CHAPTER 18

Buying Plant Assets and Paying Property Tax

2

18-1 BUYING PLANT ASSETS AND PAYING PROPERTY TAX

Assets have two categories:Current: Assets that will expected to be consumed within a year. Ex: cash, supplies, etc.Plant: Assets that will be used for a number of years in the operation of the business. Ex: Cash registers, buildings, etc.

Three major categories of plant assets:1) Equipment2) Land3) Buildings

Buying a plant asset is similar to buying a current asset like supplies.

3

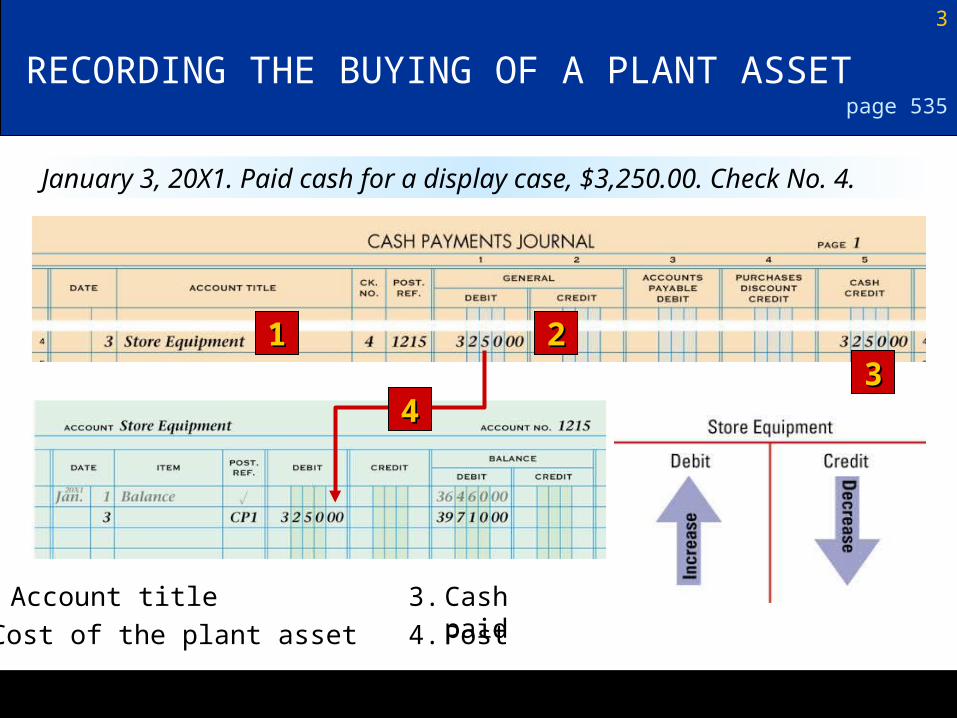

RECORDING THE BUYING OF A PLANT ASSET

11 2233

page 535

January 3, 20X1. Paid cash for a display case, $3,250.00. Check No. 4.

3. Cash paid

44

2. Cost of the plant asset

1. Account title

4. Post

4

CALCULATING AND PAYING PROPERTY TAXpage 536

February 1. Classic Parts, Inc., paid cash for property tax, $720.00. Check No. 69.

AnnualProperty Tax

=Tax Rate×Assessed

Value$720.00=1.2%×$60,000.00

State and federal governments define two types of property - Real is land an anything attached (real estate), personal is anything that is not real property. Assessors determine the assessed value of the property.

LESSON 18-2 CALCULATING DEPRECIATION EXPENSE

Plant assets are expected to be used over several years. The costof a plant asset is expensed over the useful life of the asset.

There are several methods to calculate depreciation. One popular method id the straight-line method.

6

EstimatedSalvage Value

OriginalCost

Estimated TotalDepreciation

Expense

=–

$3,000.00

AnnualDepreciation

Expense

=Years of EstimatedUseful Life

÷Estimated Total

Depreciation Expense

$600.00

$250.00$3,250.00

STRAIGHT-LINE DEPRECIATION

Calculating Annual Depreciation Expense

11

page 538

=–

=5÷$3,000.00

1. Subtract the asset’s estimated salvage value from the original cost.

2. Divide the estimated total depreciation expense by the years of estimated useful life.

22

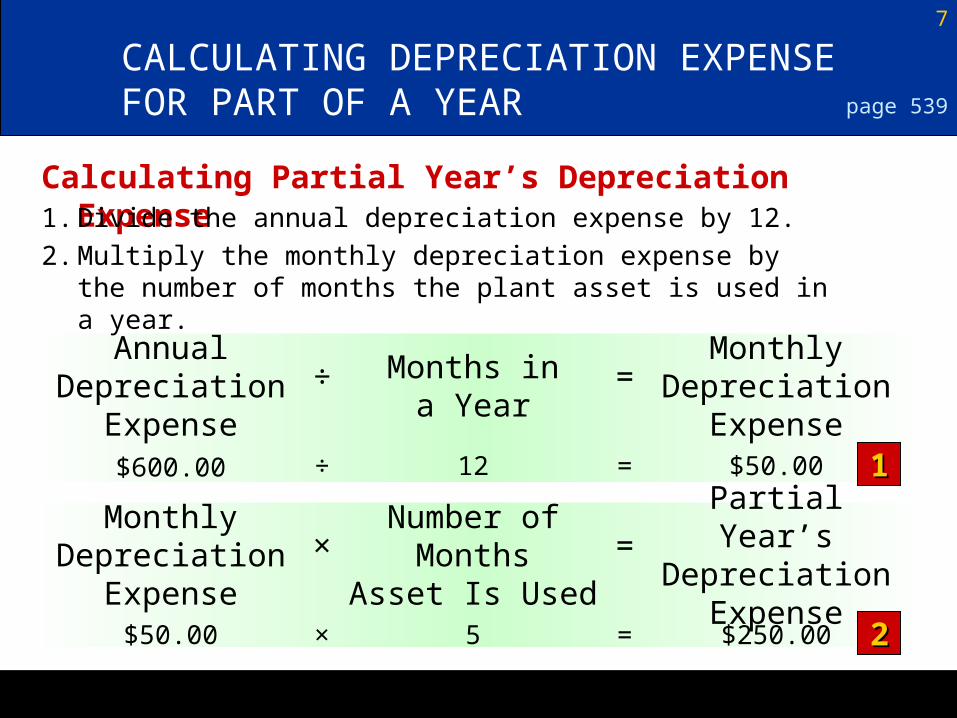

7

Months ina Year

AnnualDepreciation

Expense

MonthlyDepreciation

Expense

=÷

$50.00

Partial Year’sDepreciation

Expense

=Number of MonthsAsset Is Used

×Monthly

Depreciation Expense

$250.00

12$600.00

CALCULATING DEPRECIATION EXPENSE FOR PART OF A YEAR

Calculating Partial Year’s Depreciation Expense

11

page 539

=÷

=5×$50.00

1. Divide the annual depreciation expense by 12.

2. Multiply the monthly depreciation expense by the number of months the plant asset is used in a year.

22

8

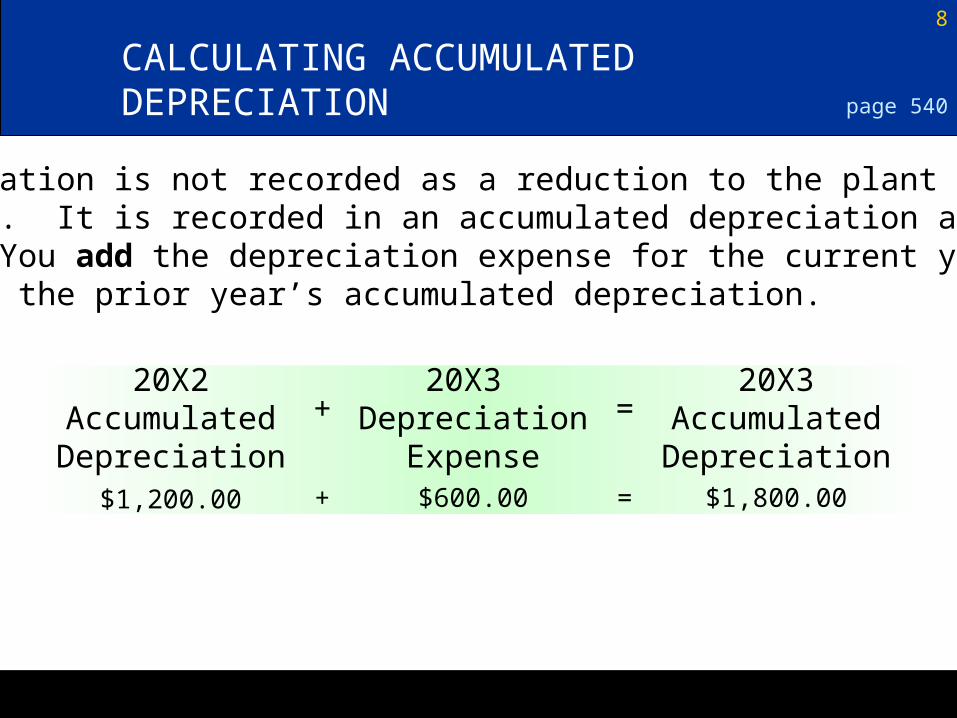

CALCULATING ACCUMULATED DEPRECIATION page 540

20X3 Depreciation

Expense

20X2 AccumulatedDepreciation

20X3 AccumulatedDepreciation

=+

$1,800.00$600.00$1,200.00 =+

Depreciation is not recorded as a reduction to the plant assetaccount. It is recorded in an accumulated depreciation account.

- You add the depreciation expense for the current yearto the prior year’s accumulated depreciation.

9

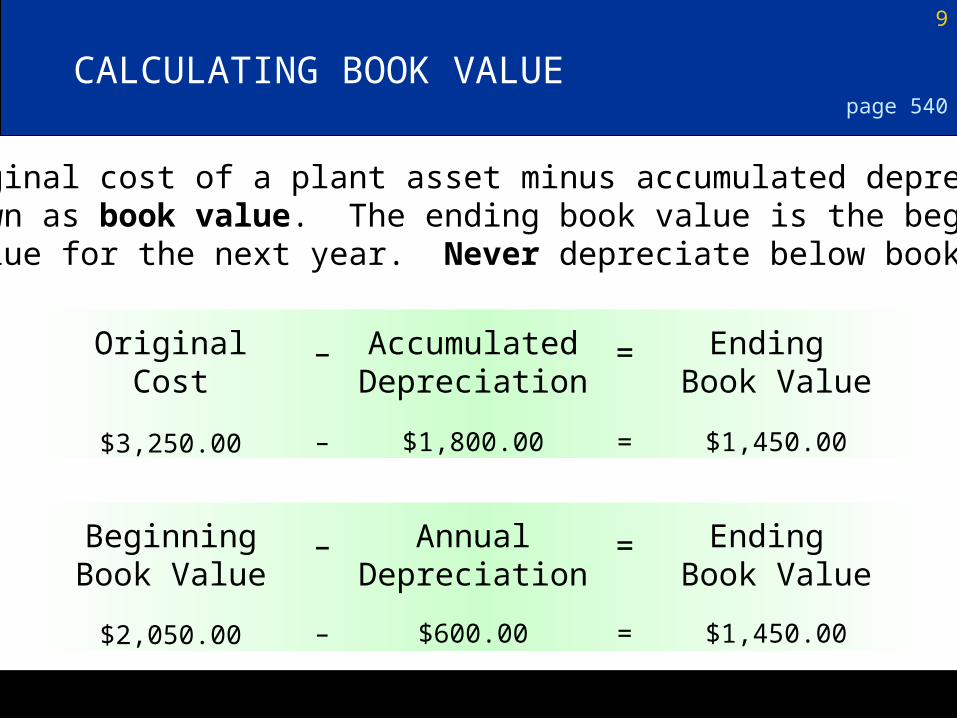

CALCULATING BOOK VALUEpage 540

AccumulatedDepreciation

OriginalCost

Ending Book Value

=–

$1,450.00$1,800.00$3,250.00 =–

AnnualDepreciation

BeginningBook Value

Ending Book Value

=–

$1,450.00$600.00$2,050.00 =–

The original cost of a plant asset minus accumulated depreciation is known as book value. The ending book value is the beginningbook value for the next year. Never depreciate below book value.

10

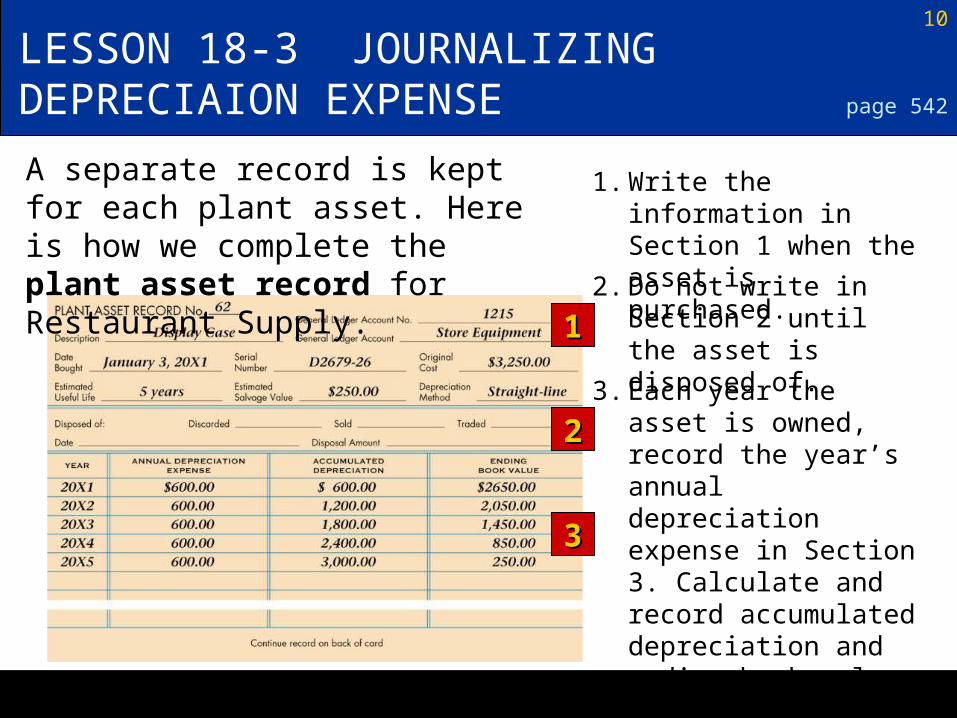

3. Each year the asset is owned, record the year’s annual depreciation expense in Section 3. Calculate and record accumulated depreciation and ending book value.

11

22

33

page 542

2. Do not write in Section 2 until the asset is disposed of.

1. Write the information in Section 1 when the asset is purchased.

LESSON 18-3 JOURNALIZING DEPRECIAION EXPENSE

A separate record is kept for each plant asset. Here is how we complete the plant asset record for Restaurant Supply.

11

JOURNALIZING ANNUAL DEPRECIATION EXPENSE page 543

3. Record adjusting entry

2. Accumulated Depreciation credit

1. Depreciation Expense debit

11

3333

22

12

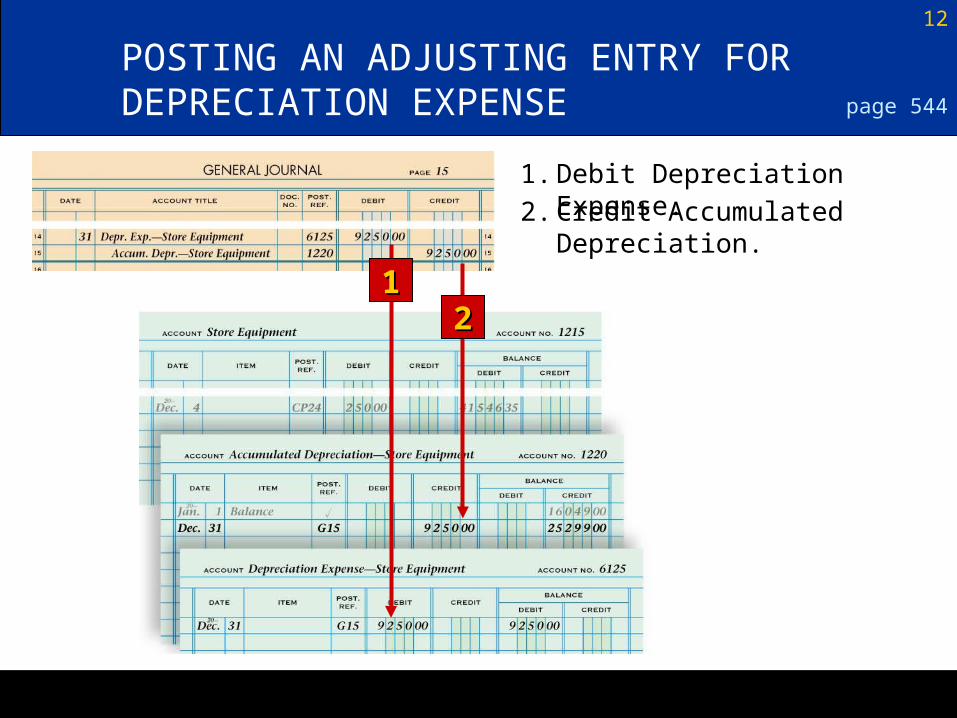

POSTING AN ADJUSTING ENTRY FOR DEPRECIATION EXPENSE

1. Debit Depreciation Expense.

page 544

2. Credit Accumulated Depreciation.

1122

LESSON 18-4 DISPOSING OF PLANT ASSETS

When a plant asset is no longer useful to a business, the asset may bedisposed of. The old plant asset may be sold, traded, for a new assets, or discarded.

A plant asset may be sold at any time during the asset’s useful life.when a plant asset is sold, its depreciation from the beginning of thecurrent fiscal year to the date of the disposal must be recorded.

Revenue that results when a plant asset is sold for more than bookvalue is called gain on plant assets.

The loss that results when a plant asset is sold for less than book value is called loss on plant assets.

14

SALE OF A PLANT ASSET FOR BOOK VALUE

1. Record an entry in the cash receipts journal to remove the original cost.

page 546

January 6, 20X6. Received cash from sale of display case, $250.00: original cost, $3,250.00; total accumulated depreciation through December 31, 20X5, $3,000.00. Receipt No. 4.

2. Check the type of disposal, and write the date, and disposal amount in Section 2 of the plant asset record.

11

22

15

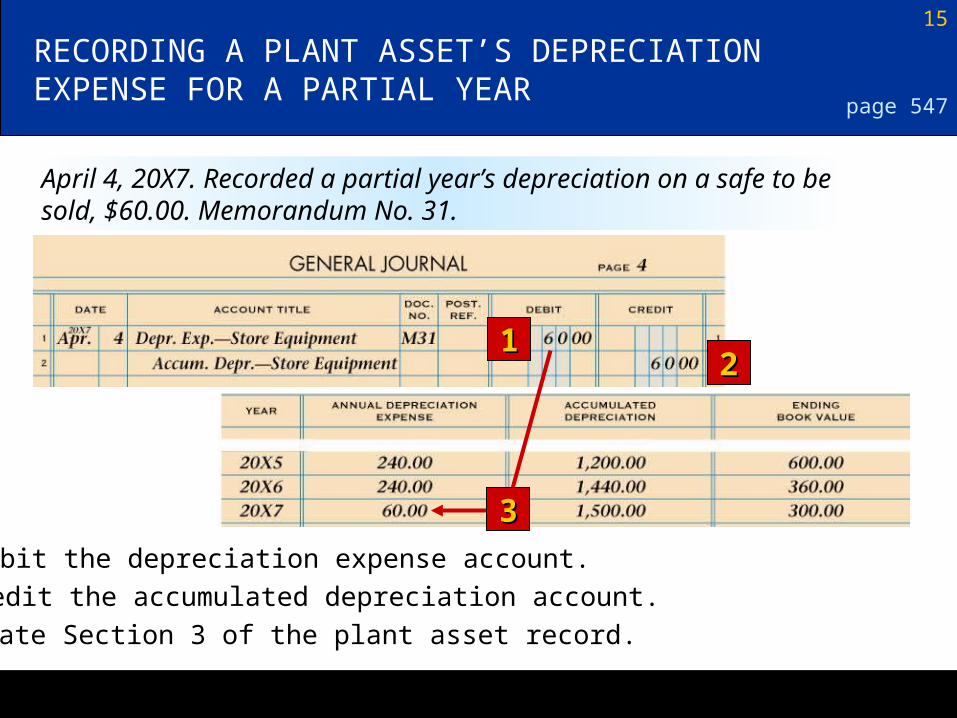

RECORDING A PLANT ASSET’S DEPRECIATION EXPENSE FOR A PARTIAL YEAR

page 547

April 4, 20X7. Recorded a partial year’s depreciation on a safe to be sold, $60.00. Memorandum No. 31.

1. Debit the depreciation expense account.

2. Credit the accumulated depreciation account.

3. Update Section 3 of the plant asset record.

1122

33

16

SALE OF A PLANT ASSET FOR MORE THAN BOOK VALUE

1. Remove the original cost. Record the gain on the sale. Record the cash received from the sale.

page 548

April 4, 20X7. Received cash from sale of safe, $425.00: original cost, $1,800.00; accumulated depreciation through April 4, 20X7, $1,500.00. Receipt No. 47.

2. Check the type of disposal. Write the date and disposal amount in Section 2 of the plant asset record.

11

22

17

1. Remove the original cost. Record the loss on the sale. Record the cash received from the sale.

SALE OF A PLANT ASSET FOR LESS THAN BOOK VALUE

11

page 549

October 6, 20X7. Received cash from sale of a computer, $150.00: original cost, $1,900.00; total accumulated depreciation through October 1, 20X7, $1,500.00. Receipt No. 281.

2. Check the type of disposal and write the date and disposal amount in Section 2.

22

LESSON 18-5 DECLINING-BALANCE METHOD OF DEPRECIATION

The straight line method charges and equal amount of depreciationexpense each year.

Some assets depreciate more in the early years of useful life.

Multiplying the book value by a constant depreciation rate at theend of each fiscal period is called the declining balance method ofdepreciation.

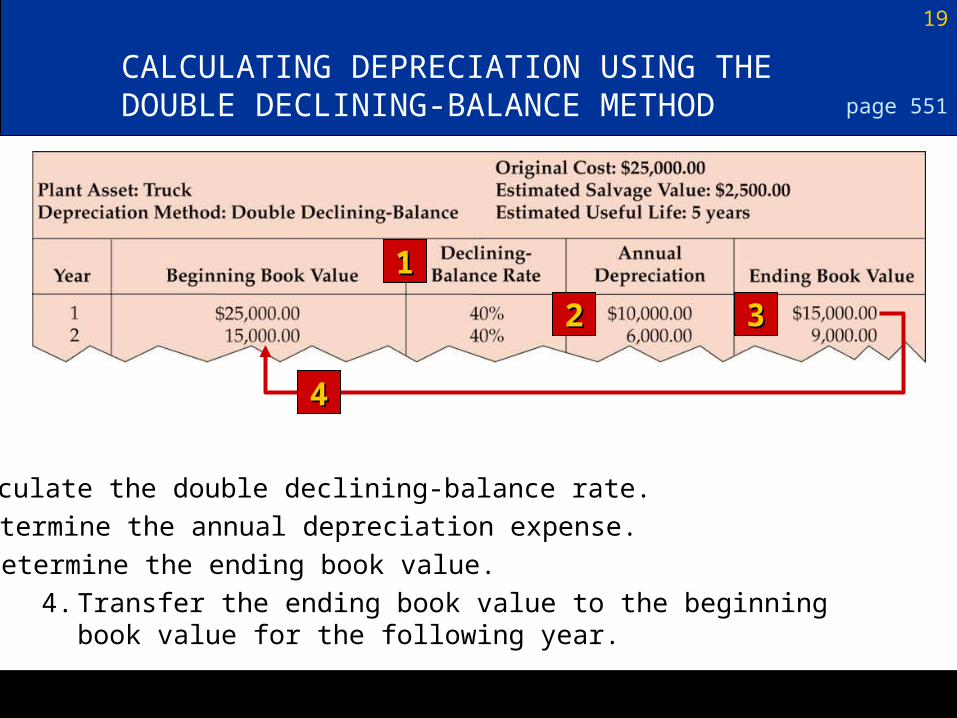

-The declining-balance depreciation rate is a multiple of thestraight line rate. Many businesses use a declining-balance ratethat is two times the straight-line rate. This method is called thedouble declining-balance method.

19

CALCULATING DEPRECIATION USING THE DOUBLE DECLINING-BALANCE METHOD

11

22 33

page 551

44

1. Calculate the double declining-balance rate.

2. Determine the annual depreciation expense.

3. Determine the ending book value.

4. Transfer the ending book value to the beginning book value for the following year.

20

CALCULATING THE LAST YEAR’S DEPRECIATION EXPENSE

22 33

page 552

1. Transfer the ending book value from Year 4 to the beginning book value of Year 5.

2. Subtract the salvage value from the beginning book value to determine the depreciation expense for the last year.

3. Verify that the ending book value is equal to the salvage value.

11

21

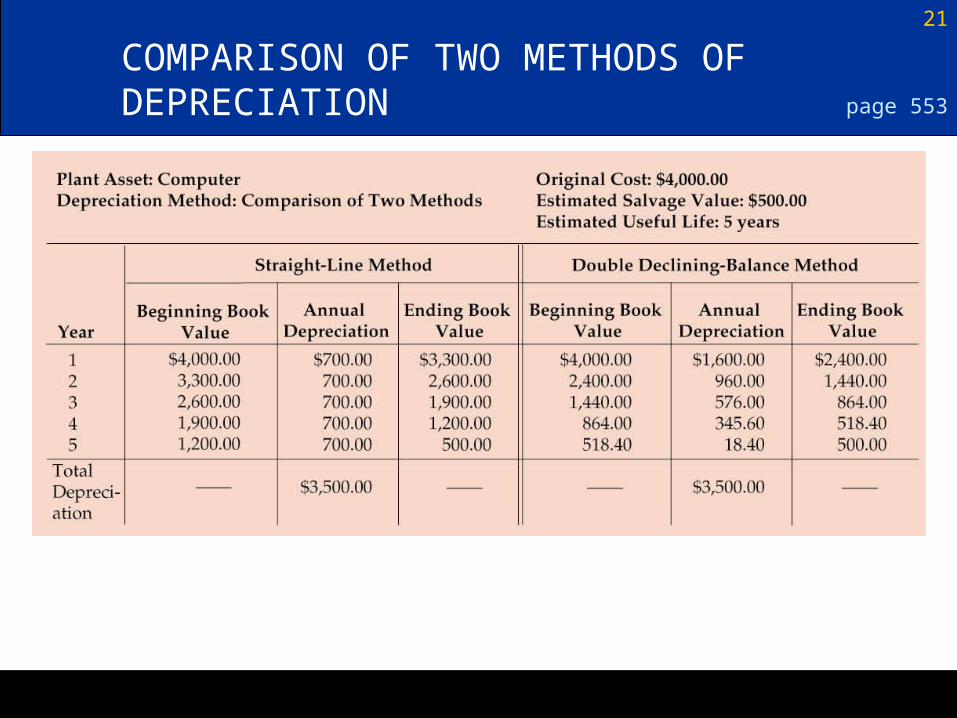

COMPARISON OF TWO METHODS OF DEPRECIATION page 553