Download - Broucher Page

February-2008

LOG ON TO BANGALORE

R E S I D E N T I A L R E A L E S T A T E R E V I E W

Key

R- Rising

F- falling

S- Stagnant

SS- Stagnant but likelt to strengthen

Sw- Stagnant but likely to weaken

Bangalore

A City Overview

?

Capital of India'.?It is the principal administrative, cultural, commercial & industrial center of Karnataka

?The city is the third-largest hub for high networth individuals (HNI/HNWI), after Mumbai & Delhi

?There are close to 61 engineering colleges in & around Bangalore

?With the roaring IT sector people from all over India and even abroad have made a beeline for the

city. Southern part of Bangalore especially Outer Ring Road and Electronic City witnessed huge IT

developments till recently.

? IT giants like IBM, Dell, Infosys, Wipro all have their campuses here. Bangalore has the highest

number of software professionals, a position it grabbed from Osaka, Japan.

?Apart from IT, the city is home to several heavy industries, aerospace, telecommunications,

machine

tools, heavy equipments & de fence establishments

?With the International Airport, the Metro Rail project, expressways, fly- overs, skywalks and

integrated townships on the anvil, the city will soon wear a new look

?Bangalore Development Authority's Comprehensive Development Plan – Master Plan 2015 talks of

vertical growth in the city. This would translate into more high-rises within the city.

?A flexible zoning system has been introduced with mixed land use, taking the ground realities into

consideration. There is enhancement of the floor area ratio (FAR) as well, upto a maximum of four,

depending on the zone and road width. A FAR upto there has been fixed for roads over 30 metres

This land of IT professionals has earned for itself sobriquets like the 'Silicon Valley of India' and 'IT

1

2

Area (Bangalore) 741 sq.km.

Location 12.97° N 77.56° E

Population (2001) 65.37 lacs

Decadal Population Growth Rate (19991-2001) 34.80%

No. of SEZs (notified as on Dec 24, 2007) 13

Total No. of Graduates (2001) 7.36 lacs

Consumer Price Index (as in Dec 2007) 551

% change in CPI Dec 2006-Dec 2007 6.2

Crime Rate 501.60

Residential Units to be delivered by Dec 2009 34,400

Source: ICICI Property Services, Ministry of Commerce & Industry, Dept. of Commerce, CSO, NCRB, Census of India -2001

Snapshot

No. of Households (2001) 14.61 lacs

House Ownership (2006): Owned 21.19 lacs

Rented 29.84 lacs

Provided by employer 0.85 lacs

Others 0.92 lacs

No. of property related transactions in Oct 2007 13,130

Growth/ Drop in the no. of property related transactions1%

in Oct 2007 over Q2 2007

Source: Census of India 2001, Marketing Whitebook 2007-08, ICICI Property Services

Residential Market

3

Average built-up area No. of units ready Total Supply

of an by Dec 2009 (ready by Dec 2009)apartment in in million sq.ft.

sq.ft.

North 1 BHK

2 BHK 1200 6750 8.1

3 BHK 1650 2250 3.7

4 BHK 3000 1000 6.0

(Villa)

South 1 BHK

2 BHK 1200 9000 10.8

3 BHK 1650 3000 4.95

4 BHK 3000 1500 4.5

East 1 BHK

2 BHK 1200 7500 9.0

3 BHK 1800 1000 1.8

4 BHK 3500 500 1.75

West 1 BHK

2 BHK 1200 700 0.84

3 BHK 1650 250 0.4

4 BHK 2500 100 .25

Central 1 BHK

2 BHK 1300 500 0.65

3 BHK 1800 250 0.45

4 BHK 3000 100 0.3

34400 53.49

Supply of Residential Units (By Grade A, B & C developers) coming up by December 2009

Source: ICICI Property Services

West

3%

Central

2%East

26%

South

40%

North

29%

Distribution of residential supply-no. of units(Category A, B, C developers)across Bangalore

Source: ICICI Property Services

4

North Bangalore South Bangalore East Bangalore West Bangalore Central Bangalore

Yashwanthpur Kothnur Whitefield Kengeri M. G. Road

Sahakar Nagar J P Nagar 6th & 7th Phase Brookefields R R Nagar Malleshwaram

HRBR Layout Sarjapur Road HSR Layout Uttarhalli Basavangudi

Ram Murthy Nagar Hosur Road Kaggadasapura Nagarbhavi Padmanabha Nagar

HBR Layout Bannerghatta Road Marathahalli Chandra Layout Koramangla

Bellary Road Kanakpura Road K R Puram Dr. Raj Kumar Vasanth Nagar

Yellahanka Gottegere Old Madras Road Vijay Nagar Indira Nagar

Sanjay Nagar & Vijaya Bank Colony C V Raman Nagar Rajaji Nagar Cox Town RMV Extn.

Banaswadi Electronic City Frazer Town

OMBR Layout Jaya Nagar Benson Town

Hebbal Outer Ring Road

5

S.No. Name Location Type Area

(in hectares)

1 WIPRO Ltd Sarjapur Road IT 6.5

2 WIPRO Ltd Electronic City IT 5.2

3 Vikas Telecom Ltd. Outer Ring Road, IT/ITES 36.9 EastTaluk,

4 Adarsh Prime Devarabaseenahalli, IT/ITES 27.9Projects Pvt. Ltd. Bhoganahalli &

Doddakanahalli

5 Tanglin Pattengere/ Mylasandra IT/ITES 26.7Development Ltd. Villages

6 Shyamaraju &Ltd. Kundalahalli Village, IT/ITES 21.8Company (I) Pvt. Krishnarajapuram

7 Cessna Garden Ltd Kadubeesanahalli Village, IT/ITES 19.3 Developers Pvt. Varthur Hobli,

District Bangalore

8 Manyata Promoters Rachenhalli & IT/ITES 22.3 Nagavara Village,Bangalore District

9 HCL Technologies Jingani Industrial Area, IT/ITES 10.9 Attibele Taluk,

Bangalore District

10 M/s Information IT/ITES 10.9Bangalore Technology park

11 Primal Projects IT/ITES 10.4Bangalore Pvt. Ltd.

12 Biocon Ltd. Anekal Taluk Bio-technology 35.6

13 Karnataka Biotechnology &

Electronic City, Bio-technology 37.5InformationPhase III Bangalore

TechnologyServices (KBITS)

924.13Total

SEZs notified as on Dec 24, 2007

Source: Ministry of Commerce & Industry, Dept. of Commerce

6

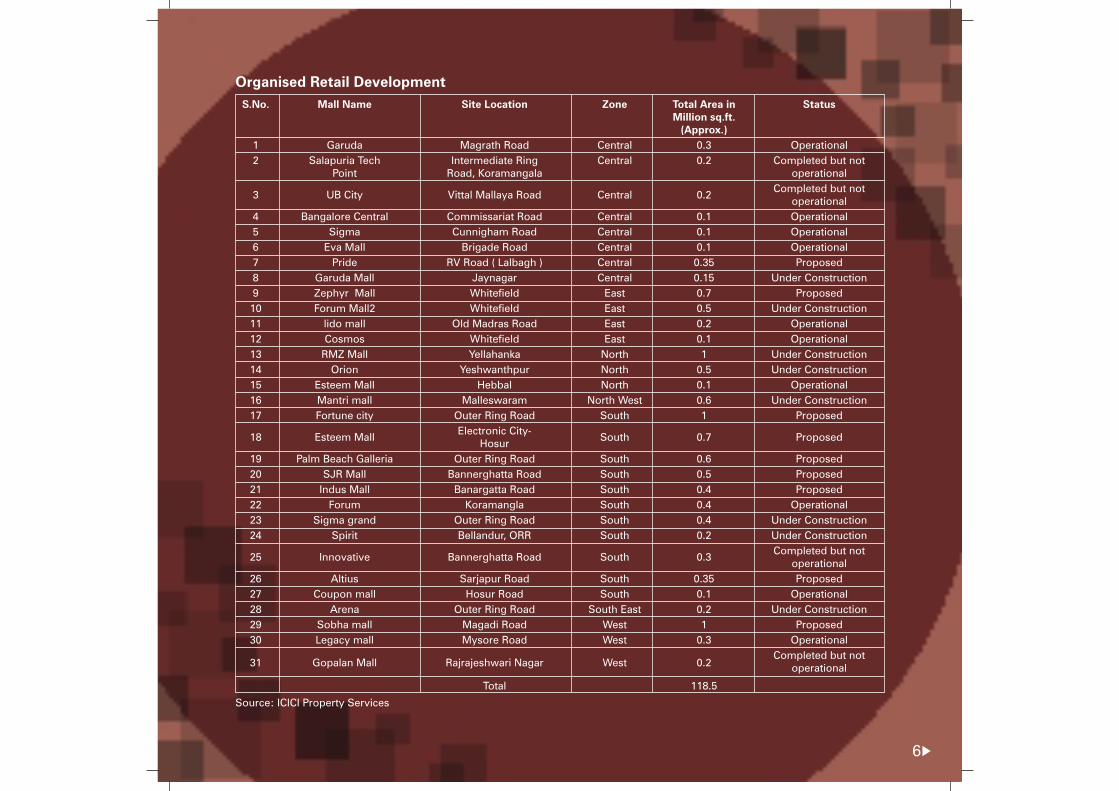

S.No. Mall Name Site Location Zone Total Area in StatusMillion sq.ft.

(Approx.)

1 Garuda Magrath Road Central 0.3 Operational

2 Salapuria Tech Intermediate Ring Central 0.2 Completed but notPoint Road, Koramangala operational

Completed but not3 UB City Vittal Mallaya Road Central 0.2

operational

4 Bangalore Central Commissariat Road Central 0.1 Operational

5 Sigma Cunnigham Road Central 0.1 Operational

6 Eva Mall Brigade Road Central 0.1 Operational

7 Pride RV Road ( Lalbagh ) Central 0.35 Proposed

8 Garuda Mall Jaynagar Central 0.15 Under Construction

9 Zephyr Mall Whitefield East 0.7 Proposed

10 Forum Mall2 Whitefield East 0.5 Under Construction

11 lido mall Old Madras Road East 0.2 Operational

12 Cosmos Whitefield East 0.1 Operational

13 RMZ Mall Yellahanka North 1 Under Construction

14 Orion Yeshwanthpur North 0.5 Under Construction

15 Esteem Mall Hebbal North 0.1 Operational

16 Mantri mall Malleswaram North West 0.6 Under Construction

17 Fortune city Outer Ring Road South 1 Proposed

Electronic City-18 Esteem Mall South 0.7 Proposed

Hosur

19 Palm Beach Galleria Outer Ring Road South 0.6 Proposed

20 SJR Mall Bannerghatta Road South 0.5 Proposed

21 Indus Mall Banargatta Road South 0.4 Proposed

22 Forum Koramangla South 0.4 Operational

23 Sigma grand Outer Ring Road South 0.4 Under Construction

24 Spirit Bellandur, ORR South 0.2 Under Construction

Completed but not25 Innovative Bannerghatta Road South 0.3

operational

26 Altius Sarjapur Road South 0.35 Proposed

27 Coupon mall Hosur Road South 0.1 Operational

28 Arena Outer Ring Road South East 0.2 Under Construction

29 Sobha mall Magadi Road West 1 Proposed

30 Legacy mall Mysore Road West 0.3 Operational

Completed but not31 Gopalan Mall Rajrajeshwari Nagar West 0.2 operational

Total 118.5

Organised Retail Development

Source: ICICI Property Services

North Bangalore

Major Locations

Sahakar Nagar, HRBR Layout, Ram Murthy Nagar, HBR Layout, Sanjay Nagar & RMV Extn., Bellary Road and Yellahanka ,Banaswadi,OMBR Layout, Hebbal , Yeshwanthpur

North Bangalore has now become one of the hottest investment destinations in the city.

This zone can expect a very good appreciation in the near future

RMV (Raj Mahal Villas) Layout , Sanjay Nagar and Sadashiv Nagar are the premium areas of north

Bangalore

Yellahanka is also an upcoming area in this zone

Ram Murthy Nagar, Kalyan Nagar, provide affordable housing in this part of the city

Growth Stimulators?This part of Bangalore was untouched till now, but the proposed international airport has

propelled the real estate prices here.

?The Eight-laned Bellary Road has improved the connectivity to the city

?Availability of large land parcels has led to development of theme based luxurious villa

developments as well as huge integrated township projects.

?Bellary road the major corridor connecting the city to the international airport enjoys premium

projects and gated communities with villas.

?Commercial developments like Manyata Tech Park, and Nagwara Techpark (in pipeline) have

generated large employment opportunities in this part of Bangalore.

?Commercial development of approximately 7 million sq.ft. will enter the market by Dec. 2009. This

translates into close to 63000 new jobs getting created by Dec 2009. (Assuming 10% vacancy

levels)

?

?

?

?

?

7

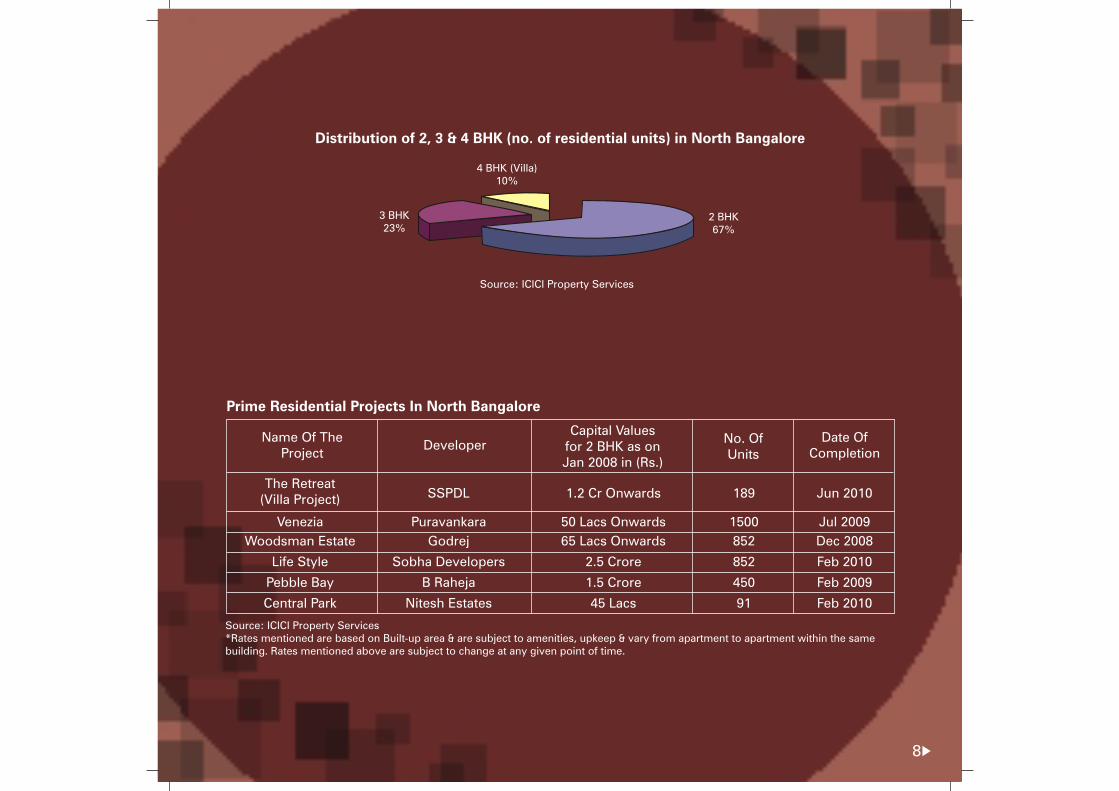

Average Apartment Size of 2 BHK in sq.ft 1200

Average Apartment Size of 3 BHK in sq.ft 1650

Average Apartment Size of 4 BHK in sq.ft 2500-3000

Total Supply (in mn. sq.ft.) by Dec. 2009 17.8

Total Supply (in no. of units) by Dec. 2009 10000

Source: ICICI Property ServicesNote: The areas mentioned are super built-up areas

Residential Market in North Bangalore

8

Distribution of 2, 3 & 4 BHK (no. of residential units) in North Bangalore

4 BHK (Villa)10%

3 BHK23%

2 BHK67%

Source: ICICI Property Services

SSPDL 1.2 Cr Onwards 189 Jun 2010

Venezia Puravankara 50 Lacs Onwards 1500 Jul 2009

Woodsman Estate Godrej 65 Lacs Onwards 852 Dec 2008

Life Style Sobha Developers 2.5 Crore 852 Feb 2010

Pebble Bay B Raheja 1.5 Crore 450 Feb 2009

Central Park Nitesh Estates 45 Lacs 91 Feb 2010

Source: ICICI Property Services*Rates mentioned are based on Built-up area & are subject to amenities, upkeep & vary from apartment to apartment within the same building. Rates mentioned above are subject to change at any given point of time.

Name Of TheProject

DeveloperCapital Values

for 2 BHK as on Jan 2008 in (Rs.)

No. OfUnits

Date OfCompletion

The Retreat(Villa Project)

Prime Residential Projects In North Bangalore

9

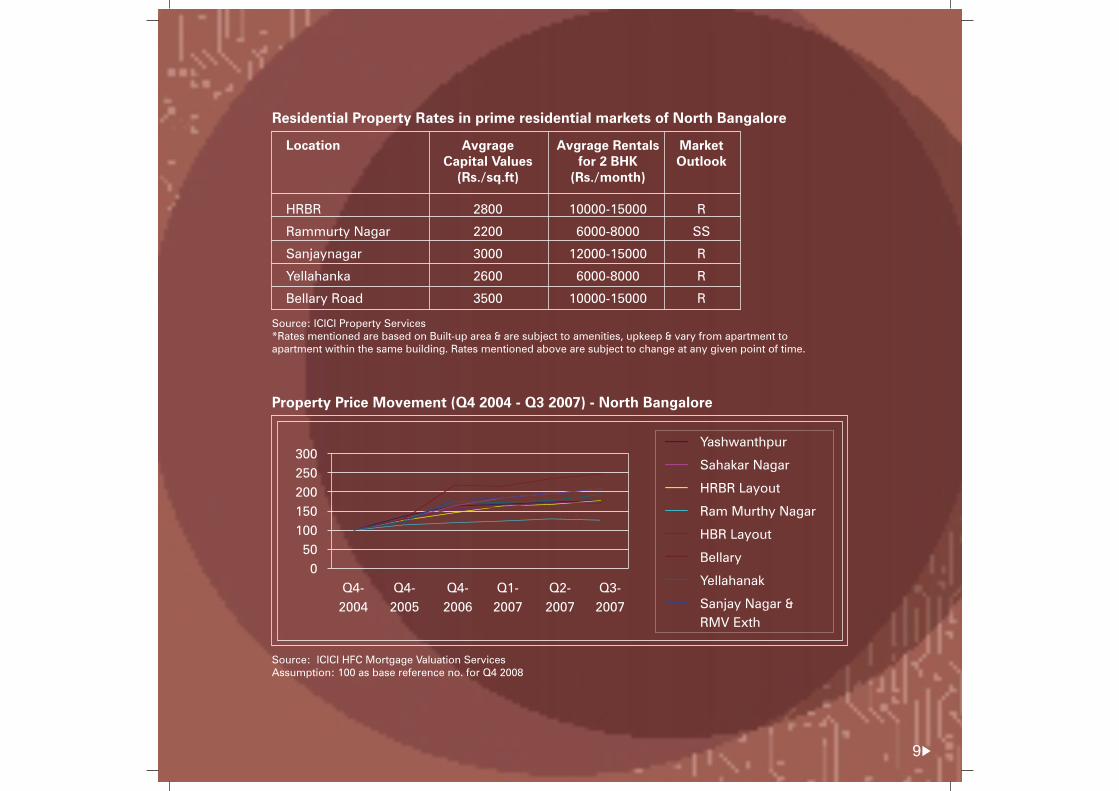

Location Avgrage Avgrage Rentals MarketCapital Values for 2 BHK Outlook

(Rs./sq.ft) (Rs./month)

HRBR 2800 10000-15000 R

Rammurty Nagar 2200 6000-8000 SS

Sanjaynagar 3000 12000-15000 R

Yellahanka 2600 6000-8000 R

Bellary Road 3500 10000-15000 R

Source: ICICI Property Services*Rates mentioned are based on Built-up area & are subject to amenities, upkeep & vary from apartment to apartment within the same building. Rates mentioned above are subject to change at any given point of time.

Residential Property Rates in prime residential markets of North Bangalore

Property Price Movement (Q4 2004 - Q3 2007) - North Bangalore

Source: ICICI HFC Mortgage Valuation ServicesAssumption: 100 as base reference no. for Q4 2008

Yashwanthpur

Sahakar Nagar

HRBR Layout

Ram Murthy Nagar

HBR Layout

Bellary

Yellahanak

Sanjay Nagar &

RMV Exth

300

250

200

150

100

50

0

Q4- Q4- Q4- Q1- Q2- Q3-

2004 2005 2006 2007 2007 2007

South Bangalore

Major Locations:

J P Nagar ,Jaya Nagar & Electronic City, Sarjapur Road, Outer Ring Road, Hosur Road, Kanakpura Road, Bannerghatta Road

?Huge residential supply in this part of Bangalore far exceeds the demand for it, as of today leading to a correction in the prices

?Bannerghatta Road has seen a spurt of development in the apartments. This is mainly in the

affordable housing sector in the range of Rs.2500-3500 pe sq. ft.

?However, South Bangalore can be termed as the second best investment destination.

?Kanakpura Road has seen good residential development in recent times.

?Sarjapur Road which lies between Outer Ring Road and Hosur Road, is another growth corridor in

Bangalore.

?Apart from its proximity to Outer Ring Road it is home to a huge number of IT companies which is

driving the market here.

?Sarjapur Road has seen tremendous residential development. Hosur Road is a mix of residential as

well as commercial real estate sector

Growth Stimulators

?NICE (Nandi Infrastructure Corridor Enterprise) will connect Electronic City(South Bangalore) to Mysore.

?21 kms expressway will connect Outer Ring Road to the new airport. This will reduce the traveling

time to the airport to 15-20 minutes

?An elevated road is also planned connecting Electronic City to Silk Board Junction.

?South Bangalore is inhabited mostly by the IT professionals. It is home to IT giants like Accenture,

Intel, Wipro, Infosys, TCS, Satyam.

?Kanakpura Road connects to the NICE corridor thus giving a convenient access to electronic city. Although it is far from the city, its connectivity to the IT corridor (Electronic City) acts as the growth driver

?Mantri has planned an 1.8 million sq.ft. mall on Sarjapur Road

?The residential real estate rates are very high in this part of the city.

?Commercial development of around 2 million sq.ft. is estimated to enter the market by Dec 2009.

This translates into 1800 new jobs getting created in the next 2 years. (Assuming 10% vacancy levels)

10

11

Source: ICICI Property Services

4 BHK11%

3 BHK22%

2 BHK67%

Average Apartment Size of 2 BHK in sq.ft 1200

Average Apartment Size of 3 BHK in sq.ft 1650

Average Apartment Size of 4 BHK in sq.ft 3000

Total Supply (in mn. sq.ft.) by Dec. 2009 20.25

Total Supply (in no. of units) by Dec. 2009 13500

Source: ICICI Property ServicesNote: The areas mentioned are super built-up areas

Distribution of 2, 3 & 4 BHK (no. of residential units) in South Bangalore

Residential Market In South Bangalore

Name of the Developer Capital Values No. of Date ofProject for 2 BHK as on Units Completion

Jan 2008 in (Rs.)

El Dorado Under Alliance 1 Cr Onwards Jun 2010

(Villa Project) Planning

Espana Mantri 1.3 Cr Onwards 650 Dec 2009

Tranquil Mantri 55 Lacs Onwards 800 Dec 2009

Horizon Elita 55 Lacs Onwards 1200 Jan 2010

Symphony Shriram 55 Lacs Onwards 400 Jan 2010

Nottinghill Prestige 55 Lacs Onwards 281 Jan 2010

Outhridge Prestige 1 Crore Onwards 264 Jan 2010

Palm Springs Brigade 1 Crore Onwards 22 Mar 2008

Source: ICICI Property Services*Rates mentioned are based on Built-up area & are subject to amenities, upkeep & vary from apartment to apartment within the same building. Rates mentioned above are subject to change at any given point of time.

Prime Residential Projects In South Bangalore

12

Location Average Capital Average Rentals for MarketValues (Rs./sq.ft) (Rs./ month) Outlook

Electronic City 2500 10000-15000 S

Sarjapur Road 2800 12000-15000 R

J P Nagar 3100 12000-15000 S

Kanakpura Road 2900 8000-10000 S

Bannargatta Road 3000 10000-12000 S

Source: ICICI Property Services*Rates mentioned are based on Built-up area & are subject to amenities, upkeep & vary from apartment to apartment within the same building. Rates mentioned above are subject to change at any given point of time.

2 BHK

Q4- Q4- Q4- Q1- Q2- Q3-

2004 2005 2006 2007 2007 2007

Property Price Movement (Q4 2004 - Q3 2007) - South Bangalore

Source: ICICI HFC Mortgage Valuation ServicesAssumption: 100 as base reference no. for Q4 2008

200180160140120100806040200

Kothnur

J P Nagar 6th & 7thPhase

Sarjapur Road

Hosur Road

Bannerghatta Road

Kanakpura Rd

Gottegere

Vijaya Bank Colony

Residential Property Rates In Prime Residential Markets Of South Bangalore

13

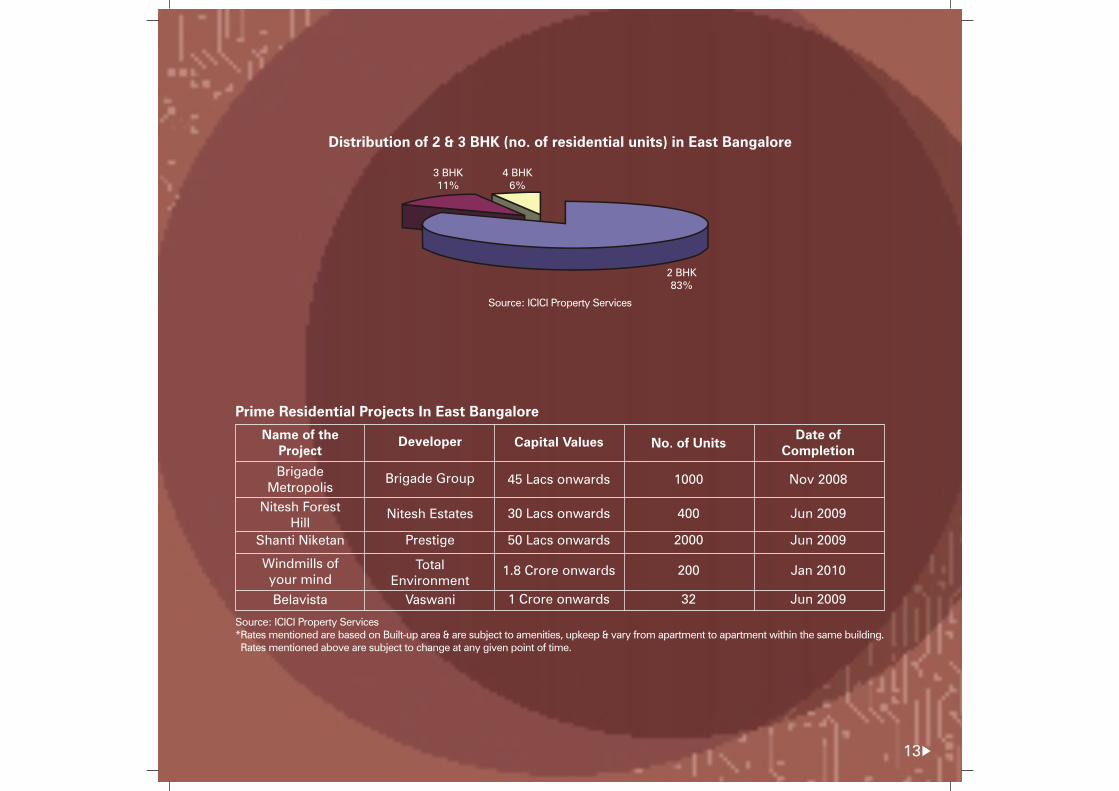

Prime Residential Projects In East Bangalore

Name of the Project

Developer Capital Values No. of UnitsDate of

Completion

Brigade Metropolis

Brigade Group 45 Lacs onwards 1000 Nov 2008

Nitesh Forest Hill

Nitesh Estates 30 Lacs onwards 400 Jun 2009

Shanti Niketan Prestige 50 Lacs onwards 2000 Jun 2009

Windmills of your mind

Total Environment

1.8 onwardsCrore 200 Jan 2010

Belavista Vaswani 1 onwardsCrore 32 Jun 2009

Source: ICICI Property Services*Rates mentioned are based on Built-up area & are subject to amenities, upkeep & vary from apartment to apartment within the same building. Rates mentioned above are subject to change at any given point of time.

Distribution of 2 & 3 BHK (no. of residential units) in East Bangalore

2 BHK83%

3 BHK11%

4 BHK6%

Source: ICICI Property Services

East Bangalore

Major Locations:

Whitefield, Brookefields, Kaggadasapura, Marathahalli, K R Puram, HSR Layout, Old Madras Road, C V Raman Nagar

• This region is witnessing a varied mix of developments ranging from high-end villas to row houses to condominiums.

• In the vicinity of the IT corridor, a large number of residential projects are being developed at Brookefields, Hoodi and Whitefield.

• In Whitefield the residential prices had dropped because of the oversupply but have now started picking up because of the entry of prominent builders in the city

• The infrastructure in this part of the city was not so great but is improving now• Brookefields lies before Whitefield and the residential rates are slightly higher than Whitefield because of

the proximity to the Outer Ring Road• Kaggadaspura has seen rampant construction on the residential front • The infrastructure here is not very well developed but because of its strategic location (proximity to Airport

Road, Whitefield, Outer Ring Road and Old Madras Road) it has witnessed a huge residential development• Kaggadaspura, C V Raman Nagar and Marathahalli offer affordabdle housing in the range of Rs.1700-2800

per sq.ft.

Growth Stimulators

• The connectivity to the present domestic & international airport is a huge contributor to the growth of this area.

• There is a high concentration of residential projects along this sector due to its proximity to the IT corridor.

• This area is home to ITPL (Information Technology Park Ltd.) which hosts renowned IT companies like Dell, Accenture, SAP Labs.

• The IT sector employees and NRIS drive the demand for residential projects which are coming up in this zone.

• Huge commercial development is estimated is this part of the city (approximately 19 million sq.ft.), which will translate into more than 1 lac new jobs getting created in this zone. (Assuming 10% vacancy levels)

Average Apartment Size of 2 BHK in sq.ft.

Average Apartment Size of 3 BHK in sq.ft.

Total Supply (in mn. sq.ft.) by Dec. 2009

Total Supply (in no. of units) by Dec. 2009

1200

1800

12.55

9000

Source: ICICI Property ServicesNote: The areas mentioned are super built-up areas

Residential Market In East Bangalore

14

15

Property Price Movement (Q4-2004 - Q3 2007) East Bangalore

0

20

40

60

80

100

120

140

160

180

200

Q4-2004 Q4-2005 Q4-2006 Q1-2007 Q2-2007 Q3-2007

Whitefield

Brookefields

HSR Layout

Kaggadasapura

Marathahalli

K R Puram

Source: ICICI HFC Mortgage Valuation ServicesAssumption: 100 as base reference no. for Q4 2008

White Filed 2800 10000-15000 SS

K R Puram 2800 7000-10000 SS

Kagadaspura 1800 8000-10000 SW

Source: ICICI Property Services*Rates mentioned are based on Built-up area & are subject to amenities, upkeep & vary from apartment to apartment within the same building. Rates mentioned above are subject to change at any given point of time.

Residential Property Rates In Prime Residential Markets of East Bangalore

Location

Average Capital Values

(Rs./sq.ft)

Average Rentals for2 BHK (Rs./month)

Market Outlook

Marthahalli 2800 8000-12000 R

Distribution of 2 & 3 BHK (no. of residential units) in West Bangalore

2 BHK66%

3 BHK24%

4 BHK10%

Source: ICICI Property Services

Source: ICICI Property Services*Rates mentioned are based on Built-up area & are subject to amenities, upkeep & vary from apartment to apartment within the same building. Rates mentioned above are subject to change at any given point of time.

Prime Residential Projects in West Bangalore

Name of the Project

Developer No. of UnitsDate of

Completion

The Garden ETA Star 55 Lacs onwards 900 Oct 2008

Temple Bells Rennaissance 60 Lacs onwards 350 Dec 2008

West BangaloreMajor Locations:Kengeri, Rajarajeshwari Nagar, Nagarbhavi, Chandra Layout, Uttarhalli, Dr. RajKumar Road, Vijay Nagar, Rajaji Nagar• West Bangalore has not witnessed a lot of IT development until now, however with the connectivity to Mysore (tierII city) this area is expected to see upward trend in demand.• Magadi Road has huge tracts land (old defunct mills) which is expected to give a filip to the area. There is

also a huge supply of retail expected to hit the market.• The metro connectivity and the recently announced 60,000 crore Bidadi township will act as a major driver

for this part of town.

16

Residential Market in West Bangalore

Source: ICICI Property ServicesNote: The areas mentioned are super built-up areas

Average Apartment Size of 2 BHK in sq.ft. 1200

1650Average Apartment Size of 3 BHK in sq.ft.

Total Supply (in mn. sq.ft.) by Dec. 2009 1.49

Total Supply (in no. of units) by Dec. 2009 1050

Capital Valuesfor 2 BHK as on Jan 2008 in (Rs.)

Property Price Movement (Q4-2004 - Q3 2007) West Bangalore

0

20

40

60

80

100

120

140

160

180

Q4-2004 Q4-2005 Q4-2006 Q1-2007 Q2-2007 Q3-2007

Kengeri

R R Nagar

Uttarhalli

Source: Assumption: 100 as base reference no. for Q4 2008

ICICI HFC Mortgage Valuation Services

Residential Property rates in prime residential markets of West Bangalore

Location Market Outlook

Kengeri 1000 2000-5000 SS

SSR R Nagar 2800 6000-10000

SSUttarahali 2000-2500 6000-10000

SSVijay Nagar 2800-3500 10000-15000

SSChandralayout/

Nagarbhavi2000-2500 6000-10000

Source: ICICI Property Services*Rates mentioned are based on Built-up area & are subject to amenities, upkeep & vary from apartment to apartment within the same building. Rates mentioned above are subject to change at any given point of time.

Avgrage Capital Values

(Rs./sq.ft)

17

Average Rentals for2 BHK (Rs./month)

Residential Market in Central Bangalore

Average Apartment Size of 2 BHK in sq.ft. 1300

1800Average Apartment Size of 3 BHK in sq.ft.

Average Apartment Size of 4 BHK in sq.ft. 3000

Total Supply (in mn. sq.ft.) by Dec. 2009 1.4

950Total Supply (in no. of units) by Dec. 2009

Source: ICICI Property ServicesNote: The areas mentioned are super built-up areas

Central Bangalore

Major Locations:M.G.Road (CBD), Malleshwaram, Basavangudi, Padmanabha Nagar, Koramangala, Vasanth Nagar & Indira Nagar,

Coxtown, Frazer Town, Benson Town

• Upmarket location, characterised by independent houses

• Dense development with little scope for expansion

• Demand for residential units far exceeds the supply

• The residential real estate rates are very high in this zone and the people are ready to offer the premium

• Land prices have also increased because of the scarcity

• Kormangala has a very good mix of residential as well as commercial supply.

• It is close to the CBD (Central Business District)

Growth Stimulators

• With the recent CDP (Comprehensive Development Plan) effecting higher FSI (Floor Space Index) in these areas, rentals in areas like Central Bangalore have maintained their dominance by fetching highest rental & capital values across the city and the capital values are expected to grow at a good rate.

• With little or no supply of land, the current CDP's proposal to 'Go Vertical' by increasing FSI will augment the stock in existing areas in the mid to short term.

• This area also has some of the best software and BPO companies like, Accenture, Microland, Sonata Software, IBM, Infosys.

18

Prime Residential Projects in Central Bangalore

Name of the Project

Developer No. of UnitsDate of

Completion

Brigade GatewayBrigade

Enterprises65 Lacs onwards 1200 Jan 2009

Canary Warlf Nitesh Estates 2.5 Crore 45 Apr 2009

Fairmount Motwani 1.4 Crore 50 Jan 2009

Source: ICICI Property Services*Rates mentioned are based on Built-up area & are subject to amenities, upkeep & vary from apartment to apartmentwithin the same building. Rates mentioned above are subject to change at any given point of time.

Distribution of 2, 3 & 4 BHK (no. of residential units) in Central Bangalore

Source: ICICI Property Services

2 BHK

59%

3 BHK29%

4 BHK

12%

19

Capital Valuesfor 2 BHK as on Jan 2008 in (Rs.)

20

Property Price Movement (Q4-2004 - Q3 2007) Central Bangalore

Source:Assumption: 100 as base reference no. for Q4 2008

ICICI HFC Mortgage Valuation Services

0

50

100

150

200

250

300

350

400

Q4-

2004

Q4-

2005

Q4-

2006

Q1-

2007

Q2-

2007

Q3-

2007

Malleshwaram

Basavagundi

Padmanabha Nagar

J P Nagar

Koramangala

Vasanth Nagar

BTM Layout

Jai Nagar

Residential Property Rates in prime residential markets of Central Bangalore

Location

Average Capital Values

(Rs./sq.ft)

Market Outlook

Malleshwaram 4500 15000-20000

15000-20000

R

R

R

Koramangala 5000

Richmond Road 11000 30000-45000

Source: ICICI Property Services*Rates mentioned are based on Built-up area & are subject to amenities, upkeep & vary from apartment to apartment within the same building. Rates mentioned above are subject to change at any given point of time.

Average Rentals for2 BHK (Rs./month)

Location Attractiveness Index

Infrastructure (connectivity,

roads, proximity

to markets, schools)

Residential Cost

Proximity to/ Prence of Organised

Retail (malls/popular

highstreets)

Proximity to Commercial

Development (offices)

Future Infrastructure Development

Future Employment Generation

Good Good Good Good GoodHighKormangala

Sarjapur Outer Ring Road

Good Good Good Good GoodHighIndiranagar

Malleshwaram Good Good Average Good AverageHigh

Average Good Good Good GoodMediumWhitefield

Electronic City Average Bad Good Good GoodLow

Bellary Road Good Average Average Good GoodHigh

Recommended locations in Bangalore

Kormangala- Sarjapur Outer Ring Road IndiranagarWhitefieldBellary RoadMalleshwaramOuter Ring Road near Hebbal

21

Growth Corridor

Whitefield

- IT hub

- 6 malls in pipeline

- Metro will touch Whitefield Phase II

- ITPL- IT campus employing close to 15000 employees

- Huge residential development: Metropolis-1000 units & Shantiniketan-2000 units

- Villa projects by developers like Prestige, Vaswani

- Very good accessibility to the entire IT corridor of Bangalore

- New international airport- to the north-west of Whitefield

Sarjapur Road

•

• Huge IT development is proposed

• Retail development is in pipeline

• Close to 4 mega malls coming up in the vicinity

• CISCO campus in pipeline on the Outer Ring Road

• Over 50 residential projects (budget class to super luxury) with apartments & villas ranging from 45 lacs to 4 crores

• Beginning of Sarjapur Road is Outer Ring Road which will develop into a sub CBD in future and other end

touches the Periphery Ring Road & the expressway to the airport

Huge commercial development planned

22

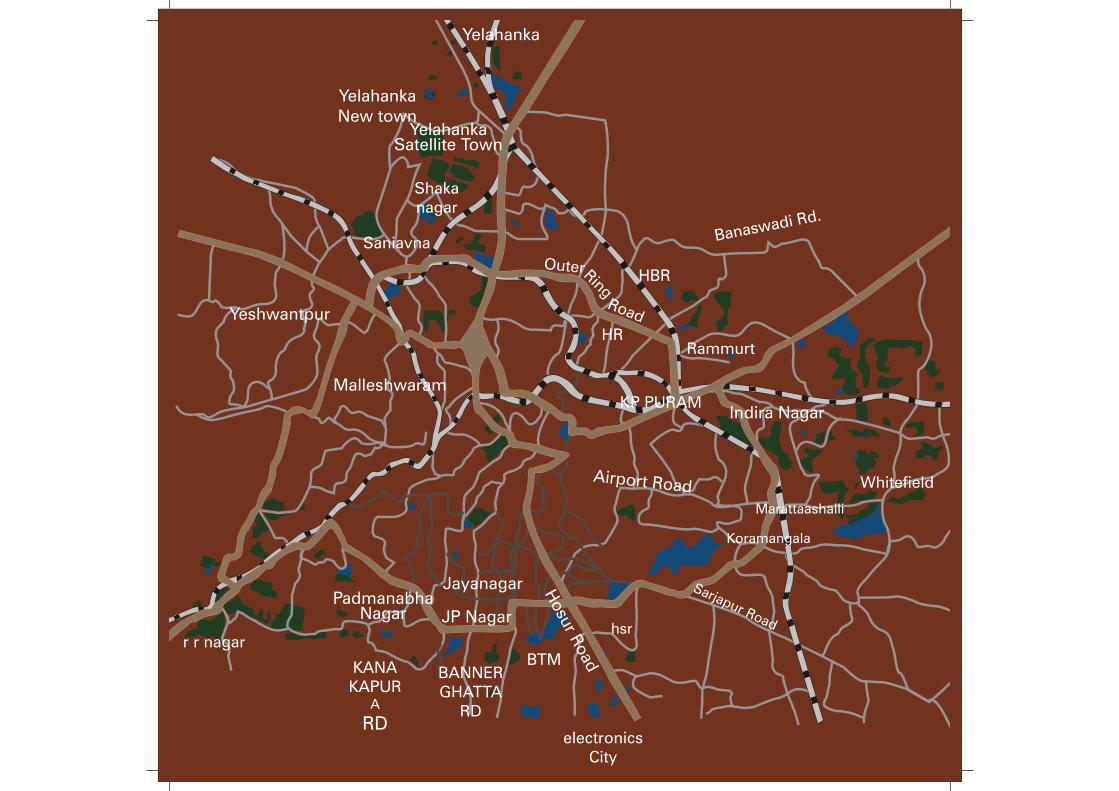

Sa j o d

r apur Ra

Koramangala

Marattaashalli

WhitefieldAirpor Rt oad

Indira Nagar

O t u erRng i

oR ad

PadmanabhaNagar

Jayanagar

JP Nagar

Hosu

rd

Roa

hsr

Malleshwaram

Yeshwantpur

Yelahanka

YelahankaSatellite Town

YelahankaNew town

KANAKAPUR

A

RD

BANNERGHATTA

RD

BTMr r nagar

Shakanagar

Saniavna

HBR

HRRammurt

KP PURAM

sBana wadi Rd.

electronicsCity

For further enquiries, please mail us at :[email protected]

“ICICI Securities Limited is proposing, subject to receipt of requisite approvals, market conditions and other considerations, a public issue of its equity shares and to file a Draft Red Herring Prospectus with SEBI.”

This report has been prepared by ICICI Property Services. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form by any means, electronic, mechanical, photocopying, recording or otherwise, without prior permission of the publisher ICICI Property Services The facts of these profiles are believed to be correct at the time of publication but cannot be guaranteed. Please note that the findings, conclusions and recommendations are based on information gathered in good faith from both primary and secondary sources, whose accuracy we are not always in a position to guarantee. ICICI Property Services cannot accept any liability whatsoever for actions taken based on any information that may subsequently prove to be incorrect.

(A division of ICICI Home Finance Company Limited)