Chorus Aviation Capital PresentationOctober 26, 2017

Certain information in this presentation may contain ‘forward-looking information’ as defined under applicable Canadian securities legislation.Forward-looking information typically contains words such as “anticipate”, “believe”, “could”, “should”, “estimate”, “expect”, “intend”, “may”,“plan”, “predict”, “project”, “will”, “would”, and similar words and phrases, including references to assumptions. Such information may involve butis not limited to comments with respect to strategies, expectations, planned operations or future actions.

Forward-looking information relates to analyses and other information that are based on forecasts of future results, estimates of amounts not yetdeterminable and other uncertain events. Forward-looking information, by its nature, is based on assumptions, including those described in thispresentation, and is subject to important risks and uncertainties. Any forecasts or forward-looking predictions or statements cannot be reliedupon due to, amongst other things, external events, changing market conditions and general uncertainties of the business. Such statementsinvolve known and unknown risks, uncertainties and other factors that may cause the actual results, performance or achievements to differmaterially from those expressed in forward-looking statements. Factors that may cause results to differ materially from expectations in thispresentation include, without limitation: risks relating to Chorus’ economic dependence on and relationship with Air Canada; risks relating to theairline industry (including the international operation of aircraft in developing countries and areas of unrest); aircraft leasing (including thefinancial condition of lessees, availability of aircraft, access to capital, fluctuations in aircraft market values, competition and political risks);energy prices, general industry, market, credit, and economic conditions (including a severe and prolonged economic downturn which couldresult in reduced payments under the Capacity Purchase Agreement (‘CPA’) with Air Canada); competition affecting Chorus and/or Air Canada;insurance issues and costs; supply issues and costs; the risk of war, terrorist attacks, aircraft incidents and accidents; epidemic diseases,environmental factors or acts of God; changes in demand due to the seasonal nature of Chorus’ business or general economic conditions; theability of Chorus to reduce operating costs and employee counts; the ability of Chorus to secure financing; the ability of Chorus to attract andretain the talent required for its existing operations and future growth; the ability of Chorus to remain in good standing under and to renewand/or replace the CPA and other important contracts; employee relations, labour negotiations or disputes; pension issues, currency exchangeand interest rates; leverage and restrictive covenants contained in debt facilities; uncertainty of dividend payments; managing growth; changesin laws, adverse regulatory developments or proceedings in countries in which Chorus and its subsidiaries operate or will operate; pending andfuture litigation and actions by third parties. For a further discussion of risks, please refer to Chorus’ most recent MD&A and to the AnnualInformation Form dated February 15, 2017. The statements containing forward-looking information in this presentation represent Chorus’expectations as of October 12, 2017, and are subject to change after such date. However, Chorus disclaims any intention or obligation toupdate or revise any forward-looking information whether as a result of new information, future events or otherwise, except as required underapplicable securities laws.

Page 2

Caution Regarding Forward-Looking Information

Page 3

Chorus at a Glance

TSX: CHRTicker symbol

Monthly dividend of$0.04 per share

~ $248 millionAdjusted EBITDA, excluding other items -2016

~ $1.3 billionOperating revenue -2016

Focused on building additional shareholder value

+104%Three year share price performance(2)

~ $1.1 billionMarket capitalization(1)

Consistently profitablesince becoming publicly traded in 2006

(1) Calculated using closing price of Chorus shares of $8.59 on the TSX on October 4, 2017.(2) Between October 4, 2014 and October 4, 2017.

• Focused on providing a full suite of regional airline services

Page 4

Chorus Lines of Business

Contracted flying operations

Maintenance, repairand overhaul (MRO)

Regionalaircraft leasing

Operated by

Focus area of growth and revenue diversification

1 2 3

Page 5

Overview of Contracted Flying Operations1

• Jazz is responsible for providing crews, airframe maintenance, flight operations, some airport operations, and general administration

• Scope operation

• ~700 daily flights

• 73 destinations in North America

• Fleet of 117 aircraft

• Three types of missions

• Smaller markets with less demand

• High density markets at off-peak times

• Point-to-point services on lower density routes

• Jazz is Air Canada’s primary regional supplier, providing ~70% of their regional capacity

Voyageur provides specialized contracted flying and aviation services

• Contract flying services

• Missions

• Flight operations

Fleet of 18 owned aircraft (16 Bombardier manufactured)

Flying ACMI missions around the world for over 12 years

Blue-chip customers such as the United Nations

Contracted services done with Canadian licenses, certifications, and designations

Air Canada Express – Operated by Jazz Voyageur

World-renowned reputation for superior safety standards and operational integrity.

Page 6

Overview of MRO Operations

Separate division under Jazz Stand alone profit centre Focused on traditional heavy

maintenance on Bombardier aircraft

Established in 2016 Regional aircraft part sales and service

Operating in North Bay, ON 200,000 square foot facility Highly specialized and custom MRO and

engineering, design for domestic & international clients

2

Page 7

Overview of Chorus Aviation Capital3

• Established in January 2017.

• Fairfax Financial invested $200 million in Chorus through a private placement of convertible debt.

• New subsidiary Chorus Aviation Capital (“CAC”) setup to build a global, regional aircraft leasing platform - further advancing Chorus’ growth and diversification strategy.

• Delivers a full suite of support services to customers worldwide by leveraging the expertise within Chorus’ group of companies.

Page 8

Strategic VisionOpportunity

Chorus established, Chorus Aviation Capital(CAC) for the purpose of acquiring, financing,leasing and trading regional aircraft.

Focused exclusively on the 70 to 135 seatcommercial market segment.

Objective is to become a leading globalregional aircraft lessor.

Create significant synergies with Chorus'other businesses.

Execution

Chorus believes there is a significantopportunity to develop a large and profitableleasing platform.

Global passenger growth continues toaccelerate.

Regional aircraft leasing segment is stableand currently underserved with limitedcompetition

Segment enjoys premium yields and sectormargins with favorable access to capital.

Accelerating Global Passenger Growth

Page 9

Over the last 20 years, passenger demand has increased at an average of 5% per annum

Outpacing GDP growth by 2.7x

Increasing size of the global fleet

Growing market share of aircraft on operating lease

Significant increase in aggregate number of aircraft on lease

Air Travel Expected to Double in the Next 15 Years Airlines are More Dependent on Operating Leases

World annual RPK (trillions)

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

1975 1985 1995 2005 2015 2025 2035

Airbus GMF 2015

ICAOtotal traffic

2x

...and will double again in the next 15 years

2,200+3,300+

5,200+

6,800+

9,600+

17%

22%

30%

34%

40%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1995 2000 2005 2010 Mar-16

% on O

perating Lease

No.

of C

omm

erci

al A

ircra

ft

Operating Lease Operating Lease Market Share (%)

Sources: Airbus Global Market Forecast (2016), Boeing Current Market Outlook (2016), ICAO Historical Traffic Figures, Ascend,ICAO (1983 – 2013) and IATA December 2015 (2014-15)

Airline passenger growth will remain robust.

Page 10

Aircraft Leasing Continues To Build Momentum

Over half of the world’s fleet expected to be leased by 2020.

19703,772 a/c17 leased

0.4%

19806,037 a/c

100 leased1.7%

19909,160 a/c

1,343 leased24.7%

200015,032 a/c

3,713 leased24.7%

201121,741 a/c

7,943 leased36.5%

2020Forecast

Over 50% leased

Sources: Boeing Current Aircraft Market Outlook 2016

Aircraft Leasing is a Financially Attractive Segment

Page 11

Profit Before Tax Margins Return on Average Equity1

15.2%

16.7%

22.8%

24.8%

25.8%

26.2%

29.7%

32.1%

36.8%

38.4%

41.8%

Aircastle

ACG

Avation

SinoAero

AerCap

Alafco

NAC

Air Lease Corp

BOC Aviation

CALC

AviaAM

6.1%

6.8%

7.3%

8.4%

10.5%

11.1%

11.9%

12.7%

14.0%

21.0%

33.9%

ACG

Aircastle

Alafco

Air LeaseCorp

Avation

AviaAM

BOC Aviation

CALC

AerCap

NAC

SinoAero

Source: Air Finance Journal Leasing Top 50, company reports, The Airline AnalystNotes: 1 Shareholder loans as equity

Five Verticals of Aviation Leasing

Page 12

Commercial Corporate Regional Helicopters Engines

Transactions / Year:

1,500 aircraftUS $100bn

Percent Leases:

40%

Large Lessors:

35+

Comments:

NB – Narrow bodyWB – Wide bodyPassenger Cargo

Transactions / Year:

650 aircraftUS $18bn

Percent Leases:

15%

Large Lessors:

1

Comments:

General AviationCivil Air Transportation

Transactions / Year:

300 aircraftUS $10bn

Percent Leases:

20%

Large Lessors:

4

Comments:

TP – Turboprops RJ – Regional Jets100 seats or less

Transactions / Year:

500 aircraftUS $6bn

Percent Leases:

15%

Large Lessors:

6

Comments:

IndustrialAir TransportEmergencyResponse

Transactions / Year:

200 enginesUS $2bn

Percent Leases:

30%

Large Lessors:

10+

Comments:

Turbine EnginesSpares and

maintenance rotation

*Large Lessors defined as corporations with assets greater than US $1bn

Uncrowded Regional Aircraft Leasing Market

Page 13

Commercial Corporate Regional Helicopters Engines

/

Large Competitors

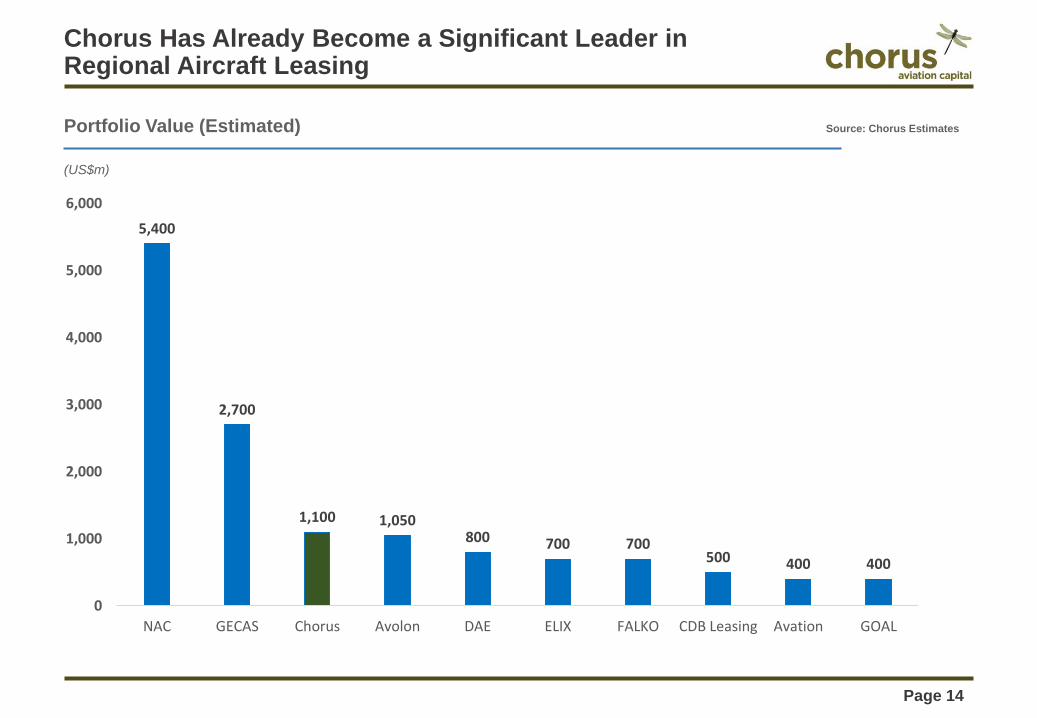

Chorus Has Already Become a Significant Leader in Regional Aircraft Leasing

Page 14

Portfolio Value (Estimated) Source: Chorus Estimates

5,400

2,700

1,100 1,050800 700 700

500 400 400

0

1,000

2,000

3,000

4,000

5,000

6,000

NAC GECAS Chorus Avolon DAE ELIX FALKO CDB Leasing Avation GOAL

(US$m)

Regional Aircraft are Fundamental to Efficient Air Transport

Page 15

Worldwide Flight Distribution By Aircraft Type Worldwide Distribution of Aircraft by Type

30% of passenger fly less than 550 km (300 mi.)

60% of the world's communities linked with regional aircraft

Regional aircraft fleet is ~24% of total commercial fleet

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Flig

hts

2012

(mill

ion)

Distance Category (km)

Turboprop (TP)Regional Jet (RJ) 61-120Narrow Body (NB)

83% of NB flights are over 500 km

63% of J61-120 flights are over 500 km

83% of TP flights are under 500 km

14,800

4,300 5,900

Narrow Body(NB)

Wide Body(WB)

Regional Aircraft(RJ/TP)

TP

RJ

Regional aircraft have specific applications for short take-off and landing and extreme conditions

Source: OAG 2012, Boeing / Bombardier

Extensive Network of Regional Airlines Worldwide

Page 16

Continent CRJ Q400 ATR eJets

North America 33 6 6 12

South America 8 - 8 10

Europe 28 10 41 24

Africa 18 3 23 5

Asia 15 4 24 23

Australia - 1 5 3

Total Operators 102 24 107 77

A diverse set of potential customers on every continent

We continue to see significant demand for regional aircraft leases

Source: Company websites, Airfleets (July 2017)

Regional Transport Dominated by Three Manufacturers

Page 17

Q400 CRJ 700/900/1000

E170/E175/E190/E195 ATR42/72

56% / 1,500

overall

44% /1,200

overall

2,700 Aircraft

Bombardier Dash 8 Family ATR Family

Turboprop Market Share1

Product Lines (in production)

Product Lines (classics)

Dash 8 - 100/200/300 CRJ - 100/200

ERJ135/ERJ140/ERJ145 Variants of 42/72

58% / 2,600

overall

42% /1,900

overall

4,500 Aircraft

Bombardier CRJ Family

Embraer ERJ / Ejets Family

Regional Jet Market Share1

Page 18

Deliveries Have Been Historically Stable

Regional Aircraft Historical and Projected Deliveries

149 150132 131

177 185 199 192 193227

107 99100 103

108 10199 99 95

95256 249232 234

285 286298 291 288

322

0

50

100

150

200

250

300

350

400

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Regional Jets Turboprops

2010–2015 Average Deliveries: 257

1 2

Source: Airline Monitor, Wall Street ResearchNotes:1 Includes CRJ700/705, CRJ900, CRJ1000, CS100, EMB135/140/145, EMB170/175, EMB190/195, SSJ100, MRJ, A318, 737-600, ARJ21 2 Includes ATR42, ATR72, Q400

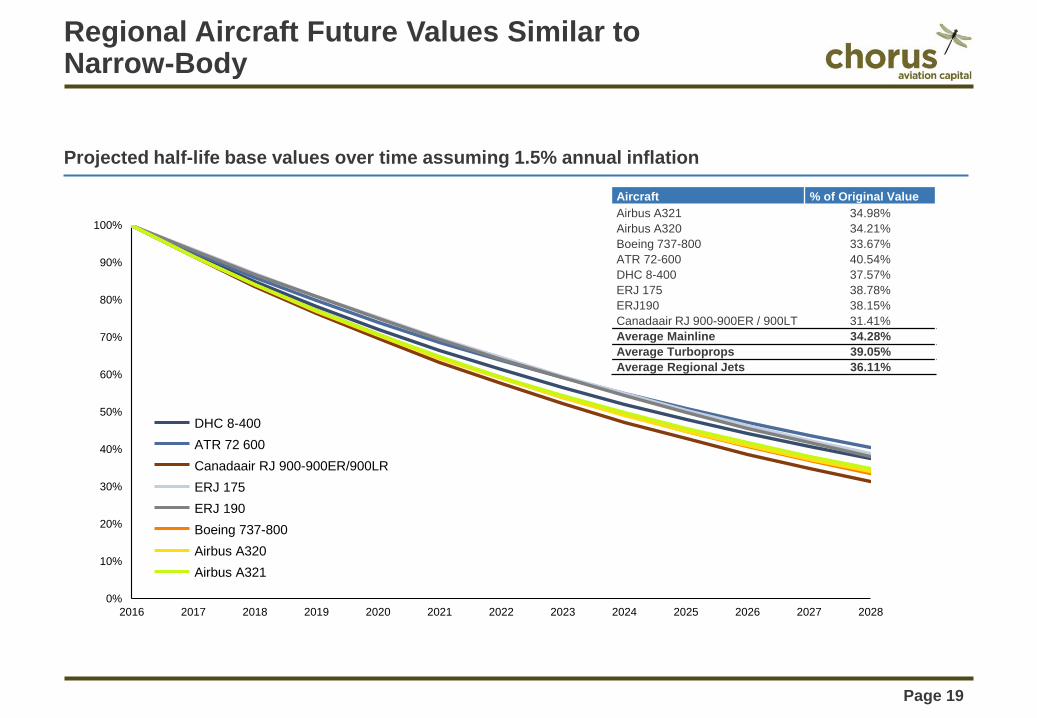

Regional Aircraft Future Values Similar to Narrow-Body

Page 19

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028

ATR 72 600

ERJ 190

Canadaair RJ 900-900ER/900LRERJ 175

Boeing 737-800

Airbus A321

DHC 8-400

Airbus A320

Projected half-life base values over time assuming 1.5% annual inflation

Aircraft % of Original ValueAirbus A321 34.98%Airbus A320 34.21%Boeing 737-800 33.67%ATR 72-600 40.54%DHC 8-400 37.57%ERJ 175 38.78%ERJ190 38.15%Canadaair RJ 900-900ER / 900LT 31.41%Average Mainline 34.28%Average Turboprops 39.05%Average Regional Jets 36.11%

Regional Aircraft: An Ideal Leased Asset

Page 20

Resilient Demand Expectations with a Broad User Base

― The 70-130+ seat fleet is expected to grow 4-5% per year over the next 20 years

― Operational efficiencies from regional aircraft play a key role in hub-and-spoke networks

Attractive Aircraft Type for Shorter Routes

― Regional aircraft allow airlines to optimize aircraft size and reduce per-seat cost

― ~50% of global passengers fly on trips below 500 miles and ~30% of global passengers fly on trips below 300 miles

Geographically Diverse Demand Dynamics

― Economic growth in emerging markets is expected to significantly outpace those in advanced economies

― The emergent urban middle classes in these areas present a real opportunity to expand air travel capabilities which will require the use of turboprop and regional jet aircraft

Stable Supply

― Historical deliveries of regional aircraft have been relatively consistent

― Regional aircraft projected deliveries are stable

Ability to Hold Values Over Time

― Values of regional jets and turboprops have proved less volatile relative to most narrow body aircraft

2

4

3

5

1

Page 21

Announced transactions for 19 regional aircraft.

Five aircraft types from three manufacturers with average age of 2.7 years.

Clients now include seven major regional airlines in seven countries on five continents.

New clients include Azul, Aeromexico, Air Nostrum, Falcon Aviation, Flybe, KLM & Virgin Australia.

Locked-in leasing stream with an average term of greater than 7 years.

Lease revenue producing expected yield.

Committed financing for all 19 new regional aircraft.

Average LTV of portfolio of 75% (Debt: Equity 3:1).

Expanded management team with five new appointments with 23 years average commercial aircraft experience.

Opened and staffed our Irish office.

Acquisitions will nicely contribute to Chorus Aviation returns in subsequent quarters.

Financial forecast metrics all meeting or exceeding our targets.

Scale

Diversity

Returns

Experience

Liquidity

Visibility

Progress to Date

Page 22

Assembled a Highly Experienced Management TeamSteven RidolfiPresident

SVP, Strategic Investments, Mergers & Acquisitions, Chorus Aviation SVP, Strategy, Mergers and Acquisitions, Bombardier President, Business Aircraft, Bombardier President, Regional Aircraft Bombardier

James Bruce PeddleChief Operating Officer

VP, Aircraft Leasing and Trading, Chorus Aviation VP, Marketing & Sales, Bombardier Flexjet VP, Commercial, Embraer North America Managing Director, Embraer Asia Pacific

Cameron MountenayChief Financial Officer

VP, Structured Finance, Bombardier VP, Finance and Contracts, Bombardier VP, Asset Management & Business Development, Bombardier

Rory McQueenVice President, Finance & Capital Markets

VP, Capital Markets, Lease Corporation International (LCI) Head of Treasury, Vistajet Director, Structured Finance, Bombardier Director, Aircraft Finance, Bank of Scotland

Jim MurphyVice President, Transactions & Control

Director, Corporate Development & Aircraft Programs, Chorus Aviation VP, Commercial Operations, Provincial Airlines Director, Marketing & Fleet Planning, Canadian Airlines

Anil MohanVice President Legal

Associate General Counsel, Chorus Aviation General Counsel, Halifax International Airport Legal Counsel, IMP Group

Una SlevinVice President, Contracts

Head of Finance and Operations, CIT Aerospace Treasury Manager, CIT Group Finance Financial Controller, CIT Group Finance

Page 23

Progress to Date

Azul 2x E195s KLM 1x E190s Aeromexico 1x E190s Aeromexico 2x E190s

Air Nostrum 4x CRJ1000s Flybe 3x ATR72-600s Virgin Australia 3x ATR72-600s Falcon 3x Q400s

Contracted for 19 aircraft with an average age of 2.7 years.

Page 24

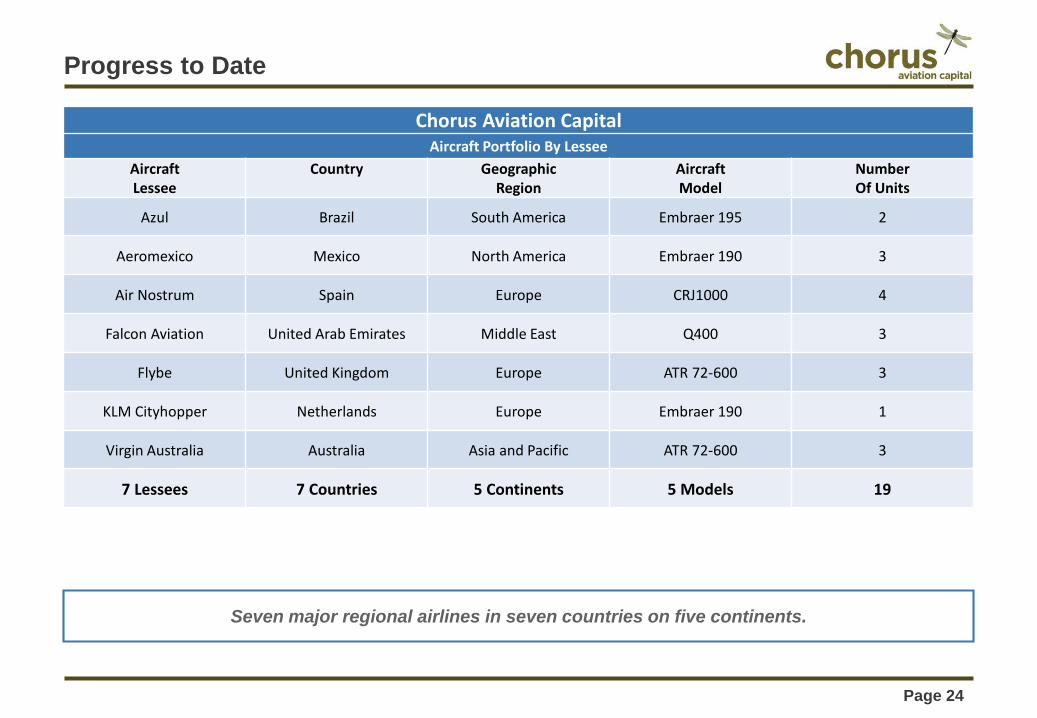

Progress to Date

Chorus Aviation CapitalAircraft Portfolio By Lessee

Aircraft Lessee

Country GeographicRegion

AircraftModel

NumberOf Units

Azul Brazil South America Embraer 195 2

Aeromexico Mexico North America Embraer 190 3

Air Nostrum Spain Europe CRJ1000 4

Falcon Aviation United Arab Emirates Middle East Q400 3

Flybe United Kingdom Europe ATR 72-600 3

KLM Cityhopper Netherlands Europe Embraer 190 1

Virgin Australia Australia Asia and Pacific ATR 72-600 3

7 Lessees 7 Countries 5 Continents 5 Models 19

Seven major regional airlines in seven countries on five continents.

Page 25

Regional Aircraft Sourcing Channels

Portfolio Acquisition Purchase of existing assets and leases from existing lessors.

Airline Sale Leaseback Sale and leaseback of existing or future aircraft deliveries.

Skyline Leases Direct purchase from OEM for subsequent lease to airlines.

There are a significant number of profitable lease transactions available to CAC.

Page 26

Chorus Aviation Capital Growth Opportunity

We believe there is a significant opportunity to develop a large and profitable leasingplatform by exploiting this currently underserved segment and prevailing marketdynamics.

We have been able to consummate a significant number of successful profitabletransactions over a short period of time. We have transitioned to a significantbusiness with strong, attractive assets and contracted leases and margins, and webelieve we can replicate and accelerate this growth.