BURGAN CAPE TERMINALS (PTY) LTD

Revised NERSA Tariff Application

Date: 17 July 2017

Contents

1 Introduction .......................................................................................................................................... 1

2 Background ........................................................................................................................................... 1

2.1 Summary of project ...................................................................................................................... 1

2.2 Business model ............................................................................................................................. 2

2.3 Value to the economy ................................................................................................................... 3

2.4 Purpose of this tariff application .................................................................................................. 4

3 The Facility ............................................................................................................................................ 4

Loading facility ...................................................................................................................... 4

Storage facility and auxiliary equipment .............................................................................. 5

Pipeline ................................................................................................................................. 5

4 Tariff methodology ............................................................................................................................... 5

4.1 Imposing a regulated tariff in a competitive environment ........................................................... 5

4.2 Tariff methodology per facility ..................................................................................................... 6

Loading and storage facilities ............................................................................................... 6

Pipeline ................................................................................................................................. 7

4.3 Useful life ...................................................................................................................................... 7

5 The Project Costs .................................................................................................................................. 7

5.1 Capital expenditure ...................................................................................................................... 7

5.2 Operating costs ............................................................................................................................. 8

5.3 Decommissioning costs ................................................................................................................. 9

5.4 Working capital ............................................................................................................................. 9

5.5 Tax .............................................................................................................................................. 10

IOC tax calculation .............................................................................................................. 10

Rate of Return tax calculation ............................................................................................ 10

5.6 Cost schedule per facility ............................................................................................................ 11

Loading facility .................................................................................................................... 11

Storage facility .................................................................................................................... 12

Pipeline ............................................................................................................................... 13

6 Regulatory Asset Base and the calculation of Trended Original Cost (TOC) ....................................... 14

6.1 Loading facility ............................................................................................................................ 14

6.2 Storage facility ............................................................................................................................ 15

6.3 Pipeline ....................................................................................................................................... 15

7 Discount Rate ...................................................................................................................................... 17

7.1 Cost of equity .............................................................................................................................. 17

Risk free rate....................................................................................................................... 18

Market risk premium .......................................................................................................... 18

Beta .................................................................................................................................... 18

Small stock premium .......................................................................................................... 18

Project specific risk ............................................................................................................. 19

Liquidity risk ....................................................................................................................... 20

Calculation of Ke ................................................................................................................. 20

7.2 Gearing and cost of debt ............................................................................................................ 22

7.3 Weighted Average Cost of Capital (WACC) ................................................................................. 22

8 Volume forecast .................................................................................................................................. 23

8.1 Total volumes ............................................................................................................................. 23

9 Tariff calculation ................................................................................................................................. 24

9.1 Loading facility tariff calculation ................................................................................................. 24

Levelised IOC tariff calculation for the loading facility ....................................................... 24

9.2 Storage facility tariff ................................................................................................................... 26

Levelised IOC tariff calculation for the storage facility ....................................................... 26

9.3 Pipeline tariff .............................................................................................................................. 28

Rate of Return tariff calculation for the pipeline ................................................................ 28

10 Conclusion and request for Approval and Setting of Tariffs ........................................................... 29

10.1 Request for approval of the tariff for loading ............................................................................. 29

10.2 Request for approval of the tariff for storage ............................................................................ 30

10.3 Request for setting of the pipeline tariff .................................................................................... 30

11 Appendix A ...................................................................................................................................... 31

11.1 Economic Indicators .................................................................................................................... 31

11.2 Capital Expenditure and allocation per facility ........................................................................... 32

Figures

Figure 1 Location of facility at the Eastern Mole site in the Port of Cape Town ........................................... 2

Figure 2 Layout of the facility........................................................................................................................ 3

Figure 3: Tariff path comparison for the loading facility ............................................................................. 26

Figure 4: Tariff path comparison for the storage facility ............................................................................ 27

Figure 5: Tariff path and expected throughput for the pipeline ................................................................. 29

Tables

Table 1: Capex for the loading facility (R’m) ............................................................................................... 11

Table 2: Operating costs including decommissioning for the loading facility (R’m) ................................... 11

Table 3: Working capital for the loading facility (R’m) ................................................................................ 11

Table 4: Tax calculation for the loading facility (R’m) ................................................................................. 12

Table 5: Capex for the storage facility (R’m) ............................................................................................... 12

Table 6: Operating costs including decommissioning for the storage facility (R’m) ................................... 12

Table 7: Working capital for the storage facility (R’m) ............................................................................... 12

Table 8: Tax calculation for the storage facility (R’m) ................................................................................. 13

Table 9: Capex for the pipeline (R’m) ......................................................................................................... 13

Table 10: Operating costs including decommissioning for the pipeline (R’m) ............................................ 13

Table 11: Working capital for the pipeline (R’m) ........................................................................................ 13

Table 12: Tax calculation for the pipeline ................................................................................................... 14

Table 13: Asset table for the loading facility (R’m) ..................................................................................... 14

Table 14: Asset table for the storage facility (R’m) ..................................................................................... 15

Table 15: Asset table for the pipeline (R’m) ............................................................................................... 16

Table 16: Small stock premium (PWC Valuation Methodology Survey 2014/15) ....................................... 18

Table 17: Risk assessment of the Burgan project ....................................................................................... 20

Table 18: Cost of equity (Ke) for the loading and the storage facility (IOC) ............................................... 21

Table 19: Cost of equity (Ke) for the pipeline (ROR) ................................................................................... 21

Table 20: Weighted Average Cost of Capital (WACC) for the loading and storage facility ......................... 22

Table 21: Weighted Average Cost of Capital (WACC) for the pipeline ....................................................... 22

Table 22: Throughput capacity for Burgan terminal ................................................................................... 23

Table 23: Volume forecast (million litres) ................................................................................................... 24

Table 24: Allowable revenue for the loading facility using the IOC method (R’m) ..................................... 25

Table 25: Levelised IOC tariff calculation for the loading facility ................................................................ 25

Table 26: Levelised IOC tariff and revenue for the loading facility ............................................................. 26

Table 27: Allowable revenue for the storage facility using the IOC method (R’m) ..................................... 26

Table 28: Levelised IOC tariff calculation for the storage facility ................................................................ 27

Table 29: Levelised IOC tariff and revenue for the storage facility ............................................................. 28

Table 30: Allowable revenue for the pipeline using the rate-of-return tariff method (R’m) ..................... 28

Table 31 Tariff for the pipeline using the rate-of-return method ............................................................... 29

Table 32: Macroeconomic indicators .......................................................................................................... 31

1

1 Introduction

In this tariff application document1 we discuss the three tariffs required by Burgan Cape Terminals. The

tariffs are for a loading facility, a storage facility and a pipeline. For the storage and the loading facility

we have made the case for NERSA to approve a multi-year tariff for the period FY172 to FY19, based on

the levelised NERSA IOC methodology for loading and storage facilities. The loading and storage tariffs

for FY17 and beyond are based on a reference base value combined with an inflationary escalation

mechanism. The reference base value is calculated for FY17. Burgan Cape Terminals requests NERSA to

approve a maximum base value of 1.47 cents/litre for the loading facility for FY17. This tariff must be

escalated with inflation to obtain the maximum tariff that will apply for subsequent years during the

period for which the approval is sought: FY17 to FY19. Burgan Cape Terminals similarly requests NERSA

to approve a maximum base value of 23.01 cents/litre for the storage facility for FY17. This tariff must

also be escalated with inflation to obtain the tariff that will apply for subsequent years during the period

for which the approval is sought: FY17 to FY19. For the interconnecting pipeline we have made the case

for NERSA to set a multi-year tariff starting from FY17 to FY19, based on the NERSA ROR methodology

for pipelines. Burgan Cape Terminals requests NERSA to set the pipeline tariff for the period as set out in

Table 31 below.

2 Background

2.1 Summary of project

Burgan Cape Terminals (Pty) Ltd is a black empowered and independent South African oil storage

company. Its shareholders are Thebe Investment Corporation (15%) with experience in the downstream

petroleum market, Jicaro (15%) a newly established 100% black owned BBBEE company and VTTI B.V.

(70%) a global terminal owner that operates in 5 continents with more than 8 million m3 of oil storage

and LPG capacity.

After being identified as the most suitable bidder, Burgan Cape Terminals was awarded a 20-year

contract by TNPA3 to develop and manage fuel storage and distribution facilities at the Eastern Mole of

Cape Town Harbour. The Burgan project is supportive of national polices and plans related to security of

supply, the maintenance of strategic stocks, infrastructure needs, spatial and capacity planning at the

1 This tariff application incorporates revisions to the original application in order to address concerns raised by NERSA during the application process. More accurate cost information is now available than at the time of the initial application and this updated information has been included in the tariff calculation.

2 Burgan’s financial years coincide with calendar years thus FY17 is the period from 1 January 2017 to 31 December 2017.

3 Transnet National Ports Authority

2

Port of Cape Town and the facilitation of greater competition. The importance of the Burgan project has

resulted in Government including it as a strategic project under Operation Phakisa – a government

initiative to unlock the potential of South Africa’s oceans in growing the economy and creating jobs. This

Greenfield project was officially launched in November 2015 by the Dutch Minister of Agriculture and

State Secretary of Economic Affairs, Martijn van Dam and the South African Director-General of the

Department of Trade and Industry (DTI), Lionel October.

The location of the facility is shown in Figure 1.

Figure 1 Location of facility at the Eastern Mole site in the Port of Cape Town

2.2 Business model

Burgan Cape Terminals will provide a multi-purpose fuel storage facility used for the distribution of both

locally produced and imported fuels. The storage of refined petroleum products will be received either

by sea with the loading facilities in Eastern Mole Berth 2 or piped from the Chevron refinery in

Milnerton (Cape Town). Tanker vessels will decant at Eastern Mole Berth 2 using the Burgan marine

loading arms. Locally produced product may also be pumped from the Chevron Oil Refinery to the

Burgan storage facility. The Burgan pipeline will connect the existing Chevron refined product pipeline

to the Burgan storage facility. Product will be dispatched from the Burgan facility via the road loading

gantry. Burgan’s state of the art truck loading facility will allow for an efficient and swift distribution to

end-users with limited impact on the surroundings. Customers will pay Burgan a fee for the use of these

facilities based on throughput of product.

The layout of the facility is shown in Figure 2. The terminal is capable of performing the following

operations:

• Jetty operations

o vessel import

3

• Storage facilities

o diesel storage (Diesel 500ppm and 50ppm with separate biodiesel system) o petrol storage (ULP with ethanol blending) o truck loading facility o Additive blending facility

• Pipeline connections

o pipeline import from Chevron refinery

Figure 2 Layout of the facility

2.3 Value to the economy

Ports are considered an integral part of the petroleum industry’s logistical value chain. However, the

increased demand for imports has put additional strains on Cape Town harbour. This will be amplified in

the future as there is a rapidly growing demand for cleaner fuels in the South African market.

Infrastructure to handle additional imports will therefore be critical. This project will result in increased

fuel storage infrastructure and allow for fuel importation thereby increasing the security of supply to the

Western Cape. The project will also help with improving the fuel distribution capacity in the Western

Cape. There have been cases of long queues and congestion at the current road loading gantries. Last

but not least is that the Burgan facility is an independent facility. i.e. it does not belong to a marketer.

This means any company with a market in Cape Town will be able to import and distribute product. The

facility will therefore enable the entrance of new players thus improving competition. The Burgan

project is compatible with and supportive of key policies and plans that include: The Liquid Fuels Energy

Security Master Plan (2007), The Port of Cape Town Port Development Plan (2013), The Draft Strategic

Stocks Petroleum Policy (2013), The National Development Plan (2012), Competition policy with respect

to the petroleum industry and The Review of Fuel Specifications and Standards (2011). Government has

included Burgan Cape Terminals as a strategic project under Operation Phakisa.

In addition, the Burgan facility will have a positive impact on security of supply in Cape Town and the

Western Cape in the following unplanned circumstances:

4

A harbour incident involving a vessel at either of the existing bulk liquid berths.

A refinery incident (fire, critical equipment failure, industrial action) which causes an

unplanned outage or slowdown of more than 6 weeks.

Damage to or failure of Chevron’s 13km white oil pipeline linking the refinery to the

harbour.

An urgent demand by Eskom for diesel as a result of county wide power shortages

The facility will also enable the following benefits to be achieved:

Making imported diesel50 available to all motorists whose vehicles require these grades and

bridging the supply gap due to the likely delay in meeting the target date of July 2017 for

refineries to upgrade to produce these fuels.

Provide storage for Clean Fuel strategic stock holding requirements4.

2.4 Purpose of this tariff application

On 9 December 2014, the Energy Regulator issued a combined licence (PPL.sf.lf.F3/174/2014) to Burgan

Cape Terminals for the operation of a petroleum storage facility, a petroleum loading facility and a

petroleum pipeline. This tariff application is submitted to NERSA in order to comply with license

condition 16 of the operating license.

In this tariff application Burgan requests NERSA to:

Approve the tariff for the Loading facility

Approve the tariff for the Storage facility

Set the tariff for the Pipeline

3 The Facility

The facility comprises marine loading arms, transfer pipes to a storage tank farm, a storage tank farm,

transfer pipes to the road loading gantry, a road loading gantry and a pipeline connecting the storage

facility to the Chevron refined product pipeline. The set of infrastructure to be built and operated is set

out in more detail in the combined licence construction application and the combined licence operation

application. In summary the separate facilities consist of the following:

Loading facility

The loading facility will be mounted on the Eastern Mole Berth 2. The loading facility consists of two 12

inch diameter marine loading arms that are capable of 1 250m3 per hour for each arm and two auxiliary

16 inch diameter (approximately 156 meter long) bidirectional pipelines. The pipelines run between the

4 The Draft Strategic Stocks Petroleum Policy, DOE (2013). The policy identifies the age of the refineries as a strategic concern that may severely disrupt supply of refined product. The draft policy recommends that petroleum manufacturers hold 14 days of refined product stocks relative to their respective market shares.

5

loading arms on Eastern Mole Berth 2 and the storage facility. The facility will therefore be capable of

loading and offloading tanker vessels.

Storage facility and auxiliary equipment

The storage facility will be located on the Eastern Mole. The storage facility will consist of 12 storage

tanks with a combined maximum storage capacity of approximately 118 670 m3 and a combined

working storage capacity of approximately 109 400 m3. The storage tank area will be covered in a raft

type foundation which will be reinforced by concrete piles. The storage tanks will be surrounded by a

bund wall with a capacity of 110% of the total tank capacity for that bund area. The storage tanks will be

able to store petrol, diesel, ethanol and bio fame. The majority of the product consisting of diesel and

unleaded petrol (ULP) will be received via the Eastern Mole Berth 2 and the Chevron Oil Refinery.

Ethanol, biodiesel and other additives needed for blending will be received via road tanker. All product

will leave the storage facility by road tanker. The distribution facility will include a 5 truck loading gantry

capable of loading multiple products simultaneously. The auxiliary infrastructure includes an office

block, fire-fighting system and a drainage system.

Pipeline

The pipeline to be constructed will be a 10 inch diameter (approximately 700 meter long) bidirectional

pipeline which will run above ground connecting the storage facility to the Chevron 12 inch diameter

refined product (“white oil”) pipeline. The pipeline will run aboveground alongside the Eastern Mole

Berth service road and enter the Burgan terminal past the FFS Refiners (Pty) Ltd facility, terminating at

the Burgan import fuel manifold.

4 Tariff methodology

4.1 Imposing a regulated tariff in a competitive environment

Although subject to NERSA regulation, the storage market is an increasingly competitive environment.

The tariff that Burgan is able to charge for storage services is thus dictated less by what the regulatory

framework will allow, and entirely by what the market is prepared to pay at any given point in time. This

is a vital consideration when determining the tariff path over time that Burgan requests NERSA to

approve.

Section 28(3) of the Petroleum Pipeline Act (60 of 2003) states the following:

(3) The tariffs set or approved by the Authority must enable the licensee to -

(a) recover the investment;

(b) operate and maintain the system; and

(c) make a profit commensurate with the risk.

6

The Act requires that the tariffs that NERSA approves (in other words the tariff path over the life of the

project) “must enable” the licensee to recover the full costs of providing the service – in other words the

approved tariffs have to comply with section 28(3) of the Act and with Regulation 4(2). For tariffs to

“enable” the full recovery of costs they must be:

Cost reflective (result in tariff levels over the life of the project that are fully reflective of the

costs); and

Recoverable (result in tariff levels that are in practice recoverable in the market over the life of

the project).

In order to compete in the storage market Burgan will have to offer commercial pricing arrangements

that are competitive and similar to what customers would expect from other suppliers in the market.

The recoverability of the tariff is thus a primary consideration when choosing the appropriate

methodology for calculating the lifetime tariff trajectory for approval by NERSA. As most commercial

storage contracts are of a multi-year nature and subject to some annual inflationary clause, the

approved tariff needs to incorporate some inflationary escalation. Rate-of-return (ROR) methods as

used for the setting of petroleum pipeline tariffs and historically for storage and loading tariffs result in

tariffs that fall in real terms over the life of the project and thus are structurally inappropriate for a

market whose expectation is to contract around constant real tariffs.

Whilst in reality the market price for new storage contracts will likely fluctuate over the life of the

project subject to the cyclical vagaries of the petroleum market, the contracts will be structured with

annually escalating clauses tied to inflation. The best proxy for the market price is thus a tariff that is

constant in real terms over the life of the project that allows the recovery of sufficient revenue to satisfy

the cost-recovery and profit provisions of the Act and Regulations.

4.2 Tariff methodology per facility

Loading and storage facilities

Burgan has used the IOC tariff methodology5 comprehensive option in order to calculate the annual

allowable revenue for the loading and storage facilities. Due to the ramping of volumes at the start of

the project it is necessary to levelise these annual allowable revenues over all project volumes in order

to derive a real starting tariff and generate a tariff path that is recoverable. The starting tariff is

calculated by dividing the present value of the allowable revenues (calculated using the nominal After

Tax WACC) by the present value of the volumes over the life of the project (calculated using the real

After Tax WACC) in order to “levelise” the costs over the volumes and provide a constant real tariff. This

tariff must be indexed by inflation on an annual basis.

5 Tariff Methodology for Storage and Loading facilities Version 3, Approved 29 March 2016

7

Pipeline

The pipeline tariff is set by NERSA and Burgan has submitted all relevant information in order to

facilitate the calculation of the pipeline tariff based on the ROR method, in line with the latest NERSA

methodology for the setting of pipeline tariffs6. Burgan has calculated a proposed tariff for the pipeline

and the results of this calculation are presented in section 9.3.1.

4.3 Useful life

Burgan is bound by the contractual terms of the lease agreement signed with TNPA. As per the TNPA

lease agreement, the operational period of the terminal is defined as “a period of 20 years commencing

1 July 2017”. In addition, the TNPA lease agreement states that twelve months prior to the Handback

Date the Authority shall notify Burgan that the terminal will either be decommissioned or transferred to

the Authority (including equipment and works related to the development). Burgan is not privy to

TNPA’s future plans and intention on the use of its land beyond the end of the lease period. As such the

appropriate economic life of all the facilities is limited to the period of the lease agreement as there is

significant possibility that Burgan will need to decommission the entire site at the lease termination. In

any event, Burgan is unable to extract any revenue from the facilities beyond the termination of the

lease agreement.

The question of appropriate useful life is moot for the IOC calculation used for the loading and storage

facility tariffs, however this is an important consideration for the pipeline tariff. Burgan’s interactions

with NERSA regarding the appropriate useful life to use for tariff calculation purposes have indicated

that despite the aforementioned lease terms, NERSA would consider the physical life of the pipeline

asset when setting the tariff. Burgan’s engineering advisory has suggested that the physical life of the

pipeline is approximately 40 years before significant sustaining capex would be required to ensure a life

extension. The figure of 40 years has been used in Burgan’s calculation of the proposed tariff that NERSA

will set. We request however that should the terms of the lease agreement be enforced and that the

facility including the pipeline is due to be demolished, that the remaining asset value at that time be

depreciated to the end date of the lease.

5 The Project Costs

5.1 Capital expenditure

Capital expenditure is expected to be limited to a project development phase and a building phase,

spanning the periods from FY14 to FY17. Amounts for the second half of FY16 and later are based on

best estimates at time of application. The loading facility, storage facility and pipeline are all built as part

of the same EPC (Engineering, Procurement, and Construction) contract and thus the appropriate capex

6 Tariff methodology for the setting of pipeline tariffs in the Petroleum Pipelines industry, Version 7, Approved 29 October 2015

8

cost of each facility is based on a rational apportionment of the EPC cost between the facilities. This

apportionment has been based on a detailed assessment of the materials requirement and construction

complexity associated with each of the facilities. The Loading facility assets are demarcated by the exit

flange on each of the two 12 inch diameter pipelines linking the Marine loading arms to the storage

facility.

The pipeline asset is limited to the pipeline that connects the Chevron “white products” pipeline to the

storage facility and is bounded by the exit flange at the point where the pipeline enters the storage

facility.

5.2 Operating costs

There are no variable operating costs associated with the facilities.

The fixed operating costs for the Loading and Storage facilities consist of the following:

Direct Personnel

o Salaries / Wages o Training

Operating Expenses o Insurance o Utilities and Energy o Environment and Safety o Other Operating Expenses

Maintenance and Repairs7

Indirect Personnel Expenses o Salaries / Wages o Allowances o Training o Other Personnel Expenses

General Expenses o Travel o Consultancy and Professional Fees o Information and Communications Technology o Office costs o Property Tax

Lease I/C Cross Charge Indirect Costs

Due to the integrated nature of the operation of the loading and storage facilities it is not possible to

distinguish the operating costs easily between the facilities. Operating costs have been allocated to the

facilities based on the Capex allocation.

The pipeline is expected to incur negligible operating costs over its lifetime and this has been set to nil.

7 Maintenance and Repairs has been estimated at 2% of the replacement cost of the facility in accordance with the methodology

9

5.3 Decommissioning costs

Provision for decommissioning has been calculated in accordance with NERSA’s proposed methodology

as set out in the Frequently Asked Questions related to the methodology for the Setting and Approval of

Tariffs in the Petroleum Pipelines Industry. In this respect the decommissioning cost is treated as an

operational expense.

The decommissioning amount is raised over the life of the project by calculating the real value of the

difference between the full liability and what has already been raised in money of the year in question.

The difference is divided by the number of years left of the project life to yield the amount that must be

raised for the current project year.

Decommissioning of a chemical plant involves the following key processes that should be taken into

account:

Decontamination

Dismantling

Disposal

Rehabilitation

Typical decommissioning and rehabilitation costs for a plant such as the Burgan Facility are in the order

of 5 – 10% of the capital expenditure. The actual quantum depends on a large number of variables,

including the extent to which the site must be restored to its original state. The decommissioning

expense has been set at a level that will not only allow Burgan to fulfil its obligations in terms of the

lease agreement with TNPA but will allow for sufficient funds to be transferred to TNPA at the

termination of the agreement for the ultimate complete dismantling and restoration of the site to its

present condition, should TNPA exercise its right to take over the assets. We have allowed for

decommissioning and rehabilitation costs at 8% of the capital expenditure.

5.4 Working capital

An assumption of 30 days has been made for both creditors and debtors resulting in the net working

capital requirement for the year being the difference between 30/365 of the annual revenue minus

30/365 of the annual operating expenses. The working capital allowance for the loading and storage

facilities has been calculated in accordance with the IOC tariff methodology by adding the annual

balance to the IOC-trended value of PPE.

Allowable revenue on working capital in our ROR calculation for the pipeline has been calculated by

allowing a nominal after tax WACC as the opportunity cost on the working capital balance. This is

different from the NERSA methodology where working capital is incorrectly added to the RAB and a real

return granted thereon. Working capital does not have an inflationary write-up each year and therefore

it is an error to apply a real after tax WACC to the working capital balance in the ROR method.8

8 We will provide NERSA with a simple demonstration model to prove this point if requested.

10

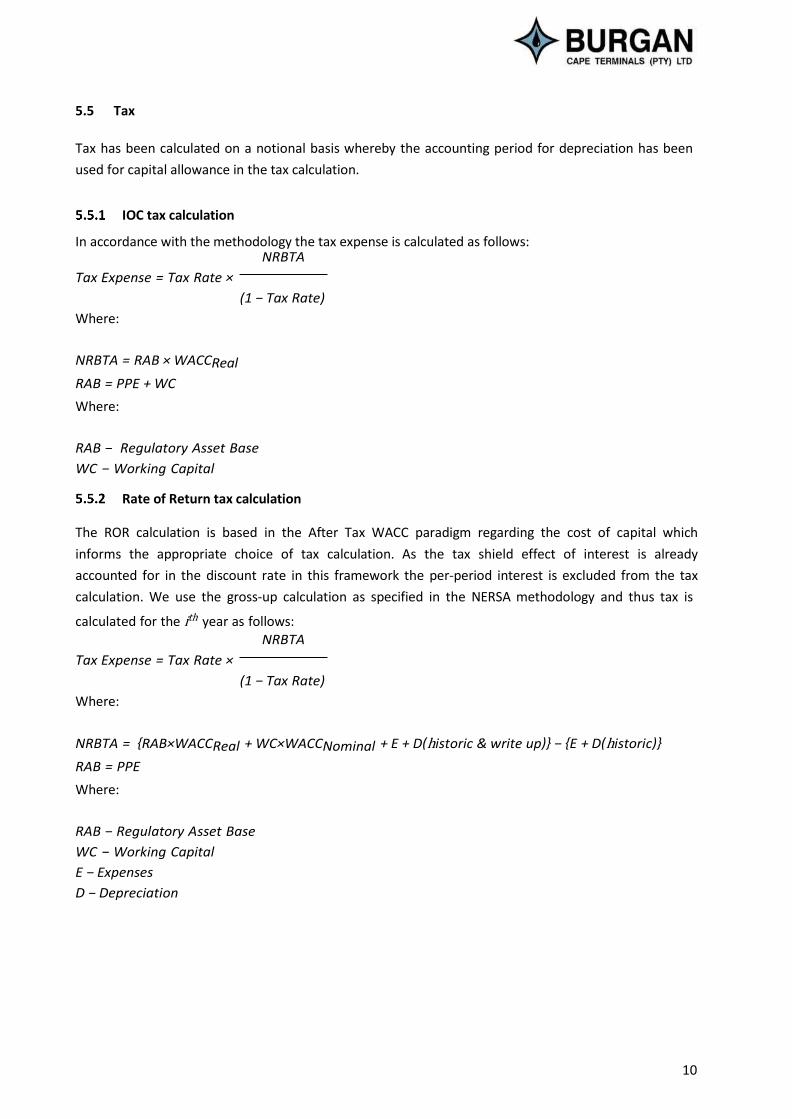

5.5 Tax

Tax has been calculated on a notional basis whereby the accounting period for depreciation has been

used for capital allowance in the tax calculation.

IOC tax calculation

In accordance with the methodology the tax expense is calculated as follows: NRBTA

Tax Expense = Tax Rate ×

(1 − Tax Rate)

Where:

NRBTA = RAB × WACCReal

RAB = PPE + WC

Where:

RAB − Regulatory Asset Base

WC − Working Capital

Rate of Return tax calculation

The ROR calculation is based in the After Tax WACC paradigm regarding the cost of capital which

informs the appropriate choice of tax calculation. As the tax shield effect of interest is already

accounted for in the discount rate in this framework the per-period interest is excluded from the tax

calculation. We use the gross-up calculation as specified in the NERSA methodology and thus tax is

calculated for the ith year as follows: NRBTA

Tax Expense = Tax Rate ×

(1 − Tax Rate)

Where:

NRBTA = {RAB×WACCReal + WC×WACCNominal + E + D(historic & write up)} − {E + D(historic)}

RAB = PPE

Where:

RAB − Regulatory Asset Base

WC − Working Capital

E − Expenses

D − Depreciation

11

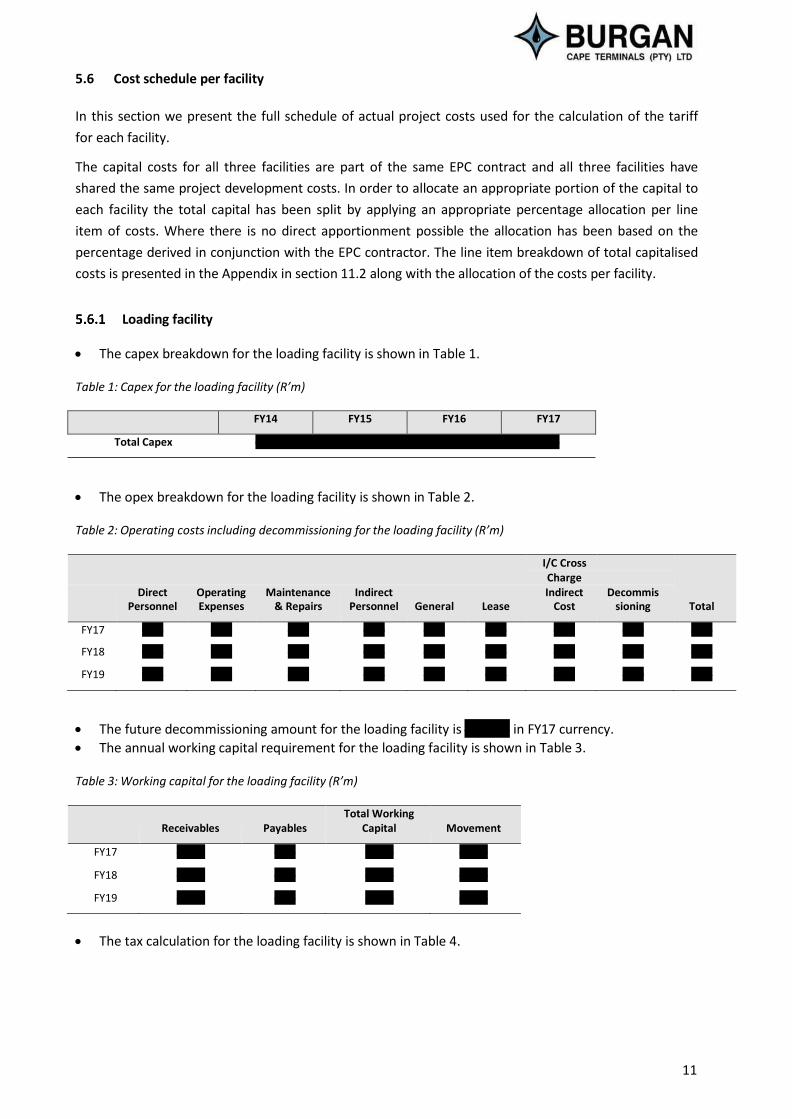

5.6 Cost schedule per facility

In this section we present the full schedule of actual project costs used for the calculation of the tariff

for each facility.

The capital costs for all three facilities are part of the same EPC contract and all three facilities have

shared the same project development costs. In order to allocate an appropriate portion of the capital to

each facility the total capital has been split by applying an appropriate percentage allocation per line

item of costs. Where there is no direct apportionment possible the allocation has been based on the

percentage derived in conjunction with the EPC contractor. The line item breakdown of total capitalised

costs is presented in the Appendix in section 11.2 along with the allocation of the costs per facility.

Loading facility

The capex breakdown for the loading facility is shown in Table 1.

Table 1: Capex for the loading facility (R’m)

FY14 FY15 FY16 FY17

Total Capex 0.47 1.63 13.80 6.08

The opex breakdown for the loading facility is shown in Table 2.

Table 2: Operating costs including decommissioning for the loading facility (R’m)

I/C Cross Charge

Direct Operating Maintenance Indirect Indirect Decommis Personnel Expenses & Repairs Personnel General Lease Cost sioning Total

FY17 0.17 0.18 0.46 0.20 0.55 0.27 0.00 0.09 1.93

FY18 0.18 0.19 0.49 0.22 0.58 0.30 0.00 0.09 2.05

FY19 0.19 0.20 0.51 0.23 0.62 0.33 0.00 0.10 2.18

The future decommissioning amount for the loading facility is R1.76m in FY17 currency.

The annual working capital requirement for the loading facility is shown in Table 3.

Table 3: Working capital for the loading facility (R’m)

Total Working Receivables Payables Capital Movement

FY17 (0.49) 0.15 (0.34) (0.34)

FY18 (0.53) 0.16 (0.37) (0.03)

FY19 (0.56) 0.17 (0.39) (0.02)

The tax calculation for the loading facility is shown in Table 4.

12

Table 4: Tax calculation for the loading facility (R’m)

RAB WACC (After

Tax, Real)

RAB x WACC

RAB x WACC (1 − Tax)

Tax

FY17 23.45 12.48% 2.93 4.06 (1.14)

FY18 25.11 12.54% 3.15 4.37 (1.22)

FY19 26.47 12.61% 3.34 4.64 (1.30)

Storage facility

The capex breakdown for the storage facility is shown in Table 5.

Table 5: Capex for the storage facility (R’m)

FY14 FY15 FY16 FY17

Total Capex 17.42 60.05 509.72 173.57

The opex breakdown for the storage facility is shown in Table 6.

Table 6: Operating costs including decommissioning for the storage facility (R’m)

FY17 5.84 6.11 16.03 7.08 19.13 9.33 0.12 3.07 66.71

FY18 6.19 6.53 16.93 7.50 20.23 10.26 0.12 3.24 71.00

FY19 6.56 6.98 17.84 7.95 21.49 11.29 0.13 3.41 75.67

The future decommissioning amount for the storage facility is R60.86m in FY17 currency.

The working capital requirement for the storage facility is shown in Table 7.

Table 7: Working capital for the storage facility (R’m)

Receivables Payables Total Working

Movement Capital

FY17 (17.09) 5.23 (11 .86) (11.86)

FY18 (18.33) 5.57 (12 .76) (0.90)

FY19 (19.47) 5.94 (13 .53) (0.76)

Direct Operating Maintenance Personnel Expenses & Repairs

Indirect Personnel

General Lease

I/C Cross Charge Indirect

Cost

Decommis sioning

Total

13

The tax calculation for the storage facility is shown in Table 8.

Table 8: Tax calculation for the storage facility (R’m)

RAB WACC (After

Tax, Real)

RAB x WACC

RAB x WACC (1 − Tax)

Tax

FY17 815.22 12.48% 101.72 141.27 (39.56)

FY18 872.73 12.54% 109.48 152.06 (42.58)

FY19 920.12 12.61% 116.05 161.18 (45.13)

Pipeline

The capex breakdown for the pipeline is shown in Table 9.

Table 9: Capex for the pipeline (R’m)

FY14 FY15 FY16 FY17

Total Capex 0.49 1.68 14.28 17.26

The opex breakdown for the pipeline is shown in Table 10.

Table 10: Operating costs including decommissioning for the pipeline (R’m)

Operating Costs Decommissioning Total

FY17 - 0.07 0.07

FY18 - 0.08 0.08

FY19 - 0.08 0.08

The future decommissioning amount for the pipeline is R2.70m in FY17 currency.

The net working capital requirement and the annual change in the net working capital requirement for the pipeline is shown in Table 11.

Table 11: Working capital for the pipeline (R’m)

FY17 (0.30) - (0.30) (0.30)

FY18 (0.62) - (0.62) (0.32)

FY19 (0.65) - (0.65) (0.03)

Receivables Payables Total Working

Capital Movement

14

The tax calculation for the pipeline is shown in Table 12. The tax calculation is based on the ROR tariff.

Table 12: Tax calculation for the pipeline

FY17 2.76 (0.41) - (0.07) 2.28 3.17 (0.89)

FY18 5.68 (0.85) - (0.08) 4.75 6.60 (1.85)

FY19 5.95 (0.85) - (0.08) 5.01 6.96 (1.95)

6 Regulatory Asset Base and the calculation of Trended Original Cost (TOC)

The calculation of a Regulatory Asset Base (RAB) based on the value of Plant, Property and Equipment is

required for both the IOC and ROR tariff calculation.

The tables below show the calculation of RAB using the IOC methodology for the loading and storage

assets and the TOC asset base for the Pipeline. The financing cost of work in progress is calculated at the

WACC (After Tax) until the plant is brought into operation. The financing cost is capitalised and used in

determining the total original cost to be trended from the year of first operation.

The IOC methodology applied to the loading and storage assets trends the RAB at CPI from the year the

plant is brought into operation.

In accordance with the TOC methodology the depreciation of the pipeline asset is on a straight line basis

from year of first operation in FY17 to the end of the pipeline physical life in FY56. Amortisation of the

inflation write-up has been calculated in accordance with the NERSA methodology.

6.1 Loading facility

The asset table for the loading facility is shown in Table 13.

Table 13: Asset table for the loading facility (R’m)

Capex

CWIP CWIP

CWIP

Financing Brought

Carried

Cost into

Forward Operation

IOC b / f

Current Period Write-Up

IOC c / f

Regulatory Asset Base

(PPE)

FY14 0.47 0.00 0. 00 0.47 0.00 0.00 0.00 0.00

FY15 1.63 0.09 0. 00 2.19 0.00 0.00 0.00 0.00

FY16 13.80 0.43 16 .42 0.00 0.00 0.00 16.42 0.00

FY17 6.08 0.00 6. 08 0.00 16.42 0.95 23.45 23.45

FY18 0.00 0.00 0. 00 0.00 23.45 1.31 24.77 24.77

FY19 0.00 0.00 0. 00 0.00 24.77 1.34 26.10 26.10

Revenue Capital Operating Decommis Income

Allowance Costs sioning Before Tax

Income Gross Up for Tax

Tax Expense

15

6.2 Storage facility

The asset table for the storage facility is shown in Table 14.

Table 14: Asset table for the storage facility (R’m)

Capex

CWIP CWIP

CWIP

Financing Brought

Carried

Cost into

Forward Operation

IOC b / f

Current Period Write-Up

IOC c / f

Regulatory Asset Base

(PPE)

FY14 17.42 0.00 0.00 17.42 0.00 0.00 0.00 0.00

FY15 60.05 3.32 0.00 80.78 0.00 0.00 0.00 0.00

FY16 509.72 15.97 606 .47 0.00 0.00 0.00 606.47 0.00

FY17 173.57 0.00 173 .57 0.00 606.47 35.18 815.22 815.22

FY18 0.00 0.00 0.00 0.00 815.22 45.65 860.87 860.87

FY19 0.00 0.00 0.00 0.00 860.87 46.49 907.36 907.36

6.3 Pipeline

The asset table for the pipeline is shown in Table 15.

Table 15: Asset table for the pipeline (R’m)

0.00 0.00 0.00 0.00 0.00 0.00

0.00 0.00 0.00 0.00 0.00 0.00

0.00 0.00 0.00 16.99 0.00 0.00

0.99 0.02 0.96 34.79 0.45 17.97

2.91 0.07 2.83 35.79 0.94 36.73

4.77 0.13 4.64 36.73 0.99 37.73

16

Write-Up Bal on which Return Earned

Write-Up Amortisation

Accumulated TOC c/f

Write-Up c/f

Total Depreciation

& Amortisation

Regulatory Asset Base

(PPE)

Capex CWIP

CWIP CWIP

Financing Brought

Carried

Cost into

Forward Operation

Current Period

Depreciation

Depreciated Original Cost c/f

Current Period

Write-Up

FY14 0.49 0.00 0.00 0.49 0.00 0.00 0.00

FY15 1.68 0.09 0.00 2.26 0.00 0.00 0.00

FY16 14.28 0.45 16. 99 0.00 0.00 16.99 0.00

FY17 17.26 0.00 17. 26 0.00 0.42 33.83 0.99

FY18 0.00 0.00 0.00 0.00 0.87 32.96 1.95

FY19 0.00 0.00 0.00 0.00 0.87 32.09 1.93

17

7 Discount Rate

As described in the tariff methodologies in section 4, the applicable discount rate for the IOC tariff

calculation performed in this application is the After Tax WACC. The ROR calculations performed to

calculate the pipeline tariff also require an after tax WACC to be used as the discount rate. In this

section we specify Burgan’s cost of equity, debt and the resultant WACC.

7.1 Cost of equity

The cost of equity is built up using the Capital Asset Pricing model. The method we have used is

informed by NERSA’s “Cost of Equity Adjustments Discussion Document for Petroleum Storage and

Loading Facilities”, 6th May 2014. We have additionally made use of the PWC Valuation Methodology

Survey, 7th Edition, 2014/20159.

We consider three adjustments to the market-derived cost of equity – a small stock premium, a project

specific risk premium and a liquidity premium. The liquidity premium is treated as a multiplier on all

other cost of equity factors as contemplated in NERSA’s FAQ document.

Our Cost of equity calculation is thus as follows: Ke = (Rf + MRP × Beta + SSP + a)× (1 + LP)

Where:

Ke − real after tax cost of equity

Rf − real risk free rate

MRP − market risk premium

Beta − appropriate stock Beta i. e. taking account of gearing −

SSP − small stock premium

a − Project Specific Risk

LP − liquidity premium

The individual elements of the calculation are described below:

9 Africa: A close look at value - Valuation methodology survey 2014/15, 7th edition, PWC (2015). Available at http://www.pwc.co.za/valuation-survey

18

Risk free rate

As determined from NERSA’s provided data10 for the tariff period 1 Jan 2017 – 31 Dec 2017 a value of

3.73% has been used.

Market risk premium

As determined from NERSA’s provided data for the tariff period 1 Jan 2017 – 31 Dec 2017 a value of

6.35% has been used.

Beta

Beta has been determined from NERSA’s document11 for the tariff period 1 Jan 2017 – 31 Dec 2017. The

unlevered value of 0.57 is used in our modelling and levered to 0.88 at a gearing level of 35% once debt

is incurred.

Small stock premium

The small stock premium assumed for Burgan is due to the following reasons:

1. Burgan is a small unlisted company which has recently been formed

2. Burgan has no access to legal expertise within its own structures, these services are purchased from

external legal counsel

3. Burgan has to purchase legal, operational and technical expertise from third parties rather than in-

house expertise

4. Burgan has never had access to operational and technical expertise under a previous shareholding

dispensation

5. Burgan is a new operator within the South African context

Using the PWC Valuation Methodology survey 2014/15 as a guide we use a small stock premium of 3.8%

based on the initial RAB and Table 16 from page 54 of the survey.

Table 16: Small stock premium (PWC Valuation Methodology Survey 2014/15)

2014 6.5% 5.2% 3.8% 2.3% 1.5% 0.7%

2012 6.7% 4.4% 2.8% 1.7% 0.9% 0.1%

2010 4.9% 3.7% 2.8% 1.3% 0.7% 0.1%

2007 5.2% 4.0% 2.7% 1.7% 1.3% 0.4%

10 Document from Nersa website: Economic Data – 30YR Market Risk Premium up to January 2016 – Petroleum Pipelines Industry.xls

11 Document from Nersa website: Beta Values – January 2015 – March 2016 Tariff Gearing May 2016 – Petroleum Pipelines Industry.pdf

Rm 0 – 250 251 – 500 501 – 1000 1001 – 1500 1501 – 2000 2001+

19

Project specific risk

The project specific risk assumed for Burgan is based on the following reasons:

1. The Eastern Mole project is a Greenfield project and is a completely new activity (independent

import terminal) with no similar previous undertaking and thus has numerous unquantifiable risks

which might only be encountered during the construction and operational phase of the project.

2. Burgan being an independent storage terminal owner and operator is fully exposed to the oil

marketers in Western Cape as potential customers to the terminal. Although discussions with these

potential customers have started, until sufficient long term contracts are signed, the returns of the

investment are uncertain. This is unlike the existing assets in Cape Town which are owned and

operated by oil marketers who have their respective market volume to utilize the assets. Note further

that Burgan will bear the risk of not finding replacement off-take agreements should the initial long-

term contracts come to an end.

3. The Eastern Mole project will be built on reclaimed land within the Port of Cape Town and as such

has brought about construction challenges due to voids etc. within the ground. These issues may

require Burgan to pile to bedrock in order to construct the planned terminals which might trigger

other potential challenges. Furthermore these challenges may impact on the construction period of

the project and given that the lease period is limited to an operational period of 20 years. This could

significantly reduce the period in which Burgan may generate returns to fund the project.

4. With no additional land/space for further expansion, Burgan’s return on this project is limited to the

current terminal design of 118,670 m3 i.e. there are no further opportunities for Burgan to generate

additional revenues from the site.

5. Competition from incumbent oil marketers who have older depreciated assets, long term

presence/experience in the South African market and coupled with strong corporate support in the

form of ‘steady state’ volumes and prices. Burgan does not have this kind of support and may need

to reduce its tariffs to compete within the market despite a higher NERSA tariff being granted. Given

the above there is further risk to Burgan that the asset may not generate the required returns to fund

the project. Note there are competing berths and pipelines currently in operation in the port of Cape

Town.

6. Burgan is being constructed based on a view of expected supply and demand factors within the port

of Cape Town. Should the above expectations not materialize there is significant market risk

exposure that the required returns for the project will not be met.

7. NERSA’s recent methodology revision has removed the claw-back provision resulting in the licensee

i.e. Burgan, shouldering the risk of annual volume fluctuations and their impact on project cash flows.

Variations in project cash flows, cash flow timing risk or financing risk, will impact considerably on the

returns Burgan expects to generate from the Eastern Mole project. Furthermore given that Burgan is

an independent storage company and not an integrated oil major, volume variations (and

consequently cash flow timing risk) are far more likely. This situation is further exacerbated by the

limited operating period for Burgan under the TNPA lease.

8. In order to meet some of its operational requirements, Burgan will need to connect to and leverage

off the Chevron pipeline. It is submitted that Burgan has little to no control over the Chevron

pipeline and any factors (outside of the control of Burgan) will impact on the returns of the project.

This infrastructural risk can manifest in the form of an inability to service a customer’s needs to

unscheduled stoppages and down time.

9. TNPA Lease agreement. Burgan faces additional project risks in respect of the lease agreement with

TNPA, for example the lease escalation is not fixed nor tied to CPI. Furthermore the lease expires in

20

2037 with Burgan being obliged to vacate and clear the site or hand over the site to TNPA, thus there

is at this stage no prospect for Burgan to generate revenue from the facility after this date.

While the determination of a project risk adjustment is a very subjective exercise, Burgan has attempted

to analyse the adjustment applied to the factors described above in Table 17.

Table 17: Risk assessment of the Burgan project

Risk Rate Assumed Likely Rate Range Refer above

Finance/cash flow 3.0% 2% - 8% 1, 2, 3, 5, 7

Market 1.25% 1% - 5% 5, 6

Other 0.75% 0.25% - 5% 2, 4, 8

Total 5.00% 3.25% - 18%

The rate assumed for project risk is within the ranges indicated in the PWC Valuation methodology

survey 2014/2015 for Southern Africa for adding specific risk premiums which falls between 1%-4% for

lower ranges and 5%-10% for upper ranges.

Liquidity risk

A liquidity risk premium of 5% has been assumed.

The liquidity risk premium assumed for Burgan is due to the following reasons:

1. Burgan shares are not publicly traded nor listed on any public exchange

2. Burgan’s main shareholder, VTTI, is not listed on any public exchange nor are its shares publicly

traded

3. Burgan has limited access to financial markets and institutions for the purposes of raising finance

5% is in line with the value proposed in NERSA’s discussion document12.

Calculation of Ke

Using the parameters described above and the equation for Ke the real after tax cost of equity can be

calculated as follows:

Ke = (Rf + MRP × Beta + SSP + a)× (1 + LP)

= (3.73% + 6.35%×0.88 + 3.80% + 5.00%)×(1 + 5%)

= 19.02% This figure represents a total premium above the market of 9.70%13

12 Cost Of Equity Adjustments Discussion Document For Petroleum Storage And Loading Facilities, 6th May 2014,Page 17, Nersa (2014)

13 19.02% - (3.73% + 6.35% x 0.88)

21

Real Ke Nominal Ke

Discount Factors Discount Factors

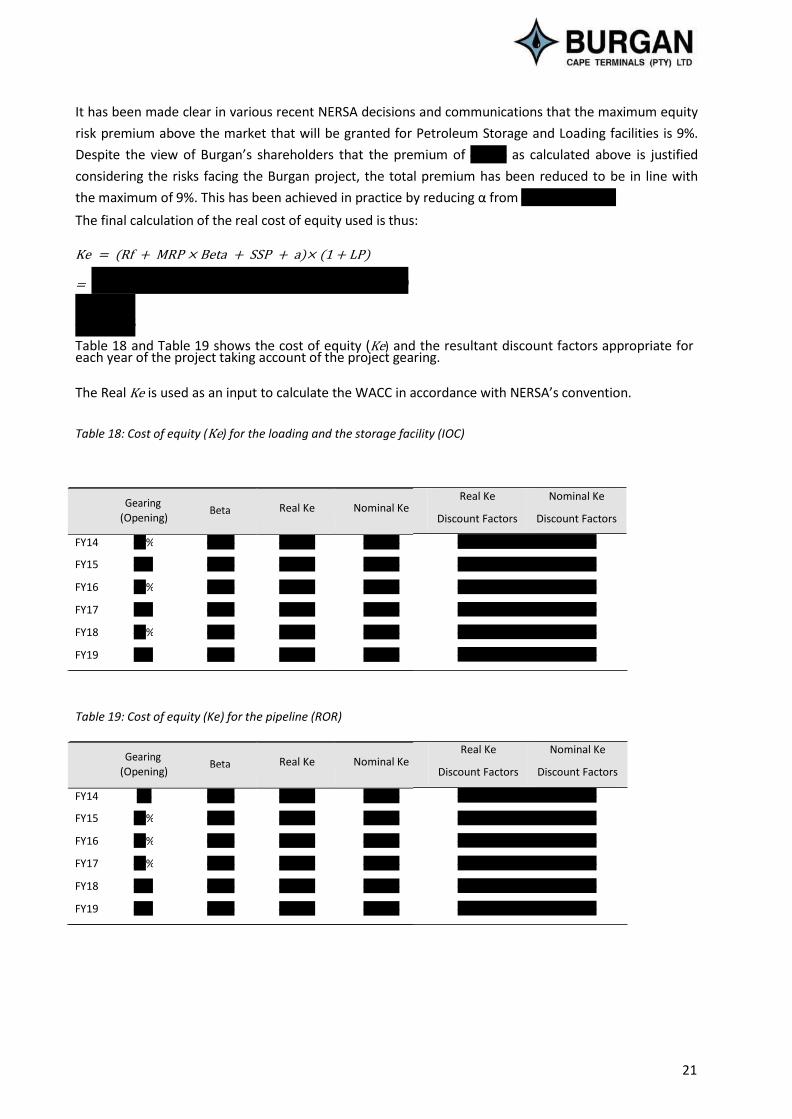

It has been made clear in various recent NERSA decisions and communications that the maximum equity

risk premium above the market that will be granted for Petroleum Storage and Loading facilities is 9%.

Despite the view of Burgan’s shareholders that the premium of 9.70% as calculated above is justified

considering the risks facing the Burgan project, the total premium has been reduced to be in line with

the maximum of 9%. This has been achieved in practice by reducing α from 5.00% to 4.33%.

The final calculation of the real cost of equity used is thus:

Ke = (Rf + MRP × Beta + SSP + a)× (1 + LP)

= (3.73% + 6.35%×0.88 + 3.80% + 4.33%)×(1 + 5%)

= 18.30%

Table 18 and Table 19 shows the cost of equity (Ke) and the resultant discount factors appropriate for each year of the project taking account of the project gearing.

The Real Ke is used as an input to calculate the WACC in accordance with NERSA’s convention.

Table 18: Cost of equity (Ke) for the loading and the storage facility (IOC)

1.65560 1.98723

1.39949 1.58135

1.18300 1.25161

1.00000 1.00000

0.84531 0.80048

0.71455 0.64199

Table 19: Cost of equity (Ke) for the pipeline (ROR)

1.65560 1.98723

1.39949 1.58135

1.18300 1.25161

1.00000 1.00000

0.84531 0.80048

0.71455 0.64199

Real Ke Nominal Ke

Discount Factors Discount Factors

Gearing Beta

(Opening)

Real Ke

Nominal Ke

FY14 35% 0.877 18.30% 23.54%

FY15 35% 0.877 18.30% 25.67%

FY16 35% 0.877 18.30% 26.34%

FY17 35% 0.877 18.30% 25.16%

FY18 35% 0.877 18.30% 24.92%

FY19 35% 0.877 18.30% 24.69%

Gearing Beta

(Opening)

Real Ke

Nominal Ke

FY14 0% 0.570 16.25% 21.40%

FY15 35% 0.877 18.30% 25.67%

FY16 35% 0.877 18.30% 26.34%

FY17 35% 0.877 18.30% 25.16%

FY18 35% 0.877 18.30% 24.92%

FY19 35% 0.877 18.30% 24.69%

22

7.2 Gearing and cost of debt

For the purpose of this tariff application debt has been modelled as a constant 35% of the asset base in

line with the IOC methodology for the Loading and Storage facility. For the pipeline ROR calculation the

TOC gearing is zero in FY14 and thereafter modelled as a constant 35% of TOC assets for the remaining

periods of the project i.e. from FY15 – FY37, in order to maintain consistency with Burgan’s expected

capital structuring schedule.

Based on the interactions with potential lenders to date, the Prime rate is a reasonable estimate of the

cost of debt that Burgan will be able to raise. As at time of application this would indicate a debt cost of

10.50% before Tax, yielding 7.56% After Tax. Using Burgan’s assumption of 5.8% for inflation for FY17

the Real After tax cost of debt is 1.66% for FY17.

7.3 Weighted Average Cost of Capital (WACC)

As described earlier the after tax WACC is required for both the IOC annual allowable revenue

calculation and the ROR method.

The appropriate values for WACC are shown in Table 20 and Table 21 using the above calculations for

the cost of equity (Ke), the cost of debt (Kd), the gearing assumptions and the macro-economic

estimates. The discount factors are based in FY17 in order to derive the FY17 tariff. All present values

are thus FY17 values.

Table 20: Weighted Average Cost of Capital (WACC) for the loading and storage facility

1.41360 1.69675

1.26137 1.42527

1.12477 1.19001

1.00000 1.00000

0.88854 0.84142

0.78902 0.70890

Table 21: Weighted Average Cost of Capital (WACC) for the pipeline

1.413595591 1.696746723

1.26137 1.42527

1.12477 1.19001

1.00000 1.00000

After Tax WACC After Tax WACC Discount Factor Discount Factor

Real Nominal

After Tax WACC After Tax WACC Discount Factor Discount Factor

Real Nominal

Gearing (Opening)

Ke (after Tax, Real)

Kd (after Tax, Real)

After Tax WACC Real

After Tax WACC Nominal

FY14 35% 18.30% 2.01% 12.60% 17.59%

FY15 35% 18.30% 0.50% 12.07% 19.05%

FY16 35% 18.30% 0.71% 12.14% 19.77%

FY17 35% 18.30% 1.66% 12.48% 19.00%

FY18 35% 18.30% 1.86% 12.54% 18.85%

FY19 35% 18.30% 2.05% 12.61% 18.69%

Gearing (Opening)

Ke (after Tax, Real)

Kd (after Tax, Real)

After Tax WACC Real

After Tax WACC Nominal

FY14 0% 16.25% 2.01% 16.25% 21.40%

FY15 35% 18.30% 0.50% 12.07% 19.05%

FY16 35% 18.30% 0.71% 12.14% 19.77%

FY17 35% 18.30% 1.66% 12.48% 19.00%

23

0.88854 0.84142

0.78902 0.70890

8 Volume forecast

8.1 Total volumes

Burgan will run its operation on a throughput basis, charging customers per cubic metre of product

dispatched from the terminal. Actual throughput rates achieved per year will fluctuate substantially

depending on factors outside of Burgan’s control and related to the business requirements of its

customers. In order to ensure the maximum efficient use of the assets Burgan will contract with its

customers based on minimum annual throughput through the use of take-or-pay provisions.

In order to calculate a reasonable annual throughput volume forecast for tariff calculation purposes

Burgan has considered the constraints on the terminal’s outbound capacity (the inbound capacity being

subject to fewer constraints). The outbound capacity is limited by health, safety and environmental

considerations. These relate to the extent to which the terminal infrastructure is utilised in order to

maximise the number of tank turns, and the natural restrictions on the dispatch of product by road

created by traffic considerations through the port area. Due to safety restrictions tanker truck vehicles

may not operate after 10pm and before 5am which restricts the ability for the terminal to operate in a

true 24/7 mode. Table 22 shows the calculation of annual throughput based on a conservative

assumption of average truck capacity, resulting in a figure of 928.2 million litres. NERSA’s own

assessment of the terminal capacity as stated in the RFD for the operating license suggested an annual

throughput volume of 1 051 200m3 (1 051.2 million litres) based on a traffic study associated with the

Environmental Impact Assessment process.

For tariff calculation purposes Burgan has assumed an annual volume of 1 000 million litres. This figure

is considered to be a reasonable assessment of the capacity of the terminal.

Table 22: Throughput capacity for Burgan terminal

Amount Unit

Average Truck Capacity 30 m3

0.03 million litres

Number of Loading Bays 5

Loading Bay Dispatch Rate 1 trucks per hour

Hours per Day 17

Days per Week 7

Weeks per Year 52

Total Throughput 928.2 million litres per annum

After Tax WACC After Tax WACC Discount Factor Discount Factor

Real Nominal

Gearing Ke (after Kd (after After Tax After Tax WACC (Opening) Tax, Real) Tax, Real) WACC Real Nominal

FY18 35% 18.30% 1.86% 12.54% 18.85%

FY19 35% 18.30% 2.05% 12.61% 18.69%

24

Burgan expects to begin operations in mid FY17 and thus will not have full throughput for the FY17

financial year. A throughput capacity of 500 million litres has been assumed for the first year of

operation. As Burgan’s lease agreement with TNPA terminates end of June FY37 the last financial year

will also only have half a year’s volumes.

Burgan expects to receive product into the terminal via both the loading facility and the pipeline. Based

on current indications from customers the volume split is expected to be 45% via the Loading facility

and 55% via the pipeline. Table 23 shows the volume forecast for each facility for all operational years

considered in this application.

Table 23: Volume forecast (million litres)

500

1 000

1 000

9 Tariff calculation

In this section we present the calculation of the loading, storage and pipeline tariffs. The loading and

storage tariffs are calculated using the IOC formulation of section 4.2.1 levelised over the project

volumes which results in a base value for FY17 that must be escalated by inflation for subsequent years

of the project. We calculate the estimated future tariff and tabulate the estimated revenue for each

year of the project based on the estimated inflation and volume assumptions.

As NERSA will set the pipeline tariff using the ROR /Allowable Revenue methodology we have calculated

a tariff using this methodology for the pipeline.

9.1 Loading facility tariff calculation

Levelised IOC tariff calculation for the loading facility

Table 24 shows the annual allowable revenue calculation for the loading facility.

Storage Facility

Loading Pipeline

Facility

FY17 22 5 275

FY18 45 0 550

FY19 45 0 550

25

Table 24: Allowable revenue for the loading facility using the IOC method (R’m)

FY17 2.93 1.84 0.09 1.14 5.99

FY18 3.15 1.96 0.09 1.22 6.42

FY19 3.34 2.09 0.10 1.30 6.82

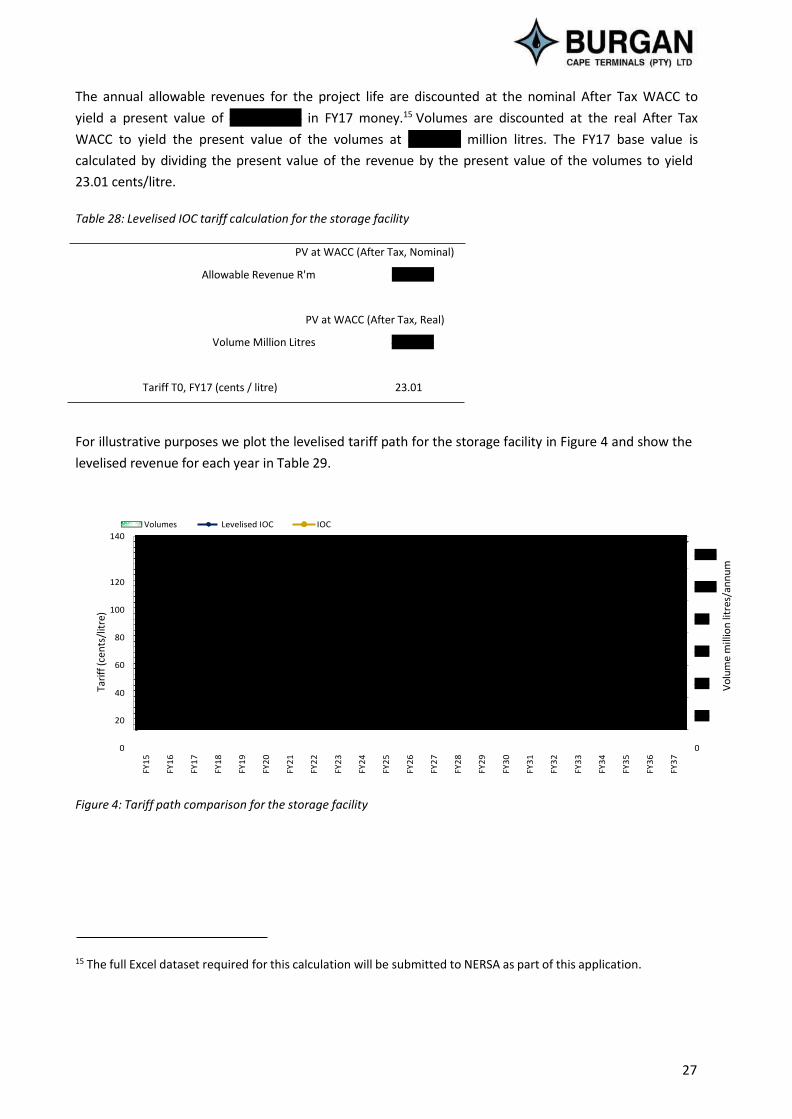

The annual allowable revenues for the project life are discounted at the nominal After Tax WACC to

yield a present value of R50.69m in FY17 money.14 Volumes are discounted at the real After Tax WACC

to yield the present value of the volumes at 3 442.29 million litres. The FY17 base value is calculated by

dividing the present value of the revenue by the present value of the volumes to yield 1.47 cents/litre in

FY17 money.

Table 25: Levelised IOC tariff calculation for the loading facility

PV at WACC (After Tax, Nominal)

Allowable Revenue R'm 50.69

PV at WACC (After Tax, Real)

Volume Million Litres 3 442.29

Tariff T0, FY17 (cents / litre) 1.47

For illustrative purposes we plot the levelised tariff path for the loading facility in Figure 3 and show the

levelised revenue for each year in Table 26.

14 The full Excel dataset required for this calculation will be submitted to NERSA as part of this application.

Return on RAB

Operating Costs

Decommissioning Tax Total

Allowable Revenue

26

Volumes Levelised IOC IOC

9

8

7

6

5

4

3

2

1

0

500

450

400

350

300

250

200

150

100

50

0

Figure 3: Tariff path comparison for the loading facility

Table 26: Levelised IOC tariff and revenue for the loading facility

Volume million IOC Allowable IOC Tariff Levelised IOC Levelised IOC litres Revenue R'm cents/litre Tariff cents/litre Revenue R'm

FY17 225 5.99 2.66 1.47 3.31

FY18 450 6.42 1.43 1.55 7.00

FY19 450 6.82 1.52 1.64 7.38

9.2 Storage facility tariff

Levelised IOC tariff calculation for the storage facility

Table 27 shows the annual allowable revenue calculation for the storage facility.

Table 27: Allowable revenue for the storage facility using the IOC method (R’m)

FY17 101.72 63.64 3.07 39.56 207.98

FY18 109.48 67.77 3.24 42.58 223.06

FY19 116.05 72.25 3.41 45.13 236.85

Return on RAB

Operating Costs

Decommissioning Tax Total

Allowable Revenue

Tari

ff (

cen

ts/l

itre

)

FY1

5

FY1

6

FY1

7

FY1

8

FY1

9

FY2

0

FY2

1

FY2

2

Vo

lum

e m

illio

n li

tres

/an

nu

m

FY3

6

FY3

7

FY2

3

FY2

4

FY2

5

FY2

6

FY2

7

FY2

8

FY2

9

FY3

0

FY3

1

FY3

2

FY3

3

FY3

4

FY3

5

27

FY1

5

FY1

6

FY1

7

FY1

8

FY1

9

FY2

0

FY2

1

FY2

2

FY2

3

FY2

4

FY2

5

FY2

6

FY2

7

FY2

8

FY2

9

FY3

0

FY3

1

FY3

2

FY3

3

FY3

4

FY3

5

FY3

6

FY3

7

The annual allowable revenues for the project life are discounted at the nominal After Tax WACC to

yield a present value of R1 759.97m in FY17 money.15 Volumes are discounted at the real After Tax

WACC to yield the present value of the volumes at 7 649.54 million litres. The FY17 base value is

calculated by dividing the present value of the revenue by the present value of the volumes to yield

23.01 cents/litre.

Table 28: Levelised IOC tariff calculation for the storage facility

PV at WACC (After Tax, Nominal)

Allowable Revenue R'm 1 759.97

PV at WACC (After Tax, Real)

Volume Million Litres 7 649.54

Tariff T0, FY17 (cents / litre) 23.01

For illustrative purposes we plot the levelised tariff path for the storage facility in Figure 4 and show the

levelised revenue for each year in Table 29.

140

Volumes Levelised IOC IOC

1 200

120 1 000

100

80

60

40

20

800

600

400

200

0 0

Figure 4: Tariff path comparison for the storage facility

15 The full Excel dataset required for this calculation will be submitted to NERSA as part of this application.

Vo

lum

e m

illio

n li

tres

/an

nu

m

Tari

ff (

cen

ts/l

itre

)

28

Table 29: Levelised IOC tariff and revenue for the storage facility

Volume IOC Allowable IOC Tariff Levelised IOC Levelised IOC million litres Revenue R'm cents/litre Tariff cents/litre Revenue R'm

FY17 500 207.98 41.60 23.01 115.04

FY18 1 000 223.06 22.31 24.30 242.96

FY19 1 000 236.85 23.68 25.61 256.08

9.3 Pipeline tariff

Rate of Return tariff calculation for the pipeline

Following the NERSA methodology16, we use the ROR method to calculate the pipeline tariff. The

allowable revenue calculation for the pipeline is shown in Table 30. Return on Assets is calculated by

multiplying the RAB from Table 15 by the real After Tax WACC from Table 21. Return on Working Capital

is calculated by multiplying the total working capital of Table 11 by the nominal After Tax WACC from

Table 21. Depreciation and Amortisation is per Table 15 and the Operating costs, decommissioning

provision and tax expense are from the cost schedules in section 5.6.3.

Table 30: Allowable revenue for the pipeline using the rate-of-return tariff method (R’m)

FY17 2.24 0.00 0.45 - 0.07 0.89 3.65

FY18 4.61 0.06 0.94 - 0.08 1.85 7.53

FY19 4.76 0.12 0.99 - 0.08 1.95 7.90

The pipeline tariff for FY17 is given by

Allowable Revenue in FY17

Pipeline Tariff, FY17 =

=

Volume in FY17

R3.65m

275 million litres

= 1.33 cents/litre

We show the tariff path and throughput volume for the pipeline in Table 31 and Figure 5.

16 Tariff methodology for the setting of pipeline tariffs in the petroleum pipelines industry, Version 7, Approved 29 October 2015

Return on Return on

Assets Working

Capital

Depreciation and

Amortisation

Operating Costs Decommissioning Tax

Total Allowable Revenue

29

Volume million litres

Allowable Tariff cents/litre

Revenue R’m

FY1

5

FY1

6

FY1

7

FY1

8

FY1

9

FY2

0

FY2

1

FY2

2

FY2

3

FY2

4

FY2

5

FY2

6

FY2

7

FY2

8

FY2

9

FY3

0

FY3

1

FY3

2

FY3

3

FY3

4

FY3

5

FY3

6

FY3

7

Table 31 Tariff for the pipeline using the rate-of-return method

FY17 275 3.65 1.33

FY18 550 7.53 1.37

FY19 550 7.90 1.44

Volumes ROR

5

600

4.5

4

500

3.5

3

400

2.5 300

2

1.5

200

1

0.5

100

0 0

Figure 5: Tariff path and expected throughput for the pipeline

10 Conclusion and request for Approval and Setting of Tariffs

This tariff application is for loading, storage and pipeline tariffs to be charged by Burgan Cape Terminals.

For the loading and the storage facility we have made the case for NERSA to approve multi-year tariffs

starting from FY17 to FY19, based on the levelised IOC methodology. For the pipeline we have made the

case for NERSA to set a multi-year tariff for the period FY17 to FY19, based on the ROR methodology.

The terminal facilities have been operational since mid 2017 and will be operating up to the full capacity

of 1 000 million litres per year by 2018.

Burgan requests that NERSA approve the loading and storage tariffs, and sets the pipeline tariff as

follows:

10.1 Request for approval of the tariff for loading

For the marine loading facility Burgan requests that NERSA approve the maximum tariff for the FY17

period (1 January 2017 to 31 December 2017) of 1.47 cents/litre. Burgan further requests the approval

of an inflationary mechanism for future tariff periods up to FY19 as follows:

Vo

lum

e m

illio

n li

tres

/an

nu

m

Tari

ff (c

ents

/lit

re)

30

CP/

CP/

Tariff FYn = Tariff FYn-1×KCPI,n

The inflationary factor KCPI,n will be determined by dividing the CPI index value for the ninth month in

FYn-1 by the CPI index value twelve months prior. The inflationary factor KCPI,n and therefore the

tariff for FYn is thus known in the 10th month of the financial year prior to the new financial year

beginning.

This is illustrated by way of example as follows:

Assuming the financial year ends in December

Tariff determination for FY18 i.e. the period 1 January 2018 to 31 December 2018

CP/30 Sep 2017

Tariff FY 18 = Tariff FY17×

30 Sep 2016

CP/30 Sep 2017 will be published by STATSSA before the end of October 2017.

10.2 Request for approval of the tariff for storage

For the storage facility Burgan requests that NERSA approve the maximum tariff for the FY17 period (1

January 2017 to 31 December 2017) of 23.01 cents/litre. Burgan further requests the approval of an

inflationary mechanism for future tariff periods up to FY19 as follows:

Tariff FYn = Tariff FYn-1×KCPI,n

The inflationary factor KCPI,n will be determined by dividing the CPI index value for the ninth month in

FYn-1 by the CPI index value twelve months prior. The inflationary factor KCPI,n and therefore the

tariff for FYn is thus known in the 10th month of the financial year prior to the new financial year

beginning.

This is illustrated by way of example as follows:

Assuming the financial year ends in December

Tariff determination for FY18 i.e. the period 1 January 2018 to 31 December 2018

CP/30 Sep 2017

Tariff FY18 = Tariff FY17×

30 Sep 2016

CP/30 Sep 2017 will be published by STATSSA before the end of October 2017.

10.3 Request for setting of the pipeline tariff

Burgan requests that NERSA set a three-year tariff for the pipeline as set out in Table 31 above.

11 Appendix A

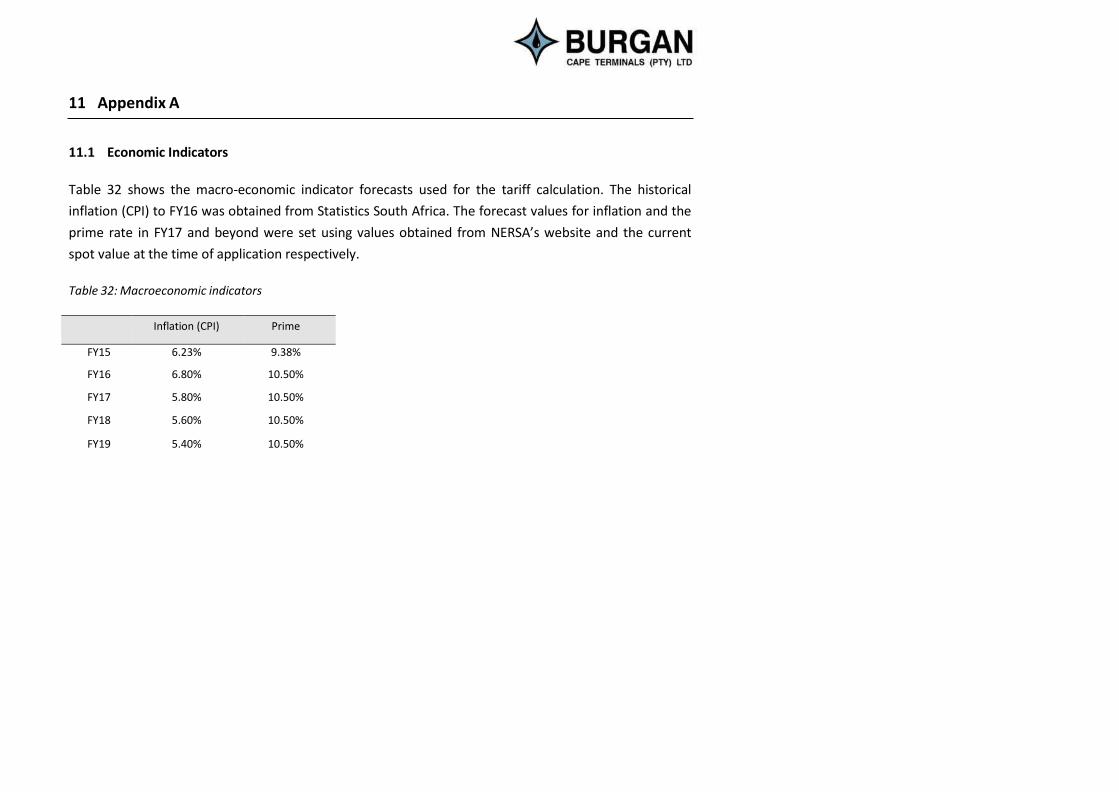

11.1 Economic Indicators

Table 32 shows the macro-economic indicator forecasts used for the tariff calculation. The historical

inflation (CPI) to FY16 was obtained from Statistics South Africa. The forecast values for inflation and the

prime rate in FY17 and beyond were set using values obtained from NERSA’s website and the current

spot value at the time of application respectively.

Table 32: Macroeconomic indicators

Inflation (CPI) Prime

FY15 6.23% 9.38%

FY16 6.80% 10.50%

FY17 5.80% 10.50%

FY18 5.60% 10.50%

FY19 5.40% 10.50%

11.2 Capital Expenditure and allocation per facility

Ref 1 Ref 2 Description Storage Loading Pipeline 2014 2015 2016 2017 1.0 100 Project Management Team 94.78% 2.57% 2.65% R - R 3 415 753 R 13 811 226 R 6 660 000 2.0 200 Flight Tickets - International 94.78% 2.57% 2.65% R - R 504 342 R 406 004 R 250 000 3.0 300 Flight Tickets - Local 94.78% 2.57% 2.65% R - R - R 5 190 R 10 000 4.0 400 Lodging / House Rental 94.78% 2.57% 2.65% R - R - R 816 967 R 12 154 5.0 500 Car Rental / Purchase 94.78% 2.57% 2.65% R - R 16 588 R 188 931 R 60 000 6.0 600 Visa Cost 94.78% 2.57% 2.65% R - R - R 390 R - 7.0 700 Transfers 94.78% 2.57% 2.65% R - R 6 289 R 5 650 R - 8.0 800 Laptops / Desktops 94.78% 2.57% 2.65% R - R - R 177 348 R - 9.0 900 Office Cost 94.78% 2.57% 2.65% R - R 57 920 R 373 028 R 180 000