs,suchasNewburyStreet.Thepairbelievedthatabrickandmortarlocationwouldhelplegitimizeandformalizethebusinessfromaconsumerperspective.TheyassumedthataphysicalpresencewouldstrengthentheCommonThreadFootwearbrandandfosterbrandloyaltywithinBoston. Abrick-and-mortarlocationwouldexclusivelysellCommonThreadFootwearshoesandwouldabrogatetheproblemsassociatedwiththird-partymarkups.TheabilitytoselltheirshoesdirectlytoconsumerswouldmeanthatPeterandLeecouldmaintainflexibilityintheircoststructureandprofitmarginswithoutcompromisingtheirvalueproposition.AutonomyoverthemarketingprocesslikewiseappealedtoPeterandLee,whoguessedthatproductdisplayandcreativepromotionswouldyieldsignificantreturns. TheaveragemonthlyrentforaretailspaceintheBostonisUS$4,000/month,excludingutilities.Theoperationandmanagementofabrick-and-mortarstorewouldrequirePeterandLeetohireatleasttwosalespeopleonanear-full-timebasis.Thesecostsalonesignaledthatthisoptionwouldinvolvesubstantialstartupandfixedcosts.Moreover,PeterandLeewerewaryofinvestingsignificantcapitalinaphysicallocation.Whatifthetermsoftheleasechanged?Whatiftheypickedthewrongblockonwhichtoopentheirstore? Model3:ShoeTruck Ultimately,PeterandLeefeltmostexcitedabouttheprospectoflaunchingamobileshoetruck.ThroughoutBoston,longlunchtimelinesonurbansidewalkshadbecomeubiquitouswiththeemergenceoffoodtrucks.PeterandLeeconsideredcapitalizingonthetrendtowardalternativeretailstrategieswiththelaunchofamobileshoetruck. Muchlikeafoodtruckorbookmobile,thistruckwouldserveasaretailshoestorethatcouldeasilymovefromblocktoblock,neighborhoodtoneighborhood,universitycampustouniversitycampus.Inadditiontomobileretailservices,thisoptionwouldoffershoerepairandpolishservices.PeterandLeefiguredthattheMobileTruckIndustryhadprovenitsworthwithrevenuesofUS$1.2Billionin2015alone,andthereseemedtobeanincreasingdesireforinnovativeretailingmodels. PeterandLeewereattractedtotheshoetruckretailmodelforfiveprinciplereasons.First,themobilityoftheshoetruckwouldallowthepairtotargetspecificdemographicsandgroupsinspecificplacesatspecifictimes.Second,thetruckcouldreachcustomerswhomightnototherwisehaveaccesstoatraditionalshoestores.Third,PeterandLeeguessedthattheirtrendy,sociallyconsciouscustomerswouldbedrawntoaninnovativemarketingmodel—especiallywhenparkedatcollegehomecomings,musicfestivals,andfarmer’smarketsintheGreaterBostonarea.Fourth,thetruckcouldserveasadynamicmarketingplatformfromwhichtoredirectcustomersgivenon-the-spotpromotionsand

5

discountstotheCTFwebsite.Finally,thetruckcouldoperatewithrelativelylowoverheadcostsandobviateabrickandmortarrental. However,purchasingandrefurbishingaboxtruckforretailoperationwouldbecostly.AusedtruckwouldcostroughlyUS$5,000upfront,andoperations,retrofits,andparkingpermitscouldaddupquickly.PeterandLeeenvisionedconvertingthetruckintoacomfortable,“boutique-styleenvironment,"completewithexteriordetailing,speakers,interiorshelves,andagrillandbenchesforoutdoorevents.Whiledoubtlesslyinspiring,thepairwonderedifoperatingashoetruckwasrealistic. UniversalCosts PeterandLeeplannedtooperateapowerfulretailwebsiteregardlessofwhichmarketentrymodeltheychosetopursue.Thecostsoflaunchingandmaintainingawebsitewouldincludeaone-timewebsitedesignfeeofUS$3,000,followedbyanannualwebsitehostfeeofUS$300. CommonThreadFootwearmayalsoneedtocontractwithawarehouseandlogisticsfirmforstorage,handling,andshippingpurposes.Inatleasttheirfirstyearofbusiness,however,PeterandLeeanticipatethatPeter’smomandherbasementwillfunctionasthewarehouseandlogisticsfirm.Beyondthefirstyearofoperation,estimatedcostofstorageandhandlingfor200shoes/monthcouldbeUS$12,000annually,excludingGuatemala-to-Bostonshipping.Theannualcostofcontractingwithalogisticfirmwouldvaryinaccordancewithstoragespacevolumeandordersize,butmaynotbenecessaryuntilCTFhasscaleditsoperationsinthecomingyears.Finally,PeterandLeeplannedtohireapart-timemarketingassistantregardlessofmarketentrymodel. LookingForward Withtheirsummerlaunchdeadlinequicklyapproaching,PeterandLeefeelhardpressedtodeterminetheirmosteffectivemarketentrystrategy.Howmighttheybestaddextra-ordinarynewvalueinextra-ordinarynewwaystotheBostonfootwearmarketandindustryatlarge?Thepairbelievedeeplyintheirmissionandvalues,buttheycan’tshakethenaggingsuspicionthatthisistheironeandonlyshotatasuccessfullaunch. TherisingsunsetstheurbanskylinealightasLeeapproachesthebarforherninthcupofcoffee.Itisnowornever.

6

EXHIBITASampleofPotentialCompetitorsintheBostonFootwearMarke

EXHIBITB

CommonThread

Footwear

Aldo Clarks ThursdayBoots

BostonBootCompany

GeographicPresence

Boston Domestic&International

Domestic&international

Domestic Boston

ProductionMethod

Handcrafted Machineonly Machineonly Handcrafted Handcrafted

ShoeTypes Pureleatherboots

Sneakers,dress,casual,oxfords,loafers,etc.

Sneakers,dress,casual,oxfords,loafers,etc.

Pureleatherboots

Pureleatherboots

TargetCustomerSegment

Economy Economy Economy Mid-leveltoPremium

Mid-leveltoPremium

SocialImpact Yes No No No NoLeatherBootsPriceRange

US$150 US$100–US$150

US$100–US$150

US$200–US$250

US$200–US$350

7

ProjectedStart-UpExpensesinYearOnebyEntryModel,inUSD

Model1:ThirdPartyRetailer

ProjectedStart-UpExpenses

Oneyearofmarketingemployeesalary $5,000.00

One-timewebsitedesigncontract $3,000.00

Annualwebsitefee $300.00

TOTAL $8,300.00

Model2:BrickandMortar

ProjectedStart-UpExpenses

Oneyearofrent $48,000.00

Oneyearoftwopart-timeretailemployeessalary $60,000.00

Oneyearofmarketingemployeesalary $5,000.00

One-timewebsitedesigncontract $3,000.00

Annualwebsitefee $300.00

TOTAL $116,300.00

Model3:ShoeTruck

ProjectedStart-UpExpenses

Truckpurchase $5,000.00

Truckrenovation $3,000.00

Oneyearofgas $1,100.00

Oneyearoftruckmaintenance $900.00

Annualcitypermit $500.00

Oneyearofmarketingemployeesalary $5,000.00

One-timewebsitedesigncontract $3,000.00

Annualwebsitefee $300.00

TOTAL $18,800.00

EXHIBITC

8

TargetDemographicFocusGroup-GeneratedConsumerProfile Peter-GeneratedConsumerProfile

• Youngurbanprofessionals• 25—39yearsold• Whitecollarjob• Valuesfashion• Classicstylewithinternationaledge• Pursuingadistinctivelook• Somewhatsociallyconscious• Identifieswithadistinctivestory/purchase

• MiddleagedmenandWomen• 40—59yearsold• Whitecollarjob• Classicstyle• Sociallyconscious• Wantstofeelgoodaboutmakinga

responsiblepurchaseand/orwantstosignalsocialresponsibilitytopeerswithpurchase

Source:FocusgroupheldatTheFletcherSchoolonMarch14,2016byPeterSaccoandLeeStroman.

EXHIBITDU.S.CensusBureau2014PopulationEstimatesforBoston-Cambridge-Newton,MA-NHMetroArea

Totalpopulation:4,650,876Age Total

25–29 7.5%/348,81630–34 6.7%/311,60935–39 6.2%/288,35440–44 7.0%/325,56145–49 7.5%/348,81650–54 7.6%/353,46755–59 6.8%/316,260

Source:U.S.CensusBureau.AmericanFactFinder:2010-2014AmericanCommunitySurvey5-YearEstimates.http://factfinder.census.gov/faces/tableservices/jsf/pages/productview.xhtml?pid=ACS_14_5YR_S0101&prodType=table.

EXHIBITE

9

Source:BureauofLaborStatistics.NewEnglandInformationOffice:ConsumerExpendituresfortheBostonMetropolitanArea,2013-14.http://www.bls.gov/regions/new-england/news-release/consumerexpenditures_boston.htm

EXHIBITF

10

Source:Rocheleau,Matt.“Howrich(ornot)isyourcommunity?:Atown-by-townlookatincomeinMassachussetts.”BostonGlobe.18December2015.https://www.bostonglobe.com/metro/2015/12/18/town-town-look-income-massachusetts/cFBfhWvbzEDp5tWUSfIBVJ/story.html

EXHIBITG

11

ExcerptsfromCollectedArticlesontheShoppingHabitsofToday’sConsumersFORBES“8ShoppingHabitsofMillennialsAllRetailersNeedtoKnowAbout”byPeterGascaDecember7,2015

1. SmartphonesareaprimarymeanstoconnecttotheInternet.2. Socialmediaisnumberoneforshoppinginformation.3. Millennialsaresensitivetoprice.4. GoogleandAmazonarefavoritesforcomparingpricesonsmartphones.5. Millennialspreferhigher-valuerebatesoverinstantdiscountsacrossshoppingcategories.6. Millennialswillconsider"BuyOnline,PickupInStore"asanincentive.7. Giftcardsarebelievedtobesafestforonlineshopping.8. Millennialsembraceloyaltyprograms.

Source:https://www.entrepreneur.com/article/253582

FORTUNE“Millennials:They’reJustLikeUs?”byAnneVanderMeySeptember28,2015Boomersv.Millennials

1. In1985,theyearafter“MaterialGirl”cameout,youngpeople’sspendingrepresentedabout101%oftheiraverageearnings—closetothenationalaverageof103%.

2. Youngadultsarestillspendingtoday,ifnotwithMadonna-styleexcess.Theirtotalaverageexpendituresmakeup91%ofearnings—aboutonparwiththenationalaverageof92%.

3. In1985,boomersspent6%lessthantheaverageAmericanonapparel.4. Millennials,ever“onfleek,”spent7%morethantheaverageAmericanonapparellastyear.5. Youngadultsspent$129onreadingmaterialsonaveragein1985,9%lessthaneveryoneelse.6. Lastyearyoungadultsspent$75onreadingmaterialsonaverage,27%lessthaneveryoneelse.7. Theboomersin1985put9%oftheirtotalspendingtowardcars.8. Millennialstodayput7%oftheirtotalspendingtowardcars.Thankstotheirsheernumber,

though,GenYnowmakesupalargermarketthanGenX.9. Youngadultsin1985spent58%morethantheaverageAmericanonrent.10. Youngadultslastyearspent69%morethantheaverageAmericanonrent.Manyofthem

(especiallythewelleducated)prefercities—thoughexpertsseepent-updemandforsingle-familyhomes.

Source:http://fortune.com/2015/09/28/millennials-boomers-consumer-spending-habits-comparison/

FORBES“10NewFindingsAboutTheMillennialConsumer”byDanSchwabel

12

January20,2015

1. Theyaren’tinfluencedatallbyadvertising.2. Theywouldratherbuyacarandleaseahouse.3. Theyreviewblogsbeforemakingapurchase.4. Theyvalueauthenticityasmoreimportantthancontent5. Theirfutureinheritancewon’tchangetheirbuyingbehavior.6. Theywanttoengagewithbrandsonsocialnetworks.7. Theywanttoco-createproductswithcompanies.8. Theyareusingmultipletechdevices.9. Theyarebrandloyal.

Source:http://www.forbes.com/sites/danschawbel/2015/01/20/10-new-findings-about-the-millennial-consumer/#3aca9d0628a8

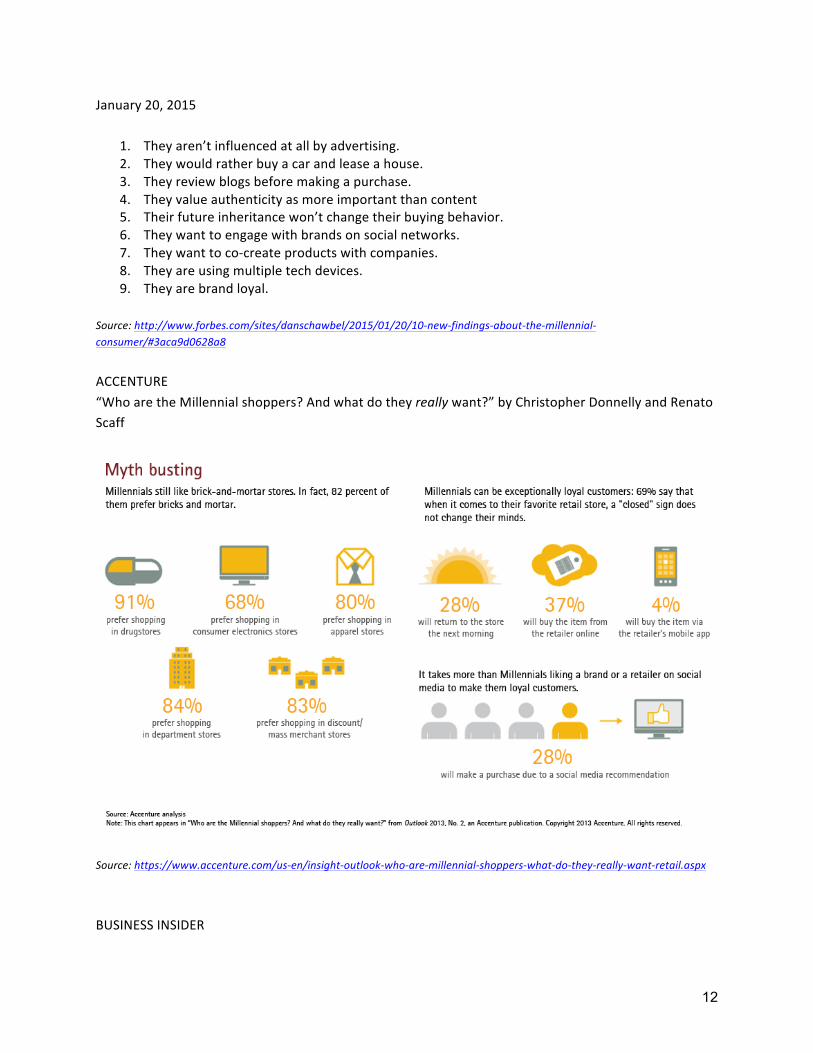

ACCENTURE“WhoaretheMillennialshoppers?Andwhatdotheyreallywant?”byChristopherDonnellyandRenatoScaff

Source:https://www.accenture.com/us-en/insight-outlook-who-are-millennial-shoppers-what-do-they-really-want-retail.aspx

BUSINESSINSIDER

13

“Thesefindingsabouthowmillennialsandbabyboomersshopmaysurpriseyou”sponsoredbySynchronyFinancialApril22,2015Howmillennialsandbabyboomersaresimilar• Coupons:Babyboomersandmillennialssharealoveforcoupons,sales,andbargains.• Onlineshopping:Botharecomfortablewithbrowsing,researching,andshoppingonline.• Femaleshoppersonsocialmedia:Inbothdemographics,womenarefarmorelikelythanmento

talkonsocialmediaaboutwhattheybought.82%offemaleboomersand83%offemalemillennialsaresharingtheirretailexperiencesonplatformslikeTwitter,Facebook,andInstagram.

Howmillennialsandbabyboomersdiffer• Digitaldevices:Whilebothgenerationshavedigitaldevices,millennialsusetheirstomakeshopping

easier,doingresearchontheirsmartphonesandtabletsbeforetheybuy.Boomersarealsotech-savvy,butthey'relesslikelytousetheirdevicesasashoppingtool.

• Word-of-mouthinfluence:82%ofmillennialstendtofavorwordofmouthfromfriends,family,andsocialmediawhenthey'redecidingwhattobuy—comparedtoonly52%ofboomers,whoareinfluencedmostbyretailwebsites,thenbyadvertisingandsalespeople.

• In-storeexperience:Whenthey'reshoppinginstores,boomersplacehighimportanceoncustomerservice(helpfulsalespeople,forexample)injudgingthequalityoftheirexperience.Millennialsalsoenjoycustomerservice,buttheyoftenturntotechnologytoimprovetheirin-storeshopping.

• Pricing:Boomersarelessmotivatedbypricethanmillennials,andthey'reloyaltothestylesandbrandstheylike.Millennialscarealotabouthowmuchthingscost,especiallyincategoriessuchasappliances,specialtyretail,electronics,anddepartmentstores.

Source:http://www.businessinsider.com/sc/how-millennials-and-baby-boomers-shop-2015-4

WorkCited

14

“2015FoodTruckIndustryStatistics.”MobileCuisine.http://mobile-cuisine.com/trends/2015-food-truck-industry-statistics-show-worth-of-1-2b/BureauofLaborStatistics.NewEnglandInformationOffice:ConsumerExpendituresfortheBostonMetropolitanArea,2013-14.http://www.bls.gov/regions/new-england/news-release/consumerexpenditures_boston.htmDonnelly,ChristopherandRenatoScaff.“WhoaretheMillennialshoppers?Andwhatdotheyreallywant?”Accenture.https://www.accenture.com/us-en/insight-outlook-who-are-millennial-shoppers-what-do-they-really-want-retail.aspxFocusgroupheldonMarch14,2016byPeterSaccoandLeeStromanatTheFletcherSchool.Gasca,Peter.“8ShoppingHabitsofMillennialsAllRetailersNeedtoKnowAbout.”Forbes.7December2015.https://www.entrepreneur.com/article/253582InterviewsbetweenFebruaryandApril2016withPeterSacco,Co-founderofCommonThreadFootwear.Personalconversation4April2016withScott,OwnerofSuedoShoesinCambridge,MA.Rocheleau,Matt.“Howrich(ornot)isyourcommunity?:Atown-by-townlookatincomeinMassachussetts.”BostonGlobe.18December2015.https://www.bostonglobe.com/metro/2015/12/18/town-town-look-income-massachusetts/cFBfhWvbzEDp5tWUSfIBVJ/story.htmlSchwabel,Dan.“10NewFindingsAboutTheMillennialConsumer.”Forbes.20January2015.http://www.forbes.com/sites/danschawbel/2015/01/20/10-new-findings-about-the-millennial-consumer/#3aca9d0628a8“Thesefindingsabouthowmillennialsandbabyboomersshopmaysurpriseyou.”BusinessInsider.22April2015.http://www.businessinsider.com/sc/how-millennials-and-baby-boomers-shop-2015-4U.S.CensusBureau.AmericanFactFinder:2010-2014AmericanCommunitySurvey5-YearEstimates.http://factfinder.census.gov/faces/tableservices/jsf/pages/productview.xhtml?pid=ACS_14_5YR_S0101&prodType=table.VanderMey,Anne.“Millennials:They’reJustLikeUs?”Fortune.28September2015.http://fortune.com/2015/09/28/millennials-boomers-consumer-spending-habits-comparison/

15