Laurent Vasilescu Professor Greenwald

[email protected] Legends of Value Investing

Page 1

Blue Nile Inc. (NYSE: NILE)

Latest Price $55.84 Recommended Price $11.34 Sales CAGR 10.40%

P/E 66.4 RecommendedP/E 11.19 5 Year Gross Margin 20.90%

52 Week Range $32.03-$67.16 Steady State Price $10.78 5 Year Operating Margin 6.70%

Market Cap ($MM) $808.79 PVGO $45.06 5 Year ROIC 23.80%

Shares Outstanding (MM) 14.481 Steady State+PVGO $55.84 5 Year EPS $0.86

Trading Data Valuation Operating Data

I. COMPANY DESCRIPTION

Blue Nile, Inc. is an online retailer of diamonds and jewelry, with a particular focus on

engagement diamonds and settings. The Company operates three Websites:

www.bluenile.com, www.bluenile.ca and www.bluenile.co.uk. Blue Nile websites showcase

diamonds and jewelry, including rings, wedding bands, earrings, necklaces, pendants, bracelets

and watches. In addition to sales of diamonds, jewelry and watches, the company provides

education, guidance and support to enable customers to learn about and purchase diamonds.

The company offers products for sale to customers in over 40 countries and territories

worldwide. The chart below shows the growth of Blue Nile stock relative to the S&P over the

last twelve months.

Laurent Vasilescu Professor Greenwald

[email protected] Legends of Value Investing

Page 2

II. THESIS SUMMARY

This summary recommends a strong SELL on Blue Nile, Inc. Blue Nile was around $32.00 a

share as of a year ago and is currently trading at $55.84 with a P/E multiple of 66.4. This

represents a 69 percent return while the S&P Index has risen by approximately 39 percent over

the same time period. The investment thesis recommends a strong SELL on Blue Nile for the

following reasons:

• Lack of a moat to sustain competitive advantage

• The strength of suppliers to determine pricing

• Risks associated with third party distribution

• Volatility of annual cash flows

• Risks of currency volatility

• Bricks and mortar competitors entering online space

Based on these factors detailed further below and the valuation model showcased as Exhibit 6

in the addendum, the company is valued at $11.34. This presents a real opportunity to short

sell Blue Nile for a significant return.

III. BUSINESS DESCRIPTION

This section provides a detailed overview of the company’s business operations without

providing a biased judgment on the company’s valuation.

Product Offering:

Blue Nile’s product offering consists of high quality diamonds and fine jewelry, with a particular

focus on engagement diamonds and settings. The company maintains diamond supplier

relationships which allow them to display suppliers’ diamond inventories on the Blue Nile

websites for sale to consumers without holding the diamonds in inventory until the products

are ordered by customers. The company purchases polished diamonds from several dozen

suppliers.

Blue Nile purchases diamonds on a “just in time” basis from suppliers when a customer places

an order for a specific diamond. The company then assembles the diamond with a ring,

pendant or earring setting from the inventory into customized diamond jewelry according to

the customer’s specifications. The finished jewelry is delivered to the customer generally within

three business days from the order date. The company offers diamonds with specified

characteristics in the areas of shape, cut, color, clarity and carat weight. A snapshot of the

company’s key website is attached below. The site allows customers to scale key

characteristics as they shop for a diamond in a certain price range. These sliding scale metrics

Laurent Vasilescu Professor Greenwald

[email protected] Legends of Value Investing

Page 3

utilize marketing conjoint analysis and allow for customers to place more importance on

different metrics such as carat weight, clarity and color. The screen shot shows that 31,640

round diamonds were found at Blue Nile ranging in price from $293 to $1,245,387.

While diamond engagement rings constitute the majority of sales for Blue Nile, the company

also offers a broad range of other fine jewelry products and watches. The fine jewelry selection

includes diamond, gemstone, platinum, gold, pearl and sterling silver jewelry and accessories as

well as settings, wedding bands, earrings, necklaces, pendants and bracelets. In the case of fine

jewelry, unlike most diamonds that Blue Nile sells, the company takes products into inventory

before they are ordered by customers. The fine jewelry and watches are purchased from over

40 manufacturers.

Suppliers:

The company typically enters into multi-year agreements with diamond suppliers that provide

for certain diamonds to be offered online to consumers exclusively through the Blue Nile

websites. The diamond supply agreements have expiration dates ranging from 2010 to 2014.

The diamond suppliers purchase rough and polished diamonds from sources throughout the

world. Their ability to supply Blue Nile with diamonds is dependent upon their ability to procure

these diamonds.

Laurent Vasilescu Professor Greenwald

[email protected] Legends of Value Investing

Page 4

Customer Service and Support:

Blue Nile provides a high level of customer service and support. The company augments the

online retail experience by providing a knowledgeable, highly trained support staff through call

centers to give customers confidence in their purchases. The call center consultants are trained

to provide guidance on all steps in the process of buying diamonds and fine jewelry.

The company prominently displays all of its guarantees and policies on the websites to create

an environment of trust. These include policies relating to privacy, security, product

availability, pricing, shipping, refunds, exchanges and special orders. Blue Nile typically offers a

return policy of 30 days. They generally do not extend credit to customers except through

third-party credit cards, although they maintain a relationship with a consumer financing

company that offers financing to customers.

Seasonality:

As with many retailers, Blue Nile generally experiences seasonal fluctuations in demand for its

products. Quarterly sales are impacted by various gift giving holidays including Valentine’s Day

(first quarter), Mother’s Day (second quarter) and Christmas (fourth quarter). As a result, the

company’s quarterly revenues are generally the lowest in the third quarter (as a result of the

lack of recognized gift giving holidays) and highest in the fourth quarter. The fourth quarter

accounted for approximately 34%, 29% and 35% of net sales in fiscal years 2009, 2008 and

2007, respectively.

Competition:

The diamond and fine jewelry retail market is intensely competitive and highly fragmented.

Competition comes from a wide array of different avenues from online and offline retailers.

Current or potential competitors include the following:

• Jewelry stores which are owned by individuals

• Retail jewelry store chains such as Tiffany & Co. and Zale’s

• Online retailers that sell jewelry such as Amazon

• Online auction sites such as EBay

• Catalog and television shopping retailers, such as Home Shopping Network and QVC

• Discount superstores and wholesale clubs, such as Wal-Mart and Costco Wholesale

• Internet shopping clubs, such as Gilt Groupe and Rue La La

Laurent Vasilescu Professor Greenwald

[email protected] Legends of Value Investing

Page 5

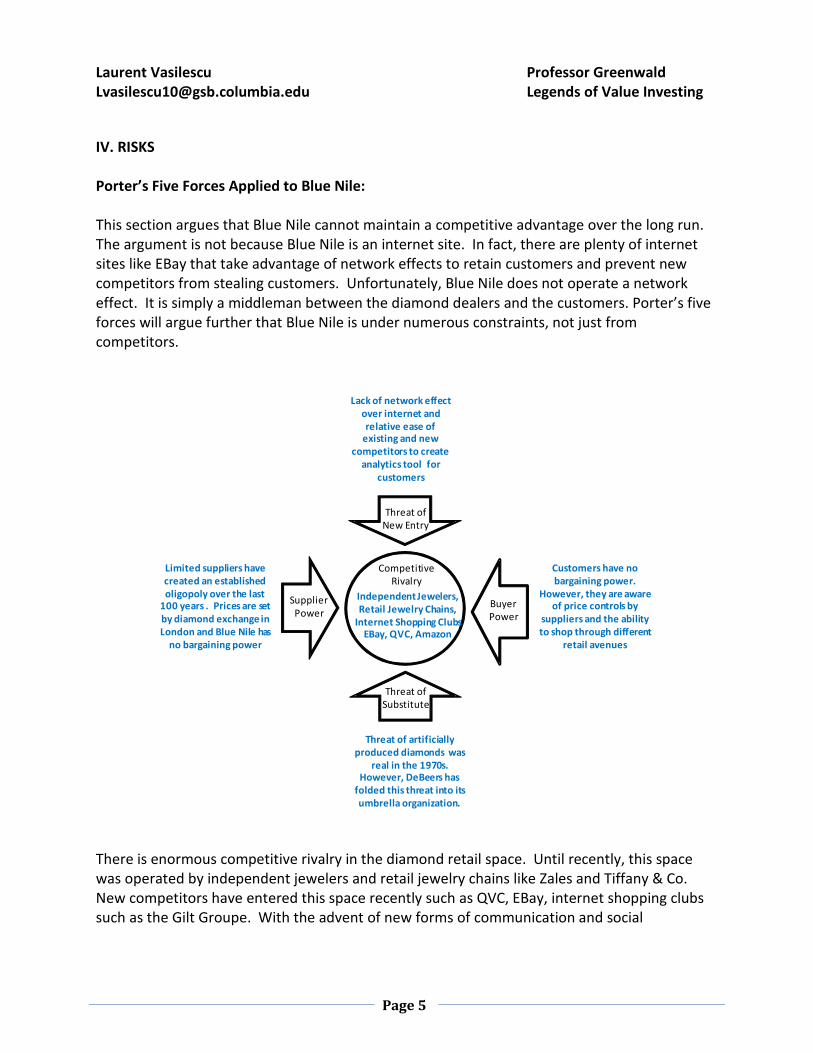

IV. RISKS

Porter’s Five Forces Applied to Blue Nile:

This section argues that Blue Nile cannot maintain a competitive advantage over the long run.

The argument is not because Blue Nile is an internet site. In fact, there are plenty of internet

sites like EBay that take advantage of network effects to retain customers and prevent new

competitors from stealing customers. Unfortunately, Blue Nile does not operate a network

effect. It is simply a middleman between the diamond dealers and the customers. Porter’s five

forces will argue further that Blue Nile is under numerous constraints, not just from

competitors.

Competitive

Rivalry

Buyer

Power

Supplier

Power

Threat of

Substitute

Threat of

New Entry

Threat of artificially

produced diamonds was

real in the 1970s. However, DeBeers has

folded this threat into its

umbrella organization.

Customers have no

bargaining power.

However, they are aware of price controls by

suppliers and the ability

to shop through different

retail avenues

Lack of network effect

over internet and

relative ease of existing and new

competitors to create

analytics tool for

customers

Limited suppliers have

created an established

oligopoly over the last 100 years . Prices are set

by diamond exchange in

London and Blue Nile has

no bargaining power

Independent Jewelers,

Retail Jewelry Chains,

Internet Shopping ClubsEBay, QVC, Amazon

There is enormous competitive rivalry in the diamond retail space. Until recently, this space

was operated by independent jewelers and retail jewelry chains like Zales and Tiffany & Co.

New competitors have entered this space recently such as QVC, EBay, internet shopping clubs

such as the Gilt Groupe. With the advent of new forms of communication and social

Laurent Vasilescu Professor Greenwald

[email protected] Legends of Value Investing

Page 6

interaction, new methods of exchanging goods will continue to put pressure on competing

retailers.

Alchemists have tried for centuries to recreate diamonds through artificial means. With the

introduction of true science during the 20th century, man finally found a way to apply nature’s

forces in a laboratory and recreate diamonds through artificially means. According to the book,

The Rise and Fall of Diamonds by Edward Jay Epstein, General Electric invented artificial

diamond production in 1954 at a laboratory located in Schenectady, New York. The first

artificial diamonds were small and industrial grade. However, over the decades, methods have

improved and now many industrial diamonds are identical to true diamonds. De Beers which

maintains a virtual monopoly on the supply of diamonds around the world has purchased

virtually all artificial means of creating diamonds and limited their supply.

Market Insight Information:

Since Blue Nile is an online retailer, this report attempts to use the market insight tools

available on the internet to gauge Blue Nile’s popularity on the internet. Google Insight is a

remarkable online tool that allows anyone to search the frequency of a word search over a

period of time. The snapshot below shows the frequency of the world search “Blue Nile

Diamond” over the last five years. The snapshot clearly shows that peak searches for the words

“Blue Nile Diamond” occurs every year during the fourth quarter prior to the Holiday Season.

The graph below also shows that the frequency has not increased or waned over the last five

years. In fact, the graph indicates that the search has remained extremely constant overtime.

This indication was factored into the valuation model with regards to the increase in sales over

the long run. The long run sales growth is estimated at 3 percent in the valuation model.

Laurent Vasilescu Professor Greenwald

[email protected] Legends of Value Investing

Page 7

In addition to the frequency of the word search over the last five years, the screenshot

provided below shows where these word searches originate. While Blue Nile boasts about the

fact that it can ship products to over 40 countries worldwide, the screenshot below is stark

realization that the majority of customers are domiciled in the United States and Canada. Blue

Nile will need to strongly reevaluate its international marketing efforts if it banks on strong

sales growth coming from abroad.

Laurent Vasilescu Professor Greenwald

[email protected] Legends of Value Investing

Page 8

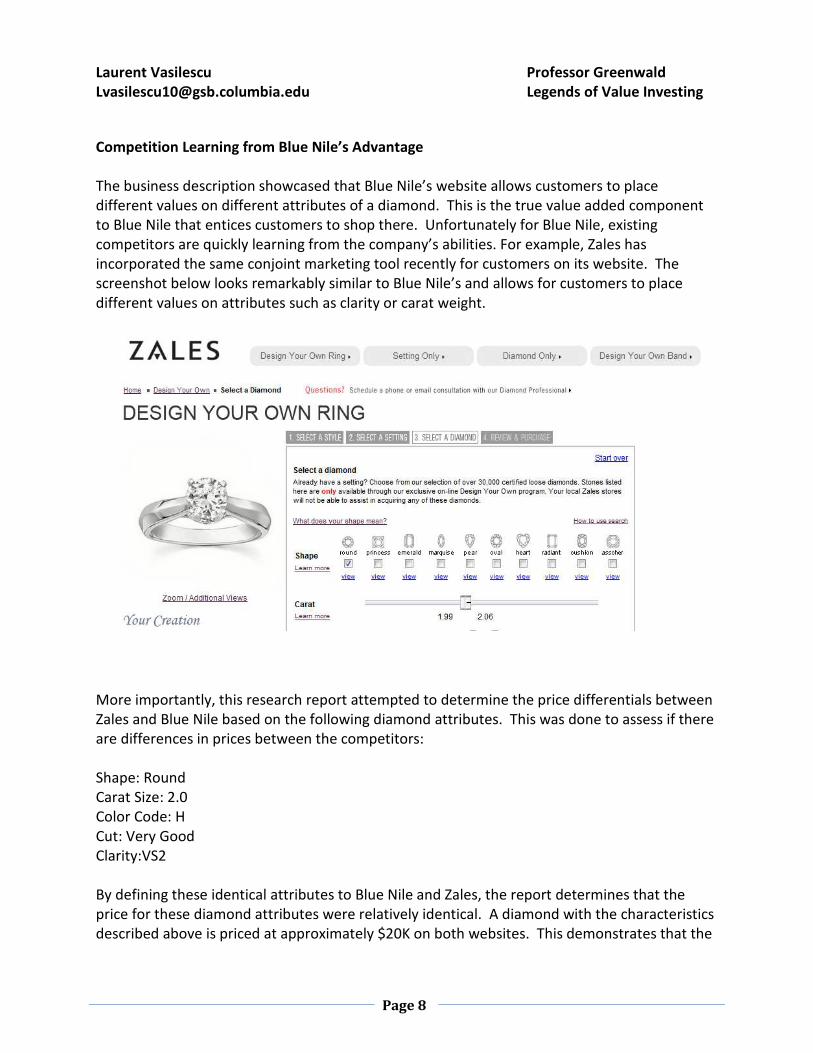

Competition Learning from Blue Nile’s Advantage

The business description showcased that Blue Nile’s website allows customers to place

different values on different attributes of a diamond. This is the true value added component

to Blue Nile that entices customers to shop there. Unfortunately for Blue Nile, existing

competitors are quickly learning from the company’s abilities. For example, Zales has

incorporated the same conjoint marketing tool recently for customers on its website. The

screenshot below looks remarkably similar to Blue Nile’s and allows for customers to place

different values on attributes such as clarity or carat weight.

More importantly, this research report attempted to determine the price differentials between

Zales and Blue Nile based on the following diamond attributes. This was done to assess if there

are differences in prices between the competitors:

Shape: Round

Carat Size: 2.0

Color Code: H

Cut: Very Good

Clarity:VS2

By defining these identical attributes to Blue Nile and Zales, the report determines that the

price for these diamond attributes were relatively identical. A diamond with the characteristics

described above is priced at approximately $20K on both websites. This demonstrates that the

Laurent Vasilescu Professor Greenwald

[email protected] Legends of Value Investing

Page 9

retailers’ prices are possibly determined by the oligopoly of suppliers that furnish the diamonds

to the retailers.

V. VALUATION

The valuation exercise employs the Discount Cash Flow approach detailed in the exhibits

attached this report. The DCF valuation comes to a price of $11.34 per share for Blue Nile. As a

result, Blue Nile is significantly overvalued with the current price of $55.84 as the market

believes that there is significant growth and Blue Nile will remain the dominant internet player

in diamond retailing. The section below outlines the individual exhibits attached to the

valuation and the assumptions made that derive a value of $11.34 per share.

Exhibits 1, 2 and 3: These exhibits provide a historical overview of Blue Nile’s Income

Statement, Balance Sheet, and Cash Flow Statement for the last six years since 2004. While

there was significant growth from 2004 to 2007, sales growth has declined and rebounded

modestly since the financial crisis. More importantly, while sales have increased, operating

margins have decreased significantly from 8.8% to 6.4% over the last five years. This

represents a 27% decrease in overall operating margin. The balance sheet shows that Blue Nile

held significant cash until the financial crisis and it now employs debt in the capital structure.

The Cash Flow Statement shows extreme volatility in the increases and decreases in cash from

year to year.

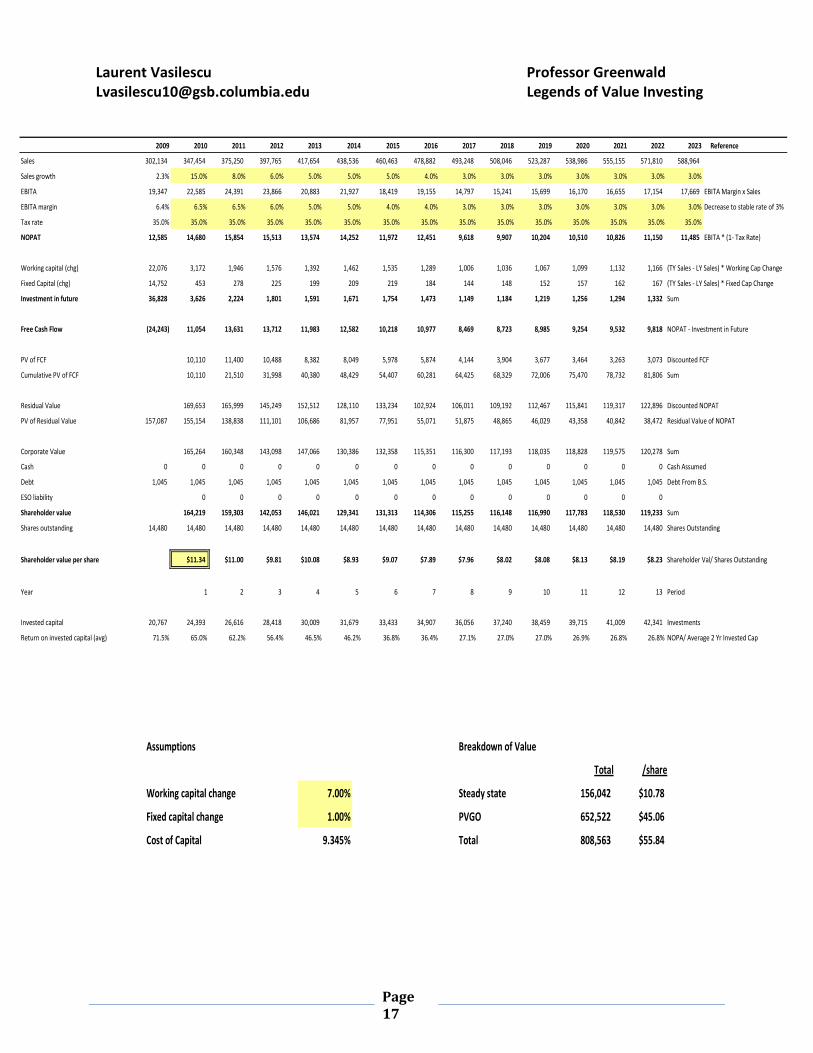

Exhibits 4, 5 and 6: Exhibit 4 uses both the financing and operating approaches to demonstrate

that free cash flow oscillates significantly on an annual basis. One year, Free Cash Flow

amounts to $12 million and other years amount to $68 million and -$24 million. Exhibits 5 and

6 create predictability and stability in sales, margins and cash flows for valuation purposes.

Blue Nile has very little debt but the WACC assumes an optimal debt to capital ratio of 25

percent as the company matures and takes advantage of future tax shields through debt

financing. The assumed WACC amounts to 9.345 percent. Exhibit 6 which details the valuation

model assumes that sales will rebound quickly to historical levels over the next two years.

However, from 2012 onwards, sales growth will mature from 5 percent to a terminal rate of 3

percent. EBITA margins will continue to erode from 6.5 percent to 3 percent as new entrants

begin competing with Blue Nile on the internet. Working and Fixed Capital changes amount to 7

percent and 1 percent, respectively. Fixed capital changes are minimal after reviewing the

annual reports and determining that relatively little fixed capital is needed to increase scale for

Blue Nile.

Laurent Vasilescu Professor Greenwald

[email protected] Legends of Value Investing

Page

10

A breakdown of the current share price is also provided in Exhibit 6. Based on the current price

of $55.84, the steady state assumes only $10.78 of the value while the remaining value of

$45.06 is attributed to present value of growth opportunity or PVGO.

VI. Conclusion:

There is clearly a mismatch in the value of Blue Nile and the current price for its shares. Blue

Nile’s website is sleek and provides a useful analytical tool for men to purchase engagement

rings for their fiancées. However, the vast majority of Blue Nile customers are not repeat

customers since most men hopefully only get married once. Blue Nile needs to capture new

customers through word of mouth from past customers. More importantly, competitors such

as Zales and Tiffany & Co. are adapting their websites to provide the same metric tools for their

customers. This added functionality will allow them to steal customers from Blue Nile. The

application of Porter’s Five forces show the intense competitive landscape and the power of

suppliers in the diamond market. The application of these forces were considered in the

valuation model which shows Blue Nile maturing very quickly over the next two years while the

market currently places a significant premium on potential growth.

Laurent Vasilescu Professor Greenwald

[email protected] Legends of Value Investing

Page

11

EXHIBIT 1: HISTORICAL INCOME STATEMENT

2004 chg. 2005 chg. 2006 chg. 2007 chg. 2008 chg. 2009 chg.

(1) Net sales 169,242.0 #DIV/0! 203,169.0 20.0% 251,587.0 23.8% 319,264.0 26.9% 295,329.0 -7.5% 302,134.0 2.3%

(2) Cost of sales 131,658.0 #DIV/0! 158,127.0 20.1% 200,734.0 26.9% 254,060.0 26.6% 235,333.0 -7.4% 236,790.0 0.6%

(3) Gross income 37,584.0 #DIV/0! 45,042.0 19.8% 50,853.0 12.9% 65,204.0 28.2% 59,996.0 -8.0% 65,344.0 8.9%

Gross margin 22.2% -- 22.2% -- 20.2% -- 20.4% -- 20.3% -- 21.6% --

(4) S, G & A 22,727.0 #DIV/0! 26,993.0 18.8% 34,296.0 27.1% 42,792.0 24.8% 44,005.0 2.8% 45,997.0 4.5%

(5) Amortization #DIV/0! #DIV/0! #DIV/0! #DIV/0! #DIV/0!

(6) Operating income (EBIT) 14,857.0 #DIV/0! 18,049.0 21.5% 16,557.0 -8.3% 22,412.0 35.4% 15,991.0 -28.6% 19,347.0 21.0%

Operating margin 8.8% -- 8.9% -- 6.6% -- 7.0% -- 5.4% -- 6.4% --

(7) Interest expense (772.0) #DIV/0! (2,504.0) 224.4% (3,423.0) 36.7% (4,175.0) 22.0% (1,865.0) -55.3% (331.0) -82.3%

(8) Other (net) #DIV/0! #DIV/0! #DIV/0! #DIV/0! #DIV/0! #DIV/0!

(9) Pretax income 15,629.0 #DIV/0! 20,553.0 31.5% 19,980.0 -2.8% 26,587.0 33.1% 17,856.0 -32.8% 19,678.0 10.2%

(10) Income tax 5,642.0 #DIV/0! 7,400.0 31.2% 6,916.0 -6.5% 9,128.0 32.0% 6,226.0 -31.8% 6,878.0 10.5%

(11) Net income 9,987.0 #DIV/0! 13,153.0 31.7% 13,064.0 -0.7% 17,459.0 33.6% 11,630.0 -33.4% 12,800.0 10.1%

(12) Earnings per share $0.60 #DIV/0! $0.75 24.3% $0.79 5.2% $1.10 39.0% $0.78 -29.0% $0.88 13.4%

(13) Shares outstanding 16,563.0 #DIV/0! 17,550.0 6.0% 16,563.0 -5.6% 15,919.0 -3.9% 14,925.0 -6.2% 14,480.0 -3.0%

(14) Tax rate 36.1% -- 36.0% -- 34.6% -- 34.3% -- 34.9% -- 35.0% --

Laurent Vasilescu Professor Greenwald

[email protected] Legends of Value Investing

Page

12

EXHIBIT 2: Balance Sheet Historicals

2004 2005 2006 2007 2008 2009

(15) Cash and equivalents 101,367.0 114,788.0 98,433.0 122,793.0 54,451.0 93,149.0

(16) Accounts receivable 1,028.0 1,877.0 1,640.0 3,576.0 1,709.0 1,835.0

(17) Inventories 9,914.0 11,764.0 14,616.0 20,906.0 18,834.0 19,434.0

(18) Other current assets 9,220.0 4,067.0 1,338.0 1,871.0 1,739.0 1,426.0

(19) Current assets 121,529.0 132,496.0 116,027.0 149,146.0 76,733.0 115,844.0

(20) Net PP&E 3,916.0 3,261.0 3,391.0 7,601.0 7,558.0 7,332.0

(21) Other assets 2,937.0 2,248.0 2,697.0 3,839.0 5,374.0 7,239.0

Total assets 128,382.0 138,005.0 122,115.0 160,586.0 89,665.0 130,415.0

(22) S-T debt 203.0 208.0 197.0 276.0 246.0 249.0

(23) Accounts payable 37,775.0 50,157.0 66,625.0 85,866.0 62,291.0 76,128.0

(24) Accrued expenses 5,713.0 5,262.0 7,315.0 9,549.0 6,607.0 9,805.0

(25) Income taxes

(26) Current liabilities 43,691.0 55,627.0 74,137.0 95,691.0 69,144.0 86,182.0

(27) Long-term debt 0.0 0.0 0.0 880.0 839.0 796.0

(28) Other liabilities 1,071.0 863.0 666.0 538.0 374.0 168.0

(29) Deferred taxes

(30) Common stock/paid in 104,684.0 106,341.0 115,751.0 134,207.0 144,913.0 156,030.0

(31) Retained earnings (19,515.0) (6,362.0) 7,110.0 24,569.0 36,199.0 48,999.0

(32) Treasury stock 636.0 18,008.0 75,395.0 95,391.0 161,841.0 161,841.0

(33) Cummulative translation adjustment 913.0 456.0 163.0 (92.0) (37.0) (81.0)

(34) Equity 83,620.0 81,515.0 47,303.0 63,477.0 19,308.0 43,269.0

Total liabilities/equity 128,382.0 138,005.0 122,106.0 160,586.0 89,665.0 130,415.0

Laurent Vasilescu Professor Greenwald

[email protected] Legends of Value Investing

Page

13

EXHIBIT 3: STATEMENT OF CASH FLOWS

2004 2005 2006 2007 2008 2009

Net earnings 9,987.0 13,153.0 13,064.0 17,459.0 11,630.0 12,800.0

(35)Depreciation 1,510.0 1,717.0 1,868.0 1,772.0 2,110.0 2,593.0

(36) Intangible amortization

(37)Changes in operating working capital 12,496.0 7,415.0 15,926.0 12,806.0 (22,773.0) 16,096.0

(38)Gains on divestitures, pension funding and other 5,758.0 8,987.0 9,660.0 9,418.0 6,106.0 7,529.0

(39)Net cash provided by operating activities 29,751.0 31,272.0 40,518.0 41,455.0 (2,927.0) 39,018.0

(40)Capital expenditures (1,826.0) (1,064.0) (1,907.0) (4,874.0) (2,000.0) (2,345.0)

(41)Purchases of businesses

(42)Divestitures and other (41,470.0) (989.0) 22,972.0 19,890.0 0.0 (15,000.0)

(43)Net cash used in investing activities (43,296.0) (2,053.0) 21,065.0 15,016.0 (2,000.0) (17,345.0)

(44)Net increase in short-term debt

(45)Proceeds from long-term debt

(46)Principle payments on long-term debt

(47)Net purchases of treasury stock 42,516.0 (17,372.0) (57,387.0) (19,996.0) (66,450.0) 0.0

(48)Dividends paid

(49)Other 145.0 575.0 2,423.0 7,700.0 3,093.0 1,981.0

(50)Net cash provided (used) in financing 42,661.0 (16,797.0) (54,964.0) (12,296.0) (63,357.0) 1,981.0

(51)Currency 0.0 0.0 0.0 78.0 (58.0) 44.0

Increase (decrease) in cash 29,116.0 12,422.0 6,619.0 44,253.0 (68,342.0) 23,698.0

Laurent Vasilescu Professor Greenwald

[email protected] Legends of Value Investing

Page

14

EXHIBIT 4: Historical Cash Flow Analysis

Operating approach

Description 2005 2006 2007 2008 2009 Reference

Net sales 203,169 251,587 319,264 295,329 302,134 line 1

- Cost of goods sold 158,127 200,734 254,060 235,333 236,790 line 2

Gross income 45,042 50,853 65,204 59,996 65,344 line 3

- R&D 0 0 0 0 0 N/A

- SG&A 26,993 34,296 42,792 44,005 45,997 line 4

- Amortization 0 0 0 0 0 line 5

EBIT 18,049 16,557 22,412 15,991 19,347

+ Amortization 0 0 0 0 0 line 5

EBITA 18,049 16,557 22,412 15,991 19,347

EBITA / Sales 8.9% 6.6% 7.0% 5.4% 6.4%

- Income tax provision 7,400 6,916 9,128 6,226 6,878 line 10

- Tax shield (902) (1,185) (1,433) (650) (116) (-line 7 - line 8)*line 14

NOPAT 11,551 10,826 14,717 10,415 12,585

Tax Rate 36% 35% 34% 35% 35%

Change in working capital (964) (34,990) 11,644 (45,896) 22,076 This Year - Last Year

Capital spending (net of depreciation) (653) 39 3,102 (110) (248) (line 40 * -1) - line 35

Acquisitions (net of divestitures) 989 (22,972) (19,890) 0 15,000 (line 41 + line 42) * -1

Total Investments (628) (57,923) (5,144) (46,006) 36,828

Free Cash Flow 12,179 68,749 19,861 56,421 (24,243)

Financing approach

Description 2005 2006 2007 2008 2009 Reference

Net income 13,153 13,064 17,459 11,630 12,800 line 11

+ Amortization 0 0 0 0 0 line 5

Adjusted income for common 13,153 13,064 17,459 11,630 12,800

- Other income, net 2,504 3,423 4,175 1,865 331 - line 7 - line 8

- Tax shield (902) (1,185) (1,433) (650) (116) (-line 7 - line 8)*line 14

NOPAT 11,551 10,826 14,717 10,415 12,585

Change in working capital (964) (34,990) 11,644 (45,896) 22,076 This Year - Last Year

Capital spending (net of depreciation) (653) 39 3,102 (110) (248) (line 40 * -1) - line 35

Acquisitions (net of divestitures) 989 (22,972) (19,890) 0 15,000 (line 41 + line 42) * -1

Total Investments (628) (57,923) (5,144) (46,006) 36,828

Free Cash Flow 12,179 68,749 19,861 56,421 (24,243)

Laurent Vasilescu Professor Greenwald

[email protected] Legends of Value Investing

Page

15

EXHIBIT 5: Weighted Cost of Capital

1. K equity = risk-free rate + (beta * equity risk premium) 2. K debt = YTM on L-T debt * (1 - cash tax rate)

Risk-free (10-year Treasury) = 3.87% Risk-free (10-year Treasury) = 3.87%

Beta = 1.66 Spread = 1.30%

Equity risk premium = 4.50% Tax rate = 35.0%

Ke = 11.34% Kd = 3.36%

3. Debt to total capital (market values) 4. Weighted average cost of capital

Target weights

Total debt = 1,045.0 Kd= 3.4% 25.0% 0.8%

Shares outstanding = 14,480 Ke= 11.3% 75.0% 8.5%

Stock price = $55.84

Current Debt/total capital = 0.13% WACC = 9.345%

Target debt/total capital = 25.00%

Laurent Vasilescu Professor Greenwald

[email protected] Legends of Value Investing

Page

16

EXHIBIT 6: Valuation

Operating approach

Description 2004 2005 2006 2007 2008 2009 Reference

Cash 101,367 114,788 98,433 122,793 54,451 93,149 line 15

Accounts receivable 1,028 1,877 1,640 3,576 1,709 1,835 line 16

Inventories 9,914 11,764 14,616 20,906 18,834 19,434 line 17

Deferred tax assets 0 0 0 0 0 0 N/A

Other 9,220 4,067 1,338 1,871 1,739 1,426 line 18

Total current assets 121,529 132,496 116,027 149,146 76,733 115,844

- NIBCLs 43,488 55,419 73,940 95,415 68,898 85,933 line 23 + line 24 + line 25

Net working capital 78,041 77,077 42,087 53,731 7,835 29,911

+Net PP&E 3,916 3,261 3,391 7,601 7,558 7,332 line 20

+Goodwill N/A

+ Intangibles N/A

+Other assets 2,937 2,248 2,697 3,839 5,374 7,239 line 21

Invested capital 84,894 82,586 48,175 65,171 20,767 44,482

(*) cash = 4 percent of sales.

Financing approach

Description 2004 2005 2006 2007 2008 2009 Reference

Current portion LT debt 203 208 197 276 246 249 line 22

Long Term debt 0 0 0 880 839 796 line 27

Deferred Taxes 0 0 0 0 0 0 line 29

+Other 1,071 863 666 538 374 168 line 28

+Minority interest N/A

Shareholders' equity 83,620 81,515 47,303 63,477 19,308 43,269 line 34 - line 15 + (line 1 * 4%)

Invested capital 84,894 82,586 48,166 65,171 20,767 44,482

Investment in future growth (I)

Description 2005 2006 2007 2008 2009 Reference

Change in working capital (964) (34,990) 11,644 (45,896) 22,076 TY - LY

Capital spending (net of depreciation) (653) 39 3,102 (110) (248) (line 40 * -1) - line 35

Acquisitions (net of divestitures) 989 (22,972) (19,890) 0 15,000 (line 41 + line 42) * -1

Investment in future growth (628) (57,923) (5,144) (46,006) 36,828

Laurent Vasilescu Professor Greenwald

[email protected] Legends of Value Investing

Page

17

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 Reference

Sales 302,134 347,454 375,250 397,765 417,654 438,536 460,463 478,882 493,248 508,046 523,287 538,986 555,155 571,810 588,964

Sales growth 2.3% 15.0% 8.0% 6.0% 5.0% 5.0% 5.0% 4.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0%

EBITA 19,347 22,585 24,391 23,866 20,883 21,927 18,419 19,155 14,797 15,241 15,699 16,170 16,655 17,154 17,669 EBITA Margin x Sales

EBITA margin 6.4% 6.5% 6.5% 6.0% 5.0% 5.0% 4.0% 4.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0% Decrease to stable rate of 3%

Tax rate 35.0% 35.0% 35.0% 35.0% 35.0% 35.0% 35.0% 35.0% 35.0% 35.0% 35.0% 35.0% 35.0% 35.0% 35.0%

NOPAT 12,585 14,680 15,854 15,513 13,574 14,252 11,972 12,451 9,618 9,907 10,204 10,510 10,826 11,150 11,485 EBITA * (1- Tax Rate)

Working capital (chg) 22,076 3,172 1,946 1,576 1,392 1,462 1,535 1,289 1,006 1,036 1,067 1,099 1,132 1,166 (TY Sales - LY Sales) * Working Cap Change

Fixed Capital (chg) 14,752 453 278 225 199 209 219 184 144 148 152 157 162 167 (TY Sales - LY Sales) * Fixed Cap Change

Investment in future 36,828 3,626 2,224 1,801 1,591 1,671 1,754 1,473 1,149 1,184 1,219 1,256 1,294 1,332 Sum

Free Cash Flow (24,243) 11,054 13,631 13,712 11,983 12,582 10,218 10,977 8,469 8,723 8,985 9,254 9,532 9,818 NOPAT - Investment in Future

PV of FCF 10,110 11,400 10,488 8,382 8,049 5,978 5,874 4,144 3,904 3,677 3,464 3,263 3,073 Discounted FCF

Cumulative PV of FCF 10,110 21,510 31,998 40,380 48,429 54,407 60,281 64,425 68,329 72,006 75,470 78,732 81,806 Sum

Residual Value 169,653 165,999 145,249 152,512 128,110 133,234 102,924 106,011 109,192 112,467 115,841 119,317 122,896 Discounted NOPAT

PV of Residual Value 157,087 155,154 138,838 111,101 106,686 81,957 77,951 55,071 51,875 48,865 46,029 43,358 40,842 38,472 Residual Value of NOPAT

Corporate Value 165,264 160,348 143,098 147,066 130,386 132,358 115,351 116,300 117,193 118,035 118,828 119,575 120,278 Sum

Cash 0 0 0 0 0 0 0 0 0 0 0 0 0 0 Cash Assumed

Debt 1,045 1,045 1,045 1,045 1,045 1,045 1,045 1,045 1,045 1,045 1,045 1,045 1,045 1,045 Debt From B.S.

ESO liability 0 0 0 0 0 0 0 0 0 0 0 0 0

Shareholder value 164,219 159,303 142,053 146,021 129,341 131,313 114,306 115,255 116,148 116,990 117,783 118,530 119,233 Sum

Shares outstanding 14,480 14,480 14,480 14,480 14,480 14,480 14,480 14,480 14,480 14,480 14,480 14,480 14,480 14,480 Shares Outstanding

Shareholder value per share $11.34 $11.00 $9.81 $10.08 $8.93 $9.07 $7.89 $7.96 $8.02 $8.08 $8.13 $8.19 $8.23 Shareholder Val/ Shares Outstanding

Year 1 2 3 4 5 6 7 8 9 10 11 12 13 Period

Invested capital 20,767 24,393 26,616 28,418 30,009 31,679 33,433 34,907 36,056 37,240 38,459 39,715 41,009 42,341 Investments

Return on invested capital (avg) 71.5% 65.0% 62.2% 56.4% 46.5% 46.2% 36.8% 36.4% 27.1% 27.0% 27.0% 26.9% 26.8% 26.8% NOPA/ Average 2 Yr Invested Cap

Assumptions Breakdown of Value

Total /share

Working capital change 7.00% Steady state 156,042 $10.78

Fixed capital change 1.00% PVGO 652,522 $45.06

Cost of Capital 9.345% Total 808,563 $55.84