Children’s Savings Accounts:

A New Strategy on the Road to Universal Savings Policy

Carl Rist, CFED2003 State IDA Policy Conference

St. Louis, MO November 10-12, 2003

2

The Facts: Children and Poverty

11,733,000 children under 18 (16.3%) lived in

poverty in 2001 (Census Bureau).

1 in 3 children will be poor at some point (Children’s

Defense Fund).

Of families with children in which the head of the household worked, the poverty rate was 9.2% in

2000 (Center on Budget and Policy Priorities).

3

Children and Poverty: An International Comparison

0

5

10

15

20

25

30

Sweden

Taiwan

Germany

PolandU.K.

U.S.

Mexico

Sweden

Taiwan

Germany

Poland

U.K.

U.S.

Mexico

4

Children and “Asset” Poverty

SOURCE: PSID, 1999

*Net Financial Assets below three-month income poverty standard.

1984 1989 1994 19990%

10%

20%

30%

40%

50%

60%

70%

BlackHispanic

All

White

5

(Early) Assets Matter

Research (summarized by Scanlon and Page-Adams):

Savings and investment income promotes educational attainment among children.

Savings and investment income—above earned income—reduces intergenerational poverty transmission.

Savings have psychosocial benefits for adults, which likely enhance the well-being of children.

6

Assets Matter

Evidence:

Returns to education

Importance of homeownership

7

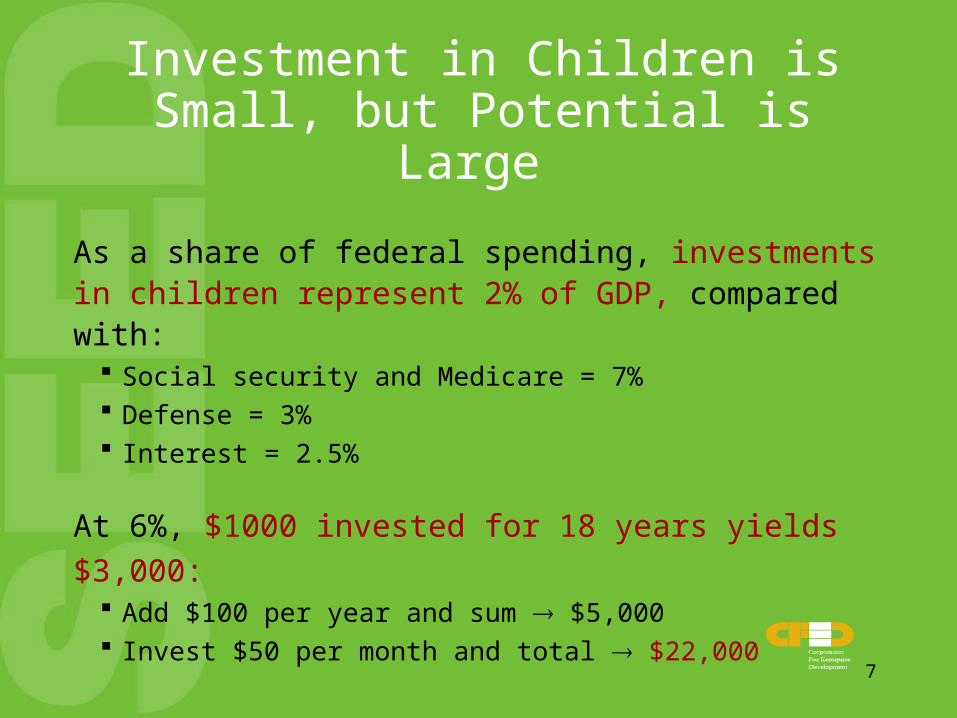

Investment in Children is Small, but Potential is Large

As a share of federal spending, investments in children represent 2% of GDP, compared with:

Social security and Medicare = 7% Defense = 3% Interest = 2.5%

At 6%, $1000 invested for 18 years yields $3,000: Add $100 per year and sum $5,000 Invest $50 per month and total $22,000

8

Precedents for Children and Youth Savings Policy:

International

Singapore: Baby Bonus

Child Development Accounts

Central Provident Fund

United Kingdom: Child Trust Fund

9

Precedents for Children and Youth Savings Policy: U.S. Federal Proposals

Children’s Financial Security Act (1996)

KidsSave (1995, 1998, 2000)

Educational Savings Accounts (1997)

Education IRAs/Coverdell ESAs (1997, 2001)

10

Precedents for Children and Youth Savings Policy:

U.S. State Policy

Oregon’s Children’s Development Accounts

(CDAs) – 1991 and 1993.

11

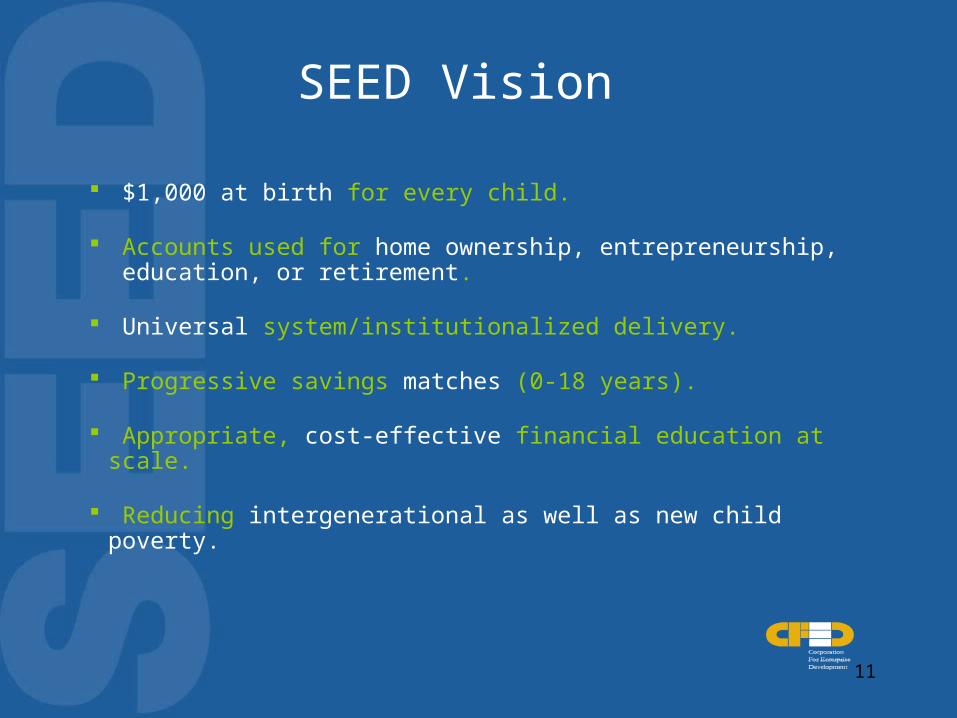

SEED Vision

$1,000 at birth for every child.

Accounts used for home ownership, entrepreneurship, education, or retirement.

Universal system/institutionalized delivery.

Progressive savings matches (0-18 years).

Appropriate, cost-effective financial education at scale.

Reducing intergenerational as well as new child poverty.

12

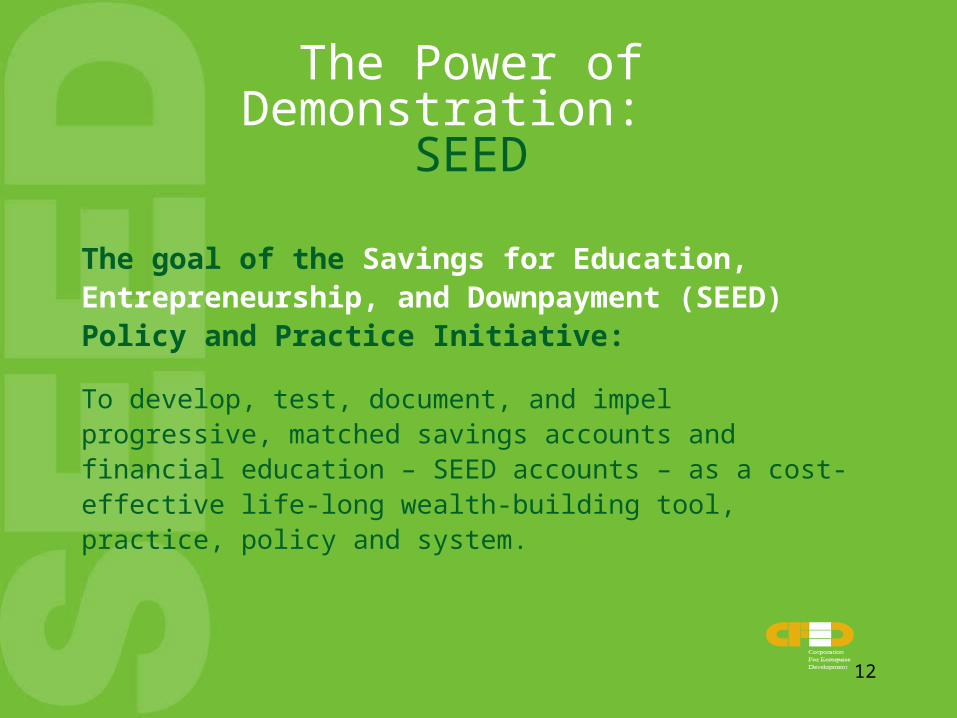

The Power of Demonstration: SEED

The goal of the Savings for Education, Entrepreneurship, and Downpayment (SEED) Policy and Practice Initiative:

To develop, test, document, and impel progressive, matched savings accounts and financial education – SEED accounts – as a cost-effective life-long wealth-building tool, practice, policy and system.

13

SEED Objectives

Accounts: Move 1000+ low-income children and their families toward economic independence through cost-effective SEED accounts.

Practice: Develop cost-effective, scalable practice models for different age cohorts of children 0-18.

Research & Evaluation: Document, research, and evaluate SEED account models and effects.

Policy: Develop, advocate, and enact progressive universal federal/state policy.

Communication: Develop and communicate effective messages, results and lessons.

Coalition: Build a diverse, inclusive, and effective coalition to guide and promote effective SEED practice and policy.

14

SEED Cohorts

Pre-school children (0-5; via parents)

Elementary school children (6-10 years)

Middle school children (11-13 years)

High school age youth (14-18 years)

15

SEED Partners

9 Community Partners: 50-75 accounts

Work with one specific age cohort

Diverse designs

1 “Experimental” Partner: 500 accounts in “treatment” group; 500 controls

Rigorous impact evaluation

Streamlined 529 Account Structure

Pre-school (age 3, HeadStart based)

16

Match and Operating Grant Model

$2,000 split at partner’s proposal among: Initial deposit — $0–$1,000 Savings matches (1:1) Benchmark deposits and other incentives

$25,000 annual operating grants for small sites.

Primary use for education through 529 plans— but also housing, business, retirement, incentive rewards.

Link with existing systems: 529s, Roth IRAs etc.

17

SEED Partners

Juma Ventures Mile High United

National Center on Poverty Law

Oakland Livingston Human Service Agency

Community Foundation for Greater New Haven

Harlem Children's Zone

Boys and Girls Clubs of Delaware

Beyond Housing

Good Faith Fund

Foundation Communities

Partner sites Experimental site

18

SEED Policy, Communication & Organizing

Focus group work up front

Message development up front

Deliberate policy development

Policy development, advocacy, and lobbying

Direct state policy grants (if funding)

SEED policy council

UK Approves Child Trust Funds

Treasurers’ response to SEED highlights 529 Opportunity (many endorsements)

19

Initiative Partners

Researchers:Center for Social Development (Washington University, St. Louis)

Kansas University

Funders:Ford FoundationCharles and Helen Schwab Foundation Jim Casey Youth Opportunities InitiativeEwing M. Kauffman FoundationRhoda and Richard Goldman FoundationEvelyn and Walter Haas, Jr. FundEdwin Gould Foundation

20

Contact:

Carl Rist

Corporation for Enterprise Development

123 W. Main St., 3rd Floor

Durham, NC 27701

919.688.6444

919.688.6580

www.cfed.org

See the SEED Website at seed.cfed.org