Candidates’ PerformanceCandidates’ Performancein the 2010 Examination – Paper 1in the 2010 Examination – Paper 1

Mr. WAN Shiu-keeMr. WAN Shiu-keeVice ChairmanVice Chairman

Hong Kong Association for BusinHong Kong Association for Business Educationess Education

2

Overall PerformanceOverall Performance

Satisfactory Possess required skill and knowledge

in presenting financial information in logical and systematic manner

Should have thorough understanding of the syllabus

Able to give appropriate answers based on the scenarios given

3

Overall PerformanceOverall Performance

Abbreviations are not acceptable Proper heading / title should be given

to each account / statement Journal narrations should not be

omitted Should show workings in their

answers

4

Overall PerformanceOverall Performance

Questions Popularity Performance

1 Good

2Satisfactorily answered

3 95.6% Good

4 31.7%Satisfactorily answered

5 72.7% Poor

5

Question 1 – Consolidated Question 1 – Consolidated financial statementsfinancial statements

Good Demonstrated an acceptable level of

understanding of consolidated financial statements

6

Question 1 – Consolidated Question 1 – Consolidated financial statementsfinancial statements

a) Well-answered Only a few candidates failed to work

out the correct amount of purchase consideration

A few others ignored the revaluation adjustment for land and building in calculating the net assets of Sea Ltd

7

8

Question 1 – Consolidated Question 1 – Consolidated financial statementsfinancial statements

b) Poor Many candidates could not give

appropriate explanation for negative goodwill

Tended to repeat same circumstances in different wordings as two separate answers

9

10

Question 1 – Consolidated Question 1 – Consolidated financial statementsfinancial statements

c) Not familiar with the adjustments relating to intra-group transactions

Most candidates reduced turnover and cost of goods sold by the amount of intra-group sales of merchandise but some could not make the adjustment correctly

Had difficulties in handling intra-group sales with 2 different profit margins normal margin treated as mark-up on costs understatement of cost of goods sold and overstatement of gross profit

11

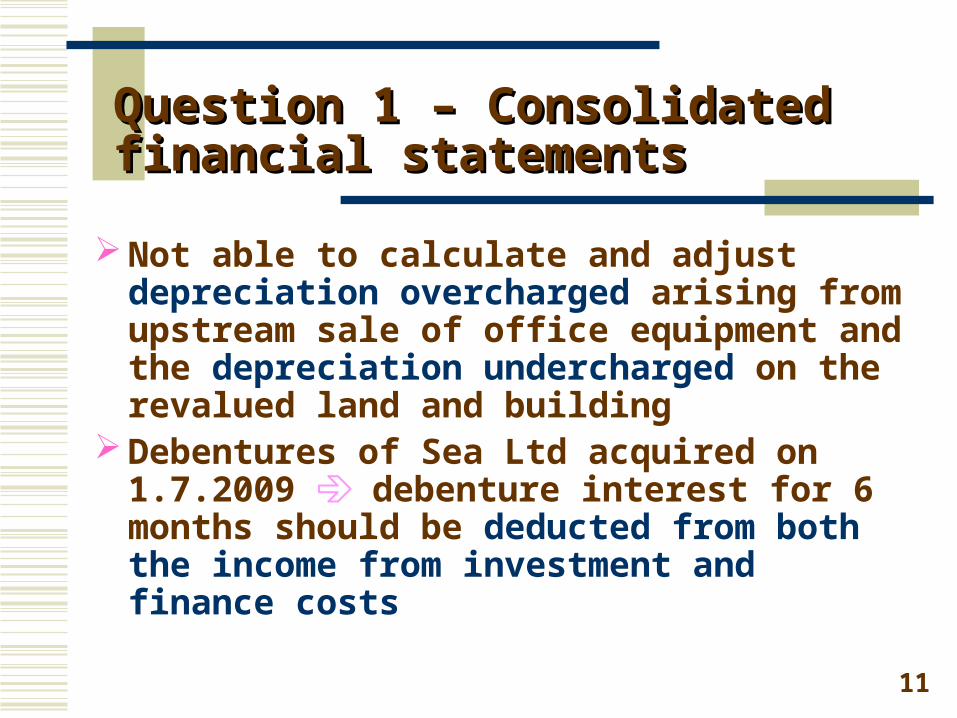

Question 1 – Consolidated Question 1 – Consolidated financial statementsfinancial statements

Not able to calculate and adjust depreciation overcharged arising from upstream sale of office equipment and the depreciation undercharged on the revalued land and building

Debentures of Sea Ltd acquired on 1.7.2009 debenture interest for 6 months should be deducted from both the income from investment and finance costs

12

Question 1 – Consolidated Question 1 – Consolidated financial statementsfinancial statements

Profits attributable to equity holders of the parent and MI were to be shown separately in the consolidated income statement

Only amount of depreciation adjustment arising from revaluation of land and building was to be shared by MI

No unrealised profits or losses arising from upstream sale of non-current assets in year 2009

13

14

Question 1 – Consolidated Question 1 – Consolidated financial statementsfinancial statements

d) Should present the consolidated balance sheet in vertical form and classify various items under appropriate headings

Not able to adjust the correct amounts of depreciation to net book values of office equipment and land and building

Overlooked the amount of intra-group debenture interest did not take it away from both trade receivables and debenture interest payable

15

Question 1 – Consolidated Question 1 – Consolidated financial statementsfinancial statements

Treated the revaluation of land and building as post-acquisition adjustment and created a revaluation reserve on the consolidated balance sheet

Unrealised profit in inventory and depreciation adjustment on office equipment should be eliminated in full against retained profits

16

Question 1 – Consolidated Question 1 – Consolidated financial statementsfinancial statements

Most candidates were able to reduce retained profits and MI with amounts of unrealised profits on intra-group sale of office equipment and depreciation adjustment on revalued land and building but some omitted the fair adjustment from MI

17

18

19

20

Question 2 – Cash flow Question 2 – Cash flow statementstatement

Satisfactorily answered Candidates were well prepared for

the question Apparently familiar with the

classification of cash flows into 3 activities

21

Question 2 – Cash flow Question 2 – Cash flow statementstatement

a) Good Some candidates did not follow the

requirements of updating the cash at bank account and prepare the bank reconciliation

22

23

Question 2 – Cash flow Question 2 – Cash flow statementstatement

b) Poor Not able to explain the accounting treat

ment for the returned cheque repeated the accounting entries made without considering the impact of the returned cheque on accrued expenses and prepaid insurance

24

25

Question 2 – Cash flow Question 2 – Cash flow statementstatement

c) Satisfactorily answered Could not work out the figures for th

e various cash flows from operating activities

Mixed up various cheques received from customers and hence could not arrive at a correct amount of cash receipts from them

26

Question 2 – Cash flow Question 2 – Cash flow statementstatement

Had difficulties in computing the amount for purchase of office equipment not able to exclude it from cash paid to suppliers

Non-cash items should not be included in cash paid for operating expenses

Other income should not be grouped under investing activities

27

Question 2 – Cash flow Question 2 – Cash flow statementstatement

NBV of the new office equipment should be calculated by taking into account the NBV of the disposed office equipment and depreciation on the old office equipment Depreciation + NBV = Cost of the new office equipment

Trade-in allowance should be excluded in computing the amount of cash paid for purchase of office equipment

28

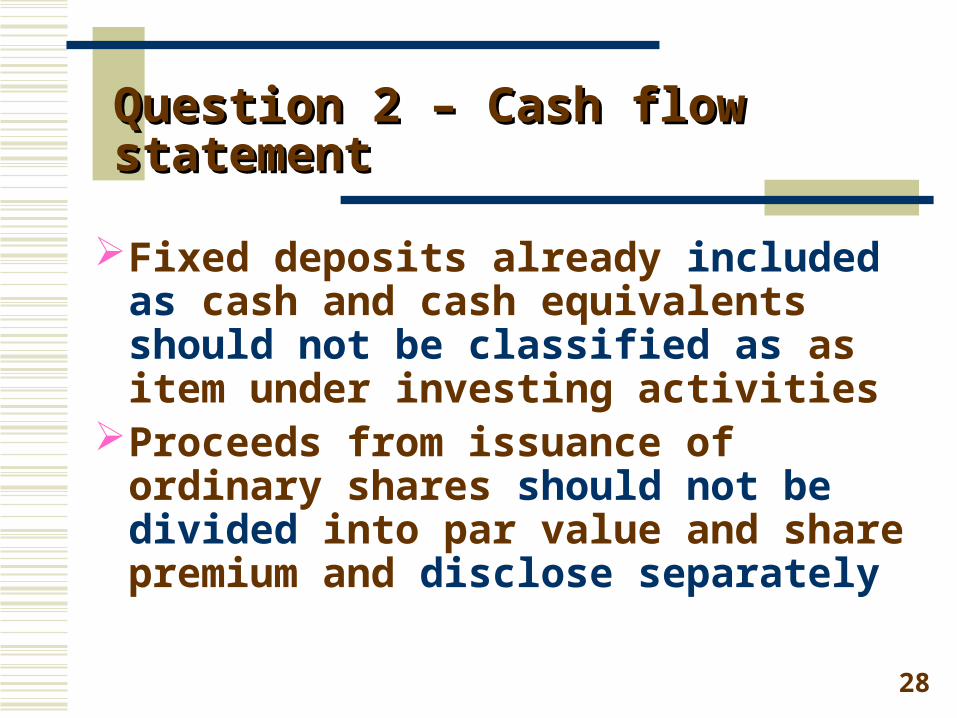

Question 2 – Cash flow Question 2 – Cash flow statementstatement

Fixed deposits already included as cash and cash equivalents should not be classified as as item under investing activities

Proceeds from issuance of ordinary shares should not be divided into par value and share premium and disclose separately

29

30

31

32

Question 3 – PartnershipQuestion 3 – Partnership

Good Quite familiar with the preparation of

various accounts for a partnership

33

Question 3 – PartnershipQuestion 3 – Partnership

a) Good. Should adopt the account names as given

in the question

34

Question 3 – PartnershipQuestion 3 – Partnership

b) Fair NO goodwill account maintained in the boo

ks amount of goodwill should be written off through the partners’ capital accounts using the old and new profit and loss sharing ratios

Many ignored that all non-current assets, except goodwill, had to be recorded back to their original NBVs basing on the new sharing ratios

35

36

Question 3 – PartnershipQuestion 3 – Partnership

c) Good Required to transfer book values of variou

s assets to the realisation account

Some failed to show net amount of motor vehicles and plant and machinery

Others forgot to include cash at bank and deduct allowance for doubtful debts from trade receivables

37

Question 3 – PartnershipQuestion 3 – Partnership

Amount of trade receivables collected by Kam did not include discounts allowed and uncollectible debts

Commission to be credited to the capital acoount of Kam should be based on the amount collected

Interest on capital and share of profit should NOT be credited to partners’ capital accounts

38

39

Question 4 – Ratios analysis and Question 4 – Ratios analysis and Valuation of inventoriesValuation of inventories

Satisfactorily answered Weak in answering conceptual

questions

40

Question 4 – Ratios analysisQuestion 4 – Ratios analysis

A. Could not interpret dividend cover

correctly only able to describe how the ratio was to be calculated

Able to state 3 limitations of using ratio analysis in assessing financial position of a company

41

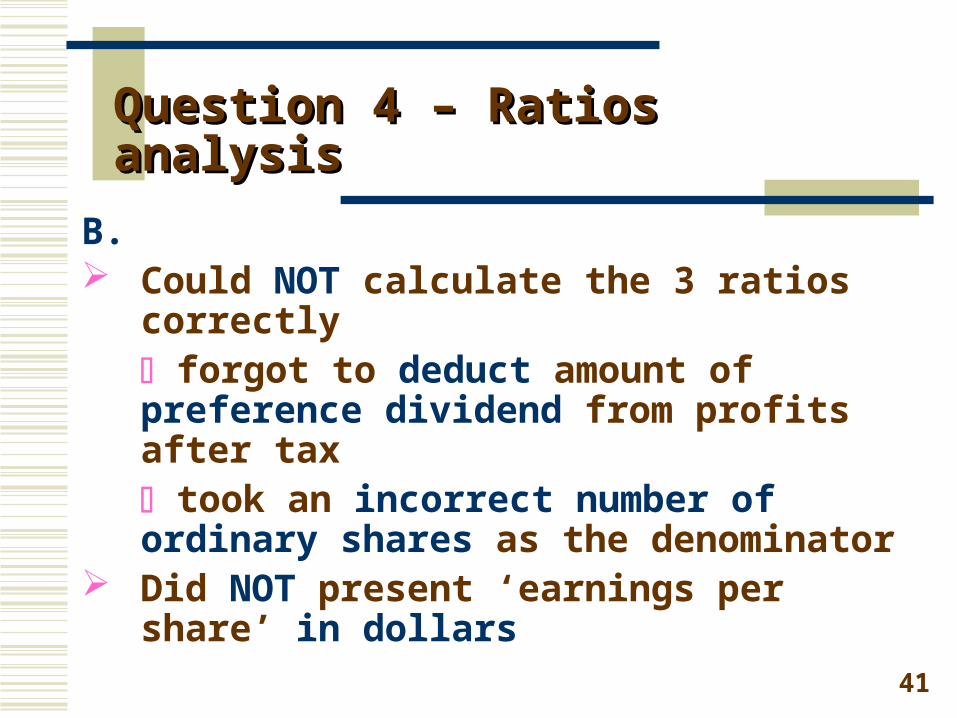

Question 4 – Ratios analysisQuestion 4 – Ratios analysis

B. Could NOT calculate the 3 ratios

correctly forgot to deduct amount of preference dividend from profits after tax took an incorrect number of ordinary shares as the denominator

Did NOT present ‘earnings per share’ in dollars

42

43

Question 4 – Valuation of Question 4 – Valuation of inventoriesinventories

C. Not aware of the adoption of

perpetual inventory system and FIFO method

Not familiar with journal entries relating to sales, returns inwards, abnormal inventory loss and inventory written-down

44

Question 4 – Valuation of Question 4 – Valuation of inventoriesinventories

Could NOT work out the right amounts of sales and cost of goods sold on 20.1.2010 and 31.1.2010

Did Not prepare journal entries to update cost of goods sold and inventory for sales and returns inwards

Could state 1 or 2 situations in which NRV of inventory was less than cost

45

46

Question 5 – Errors and Control Question 5 – Errors and Control accountsaccounts

Poor NOT aware that sales ledger control

account was kept as part of double entry system while sales ledger was kept on a memorandum basis

Ignored that the books had not been closed

47

Question 5 – Errors and Control Question 5 – Errors and Control accountsaccounts

a) Many recorded the corrections or omissions directly to P&L instead of various revenues and expenses accounts

Sales ledger control account should be adjusted instead of debtors’ account

48

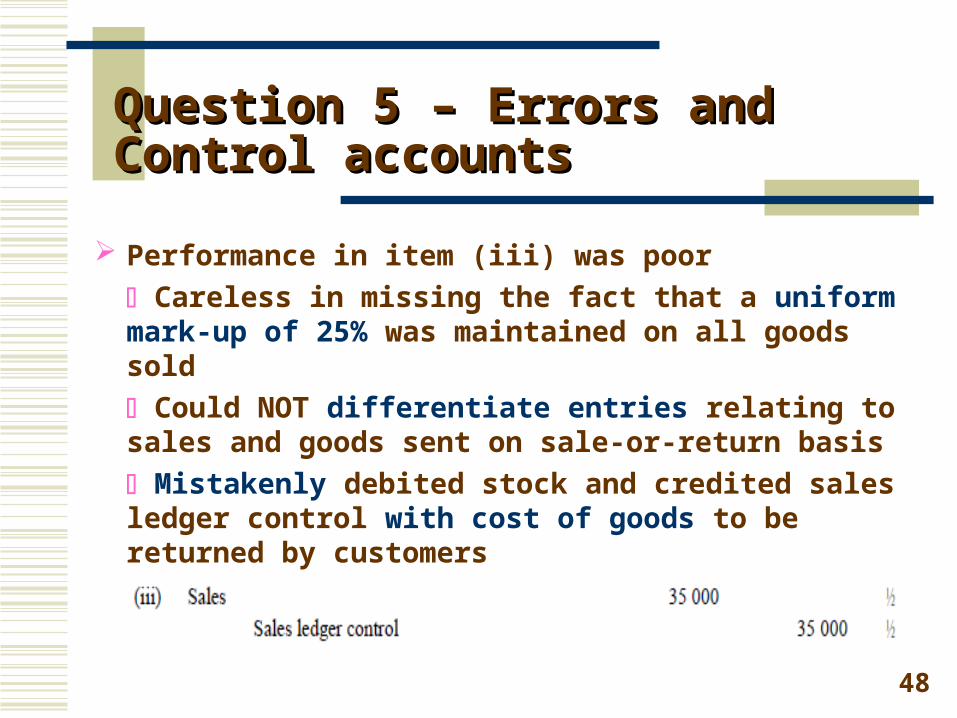

Question 5 – Errors and Control Question 5 – Errors and Control accountsaccounts

Performance in item (iii) was poor

Careless in missing the fact that a uniform mark-up of 25% was maintained on all goods sold

Could NOT differentiate entries relating to sales and goods sent on sale-or-return basis

Mistakenly debited stock and credited sales ledger control with cost of goods to be returned by customers

49

Question 5 – Errors and Control Question 5 – Errors and Control accountsaccounts

Did NOT possess sufficient understanding of finance lease

Could NOT show journal entries relating to acquisition of leased office equipment, payments made and lease interest for year 2009

50

Question 5 – Errors and Control Question 5 – Errors and Control accountsaccounts

b) Well-answered Some prepared an account instead

of a statement in columnar form to update the totals of the extracted sales ledger balances

51

Question 5 – Errors and Control Question 5 – Errors and Control accountsaccounts

c) Could NOT point out when a credit note was to be used by a company

Thank you !Thank you !