1

Changes in Income Tax brought by the Finance Act 2017

September 2017

2

Personal Income: Individual/Firm Tax Rates

For Bangladeshi

individuals, resident

foreigners, and firms

First Tk. 250,000

Next Tk. 400,000

Next Tk. 500,000

Next Tk. 600,000

Next Tk. 3,000,000

On Balance

Nil

10%

15%

20%

25%

30%

Income Tax Rate

For non-resident foreigner, flat tax rate of 30% will remain unchanged

3

Personal Income: Nil Tax Limit

General – Individuals & Firms

Women and senior citizens

(65+)

Physically challenged persons

War-wounded gazetted freedom

fighters

Tk. 250,000

Tk. 300,000

Tk. 375,000

Tk. 425,000

Type of Individual Tax payerFY 16/17

Income

For parents or legal guardians of physically challenged persons the

Nil Tax Limit will be increased by Tk 25,000.

Tk. 250,000

Tk. 300,000

Tk. 400,000

Tk. 425,000

FY 17/18

Income

4

Personal Income: Perquisites and allowance

• Lower of 50% of basic salary; or

• Tk. 25,000 per month will be

exempted

Higher of 5% of basic salary or Tk.

60,000 per year would be added to

the income

House rent allowance

Conveyance provided for

personal or private use

5

Personal Income: Perquisites and allowance

Medical expenses

General Individual

Mentally Retarded Person

Lower of 10% of BS

and Tk. 120,000

Tk. 1,000,000

6

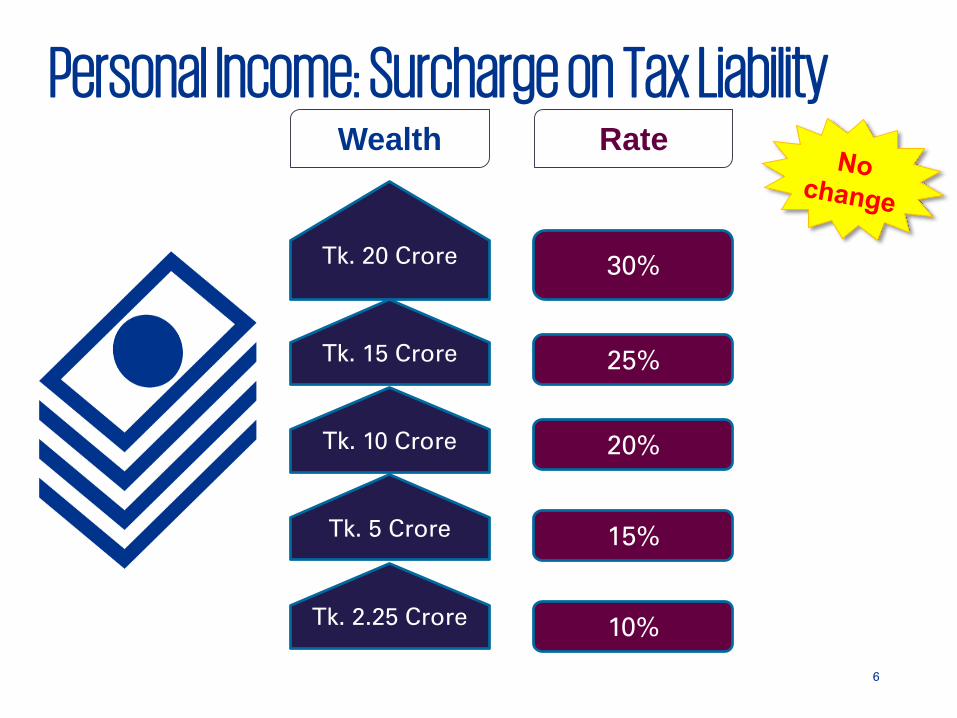

Personal Income: Surcharge on Tax LiabilityWealth Rate

Tk. 20 Crore

Tk. 15 Crore

Tk. 10 Crore

Tk. 5 Crore

Tk. 2.25 Crore

30%

25%

20%

15%

10%

7

Statement of assets, liabilities and life style

BDT 20 Lakh BDT 25 Lakh

Statement of assets,

liabilities and life style

return need to be

submitted

FY 2016/17

LimitFY 17/18

Limit

If gross wealth exceeds

8

Personal Tax: Minimum Tax AmountMinimum Tax Amount at Tax Return Level

Location FY 2016/17

Dhaka and Chittagong City Corporation Tk. 5,000

Other City Corporations Tk. 4,000

Other areas Tk. 3,000

9

Personal Income: Investment Rebate

15%of Allowable Investment (Eligible Amount)

TK. 15,000,000 Actual Investments

Whichever is lower of:

25% of Total Income

10

Corporate Tax: Rates (1)

Non listed companies including branch companies

Listed Companies

Banks, insurance and other FIs – Listed

Banks, insurance and other FIs – Non- listed

Merchant Banks – Listed and Non listed

Cigarette manufacturer – Listed and Non-listed

Mobile phone operators – Listed

Mobile phone operators – Non-listed

Companies

Co-operative Society

25%

35%

42.5%

40%

37.5%

40%

45%

45%

Rate of Tax

15%

11

Corporate Tax: Rates (2)

Companies

Rate of Tax

Ready-Made Garments 20%

FY 2016/17 FY 2017/18

12%

20% 10%Ready-Made Garments with

internationally recognised green

building certification

12

Corporate Tax: Rates (3)

Cigarette, bidi, zarda, chewing tobacco/gul, or any other

tobacco products manufacturers

Rate of Tax 45%

Rate of Surcharge2.5% on

income

45%

FY 2016/17

Rate

FY 2017/18

Rate

0%

13

Clarification in Definition of Income Year

July to JuneJanuary to December

Other FIs

Subsidiaries of FI

Insurance Company

OthersBanks

Multinational companies are

allowed to follow parent companies'

accounting year

Branch and liaison offices are also allowed to follow it’s head office

accounting year

14

Corporate Tax: DisallowancesSection 30(aaaa)

Employers are required to ensure that the tax

returns of their employees were submitted who are

required to submit return on or before the Tax Day

i.e. 30 November (of employees) or as extended

1

Failure to ensure this requirement will result in

related salary expenses disallowance2

15

Corporate Tax: Allowable Perquisites

Generally

Section 30(e)

Tk. 475,000

*For a person

with disabilityTk. 2,500,000

“an individual registered as person with disability under sec 31 of

Protection of the Rights of the Persons with Disabilities Act, 2013”

16

Corporate Tax: Allowable Overseas Travel

Up to 1.25%

of the

disclosed

turnover are

allowed

Section 30(k)

Not applicable for an assesse engaged in

providing any service to the Government where overseas traveling is a key requirement of that

service.

17

Corporate Tax: Disallowance

Payment made to following persons without TIN will result in disallowance:• Agency or distributorship of a company• Commission, fee or other sum for money transfer• Advisory, consultancy etc. by a resident company

Section 30(o)

18

Unexplained investments deemed to be Income

Fiscal year 2016/17

Section 19(31)

Additional income subjecting to tax exemption or reduced

tax rates shown in the revised returns under sections 78 or

93 will be considered as Income from Other Sources

Fiscal year 2017/18

Includes revised or amended return under section 82BB

19

Unexplained investments deemed to be Income

Fiscal year 2016/17

Section 19(28)

Loans or gifts received for amount(s) over Tk. 500,000 other

than through Crossed cheque or Bank transfer, will be

treated as Income

Fiscal year 2017/18

Will not be income if such amount is received from spouse or

parents as long as banking or formal channel is involved in

process

20

Tax DAYAn assessee is required to file income tax

return on or before the Tax Day

Company

Others

15th day of

seventh month

following the end

of income year

30th November

Or

*In case of a holiday, the next working day following the Tax Day!

15th September following the end of the income year where said 15th day falls before the

15th September

21

Return of Income: Who will File?

If the total income exceed Nil Tax Amount

Those whose income are exempted from tax or subject at lower tax other than a charitable

institution or fund,

Mentions few persons

specifically

If the person full-fills any of the specified

conditions

Few changes to the conditions

specified*

If he has assessed in one of 3 years

preceding the income year

Includes employee holding executive or management

position

22

Electronic filing and system generated notice, etc.

Production of accounts: Now onwards, the DCT may

request for information in electronic forms1

System or computer generated notice, order,

requisition, certificate, communication, letter or an

acknowledgment of receipt may be served2

Return, statement, application or documents may be

filed in electronic form and manner as may be

specified by NBR3

23

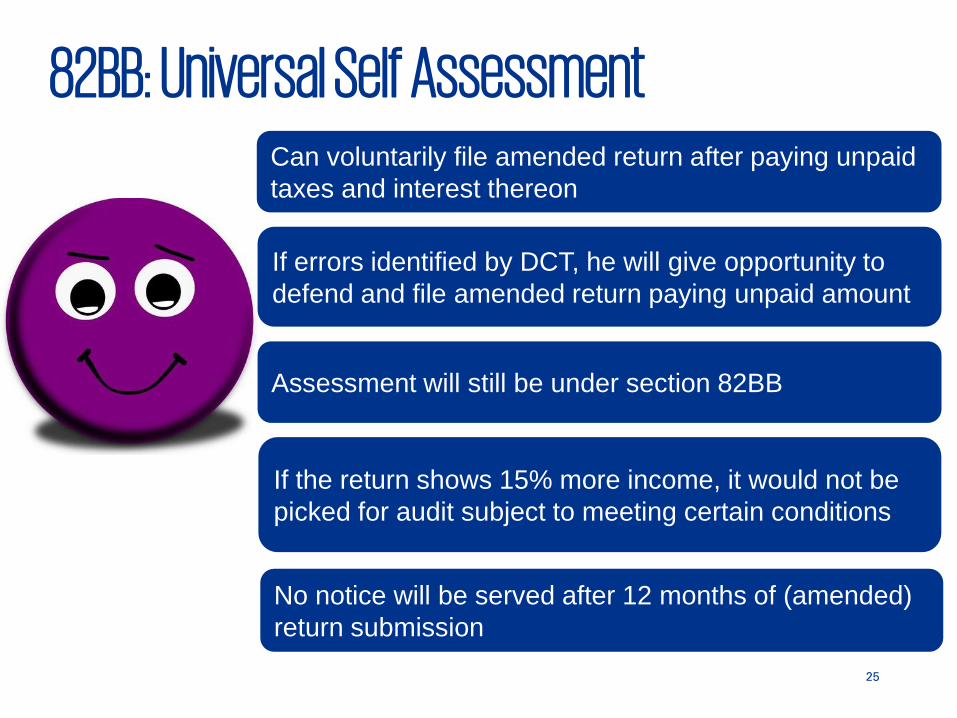

82BB: Universal Self Assessment

Mentions 12-digit E-TIN in

the return

Assessee

Issues acknowledgement

DCT

Submits return on time Acknowledgement acts as

Assessment Order

Pays tax while submitting

tax return

No notice shall be served

after 12 months from the

date of return submission

24

82BB: Universal Self AssessmentI made a

mistake, can

I amend my

return?

If the DCT

finds out the

mistake, will I

be allowed to

amend my

return?

Shall I still

be assessed

under

section

82BB?

25

82BB: Universal Self AssessmentCan voluntarily file amended return after paying unpaid

taxes and interest thereon

If errors identified by DCT, he will give opportunity to

defend and file amended return paying unpaid amount

Assessment will still be under section 82BB

If the return shows 15% more income, it would not be

picked for audit subject to meeting certain conditions

No notice will be served after 12 months of (amended)

return submission

26

82BB: At a Glance

• DCT will check for arithmetic accuracy of the return submitted.

• DCT will serve notice to the assessee communicating any

difference.

• DCT will give the assessee an opportunity to defend him/her

self and file amended return.

• DCT will issue a letter of acceptance of amended return given

the differences are resolved duly within 60 days of such

submission.

• If the assessee does not respond within the required deadline,

DCT will serve demand notice within 6 months of serving the

original notice.

27

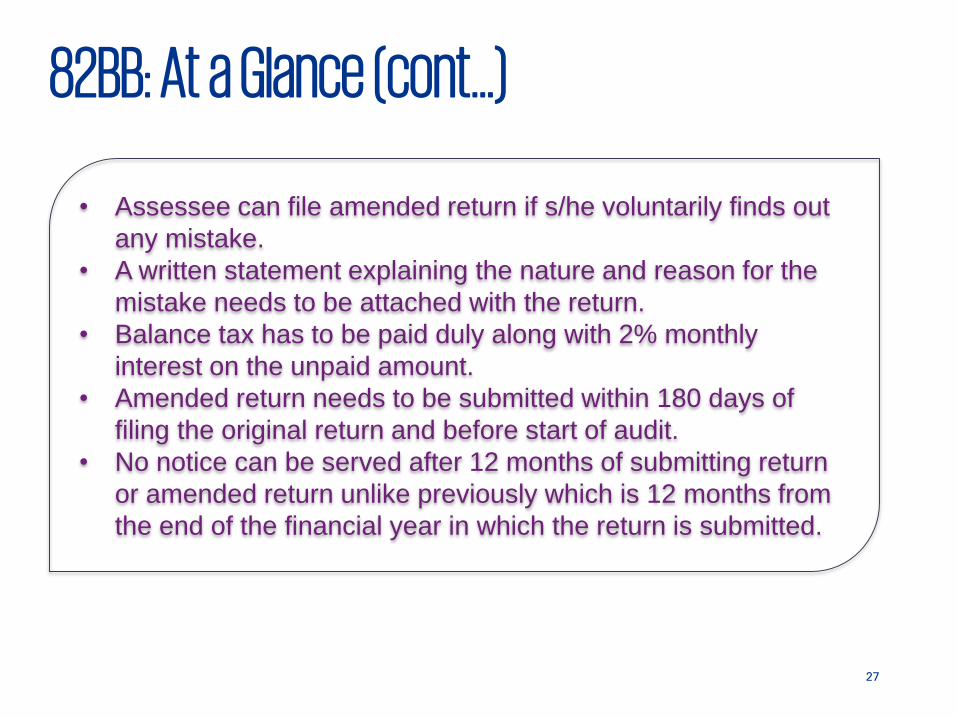

82BB: At a Glance (cont…)

• Assessee can file amended return if s/he voluntarily finds out

any mistake.

• A written statement explaining the nature and reason for the

mistake needs to be attached with the return.

• Balance tax has to be paid duly along with 2% monthly

interest on the unpaid amount.

• Amended return needs to be submitted within 180 days of

filing the original return and before start of audit.

• No notice can be served after 12 months of submitting return

or amended return unlike previously which is 12 months from

the end of the financial year in which the return is submitted.

28

82BB: At a Glance (cont…)

• NBR may select a number of returns for audit. However,

returns fulfilling certain conditions will not be picked for audit.

• Except for 15% income increase, all other conditions remain

same. In calculating 15% income increase, like for like income

between two years will be considered.

• If any anomaly is found, then DCT will serve a notice requiring

the assessee to file an amended return.

• If the DCT is satisfied with the amended return, he will issue a

letter of acceptance.

• If the DCT is not satisfied, then s/he will proceed to make

assessment under section 83 or 84, whichever is applicable.

29

82BB: At a Glance (cont…)

• No question of the initial capital will be asked if at least 20% of

such is shown as income, which is lower than the previous

threshold of 25%.

• Initial capital will have to be kept for the next subsequent

income years. If it gets reduced, then the shortfall amount will

be considered as income in the income year in which it falls

short.

30

93: Tax, etc. escaping payment

Other than the following, the section remains the same

• DCT may issue a notice asking to submit return and pay the

sum that escaped payment. Letter of Acceptance will be

issued upon fulfilling certain conditions.

• Will proceed to make assessment under section 83 or 84 if the

conditions are not fulfilled.

• IJCT’s approval will only be required in case of completed

assessment or for returns filed in compliance with section

82BB.

31

93: Tax, etc. escaping payment

No return is filed, No

assessment was made

Conditions

No return is filed, assessment

completed

All other cases

At any time

Notice to be

issued

Within 6 years from

the end of AY

Within 5 years from

the end of AY

Commissioner may extend the time up to 6 years if the escape of

payment was due to failure in making full disclosure by the

assessee

32

Specification of escaped paymentIncome escaped

assessmentConcealment or

misrepresentation of any income,

asset or expenditure

Excessive relief or loss or

deduction or allowance

Lower tax computed or paid because of lower base

Application of tax rate lower than

the due rate

Understated Income

33

Corporate Tax: limitation of assessment

Fiscal year 2016/17

• 82BB - 2 years

• 107C - 3 years

• In other case- 6 months

from the end of

assessment year

Fiscal year 2017/18

• 82BB – 2 years

• 107C – 3 years

• In other case- 6 months

from the end of assessment

year

Section 94

• 93(3)(a) & (b)– 2 years

• 93(3)(c) – 1 years• 93 - within 2 years.

34

Corporate Tax: Computation of Depreciation

FY 2017/18

• An inconsistency has been resolved by updating the

cross referencing as in the proviso. In case of motor

vehicle, 25 lac will be maximum limit.

• It also states that nothing of this clause will apply for

bus and minibus used for transportation of students,

teachers, employees of business organization and

profession.

3rd Schedule

35

Requirements of 12-digit TIN replaced entirely

Board can exempt from having twelve-digit TIN;

The responsible person need to ensure that the required person has twelve-digit TIN.

New items added, namely:

i. Agency distributorship of a company;

ii. Commission, fee or other sum in relation to money transfer through mobile banking or other electronic means;

iii. Advisory or consultancy services, catering service, event management service, supply of man power or providing security service;

iv. Bill of entry for import or export.

The entire section has been replaced and mainly

enhancement of service area has been done.

36

Previously

Failure to ensure the authenticity of twelve-digit TIN of the required person by the responsible person.

Penalty will be not more than BDT 50,000.

New inclusion

Failure to ensure of having twelve-digit TIN of the required person by the responsible person.

Penalty will be not more than BDT 200,000.

The entire section has been replaced and mainly

enhancement of penalty has been done.

Enhancement of penalty for failure to verify TIN

37

Inclusion of “Revision of penalty based on the revised amount of income”

DCT shall revise penalty at the time of revising the income

The affected parties has been given a reasonable opportunity of

hearing

Affected parties can apply for revision of penalty to DCT if not

revised after revision of assessment order. If no order is made within

180 days, penalty amount is deemed revised

New Section 133A added

38

Changes in TDS Sections (1)Deduction from payment to contractors, etc.

Section-52

0% to 7%

FY 2016/17

3% to 5%

FY 2017/18

2% to 7%

Execution of contract

Manufacture, process or

conversion; or

printing, packaging or

binding

39

Changes in TDS Sections (2)Deduction from payment to contractors, etc.

Section-52

Supply of goods 2% to 7%

No deduction required for purchase of direct

materials as part of cost of sales or cost of goods

sold

For supply of imported goods, tax deduction

would be reduced by AIT paid at import stage

Risk of disclosing business

secret/margin

40

Changes in TDS Sections (3)Deduction or collection at source from (commission, discount or

fees)- Section-53E

10% of

payment

FY 2016/17

10% of

payments

FY 2017/18

10% of

payment/

benefits

1.5% of

payments

Payment of commission

discount, fees, incentives,

performance bonus/related

incentives or similar benefits

for distribution or marketing

Payment for promotional

activities

41

Changes in TDS Sections (4)Deduction or collection at source from (commission, discount or

fees)- Section-53E

Fiscal year 2016/17

Fiscal year 2017/18

5% x 6% x

selling price

5% x 5% x

selling price

Sells to distributor at lower

than retail price

42

Changes in TDS Sections (5)Section 52BB and 52BBBB – withholding tax on export

Fiscal year 2016/17

Fiscal year 2017/18

In tax law 1% which

subsequently

reduced to 0.7%

through SRO

effective up to 30

June 2017

In tax law 1%

which

subsequently

reduced to 0.7%

through SRO

effective up to 30

June 2018

Withholding tax on

export

(except Jute

products)

No change in substance

43

Changes in TDS Sections (6)Section 52AA : Creative media service, Public relations

service, organization and management service and any

other service of similar nature

Withholding Tax Rates on Based

Amount

Base amount

up to

Tk. 25 Lakh

Base amount

exceeds

Tk. 25 Lakh

(b) On gross receipts

(a) On commission 10%

1.5%

12%

2%

44

Changes in TDS Sections (7)

Section 52AA : Media buying agency service

Withholding Tax Rates on Based

Amount

Base amount

up to

Tk. 25 Lakh

Base amount

exceeds

Tk. 25 Lakh

(b) On gross receipts

(a) On commission 10%

0.5%

12%

0.65%

45

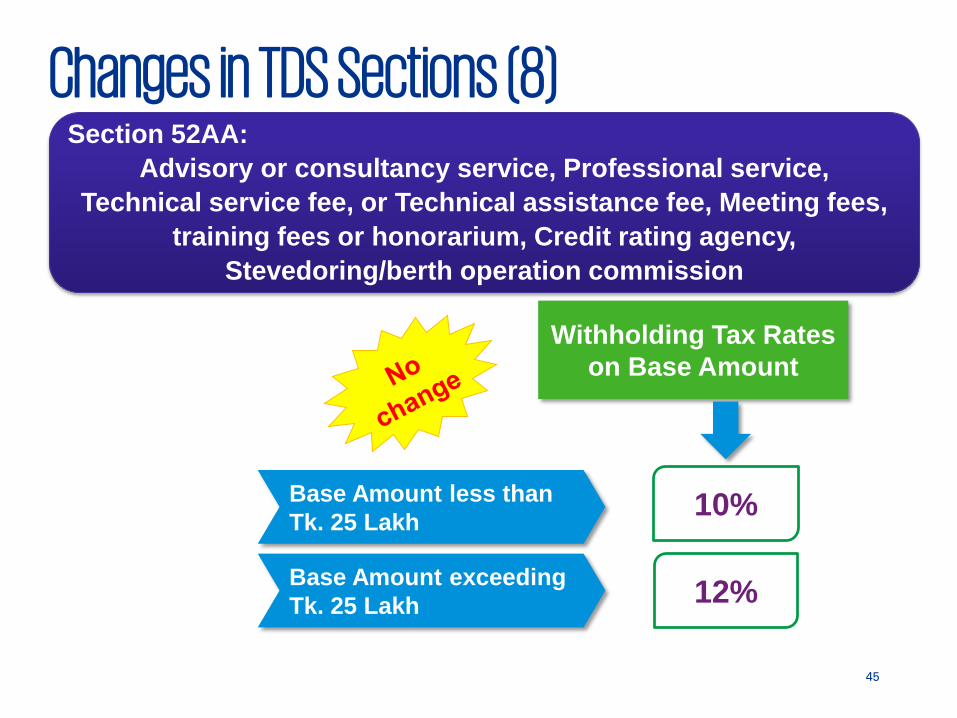

Changes in TDS Sections (8)

10%

Withholding Tax Rates

on Base Amount

12%

Section 52AA:

Advisory or consultancy service, Professional service,

Technical service fee, or Technical assistance fee, Meeting fees,

training fees or honorarium, Credit rating agency,

Stevedoring/berth operation commission

Base Amount less than

Tk. 25 Lakh

Base Amount exceeding

Tk. 25 Lakh

46

Changes in TDS Sections (9)Section 52AA:

Mobile network operator, technical support service provider or

service delivery agents engaged in mobile banking operations

10%

Withholding Tax Rates

on Base Amount

12%

Base Amount less than

Tk. 25 Lakh

Base Amount exceeding

Tk. 25 Lakh

47

Changes in TDS Sections (10)

10%

Withholding Tax Rates on Based

Amount

12%

Section 52AA:

Any other service which is not mentioned in Chapter VII

of this Ordinance and is not a service provided by any

bank, insurance or financial institutions

Base Amount less than

Tk. 25 Lakh

Base Amount exceeding

Tk. 25 Lakh

48

Changes in TDS Sections (11)

6%

Withholding Tax Rates on Based

Amount

8%

Section 52AA:

Indenting commission, Private container port or dock

yard service, Motor garage or workshop, Shipping

agency commission

Base Amount less than

Tk. 25 Lakh

Base Amount exceeding

Tk. 25 Lakh

49

Changes in TDS Sections (12)

3%

Withholding Tax Rates on Based

Amount

4%

Section 52AA:Transport service, car rental

Base Amount less than

Tk. 25 Lakh

Base Amount exceeding

Tk. 25 Lakh

50

Changes in TDS Sections (13)

(b) On gross receipts

Withholding Tax Rate on Based

Amount

Up to

Tk. 25 Lakh

Exceeding

Tk. 25 Lakh

Section 52AA:

Catering service, cleaning service, collection and recovery

agency, event management, supply of manpower, and private

security service provider-

(a) On commission 10%

1.5%

12%

2%

51

Changes in TDS Sections (14)Section 52AA:

Where both commission/fee and gross bill

amount mentioned

Withholding Tax shall be higher of

Tax on commission or

fee applying relevant rate

Gross

bill

3.5% for Media

buying agency

and

10% for Others

Rate of tax

on

commission

or fee

52

Tax liability for shipping business of non-resident: Sec 102

8% on income on

account of carriage of

passengers, livestock,

mail or goods

8% on existing scope

Demurrage charge or

handling charge or any other

amount of similar nature

Fiscal year 2016/17 Fiscal year 2017/18

Supplementary return shall be submitted for demurrage income

within 30 days from the end of month in which the income accrued.

53

Value Added Tax

54

New VAT Act 2012

The New VAT Act 2012 implementation has

been delayed

It is now expected to be enforced from 1 July

2019

55

VAT Alerts

Price Declaration is present

Current Account needs to be maintained

Current Account needs to be maintained

Advance trade VAT will remain at 4%

Full deduction of withholding VAT

Truncated VAT, tariff VAT, package VAT are present

56

VAT Registration Businesses who are centrally registered under VAT Act 1991 will need

to obtain 9 digit e-BIN online

All VAT obligations under the VAT Act 1991 will be performed with this

9 digit e-BIN

All unit VAT registration will also need to be converted to 9 digit e-BIN

separately online

All VAT obligations performed currently with the respective VAT

circles will continue to be performed with the same VAT circles

VAT return is required to be filed with the respective regional

commissioner by the Unit VAT Registered person mentioning the 9

digit e BIN

9 digit e-BIN should be obtained by 31 Dec 2017. In the transition time

11 digit VAT registration will be effective

57

VAT Registration

All 9 digit e BIN central registration taken after 31 March 2017 by

businesses which previously had unit registrations will be

invalid as long as VAT Act 1991 is effective

Business will need to obtain unit registration for each unit of

operation

If they wish to obtain central registration, then they will have to

apply for central registration under the VAT Act 1991

58

Extension of VAT exemption facility

Local manufacturers of

Refrigerator and freezer

Extension time limit

30 June 2019

To promote the growth of domestic heavy

industry

Air conditioner

Palm oil & soya bean oil

59

Customs Duty

60

Import Duties

Customs Duty

Regulatory Duty

Supplementary

Duty

61

Export Duty

H.S.Code included products on which Export Duty has been imposed

Sl. No. H.S. Code DescriptionProposed

Rate (%)

1. 2402.10.00Cigars, cheroots and cigarillos, containing

tobacco25

2. 2402.20.00 Cigarettes containing tobacco 25

3. 2402.90.00Other Cigars, cheroots, of tobacco

substitutes25

4. 2403.11.00 Water pipe tobacco 25

5. 2403.19.00 Other Smoking tobacco 25

6. 2403.91.00 "Homogenised" or "reconstituted" Tobacco 25

7. 2403.99.00 Other tobacco extracts 25

62

Excise Duty

63

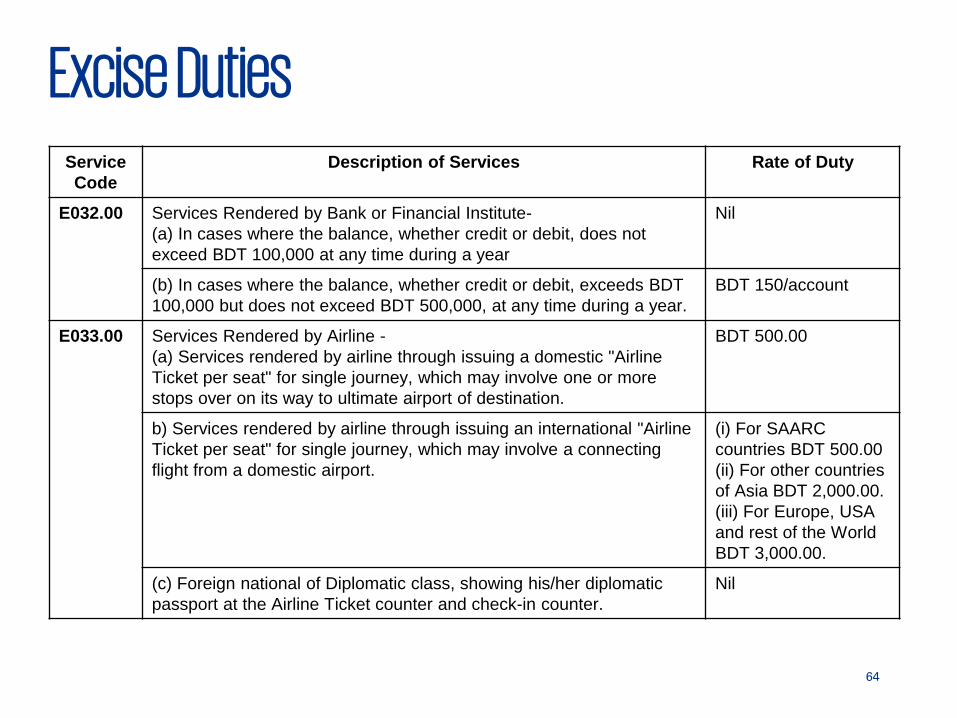

Excise DutyService

Code

Description of Services Rate of Duty

E032.00 Services Rendered by Bank or Financial Institute-

(a) In cases where the balance, whether credit or debit, does not

exceed BDT 100,000 at any time during a year

Nil

(b) In cases where the balance, whether credit or debit, exceeds BDT

100,000 but does not exceed BDT 500,000, at any time during a year.

BDT 150/account

(c) In cases where the balance, whether credit or debit, exceeds BDT

500,000 but does not exceed BDT 1,000,000, at any time during a

year.

BDT 500/account

(d) In cases where the balance, whether credit or debit, exceeds BDT

1,000,000 but does not exceed BDT 10,000,000, at any time during a

year.

BDT 2,000/account

(e) In cases where the balance, whether credit or debit, exceeds BDT

10,000,000 but does not exceed BDT 50,000,000, at any time during a

year.

BDT 12,000/account

(f) In cases where the balance, whether credit or debit, exceeds BDT

50,000,000, at any time during a year.

BDT 25,000/account

64

Excise DutiesService

Code

Description of Services Rate of Duty

E032.00 Services Rendered by Bank or Financial Institute-

(a) In cases where the balance, whether credit or debit, does not

exceed BDT 100,000 at any time during a year

Nil

(b) In cases where the balance, whether credit or debit, exceeds BDT

100,000 but does not exceed BDT 500,000, at any time during a year.

BDT 150/account

E033.00 Services Rendered by Airline -

(a) Services rendered by airline through issuing a domestic "Airline

Ticket per seat" for single journey, which may involve one or more

stops over on its way to ultimate airport of destination.

BDT 500.00

b) Services rendered by airline through issuing an international "Airline

Ticket per seat" for single journey, which may involve a connecting

flight from a domestic airport.

(i) For SAARC

countries BDT 500.00

(ii) For other countries

of Asia BDT 2,000.00.

(iii) For Europe, USA

and rest of the World

BDT 3,000.00.

(c) Foreign national of Diplomatic class, showing his/her diplomatic

passport at the Airline Ticket counter and check-in counter.

Nil

65

Thank you