Buying Mutual Funds Titling fund ownership Individual Joint Tenants with Right of

Survivorship Equal owners Tenants in Common

Can be unequal ownership Assets don’t transfer automatically at death

Gifts or Transfers to Minors UGMA or UTMA (TN - both)

http://www.finaid.org/savings/ugma.phtml UTMA is more flexible Adult owner or custodian

minors do not have contract rights fiduciary responsibility

Transfers at majority (TN: UGMA – 18; UTMA – 21)

$14,000 per year Taxes – First $850 tax free, next $850 at

child’s rate, anything more at parent’s rate

Trust Trustee and beneficiary Living Trust

Corporation, partnership, or other legal entity

What to Look For Retirement plans Automatic Investment Plans Automatic Reinvestment Transaction

Phone or computer Website Exchange privileges Check writing Withdrawals

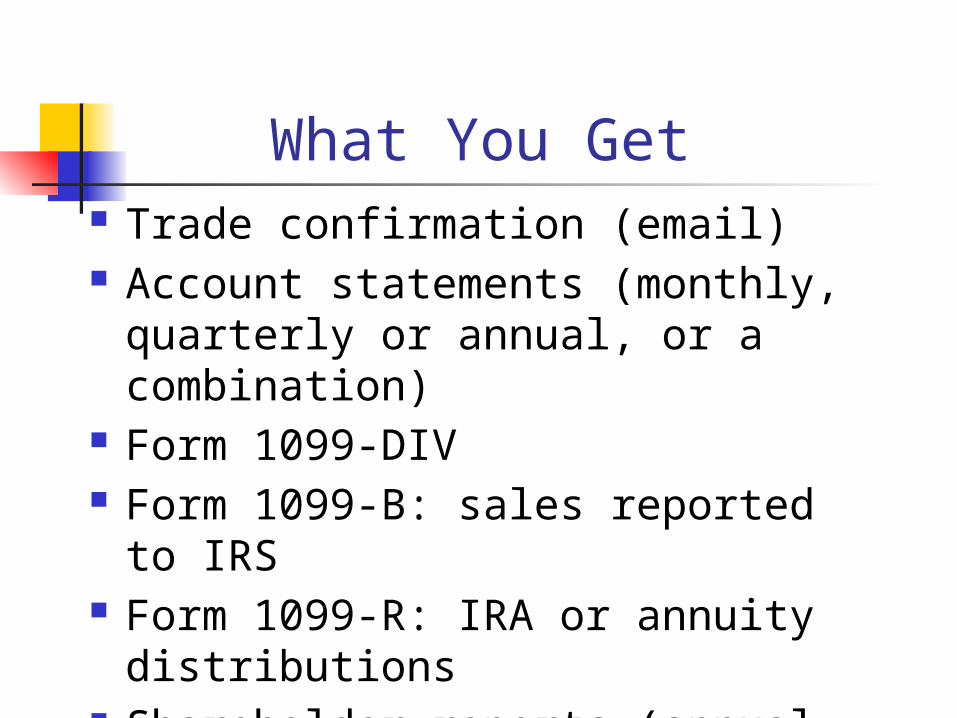

What You Get Trade confirmation (email) Account statements (monthly,

quarterly or annual, or a combination)

Form 1099-DIV Form 1099-B: sales reported to IRS Form 1099-R: IRA or annuity

distributions Shareholder reports (annual and

semiannual)

Fund Supermarkets Basically a brokerage account

May just be for mutual funds Consolidated record keeping Lower custodial fees Easier to switch families (tax-loss

harvesting) Margin - maybe

Financial Advisors BEWARE!!! DO YOUR HOMEWORK Ask about fees Ask for references Check arbitrations – NASD CFA CFP CLU and ChFC – life insurance Personal Financial Specialist – CPA with

financial planning training

Asset Allocation Individual decision Income or growth Rebalancing

tax implications 90% of portfolio performance is

asset allocation, not security selection

Asset Allocation Risk and Return Questions

Age Objectives - time Risk tolerance Investment size How much are you involved? Taxes

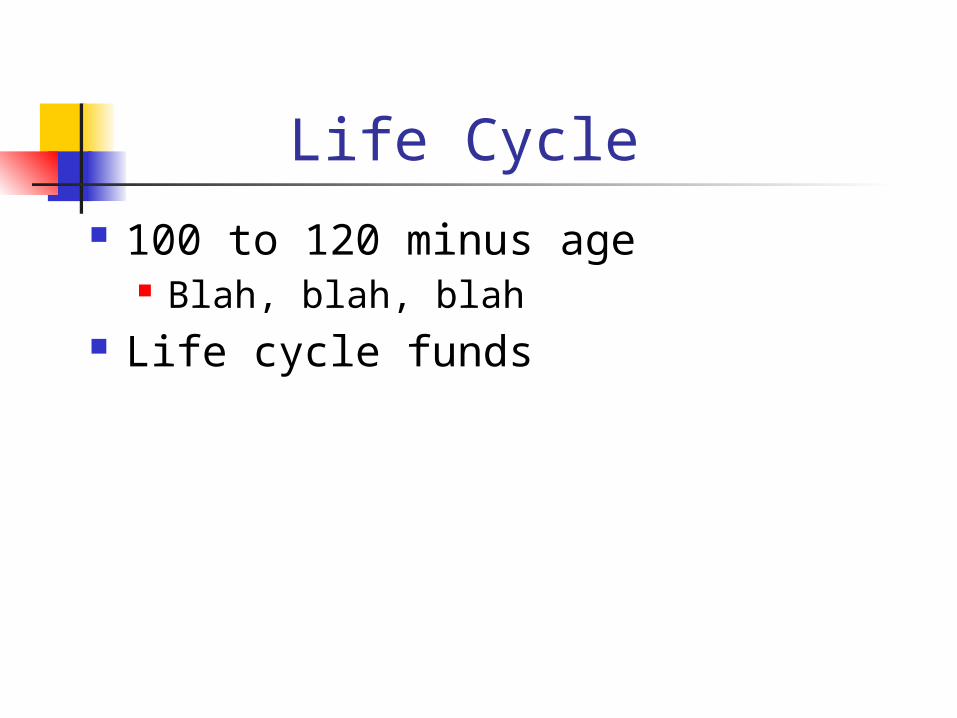

Life Cycle 100 to 120 minus age

Blah, blah, blah Life cycle funds

Fund Types Stock Bond International Global Country specific Index Money market

Stock Funds Aggressive growth Growth Equity income Growth & Income International Global

Stock funds Market capitalization Growth or value

P/E, P/CF/ P/B Dividend yield Cyclical or defensive Fundamental or technical Concentrated or not

International (volatile) Exchange rate risk

Sector (volatile) Derivatives Fund size

Morningstar Fidelity Low-Priced Stock Fund

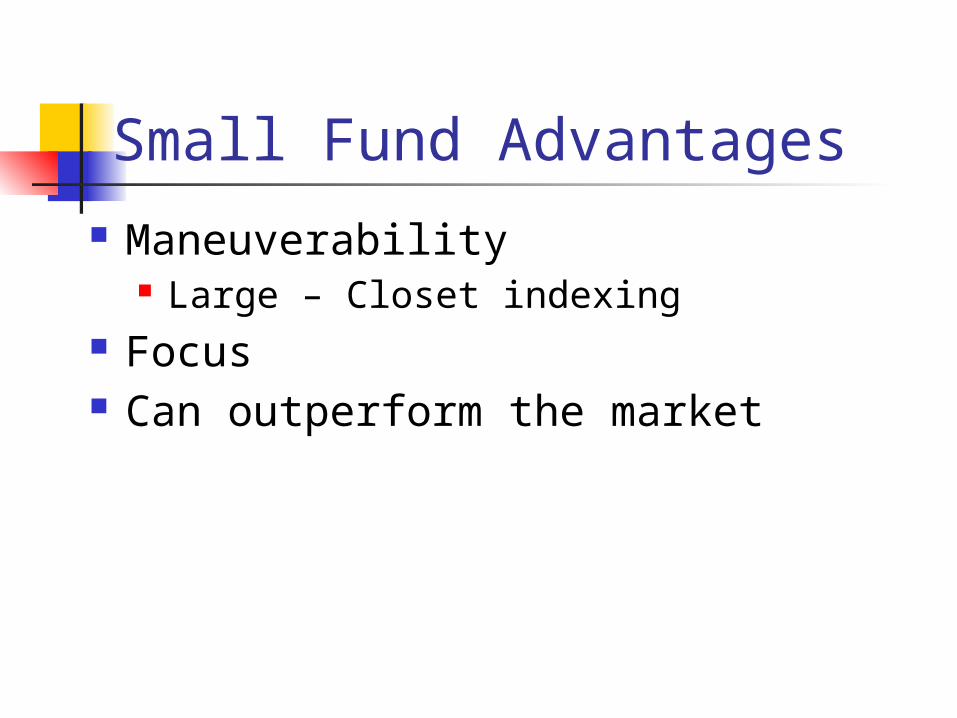

Small Fund Advantages Maneuverability

Large – Closet indexing Focus Can outperform the market

Large Fund Advantages Lower expenses Better management talent Lower trading costs

Bond Funds Why invest in bonds funds:

Liquidity Capital preservation – less volatile Income Diversification

Bond Type U.S. Government MBS Corporate Municipal Convertible Foreign government Foreign corporate

Bond FundsWhat to Look For

Credit quality Maturity – duration Taxability Type of bond

Government, corporate, asset backed, convertible

Country of origin Indexing – probably not

Taxability Taxable fund – 8% Tax rate – 39% Equivalent aftertax return

R = Rpretax(1 – t) R = 8%(1 - .39) R = 4.88%

State vs. Federal

Bond Fund Risks Market risk – Price vs. yield Reinvestment risk Credit risk Call risk

Management Tenure Background Team?

Market Indices DJIA S&P 500 Wilshire 5000 (actually more

>7,000) Wilshire 4500 (Wilshire 5000 –

S&P500) Russell 3000 (98% of market

value) Russell 1000 (largest 1,000) Russell 2000 (1,001 to 3,000)

Mutual Fund Risk Beta Standard deviation Bear market decile (Morningstar) Sector risk

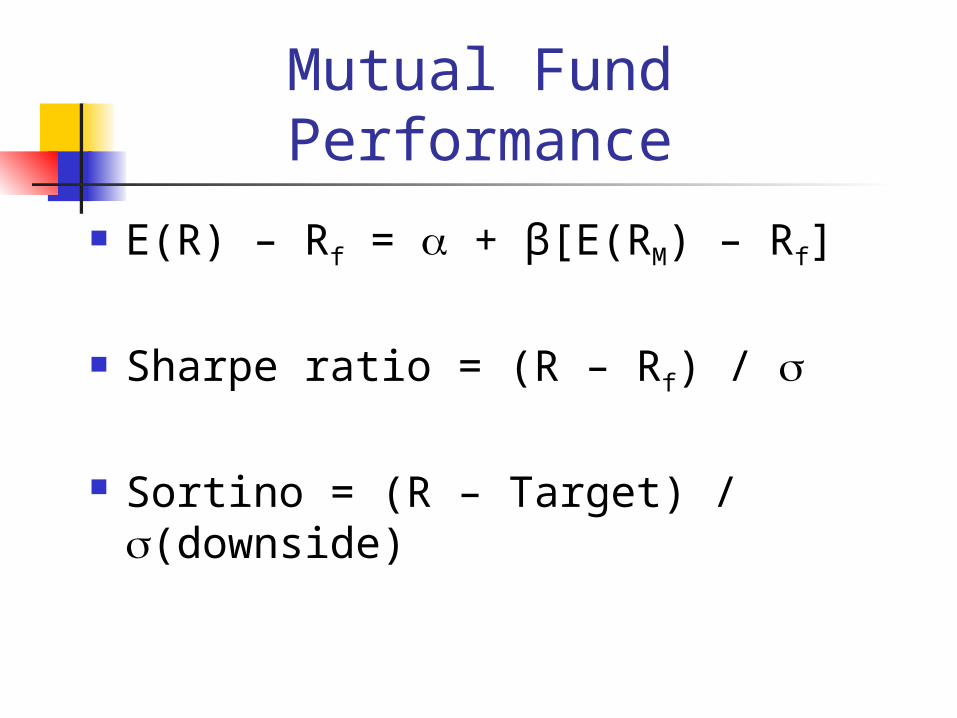

Mutual Fund Performance

E(R) – Rf = + β[E(RM) – Rf]

Sharpe ratio = (R – Rf) /

Sortino = (R – Target) / (downside)

More Performance Evaluation

S&P or appropriate index Peers

What to Look For Fees & Expenses!!!! Turnover Closet Indexing

Performance PersistencePretax alpha

-0.4

-0.3

-0.2

-0.1

0

0.1

0.2

0.3

0.4

0.5

0.6

1 2 3 4 5

1

3

5

7

10

Repeat Winners – above median performance

Fi gur e 1: P er c entage of R epeat Wi nner s by Y ear

0. 0

10. 0

20. 0

30. 0

40. 0

50. 0

60. 0

70. 0

80. 0

90. 0

100. 0

I n it ial Y ear

Repeat

Winners

Required

Winners

Deciles

![[Insert authors name] [Job title] [Team] Home Ownership for [……] Council Tenants Council or Housing Association tenants Insert logo](https://cdn.vdocuments.us/doc/165x107/56649c885503460f949407c8/insert-authors-name-job-title-team-home-ownership-for-council.jpg)