Building Better Home Builders

© 2010 Building Better Home Builders Inc. (BBHB). All rights reserved. The content of this presentation is protected by the copyrights of BBHB.

No part of the content may be reproduced, distributed in any form or otherwise used without the prior written permission of BBHB.

Introduction

Building Better Home Builders was established for the sole purpose of providing professional , confidential consulting services for the

homebuilding industry.

JOB ESTIMATING: IT CAN MAKE

OR BREAK YOUR COMPANY

Presentation to GOHBA Renovator’s Council

July 21, 2010

By Rick Ottenhof

BUILDING BETTER HOME BUILDERS

All the help you need under one roof!

Today’s presentation

Elements of your job estimate

Different forms of estimating projects

Understanding overheads and determining the value

Markups

Some closing thoughts

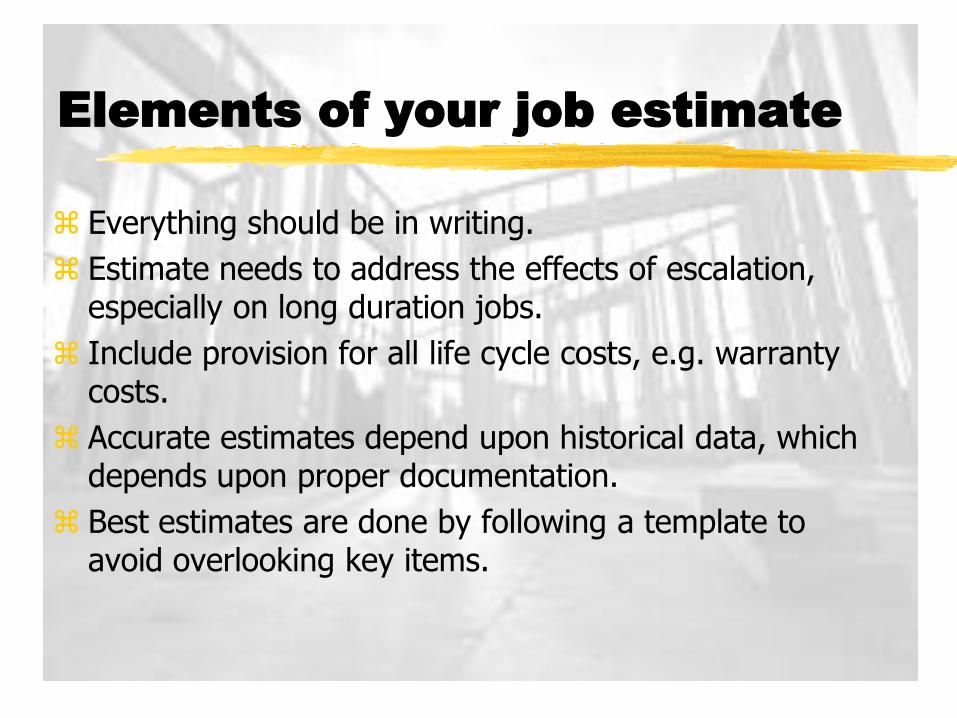

Elements of your job estimate

Everything should be in writing.

Estimate needs to address the effects of escalation, especially on long duration jobs.

Include provision for all life cycle costs, e.g. warranty costs.

Accurate estimates depend upon historical data, which depends upon proper documentation.

Best estimates are done by following a template to avoid overlooking key items.

Elements of your job estimate

Direct labour, materials and sub trade contracts

Direct labour- Dollar value of labour, benefits, employer CPP, EI, WSIB, EHT, etc. for employees that can be charged/assigned to the specific job (including the owner).

Materials – the cost of materials that will be consumed/installed in the job including shipping and handling.

Sub-trades – the negotiated price for a specific job or a pre-negotiated price for a set piece of work (standing offer for work).

Elements of your job estimate

Overhead costs

Advertising and Marketing – brochures, newspaper ads, fliers, direct mail, travel to promote business, trade shows, GOHBA dinner meetings, promotion expense, conferences.

Sales – agency fees, commissions, sales office, promotional expenses, finder’s fees.

Office – rent, home office, computer, telephone, office equipment, stationery, staff, property/business taxes.

Job expenses – computers, cell phones, radios, tools and equipment, staff supervision of jobs (including payroll costs and performance bonuses), vehicle expenses, etc.

Elements of your job estimate

Overhead costs

Administrative – owner’s salary, education/training, licensing and association fees, accounting, legal, insurance (liability), banking, business financing, bad debts, etc.

Warranty - estimated cost of maintaining the communicated building warranty.

Cash flow reserve - estimated amount of cash on hand required to “float/bridge” cash requirements when expenses can’t be supported by cash receipts.

Elements of your job estimate

Profit

What’s left over for you – calculated as:

Sales - less job costs – overhead = Profit.

Elements of your job estimate

Understanding overheads

Don’t forget to pay yourself!

Every business has overhead.

Overheads calculated as annual costs (your budget).

Update overheads as circumstances change.

Differentiate the fixed and variable overhead for ease of determining in-year adjustments.

Don’t use a flat rate obtained from some other business –everyone is different!

Remember it is a budget and needs to be monitored.

The different forms of

estimating projects

GUESSTIMATING DON’T GO THERE!

STICK ESTIMATING

UNIT COSTING

The different forms of

estimating projects

GUESSTIMATING

Accompanied by little or no documentation, hence no intelligence for the future and no ability to address questions or enquiries about cost.

Customers see through it – your credibility can suffer.

You will lose money – eventually.

If you do make money you won’t know where or how you did!

Not sustainable – hard to repeat the formula!!!!!!!

Stressful way to run a business.

The different forms of

estimating projects

STICK ESTIMATING

Review sketches and plans.

Complete a material take off list and obtain supplier pricing.

Estimate the labour required to perform individual tasks.

Add up materials and labour - add markup and profit.

Make sure that you have a good/up to date set of drawings, sketches.

The different forms of

estimating projects

STICK ESTIMATING

The pros and cons:

Requires more time to prepare

Materials list and labour of little value if no contract

Time better spent on value add work

May work for a unique, one of a kind, specialty job

The different forms of

estimating projects

UNIT COSTING

Unit costing is also called “lump sum costing”.

Every job can be broken out into a series of work units Work Breakdown Structure (WBS).

Follow predetermined/known steps in completing a renovation.

Estimate the labour component, materials and sub-contracts for each step.

Make sure that you have a good/up to date set of drawings.

The different forms of

estimating projects

UNIT COSTING

The pros and cons:

Time is money and this approach can make estimating quicker

Michael Stone says “using this method can reduce time taken for estimating by 30 to 40%”

Actual costs can be recorded against each item/step for tracking purposes

Keeps you disciplined and covers ALL components of the job – less chance of missing something

The different forms of

estimating projects

UNIT COSTING

The pros and cons

The steps you are planning can be easily explained to the customer

When you decide you are ready for technology – taking that next step is easier

Should be more accurate (remember the point about tracking and history)

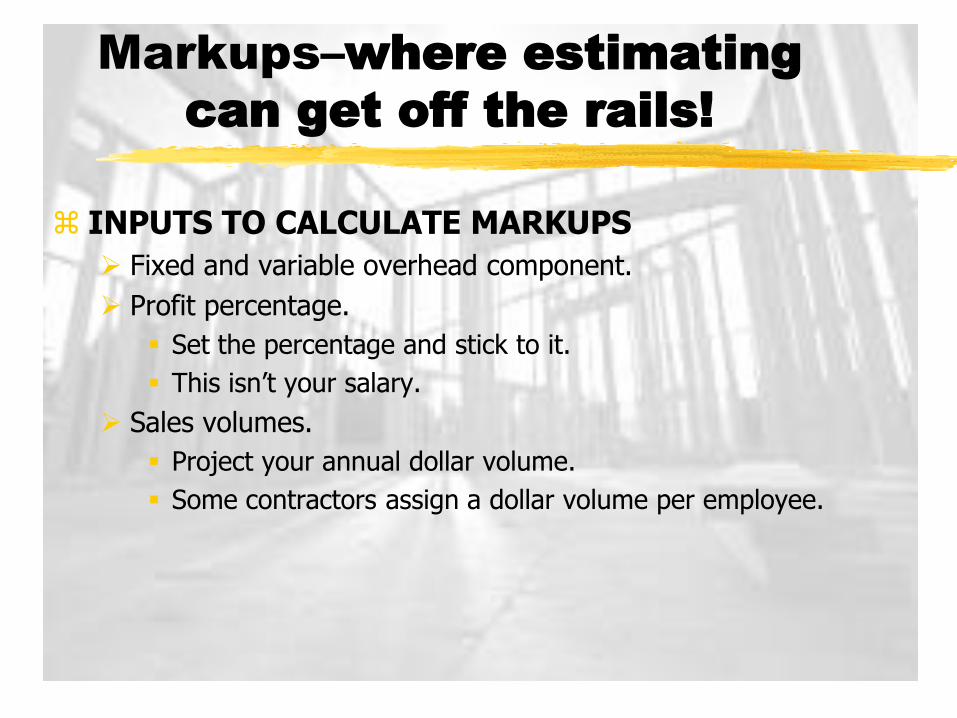

Markups–where estimating

can get off the rails!

INPUTS TO CALCULATE MARKUPS

Fixed and variable overhead component.

Profit percentage.

Set the percentage and stick to it.

This isn’t your salary.

Sales volumes.

Project your annual dollar volume.

Some contractors assign a dollar volume per employee.

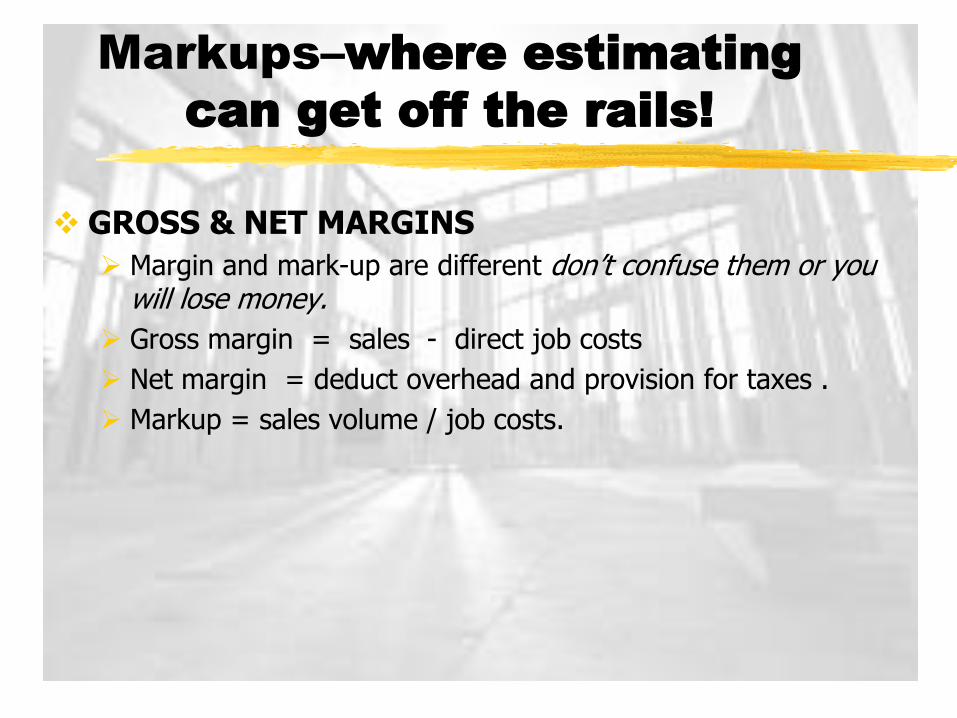

Markups–where estimating

can get off the rails!

GROSS & NET MARGINS

Margin and mark-up are different don’t confuse them or you will lose money.

Gross margin = sales - direct job costs

Net margin = deduct overhead and provision for taxes .

Markup = sales volume / job costs.

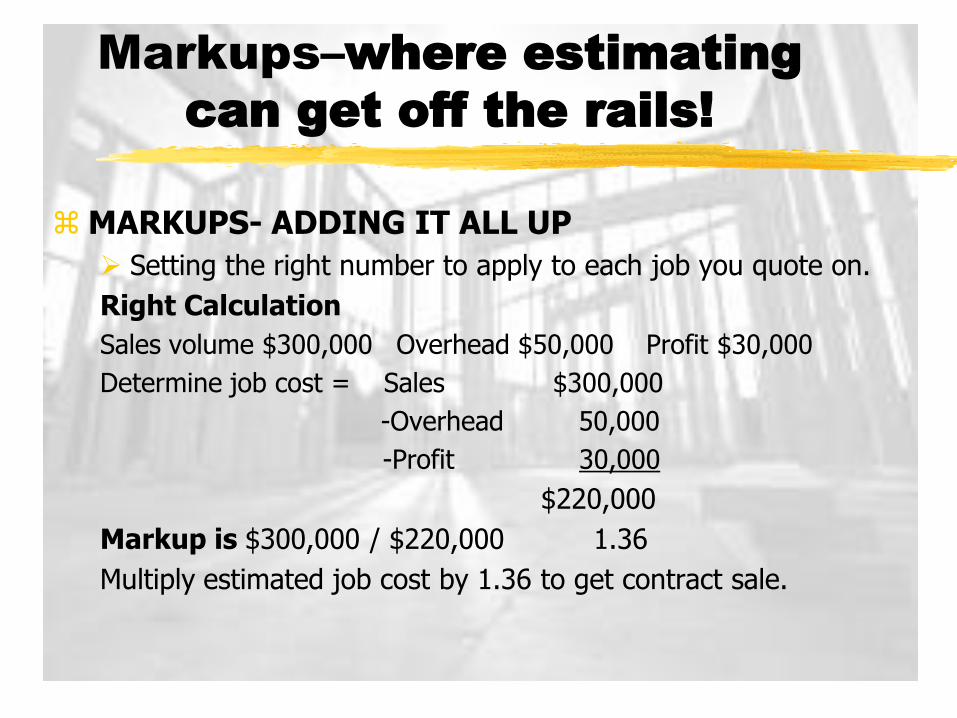

Markups–where estimating

can get off the rails!

MARKUPS- ADDING IT ALL UP

Setting the right number to apply to each job you quote on.

Right Calculation

Sales volume $300,000 Overhead $50,000 Profit $30,000

Determine job cost = Sales $300,000

-Overhead 50,000

-Profit 30,000

$220,000

Markup is $300,000 / $220,000 1.36

Multiply estimated job cost by 1.36 to get contract sale.

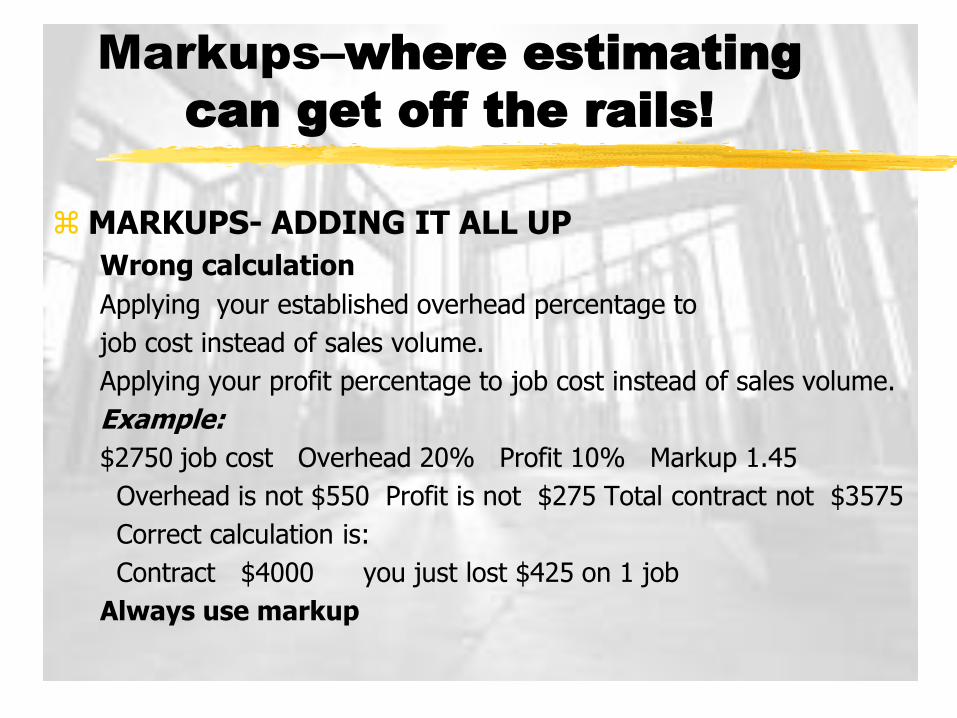

Markups–where estimating

can get off the rails!

MARKUPS- ADDING IT ALL UP

Wrong calculation

Applying your established overhead percentage to

job cost instead of sales volume.

Applying your profit percentage to job cost instead of sales volume.

Example:

$2750 job cost Overhead 20% Profit 10% Markup 1.45

Overhead is not $550 Profit is not $275 Total contract not $3575

Correct calculation is:

Contract $4000 you just lost $425 on 1 job

Always use markup

Markups–where estimating

can get off the rails!

COST PLUS – Yuk!

Usually materials and labour plus a percentage.

Customers don’t understand overhead and profit.

You are exposing your business model.

The customer will not accept a “plus” of 45%.

Stick to a contract price.

Some closing thoughts

Number one issue facing the industry – sleep deprivation.

The odds are against you if you don’t understand overheads, markup and profit.

Businesses fail - they don’t have a handle on each component.

Importance of estimating –

initial estimate to sell the job.

detail required for the contract , budget and a project management anchor.

anchor estimate used as basis to monitor variance.

"as built" costing for use in future estimate preparation.

Some closing thoughts

Add and re add your estimates – you are not a charity!

Allow for contingency provisions to address uncertainty - no one’s “purfick”.

Written contracts -should include a timeframe for validity, escalation provision for longer duration projects, payment terms, assumptions and dependencies and general conditions.

Show me the money – deposits, discounts and prompt payment incentive.

Some closing thoughts

Document your job costs – learn from your mistakes – react quickly.

Share information with each other – there is enough work for all of you!

Next month’s presentation –?????????

Thank you!