1 / 38

BANK OF CHINA LIMITED JOHANNESBURG BRANCH

Pillar 3 Disclosure

December 2019 (Annual)

2 / 38

Table of contents

Regulatory framework for disclosures 4

Pillar 3 disclosures 4

Reporting oversight 5

Overview of risk management and RWA 6

Key Metrics (KM1) 6

Bank risk management approach (OVA) 7

Overview of RWA (OV1) 8

Linkages between financial statements and regulatory exposures 9

Differences between accounting and regulatory scopes of consolidation and mapping of

financial statement categories with regulatory risk categories (LI1) 9

Main sources of differences between regulatory exposure amounts and carrying values in

financial statements (LI2) 10

Explanation of differences between accounting and regulatory exposure amounts (LIA)

Prudential valuation adjustments (PV1) 11

Composition of capital and TLAC 12

Composition of regulatory capital (CC1) 12

Reconciliation of regulatory capital to balance sheet (CC2) 15

Main features of regulatory capital instruments and of other TLAC-eligible instruments

(CCA) 16

Macro-prudential Supervisory Measures 17

Geographical distribution of credit exposures used in the countercyclical capital buffer (CCyB1)

Leverage ratio 18

Summary comparison of accounting assets vs leverage ratio exposure (LR1) 18

Leverage ratio common disclosure template (LR2) 19

Liquidity Risk 20

Liquidity risk management (LIQA) 20

Liquidity Coverage Ratio (LIQ1) 20

Net Stable Funding Ratio (LIQ2) 21

Credit risk 23

General qualitative information about credit risk (CRA) 23

Credit quality of assets (CR1) 23

Changes in stock of defaulted loans and debt securities (CR2) 23

Additional disclosure related to the credit quality of assets (CRB) 23

Qualitative disclosure requirements related to credit risk mitigation techniques (CRC) 28

Credit risk mitigation techniques – overview (CR3) 28

3 / 38

Qualitative disclosures on bank’s use of external credit ratings under the standardized

approach for credit risk (CRD) 28

Standardised approach – credit risk exposure and credit risk mitigation effects (CR4) 29

Standardised approach – exposures by asset classes and risk weights (CR5) 30

Counterparty credit risk 31

Qualitative disclosure related to counterparty credit risk (CCRA) 31

Analysis of counterparty credit risk (CCR) exposure by approach (CCR1) 31

Credit valuation adjustment (CVA) capital charge (CCR2) 32

Standardised approach of CCR exposures by regulatory portfolio and risk weights 32

(CCR3)

Exposures to central counterparties (CCR8) 33

Market Risk

General qualitative disclosure requirements related to market risk (MRA) 34

Market Risk under SA (MR1) 35

Remuneration

Remuneration policy (REMA) 36

Remuneration awarded during the financial year (REM1) 37

Special payments (REM2) 37

Deferred Remuneration (REM3) 38

4 / 38

Regulatory framework for disclosures

Bank of China Limited – Johannesburg Branch (“The Branch”) is supervised by the South

African Reserve Bank, which receives information on the capital adequacy of, and sets capital

requirements for South African banks. The capital requirements is calculated based on the

various regulations relating to financial services, including Basel Capital Accord (Basel) III. The

Basel Committee’s framework is structured around three ‘pillars’: the Pillar 1 minimum capital

requirements and Pillar 2 supervisory review process are complemented by Pillar 3 market

discipline. The aim of Pillar 3 is to produce disclosures that allow market participants to assess

the scope of application by banks of the Basel Committee’s framework and the rules in their

jurisdiction, their capital condition, risk exposures and risk management processes, and hence

their capital adequacy. Pillar 3 requires all material risks to be disclosed, enabling a

comprehensive view of a bank’s risk profile.

Pillar 3 disclosures

The Branch’s Pillar 3 disclosures of 2019 comprise all information required under Pillar 3, both

quantitative and qualitative. Pillar 3 requirements may be met by inclusion in other disclosure

media. Where we adopt this approach, references are provided to the relevant pages of the

Annual Report and Accounts or other location. Any disclosures not relevant to the Branch are

not included or mentioned in this report. The numbers are reported in Rand millions if there are

no specific units in the report.

Financial Position

As at the end of December 2019 the financial position of the Branch was as follows:

Total Assets R46.87 billion

Total Liabilities R38.41 billion

Total Equity R8.46 billion

Total assets increased by 6% compared to that of 31 December 2018. This is a combination

result of business development and regulatory requirements.

Financial Performance

As at the end of December 2019 the Branch reported that operating revenue is line with

expectation and operating expenditure is within the budget set for the 2019 financial year.

International Financial Reporting Standards (IFRS) 16 has been implemented and did not

negatively impact the Branch’s financial performance.

5 / 38

Report oversight

The review of the report has been completed by Branch and the external auditors of the

Branch (Ernst & Young). As at 31 December 2019, the Branch is satisfied of the following:

• Risk, compliance, treasury and capital management generally operated effectively

• Business activities have been managed within the Branch approved risk appetite

• Operation is adequately funded and capitalized to support the execution its strategy.

6 / 38

Overview of risk management and RWA

Table 1: Key Metrics (KM1)

The table provides an overview of a Branch’s key prudential metrics.

On 1 January 2019, the Branch adopted IFRS 16 – Financial Instruments. For more

information on the IFRS 16 transition adjustment, please refer to the Branch’s 2019 annual

financial statement. The Branch adopted IFRS 16 using the modified retrospective approach.

However, the adoption of IFRS16 did not have a significant impact on the key metrics.

The quarter on quarter decrease in the risk weighted assets, increase in capital adequacy ratio

and net stable funding ratio is due to repayment of corporate loans. The decrease in liquidity

coverage ratio is due to the decrease in the loans which resulted in the increase in net cash

outflow during the quarter ended 31 December 2019.

December

2019 ('m)

September

2019 ('m)

June 2019

('m)

March 2019

('m)

December

2018 ('m)

a a a a d

Available capital (amounts)

1 Common Equity Tier 1 (CET1) 7,820 7,827 7,828 7,229 7,198

1a Fully loaded ECL accounting model 7,820 7,827 7,828 7,229 7,198

2 Tier 1 7,820 7,827 7,828 7,229 7,198

2a Fully loaded ECL accounting model Tier 1 7,820 7,827 7,828 7,229 7,198

3 Total capital 8,105 8,056 8,242 7,582 7,529

3a Fully loaded ECL accounting model total capital 8,105 8,056 8,242 7,582 7,529

Risk-weighted assets (amounts)

4 Total risk-weighted assets (RWA) 34,100 37,015 35,469 30,854 28,528

Risk-based capital ratios as a percentage of RWA

5 Common Equity Tier 1 ratio (%) 22.93 21.15 22.07 23.43 25.23

5a Fully loaded ECL accounting model Common Equity Tier 1 (%) 22.93 21.15 22.07 23.43 25.23

6 Tier 1 ratio (%) 22.93 21.15 22.07 23.43 25.23

6a Fully loaded ECL accounting model Tier 1 ratio (%) 22.93 21.15 22.07 23.43 25.23

7 Total capital ratio (%) 23.77 21.76 23.24 24.57 26.39

7a Fully loaded ECL accounting model total capital ratio (%) 23.77 21.76 23.24 24.57 26.39

Additional CET1 buffer requirements as a percentage of RWA

8 Capital conservation buffer requirement (2.5% from 2019) (%) 2.50 2.50 2.50 2.50 1.88

9 Countercyclical buffer requirement (%) 0.52 0.61 0.61 0.27 0.55

10 Bank G-SIB and/or D-SIB additional requirements (%) N/A N/A N/A N/A N/A

11Total of bank CET1 specific buffer requirements (%) (row 8 + row 9 + row

10)3.02 3.11 3.11 2.77 2.43

12 CET1 available after meeting the bank’s minimum capital requirements (%) 14.91 13.04 13.96 15.66 16.93

Basel III leverage ratio

13 Total Basel III leverage ratio exposure measure 49,984 54,950 50,947 50,788 47,010

14 Basel III leverage ratio (%) (row 2 / row 13) 15.64 14.24 15.36 14.23 15.31

14aFully loaded ECL accounting model Basel III leverage ratio (%) (row 2a /

row13)15.64 14.24 15.36 14.23 15.31

Liquidity Coverage Ratio

15 Total HQLA 11,314 10,760 9,139 7,790 7,275

16 Total net cash outflow 4,974 4,219 1,859 1,501 2,205

17 LCR ratio (%) 227 255 492 519 330

Net Stable Funding Ratio

18 Total available stable funding 26,798 27,023 26,971 26,583 27,397

19 Total required stable funding 23,283 26,474 25,934 24,605 23,919

20 NSFR ratio (%) 115 102 104 108 115

7 / 38

Overview of risk management and RWA

Bank Risk Management Approach (OVA)

The Branch’s major risks, namely credit risk, market risk and operational risk are well

managed and controlled through the branch’s internal policies and procedures. With regards to

Credit and Market Risk (relating to the banking book), the Branch has adopted the

Standardised Approach for Credit and Market risks whilst the Basic Indicator Approach was

selected for Operational Risk.

Liquidity Risk:

The Branch formulated three liquidity risk policies that including Liquidity Risk Management

Policy, Liquidity Risk Contingency Plan and Implementation Rules for Liquidity Risk Stress

Test; optimised the policies and forecast process of LCR and NSFR, updated the assumptions

of Contractual mismatch, Business mismatch and bank - specific stress mismatch according to

regulatory requirement, which give us much more confidence in managing liquidity risk.

Interest Rate Risk:

Our assets and liabilities are reasonably matched as per stress testing mode and the interest

rate risk in the banking book is monitored and controlled through interest rate risk indicators

periodically.

Foreign Exchange Control Risk:

The Branch ensures that its net open position is maintained within the prescribed regulatory

limit.

8 / 38

Overview of risk management and RWA (Continued)

Table 2: Overview of RWA (OV1)

The table provides an overview of total RWA forming the denominator of the risk-based capital

requirements. The current minimum capital requirement to the RWA is 12.02% which is made

up of 8% base minimum, 1% systemic risk add-on, 2.5% conservation buffer and 0.52%

countercyclical buffer (refer to table 9)

The Quarter-on-Quarter movement on the RWA is mainly due to a decrease in the lending of

about R2.5 billion. Most of the movement was attributable to loan repayments.

a b c

Dec-19 Sep-19 T

1 31,773 34,890 3,850

2 31,773 34,890 3,850

3 - - -

4 - - -

5 - - -

6 98 64 12

7 98 64 12

8 - - -

9 - - -

10 70 45 -

11 - -

12 - - -

13 - - -

14 - - -

15 - - -

16 - - -

17 - - -

18 - - -

19 - - -

20 15 9 2

21 15 9 2

22 - - -

23 - - -

24 1,956 1,825 235

25 258 227 -

26 - -

27 34,170 37,060 4,099

Of which: foundation internal ratings-based (F-IRB) approach

RWAMinimum capital

requirements

Credit risk (excluding counterparty credit risk)

Of which: standardised approach (SA)

Settlement risk

Of which: supervisory slotting approach

Of which: advanced internal ratings-based (A-IRB) approach

Counterparty credit risk (CCR)

Of which: standardised approach for counterparty credit risk

Of which: Internal Model Method (IMM)

Of which: other CCR

Credit valuation adjustment (CVA)

Equity positions under the simple risk weight approach

Equity investments in funds - look-through approach

Equity investments in funds - mandate-based approach

Equity investments in funds - fall-back approach

Total (1 + 6 + 10 + 11 + 12 + 13 + 14 + 15 + 16 + 20 + 23 + 24 +

25 + 26)

Securitisation exposures in banking book

Of which: securitisation internal ratings-based approach (SEC-

Of which: securitisation external rating-based approah (SEC-

Of which: securitisation standardised approach (SEC-SA)

Market risk

Of which: standardised approach (SA)

Of which: internal model approaches (IMA)

Capital charge for switch between trading book and banking book

Operational risk

Amounts below the thresholds for deduction (subject to 250%

risk weight)

Floor adjustment

9 / 38

Linkages between financial statements and regulatory

exposures

The Pillar 3 Disclosures at 31 December 2019 are prepared in accordance with regulatory

capital adequacy concept and rules while the annual financial statements are prepared in

accordance with IFRS. The regulatory exposure classes include an estimation of risk and are

expressed as the amount expected to be outstanding if and when the counterparty defaults.

Moreover, regulatory exposure classes are based on different criteria from accounting asset

types and are therefore not comparable on a line by line basis.

Table 3 shows the difference between the accounting and regulatory scope and a breakdown

of the accounting balances into the risk types that form the basis for regulatory capital

requirements. Table 3 then shows the main differences between the accounting balances and

regulatory exposures by regulatory risk type.

Table 3: Differences between accounting and regulatory scopes of consolidation

and mapping of financial statement categories with regulatory risk categories (LI1)

The loans and advances are usually subjected to more than one category of risk framework.

The gross carrying amount is subjected to the credit risk framework while the net amount of

the loans is subjected to the market risk framework. All liabilities denominated in foreign

currency are subjected to the Market risk framework while liabilities denominated in ZAR are

not subjected to any capital requirements.

a b c d e f g

Carrying values as

reported in published

financial statements

Carrying values

under scope of

regulatory

consolidation

Subject to credit

risk framework

Subject to

counterparty

credit

risk framework

Subject to the

securitisation

framework

Subject to the

market risk

framework

Not subject to

capital

requirements or

subject to

deduction from

capital

Assets

Cash and cash Equivalents 2,796 - - - - - -

Cash and balances at central banks - 821 821 - - - -

Property and equipment 24 24 24 - - - -

Intangible Assets - - - - - - -

Derivative financial instruments 79 79 79 79 - 4

Deferred tax income assets 104 103 103 - - - -

Loans and advances to banks 9,137 11,933 11,933 - - 9,137 -

Loans and advances to customers 22,751 22,751 22,751 - - 15,538 -

Current income tax assets 6 6 - - - - 6

Available for sale financial investments 11,147 11,147 11,147 - - - -

Other Assets 824 3 3 - - - -

Total assets 46,868 46,868 46,862 79 - 24,678 6

Liabilities

Deposits from customers 16,941 16,941 - - - 1,292 15,649

Deposits from banks 17,727 17,727 - - - 17,382 345

Derivative financial instruments 7 7 - 7 - 2 -

Provisions 77 77 - - - 45 32

Commercial Paper 3,500 3,500 - - - 3,047 453

Other liabilities 161 161 - - - 120 41

Total liabilities 38,414 38,413 - 7 - 21,888 16,520

10 / 38

Linkages between financial statements and regulatory

exposures (Continued)

Table 4: Main sources of differences between regulatory exposure amounts and

carrying values in financial statements (LI2)

Explanation of differences between accounting and regulatory exposure amounts

(LIA)

Off balance sheet amounts

Off-balance sheet amounts subject to credit risk regulatory framework include undrawn

portions of committed facilities, various trade finance commitments and guarantees. We apply

a credit conversion factor to these items.

Valuation techniques

The Branch has performs the valuation based on the unadjusted quoted prices for identical

assets or liabilities in active markets where the quoted price is readily available and the price

represents actual and regularly occurring market transactions on an arm’s length basis.

Valuation adjustments

The revaluation is performed on a daily basis and is automatically run by the Bank of China

valuation system (which originated from Head Office).

Expected credit losses

The carrying value of assets is net of credit risk adjustments. The regulatory exposure value is

the amount before deducting the credit risk adjustments.

a b c d e

Credit risk

framework

Securitisation

framework

Counterparty

credit risk

framework Market risk

1 Asset carrying value amount under scope of regulatory consolidation (as per template LI1) 46,868 46,862 - 79 24,678

2 Liabilities carrying value amount under regulatory scope of consolidation (as per template LI1) 38,413 - - 7 21,888

3 Total net amount under regulatory scope of consolidation 8,455 46,862 - 72 2,790

4 Off-balance sheet amounts 7,145 7,145 - - -

5 Differences in valuations 596 577 - 18 -

6 Differences due to different netting rules, other than those already included in row 2 - - - - -

7 Differences due to consideration of provisions -797 -797 - - -

8 Differences due to prudential filters - - - - -

10 Exposure amounts considered for regulatory purposes 15,398 53,787 - 90 2,790

Total

Items subject to:

11 / 38

Linkages between financial statements and regulatory

exposures (Continued)

Table 5: Prudent valuation adjustments (PV1)

The Branch mainly has derivatives which are subject to the prudent valuation adjustment

framework. The values based on the figures shown in the table are insignificant.

a b c d e f g h

Equity Interest rates FX Credit Commodities TotalOf which: In the

trading book

Of which: In the

banking book

1 Closeout uncertainty, of which:

2 Mid-market value

3 Closeout cost

4 Concentration

5 Early termination

6 Model risk

7 Operational risk

8 Investing and funding costs

9 Unearned credit spreads

10 Future administrative costs

11 Other 0.1 0.1

12 Total adjustment 0.1 0.1

12 / 38

Composition of Capital

In terms of the requirements of the Banks Act and the Regulations, the Branch has met the

minimum capital requirements for periods under review.

The minimum capital requirements are defined by the following capital adequacy ratio namely:

Common Equity Tier 1 capital as a percentage of risk-weighted assets;

Tier 1 capital as a percentage of risk-weighted assets; and

Total qualifying capital as a percentage of risk-weighted assets.

The Branch assesses the capital adequacy by considering the resources necessary to cover

unexpected losses arising from risks, being those which it chooses to accept (such as credit

and market risk), and risks which may arise in the operations environment. The capital

management framework and related policies of the Branch are defined in the Internal Capital

Adequacy Assessment Process (ICAAP).

This ensures that the Branch’s level of capital:

Remains sufficient to support the Branch’s risk profile and outstanding commitments;

Exceeds the Branch’s minimum regulatory capital requirements by an appropriate buffer;

Is capable of withstanding a severe economic downturn stress scenario; and

Remains consistent with the Branch’s strategic and operational goals and BOC Group’s

expectations.

As at 31 December 2019 the Branch reported a capital adequacy ratio of 23.77%. The change

in capital adequacy is mainly as a result of credit risk which constitutes approximately 93% of

total risk exposure. There have been no significant capital movements since the R2.5 billion

capital injection which occurred in December 2018.

Table 6: Composition of regulatory capital (CC1)

.

a b

Amounts

Source based on reference

numbers/letters of the

balance sheet under the

regulatory scope of

consolidation

Common Equity Tier 1 capital: instruments and reserves

1Directly issued qualifying common share (and equivalent for non-joint stock

companies) capital plus related stock surplus 5,800 1

2 Retained earnings 1,930

3 Accumulated other comprehensive income (and other reserves) 90 2

4Directly issued capital subject to phase-out from CET1 (only applicable to non-joint

stock companies)

5Common share capital issued by subsidiaries and held by third parties (amount

allowed in group CET1)

6 Common Equity Tier 1 capital before regulatory adjustments 7,820

13 / 38

Composition of Capital (Continued)

7 Prudent valuation adjustments 0

8 Goodwill (net of related tax liability) (a) minus (d)

9 Other intangibles other than mortgage servicing rights (net of related tax liability) (b) minus (e)

28 Total regulatory adjustments to Common Equity Tier 1 0

29 Common Equity Tier 1 capital (CET1) 7,819

Additional Tier 1 capital: instruments

30 Directly issued qualifying additional Tier 1 instruments plus related stock surplus (i)

31 Of which: classified as equity under applicable accounting standards

32 Of which: classified as liabilities under applicable accounting standards

33 Directly issued capital instruments subject to phase-out from additional Tier 1

Additional Tier 1 capital: instruments

34 Directly issued qualifying additional Tier 1 instruments plus related stock surplus

35 Of which: classified as equity under applicable accounting standards

36 Additional Tier 1 capital before regulatory adjustments -

Additional Tier 1 capital: regulatory adjustments

37 Investments in own additional Tier 1 instruments

38 Reciprocal cross-holdings in additional Tier 1 instruments

39

Investments in the capital of banking, financial and insurance entities that are outside

the scope of regulatory consolidation, where the bank does not own more than 10%

of the issued common share capital of the entity (amount above 10% threshold)

40Significant investments in the capital of banking, financial and insurance entities that

are outside the scope of regulatory consolidation

41 National specific regulatory adjustments

42Regulatory adjustments applied to additional Tier 1 due to insufficient Tier 2 to cover

deductions

43 Total regulatory adjustments to additional Tier 1 capital -

44 Additional Tier 1 capital (AT1) -

45 Tier 1 capital (T1 = CET1 + AT1) 7,819

Tier 2 capital: instruments and provisions

46 Directly issued qualifying Tier 2 instruments plus related stock surplus

47 Directly issued capital instruments subject to phase-out from Tier 2

48Tier 2 instruments (and CET1 and AT1 instruments not included in rows 5 or 34)

issued by subsidiaries and held by third parties (amount allowed in group Tier 2)

49 Of which: instruments issued by subsidiaries subject to phase-out

50 Provisions 285

51 Tier 2 capital before regulatory adjustments 285

Tier 2 capital: regulatory adjustments

52 Investments in own Tier 2 instruments

53 Reciprocal cross-holdings in Tier 2 instruments and other TLAC liabilities

54

Investments in the capital and other TLAC liabilities of banking, financial and

insurance entities that are outside the scope of regulatory consolidation, where the

bank does not own more than 10% of the issued common share capital of the entity

(amount above 10% threshold)

54a

Investments in the other TLAC liabilities of banking, financial and insurance entities

that are outside the scope of regulatory consolidation and where the bank does not

own more than 10% of the issued common share capital of the entity: amount

previously designated for the 5% threshold but that no longer meets the conditions

(for G-SIBs only)

55

Significant investments in the capital and other TLAC liabilities of banking, financial

and insurance entities that are outside the scope of regulatory consolidation (net of

eligible short positions)

56 National specific regulatory adjustments

57 Total regulatory adjustments to Tier 2 capital -

58 Tier 2 capital (T2) 285

59 Total regulatory capital (TC = T1 + T2) 8,105

60 Total risk-weighted assets 34,100

Capital ratios and buffers

61 Common Equity Tier 1 (as a percentage of risk-weighted assets) 22.9309

62 Tier 1 (as a percentage of risk-weighted assets) 22.9309

63 Total capital (as a percentage of risk-weighted assets) 23.7676

64

Institution-specific buffer requirement (capital conservation buffer plus

countercyclical buffer requirements plus higher loss absorbency requirement,

expressed as a percentage of risk-weighted assets) 3.0164

65 Of which: capital conservation buffer requirement 2.5000

66 Of which: bank-specific countercyclical buffer requirement 0.5164

67 Of which: higher loss absorbency requirement N/A

68Common Equity Tier 1 (as a percentage of risk-weighted assets) available

after meeting the bank’s minimum capital requirements 14.9145

National Minima (if different from Basel III)

69 National Common Equity Tier 1 minimum ratio (if different from Basel III minimum)

70 National Tier 1 minimum ratio (if different from Basel III minimum)

71 National total capital minimum ratio (if different from Basel III minimum)

Amounts below the thresholds for deduction (before risk weighting)

14 / 38

Composition of Capital (Continued)

72Non-significant investments in the capital and other TLAC liabilities of other financial

entities

73 Significant investments in the common stock of financial entities

74 Mortgage servicing rights (net of related tax liability)

75 Deferred tax assets arising from temporary differences (net of related tax liability) 103 3

Applicable caps on the inclusion of provisions in Tier 2

76Provisions eligible for inclusion in Tier 2 in respect of exposures subject to

standardised approach (prior to application of cap) 285

77 Cap on inclusion of provisions in Tier 2 under standardised approach 397

78Provisions eligible for inclusion in Tier 2 in respect of exposures subject to internal

ratings-based approach (prior to application of cap)

79 Cap for inclusion of provisions in Tier 2 under internal ratings-based approach

Capital instruments subject to phase-out arrangements (only applicable

between 1 Jan 2018 and 1 Jan 2022)

80 Current cap on CET1 instruments subject to phase-out arrangements

81Amount excluded from CET1 due to cap (excess over cap after redemptions and

maturities)

82 Current cap on AT1 instruments subject to phase-out arrangements

83Amount excluded from AT1 due to cap (excess over cap after redemptions and

maturities)

84 Current cap on T2 instruments subject to phase-out arrangements

85Amount excluded from T2 due to cap (excess over cap after redemptions and

maturities)

15 / 38

Composition of Capital (Continued)

Table 7: Reconciliation of regulatory capital to balance sheet (CC2)

1. The BA return does not have a separate line for cash and cash equivalent and the amount

is added to loans and advances to banks.

2. The cash and balances at central bank is added to other assets in the financial statements

The IFRS16 was implemented on 1 January 2020 and this resulted in an increase in property,

plant and equipment for the building leases that was previously expensed.

a b c

Balance sheet as

in published

financial

statements

Under regulatory

scope of

consolidation Reference

As at period-end As at period-end

Assets

Cash and cash Equivalents 2,796

Cash and balances at central banks 821

Property and equipment 24 24

Intangible Assets - -

Derivative financial instruments 79 79

Deferred tax income assets 104 103

Loans and advances to banks 9,137 11,933

Loans and advances to customers 22,751 22,751

Current income tax assets 6 6

Available for sale financial investments 11,147 11,147

Other Assets 824 3

Total assets 46,868 46,868

Liabilities

Deposits from customers 16,941 16,941

Deposits from banks 17,727 17,727

Derivative financial instruments 7 7

Provisions 77 77

Commercial Paper 3,500 3,500

Other liabilities 161 161

Total liabilities 38,413 38,413

Equity

Branch capital 5,800 5,800 1

Retained earnings 2,565 2,565

Fair value reserves 90 90 2

Total shareholders' equity 8,455 8,455

16 / 38

Composition of Capital (Continued)

Table 8: Main features of regulatory capital instruments (CCA) and of other

TLAC-eligible instruments

a

Quantitative /

qualitative information

1 Issuer Bank of China Limited

2Unique identifier (eg CUSIP, ISIN or Bloomberg identifier for private

placement) None

3 Governing law(s) of the instrument South Africa

3a

Means by which enforceability requirement of Section 13 of the TLAC

Term Sheet is achieved (for other TLAC-eligible instruments governed

by foreign law) N/A

4 Transitional Basel III rules CET1

5 Post-transitional Basel III rules CET1

6 Eligible at solo/group/group and solo Solo

7 Instrument type (types to be specified by each jurisdiction) CET1

8Amount recognised in regulatory capital (currency in millions, as of

most recent reporting date) 5,800

9 Par value of instrument 5,800

10 Accounting classification IFRS: Equity

11 Original date of issuance 2000

12 Perpetual or dated Perpetual

13 Original maturity date No maturity

14 Issuer call subject to prior supervisory approval N/A

15 Optional call date, contingent call dates and redemption amount N/A

16 Subsequent call dates, if applicable N/A

Coupon/dividends

17 Fixed or floating dividend/coupon N/A

18 Coupon rate and any related index N/A

19 Existence of a dividend stopper N/A

20 Fully discretionary, partially discretionary or mandatory N/A

21 Existence of step-up or other incentive to redeem N/A

22 Non-cumulative or cumulative N/A

23 Convertible or non-convertible N/A

24 If convertible, conversion trigger(s) N/A

25 If convertible, fully or partially N/A

26 If convertible, conversion rate N/A

27 If convertible, mandatory or optional conversion N/A

28 If convertible, specify instrument type convertible into N/A

29 If convertible, specify issuer of instrument it converts into N/A

30 Writedown feature N/A

31 If writedown, writedown trigger(s) N/A

32 If writedown, full or partial N/A

33 If writedown, permanent or temporary N/A

34 If temporary write-own, description of writeup mechanism N/A

34a Type of subordination N/A

35

Position in subordination hierarchy in liquidation (specify instrument

type immediately senior to instrument in the insolvency creditor

hierarchy of the legal entity concerned). N/A

36 Non-compliant transitioned features N/A

37 If yes, specify non-compliant features N/A

17 / 38

Macro prudential Supervisory Measures

The proportion of capital held for CCyB requirements in geographies other than South Africa

are shown in the table below.

Table 9: Geographical distribution of credit exposures used in the countercyclical

capital buffer (CCyB1)

The countercyclical capital buffer rate has been calculated for BCBS jurisdictions which the

Branch have private sector credit exposure and applied it to RWA consistent with it being an

extension of the capital conservation buffer. The countercyclical buffer amount has been

added to total RWA. The Countercyclical Capital buffer rate was obtained from the BCBS

website. The change from the previous reporting period was that the Countercyclical Capital

buffer rate had changed for Hong Kong from 2.5% to 2% and the Branch no longer had

exposures relating to Sweden (loan repayment). The Countercyclical Capital buffer rate for the

United Kingdom remained unchanged.

a b c d e

Geographical breakdown

Countercyclical

capital buffer

rate

Exposure valuesRisk weighted

Assets

Hong Kong 2.00% 5,224 5,224

United Kingdom 1.00% 1,197 1,057

Sum 6,421 6,281

Total 53,956 31,775 0.5164 176

Exposure values and/or risk-weighted

assets used in the computation of the

countercyclical capital buffer

Bank-specific

countercyclical

capital buffer rate

Countercyclical

buffer amount

18 / 38

Leverage Ratio

The leverage ratio calculated in accordance with South African Banks Act, 1990 was 15.64%

at 31 December 2019, up from 14.24% at 30 September 2019. The movement was mainly due

to the decrease on the on-balance exposures of R3.7 billion (which consists of corporate loans

and bank loans) and off-balance sheet exposures of R1.3 billion (which consists of

commitments and guarantees). The exposures that have been disclosed are balances as at

each Quarter-end.

Table 10: Summary comparison of accounting assets vs leverage ratio exposure

(LR1)

The table below shows the reconciliation of the total assets in the financial statements to the

leverage ratio exposure measure.

Item R'm

1 Total consolidated assets as per published financial statements 46,868

2

Adjustment for investments in banking, financial, insurance or

commercial entities that are consolidated for accounting purposes but

outside the scope of regulatory consolidation

-

3

Adjustment for fiduciary assets recognised on the balance sheet

pursuant to the operative accounting framework but excluded from the

leverage ratio exposure measure

-

4 Adjustments for derivative financial instruments 90

5Adjustment for securities financing transactions (ie repos and similar

secured lending)

-

6Adjustment for off-balance sheet items (ie conversion to credit equivalent

amounts of off- balance sheet exposures) 3,025

7 Other adjustments -

8 Leverage ratio exposure 49,984

19 / 38

Leverage Ratio (Continued)

Table 11: Leverage ratio common disclosure template (LR2)

The table below provides a detailed breakdown of the components of the leverage ratio.

Item T T-1

Dec 2019 ('m) Sep 2019 ('m)

1On-balance sheet items (excluding derivatives and SFTs, but including

collateral)

46,789 50,533

2 (Asset amounts deducted in determining Basel III Tier 1 capital) - -0

3 Total on-balance sheet exposures (excluding derivatives and 46,789 50,533

Other risk Other risk

4Replacement cost associated with all derivatives transactions (ie

net of eligible cash variation margin)

79 3

5 Add-on amounts for PFE associated with all derivatives transactions 90 124

6Gross-up for derivatives collateral provided where deducted from the

balance sheet assets pursuant to the operative accounting framework

7(Deductions of receivables assets for cash variation margin

provided in derivatives transactions)

8 (Exempted CCP leg of client-cleared trade exposures)

9 Adjusted effective notional amount of written credit derivatives

10(Adjusted effective notional offsets and add-on deductions for written

credit derivatives)

11 Total derivative exposures (sum of lines 4 to 10) 170 127

12Gross SFT assets (with no recognition of netting), after adjusting for

sales accounting transactions

13(Netted amounts of cash payables and cash receivables of gross SFT

assets)

14 CCR exposure for SFT assets

15 Agent transaction exposures

16Total securities financing transaction exposures (sum of lines 12

to 15)

- -

17 Off-balance sheet exposure at gross notional amount 3,025 4,290

18 (Adjustments for conversion to credit equivalent amounts) - -

19 Off-balance sheet items (sum of lines 17 and 18) 3,025 4,290

20 Tier 1 capital 7,820 7,827

21 Total exposures (sum of lines 3, 11, 16 and 19) 49,984 54,950

22 Basel III leverage ratio 15.64% 14.24%

Securities financing transaction exposures

Other off-balance sheet exposures

Capital and total exposures

Leverage ratio

On-balance sheet exposures

Derivative exposures

20 / 38

Liquidity Risk

Liquidity risk is the risk that the Branch does not have sufficient financial resources to meet its

obligations as they fall due, or will have to access such resources at excessive cost. This

includes repaying depositors or maturing wholesale debt. The risk arises from mismatches in

the timing of cash flows. The Branch follows the group liquidity framework.

The objective of the Group’s internal liquidity and funding risk management framework is to

allow it to withstand very severe liquidity stresses and be adaptable to changing business

models, markets and regulations.

Liquidity Risk Management (LIQA)

The Branch has an internal liquidity and funding risk management framework which aims to

allow it to withstand severe liquidity stresses. It is designed to be adaptable to changing

business models, economic environment and regulations.

We maintain a funding structure of stable customer deposits and long term wholesale funding

well in excess of liquid assets requirements. We strive to diversify the funding base avoiding

undue concentration by investor type, maturity, market source, instrument and currency to

ensure a varied funding mix to support loan growth. We remain confident in our ability to rise

funding appropriate to our needs.

Table 12: Liquidity Coverage Ratio (LIQ1)

LCR promotes short-term resilience of the Branch’s 30 calendar day liquidity risk profile by

ensuring it has sufficient HQLA to meet potential outflows in a stressed environment. The

simple average for working days is used in the table are data from 1 October 2019 to 31

December 2019. Un-weighted value represents the outstanding balances maturing or callable

within 30 days for cash inflows and cash outflows. Total weighted value is calculated after

application of weightings of cash inflows and outflows.

The key main drivers which normally impact the movement of the LCR is the deposits (cash

outflows), loans and advances (cash inflows) and Government Bonds and Treasury Bills (High

Quality Liquid assets). The Branch is reliant on the Group for USD borrowing funds and issued

aa CNY 1.5 billion Rainbow Bond in 2017. All HQLA is in ZAR.

The following factors would cause the movements in the LCR

- Deposits and loans are nearing maturity which means that some loans and deposits

would move to within 30 days and would impact on the net cash outflow/inflow.

- The maturity or the purchase of Treasury Bills which would affect the movement of the

High Quality Liquidity Assets.

21 / 38

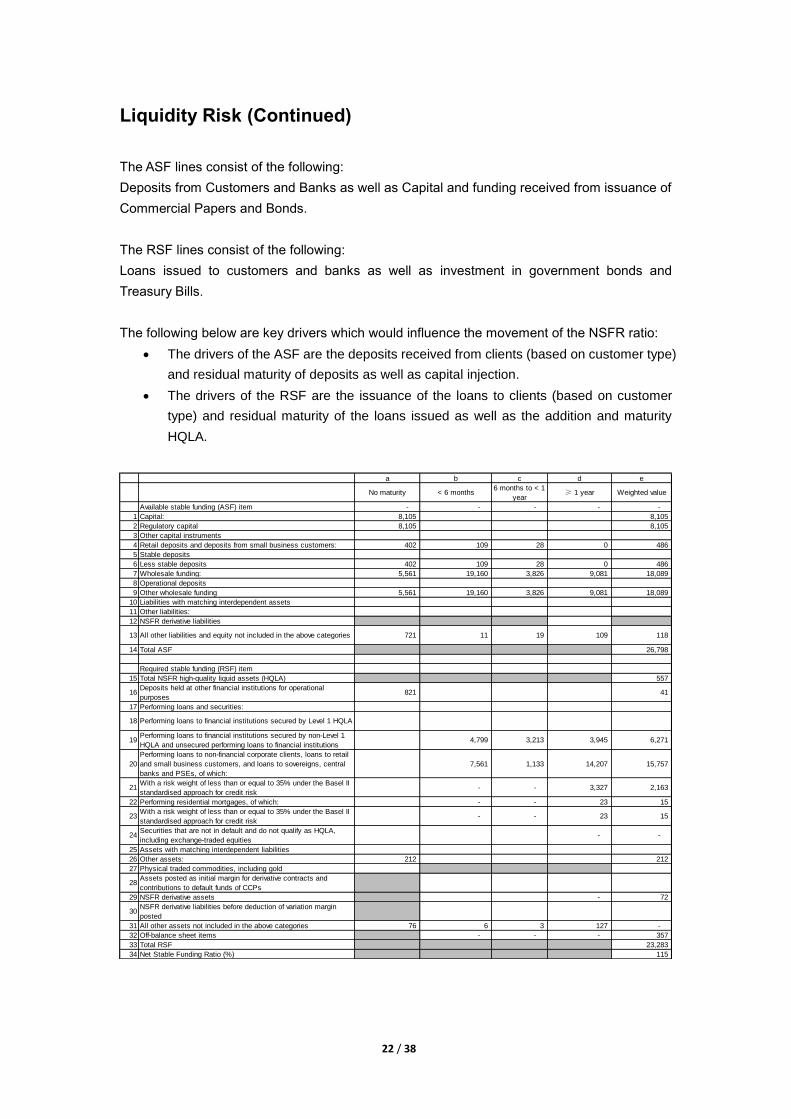

Liquidity Risk (Continued)

Table 13: Net Stable Funding Ratio (LIQ2)

The Branch has been subjected to the Basel III NSFR standards from 1 January 2018,

pursuant to the Banks Act D8/2017 with the objective to promote funding stability and

resilience in the banking sector by requiring banks to maintain a stable funding profile in

relation to the composition of its assets and off-balance sheet activities.

On 30 September 2019 NSFR ratio was 102%, as at 31 December 2019 NSFR ratio was

115%. Compared to Quarter 3 of 2019, the NSFR movement was caused by a significant

decrease on the RSF. This was mainly caused by decrease in the performing loans as well as

maturity of the Treasury Bills.

The Branch maintains and ensures that its NSFR remains above the specified regulatory

minimum requirements. The Branch maintained NSFR compliance in excess of the 100%

regulatory requirement and operates above risk appetite and management internal buffer

requirements.

Total unweighted valueTotal weighted value

(average) (average)

1 Total HQLA 11,314

2Retail deposits and deposits from small business customers, of

which:288 20

3 Stable deposits -

4 Less stable deposits 201 20

5 Unsecured wholesale funding, of which: 36,744 7,228

6Operational deposits (all counterparties) and deposits in networks of

cooperative banks-

7 Non-operational deposits (all counterparties) 12,568 7,228

8 Unsecured debt

9 Secured wholesale funding

10 Additional requirements, of which: 503 228

11Outflows related to derivative exposures and other collateral

requirements32 32

12 Outflows related to loss of funding on debt products -

13 Credit and liquidity facilities 303 28

14 Other contractual funding obligations 168 168

15 Other contingent funding obligations

16 TOTAL CASH OUTFLOWS 7,477

17 Secured lending (eg reverse repos) - -

18 Inflows from fully performing exposures 3,037 2,430

19 Other cash inflows 72 72

20 TOTAL CASH INFLOWS 2,502

21 Total HQLA 11,314

22 Total net cash outflows 4,974

23 Liquidity Coverage Ratio (%) 227

High-quality liquid assets

Cash outflows

Cash inflows

Total adjusted value

22 / 38

Liquidity Risk (Continued)

The ASF lines consist of the following:

Deposits from Customers and Banks as well as Capital and funding received from issuance of

Commercial Papers and Bonds.

The RSF lines consist of the following:

Loans issued to customers and banks as well as investment in government bonds and

Treasury Bills.

The following below are key drivers which would influence the movement of the NSFR ratio:

The drivers of the ASF are the deposits received from clients (based on customer type)

and residual maturity of deposits as well as capital injection.

The drivers of the RSF are the issuance of the loans to clients (based on customer

type) and residual maturity of the loans issued as well as the addition and maturity

HQLA.

a b c d e

No maturity < 6 months6 months to < 1

year≥ 1 year Weighted value

Available stable funding (ASF) item - - - - -

1 Capital: 8,105 8,105

2 Regulatory capital 8,105 8,105

3 Other capital instruments

4 Retail deposits and deposits from small business customers: 402 109 28 0 486

5 Stable deposits

6 Less stable deposits 402 109 28 0 486

7 Wholesale funding: 5,561 19,160 3,826 9,081 18,089

8 Operational deposits

9 Other wholesale funding 5,561 19,160 3,826 9,081 18,089

10 Liabilities with matching interdependent assets

11 Other liabilities:

12 NSFR derivative liabilities

13 All other liabilities and equity not included in the above categories 721 11 19 109 118

14 Total ASF 26,798

Required stable funding (RSF) item

15 Total NSFR high-quality liquid assets (HQLA) 557

16Deposits held at other financial institutions for operational

purposes821 41

17 Performing loans and securities:

18 Performing loans to financial institutions secured by Level 1 HQLA

19Performing loans to financial institutions secured by non-Level 1

HQLA and unsecured performing loans to financial institutions4,799 3,213 3,945 6,271

20

Performing loans to non-financial corporate clients, loans to retail

and small business customers, and loans to sovereigns, central

banks and PSEs, of which:

7,561 1,133 14,207 15,757

21With a risk weight of less than or equal to 35% under the Basel II

standardised approach for credit risk- - 3,327 2,163

22 Performing residential mortgages, of which: - - 23 15

23With a risk weight of less than or equal to 35% under the Basel II

standardised approach for credit risk- - 23 15

24Securities that are not in default and do not qualify as HQLA,

including exchange-traded equities- -

25 Assets with matching interdependent liabilities

26 Other assets: 212 212

27 Physical traded commodities, including gold

28Assets posted as initial margin for derivative contracts and

contributions to default funds of CCPs

29 NSFR derivative assets - 72

30NSFR derivative liabilities before deduction of variation margin

posted

31 All other assets not included in the above categories 76 6 3 127 -

32 Off-balance sheet items - - - 357

33 Total RSF 23,283

34 Net Stable Funding Ratio (%) 115

23 / 38

Credit Risk

General information about credit risk (CRA):

Credit Risk Management is defined as the risk that parties with whom the Branch has

contracted fail to meet their obligations (both on and off-balance sheet). Credit risk appetite is

monitored and reported on a monthly basis through a suite of risk metrics derived from credit

portfolio performance measures.

Table 14: General qualitative information about credit risk (CR1)

The following table provides a breakdown of the credit quality of on and off balance sheet

assets (gross and net of impairments) and reconciles to the amounts reported in the annual

financial statements.

The Branch applies a consistent definition to default for regulatory and accounting purposes.

Refer to CRB for the Branch’s default definition.

Table 15: Changes in stock of defaulted loans and debt securities (CR2)

The table below depicts the changes in the Branch’s stock of defaulted exposures, the flows

between non-defaulted and defaulted exposure categories and reductions in the stock of

defaulted exposures due to write-offs. In the last quarter of 2019, the Branch has written off

two non-performing loans. There are only two remaining default loans.

Additional disclosure related to the credit quality of assets (CRB):

The Branch applies International Financial Reporting Standard 9 for impairments. The

impairments for the Branch are determined by qualitative, quantitative and Backstop methods.

The measurement of the impairment is the Expected Credit Loss Model (“ECL”). Details

information is disclosed as below:

a b c d

Defaulted exposuresNon-defaulted

exposures

1 Loans 587 34,886 -783 34,690

2 Debt Securities - 11,147 -17 11,130

3 Off-balance sheet exposures 29 7,115 -14 7,131

4 Total 617 53,149 -815 52,951

Gross carrying values ofAllowances/

impairments

Net values

(a+b+c)

a

1 Defaulted loans and debt securities at end of the previous reporting period 859

2 Loans and debt securities that have defaulted since the last reporting period

3 Returned to non-defaulted status

4 Amounts written off 242

5 Other changes -1

6Defaulted loans and debt securities at end of the reporting period (1+2-3-4+-

5)617

24 / 38

Credit Risk (Continued)

1. Measurement of the ECL:

In accordance with IFRS-9 requirements, based on the change in credit quality since the initial

recognition of the financial instruments, ECL under different periods of time should be

recognized, and the new standard outlines a “three-stage” model to calculate the ECL as

follows:

(1) Stage 1: The financial instruments without significant increases in credit risk after initial

recognition apply the Stage I Model of the ECL to calculate its impairment allowance at an

amount equivalent to the ECL of the financial instrument for the next 12 months;

(2) Stage II: Financial instruments that have had a significant increase in credit risk since

initial recognition but have no objective evidence of impairment apply the Stage II Model of

the ECL, with their impairment provision measured at an amount equivalent to the ECL

over the lifetime of the financial instruments;

(3) Stage III: Financial assets with objective evidence of impairment at the balance sheet date

apply the Stage III Model of ECL, with their impairment provisions measured at the amount

equivalent to the ECL for the lifetime of the financial instruments.

2. Methodology for determining a significant increase in credit risk

Our Branch considers a credit asset to have experienced a significant increase in credit risk

when one or more of the following quantitative, qualitative or backstop criteria have been met:

25 / 38

Credit Risk (Continued)

2.1 Quantitative criteria

(1) At the reporting date, the increase in remaining lifetime probability of default (PD) is

considered significant, comparing with the one at initial recognition;

(2) The determination of what is ‘significant’ requires judgment. In making this judgment, the

Branch evaluates, among other factors, the changes in internal operating results of the

borrower; expected changes in interest rates and internal price indicators of credit risk;

2.2 Qualitative criteria

(1) Significant adverse change in debtor’s operation or financial status;

(2) Be classified into Special Mention category within five-tier loan classification.

2.3 Backstop criteria

The contractual payments of the debtor’s any principal, advances, interest or corporate bond

are more than 30 days past due.

3. Definition of credit impaired assets

The standard adopted by the Branch to determine whether credit impairment occurs under

IFRS 9 is consistent with the internal credit risk management objectives of the relevant

financial instrument, taking into account quantitative and qualitative criteria. When the Branch

assesses whether the credit impairment of debtor occurred, the following factors are mainly

considered:

(1) Significant financial difficulty of the issuer or the debtor;

(2) Debtors are in breach of contract, such as defaulting on interest or becoming overdue on

interest or principal payments overdue;

(3) The creditor of the debtor, for economic or contractual reasons relating to the debtor’s

financial difficulty, having granted to the debtor a concession that the creditor would not

otherwise consider;

(4) It is becoming probable that the debtor will enter bankruptcy or other financial

reorganization;

(5) The disappearance of an active market for that financial asset because of financial

difficulties;

(6) The purchase or origination of a financial asset at a deep discount that reflects the

incurred credit losses;

(7) The debtor leaves any of the principal, advances, interest or investments in corporate

bond of the Branch overdue for more than 90 days.

The credit impairment of a financial asset may result from the combined effect of multiple

events and may not be necessarily due to a single event.

26 / 38

Credit Risk (Continued)

4. Definition of Default:

The Branch defines its credit exposures as default in the case of:

4.1 exposures other than retail exposures, to be deemed to have occurred when the branch

is of the opinion that an obligor is unlikely to meet their credit obligations in full without any

resource by the branch to actions such as the realization of security, which opinion of the

Branch as a minimum, are based on the matters specified below:

(1) The Branch has assigned non-accrued status to the relevant credit obligation;

(2) The Branch has written off a portion or raised a specific provision in respect of the

relevant credit exposure due to a significant perceived decline in the credit obligor since the

branch incurred the said exposure;

(3) The Branch is about to sell the credit obligation at a material credit-related economic loss;

(4) The Branch has consented to a distressed restructuring of the credit obligation, which

restructuring is likely to result in a reduced financial obligation caused by, for example, the

postponement of principal, interest or fees;

(5) The Branch has applied for or has been placed in bankruptcy or similar protection and the

said event is likely to avoid or delay repayment of the credit obligation to the Banking Group.

(6) The Obligor has applied for or has been placed in bankruptcy or similar protection and the

said even is likely to avoid or delay repayment of the credit obligation to the BOC Group.

4.2 exposures other than retail exposures are deemed to have occurred when a material

obligation of an obligor is overdue for more than 90 days;

4.3 retail exposures to be deemed to have occurred when the criteria specified paragraph 4.1

or 4.2 above are present at a facility level instead of an obligor level;

4.4 An overdraft facility is deemed to have occurred when:

(1) An obligor exceeded an advised limit for more than 90 days, that is, the relevant obligor

failed to reduce the outstanding amount within the said period of time to an amount that is

within the authorized limit; or

(2) An obligor is advised of a limit smaller than the obligor’s existing outstanding amount and

the relevant obligor failed to reduce the outstanding amount within a period of 90 days to an

amount that is within the newly advised limit;

(3) The Branch extends credit to a person with no authorised limit, which credit is not repaid

within 90 days.

5. Definition of Write-offs

Bad debts may apply for write-offs in accordance with the following conditions:

(1) Credit facility’s capital, interest, and investment assets that are incapable to recover after

disposal;

(2) Approved Credit facility’s capital and interest debt reduction;

(3) For bad debts that have been approved for write-offs, the loss of collateral liquidation after

the disposal of collateral (the amount of collateral liquidation loss = the amount of collateral –

the recovery amount of liquidation + the cost of collateral liquidation);

27 / 38

Credit Risk (Continued)

(4) Credit facility’s capital, interest or investment assets that shall be written-off in accordance

with South Africa Law or specific requirements from regulatory authorities.

6. Definition of Restructured Exposures

The Branch defines its exposures as Restructured Exposures when the credit facility granted

to the obligor with weakened credit obligations to the Branch such as decrease interest rate,

change in repayment plan, change in debt servicing obligor, reduce the collaterals ceded to the

Branch, etc. due to its distressed financial conditions which caused their capabilities to fulfill

debt payments to the Branch. At 31 December 2019, total restructured loans are R117 million.

An analysis of gross credit exposures by industry:

Gross credit counterparty exposures by residual contractual maturity at 31 December

2019

On balance

sheet

exposure

Off balance

sheet

exposure

Derivative

instrumentsTotal

Agriculture, hunting, forestry and fishing 320 383 - 704

Mining and quarrying 2,354 1,663 - 4,017

Manufacturing 7,031 1,509 - 8,540

Electricity, gas and water supply 333 70 - 403

Construction 322 336 - 659

Wholesale and retail trade, repair of specified items, hotel103 276 2 381

Transport, storage and communication 3,704 1,559 - 5,264

Financial intermediation and insurance 24,339 924 167 25,430

Real estate 7,267 69 - 7,335

Business services 180 - - 180

Community, social and personal services - - - -

Private households 23 - - 23

Other 644 356 - 999

Total 46,620 7,145 170 53,935

Up to 3 monthsThree to Six

months

Six months to

one year

One to Five

Years

Five to Ten

Years> 10 years Total

Loans and advances to banks 2,025 - 3,189 3,923 - - 9,137

Cash placements at banks - - -

Investment securities 1,564 2,734 3,726 3,124 11,147

Derivative financial instruments 79 79

Loans and advances to customers 2,520 5,194 1,243 4,860 8,189 745 22,751

Total on-balance sheet exposures 6,188 7,928 8,157 11,908 8,189 745 43,114

Guarantees - 135 - 3 259 397

Contingent liabilities, committed facilities and other - - - - 506 - 506

Total off-balance sheet exposures - 135 - 3 765 - 902

Total gross credit exposures 6,188 8,063 8,157 11,910 8,954 745 44,017

28 / 38

Credit Risk (Continued)

An age analysis of past due and default loans and advances to customers

Qualitative disclosure requirements related to credit risk mitigation techniques

(CRC)

Credit risk mitigation refers to various actions that the manages its credit risk exposure (proactively and reactively). Generally, the Branch takes credit risk mitigation methods as the second source of debt payments from its clients; however the primary source of debt payments from the clients themselves should be the core lending consideration.

The Branch has established its credit risk mitigation appetite, and measures on how to manage the Branch’s collaterals. The collaterals are being valued at the inception of the lending business, being dynamically and regularly monitored, and periodically reviewed over the lending lifecycle.

Table 16: Credit risk mitigation techniques – overview (CR3)

The following table reports the extent of use of CRM techniques used to reduce capital

requirements as well as the extent of exposures secured by collateral and/or guarantees.

The secured exposures are reported as EAD pre any credit conversion factors or mitigation in

the current reporting period and only contains exposures that have security against them

either in full or partially.

All exposures not secured by both eligible collateral and/or a qualifying guarantee are

regarded as unsecured.

There have been no changes in the credit risk mitigation disclosure compared to prior periods.

Dec-19

Default loans 587

1 - 30 days -

31 - 60 days -

61 - 90 days -

Total 587

a b c d e f g

Exposures unsecured:

carrying amount

Exposures

secured by

collateral

Exposures

secured by

collateral, of

which secured

amount

Exposures

secured by

financial

guarantee

Exposures

secured by

financial

guarantee, of

which secured

amount

Exposures

secured by

credit

derivative

Exposures

secured by

credit derivative,

of which

secured amount

1 Loans 34,573 117 91 - - - -

2 Debt Securities 11,130 - - - -

3 Total 45,703 117 91 - - - -

4 Of which defaulted 76

29 / 38

Credit Risk (Continued)

Qualitative disclosures on bank’s use of external credit ratings under the

standardized approach for credit risk (CRD)

The Branch applies the standardized approach for calculating capital requirements in the

assessment of its credit and counterparty exposures. The Branch conducts the mapping of

credit and counterparty exposures in accordance with the mapping procedures specified by

the South African Reserve Bank.

The Branch applies the external credit rating from the external credit assessment institutions

(ECAIs), namely Standard and Poor’s, Fitch and Moody’s for standardized approach

calculation. In the case the client is rated by two institutions, the rating of the higher one will be

applied. The middle of the ratings will be applied if the client has rating from three ECAIs.

Internal and external credit ratings are included in the assessment of the credit risk of clients.

The Branch internal rating system divides the credit rating into 27 levels based on the level of

debtors rating and default risk.

Customers' credit rating results are important reference for the Branch to carry out the

management of credit approval, customer entry, risk monitoring, limit management,

post-lending management, credit policy, risk report, economic capital, risk preference, loss

reserve, risk pricing and performance appraisal.

Table 17: Standardised approach – credit risk exposure and Credit Risk Mitigation

(CRM) effects (CR4)

The table below illustrates the effect of eligible collateral as defined in the standardized

approach for credit risk.

a b c d e f

Asset classes

On-balance

sheet amount

Off-balance

sheet

amount

On-balance

sheet amount

Off-balance

sheet

amount

RWARWA

density

1 Sovereigns and their central banks 11,547 355 11,547 177 578 5%

2 Non-central government public sector entities (PSEs) 3,327 3,327 665 20%

3 Multilateral development banks (MDBs) 0%

4 Banks 12,130 424 12,130 212 8,875 72%

5 Securities firms 0%

6 Corporates 19,180 6,324 19,089 2,472 21,559 100%

7 Regulatory retail portfolios 17 13 17 2 16 90%

8 Secured by residential property 23 23 8 35%

9 Secured by commercial real estate 0%

10 Equity 0%

11 Past-due loans 587 29 76 15 45 50%

12 Higher-risk categories 0%

13 Other assets 848 848 27 3%

14 Total 47,660 7,145 47,057 2,878 31,773 64%

Exposures before CCF

and CRM

Exposures post CCF and

CRMRWA and RWA density

30 / 38

Credit Risk (Continued)

RWA is driven by exposures to corporates (68%) and Banks (28%) compared to 2018 of

corporates (71%) and Banks (24%)

Table 18: Standardised approach – exposures by asset classes and risk weights

(CR5)

The table below presents the breakdown of credit risk exposures under the market based

approach by asset class and risk weight, corresponding to the RW%. There were no

significant changes to the exposure overall. However, there was an increase in exposures

under Sovereign and Central Banks mainly due to the additional purchase of Treasury

Bills.

a b c d e f g h i j

Risk

weight

Asset classes

0% 10% 20% 35% 50% 75% 100% 150% Others

Total credit

exposures amount

(post CCF and post-

CRM)

1 Sovereigns and their central banks 11,147 578 11,725

2 Non-central government public sector entities (PSEs) 3,327 3,327

3 Multilateral development banks (MDBs) -

4 Banks 2,687 276 1,067 8,312 12,342

5 Securities firms -

6 Corporates 21,561 21,561

7 Regulatory retail portfolios 3 15 18

8 Secured by residential property 23 23

9 Secured by commercial real estate -

10 Equity -

11 Past-due loans 90 90

12 Higher-risk categories -

13 Other assets 821 27 848

14 Total 14,655 - 3,604 23 1,160 - 30,493 - - 49,935

31 / 38

Counterparty Credit Risk

Qualitative disclosure related to counterparty credit risk (CCRA)

Counterparty credit risk refers to the risk that a counterparty to a transaction may default

prior to the satisfactory final settlement of the cash flows of one of the following types of

the transactions: derivative instruments, repo transactions, securities or commodities

lending, long settlement transactions and margin lending transactions.

The Branch uses Murex system for CCR measurement purpose. The derivative portfolio

consists of FX swap, FX forward and Cross Currency swaps. The Branch applies

Standardised Approach and Standardised CVA to calculate its total CCR capital charge.

The Branch shall strictly review the counterparty eligibility criteria and scope of applicable

products before transactions. In the case of credit to corporate counterparty, the business

unit shall initiate credit application with the support of the treasury transactions

departments and manage credit limit.

The semi-annual comparison showed that there was a decrease in the valuation of the

derivative portfolios and fewer derivative transactions from 30 June 2019. This meant that

there was a decrease in the RWA.

Table 19: Analysis of counterparty credit risk (CCR) exposure by approach (CCR1)

The following table provides a summary of the methods used to calculate counterparty

credit risk regulatory requirements and the main parameters used within each method.

a b e f

Replacemen

t cost

Potential

future

exposure

EAD post-

CRMRWA

1 SA-CCR (for derivatives) 79 90 170 28

2 Internal Model Method (for derivatives and SFTs)

3 Simple Approach for credit risk mitigation (for SFTs)

4 Comprehensive Approach for credit risk mitigation (for SFTs)

5 VaR for SFTs

6 TOTAL 28

32 / 38

Counterparty Credit Risk (Continued)

Table 20: Credit valuation adjustment (CVA) capital charge (CCR2)

The following table provides a summary of the CVA regulatory calculation under the

standardised approach

Credit valuation adjustment (CVA) in the regulatory context is a capital charge to be taken

into account possible volatility in the value of derivative instruments due to changes in the

credit quality of the Branch’s counterparty. The decrease year on year is mainly due to

fewer derivatives transactions.

Table 21: Standardised approach of CCR exposures by regulatory portfolio and risk

weights (CCR3)

The following table provides a breakdown of counterparty credit risk exposures excluding

all CVA exposures that are reported in CCR2 as well as exposures to central

counterparties, calculated according to the standardised approach: by portfolio (type of

counterparties) and by risk weight.

a b

EAD post-CRM RWA

Total portfolios subject to the Advanced CVA capital charge

1 (i) VaR component (including the 3×multiplier)

2 (ii) Stressed VaR component (including the 3×multiplier)

3 All portfolios subject to the Standardised CVA capital charge 170 70

4 Total subject to the CVA capital charge 170 70

a b c d e f g h j

Risk

weight

Regulatory portfolio

0% 10% 20% 50% 75% 100% 150% Others

Total

credit

exposure

Sovereigns -

Non-central government public sector

entities (PSEs)-

Multilateral development banks (MDBs) -

Banks 39 128 0 167

Securities firms -

Corporates 2 2

Regulatory retail portfolios 0 0

Other assets -

Total 39 - 128 - - 3 - - 170

33 / 38

Counterparty Credit Risk (Continued)

Table 22: Exposures to central counterparties (CCR8)

a b

EAD (post-CRM) RWA

1 Exposures to QCCPs (total)

2

Exposures for trades at QCCPs (excluding

initial margin and default fund

contributions); of which

3 (i) OTC derivatives

4 (ii) Exchange-traded derivatives

5 (iii) Securities financing transactions

6(iv) Netting sets where cross-product

netting has been approved

7 Segregated initial margin

8 Non-segregated initial margin

9 Pre-funded default fund contributions

10 Unfunded default fund contributions

11 Exposures to non-QCCPs (total) -

12

Exposures for trades at non-QCCPs

(excluding initial margin and default fund

contributions); of which

170 -

13 (i) OTC derivatives 170 -

14 (ii) Exchange-traded derivatives

15 (iii) Securities financing transactions

16(iv) Netting sets where cross-product

netting has been approved

17 Segregated initial margin

18 Non-segregated initial margin

19 Pre-funded default fund contributions

20 Unfunded default fund contributions

34 / 38

Market Risk

General qualitative disclosure requirements related to market risk (MRA)

Strategy and processes of the Bank

The Branch is exposed to the following market related risks, the currency risk and interest

rate risk. The Branch enters into a variety of derivative financial instruments for risk

management purposes.

Interest rate risk

The strategies and objectives of the Branch is to optimise net interest income, given the

current market interest rate levels.

The Branch’s operations are subject to the risk of interest rate fluctuations to the extent

that interest-earning assets (including investments) and interest-bearing liabilities mature

or reprice at different times or in differing amounts. As such, the Branch enters into

interest rate derivatives to bridge the mismatch in the repricing of assets and liabilities.

This is done in accordance with the guidelines established by the Branch’s asset-liability

management committee.

Part of the Branch’s return on financial instruments is obtained from controlled

mismatching of the dates on which interest receivable on assets and interest payable on

liabilities are next reset to market rates or, if earlier, the dates on which the instruments

mature.

Currency risk

The Branch is exposed to currency risk through transactions in foreign currencies. The

Branch’s funding is diversified in local currency and foreign currencies. As the currency in

which the Branch presents its annual financial statements is the South African Rand, the

Branch annual financial statements are affected by movements in the exchange rates

between the South African Rand and the foreign currencies.

The Branch’s transactional exposures give rise to foreign currency gains and losses that

are recognised in the statement of other comprehensive income. As such, the Branch

would enter into FX Swaps as means to manage the transactional exposures which would

give rise to the foreign currency gains and losses.

35 / 38

Market Risk (Continued)

Structure Governance

The market risk is governed by the guidelines established by the Branch’s asset-liability

management committee. The committee meets at least on a quarterly basis and would set

guidelines in order to manage the market risk in line with the Branch’s strategy.

Scope and nature of risk reporting and/or measurement systems.

The disclosures relating to Market Risk are disclosed annually on the Annual Financial

Statements.

The Branch measures the derivatives at fair value and they determine the fair value based

on the amount the Branch would receive or pay to terminate the contract at the statement

of financial position date taking into account current market conditions and current

creditworthiness of the counterparties. The measurement systems are usually industry

Standard models.

Table 23: Market Risk under the SA (MR1)

The products that the Branch has under the Standardised Approach are outright products

which are subjected to the foreign exchange risk. The major currencies that subject to the

market risk are USD and CNY. There has been no significant movements compared with

June 2019.

a

RWA

Outright products

1 Interest rate risk (general and specific)

2 Equity risk (general and specific)

3 Foreign exchange risk 15

4 Commodity risk

Options

5 Simplified approach

6 Delta-plus method

7 Scenario approach

8 Securitisation

9 Total 15

36 / 38

Remuneration

Remuneration policy (REMA)

The Branch’s philosophy is to employ high caliber individuals who are characterized by

integrity and professionalism and who adhere and subscribe to its culture and values. The

Branch attracts and retains talents through providing a competitive annual cost-to-company

package, which includes a fixed annual salary and employee fringe benefits, and rewards it

employees for their positive contribution and performance through payment of a variable

remuneration in the form of performance bonus.

The remuneration committee at Bank of China Head Office level is an integral part of the

group’s governance structure and organization, who oversees and reviews the group’s

remuneration policy and system design. The Remuneration Division of Bank of China Head

Office Human Resource Department drafts the group’s remuneration policies, processes,

practices and procedures, and overseas the remuneration operation of the group.

The Remuneration Division of Bank of China Head Office Human Resource Department

monitors and reviews the operation relating to remuneration matters of all domestic and

overseas branches/institutions on a quarterly/bi-annually/annually basis via various reports.

The Branch subscribes to the Head Office’s remuneration policy and procedure, and adheres

to its monitoring and review program on the Branch’s remuneration related operation, and

submits periodic review reports according to the Head Office’s requirement

The Branch’s policies, processes, practices, procedures relating remuneration encompassed

the BCBS corporate governance principle to banks, thus support and promote sound

corporate governance and effective risk management.

37 / 38

Remuneration (Continued)

REM1: Remuneration awarded during the financial year

The remuneration awarded was paid in line with the Branch’s policies, processes, practices

and procedures during the 2019 financial year and there were no significant movements noted

during the year.

Table 24: Remuneration awarded during the financial year

* Employee fringe benefits

# includes 3 ex-executive members and 4 current executive members

REM2: Special payments

Table 25: Special payments

(In ZAR, before tax)

Remuneration amount Senior management Other material risk-takers

1 Number of employees 5

2 Total fixed remuneration (3 + 5 + 7) 22 -

3 Of which: cash-based 19

4 Of which: deferred -

5 Of which: shares or other share-linked instruments -

6 Of which: deferred

7 Of which: other forms * 3

8 Of which: deferred -

9 Number of employees # 7

10 Total variable remuneration (11 + 13 + 15) 20

11 Of which: cash-based 20

12 Of which: deferred 18

13 Of which: shares or other share-linked instruments -

14 Of which: deferred

15 Of which: other forms -

16 Of which: deferred

17 Total remuneration (2 + 10) 42 -

Fixed remuneration

Variable

remuneration

REM1

REM2

Number of employees Total amount Number of employees Total amount Number of employees Total amount

Senior management - - - - - -

Other material risk-takers - - - - - -

Guaranteed bonuses Sign-on awards Severance payments

38 / 38

Remuneration (Continued)

REM3: Deferred remuneration

Table 26: Deferred remuneration

REM3

a=b+e b=c+d c d e

Deferred and retained

remuneration

Total amount of

outstanding deferred

remuneration

Of which: Total amount of

outstanding deferred and

retained remuneration exposed

to ex post explicit and/or implicit

adjustment

Total amount of

amendment during the

year due to ex post

explicit adjustments

Total amount of

amendment during the

year due to ex post

implicit adjustments

Total amount of deferred

remuneration paid out in

the financial year

Senior management 20 18 12 6 2

Cash 20 18 12 6 2

Shares

Cash-linked instruments

Other

Other material risk-takers

Cash

Shares

Cash-linked instruments

OtherTotal 20 18 12 6 2