156

CHAPTER –VI

SOCIO-ECONOMIC STATUS OF DRYLAND FARMERS

The dryland agriculture reached a part of plateau in terms of livelihood

conditions. It is not able to provide full employment and sufficient income for the

people living in dryland agriculture .Farm profitability has witnessed a sharp

decline due to land degradation, risk and uncertainty associated with dryland

agriculture. As farming alone is not able to generate sufficient income to small

and marginal farmers, dryland farmers are in deep crisis. In this regard, to bring

into light the socio-economic status of the dryland farmers, the socio-economic

variables like caste, education, family structure, housing , access to civic facilities,

assets ownership, land ownership, cropping pattern yield pattern, source of credit ,

outstanding debt ,income and consumption expenditure are analysed in this

chapter to estimate the socio-economic status of the farming community.

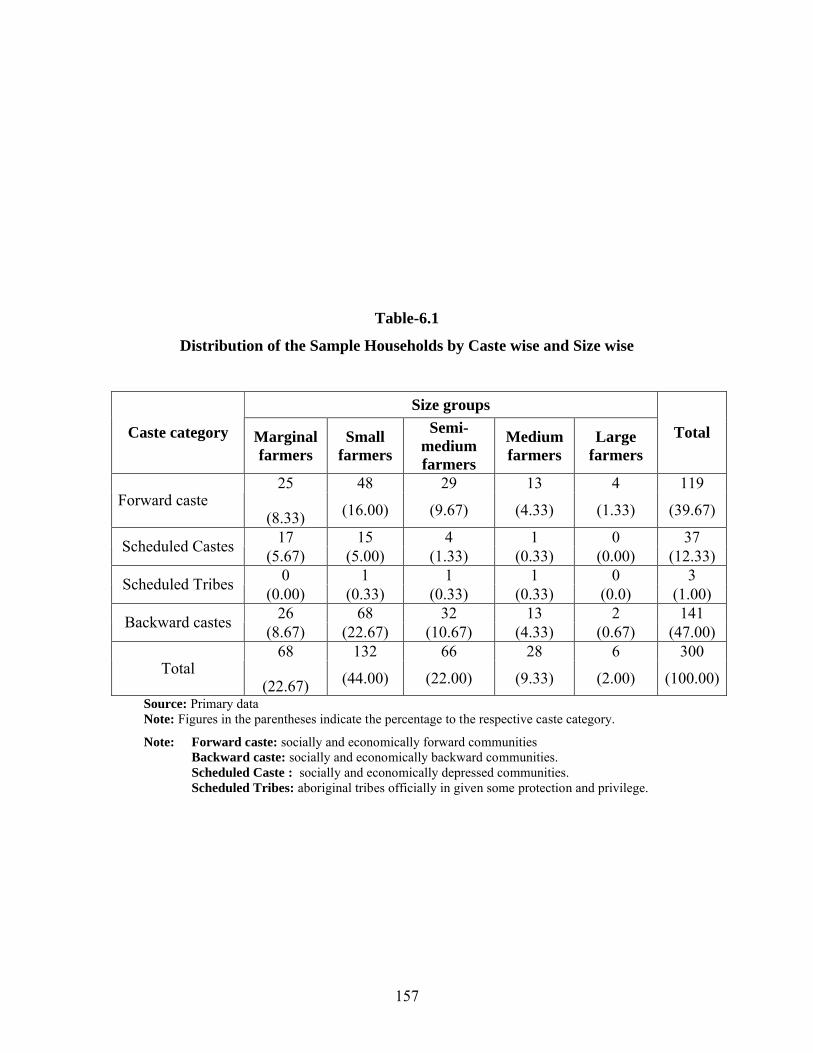

6.1 Distribution of Sample Households by Social Group

The social group composition of sample household is presented in table -

6.1. An examination of data reveals that the proportion of farmers representing

backward castes in the dryland farming is 47 per cent, followed by forward castes

with 39.67 per cent and scheduled caste and scheduled tribes who constitute

12.33per cent and 1.00 per cent respectively. It shows clearly that most of the

socially and economically backward communities depend on dryland cultivation

for their livelihood. That is to say, majority of poor people live on dry land

agriculture.

6.2 Family status of the Farm Households

Type of family is again another important social variable that influences

social behaviour of an individual in the society. Distribution of farm households

by family type is presented in table-6.2. It reveals that joint family system is a

common phenomenon in the rural Indian society. However in the present study,

out of 300 farm households, 119 accounting for 39.70 per cent are joint families.

157

Table-6.1

Distribution of the Sample Households by Caste wise and Size wise

Size groups

Caste category Marginal farmers

Small farmers

Semi-medium farmers

Medium farmers

Large farmers

Total

25 48 29 13 4 119Forward caste

(8.33) (16.00) (9.67) (4.33) (1.33) (39.67)

17 15 4 1 0 37Scheduled Castes

(5.67) (5.00) (1.33) (0.33) (0.00) (12.33)0 1 1 1 0 3

Scheduled Tribes(0.00) (0.33) (0.33) (0.33) (0.0) (1.00)

26 68 32 13 2 141Backward castes

(8.67) (22.67) (10.67) (4.33) (0.67) (47.00)68 132 66 28 6 300

Total(22.67) (44.00) (22.00) (9.33) (2.00) (100.00)

Source: Primary dataNote: Figures in the parentheses indicate the percentage to the respective caste category.

Note: Forward caste: socially and economically forward communities Backward caste: socially and economically backward communities.Scheduled Caste : socially and economically depressed communities. Scheduled Tribes: aboriginal tribes officially in given some protection and privilege.

158

Table - 6. 2

Family Status of the Farm Households

Size groups FamilyStatus Marginal

farmersSmall

farmers

Semi-medium farmers

Medium farmers

Large farmers

Total

19 55 26 14 5 119Joint

(27.94) (41.67) (39.39) (50.00) (83.30) (39.70)49 77 40 14 1 181

Nuclear(72.06) (58.33) (60.61) (50.00) (16.70) (60.30)

68 132 66 28 6 300Total

(100.00) (100.00) (100.00) (100.00) (100.00) (100.00)Source: Primary dataNote: Figures in the parentheses indicate the percentage to the size groups.

159

The general notion is that as development takes place, people prefer

nuclear family norm. This nuclear family system still exists in the study area

inspite of its backwardness. The joint family system is closely associated with

large farms. Proportion of joint families to the total farm households increases

with the farm size. The proportion of nuclear families decreases with the farm

size. Nuclear family system found to be more among marginal and small farm

households.

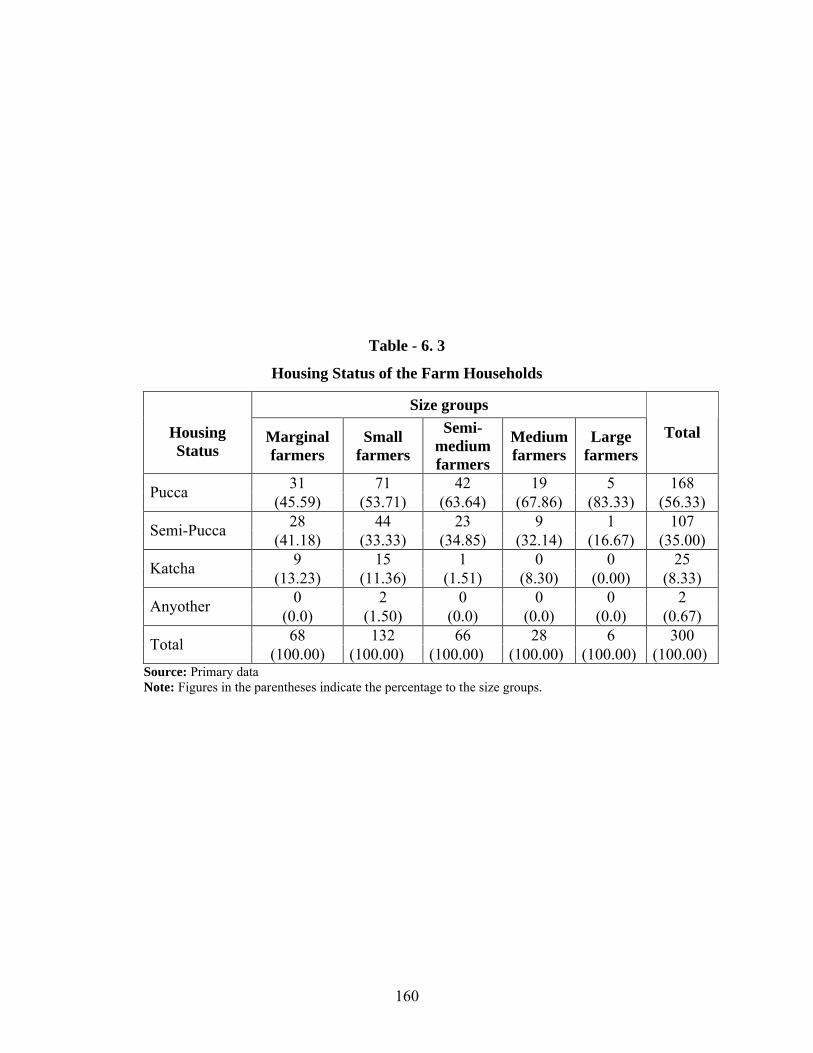

6.3 Distribution of Farm Households by Housing Status

Food, clothing and shelter are the minimum needs for life. Type of house

is one of the economic indicators of the household. In rural economy farmer is a

productive entrepreneur. The standard of living of farm entrepreneur can be

measured in terms of conditions in which he is living. So, an attempt is made to

know the type of house possessed by the sample farm households. Distribution of

farm household by farming category by type of house is presented in table-6.3. It

reveals that 56.33 Per cent (168) of farm households possess R.C.C. or pucca

houses, 35 per cent (105) of farm households possess semi-pucca houses. The

remaining farm households live in katcha houses. This clearly indicates the low

standard of living of the farm households, that is to say, that 44 per cent of farm

households without possession of a pucca house reflects the poverty among farm

households. Distribution of farm households by the type of house across size

groups reveals that 16.67 per cent of the large farm households and 32 per cent of

medium farm households are living in katcha houses. Since small and marginal

farms are covered under government housing scheme, 45 per cent of marginal and

53 per cent of small farm households could live in small pucca houses. Thus the

data on housing clearly reveals the poor living conditions of farm households.

160

Table - 6. 3

Housing Status of the Farm Households

Size groups

Housing Status

Marginal farmers

Small farmers

Semi-medium farmers

Medium farmers

Large farmers

Total

31 71 42 19 5 168Pucca

(45.59) (53.71) (63.64) (67.86) (83.33) (56.33)28 44 23 9 1 107

Semi-Pucca(41.18) (33.33) (34.85) (32.14) (16.67) (35.00)

9 15 1 0 0 25Katcha

(13.23) (11.36) (1.51) (8.30) (0.00) (8.33)0 2 0 0 0 2

Anyother(0.0) (1.50) (0.0) (0.0) (0.0) (0.67)68 132 66 28 6 300

Total(100.00) (100.00) (100.00) (100.00) (100.00) (100.00)

Source: Primary dataNote: Figures in the parentheses indicate the percentage to the size groups.

161

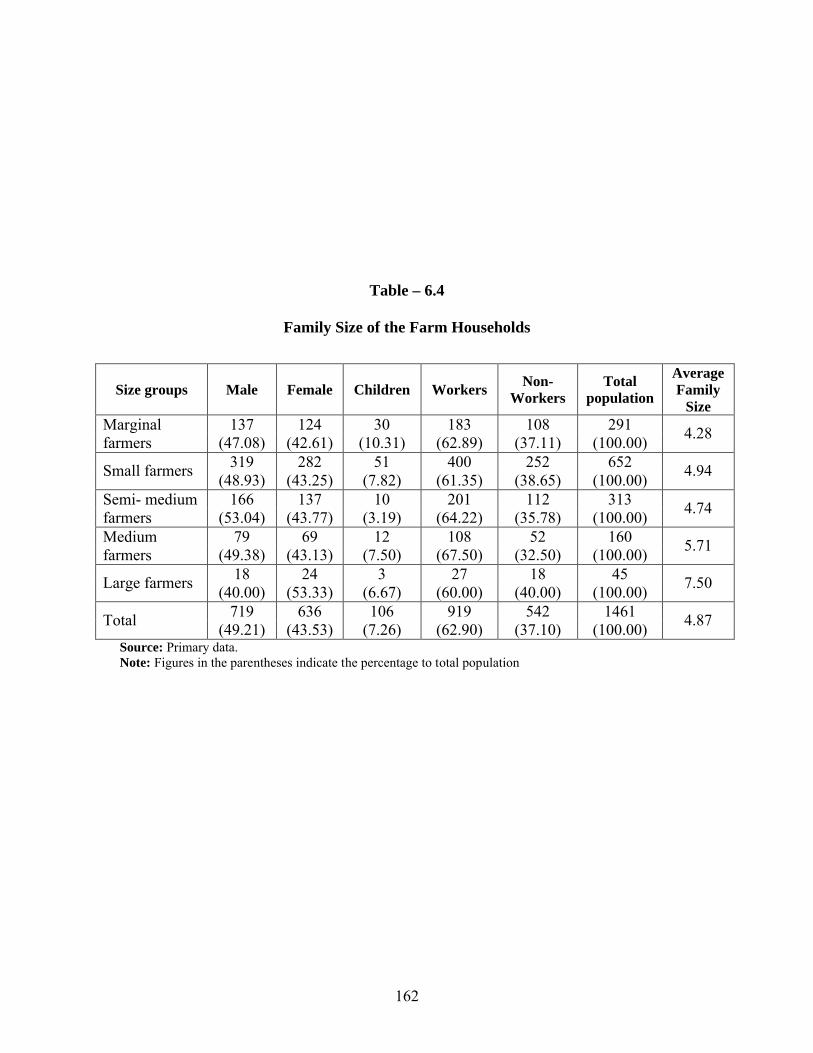

6.4 Composition of Population and Family Size

The demographic profile of the selected sample households revealing the

sizes of their respective families is distributed as per the farm sizes. As shown in

the table- 6.4, male population constitutes 47.08 per cent to the total composition

of sample households and that of female constitutes 42.61 per cent and the

children constitute 10.31 per cent. It is observed that the proportionate size of

male population is higher than that of female in all farming categories and it is

higher among semi-medium farms when compared to other farm size groups. It is

almost same with the medium (49.38 per cent) and small farmers (48.93). As for

children they constitute higher proportion among marginal (10.31 per cent) and

small farms (7.82 per cent). With regard to female population, their proportion is

higher among large farmers. The average size of the family is small for marginal

and small farms when compared with the other farmers. Among all farming

categories the average family size of large farms is high, which is ‘7.50’. The

average size of the family of the total farm household is 4.87.

6.5 Access to Civic Amenities

The provision of facilities like, availability of drinking water, sanitation,

roads and electricity indicate the living conditions of the farm households. Access

to civic facilities across the farm size group holdings is presented in table-6.5.

Only 31.33 per cent of the farm households have drinking water facility at their

house premises and the remaining 69.67 per cent of the households depend on

public tap or public hand pumps. Out of 300 farm households 96 per cent of the

households have electricity connections; only 4 per cent of the households do not

have the electricity. Drainage facility is one of the development indicators, but

only 15.33 per cent of the households have drainage facility. This clearly indicates

that the dryland farmers are deprived of minimum civic facilities in the study area.

162

Table – 6.4

Family Size of the Farm Households

Size groups Male Female Children WorkersNon-

WorkersTotal

population

Average Family

Size137 124 30 183 108 291Marginal

farmers (47.08) (42.61) (10.31) (62.89) (37.11) (100.00)4.28

319 282 51 400 252 652Small farmers(48.93) (43.25) (7.82) (61.35) (38.65) (100.00)

4.94

166 137 10 201 112 313Semi- medium farmers (53.04) (43.77) (3.19) (64.22) (35.78) (100.00)

4.74

79 69 12 108 52 160Medium farmers (49.38) (43.13) (7.50) (67.50) (32.50) (100.00)

5.71

18 24 3 27 18 45Large farmers(40.00) (53.33) (6.67) (60.00) (40.00) (100.00)

7.50

719 636 106 919 542 1461Total(49.21) (43.53) (7.26) (62.90) (37.10) (100.00)

4.87

Source: Primary data.Note: Figures in the parentheses indicate the percentage to total population

163

Table - 6. 5

Access to Civic Facilities by Size Groups

Size GroupDrinking water

facilityProvision of the

ElectricityPermanent

drainage facility 13 64 6

Marginal farmers(19.12) (94.11) (8.80)

30 125 15Small farmers

(22.72) (94.70) (11.36)17 65 12

Semi-medium farmers(25.75) (98.48) (18.18)

7 28 6Medium farmers

(25.00) (100.00) (21.43)3 6 4

Large farmers(50.00) (100.00) (66.67)

94 288 46Total

(31.30) (96.00) (15.33)Source: Primary dataNote: Figures in the parentheses indicate the percentage to the respective size groups.

164

6.6 Possession of Consumer Goods

The possession of consumer durable goods represents the socio-economic

status of households. The distribution of households by the possession of

consumer durables across the farm size groups is presented in table-6.6. Only

13.33 per cent of the households have Radio, 66.67 per cent of the farm

households have TV, 30.33 per cent have LP Gas, 77 per cent have electric fans.

55 per cent have cell phones, 50.67 per cent have bicycles, 15 per cent have two

wheelers, 6.33 per cent have VCD/ DVD players, 2 per cent have refrigerator and

1 per cent of farm households have domestic pump sets. Though, LPG gas is one

of the basic needs of the households, 70 per cent of the dryland farmers do not

have access to it. They depend on firewood for cooking. The data further reveals

that T.V and electric fan have become important consumer goods.

6.7 Education Levels of the Farm Households

Level of literacy is one of the important parameters that indicate the social

and economic status of farm households. This in turn brings in change in

economic status. The level of literacy among sample farm households by the size

of the farms is presented in table-6 7. The data reveals that 57 per cent of heads of

the farm households do not have any formal education. Of the remaining farm

households, 11.33 per cent of the farmers have primary education, 22 percent of

the farmers have school level education and 10 per cent of the dryland farmers

have got educated above 10th level. The data on literacy among the dryland

farmers appears to be low when compared to overall state rural population

literacy, which is 47 per cent.

165

Table-6.6

Consumer Durables

Size Groups

Goods Marginal farmers

Small farmers

Semi-medium farmers

Medium farmers

Large farmers

Total

12 18 5 3 2 40Radio

(17.64) (13.64) (7.58) (10.71) (33.33) (13.33)44 74 51 25 6 200

T.V(64.71) (56.06) (72.27) (89.28) (100.0) (66.67)

22 34 19 11 5 91LP gas

(32.35) (25.76) (28.78) (39.28) (83.33) (30.33)1 1 0 0 0 2

Gobar gas(1.47) (0.75) (0.00) (0.00) (0.00) (0.67)

47 96 60 22 6 231Electric fan

(69.12) (72.73) (90.91) (78.6) (100.0) (77.00)0 1 2 1 2 6

Refrigerator(0.00) (0.75) (3.00) (3.57) (33.33) (2.00)

1 0 0 1 1 3Domestic pumpset (1.47) (0.00) (0.00) (3.57) (16.67) (1.00)

1 4 6 5 3 19VCD or DVD

(1.47) (3.03) (9.09) (17.85) (50.00) (6.33)29 64 49 17 6 165Cell phone or

land line phones (42.65) (48.48) (74.24) (60.71) (100.00) (55.00)32 69 31 16 4 152

Bicycle(47.05) (52.27) (47.00) (57.14) (66.66) (50.67)

6 14 12 9 4 45Two wheeler

(8.82) (10.61) (18.18) (32.14) (66.67) (15.00)0 1 0 0 0 1

Jeep(0.00) (0.75) (0.00) (0.00) (0.00) (0.33)

Source: Primary dataNote: Figures in the parentheses indicate the percentage to the respective size groups.

166

Table - 6. 7

Education Level of the Farm Households

Size Groups Educational

level Marginal farmers

Small farmers

Semi-medium farmers

Medium farmers

Large farmers

Total

40 79 38 12 2 171Illiterate

(58.82) (59.84) (57.58) (42.86) (33.33) (57.00)

11 17 4 2 0 34Primary

(16.17) (12.88) (6.06) (7.14) (0.00) (11.33)

12 29 15 9 1 66Middle and high school (17.65) (21.98) (22.73) (32.14) (16.67) (22.00)

3 6 6 3 2 2010th pass and Inter (4.41) (4.54) (9.09) (10.71) (33.33) (6.67)

2 1 3 2 1 9Graduation and above (2.94) (0.76) (4.54) (7.14) (16.67) (3.00)

68 132 66 28 6 300Total

(100.00) (100.00) (100.00) (100.00) (100.00) (100.00)Source: Primary dataNote: Figures in the parentheses indicate the percentage to the size groups.

167

6.8 Occupations of the Farm Households

Occupation impacts socio-economic status of the household. So

occupational distribution of the farm households is examined to know the levels

of living. The occupational distribution of sample farm households across the

farm size groups is presented in table- 6.8 and 6.8a. Cultivation is the main

occupation for 94.34 per cent of farm households. Among marginal farms 2.94

per cent have reported that their main income is from wage labour. The intra size

group comparison reveals that about 17 per cent of large farm households, 7 per

cent of medium farm households, 3 per cent of semi-medium farm households, 2

per cent of small households and 6 per cent of marginal farm households get their

main income from employment either in government or in private organizations.

Nearly 66.33 per cent of farm households have agricultural wage labour as the

subsidiary occupation. To say category wise, 70 per cent of small and marginal

farms, 61 per cent of medium and semi-medium farms and 33.33 per cent of large

farms work as agricultural wage workers to meet their family needs.

6.9 Possession of Livestock

Livestock is one of the important productive assets which are

complimentary to crop production. Most of the people in the developing

economies depend on livestock for their livelihood. It includes many categories of

animals such as buffaloes, cows, bullock, goat, sheep and poultry birds. However,

poultry farms and commercial buffalo farms are not included in the present study.

The distribution of livestock among size groups of farm households is presented

in table-6.9. It shows that 52 per cent of farm households own cows or buffaloes

for milk products. Nearly 34.33 per cent of households own bullocks for

cultivation and for hiring out and 10.33 per cent of households rare goat and

sheep. Dryland farm households do not possess large number of cattle due to the

fact that livestock enterprise might not be a variable often for them because they

don’t get fodder throughout the year.

168

Table-6.8

Distribution of Farm Households by Main Occupation

Size Groups

Main Occupation

Marginal farmers

Small farmers

Semi-medium farmers

Medium farmers

Large farmers

Total

62 126 64 26 5 283Cultivation

(91.12) (95.45) (96.97) (92.86) (83.33) (94.34)2 2 0 0 0 4Agricultural

Labourer (2.94) (1.51) (0.00) (0.00) (0.00) (1.33)0 1 0 0 0 1

Technical worker(0.00) (0.75) (0.00) (0.00) (0.00) (0.33)

4 3 2 2 1 12Employment in Govt or Privatesector (5.88) (2.27) (3.03) (7.14) (16.67) (4.00)

68 132 66 28 6 300Total

(100.00) (100.0) (100.00) (100.00) (100.00) (100.00)Source: Primary dataNote 1: Figures in the parentheses indicate the percentage to the size groups. Note 2: Here the main occupation of the head of the farm households only is taken into account

169

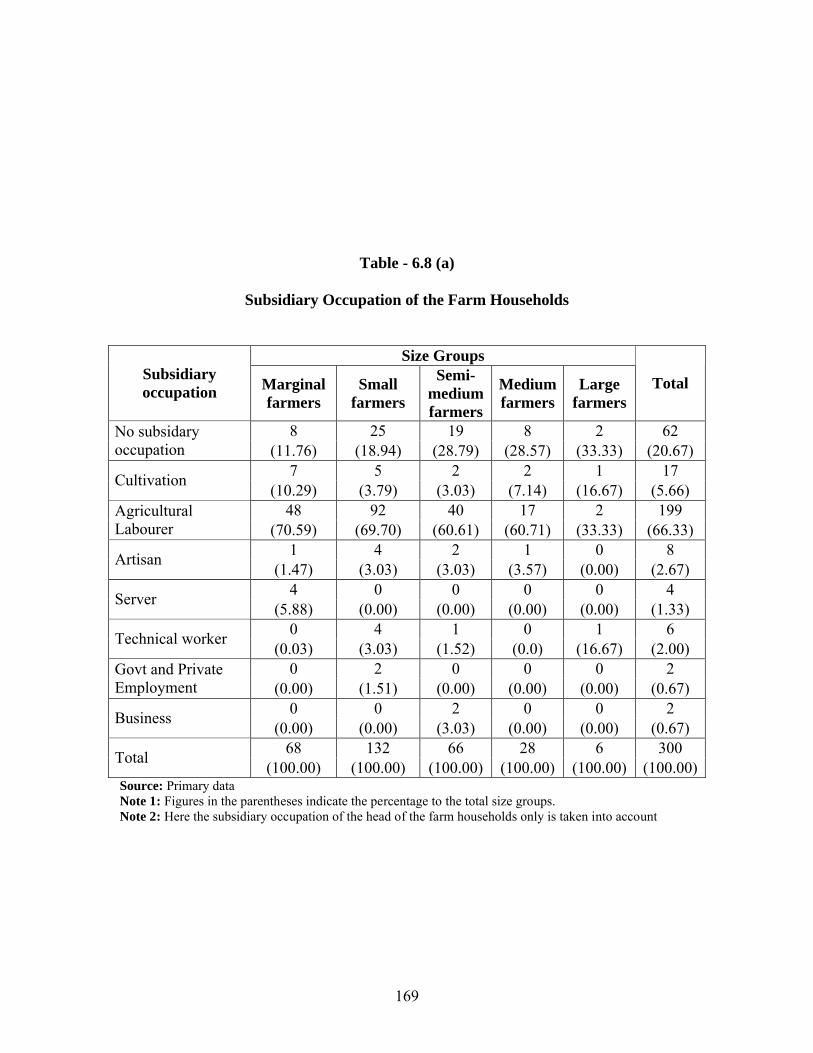

Table - 6.8 (a)

Subsidiary Occupation of the Farm Households

Size Groups Subsidiary occupation Marginal

farmersSmall

farmers

Semi-medium farmers

Medium farmers

Large farmers

Total

8 25 19 8 2 62No subsidary occupation (11.76) (18.94) (28.79) (28.57) (33.33) (20.67)

7 5 2 2 1 17Cultivation

(10.29) (3.79) (3.03) (7.14) (16.67) (5.66)48 92 40 17 2 199Agricultural

Labourer (70.59) (69.70) (60.61) (60.71) (33.33) (66.33)1 4 2 1 0 8

Artisan(1.47) (3.03) (3.03) (3.57) (0.00) (2.67)

4 0 0 0 0 4Server

(5.88) (0.00) (0.00) (0.00) (0.00) (1.33)0 4 1 0 1 6

Technical worker(0.03) (3.03) (1.52) (0.0) (16.67) (2.00)

0 2 0 0 0 2Govt and Private Employment (0.00) (1.51) (0.00) (0.00) (0.00) (0.67)

0 0 2 0 0 2Business

(0.00) (0.00) (3.03) (0.00) (0.00) (0.67)68 132 66 28 6 300

Total(100.00) (100.00) (100.00) (100.00) (100.00) (100.00)

Source: Primary dataNote 1: Figures in the parentheses indicate the percentage to the total size groups.Note 2: Here the subsidiary occupation of the head of the farm households only is taken into account

170

Table-6.9

Distribution of Livestock Population by Size Groups

Size Groups

Livestock Marginal farmers

Small farmers

Semi-medium farmers

Medium farmers

Large farmers

Total

3 17 25 11 2 58Cows

(4.41) (12.88) (37.88) (39.33) (33.33) (19.33)

16 41 25 12 4 98Buffalow

(23.53) (31.06) (37.88) (42.88) (66.67) (32.67)

6 38 33 21 5 103Bullocks

(8.82) (28.78) (50.00) (75.00) (83.33) (34.33)

3 15 8 4 1 31Goats and sheep

(4.41) (11.40) (12.12) (14.33) (16.67) (10.33)

Source: Primary dataNote: Figures in the parentheses indicate the percentage to the total livestock

171

6.10 Assets of the Farm Households

The total value of assets owned is an important indicator of economic

status of the farm households. Assets can be divided into physical assets and

liquid assets. Physical assets include land, house, farm house, agricultural

implements and livestock etc. Liquid assets include cash, gold, savings etc. The

average value of assets of the farm household by farming category is presented in

the table-6.10. The data reveals that the marginal farmers have physical assets

worth of Rs. 2,23,382/- and liquid assets worth of Rs. 14,603/- small farmers have

physical assets worth of Rs. 2,86,970/- and liquid assets worth of Rs.25,924/-. The

semi-medium farmers have physical assets worth of Rs. 5, 80,455/- and liquid

assets worth of Rs.34, 311/-. Medium farmers have physical assets worth of

Rs.7, 57,143/- and liquid assets worth of Rs. 52,589/- .

Large farmers have physical assets worth of Rs. 19,21,667/-, and liquid

assets worth of Rs. 1,26,667/- at current price. This reveals that there is direct

relation between values of assets and farm size. Land as a productive asset

constitutes the major component of assets for dryland farmer.

6.11. Average Size of the Holding

Area operated by farm holding is an indicator of the productive capacity of

the farm enterprise. The average farm sizes of different farm groups are calculated

in the table-6.11. The average size of the dryland farms in the study area is 5.37

acres. Semi- medium, medium and large farms have leased in lands, while the

small farms leased out their land. The data on leased in and leased out land

reveals that tenancy is not present much in the study area. The small and marginal

farm households have leased out their land due to the fact that small operated area

is not economical. Semi-medium and medium farms have leased in land from

small and marginal farms to make the operated area economical.

172

Table-6.10

Assets of the Farm Households

(In rupees)

Source: Primary data

Total value of assetsSize Groups

Physical Liquid

Marginal farmers 223382 14603

Small farmers 286970 25924

Semi-medium farmers 580455 34311

Medium farmers 757143 52589

Large farmers 1921667 126667

Total 413700 29707

173

Table-6.11

Average Size of the Farm Holding

(Area in acres)Size groups

Land Ownership Marginal Small

Semi-Medium

Medium LargeTotal

Total owned land

1.72 3.41 5.74 11.2 26.33 5.37

Total leased in Land

0 0 0.29 1.52 7.83 0.47

Total leased outLand

0 0.02 0 0 0 0.01

Average operated area

1.72 3.39 6.04 12.72 34.17 5.83

Source: Primary data

174

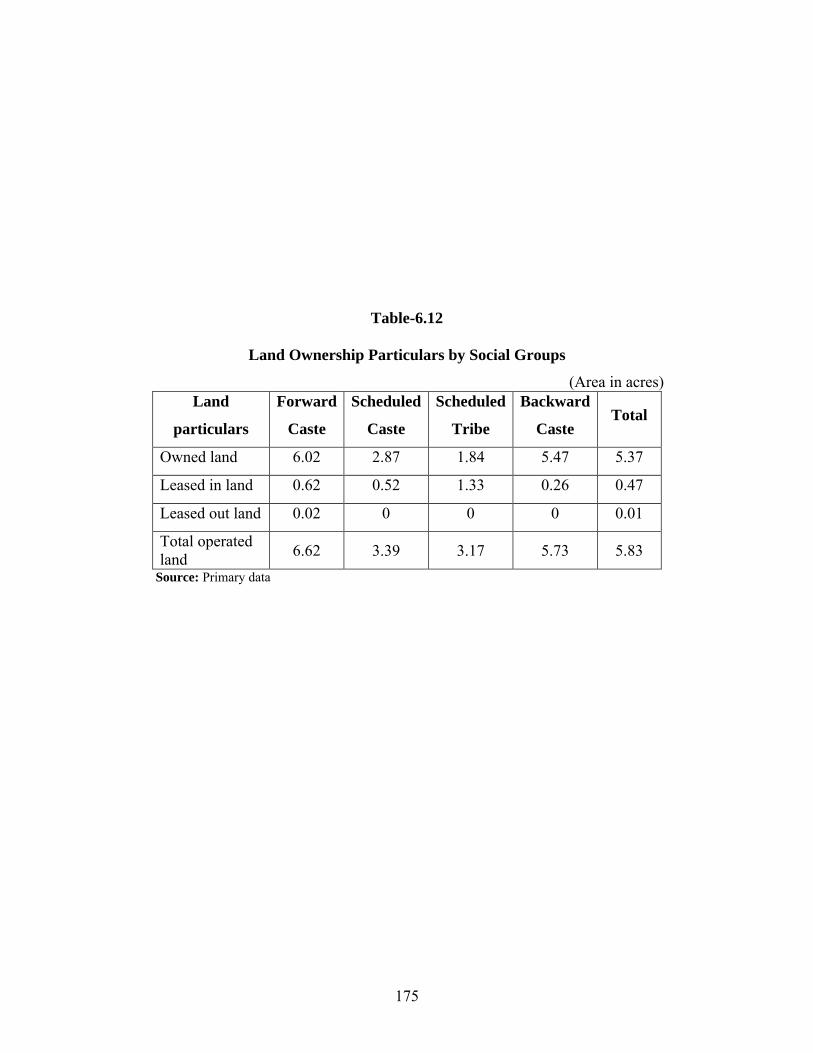

6.12 Land Ownership Particulars by Social Groups

Majority of the people living in dryland regions earn livelihood from

cultivation. The necessary conditions for improving standard of living of the

people living on agriculture is, just and rational distribution of land among

different categories of people. The distribution of lands among different social

groups is presented in table-6.12. Farmers are divided as per social category,

namely Forward Caste (FC), Scheduled Caste (SC), Scheduled Tribes (ST) and

Backward Caste (BC) to identify the relation between social status and land

ownership. The distribution of farm households as per social category shows that

the average size of land owned by forward caste is 6.02 acres (90.94 per cent),

while their average leased in land and leased out land sizes respectively are 0.62

acres and 0.30 acres (9.37 and 0.30 per cent). The average size of land owned by

Scheduled Caste is 2.87 acres and their average size of leased in land is 0.52

acres. The average owned land among Schedule Tribes and Backward Castes are

1.84 acres and 5.47 acres respectively. Further some of the Scheduled Tribes and

Backward Castes have leased in land of 1.33 acres and 0.26 acres respectively.

There is a close relation between farm size and social hierarchy.

6.13 Cropping Pattern of the Sample Households

The shift in cropping pattern of the sample households in a period of ten

years is presented in table-6.13. As shown in the table, there is no significant shift

in the area under different crops. Ten years ago, the largest average cropped area

found to be of groundnut, while it is shifted to sunflower in the current year. The

average cropped areas of chillies, castor, cotton and groundnut have also

decreased. The average area under pulses has also declined during the ten years

period. It is also to be noted that the average cropped areas of jowar and

sunflower crops have declined. Further, it can also be said that this decline in

cropped areas has occurred in order to reduce the investment on crops as the

financial status of the farm households in the study areas is at stake due to drought

conditions.

175

Table-6.12

Land Ownership Particulars by Social Groups

(Area in acres)Land

particulars

Forward

Caste

Scheduled

Caste

Scheduled

Tribe

Backward

CasteTotal

Owned land 6.02 2.87 1.84 5.47 5.37

Leased in land 0.62 0.52 1.33 0.26 0.47

Leased out land 0.02 0 0 0 0.01

Total operated land

6.62 3.39 3.17 5.73 5.83

Source: Primary data

176

Table- 6.13

Shift in Cropping Pattern in the Sample Households during the last Ten Years

(Area in Acres)

Source: primary data

Current year area Ten years back Area

CropsMarginal Small

Semi-Medium

Medium Large Total Marginal SmallSemi-

MediumMedium Large Total

Cotton1.48 2.31 2.66 5.58 5.5 2.65 1.78 2.75 3.80 4.00 13.00 3.47

Redgram1.21 1.93 3.02 4.5 10.3 2.72 1.71 2.57 3.68 5.56 9.00 3.25

Chillies1.00 1.33 1.46 2.00 1.00 1.54 0.00 0.00 2.50 0.00 0.00 2.50

Green-Gram 1.06 2.01 2.67 5.86 0 2.63 1.50 2.57 3.58 5.5 0 3.28

Groundnut2.91 2.86 3.27 3.87 2.57 3.21 1.90 3.29 5.19 10.31 18.33 5.93

Jowar1.88 2.30 3.02 6.87 7.67 4.04 1.90 2.33 3.53 5.82 6.5 3.92

Sunflower1.00 1.00 3.29 5.05 6.00 4.11 0 0 3.00 5.00 5.00 3.50

Castor1.00 1.00 2.80 2.88 0.00 2.50 0.00 2.00 0.00 2.00 0.00 2.00

177

It is also to be noted that the farmers have shifted their crops to sunflower,

which is a low investment crop, from groundnut, chillies and cotton, which are

high investment crops.

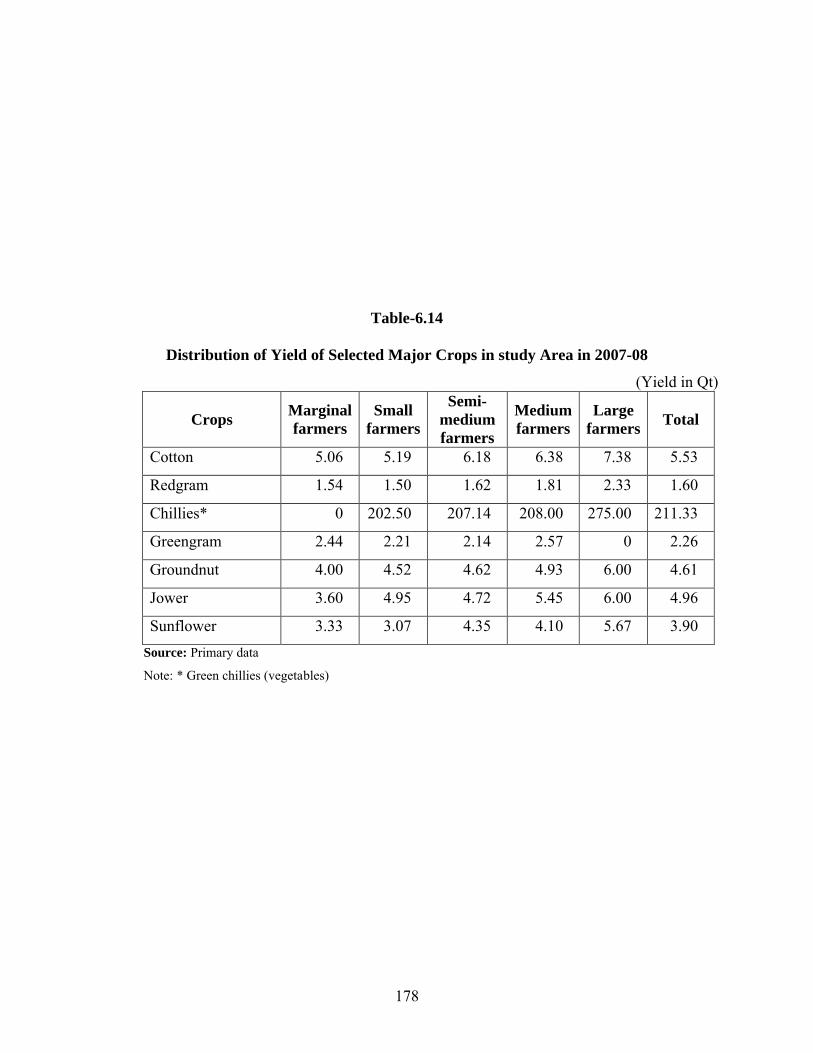

6.14 Distribution of Yields of Selected Major Crops (1998-1999 to 2008-

2009)

An observation is made in respect of yields of major crops in the selected

areas during the decade. The statistics displayed in tables-6.14 and 6.14(a) clearly

show that there is a significant decline in the yields of major crops during the ten

years period. The rate of decline varies across the size groups. The declining

yields indicate the declining productive capacity of land. Land degradation is

found to be the major contributing factor for declining yields. The data on crop

yield in two periods clearly reveals a direct relation between ten years yield and

farm size. Per acre yield of major crop increases with farm size in both periods

6.15 Source of Credit

In the dryland cultivation, agricultural credit assumes more importance

when compared to other irrigated farming. Limited availability of money for

farmers to save does not allow them to finance farm expenses. Though private

agencies play an exploitative role, credit through institutional channels is the only

way to break agricultural stagnation in dryland regions

So the farmers depend on loan to meet the costs in raising the crops.

Farmers are engaged in cultivation to make profit out of capital by investing on

land and extracting surplus value from work, but as a means of self-employment

and family maintenance, typically, a farmer in India, particularly in dryland

regions would still be the owner cultivator, who mainly cultivates land with

family labour. The returns they get from land in a large measure are a response of

their family labour expected in the production process. However, since cultivation

needs cash investments, farmers have to borrow money to carry out the

agricultural activities, either from government or from cooperative institution or

from private money lenders

178

Table-6.14

Distribution of Yield of Selected Major Crops in study Area in 2007-08

(Yield in Qt)

CropsMarginal farmers

Small farmers

Semi-medium farmers

Medium farmers

Large farmers

Total

Cotton 5.06 5.19 6.18 6.38 7.38 5.53

Redgram 1.54 1.50 1.62 1.81 2.33 1.60

Chillies* 0 202.50 207.14 208.00 275.00 211.33

Greengram 2.44 2.21 2.14 2.57 0 2.26

Groundnut 4.00 4.52 4.62 4.93 6.00 4.61

Jower 3.60 4.95 4.72 5.45 6.00 4.96

Sunflower 3.33 3.07 4.35 4.10 5.67 3.90

Source: Primary data

Note: * Green chillies (vegetables)

179

Table-6.14 (a)

Ten Years Back Yield

(Yield in Qt)

CropsMarginal farmers

Small farmers

Semi-medium farmers

Medium farmers

Large farmers

Total

Cotton 5.89 6.20 7.20 6.33 5.00 6.21

Redgram 2.82 3.22 3.20 3.19 4.50 3.17

Chillies* 0 0 275.00 0 0 275.00

Greengram 2.40 1.92 2.54 2.50 0 2.26

Groundnut 4.20 4.82 4.44 4.93 6.33 4.66

Jowar 2.80 3.30 3.21 3.50 4.00 3.31

Sunflower 0 0 5.00 3.00 5.00 4.33

Source: Primary dataNote : * Green chillies (vegetables)

180

It should be kept in mind that unlike other professions and occupations,

farmers do not receive their income on a daily or weekly or monthly basis.

Income for them comes only at the end of the crop season. So, farmers borrow

money not only to meet the cultivation expenses, but also to meet their

consumption and family needs. It is also difficult to demarcate clearly the loans

taken by farmers as the ones taken for cultivation purpose and family needs, as

they may spend the loan amount on both, as the situation demands.

The credit requirements of the farms are met by obtaining loans from

institutional and non- institutional agencies. Institutional agencies particularly that

provide loan to farmers are banks, cooperative societies and bank sponsored self

help groups. The non institutional agencies include commission agents, input

dealers, money lenders and others. The distribution of farms by source wise credit

is presented in the table 6.15.

The credit made available through banks and co-operative societies is

found to be main component in the study area. Nearly 75 per cent of farm

households found to have access to bank credit. Nearly 10 per cent of the farm

households who do not have access to bank credit are getting loan from self-help

groups. Nearly 80 per cent of marginal and small farm households, 84 per cent of

semi-medium farm households, 81 per cent of medium farms and 83 per cent of

large farm households will borrow loans from banks. The role of co-operative

societies found to be very limited in meeting the credit requirements of the farms.

Inspite of institutional support in meeting the credit needs of the farms in the

study area, the non-institutional sources of farm credit are found to be very

important in the composition of total credit needs of the farm households. Nearly

54 per cent of the farm households are depending on non-institutional sources also

to meet their total credit requirements.

181

Table- 6.15

Source wise Distribution of Debt Holders by size groups (Current year)

Marginal farmers

Small farmersSemi-medium

farmersMedium farmers

Large farmers TotalSource of Credit

No % to

the totalNo

% to the total

No % to

the totalNo

% to the total

No % to the

totalNo

% to the total

Banks 49 72.06 99 75.00 53 80.30 21 75.00 5 83.33 227 75.67Co-operative societies 4 5.88 7 5.30 6 9.09 1 3.57 3 50.00 21 7.00SHGs 9 13.24 14 10.61 6 9.09 3 10.71 0.00 32 10.67Institutional (A) 50 73.53 105 79.55 55 83.33 21 75.00 6 100.00 237 79.00Commission agent 0.00 1 0.76 1 1.52 0.00 0.00 2 0.67Input dealers 8 11.76 19 14.39 8 12.12 4 14.29 2 33.33 41 13.67Money lenders 22 32.35 59 44.70 31 46.97 13 46.43 3 50.00 128 42.67Friends and others 2 2.94 0.00 1 1.52 0.00 0.00 3 1.00Non institutional (B) 31 45.59 74 56.06 37 56.06 17 60.71 4 66.67 163 54.33Total current year Debt (A+B) 61 89.71 124 93.94 63 95.45 26 92.86 6 100.00 280 93.33Source: Primary data Note: Per cent to respective size groups.

182

Further, it is found that irrespective of the farm size, the proportions of

farm households borrowing from non institutional sources are same. The

institutional agencies are not able to meet the credit requirements of the farmers.

The farmers in the study area are borrowing loan from money lenders,

commission agents and input dealers at high interest rates.

6.16 Amount Borrowed from Different Sources

The average loan amount borrowed by farm households from different

sources is presented in the table-6.16. The loan which is borrowed from banks on

an average is Rs 6632/- per acre. For marginal farms it is Rs 8357/- per acre and

Rs 2264 per acre for large farms. That is, per acre average credit by banks is

decreasing when farm size is increasing. Farmer who has availed credit from co-

operative society has got Rs 8780/- per acre and small farmers have borrowed Rs

4430/- per acre. The marginal farms who have availed loan from non-institutional

agencies have received Rs 11316/- per acre, while it is Rs 8646/- in case of small

farms, Rs 4352/- in case of semi-medium farms, Rs. 2408/- in case of medium

farms and Rs. 1696/- per acre in case of large farms. Per acre credit from non-

institutional sources is higher among small and marginal farms. Per acre loan

from both institutional and non institutional sources is found to be Rs 10825/- per

acre. The loan borrowed per acre is found to be increasing with the decreasing

farm size. The small and marginal farms need credit to meet their family

expenditure also when they work in their farms. So per acre credit might be

increasing with the decreasing in farm size.

Return to cultivation and absence of non-farm opportunities are said to be

the indication of the larger socio- economic analysis of dryland cultivation. This

will alienated by multiple risks like, income, yield, price and credit among others.

This has led to the incidence of indebtedness among farm households.

183

Table-6.16

Source wise Average Loan Amount per acre by Faming Category (Current year)

(In rupees)Size Groups

Source Marginal farmers

Small farmers

Semi-medium farmers

Medium farmers

Large farmers

Total

Banks 8357 6926 5730 4544 2264 6632

Co-operative societies 10000 17297 2870 2083 1335 8780

SHGs 6480 4109 3543 1551 0 4430

Total Institutional 10156 8231 6221 4865 2554 7729

Commission agent 0 1660 700 0 0 1180

Input dealers 4479 3808 1981 998 1131 3178

Money lenders 12817 9590 4640 2842 1508 8071

Friends and others 16500 0 625 0 0 11208

Total Non-institutional

11316 8646 4352 2408 1696 7358

Total current debt 14075 12129 7987 5504 3685 10825

Source: Primary data

184

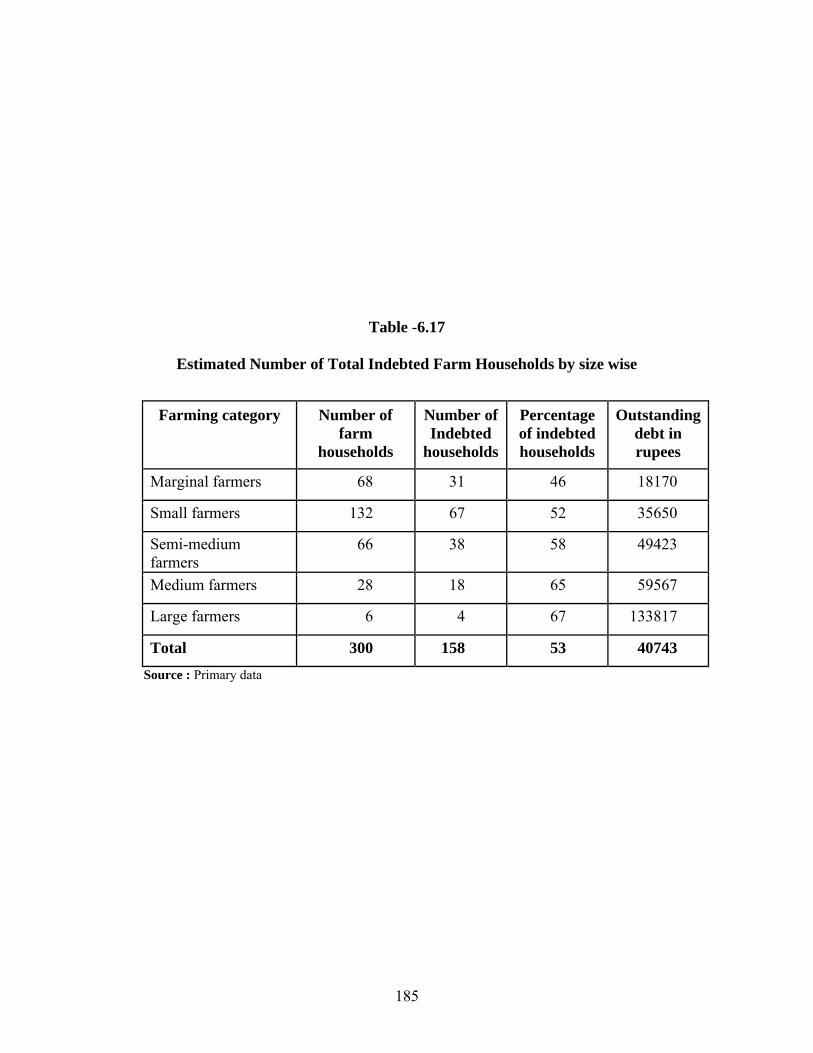

6.17 Indebtedness among Farm Households

The indebtedness among farm households is the indication of distress in

dryland cultivation. The outstanding debt of the farm households by size wise and

source wise is presented in the table-6.17. A farmer gets income from cultivation,

farming other than cultivation, other agricultural activities, wage employment,

non-farm employment, pension and other sources. A farm household is

considered to be indebted if he could not repay the loan out of the total receipts

from all sources of income at the end of the agricultural year.

The indebtedness of farm households is presented in the table. Out of 300

farm households, 80 per cent are reported to be indebted. The prevalence of

indebtedness is increasing with the farm size. The percentage of indebted farm

households is high among large and medium farms. About 46 per cent of the

marginal, 52 per cent of small, 58 per cent of semi-medium, 65 per cent of

medium, 67 per cent of large farms are reported to be indebted. A farm household

on an average reported to be indebted an amount of Rs 40743/-. Average

outstanding debt among marginal, small, semi-medium, medium and large farms

are found to be Rs 18120/-, 35650/-, Rs 49423/-, Rs 59567/- and Rs 133817/-

respectively. Farmers have reported that they are repaying the loans taken from

banks, cooperatives societies and self-help groups at the end of the year by

borrowing from other non-institutional sources. So this credit limits gets

enhanced. It leads to a situation that debt gets accumulated over the years. Thus

the debt brings out situation of debt trap among farm households. This clearly

reveals the stress conditions of households

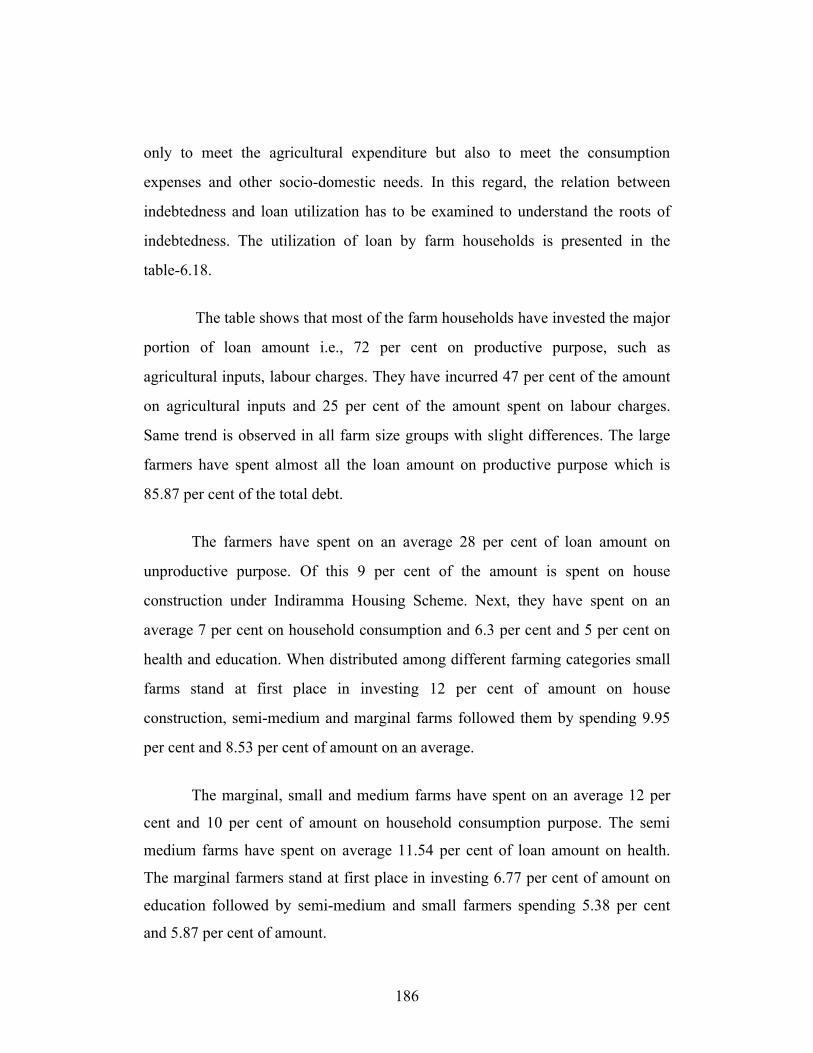

6.18 Utilization of Loan Amount

The main purpose of agricultural loan is to meet the expenses in crop

cultivation. The farmers get income only at the end of crop season. As there is no

other main source of income other than agriculture, the farmers borrow money not

185

Table -6.17

Estimated Number of Total Indebted Farm Households by size wise

Farming category Number of farm

households

Number of Indebted

households

Percentage of indebted households

Outstanding debt in rupees

Marginal farmers 68 31 46 18170

Small farmers 132 67 52 35650

Semi-medium farmers

66 38 58 49423

Medium farmers 28 18 65 59567

Large farmers 6 4 67 133817

Total 300 158 53 40743

Source : Primary data

186

only to meet the agricultural expenditure but also to meet the consumption

expenses and other socio-domestic needs. In this regard, the relation between

indebtedness and loan utilization has to be examined to understand the roots of

indebtedness. The utilization of loan by farm households is presented in the

table-6.18.

The table shows that most of the farm households have invested the major

portion of loan amount i.e., 72 per cent on productive purpose, such as

agricultural inputs, labour charges. They have incurred 47 per cent of the amount

on agricultural inputs and 25 per cent of the amount spent on labour charges.

Same trend is observed in all farm size groups with slight differences. The large

farmers have spent almost all the loan amount on productive purpose which is

85.87 per cent of the total debt.

The farmers have spent on an average 28 per cent of loan amount on

unproductive purpose. Of this 9 per cent of the amount is spent on house

construction under Indiramma Housing Scheme. Next, they have spent on an

average 7 per cent on household consumption and 6.3 per cent and 5 per cent on

health and education. When distributed among different farming categories small

farms stand at first place in investing 12 per cent of amount on house

construction, semi-medium and marginal farms followed them by spending 9.95

per cent and 8.53 per cent of amount on an average.

The marginal, small and medium farms have spent on an average 12 per

cent and 10 per cent of amount on household consumption purpose. The semi

medium farms have spent on average 11.54 per cent of loan amount on health.

The marginal farmers stand at first place in investing 6.77 per cent of amount on

education followed by semi-medium and small farmers spending 5.38 per cent

and 5.87 per cent of amount.

187

Table-6.18

Utilization of Loan Amount

(Percentage)Size Groups

Different Uses Marginal farmers

Small farmers

Semi-medium farmers

Medium farmers

Large farmers

Total

Agricultural inputs 46.75 42.9 39.68 52.8 55.87 47.00Labour charges 20.46 20.82 25.73 24.38 30 25.00Productive purposes 67.21 63.72 65.41 77.18 85.87 72.00Health 3.35 4.98 11.54 2.22 2.86 6.31Education 6.77 5.38 5.87 1.31 2.17 5.00Marriage/ rituals 2.14 3.07 2.23 2.00 0.00 0.70House construction expenses 8.53 12.85 9.95 7.3 9.1 9.00House hold consumption 12.00 10.00 5.00 10.00 0.00 7.00Un productive purpose 32.79 36.28 34.59 22.83 14.13 28.00Total 100.00 100.00 100.00 100.00 100.00 100.00Source: Primary data

188

It is observed that 72 per cent of farm households have invested amount

borrowed, on productive purpose and 28 per cent of them have invested on

unproductive purpose. The data clearly reveals that the indebtedness among farm

households is due to un-productive consumption like social ceremonies, marriages

and other religious ceremonies

6.19 Average Monthly Income of the Respondents

The average total monthly income of the households across farm size

groups is presented in the table-6.19. The average monthly income is Rs. 3,171/-

(annual income of Rs.3,80,491/-). The table reveals that among the different

sources consider, income from the hiring out labour is the most important source

of income for farm household. In the study area, average monthly income from

cultivation is Rs.419/-, while the monthly income from the hiring out of labour is

Rs.881/- Income for farm household from hiring out machinery and drought

animals is Rs.425/-. Income generated from non-farm business is Rs. 843/- and

income from dairy and poultry is Rs. 423/-. However there is a large difference in

the total income across the size groups of farm households. The total income for

marginal and small farms was much lower than that for the other size groups.

Income from cultivation for marginal and small farm households is found to be

very low. The share of monthly income from cultivation in total income is much

lower among marginal, small and semi-medium farm households than that of the

other size groups. The above analysis clearly reveals that the income from

cultivation is not sufficient to meet all the basic necessities of the family. From

cultivation an average household gets a net income of Rs.419/- (on annual income

of Rs. 5031/-). In order to cross poverty line, one household needs more than Rs.

20000/-. Incomes of marginal and small farms from cultivation are found to be

much lower than that of the average farm household consumption accounting for

58 per cent and the remaining 27 per cent of the expenditure is spent on non-food

expenditure.

189

Table-6.19

Average Monthly Income from the Agriculture and Allied and Off- farm

Activities of the Farm Households

(In rupees)Source of Income Marginal

FarmersSmall

farmersSemi-

medium farmers

Medium farmers

Large farmers

Total

Agriculture. A 38 310 646 865 2574 419

Income from Dairy and Poultry

226 443 499 491 1083 423

Income from Machinery and Drought labour

116 294 611 994 2111 425

Income from Hiring out of labour

1100 983 650 527 347 881

Income from other than Agriculture

152 197 182 148 192 179

Agriculture and allied. B 1595 1917 1942 2160 3733 1908

Income from Off-Farm activities. C

610 602 1484 1036 833 843

Total Income (A+B+C) 2243 2829 4072 4061 7141 3171

Source: Primary data

190

Many of the households depend on wage and non-farm business to

augment their incomes even though incomes may not be sufficient to meet basic

necessities including health and education. The monthly average farmer

household expenditure is Rs. 5525/- the average monthly income of the farmer is

Rs.3171/- which indicates that the income received is not sufficient to meet the

minimum family needs.

6.20 Average Monthly Household Expenditure

Income and proportion of income spent on consumption are indicators that

are used in poverty and consumption studies. The monthly consumption

expenditure here refers to food items like cereal and cereals products, pulses,

edible oil, milk, curd and other milk products, eggs, fish, meat, vegetables and

fruits, sugar, salt and other spices, and other food items. The non-food items like

education, medical, clothing’, soaps, detergents, toothpaste and other cosmetics,

electricity, liquor, pan and tobacco, fuel and lighting, telephone, consumer

durables, rent, and other miscellaneous goods and services. This is the

consumption expenditure which measures the standard of living. The average

consumption expenditure of different size groups are presented in the table-6.20.

Farmers find it difficult to meet their consumption needs from their income. Some

of them have to borrow or spend less time of flow returns from cultivation. The

consumption expenditure in cases of marginal and small farms is found to be

bellowing their income. In a normal crop year with no emergent expenses coming

in between, the small farmers should be in a position to save a little. The medium

farmers will normally have some surplus after meeting the family expenses. The

large farmers will be in a position to save a considerable part of the income. The

table shows that the large share of monthly per capita expenditure goes for food

consumption accounting for 58 per cent and the remaining 27 per cent of the

expenditure is spent on non-food expenditure.

191

Table-6.20

Average Monthly Expenditure of the Farm Households

(In rupees)Farming category

Total Food Expenditure

Total Non-Food

Expenditure

Medical Education Liquor and

Tobacco

Total expenditure

2515 1157 148 165 114 4099Marginal farmers (61.36) (28.23) (3.61) (4.03) (2.78) (100.00)

3009 1350 150 361 199 5069Small farmers (59.36) (26.63) (2.96) (7.12) (3.93) (100.00)

3396 1659 174 1030 234 6493Semi-medium farmers

(52.30) (25.55) (2.68) (15.86) (3.60) (100.00)

4495 1904 221 875 254 7749Medium farmers (58.01) (24.57) (2.85) (11.29) (3.28) (100.00)

6333 2392 200 1667 117 10708Large farmers (59.14) (22.34) (1.87) (15.57) (1.09) (100.00)

3187 1447 163 538 191 5525Total(57.68) (26.19) (2.95) (9.74) (3.46)) (100.00)

Source: Primary dataNote: Figures in the parentheses indicate the percentage to the total expenditure

192

The lions share of non- food expenditure is nearly 10 per cent which is

spent on education and 3.5 per cent expenditure is spent on liquor, pan and

tobacco and the remaining percentage of among is spent on medical expenses.

The expenditure on non food items has increased during recent years. This

expenditure on non-food expenditure is essential now-a-days. The expenditure on

medical and education purposes has become essential expenditure. Farm

households are found to be struggling hard to meet the consumption expenditure

out of cultivation. This leads to the conclusion that the monthly consumption

expenditure is greater than the monthly realized income and food taking the lion’s

share of expenditure. This is a greater probability for households to consuming

less than the recommended minimum nutrition intake levels. Though the monthly

per capita consumption expenditure is increasing with the size of the land

possessed, family size also found to be increasing with the size of the land

possessed. i.e., even large and medium farm households are consuming less than

the recommended minimum intake levels in the study area.

To sum up, the above analysis of the socio-economic dimensions of

dryland farmers reveal that socio-economic conditions of the farm households are

poor in the study area. The socio-economic structure does not have any direct

influence on the cultivation. From the analysis it is clearly evident that 47 per cent

of the farmers belong to backward caste, 39.67 per cent of farm households

belong to forward caste and 13.33 per cent are scheduled caste and scheduled

tribes communities.

The data on family system clearly reveals that 60 per cent of the families

are nuclear families. The average size of the family of the total farm households is

4.87. Among all farming categories the average family size of large farms is high,

which is ‘7.50, while the overall average size among the family is small for

marginal and small farms when compared with other farmers.

193

Distribution of farm households by the housing status across size groups

reveals that 55 per cent, 47 per cent, 32 per cent, 16.67 per cent of marginal,

small, semi-medium, medium and large farm households are living in katcha

houses. Thus the data on housing clearly indicates the poor living conditions of

farm households. The data on civic amenities reveals that 69.67 per cent of the

households are depending on public tap or public hand pumps for drinking water.

Only 15.33 per cent of the households have drainage facility. Nearly 70 per cent

of the dryland farmers do not have LPG gas. They depend on firewood for

cooking. The data further reveals that T.V and electric fan have become important

consumer goods.

The data on literacy reveals that 57 per cent of farm households are

illiterates which shows that the literacy rate is low when compared to overall state

rural population literacy, which is 47 per cent. The occupation structure of the

farm households reveals that for 94.34 per cent of farm households cultivation is

the main occupation. Nearly 66.33 per cent of farm households have agricultural

wage labour as the subsidiary occupation. Dryland farm households do not

possess large number of cattle due to the fact that livestock enterprise might not

be a variable often for them because they don’t get fodder throughout the year.

Thus there is direct relation between values of assets and farm size. Land as a

productive asset constitutes the major component of asset for dryland farmer.

The average size of the dryland farms in the study area is 5.37 acres.

Semi- medium, medium and large farms have leased in lands. The data on leased

in and leased out land reveals that tenancy is not present much in the study area.

The distribution of land among different social categories reveals that there is

close relation between farm size and social hierarchy.

194

It can also be said that this decline in cropped areas has occurred in order

to reduce the investment on crops as the financial status of the farm households in

the study areas is at stake due to drought conditions. It is also to be noted the

farmers have shifted their crops to sunflower, a low investment crops from

groundnut, chillies and cotton, which are high investment crops.

Nearly 75 per cent of farm households found to have access to bank credit.

Nearly 54 per cent of the farm households depend on non institutional sources

also to meet their total credit requirements. It is found that irrespective of the farm

size, the proportion of farm households borrowing from non institutional sources

is same. The institutional agencies are not able to meet the credit requirements of

the farmers. The farmers in the study area are borrowing loan from money lenders

or commission agents or input dealers at high interest rates.

The per acre loan borrowed is found to be increasing with the decreasing

farm size. The small and marginal farms need credit to meet their family

expenditure when they work in their farms. So per acre credit might be increasing

with decreasing in farm size. Indebtedness among farm households reveals that 80

per cent of farm households are reported to be indebted. Average outstanding debt

among marginal, small, semi-medium, medium and large farms are found to be

Rs 18,120/-, Rs. 35,650/-, Rs. 49,423/-, Rs. 59,567/- and Rs. 1,33,817/-

respectively. It leads to a situation that debt gets accumulated over the year. Thus

the debt brings out situation of debt trap among farm households. This clearly

reveals the stress conditions of households. It is observed that 72 per cent of farm

households have invested amount borrowed on productive purpose and 28 per

cent of them have invested on unproductive purpose. The data clearly reveals the

indebtedness among farm households due to unproductive consumption like

social ceremonies, marriages and other religious ceremonies.

195

The above analysis clearly reveals that the income from cultivation is not

sufficient to meet all the basic necessities of the families. From cultivation an

average household gets a net income of Rs.419/- (an annual income of Rs. 5,031).

One household needs more than Rs. 20,000/- in order to cross poverty line.

Incomes of marginal and small farms from cultivation are found to be much lower

than the average income of farm household. Many of the households depend on

wage and non-farm business to augment their incomes. Even these incomes may

not be sufficient to meet basic necessities including health and education. While

the monthly average farmer household expenditure is Rs. 5,525/- the average

monthly farmer income is Rs.3,171/- which indicates that the income reveals that

the income received is not sufficient to meet the minimum family needs; that the

monthly consumption expenditure is greater than the monthly realized income and

food taking the lion’s share of expenditure. This is a greater probability for

households to consuming less than the recommended minimum nutrition intake

levels. Though the monthly per capita consumption expenditure is increasing with

the size of the land possessed family size also found to be increasing with the size

of the land possessed. i.e., even large and medium farm households consuming

less than the recommended minimum intake levels in the study area.