BotswanaBotswanaDiamondsDiamonds

Letsema MbayiLetsema Mbayi

MMCP MMCP

March 2010March 2010

HypothesisHypothesis

Diamond Beneficiation will enable Diamond Beneficiation will enable Botswana to make the most of its Botswana to make the most of its

remaining diamond resource if it results in remaining diamond resource if it results in downstream linkages that enhance and downstream linkages that enhance and

broaden the local economy’s benefit from broaden the local economy’s benefit from diamond miningdiamond mining

Research AimsResearch Aims

a.a. the determinants to developing downstream the determinants to developing downstream activities with output from the diamond mining activities with output from the diamond mining industry in Botswana;industry in Botswana;

b.b. the key challenges to the developing the key challenges to the developing downstream activities in Botswana’s diamond downstream activities in Botswana’s diamond industry; and industry; and

c.c. the policies and strategies that can be the policies and strategies that can be formulated to address these key challenges formulated to address these key challenges and enhance downstream linkages. and enhance downstream linkages.

Specific QuestionsSpecific Questions1.1. What was the role of policy and ownership in creating and supporting downstream What was the role of policy and ownership in creating and supporting downstream

linkages?linkages?2.2. To what extent is Botswana managing to create a diamond cutting and polishing To what extent is Botswana managing to create a diamond cutting and polishing

industry and its related activities?industry and its related activities?3.3. What problems are being faced in Botswana’s cutting and polishing industry and What problems are being faced in Botswana’s cutting and polishing industry and

its related activities?its related activities?4.4. What role is the national system of innovation (NSI) playing in enhancing What role is the national system of innovation (NSI) playing in enhancing

downstream linkages?downstream linkages?5.5. How are local skills being created and can these skills being transferred within the How are local skills being created and can these skills being transferred within the

downstream linkages? downstream linkages? 6.6. How does the global political economy of the diamond supply chain affect How does the global political economy of the diamond supply chain affect

Botswana cutting and polishing industry and its linkages with local economy? Botswana cutting and polishing industry and its linkages with local economy? 7.7. To what extent will the current financial crisis affect downstream linkages in To what extent will the current financial crisis affect downstream linkages in

Botswana’s diamond industry? Botswana’s diamond industry? 8.8. How will the depletion of Botswana’s current diamond reserves affect downstream How will the depletion of Botswana’s current diamond reserves affect downstream

linkages? What are the possibilities for new diamond deposits that can increase linkages? What are the possibilities for new diamond deposits that can increase the time-path to depletion? the time-path to depletion?

9.9. What are the policy implications of the above findings? What are the policy implications of the above findings?

MethodologyMethodology Desktop researchDesktop research Department of Minerals and the Diamond Hub Department of Minerals and the Diamond Hub

first point of entry into the industry.first point of entry into the industry. Goal to interview all the key players in the existing downstream Goal to interview all the key players in the existing downstream

value chain, value chain, the critical supplier (DTCB),the critical supplier (DTCB), the manufactures (Sightholders), the manufactures (Sightholders), the service providers (ancillary companies)the service providers (ancillary companies) the institutions both public and private. the institutions both public and private.

Challenges Challenges Interviews were semi-structured and took from 30mins to 2 hours. Interviews were semi-structured and took from 30mins to 2 hours. Interviews were conducted in English and SetswanaInterviews were conducted in English and Setswana The data collected was overwhelmingly qualitative. The data collected was overwhelmingly qualitative.

Fig 1.1: Diamond Pipeline

Exploration

Mining

Sorting and Valuing

Rough Trading

Cutting and Polishing

Polished Sales

Jewellery Manufacturing

Retail Sales

Upstream Linkages

Downstream Linkages

Aggregation End 2010

2006

1960s

1970s

1970s

2006

End 2010

SupplierSupplier

DeBeers DeBeers ExplorationExploration MiningMining Sorting and Valuing Sorting and Valuing Rough SalesRough Sales

Cutting and polishing industryCutting and polishing industry 11stst attempt in the 1980s attempt in the 1980s 22ndnd attempt 2006 attempt 2006

Diamond Trading Company Botswana (DTCB)Diamond Trading Company Botswana (DTCB) 15% of supply15% of supply

AggregationAggregation

Fig. 2.1: Current Aggregation Process

Fig. 2.2: Future Aggregation Process

Mixed Parcels Gaborone Mix

India & Others

South Africa

Namibia

Canada

Botswana

South Africa

Canada

Namibia

Open Market

Mixed Parcels London Mix

India & Others

South Africa

Namibia

Canada

Botswana

Botswana

South Africa

Canada

Namibia

Open Market

BuyersBuyersPopulation (16) Country of

Origin Respondents (7) Person Interviewed

Leo Schachter Diamond Manufacturing Botswana Teemane Manufacturing Botswana Eurostar Botswana SAFDICO Suashish Lazare Kaplan Botswana Steinmetz Rand Diamonds Botswana Pluckzenic Botswana Dalumi Yerushalmi Zebra Diamonds Sherenuj Motiganz H&A Piofine Tools

Israel Belgium Belgium Belgium RSA India Israel Israel RSA Belgium Israel Israel Belgium India Israel Thailand Botswana

Motiganz Diamonds Botswana Suashish Diamonds Botswana Leo Schatcher Botswana Steinmetz Diamonds Botswana Eurostar Botswana Lazare Kaplan Botswana Diamond Manufacturing Botswana

Production Manager Managing Director Production Manager Managing Director General Manager Managing Director Managing Director

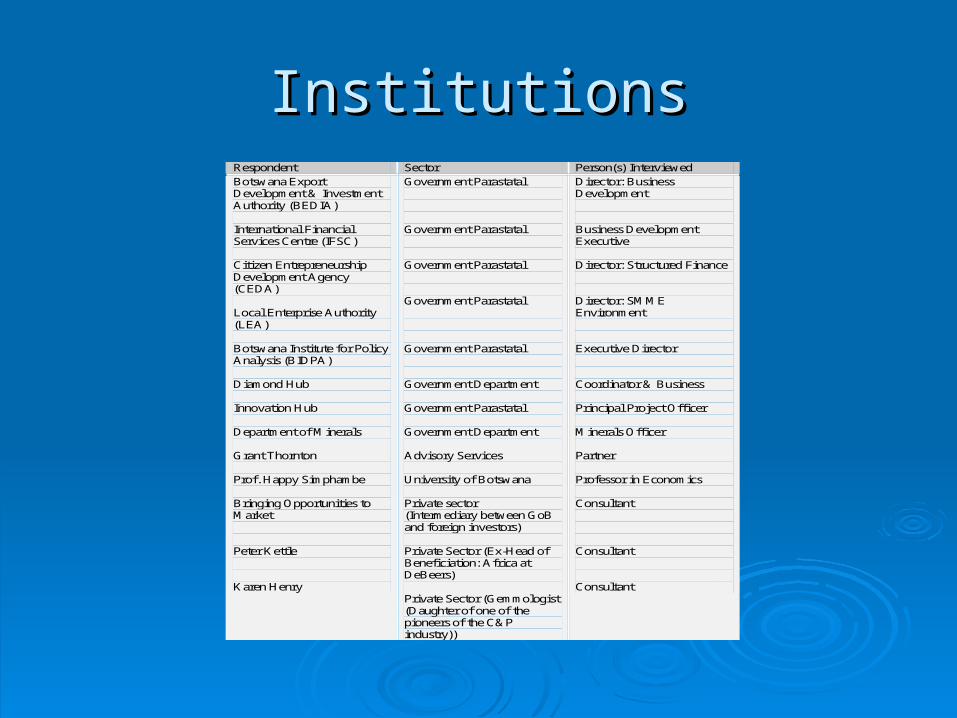

InstitutionsInstitutions Respondent Sector Person(s) Interviewed Botswana Export Development & Investment Authority (BEDIA) International Financial Services Centre (IFSC) Citizen Entrepreneurship Development Agency (CEDA) Local Enterprise Authority (LEA) Botswana Institute for Policy Analysis (BIDPA) Diamond Hub Innovation Hub Department of Minerals Grant Thornton Prof. Happy Simphambe Bringing Opportunities to Market Peter Kettle Karen Henry

Government Parastatal Government Parastatal Government Parastatal Government Parastatal Government Parastatal Government Department Government Parastatal Government Department Advisory Services University of Botswana Private sector (Intermediary between GoB and foreign investors) Private Sector (Ex-Head of Beneficiation: Africa at DeBeers) Private Sector (Gemmologist (Daughter of one of the pioneers of the C&P industry))

Director: Business Development Business Development Executive Director: Structured Finance Director: SMME Environment Executive Director Coordinator & Business Principal Project Officer Minerals Officer Partner Professor in Economics Consultant Consultant Consultant

Pre-identified constraintsPre-identified constraints

1.1. SkillsSkills

2.2. Assess to FinanceAssess to Finance

3.3. Assess to TechnologyAssess to Technology

4.4. Business environmentBusiness environment

Service ProvidersService Providers

Population (12) Activities Respondents (6) Gemmological Institute of America (GIA) Malca-Amit Botswana Brinks Botswana ABN ABRO Bank Botswana Stanbic Bank Standard Charted I Hennig & Co Rotheschild Diamond BONAS Marsh AON G4S

Gemmology Logistics Logistics Financing Financing Financing Brokers Brokers Brokers Insurers Insurers Security

Gemmological Institute of America (GIA) Malca-Amit Botswana ABN ABRO Bank Botswana I Hennig & Co Marsh AON

LinkagesLinkages Linkages Linkages withinwithin the Botswana’s downstream diamond industry have the Botswana’s downstream diamond industry have

recently been developed and are strengthening overtime. recently been developed and are strengthening overtime. Cutting and polishing industry is working to a large extent Cutting and polishing industry is working to a large extent Local cutting and polishing skills have grown from nearly non-existent Local cutting and polishing skills have grown from nearly non-existent

and are growing over time but will continue to be a constraint for years and are growing over time but will continue to be a constraint for years to cometo come

The Sightholders are well financed by their parent companies and The Sightholders are well financed by their parent companies and access to finance and technology are not major constraints. access to finance and technology are not major constraints.

Quantitative data is not readily available and magnitude of the industry Quantitative data is not readily available and magnitude of the industry is yet to be determined. is yet to be determined.

All specialised inputs imported from major diamond cutting and polishing All specialised inputs imported from major diamond cutting and polishing centres centres

None specialised inputs are imported from South Africa. None specialised inputs are imported from South Africa. All Botswana offers the buyers is the availability of rough diamond All Botswana offers the buyers is the availability of rough diamond

supply and unskilled labour. supply and unskilled labour.

LinkagesLinkages

All the factories interviewed: All the factories interviewed: imported their technology from the major diamond cutting and imported their technology from the major diamond cutting and

polishing centres such as Belgium, Israel and India. polishing centres such as Belgium, Israel and India. None saw access to technology as a problem None saw access to technology as a problem

• “ “..if you have the money you can import the technology you need” ..if you have the money you can import the technology you need” maintenance of the specialised equipment a constraintmaintenance of the specialised equipment a constraint

• lack of local technicianslack of local technicians• cost of bringing in foreigners too high cost of bringing in foreigners too high • visa process is a hassle. visa process is a hassle.

existing servicing contracts with technology suppliers. existing servicing contracts with technology suppliers. • State-funded technicianState-funded technician• Industry penetrationIndustry penetration

LinkagesLinkages The linkages between the downstream diamond industry and local The linkages between the downstream diamond industry and local

economy are not extensive. economy are not extensive. ‘‘enclave industry’ enclave industry’

capital is controlled by foreigners resulting in few linkages with the rest capital is controlled by foreigners resulting in few linkages with the rest of the economy. of the economy.

Local participation in knowledge intensive services is very low Local participation in knowledge intensive services is very low companies relocated/expanded from South Africa’s cutting and polishing companies relocated/expanded from South Africa’s cutting and polishing

industry industry set up front offices in Botswana to service their new clientsset up front offices in Botswana to service their new clients locals lack knowledge and understanding on the downstream activities locals lack knowledge and understanding on the downstream activities

• ill-equipped to take advantage of knowledge intensive opportunities in ill-equipped to take advantage of knowledge intensive opportunities in downstream industry. downstream industry.

• high barriers to entry in the industry make it difficult for locals to become high barriers to entry in the industry make it difficult for locals to become service providersservice providers

SupplierSupplier marketing contract between DeBeers and the GoB, marketing contract between DeBeers and the GoB,

the DTCB has the full distribution license to all of Debswana’s output. the DTCB has the full distribution license to all of Debswana’s output. the sole supplier of diamonds in Botswana.the sole supplier of diamonds in Botswana. 6 buyers of gem stones and one buyer of industrial stones.6 buyers of gem stones and one buyer of industrial stones.

market structure market structure supplier power supplier power supplier driven value chain where thesupplier driven value chain where the governance structure of the value chain is controlled by one suppliergovernance structure of the value chain is controlled by one supplier current marketing contract expires at the end of 2010 current marketing contract expires at the end of 2010

• renegotiated renegotiated • to change the current structure of the value chain. to change the current structure of the value chain. • independent marketing channel outside of the DeBeers distribution channelindependent marketing channel outside of the DeBeers distribution channel• new producers African Diamonds and DiamonEx will be able to market their diamonds outside of the new producers African Diamonds and DiamonEx will be able to market their diamonds outside of the

DTCB arrangement. DTCB arrangement. captive governance structure where captive governance structure where

DeBeers sets rules DeBeers sets rules • Price of rough diamondsPrice of rough diamonds• Quantity Quantity • Selling datesSelling dates• Number of manufacturesNumber of manufactures• Manufacturing companiesManufacturing companies

BuyersBuyers DMB Motiganz Steinmetz Eurostar Suashish Leo

Schachter LKI

Country of Origin

Belgium Israel Israel Belgium India Israel Israel

Ownership Family Business

Family Business

Family Business

Family Business

Family Business

Family Business

Family Business

Est. 1982 2007 2007 2004 2007 1990 2007 Pre-Crisis Employ.

206 293 (33) 170 550 90 (18) 360 n/a

Post-Crisis Employ.

103 (10) 226 (46) 125 (6) 318 (15) 60 (12) 201 (20) n/a

Ave. Salary P900 – P3000

P1000 P1500 n/a

Other Operations

Israel, India (jewellery)

China, India & Israel

South Africa, Namibia, Mauritius, Geneva, New York & Antwerp

China India Thailand, (South Africa)

Israel

Sizes of stones

Small ( 2.5 – 4) & big (4 to 8)

Cubes Small & big

Small Big All sizes, prefer 4 carats

5 to 14.5 carats

Export destination

Antwerp Israel Europe Belgium India Israel

Own or Rent Property

Own Rent Own Own Rent Own Own

Located in DH?

No No Yes No No No Yes

BuyersBuyers

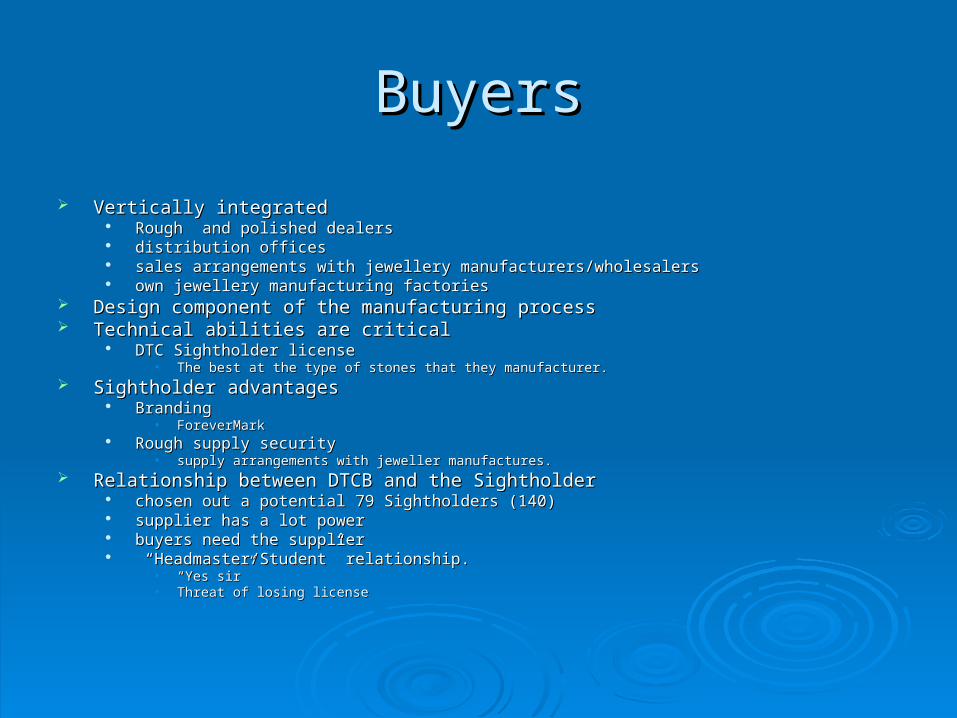

Vertically integrated Vertically integrated Rough and polished dealers Rough and polished dealers distribution offices distribution offices sales arrangements with jewellery manufacturers/wholesalers sales arrangements with jewellery manufacturers/wholesalers own jewellery manufacturing factoriesown jewellery manufacturing factories

Design component of the manufacturing process Design component of the manufacturing process Technical abilities are critical Technical abilities are critical

DTC Sightholder licenseDTC Sightholder license• The best at the type of stones that they manufacturer. The best at the type of stones that they manufacturer.

Sightholder advantagesSightholder advantages Branding Branding

• ForeverMark ForeverMark Rough supply security Rough supply security

• supply arrangements with jeweller manufactures.supply arrangements with jeweller manufactures. Relationship between DTCB and the SightholderRelationship between DTCB and the Sightholder

chosen out a potential 79 Sightholders (140)chosen out a potential 79 Sightholders (140) supplier has a lot powersupplier has a lot power buyers need the supplier buyers need the supplier “ “Headmaster/Student” relationship. Headmaster/Student” relationship.

• ““Yes sir” Yes sir” • Threat of losing licenseThreat of losing license

BuyersBuyers Diamond industry Diamond industry

secretive secretive trust is criticaltrust is critical

Production Information is not easy given out Production Information is not easy given out Compete globally Compete globally

Production figures valuable to the competitionProduction figures valuable to the competition Unable to determine each Sightholders production levels and capabilities. Unable to determine each Sightholders production levels and capabilities.

All the Sightholders agreed that the biggest constraint All the Sightholders agreed that the biggest constraint Hassle of doing business in Botswana. Hassle of doing business in Botswana. Time is crucial Time is crucial

• internet connectivity problems internet connectivity problems • or power cuts make a real impact on their timelines or turnaround timesor power cuts make a real impact on their timelines or turnaround times

Slow service delivery in general Slow service delivery in general Getting anything done is a real hassleGetting anything done is a real hassle

Reason for being in Botswana Reason for being in Botswana availability of supply availability of supply strategic decisions still made by the parent companiesstrategic decisions still made by the parent companies local operations focusing on production. local operations focusing on production.

Service ProvidersService Providers New ancillary services providers New ancillary services providers

Set up especially to meet needs of the new buyersSet up especially to meet needs of the new buyers Reputation is everything in the industry Reputation is everything in the industry

All the major service providers operate branches in all major All the major service providers operate branches in all major diamond cutting sector diamond cutting sector

Recognised by the Sightholder Recognised by the Sightholder Already work with Sightholders in other cutting and polishing Already work with Sightholders in other cutting and polishing

centres. centres. Barriers to entry very high. Barriers to entry very high. Head offices located Head offices located

• South Africa South Africa • Major diamond cutting and polishing centreMajor diamond cutting and polishing centre

Botswana Botswana • Front offices that focus Front offices that focus • Servicing local clientsServicing local clients

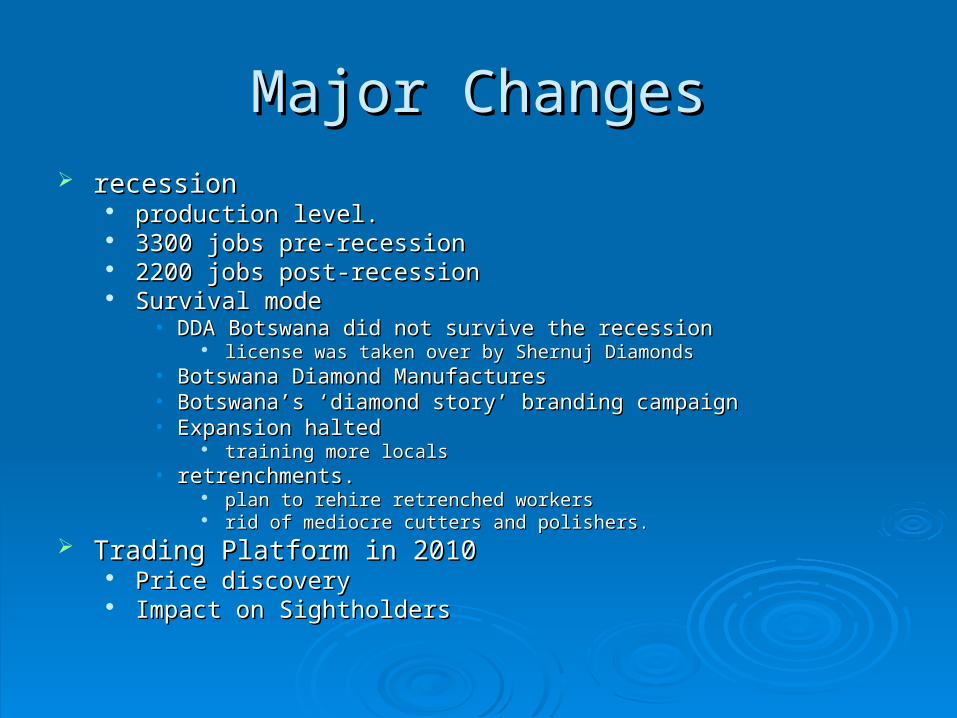

Major ChangesMajor Changes recession recession

production level. production level. 3300 jobs pre-recession3300 jobs pre-recession 2200 jobs post-recession2200 jobs post-recession Survival modeSurvival mode

• DDA Botswana did not survive the recessionDDA Botswana did not survive the recession license was taken over by Shernuj Diamondslicense was taken over by Shernuj Diamonds

• Botswana Diamond Manufactures Botswana Diamond Manufactures • Botswana’s ‘diamond story’ branding campaignBotswana’s ‘diamond story’ branding campaign• Expansion haltedExpansion halted

training more locals training more locals • retrenchments. retrenchments.

plan to rehire retrenched workers plan to rehire retrenched workers rid of mediocre cutters and polishers.rid of mediocre cutters and polishers.

Trading Platform in 2010 Trading Platform in 2010 Price discoveryPrice discovery Impact on SightholdersImpact on Sightholders

OwnershipOwnership

Key factor to determining the breath and Key factor to determining the breath and depth of linkages from the mining sectordepth of linkages from the mining sector

• SupplySupply• ManufacturingManufacturing

Ownership: SupplyOwnership: Supply

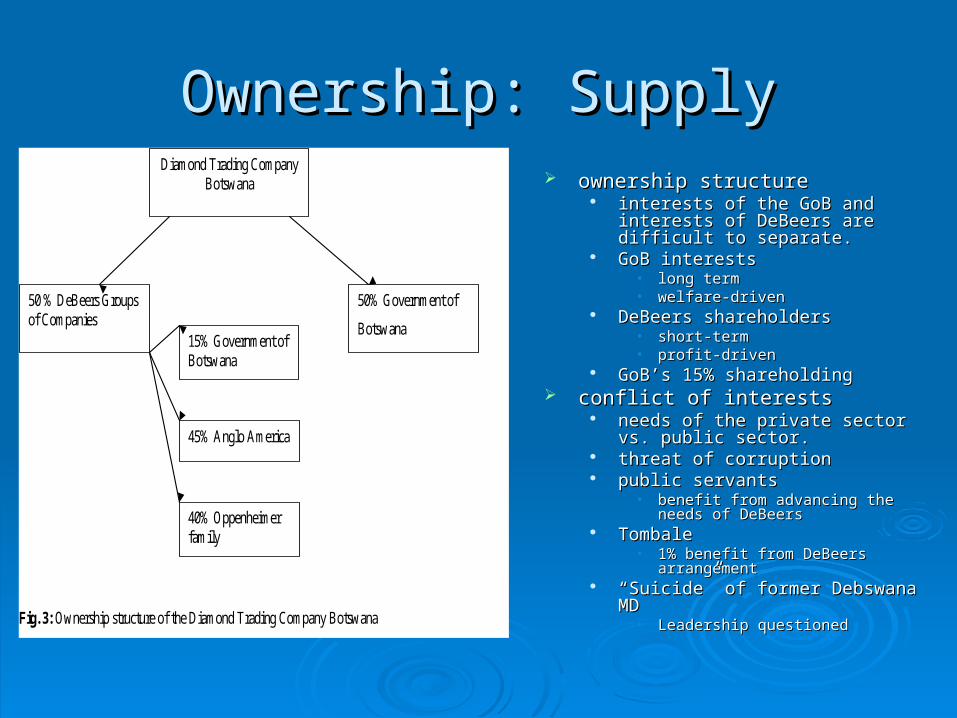

Fig. 3: Ownership structure of the Diamond Trading Company Botswana

Diamond Trading Company Botswana

50% Government of

Botswana

50 % DeBeers Groups of Companies

40% Oppenheimer family

45% Anglo America

15% Government of Botswana

ownership structure ownership structure interests of the GoB and interests of interests of the GoB and interests of

DeBeers are difficult to separate. DeBeers are difficult to separate. GoB interestsGoB interests

• long term long term • welfare-driven welfare-driven

DeBeers shareholders DeBeers shareholders • short-term short-term • profit-drivenprofit-driven

GoB’s 15% shareholding GoB’s 15% shareholding conflict of interests conflict of interests

needs of the private sector vs. public needs of the private sector vs. public sector. sector.

threat of corruption threat of corruption public servantspublic servants

• benefit from advancing the needs of benefit from advancing the needs of DeBeersDeBeers

TombaleTombale• 1% benefit from DeBeers arrangement1% benefit from DeBeers arrangement

““Suicide” of former Debswana MDSuicide” of former Debswana MD• Leadership questionedLeadership questioned

Ownership: ManufacturingOwnership: Manufacturing Diamantaire families Diamantaire families

foreign capitalforeign capital holding companies/parent listed in major stock holding companies/parent listed in major stock

exchangesexchanges maximise profits maximise profits take advantage of the supply take advantage of the supply

• investment in Botswana was long terminvestment in Botswana was long term• recover their initial investments majority ofrecover their initial investments majority of• Own propertyOwn property

limiting breadth and depth of linkages in the limiting breadth and depth of linkages in the industry in knowledge intensive servicesindustry in knowledge intensive services

• limiting this knowledge transfer by limiting this knowledge transfer by • focusing locals on local production only focusing locals on local production only • not the global aspects of the downstream industrynot the global aspects of the downstream industry

local production managers local production managers very limited knowledge very limited knowledge

• GVC chain GVC chain • operations of their parent company. operations of their parent company.

strategic decisions strategic decisions parent companyparent company operations in Botswana only focus on production.operations in Botswana only focus on production. foreign owners do not stay in Botswana foreign owners do not stay in Botswana

• Sight weeks Sight weeks • important industry events like the Town Hall meeting. important industry events like the Town Hall meeting.

The GoB wants to create local expertise in the The GoB wants to create local expertise in the downstream diamond industry but the ownership downstream diamond industry but the ownership structure isstructure is

Fig. 4: Typical Ownership Structure of Buyers

International Sightholder

Local Sightholder

Diamantaire Family

License from DTC London

License from DTC Botswana

Local Shareholder

Listed in Major Stock Exchange

Israel (6)

Indian (2)

Belgium (5)

RSA (2)

Thailand (1)

Infrastructure Infrastructure

Infrastructure does not appear to be a major Infrastructure does not appear to be a major factor in determining the breath and depth of factor in determining the breath and depth of linkages in the downstream diamond industry. linkages in the downstream diamond industry.

Lack of some infrastructure currently being Lack of some infrastructure currently being addressed by the GoB. addressed by the GoB.

Industry started necessary infrastructure was not Industry started necessary infrastructure was not in placein place Informal exported Informal exported P40 million diamond security transfer facility P40 million diamond security transfer facility high security road connecting the airport and the high security road connecting the airport and the

diamond hub has also been built. diamond hub has also been built.

Skills SpilloversSkills Spillovers

Skill spillovers are not a major factor determining Skill spillovers are not a major factor determining linkages in the current and polishing industrylinkages in the current and polishing industry some skill spillovers public servants trained in the some skill spillovers public servants trained in the

mining industry mining industry now working in the cutting and polishing industry now working in the cutting and polishing industry

Industry specific skillsIndustry specific skills Piecemeal skillsPiecemeal skills Greatest potential in knowledge intensive Greatest potential in knowledge intensive

servicesservices

NSINSI Currently the NSI is not a major factor Currently the NSI is not a major factor

determining the breath and depth of linkages in determining the breath and depth of linkages in the downstream diamond industry but in the the downstream diamond industry but in the future it is expected to become a more important future it is expected to become a more important factor. factor. The Innovation Hub The Innovation Hub

• Knowledge intensive economyKnowledge intensive economy• Science and Technology Park Science and Technology Park • downstream industrydownstream industry• Oodi School of Technology Oodi School of Technology • Courses that will provide skills for the downstream industry. Courses that will provide skills for the downstream industry.

The importance of the NSI is determining the breath The importance of the NSI is determining the breath and depth of linkages is expected to grow over time. and depth of linkages is expected to grow over time.

Links with regional hubsLinks with regional hubs

Links with the South Africa’s diamond industry Links with the South Africa’s diamond industry play a factor in determining the breath and depth play a factor in determining the breath and depth of linkages in the Botswana’s downstream of linkages in the Botswana’s downstream industry. industry. inputs. inputs. Two issues Two issues

• Prices 15% to even 100% inflated in BotswanaPrices 15% to even 100% inflated in Botswana• time it took to get goods delivered time it took to get goods delivered

Service providers (AON, Marsh, ABN AMRO) with Service providers (AON, Marsh, ABN AMRO) with parent companies in South Africa and parent companies in South Africa and

• employ South African labour employ South African labour

PolicyPolicy Policy is a key factor in determining the breath and depth Policy is a key factor in determining the breath and depth

of linkages in the downstream industryof linkages in the downstream industry Political will Political will Industry specific policy is not yet available Industry specific policy is not yet available sensitive to the negotiations. sensitive to the negotiations.

Incentives:Incentives: 15% corporate tax for manufacturing industry vs. 20% for the 15% corporate tax for manufacturing industry vs. 20% for the

other industriesother industries No export duties on polished diamondsNo export duties on polished diamonds No import duties on equipmentNo import duties on equipment No training levy No training levy Training rebatesTraining rebates Tax on profits vs. tax on turnover (as in common practice in Tax on profits vs. tax on turnover (as in common practice in

other cutting and polishing centres)other cutting and polishing centres)

Additional MMCP IssuesAdditional MMCP Issues

Unavailability of quantitative dataUnavailability of quantitative data DiplomacyDiplomacy

Still to doStill to do

Refine questionnairesRefine questionnaires Complete interviews Complete interviews Get more quantitative dataGet more quantitative data Understand traditional and untraditional Understand traditional and untraditional

cutting and polishing centrescutting and polishing centres

Thank youThank you