Download - Bob Torkelson

Sutter Home Winery was shut down during Prohibition. It remained abandoned until 1947, when it was purchased by Mario and John Trinchero. They were immigrant brothers from NYC whose family had long been active

in the Italian wine business.

Mario Trinchero

Mario and Mary Trinchero with their

children Bob, Vera and Roger

The 1950s and 1960s

Sutter Home WineryBob Trinchero

1972: While experimenting with new ways to make his Zinfandel more robust, Bob drew off some of his free-run juice and fermented it as a “white” wine. When the first vintage of Oeil de Pedrix (Eye of the Partridge) was released it became an instant hit and all 220

cases sold out.

1975: The family changed the name of their successful pink wine to White Zinfandel and in 1987, it became the best selling premium wine in the USA!

Roger, Mario, and Bob Trinchero

Source: Nielsen Total US Food Data 26 weeks ending 10/12/13*Gomberg Fredrickson.

Source: Nielsen: Total US Retail Plus 52 Wks Ending 11/9/13

$10.0 $13.1

$30.7

$55.8

TTL SPIRITS TTL WINE TTL BEER TTL ALCH BEV

Source: Nielsens Total Retail

CHARDONNAY 18.1%

CABERNET SAUVIGNON 10.6%

PINOT GRIGIO/PINOT GRIS 8.5%

MERLOT 7.5%

OTHER RED BLEND 6.2%

PINOT NOIR 3.6%

SAUV BLANC/FUME 3.6%

MUSCAT/MOSCATO 5.1%

WHITE ZINFANDEL 5.0% OTHER SPARKLING

1.9%

OTHER RED 2.8%

OTHER CHAMPAGNE

1.6%

RIESLING 1.6%

MALBEC 1.4% OTHER WHITE BLEND

2.5%ZINFANDEL

1.0%

ALL OTHER18.8%

2.5%

3.7% 10.1%

(2.2%)

19.3%

9.5%9.1%

12.2%

(8.5%)

8.0%

(0.6%)

4.6%

(4.9%)

11.3%13.4%

(0.3%)

(10.0%)

0.0%

10.0%

20.0%

30.0%

*Other Red Blends includes Sweet Reds**Other Reds does not include any blends, only lesser known single varietals

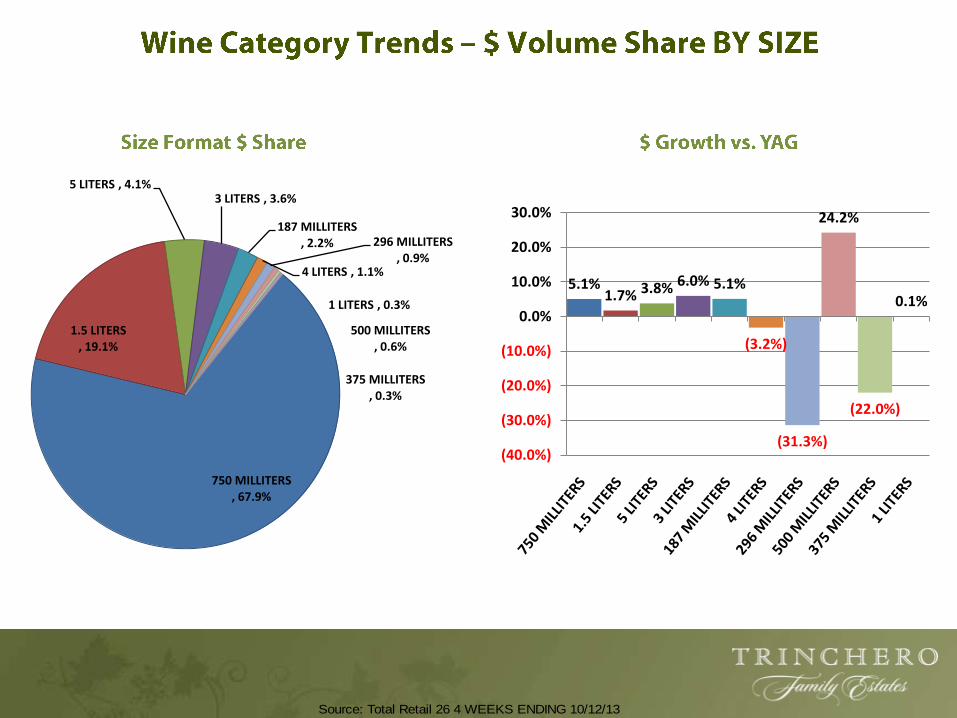

Source: Total Retail 26 4 WEEKS ENDING 10/12/13

Source: Total Retail 26 4 WEEKS ENDING 10/12/13

750 MILLITERS , 67.9%

1.5 LITERS , 19.1%

5 LITERS , 4.1%3 LITERS , 3.6%

187 MILLITERS , 2.2%

4 LITERS , 1.1%

296 MILLITERS , 0.9%

500 MILLITERS , 0.6%

375 MILLITERS , 0.3%

1 LITERS , 0.3%

5.1%1.7% 3.8% 6.0% 5.1%

(3.2%)

(31.3%)

24.2%

(22.0%)

0.1%

(40.0%)

(30.0%)

(20.0%)

(10.0%)

0.0%

10.0%

20.0%

30.0%

$20+4.2%

$15-19.995.8%

$12-14.9910.7%

$9-11.9922.6%

$6-8.9914.5%

$3-5.9934.9%

$0-2.997.2%

14.8%

8.8%

11.9%10.6%

(2.8%)

1.2% 1.3%

(10.0%)

0.0%

10.0%

20.0%

Source: Total Retail 26 4 WEEKS ENDING 10/12/13

24%

17%

14%

5% 4%4%

2% 2% 1% 1% 1% 1% 1% 1% 1%

21.0%

0%

5%

10%

15%

20%

25%

E&J G

ALLO

THE W

INE G

RO

UP

CO

NSTELLA

TION

TRIN

CH

ERO

FAM

ILY

TREA

SUR

Y WIN

E ESTATES

DEU

TSCH

FAM

ILY

STE MIC

HELLE ESTA

TES

BA

NFI V

INTN

ERS

JAC

KSO

N FA

MILY W

INES

DFV

WIN

ES

PA

LM B

AY IN

TERN

TL

DIA

GEO

BR

ON

CO

WIN

E CO

MP

AN

Y

BO

GLE V

INEYA

RD

S

FETZER V

INEYA

RD

S

All O

thers

Total WineCases +0.6%

Source: Nielsen 52 weeks ending 10/12/13

E&J GALLO THE WINE

GROUP CONSTELLAT

ION TRINCHERO

FAMILY TREASURY

WINE ESTATES DEUTSCH FAMILY

STE MICHELLE ESTATES

BANFI VINTNERS

JACKSON FAMILY WINES

DFV WINES PALM BAY INTERNTL

DIAGEO BRONCO

WINE COMPANY

BOGLE VINEYARDS

FETZER VINEYARDS

Case Growth

1% -4% 5% 1% -1% 5% 7% -3% 4% 22% 0% -10% -19% 20% 0%

Price Change

$ 0.25 $ 0.16 $(0.05) $ 0.22 $ (0.12) $ 0.01 $ 0.28 $ 0.07 $(0.10) $ 0.24 $ 0.14 $ 0.53 $ 0.14 $(0.09) $ 0.07

4.6%

4.0%

2.2%

2.8%

(2.2%)

5.6%

9.3%

5.7%

(1.5%)

(4.4%)

(10.0%) 0.0% 10.0% 20.0%

E&J GALLO

CONSTELLATION

THE WINE GROUP

TRINCHERO FAMILY

TREASURY WINE ESTATES

DEUTSCH FAMILY

STE MICHELLE ESTATES

JACKSON FAMILY WINES

BANFI VINTNERS

DIAGEO

Source: Nielsens Total Retail 26 4 WEEKS ENDING 10/12/13

•

•

•

•

•

•

•

•

Source: Total Retail 26 4 Weeks Ending 10/12/13

% Beer % Wine % Liquor

1994 71 14 13

2013 41 24 28

Change -30 10 15

Source: Gallup Poll, Aug. 2013

Key Bev-Al Category Trends

Consume Differently

• Nostalgic, Authentic, Local

• New is good; new brands, new flavors, new formats

Sweet and Decadent

• Sweeter wines(red blends, Moscatos) flavored spirits and liqueurs

• RTD Cocktails and mixers (pouch, glass, plastic)

Beyond Beer

• Premiumization; dark, craft, local

• Ciders, shandys, premium FMB’s

Source: Nielsen Scantrack - Total U.S. – All Outlets Combined ; 52 w/e 7-20-2013 versus prior year; UPC-coded; 119 categories (>$100MM annually)Bev Al; 52 w/e 5-25-2013; Nielsen Food, Drug, Mass, Walmart, Club, Dollar, Conv, MilitaryNote: Spirits excludes WA State

items

More Access Points

• Emerging channels; Convenience, Dollar Stores, Drug

• DTC, $1.46 B, growing at 10%

Source: Nielsen Scantrack - Total U.S. – All Outlets Combined ; 52 w/e 10-14-2013 versus prior year; UPC-coded; 119 categories (>$100MM annually)Bev Al; 52 w/e 5-25-2013; Nielsen Food, Drug, Mass, Walmart, Club, Dollar, Conv, MilitaryNote: Spirits excludes WA State

Key Retail Marketing Trends

Loyalty/Rewards Program

• E-coupons

• Fuel Rewards Programs

Private Label/Control Label

• Margin Makers

• Differentiation

Account Specific – Shopper Marketing

• Dunhumby/News America/In-store Radio

• Catalina

Source: Nielsen Scantrack - Total U.S. – All Outlets Combined ; 52 w/e 7-20-2013 versus prior year; UPC-coded; 119 categories (>$100MM annually)Bev Al; 52 w/e 5-25-2013; Nielsen Food, Drug, Mass, Walmart, Club, Dollar, Conv, MilitaryNote: Spirits excludes WA State

99

111

121

128

131

154

307

350

450

454

0 100 200 300 400 500

Germany

Chile

South Africa

Australia

Argentina

China

USA

Spain

France

Italy

Source: Trade Data and Analysis

Millions of Cases Produced

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

2008 2009 2010 2011 2012 2013

$930 $974

$800

$1,234$1,291

$1,410

*In Millions of US$

Source: Dept. of Commerce, Excludes re-exports of imported wines, 2013 results adjusted for apparent $70 million reporting error

+9%

•

•

•

•

•

•

•

• Declining consumer confidence, the government shutdown, and economic uncertainty have resulted in slower sales growth.

• Competition for market share from non-wine beverages. Craft beers, craft distilleries, and RTDs are grabbing share from the category.

• Channel blurring gives the consumer more options. Food store scan results are less of an impact today with the growth of chains like Costco, BevMo, Cost Plus & Trader Joes that are not reported.

• Muscat/Moscato trends are slowing. White Moscato sales are down in major retail, but pink and red Moscatos are still showing small growth.

• Economy wine sales are off especially in large size formats.

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

4500000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

White

Red

Total

20%

-7%

-3%21%

-6%4%

-16%

35%

-3%-8%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Coastal

Interior

Source: California Department of Food & Agriculture. Prepared by Gomberg Fredrickson & Associates

•

•

•

•