Level 6, 27 Currie Street, Adelaide, SA 5000 GPO Box 551 Adelaide SA 5001 Telephone: (08) 8425 4999 Facsimile: (08) 8410 1597

Futuris Corporation Limited A.B.N. 34 004 336 636

21 September 2007 Company Announcements Platform Australian Securities Exchange Limited

ANNUAL REVIEW & TOP 20 In accordance with Listing Rule 4.5.1, please find attached Futuris Annual Review and Top 20 Shareholder listing for the year ended 30 June 2007. Sonya Furey Company Secretary

2 0 0 7 A n n u A l R e v i e w

The future is now.Tomorrow’s challenge is today’s opportunity.

Futuris Corporation limitedABN 34 004 336 636

Annual General Meeting The 2007 annual general meeting of Futuris Corporation Limited will be held on Tuesday 23 October at the Adelaide Festival Centre commencing at 9.30am Central Standard Time. A formal notice of meeting has been mailed to shareholders. Additional copies can be obtained from the Company’s registered office or down loaded from its website at www.futuris.com.au

Terms and Abbreviations This report uses terms and abbreviations relevant to the Company’s activities and financial accounts. The terms

“the Company”, “Futuris Corporation” and “Futuris” are used in this report to refer to Futuris Corporation Limited and or its subsidiaries. The terms “the year” and

“2007” refer to the twelve months ended 30 June 2007 unless otherwise stated. Similarly, references to 2006 or 2008 refer to the twelve months to 30 June of that year. Unless otherwise specified, the term “30 June” refers to 30 June 2007.

Annual Report This publication is one of two documents published by Futuris to report on the Company’s performance in the year to 30 June 2007:

– the Annual Review provides an overview of the Company, discussion of its results and a Concise Report. It also includes a Directors’ Report and Auditor’s Report.

– the Annual Financial Report provides a complete set of financial statements for the year.

The Concise Report does not, and cannot be expected to, provide as full an understanding of the financial performance and position and financing and investing activities of the consolidated entity as the complete set of financial statements contained in the Annual Financial Report.

Shareholders may elect to receive either or both of the reports free of charge upon request.

Shareholders wishing to arrange or alter the mailing of these reports can do so by notifying the Company’s share registry (at the address provided in the Company Directory on the inside back cover of this report) or by contacting the Company on 61 (0)8 8425 4999.

Copies of either the Annual Review or the Annual Financial report can be down loaded from our website at www.futuris.com.au.

is building businesses to commercially meet the challenges of the future.

These challenges: • sustainability; • the need to produce greater volumes

of food, paper and wood from fi nite resources;

• innovation with, and productiveadoption of, new technology;

• product integrity, traceability and quality; • varietal improvement;• balancing global integration with

local capabilities, and• maintaining the vitality and

economic health of our rural andregional communities;

are themes through which our businesses are growing in signifi cance and value.

2

3

Futuris is building businesses that are finding sustainable solutions for the needs of day-to-day living.

Our forestry operations are reducing the demands made on the world’s high conservation forests and reducing atmospheric carbon levels.

Our rural service and agriculture operations are helping farmers access varieties that are productive and more suited to modern Australian conditions.

Our aquaculture interests are researching large scale production of seafood to help satisfy growing demand for protein through a sustainable alternative to the depletion of natural aquatic resources.

Futuris is carbon negative.

The future is

sustainable.

Left: On the Baboo Pastoral Company property at Green Range, Western Australia, Tasmanian Blue Gum trees are grown in addition to traditional crops such as canola (foreground). Pulpwood produced by plantation such as these is helping replace supply from native forests.

4

5

Futuris is building businesses which create value by helping rural and regional communities integrate into global information matrices and improving the effi ciency of supply chains and access to markets for producers.

Our telecommunications interests have won the tender to build and operate Australia’s rural and regional broadband network.

Elders Rural Services is restructuring supply chains for wool and grain producers, providing growers with new and more effi cient routes to market. Farm input supply chains are being optimised to give growers the benefi t of speedy and more cost effective delivery of the best inputs for their endeavours.

The future is

better connected.

Left: High capacity fi bre-optic cable being laid near Roseworthy, South Australia. Amcom Telecommunications extended its broadband network to Roseworthy where Elders Roseworthy branch will be one of a number of locations where the Company will showcase and pioneer broadband applications.

6

7

Futuris links strong local presence in the Australian rural and regional sector with global markets.

Our rural services businesses are matching the production capabilities of Australian farmers with domestic and international buyers of wool, grain, meat and livestock and horticulture. We pioneered offshore wool auctions, taking the sale of fine Australian wool to its largest market, and the export of livestock to offshore markets.

Our forestry operations are establishing plantations in regions identified as being the most appropriate by a comprehensive national profiling exercise.

Our financial services operations give rural and regional Australians local service in banking, insurance and wealth management with a range of products designed to meet their needs.

Backing it all up is a network of approximately 400 locations around Australia linking country Australia with international primary produce buyers.

The future is local presence and a global vision.

Left: Kylie Kemp of Elders Roseworthy branch assists a client with an order. Roseworthy, which is one of 400 Elders locations around Australia, serves an area of approximately 20,000 square kilometres for clients engaged in cropping, viticulture, horticulture, wool and livestock production.

8

is focussed on the Australian rural and regional sector and the value it generates in Australia and internationally through:

• world class production of food and fi bre• sustainable forestry and carbon management• responsible land management• varietal improvement• and best practice supply of inputs and services to successful primary producers and the growing regional population.

Review of operationsOur Businesses

9

Additional income in FY2007 was also sourced from interests held in the automotive sector and from property development operations divested during the year.

Our Business is developing around four key business streams within the rural and regional value chain, and is supplemented by interests in leading corporate food producers.

Management of one of Australia’s largest hardwood timber plantation estates. Processing and sale of value-added hardwood timber products.

ForestryF07 EBIT: $57 millionEBIT share: 35%

Rural ServicesFarm inputs, servicesand supply chain to andfrom farm-gate through Elders, Australia’s leading rural retailer.

F07 EBIT: $49 millionEBIT share: 30%

TelecommunicationsRetail to rural and regional consumers through Elders.

Won tender to build and operate government funded wholesale broadband network to rural and regional Australia.

49% shareholder Amcom Telecommunications.

Not material in FY08.

To be reported separately from FY08

Banking, Insurance and wealth management by APRA licensed and prudentially regulated entities.

Financial ServicesF07 EBIT: $27 millionEBIT share: 16%

F07 $7 million (equ. acc. NPAT)

NPAT share: 7%

Beef, Horticulture and AquacultureFuturis is Australia’s largest individual interest holder in corporate production of beef, fi sh and horticulture.

10

The year in briefRecord earnings in a tough year.

FinancialHighest ever underlying profit

• Sales revenue down 4% to $3,228.5 million• Record underlying profi t to shareholders up 15% of $101.7 million• Reported profi t to shareholders of $100.7 million• Year end gearing of 24%

Elders Rural ServicesSolid performance in drought affected year

• Underlying EBITDA up 1% to $64.3 million• EBIT of $49.1 million, 5% lower• Increased contribution from Wool, Real Estate and Distribution of Financial Services • Commissioning of Shangdong wool processing operations

Financial Services Ongoing growth

• Earnings before tax up 5% to $39.5 million• Elders Rural Bank profi t up 11%• Insurance earnings before tax maintained at $24 million

ForestryImproved processing operations, increased MIS sales

• ITC increases EBIT by 43% to $56.9 million• Acquisition of 9,000 hectares of plantation to bring estate size to 160,000 hectares• MIS sales increase 30% • Processing operations lift performance and profi t• 5% increase in woodchip prices secured

TelecommunicationsStrategy rewarded with funding for new business stream

• Elders Optus joint venture wins $958 million funding from Australian Government to build and operate rural and regional broadband network

• Shareholding in Amcom increased to 49.1% Corporate DevelopmentTransition to rural and regional focus advanced

• Property Development operations divested• Aquaculture interests expanded• Increased shareholding in Webster, Forest Enterprises Australia

11

Year ended 30 June

$ million unless otherwise indicated 2007 2006 Change

Sales revenue 3,228.5 3,355.8 -4%

EBIT underlying 164.7 157.1 5%

Net interest 40.0 39.0 3%

Profi t before tax underlying 124.7 118.2 5%

Tax on underlying profi t (20.2) (29.9) -32%

Minority interests 2.8 9.0 -69%

Underlying profi t to shareholders 101.7 88.3 15%

Non-recurring items after tax (1.0) (0.9) n/m

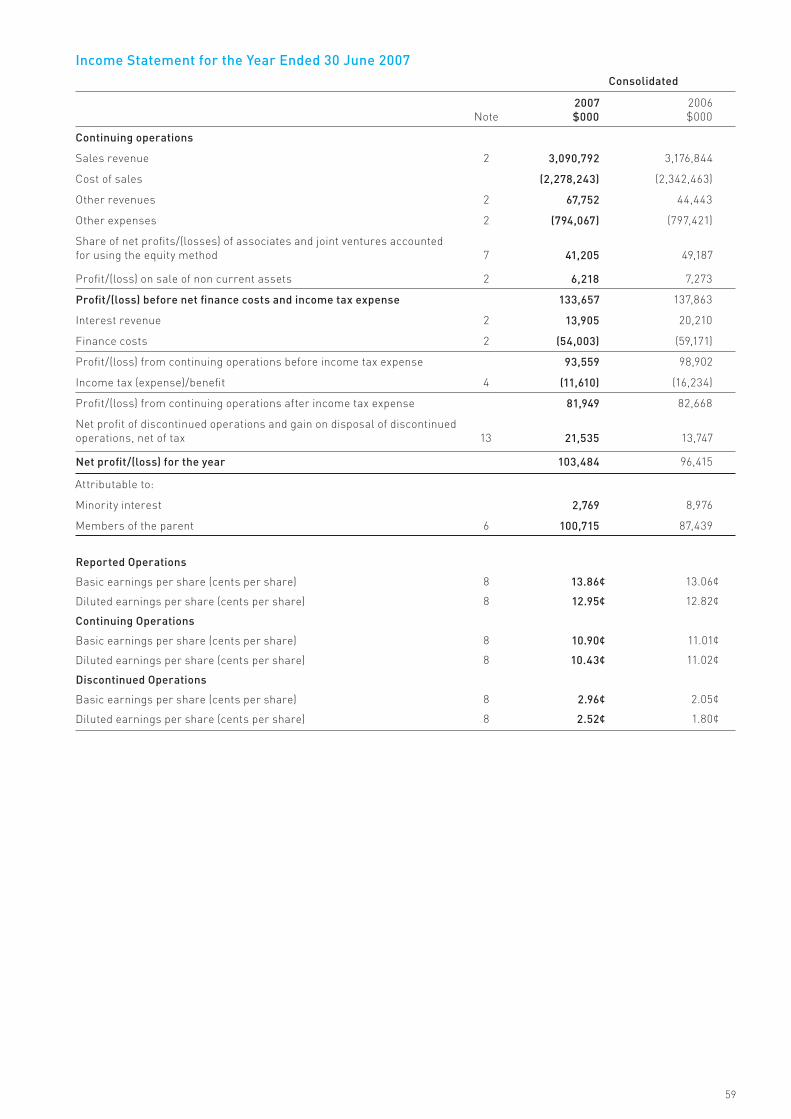

Net profi t after tax and minority interests 100.7 87.4 15%

Cash fl ow from operating activities 85.0 127.4 -33%

Borrowings 609.2 739.5 -18%

Net debt 364.9 202.0 +81%

Net Assets 1,186.5 1,227.9 -3%

Dividend per share (cents) 9.5 9.0 6%

Earnings per share (underlying cents) 14.00 13.18 6%

Earnings per share reported (cents) 13.86 13.06 6%

Gearing (% net debt/net debt+equity) 24 14 n/m

Employees (no) 5,928 6,033 -2%

Share price ($ per share) 2.78 2.10 32%

48

7.65

9.57

14.0013.18

10.86

Earnings per share(cents underlying)

63

102

88

72

Profi t after tax (underlying $ million)

2464

1.68 1.58

2.78

2.10

1.82

Share Price ($ per share)

2707

32293356

3175

2003 2004 2005 2006 2007

Sales revenue ($ million)

8496

165157

131

EBIT(underlying $ million)

2003 2004 2005 2006 2007 2003 2004 2005 2006 2007 2003 2004 2005 2006 2007 2003 2004 2005 2006 2007

12

Stephen GerlachChairman

Dear Shareholder

I am pleased to report that your Company has completed one of its most challenging years with one of its best ever profit results.

Futuris recorded a statutory profi t of $100.7 million in 2007, 15% higher than the previous year’s result of $87.4 million. The 2007 fi nancial results included non-recurring items totalling $1.0 million after tax ($0.9 million in 2006), which are detailed in the Discussion and Analysis of the Income Statement.

After exclusion of non-recurring items, the underlying profi t to shareholders for the year was $101.7 million, 15% above the 2006 result of $88.3 million.

As I have noted above, these results were achieved in testing circumstances, with the majority of Australian agricultural regions suffering protracted and severe rainfall defi ciency that extended for nearly 10 months of the year, brought by a recurrence of the El Nino weather pattern.

The impact of this drought on the rural economy and Futuris was signifi cant. In previous comparable El Nino events, the Company suffered earnings contraction as a result. But in 2007, Futuris was able to take its underlying profi t to new levels because its businesses with low seasonal exposure continued to grow whilst those sensitive to seasonal conditions have performed well in diffi cult markets.

From the Chairman

Strategic direction and operations

The strategic direction taken by the Company to build its business around the Australian rural and regional sector is being increasingly refl ected in its asset base as new initiatives are completed each year.

This process is being supported by ongoing changes to reporting structures to maintain appropriate concentration of management and governance and to provide transparency of performance for key elements of its strategy.

In 2007, the Company commenced separate reporting of Elders Rural Services (which incorporates Elders’ traditional agency, supply chain and farm supply operations) and Elders Financial Services operations.

The performance of Elders Rural Services was appropriate given the circumstances. These operations recorded a 5% drop in EBIT, a result which shows the progress that has been made since the comparable El Nino event of 2002/03 when EBIT contracted by more than 20%.

Elders Financial Services operations have continued to advance and increase their contribution to the Company. Elders Rural Bank recorded another year of strong growth. Insurance operations broadly maintained their earnings before tax at $24 million.

Integrated Tree Cropping (ITC) became a wholly-owned subsidiary of Futuris during the year and achieved improvement across its operations. ITC’s plantation estate and harvest volumes expanded further, while the income from timber processing increased.

ITC’s development is progressing in line with Futuris’ vision for the business as Australia’s leading supplier of sustainably produced timber and woodfi bre.

13

contributors to the Company’s long term development from a small company to today’s position. On behalf of the Board and all shareholders I would like to record our appreciation and thanks for their considerable contributions to Futuris.

Mr Ian MacDonald was appointed to the Board in November 2006 as a non-executive director. Mr MacDonald has joined Futuris after a long and successful career in banking.

Conclusion and outlook

Futuris has concluded 2007 with strong fi nancial results and positive momentum in its businesses.

The Company’s Financial Services and Forestry businesses are growing, while its Rural Services operations are positioned to benefi t from improved seasonal conditions.

At a more general level, the leading positions held by the Company’s businesses mean that Futuris expects to be a benefi ciary of the rising demand for agricultural and forestry produce, the introduction of broadband telecommunications to rural and regional Australia and economic recognition of carbon impacts. Futuris has a promising outlook and, given normal business and seasonal conditions, expects to generate earnings improvement for the foreseeable future.

In closing, I would like to acknowledge the efforts of the Company’s employees, thank them for their efforts and wish them every success in the newfi nancial year.

Stephen GerlachChairman

ITC is now the lead negotiator for certifi ed plantation woodchip exports from Australia to Japan and its signifi cance as a supplier is set to rise as its existing plantations mature and sales volumes rise to exceed 1 million tonnes per annum. As the manager of one of Australia’s largest hardwood plantation estates, ITC is positioned to be one of the nation’s larger generators of carbon credits.

The development of the Company’s rural and regional and telecommunications assets and strategy means that its remaining automotive operations account for a much smaller share of Futuris’ asset base and earnings than has been the case. These assets are being managed and developed according to a medium term strategy proven with Air International’s Global Thermal division.

Financial results from Futuris Automotive in 2007 refl ect conditions in the local passenger vehicle sector. However, the business made good progress with the key element of its strategy - the development of a well-founded business in China.

Futuris is now no longer involved in property development following the sale of Caversham Property during the year. The sale enabled the Company to bring forward profi t and capital realisation from its Property assets and to reallocate those funds to help meet the needs of its growing rural and regional assets.

The Company has continued to achieve improvement in its occupational health and safety outcomes. Ongoing improvement is being sought in all areas of our operations.

Sustainability is a common consideration in the Company’s development as it builds its businesses. The Company has an overall

commitment to environmentally responsible conduct across all of its operations and also supports initiatives to promote sustainability and the communities in which it operates.

During the year Elders made a major commitment to support sustainable land use through a 5 year partnership with Landcare Australia. The Elders Landcare Farming Partnership is designed to promote environmental sustainability in the rural sector.

Corporate Governance

Futuris supports the spirit of the ASX Corporate Governance Council’s Principles of Good Corporate Governance and Best Practice Recommendations. A comparison of the Company’s corporate governance polices and practices against the Council’s Recommendations is included in the Corporate Governance Report of this document.

The Company’s governance practices comply in all substantial respects with the Council’s Recommendations. Futuris has appropriate corporate governance policies and practices and a Board of Directors who exercise independent judgement in the best interests of the Company.

Board of Directors

During the year Mr Alan Newman retired from the Board of Directors due to ill health. Mr Newman served as Managing Director from 1989 to 2003 and subsequently as a non-executive Director.

Deputy Chairman Mr Walter Johnson has advised that he will not seek reappointment to the Board at the forthcoming AGM and, accordingly, will retire from the Board in October 2007 after nearly 26 years service as a Director.

Mr Johnson and Mr Newman have both been major and long term

Futuris has concluded 2007 with strong fi nancial results, positive momentum in its businesses and having successfully executed strategic corporate development initiatives.

14

Chief Executive’s Report

Performance overview

Futuris’ corporate strategy over the last four years has sought to deliver consistent and reliable earnings growth while restructuring the Company’s asset base towards the leading assets in the Australian rural and regional sector. In doing so, the Company has balanced the need to consistently deliver satisfactory annual fi nancial growth with the investment and business building required for medium to long term performance.

In 2007, your Company maintained its record of meeting these twin objectives, and did so emphatically, setting new profi t and share price benchmarks and taking initiatives that have signifi cantly advanced our strategic position.

In respect of earnings, the 2007 underlying profi t to shareholders of $101.7 million is the highest yet recorded by Futuris and the fourth successive annual result to feature double-digit growth rates. More importantly, earnings growth has been achieved on a per-share basis with Futuris’ underlying basic EPS having grown at a compound rate of 16% per annum over the four years to 30 June 2007.

This performance has been sustained despite indifferent to extremely poor seasonal conditions for Australian farmers over the past 3 years, highlighting the momentum provided by the Company’s initiatives in new business streams.

Through building its share of earnings from areas such as fi nancial services, regional property management and forestry, Futuris has increased the quantum and share of its earnings which carry low seasonal exposure – while retaining the potential for seasonal upside through its traditional agricultural service operations.

The results achieved in 2007 have demonstrated the progress and benefi ts of this strategy.

Strategic initiatives and corporate development

Corporate development during the year saw Futuris largely complete the transition in its asset base towards the rural and regional sector. As a result of this, non-related assets now account for 6% of the Company’s earnings base.

Ongoing corporate development will focus largely on building leading businesses and positions in the Company’s target sectors of rural services, fi nancial services, forestry and telecommunications and its agricultural producing associates.

2007 ranks as one of the most signifi cant years in Futuris’ corporate development. The initiatives undertaken during the year have had 4 major outcomes:

1) Futuris is positioned to be a lead player in rural and regional telecommunications Elders, in joint venture with Optus, was selected by the Australian Government as the sole successful tenderer for funding to build and operate a wholesale broadband network to service rural and regional Australia. The initiative is subject to the completion of funding and joint venture agreements.

The OPEL (Optus Elders joint venture) network is expected to be the principal operating asset of Futuris’ telecommunications operations and will substantially broaden our exposure and involvement in the Australian rural and regional economy.

Les WozniczkaChief Executive Offi cer

15

In many respects, telecommunications has parallels with banking and the Company’s initiative in forming Elders Rural Bank. Both are critical services where regional and rural communities have experienced declining local presence and a widening gap in service levels relative to the major population centres. The success of Elders Rural Bank has demonstrated the effectiveness of Elders staff and network in satisfying the local service needs of rural and regional communities. Similar opportunities exist in telecommunications.

Futuris’ position in the sector is also supported by its shareholding in Amcom, one of Australia’s leading second tier telecommunications fi bre owner/operator. During the year Futuris increased its shareholding to 49.1% as a result of fi nancing transactions to support Amcom’s acquisition of a 19.98% interest in iiNet, Australia’s third largest internet service provider (ISP) and the largest independent ISP to rural and regional Australia.

2) Capital is being realised from business activities that are ancillary to corporate strategyThe Company divested its property development operations.

Sale of the property development operations resulted in proceeds of $121 million during the year with a further estimated $60 million to be realised on completion of conditions.

3) The Company has reinforced its growing Forestry sector positionForestry is forecast to be a source of rising income generation within Australia due to the expansion of export volumes enabled by the maturation of plantation estates, structural changes in demand and supply and rising consumption by Asian economies.

The emerging importance of forestry for carbon management is forecast to be an added source of value.

Futuris reinforced its position in the industry in 2007 through ITC’s investment of a total of $63.1 million in plantation and processing assets and an increase in its investment in Forest Enterprises Australia (FEA).

These investments will all generate incremental earnings in the new year with the processing assets having already contributed to the better results achieved from ITC Timber in 2007.

4) Further development of the Company’s interest in aquaculture

Futuris expects corporate aquaculture will account for a growing share of regional food supply as it proves to be a sustainable, clean, quality-assured source of supply that eases pressure on wild fi sh resources.

Futuris is, through the Company’s interest in Webster Limited, the major shareholder in Tassal Limited, Australia’s largest salmon producer. Futuris increased its interest in aquaculture in 2007 through:

• increasing its interest in Webster Limited to 26.9% (now 29.5%). Webster’s interests include a 28% shareholding in Tassal, Australia’s largest salmon producer.

• acquiring a cornerstone (5.5%, fully diluted) shareholding in Clean Seas Tuna Limited, which is pioneering commercial breeding of southern bluefi n tuna; and

• acquiring a 50% interest in Aqa Oysters, one of Australia’s largest producers of Pacifi c Oysters. Aqa Oysters is engaged in consolidating production interests in what is a highly fragmented industry with the object of achieving the mass and economies that permit export of farm produced oysters to high value international markets.

The positions taken in Clean Seas Tuna and Aqa Oysters are essentially exploratory and involve modest fi nancial capital commitment of $12.9 million in total. Through involvement at the formative stage of these enterprises, Futuris has been able to economically secure participation in operations with strong potential and which complement the Company’s interest in Tassal.

Review of operations

Futuris has realigned its reporting segments to refl ect the key elements of the Company’s corporate strategy.

The new reporting framework means that the progress of our strategic plan can be readily assessed as can the performance of businesses in each sector.

The 2007 accounts are the fi rst to provide separate reporting of Elders Rural Services and Elders Financial Services, which had previously been reported within the Elders result. Telecommunications will be reported separately in the 2008 fi nancial year following OPEL’s operational commencement.

Elders Rural ServicesElders Rural Services recorded a relatively strong performance considering the severe drought conditions that affected Australia for most of 2007.

Its underlying EBIT contribution of $49.1 million, compares favourably to the previous year’s result of $51.9 million and is a demonstrably stronger result than recorded in the last comparable El Nino event in the 2002/03 fi nancial year.

The strength of the result is attributable to the building of supplementary earnings streams with low sensitivity to seasonal conditions, such as property

Earnings growth has been achieved on a per-share basis with Futuris’ underlying basic EPS having grown at a compound rate of 16% per annum over the four years.

16

Webster Limited increased its equity accounted profi t contribution from $1.8 million to $2.0 million. Webster gives Futuris participation in aquaculture (through its shareholding in Tassal Group Limited) and horticulture operations.

Elders Financial ServicesElders Financial Services generated underlying earnings before tax of $39.5 million, 5% higher than its 2006 contribution of $37.6 million.

2007 was the fi rst full year the fi nancial services operations have operated under dedicated reporting and management structures. The change has been benefi cial in increasing focus on the fi nancial services entities and the development of management plans and strategies for operations.

The performance of Elders Rural Bank over the diffi cult seasons of 2006 and 2007 has been exemplary and a telling indication of the quality of its credit policy and business model.

Insurance operations, while benefi ting from a lower incidence of catastrophe claims, bore additional distribution costs of $6 million introduced to recognise commercially based service delivery fees by the Elders Rural Services network.

The capital funding requirements for ongoing growth of these operations has been material with the Company having invested a total of $57.1 million in the past 4 years. However, the Company has been rewarded, with the performance of the fi nancial services operations having been one of the most signifi cant factors in the Company’s achievement of ongoing profi t growth despite variable seasonal conditions.

management, real estate and distribution of fi nancial services as well as an increased contribution from wool operations.

Merchandise operations fi nished a demanding year with strong momentum, achieving record sales in May and June following the rains in southern and eastern Australia.

As is customary following drought conditions, livestock and wool operations are expected to experience tighter markets.

Agricultural Producing AssociatesThe Rural Services segment result includes the equity-accounted profi ts from the Company’s agricultural producing associates Australian Agricultural Company (AACo) (43.1% interest) and Webster.

AACo provides Futuris with excellent exposure to the Australian premium beef production assets. Futuris holds a 43% interest in AACo. AACo contributed $5.2 million to the 2007 profi t compared with $6.1 million in 2006.

AACo’s year to year fi nancial results will vary with cattle prices and short term market fl uctuations, but the underlying value of the business is growing steadily as the market value of its prime cattle production properties increases and the expansion of herd numbers, particularly in the high value Wagyu herd.

This non-cash capital appreciation is not refl ected in annual fi nancial results but has been recognised by the share market in AACo’s share price. The market value of the Company’s share-holding in AACo rose by $109 million in the twelve months to 30 June.

AACo’s assets and production capability are expected to acquire increasing signifi cance and value over the long term as regional demand for traceable, quality assured beef rises and supply of pastoral land tightens.

EBIT $ million 2006 2007

Forestry 39.9 56.9

Elders Rural Services 51.9 49.1

Elders Financial Services 26.9 27.2

AACo/WBA 7.9 7.2

Property 18.2 21.5

Futuris Automotive 20.8 9.5

Investment & other -8.4 -6.7

$ million 2007

Forestry 174

Elders Rural Services 2,309

Elders Financial Services 204

Property 138

Futuris Automotive 330

Investment & Other 74

Sales Revenue by business stream

Earnings by business stream

EBIT $ million

2006 2007

200

150

100

50

0

17

ForestryITC’s results refl ect the expansion of its plantation operations and the turnaround achieved in its timber processing operations.

With timber markets having been affected by weak demand and excess stock, considerable effort has been made to lift the effi ciency and returns from ITC’s timber processing operations. The success of these efforts is evident in the improved fi nancial results.

Investments made in processing assets are contributing to better returns. The hardwood sawmilling sector is undergoing consolidation. This process, and improving market conditions, are being refl ected in sales and reduced industry stock levels.

Plantation operations expanded during the year to an estate totalling 160,000 hectares. A further 12,700 hectares will be established for Managed Investment Scheme (MIS) projects sold during the year. ITC’s commitment to a comprehensive review and reform of its MIS development and sale function was rewarded with the Company lifting sales by 30% despite industry sales being broadly in line with 2006.

The plantation timber industry is assuming a greater level of signifi cance as the volume of woodfi bre produced by maturing plantations increases. Plantation grown forest products now account for approximately 57% of Australian production. Plantation grown product is now priced separately, and at a premium, to that sourced from native forests.

In 2007 ITC secured a 4.6% rise in the benchmark price for certifi ed plantation grown hardwood woodchips. The increase, the most signifi cant for several years, is a positive indication of the demand outlook for ITC’s woodchips.

It now appears likely that some form of market-based carbon management schemes will be introduced by Australian and other international governments within 5 years. The implementation of such schemes has the potential to increase the value of ITC’s plantation estate through the economic value attributed to the estate’s carbon sequestration capability.

Until the relevant carbon management schemes are fi nalised, it is not possible to reliably attribute a fi nancial value for the carbon sequestration performed by ITC’s tree plantations.

ITC is, like the Company’s fi nancial services operations, a growing business which requires capital to fund its development. Ongoing capital expenditure is anticipated in the medium term to build ITC’s estate to the point where economies of scale are realised and the estate is self-sustaining after the rotation of harvested plantations.

Futuris Automotive Futuris Automotive is the last of the manufacturing assets still held by the Company and is the subject of a business development program designed to capture value inherent in its capabilities. A key element of this program is the leveraging of Futuris Automotive’s capability in the manufacture and supply of automotive interior systems into the rapidly growing Chinese automotive industry.

During 2007 the Company, through a 70% owned joint venture, completed construction and commissioning of a manufacturing facility to supply seating to emerging Chinese manufacturer Chery Automobile Co. Production from the facility commenced late in the fi nancial year and is expected to ramp up over the course of 2008.

Underlying EBIT of $9.5 million was generated by Futuris Automotive in 2007, lower than the previous year’s result of $20.8 million due to the costs of restructuring Australian operations, reduced demand levels and a lower contribution from associates.

Balance sheet and capital Management

The Company reduced its gross debt levels by 18% over the course of the year. However reduced cash balances resulted in higher net debt and gearing fi gures.

At 30 June Futuris had net debt of $364.9 million and a gearing ratio of 24%, which compares to the corresponding fi gures of $202.0 million and 14% at the beginning of the year.

Conclusion

In conclusion, the Company’s results for 2007 have highlighted its capacity to perform in both favourable and unfavourable conditions.

Futuris’ rural and regional asset base combines a balanced mix of established market leading businesses, newer businesses building market share and earnings and exciting areas of opportunity. All made good progress in 2007, and have the market position, strategy and opportunities from which shareholders can reasonably expect ongoing growth.

Les Wozniczka

Chief Executive Offi cer

Futuris’ rural and regional asset base combines a balanced mix of established market leading businesses, newer businesses building market share and earnings and exciting areas of opportunity.

18

$ million unless otherwise indicated 2007 2006 2005 2004 2003 2002 2001 2000 1999 1998

Profitability

Sales revenue 3,228.5 3,355.8 3,174.7 2,707.3 2,464.3 2,145.8 1,968.4 1,759.7 1,482.2 1,211.6

Total revenue 3,366.9 3,422.6 3,232.0 2,791.0 2,844.8 2,537.6 2,177.7 1,832.6 1,570.5 1,469.7

Reported EBIT*

Rural Services1 56.3 65.8 26.8 19.0 152.3 47.3 101.0 86.7 72.6 46.2

Financial Services1 27.2 26.9 - - - - - - - -

Forestry 56.9 39.9 32.2 10.9 - - - - - -

Automotive Systems 9.5 16.3 99.3 19.5 19.3 30.7 22.4 21.1 21.4 25.3

Property 30.4 16.3 -3.3 7.5 0.3 4.8 1.4 - - -

Other -16.2 -8.4 -11.8 -5.0 -5.5 17.1 3.2 11.6 2.9 12.5

Total EBIT 164.1 156.8 143.2 51.9 166.4 99.9 128 119.4 96.9 84.0

Underlying** EBIT 164.7 157.1 131.3 96.1 84.0 91.9 88.6 108.9 91.4 69.9

Underlying** profi t before tax 124.7 118.2 106.4 86.1 65.0 71.2 65.2 81.1 81.0 63.6

Abnormal & non-recurring items -1.0 -0.9 -13.2 -44.2 82.4 8.0 39.4 10.5 12.2 72

Tax expense 20.5 -21.4 -47.9 -12.2 -38.5 -13.9 -18.1 -12.3 -19.6 -17.3

Minority interests -2.8 -9.0 -11.8 -5.9 -6.9 -2.9 -6.5 -5.1 -5.3 -4.3

Statutory profi t 100.7 87.4 58.6 23.8 102.0 62.4 80.0 74.2 68.3 114.0

Underlying profi t after tax 101.7 88.3 71.8 62.8 48.0 56.5 55.8 61.5 64.0 53.4

Cash flow from operating activities 85.0 127.4 -9.3 121.1 -55.6 113.8 188.8 64.7 75.0 34.8

Shareholder’s equity 1,186.5 1,227.9 970.3 961.2 843.6 749.1 723.0 692.4 612.0 569.4

Share information

Dividend per share (cents)

Interim 4.0 4.0 4.0 4.0 4.0 4.0 4.0 4.0 3.6 2.9

Final 5.5 5.0 5.0 4.0 4.0 4.0 4.0 4.0 3.6 3.9

Total 9.5 9.0 9.0 8.0 8.0 8.0 8.0 8.0 7.2 6.8

Dividend provided for or paid# 65.4 59.9 53.7 52.3 50.6 48.7 48.4 47.9 37.4 36.2

Hybrid distribution 8.9 1.8 - - - - - - - -

Share price^ ($ per share) 2.78 2.1 1.82 1.58 1.68 1.36 2.64 1.8 1.97 1.27

Market capitalisation^ 2,045 1,514 1,207 1,041 1,096 836 1,595 1,087 1,013 636

Number of shareholders^ 31,956 33,337 35,394 40,028 42,625 45,508 30,844 28,233 22,499 18,939

Ordinary shares on issue^ 735,640,128 720,911,089 663,243,696 659,138,427 652,293,766 614,870,776 605,136,707 604,159,207 514,065,747 500,151,804

Share issues Dividend Dividend Dividend Dividend Dividend Dividend Dividend Dividend Conversion Dividend reinvestment reinvestment reinvestment reinvestment reinvestment reinvestment reinvestment reinvestment of options reinvestment plan, plan, plan, plan, plan, private plan plan, plan, and notes, and bonus conversion conversion conversion conversion placement conversion conversion conversion 10% bonus share plans of options, of options of options of options conversion of options of options of options conversion Convertible notes institutional of options of options conversion placement and notes

Ratios and statistics

Reported earnings per share (cents) 13.9 13.1 8.9 3.6 16.2 10.2 13.2 12.9 12.2 21

Net tangible assets per share ($) 1.21 1.17 0.82 0.94 0.88 0.8 0.85 0.84 0.81 0.85

Gearing %† 24 14 23 1 0 15 33 37 51 49

Dividend payout ratio % 68 69 65 222 49 78 61 62 59 32

1 Prior to 2006 Financial services result reported within Rural Services

* Reported earnings before interest and tax (inclusive of non-recurring and abnormal items).

** Underlying profi t and earnings results excluding abnormal and non-recurring items (includes material profi t/loss on asset disposal)

# In respect of dividends declared for the fi nancial year.

^ As at 30 June.

† As measured by ratio of net interest-bearing debt/shareholders equity+net interest-bearing debt.

10 Year Summary Financial Results

19

Report of OperationsRural Services

Key financial results

$ million 2007 2006

Sales 2,309.5 2,364.5

Underlying EBITDA 64.3 63.5

Depreciation & Amortisation 15.2 11.6

Total underlying EBIT 49.1 51.9

Non-recurring items - 6.1

EBIT reported 49.1 58.0

Main features and outcomes

Sales revenue affected by drought, down 2%EBITDA up 1%Underlying EBIT 5% lower to $49 millionIncreased contribution from Wool, Real Estate and Financial Services distributionGrain business developing

•

••

•

•

Elders Rural Services’ underlying EBIT for the year of $49.1 million was 5% lower than the previous year’s result of $51.9 million. The movement in EBIT and sales is due to the impact of drought conditions on merchandise and meat and livestock operations. Contribution from wool, real estate operations and the distribution of fi nancial services products increased.

Operations

Elders’ business involves the delivery of an integrated suite of products and services to the rural and regional sector through an Australia-wide branch network of 298 branches. In addition, Elders has approximately 150 franchised real estate agencies, located in major capital cities.

Elders livestock agent Ray Norman (centre) fl anked by Albany Branch Manager Tom Marron (left) and Brad Preston, Territory Sales Manager, Donnybrook conducting Elders’ weekly trade sale at Albany. Elders is Australia’s largest livestock agent.

20

Business Development

Elders seeks to develop its business through a strategy which leverages the value of its network, relationships with approximately 100,000 farmers and the goodwill that the business has earned through 167 years of service. Business growth is being pursued through three avenues:

(1) increasing the value transacted through the network through increasing sales under existing product areas and developing new products;

(2) capitalising on Elders’ presence and goodwill as a regional service provider; and

(3) extending participation along the value chain upstream and downstream of the farm gate where appropriate.

Performance

Sales revenue of $2,309 million was 2% lower than in the preceding year.

The major factors in the movement were lower merchandise sales and lower revenue from wool operations. All other product areas recorded increased revenue.

Key features of Elders’ operations and performance in individual product areas is as follows:

Elders has six principal product areas: farm merchandise (supply of farm inputs), livestock production and marketing services, wool production and marketing services, real estate and banking and insurance, which are delivered via exclusive distribution agreements with Elders Rural Bank and Elders Insurance. Product streams are also being developed in grain accumulation.

Elders supports its network operations through participating in the value chain upstream and downstream of ‘the farm gate’ through its initiatives in meat and livestock, grain, horticultural produce, wool and farm inputs. These initiatives include:

• Supply chain activities whereby the Elders network provides a conduit for buyers seeking to source Australian agricultural produce that meets their specifi cations.

• Operations through which Elders participates in value-adding sectors of the supply chain. These initiatives include Elders involvement in feedlots, live export, sale of animal and plant genetics, conduct of wool auctions and exchanges in Australia and overseas, wool trading and processing (through BWK) and wool dumping and handling (Australian Wool Handlers joint venture).

• Participation in commercial operations such as HiFert to support competitive supply arrangements and share in earnings generated at the wholesale level of the farm services sector.

Elders is building its grain accumulation and sale operations as the progressive deregulation of the Australian grain sector permits. In 2007 Elders executed grain sales of 920,000 tonnes, 19% higher than the preceding year’s executed sales of 770,000 tonnes.

$ million 2007

Merchandise 1039

Meat & Livestock 526

Wool 423

Real Estate 88

Grain 176

Financial products distribution 40

Other 17

Sales Revenue

21

MerchandiseElders retails farm inputs including fertiliser, agricultural chemicals, animal health products, seed, fencing and other general merchandise used in farming operations. Elders also participates in wholesale fertiliser distribution through an equity-accounted 50% shareholding in HiFert.

Elders’ sales of merchandise fell by 7% to $1,039 million due to the contraction in expenditure on agricultural chemicals, fertiliser, seed and general merchandise caused by seasonal conditions.

Meat and LivestockElders’ meat and livestock operations include its traditional stock agent services and its initiatives which extend its presence in the supply chain within Australia and internationally.

Contribution from meat and livestock operations fell compared with the previous year due to the impact of the drought on livestock prices. Elders sold a total of 2.50 million cattle in 2007 compared with 2.51 million in 2006. Sheep volumes sold were largely unchanged at 14.08 million compared with 14.03 million.

Feedlot operations recorded another year of solid performance, but income from meat and livestock supply chain initiatives was below the levels of the previous year.

Wool Elders’ wool operations comprise its traditional agency operations and supply chain initiatives which extend from operation of independent auctions and wool exchanges, trading operations, handling, dumping and storage of greasy wool through to early stage wool processing.

Wool operations benefi ted from higher prices and sales volumes. Elders sold a total of 745,200 bales in 2007, compared with 725,300 in the previous

year. The average price received rose from $758.60 per bale to $915.10 per bale. Trading operations benefi ted from the stronger market conditions.

Elders continued the process of restructuring BWK’s wool processing operations to a status which is sustainable in current and anticipated textile market conditions. Commissioning of the wool plant relocated to the Yantai BWK joint venture was completed prior to year-end. Production by the 50:50 joint venture with Chinese wool processor Shandong Nanshan Industrial Company will commence in 2008.

Real EstateElders Real Estate comprises real estate services delivered through the network of Elders branches and stores throughout rural and regional Australia and the franchise of a further 150 real estate businesses in metropolitan locations under the Elders Real Estate brand. Property management provides an additional source of income.

Elders’ real estate operations increased their fi nancial contribution in 2007. Revenue generated rose by 14%, as increased residential sales and property management enabled Elders to offset lower broadacre sales.

Elders sold 1,837 broadacre and 6,455 residential properties compared with 2,022 broadacre, and 5,714 residential properties in the previous year. Elders had 13,015 properties under management at year-end.

GrainElders is building its grain accumulation and sale operations as the progressive deregulation of the Australian grain sector permits. In 2007 Elders executed grain sales of 920,000 tonnes, 19% higher than the preceding years executed sales of 770,000 tonnes.

The deregulation of the South Australian barley market was announced during the year, providing further market opportunity for the Company in 2008. The formation of a grain accumulation and marketing joint venture with Toepfer International Asia, announced subsequent to year-end, will increase the options and capacity available to Elders as it builds its position in grain.

Sustainability

EnvironmentElders’ feedlots at Charlton (Victoria) and Killara (New South Wales) are subject to local and state government environmental and animal welfare legislation.

Operations at both feedlots are quality assured under the National Feedlot Accreditation Scheme, which is independently administered and audited annually by Aus-Meat. In addition, the operations are conducted under the provisions of the Australian Code of Practice for the Welfare of Cattle in Beef Feedlots (1996) and the Australian Model Code of Practice for the Welfare of Animals - Cattle (1992).

No breaches of any of the relevant acts, codes of practice or accreditation schemes under which Killara or Charlton feedlots are approved and operate were reported during the year ended 30 June 2007 or to the date of this report.

Certain states have state and local government regulations that apply to saleyards owned and/or operated by Elders, in particular, in relation to effl uent run-off, dust and noise. These regulations vary from state to state and generally only apply to saleyards above a prescribed size.

No breaches of these environmental regulations were reported during the year ended 30 June 2007 or to the date of this report.

22

Units), was launched in conjunction with Southern Cross University with 70 participants. This program prepares targeted managers by further exposing them to a range of business concepts, disciplines and skills they require to operate effectively at a senior level.

The continuing development of the Company’s e-learning capability is reaching well beyond the induction and compliance arena into role specifi c training that includes best practice ‘blended learning’ solutions. The number of e-learning modules available rose by over 90% to over 120 during the year. Enrolments exceeded 100,000 and voluntary completion rates exceeded 65%.

Occupational health and safety was also incorporated into the Elders Compliance program to enable auditing of key OHS compliance activities and increased accountability. The strategic approach to safety management is being driven by an OH&S Strategic Plan developed during the year. Additional resources were committed to the development of risk reduction strategies.

The incidence of workplace injuries declined (from 444 to 428) during the year. However, a valued employee lost their life in the course of their duties as a result of a criminal offence committed within an Elders real estate property management offi ce. Elders supported staff members who were witness to the incident, with the resultant lost time being the reason for an increase in the lost time injury frequency rate during the year from 4.54 per million hours worked in 2006 to 5.40 in 2007.

Elders maintains a large motor vehicle fl eet as well as a dedicated forklift operation to conduct its operations throughout rural and regional Australia. A range of initiatives including driver training, vehicle effi ciency, vehicle

Elders’ merchandise operations are subject to state environmental regulations governing the storage, handling and transportation of dangerous goods such as agricultural and veterinary chemicals and fertilisers.

The majority of Elders’ merchandise operations are accredited under the Agsafe co-regulatory accreditation program. The program provides accreditation for premises and training and accreditation for individuals in the safe transport, handling and storage of agricultural and veterinary chemicals.

Licences for the handling and storage of dangerous goods are obtained and maintained by Elders wherever necessary as part of the Agsafe process.

No material incidents were reported in relation to the handling and storage of dangerous goods during the year.

Human ResourcesElders (comprising Elders Rural Services and Elders Financial Services Group) employed 4,430 people, at 30 June, representing 3,374 full time equivalent employees; virtually unchanged from the previous year’s level of 4,400 persons (3,475 full time equivalents).

Elders aims to employ and develop capable people within in a progressive and fair workplace. In 2007, $2.7 million was invested in a range of training initiatives designed to support and achieve these outcomes.

Over 90 staff started the Elders Frontline Management Program, now a full Cert IV status program and approved for 1 full unit credit at MBA level. This program gives the Elders manager an excellent grounding in the disciplines and processes they need to lead teams effectively.

The Senior Manager Program, a 2 year, Graduate Certifi cate program (4 MBA

benchmarking, detailed business performance reporting and accident and incident management systems support the safe operation of the vehicle fl eet.

CommunityAs a rural service organisation, Elders is committed to supporting the communities which it serves. Elders provides employment and a range of services to its network of branches throughout Australia. Elders‘ branches support local initiatives and charities and Elders’ staff members participate in community service organisations.

As noted by the Chairman, Elders made a $2.5 million, fi ve-year commitment to work in partnership with Landcare Australia during the year to help promote environmental sustainability amongst Australian farmers. Elders’ initiatives supported a number of charities including the Royal Flying Doctor Service, and the McGrath Foundation whichfunds breast care nurses primarily in the rural areas. Through Futuris, Elders was also a principal sponsor of the Australian String Quartet’s 2007 Regional Performance Program.

Elders made a $2.5 million, fi ve year commitment to work in partnership with Landcare Australia to help promote environmental sustainability amongst Australian farmers.

23

Financial ServicesMain features and outcomes

Underlying and reported EBIT up 1% to $27 millionEarnings before tax up 5%Introduction of new insurance distribution fee arrangementElders Rural Bank increased profi t contribution 15%Underlying improvement from insurance operations

•••••

Key financial results

$ million 2007 2006

Sales revenue 204.0 185.7

Reported EBIT 27.2 26.9

Insurance investment interest 12.3 11.6

Earnings before tax 39.5 37.6

OperationsElders Financial Services Group comprises the Company’s prudentially regulated operations in banking, insurance and wealth management.

Elders Rural Bank is the holder of APRA authorisation to operate as an authorised deposit taking institution under the terms of the Banking Act 1959. The bank is a 50:50 joint venture of Futuris and Bendigo Bank Limited. Elders Rural Bank concentrates on rural lending, with its products and services being distributed through the Elders network under an exclusive distribution agreement. The bank’s funding requirements are overwhelmingly sourced from retail deposits. Elders Rural Bank is reported as an equity-accounted joint venture within the Company’s fi nancial report.

Insurance operations consist of underwriting through Elders Insurance Limited, an APRA licensed insurer, and insurance agency services. Insurance products are distributed through the Elders network in a business model based on local presence and prompt local service. Elders’ insurance operations are supported by a franchise network of 207 agents and salespeople throughout Australia.

Wealth management operations are conducted through 32 licensed fi nancial advisors providing fi nancial planning and advice to rural and regional clients.

Elders Rural Bank

Elders Rural Bank contributed equity accounted profi t of $17.9 million in 2007, 15% above its previous year’s contribution of $15.5 million. The bank achieved strong growth in profi t and loans whilst maintaining credit quality.

Gross loans at 30 June of $3.2 billion were 14% higher than the 2006 comparative of $2.8 billion. Deposits rose by 12% to $3.2 billion compared with $2.9 billion in the previous year. The ratio of net non-performing loans was 0.36%.

Notwithstanding drought conditions, the bank has received upgrades in its credit rating and outlook since the 2006 year end. Standard and Poors’ upgrade of Elders Rural Bank’s outlook from ‘Stable’ to ‘Positive’ in the fi rst half was followed shortly after year-end with an upgrade of its short term and long term credit ratings. The upgrade resulted in Elders Rural Bank moving from its initial rating of BBB-A2 to BBB A3.

Insurance

Insurance operations contributed earnings before tax of $23.9 million compared with $24.6 million in the previous year. However, it should be noted the 2007 result incorporates $6 million of distribution fees introduced during 2007. Exclusion of these fees to enable a like-for-like comparison, results in earnings growth in 2007 of 27%.

Gross Written Premium of $427.8 million was 4% higher than the 2006 comparative of $413.2 million. Results benefi ted from lower than average claims, with natural disaster incidence being signifi cantly lower than in 2006. Net loss ratio for the year was 68.0% compared with 70.1% in 2006.

Interest earned on insurance reserves was $12.3 million compared with $11.6 million in the previous year.

Right: Peter Hassell, Elders District Banking Manager, Albany, Western Australia (left) with clients, the Smith Family of Baboo Pastoral Company at Green Range Western Australia.

24

Financial results from processing operations (ITC Timber) improved signifi cantly, rising from an EBITDA contribution of $0.3 million to $3.8 million. The improvement follows successful integration of new resource and processing assets and restructuring of operations. ITC Timber increased sales revenue from $49.6 million to $61.5 million.

Equity accounting of ITC’s share of Forest Enterprises Australia’s (FEA) and the SmartFibre joint venture contributed $6.4 million to ITC’s earnings compared with $5.5 million in 2006. ITC increased its shareholding in FEA to 30.7% during the year.

Sustainability

EnvironmentITC’s approach to its environmental responsibilities form a key component of the Company’s forward strategy. No signifi cant breaches of relevant environmental legislation or regulations occurred during the period covered by this report.

ITC holds ISO14001:1996 accreditation in respect of its environmental management system for its Forestry division and is pursuing certifi cation to Safety Standard AS4801.

The Company was successfully audited under its Forest Stewardship Council (FSC) certifi cation during the year. Approximately 80% of the Company’s plantations under management are now FSC certifi ed. ITC is also pursuing FSC certifi cation for its Queensland plantations.

ITC continued its corporate partnership with leading environmental organisation, WWF-Australia. The partnership was established to encourage sustainable forestry management practices and has seen the establishment of the Australia Forest and Trade Network (AFTN) a group of like-minded producers and

ITC is also engaged in the export of woodfi bre and operation of associated facilities. In Tasmania, ITC is a 50% interest holder in the SmartFibre joint venture with FEA. In Western Australia, ITC is also a 50% interest holder in the Plantation Pulpwoods Terminals joint venture, which owns and operates the 1 million tonne per annum capacity Albany Chip Terminal handling and loading facility in Albany, Western Australia.

ITC harvested and sold woodfi bre from approximately 3,000 hectares of plantations located in the Bunbury and Albany regions during the year.

Processing operations involve the harvest, sawmilling and value-adding of regrowth native timber under sustainable management practices in Victoria and Tasmania.

Financial Results

ITC’s underlying EBIT rose from $39.9 million to $56.9 million in 2007 with higher earnings being generated by all operations. Revenue increased by 19% to be $200.8 million.

Plantation operations benefi ted from higher MIS sales, a 9,000 hectare expansion in areas under management and improved harvest and land valuations. A 5% increase in the benchmark price for Australian plantation grown woodchip was negotiated with Japanese buyers during the year. The new price has increased the premium for certifi ed plantation grown product and is indicative of favourable near term demand outlook for ITC’s end-product.

ITC’s 2007 MIS product offering achieved sales of $61.5 million, which will fund the planting of an estimated 12,700 hectares of pulpwood, teak, red mahogany and sandalwood. Approximately 56% of the 2007 MIS sales will be carried forward and recognised as revenue in future years.

ITC contributes to the communities where it operates through support for local sporting, cultural and charity events and organisations.

Forestry

Main features and outcomes

43% increase in EBITPlantation estate increased to 160,000 hectaresMIS sales up 30% to $61.5 millionImproved returns from processing5% price increase in woodchip price

••

•

•

•

Key financial results

12 months to 30 June

$ million 2007 2006

Revenue 200.8 168.6

EBITDA 61.9 43.5

Depreciation & Amortisation 5.0 3.6

EBIT 56.9 39.9

Non-recurring items - -

Reported EBIT 56.9 39.9

Operations

ITC is an integrated forestry and timber company engaged in forestry management, the harvest, handling and export sale of woodfi bre and the sustainable production of value-added hardwood timber products.

Plantation operations consist of hardwood forest, managed on behalf of investors, who have funded the estate through subscription to managed investment schemes (MIS) or through direct investment. Plantations are predominantly eucalypt and eucalypt hybrids, with smaller plantings in sandalwood, teak and red mahogany. ITC had 160,000 hectares of plantation under management at 30 June. Plantations are located in southern Western Australia, Kununurra, the Green Triangle region and northern Queensland.

25

purchasers of sustainable forest products. Through the AFTN, ITC and WWF-Australia are working together to develop and promote strategies for best practice sustainable forest management and enhancing consumer and market awareness of sustainable, forest products.

CommunityITC contributes to the regional communities where it operates through participation, and support for local sporting, cultural and charity events and organisations. ITC provided in-kind support and sponsorship for over 50 events and organisations in 2007. Through Futuris, ITC was also a sponsor of the Australian String Quartet’s 2007 Regional Performance Program.

Human resources and safety managementITC had 389 employees as at 30 June compared with 332 at the beginning of the year.

ITC’s safety performance standards are benchmarked against the Australian Safety Standards. ITC recorded 58 lost time injuries during the year.

Right: 8 year old eucalypts at ITC’s Wimbush plantation, near Albany, Western Australia.

26

Futuris’ telecommunications interests comprise its shareholding in Amcom Telecommunications Limited, its 50% interest in the OPEL joint venture and retail of telecommunications services conducted through the Elders network.

Financial results from these operations are included under the category of Investment and Other in the 2007 accounts, but will be reported separately from 2008 onwards.

Amcom Telecommunications

Amcom owns and operates telecommunications fi bre in Perth, Adelaide and Darwin for a client base that principally consists of government and corporate users and other carriers. Amcom is the second largest fi bre owner in Perth and Adelaide.

Amcom is also a 19.98% shareholder in iiNet, Australia’s third largest internet service provider. During 2007 Futuris increased its shareholding in Amcom to 49.1% following the provision of equity backed fi nance to Amcom to fund the acquisition of its shareholding in iiNet.

Amcom is listed on the ASX under the ticker code AMM.

OPEL Networks

OPEL is a 50:50 joint venture of Futuris and Optus, formed to bid for federal funding to build and operate a new broadband network for rural and regional Australia.

In June OPEL was advised that it was the sole successful tenderer for funding and would be offered a total of $958 million (comprising $600 million from the Broadband Guarantee Infrastructure Program and further funding of $358 million) to build its proposed network. The initiative is subject to the completion of funding and joint venture agreements.

Preparation of the bid and establishment of the OPEL joint venture resulted in expenditure of $9.5 million which has been recorded as a non-recurring item in the 2007 accounts.

It is proposed that OPEL build and operate a broadband network for a period of 10 years commencing in the current fi nancial year. The OPEL network, which has a projected capital cost of $1.3 billion, will use a combination of ADSL2+ and wireless technologies to service a network footprint that takes in approximately 9 million premises in rural, regional and outer metropolitan regions over 600,000 square kilometres. OPEL’s primary market will be the majority of underserved homes and businesses within rural and regional Australia that are currently unable to access sustainable metro-comparable broadband service.

OPEL’s proposal is to operate an open access wholesale network providing primary voice and data services to retailers that will include Optus, Elders and local independent service providers. Network build is forecast to take two years to complete. OPEL will be reported within the Futuris accounts as an equity accounted joint venture.

Main features and outcomesOptus Elders joint venture wins Broadband Connect fundingIncreased shareholding in Amcom

•

•

Telecommunications

OPEL’s primary market will be the majority of underserved homes and businesses within rural and regional Australia that are currently unable to access sustainable metro-comparable broadband service.Senator the Hon Helen Coonan, Minister for Communications, Information Technology and the Arts (centre), fl anked by the Prime Minister, the Hon John Howard, Deputy Prime Minister, the Hon Mark Vaille, with Futuris CEO Les Wozniczka (far right), General Manager, Elders Telecommunications, Jason Horley (second from right) and staff of Elders Goulburn branch at the announcement of the OPEL joint venture successful tender.

27

Automotive

Key fi nancial results

12 months to 30 June

$ million 2007 2006

Sales 329.9 457.2

Underlying EBITDA 27.7 40.3

Depreciation & Amortisation 18.2 19.5

EBIT

Futuris Automotive 10.7 16.0

Associates (equity acc) (1.2) 4.7

Underlying EBIT 9.5 20.8

Non-recurring items - (4.5)

Reported EBIT 9.5 16.3

Futuris Automotive is engaged in the design, development and manufacture of interior systems (seat systems, seat hardware, fl oor carpets, headliners, steering columns, pedal assemblies and after market products) for passenger vehicles.

Operations are conducted in Australia, under long term contracts to local vehicle manufacturers including General Motors Holden and Ford Australia, and in China, through the Futuris Automotive Interiors (Anhui) joint venture and in South Africa through a joint venture with Feltex. The Chinese joint venture is contracted to supply seating for emerging Chinese manufacturer Chery Automobile Co. Futuris Automotive also has a US design offi ce in Detroit, Michigan.

Futuris Automotive also holds a 35% interest in Air International Global Thermal Systems, a supplier of passenger vehicle thermal systems to the Australian, US and Chinese automotive sectors.

Financial results

Futuris Automotive recorded lower sales revenue in 2007 than the previous year due to the transfer of Rail and Bus reporting (which contributed sales of

$66 million in 2006) and reduced demand from Australian passenger vehicle producers. Sales revenue from Interior Systems was 15% lower due to the lower demand levels. Results from the Rail and Bus operations are now reported within the Investment and Other segment.

EBIT from Interior systems operations was also adversely affected by costs of $9.0 million incurred in restructuring during the year to achieve effi ciency through plant consolidation.

Equity accounted associates (which includes Global Thermal and Futuris Automotive Interiors (Anhui)) contributed a loss of $1.2 million. The loss is attributable to a lower contribution from Global Thermal and start up of the Anhui joint venture.

Business development

Consolidation of Australian operations at the Edinburgh Park and Campbellfi eld plants was substantially advanced during the year. The restructuring, which involves the relocation and outsourcing of plant functions previously performed at Golden Grove is scheduled for completion shortly after the 2008 fi rst half.

Futuris Automotive added interior trim to its product offering during the year, and is supplying door and headliner trim to Australian vehicle manufacturers.

In China, the Automotive Interiors (Anhui) Company Limited joint venture completed construction of a production facility for the production of seating to fulfi ll its supply contracts with Chery Automobile Co. The facility was completed in the fi nal quarter of the year and has commenced operations. Production volumes are forecast to escalate over the course of 2008.

Sustainability

Futuris Automotive conducts its operations within the parameters of management plans to ensure its day-to-day activities are completed safely and in an environmentally and socially responsible manner.

EnvironmentFuturis Automotive’s key manufacturing plants in Australia are all accredited to ISO 14001 certifi cation.

The organisation’s operating facilities are subject to relevant environmental protection legislation and regulation in the areas in which they operate. There were no reportable incidents or breaches of applicable environmental legislation arising from Futuris Automotive’s operations during the year.

SafetySafety is managed through a series of safety committees at each operation which report to senior management on performance. During the 12 months to 30 June 2007, Futuris Automotive recorded a lost time injury frequency rate of 8.5 per million hours worked compared to the preceding year’s rate of 20 per million hours worked.

Human ResourcesFuturis Automotive employed a total of 861 people in Australia at 30 June compared with 1,085 at the same time in the previous year. This reduction was due to lower production volumes from Australian customers and operational restructuring initiatives undertaken.

As of the same date, Futuris Automotive employed a further 220 people in China as at 30 June (65 people as at 30 June 2006) with the increase being attributable to the commencement of operations by the Anhui joint venture. Futuris Automotive also employed 3 people in the US.

Main features and outcomesLower sales due to reduced demand Plant consolidation advancedNew plant constructed and commissioned in China

•••

28

Board of DirectorsMr Stephen Gerlach LLB Chairman Mr Gerlach age 62 - Non-Executive member of the Board since November 1996 and Chairman since July 2003. He chairs the Company’s Nomination & Prudential and Remuneration Committees. Formerly Managing Partner of Adelaide legal fi rm Finlaysons, Mr Gerlach has extensive experience as a corporate advisor and company director. Mr Gerlach also holds directorships at Santos Limited (Chairman), Santos Finance Ltd (Chairman) and Challenger Listed Investments Ltd. He is the Chairman of Foodbank SA Inc., a Director of Foodbank Australia Ltd and a Trustee of the Australian Cancer Research Foundation. During the past three years, Mr Gerlach served as a director of the following listed companies: Beston Pacifi c Vineyard Management Limited (1997-2005) and Southcorp Limited (1994-2005). Mr Gerlach is a resident of South Australia.

Mr Charles Bright, BA MA(Oxon) Mr Bright age 62 - Non-Executive member of the Board since May 2002. He is a member of Nomination & Prudential Committee and a director Integrated Tree Cropping Ltd, APT Projects Limited and ITC Project Management Limited. Mr Bright has over 30 years’ experience in investment banking with positions including Chairman of Potter Warburg Securities and Head of Corporate Finance for HSBC in Australia. Mr Bright is also a director of Australian Agricultural Company Limited, Tassal Group Limited and Webster Limited. During the past three years, Mr Bright served as a director of Australian Plantation Timber Limited (2002-2005). Mr Bright is a resident of Victoria.

Dr James Charles Fox BE, MEngSci, PhD Dr Fox age 55 - Non-Executive member of the Board since July 1985. He is a member of Remuneration and Nomination & Prudential Committees. Mr Fox has extensive experience in the development and operation of technology-based product businesses in international markets. He was the Managing Director of Vision Systems Limited from December 1993 until December 2006 when an on-market takeover of the company by USA-based Danaher Corporation was completed. He is a director of Air New Zealand Ltd and TTP Group p/c (UK). Mr Fox is a resident of Victoria.

Mr Leslie Peter Wozniczka MBA, BSc(Hon) Mr Wozniczka age 52 - Executive Director of the Board since January 2002. He is the Chief Executive and Managing Director of the Futuris Group. He is a member of the Remuneration and Nomination & Prudential Committees and a director on all main operating subsidiary boards including: Elders Australia Ltd, Elders Financial Services Group Pty Ltd, Elders Insurance Ltd, Integrated Tree Cropping Limited and Futuris Automotive Group Ltd. Prior to joining the Board, Mr Wozniczka served in the role of Chief Operating Offi cer of Futuris from January 1999. Prior to joining Futuris, Mr Wozniczka managed private investment interests and held senior management positions within the corporate service and investment banking sectors including the position of Director Corporate, Potter Warburg. Mr Wozniczka also holds directorships in Australian Agricultural Company Limited, Hi Fert Pty Ltd, Amcom Ltd and Forest Enterprises Australia Limited. Mr Wozniczka is a resident of South Australia.

Mr Graham Walters AM, FCA Mr Walters age 65 - Non-Executive member of the Board since January 2002. He is Chairman of the Audit Committee and a Director of Elders Insurance Ltd, Elders Insurance Brokers Pty Ltd, Elders Trustee Ltd and Elders Financial Services Group Pty Ltd. Mr Walters has extensive experience in accounting, having formerly held roles as Chairman of Partners at KPMG South Australia and Member of the National Board of KPMG. Mr Walters also holds directorships of Australian Rail Track Corporation Limited, Minelab International Pty Ltd (Chairman) and Royal Automobile Association of South Australia. He is also Chairman of the South Australian Executive Committee of Westpac Banking Corporation. Mr Walters is a resident of South Australia.

Mr Anthoni Salim, B Bus Mr Salim age 58 - Non-Executive member of the Board since March 2003. He is President and Chief Executive Offi cer of Salim Group, one of Indonesia’s leading business groups. Salim Group holds extensive interests in the importation, manufacture and distribution of food and foodstuffs. Mr Salim is a director of First Pacifi c Company Limited, Chief Executive of PT Indofood Sukses Makmur and a member of the advisory board for Allianz Group, one of the world’s leading insurance groups. Mr Salim is a resident of Jakarta, Indonesia.

Mr Ian MacDonald SF Fin Mr MacDonald age 53 – Non-Executive member of the Board since November 2006. He is a director of Elders Insurance Ltd, Elders Rural Bank Ltd, Elders Insurance Brokers Pty Ltd, Elders Trustee Ltd and Elders Financial Services Group Pty Ltd. He is also a member of the Australian Institute of Company Directors and Senior Fellow of Financial Services Institute of Australasia. Mr MacDonald has had an extensive career in banking both in Australia and Internationally, having served National Australia Bank Ltd for 34 years including performance of a number of senior management roles, including Chief Operating Offi cer, Yorkshire Bank, Executive General Manager, Financial Services Australia, and Group Chief Information Offi cer. Mr MacDonald is a director of Arab Bank Australia Ltd and CPT Global Ltd. Mr MacDonald is a resident of Victoria.

Mr Walter Hubert Johnson ASA (Deputy Chairman) Mr Johnson age 64 - Deputy Chairman and has been a Non-Executive member of the Board since 1981. He is also a member of the Audit Committee. Mr Johnson has extensive accounting and business experience in a number of areas including primary production, forestry management and saw-milling and has served on the board of a number of public and private companies. Mr Johnson is a resident of Western Australia.

Mr Raymond G Grigg, F.SAE-I., F.A.I.C.D. Mr Grigg age 66 - Non-Executive Member of the Company since February 2004. He is also Chairman of Futuris Automotive Group of companies, and a member of Futuris Audit committee. Mr Grigg has extensive experience in senior management within the automotive industry, having joined the Board following a 47 year career with General Motors Corporation where Mr Grigg held a number of senior positions both in Australia and overseas. At retirement Mr Grigg was President and Representative Director, General Motors Asia Pacifi c (Japan) as well as Chairman, CEO and Representative Director of GM Japan. Mr Grigg is a non-executive director of Adtrans Group Limited and a Board member of the Royal Automobile Association of SA Inc and Bedford Industries Ltd. Mr Grigg is a resident of South Australia.

Company Secretaries - Mr Michael Peter Sadlon LLB Mr Sadlon has been Director, Corporate for Futuris since late 2005 and Company Secretary since July 2000. Previously Mr Sadlon was Legal Counsel for Futuris and Manager, Legal Services for the Elders Group. Mr Sadlon holds a Bachelor of Laws from the University of Adelaide and, prior to joining Futuris, worked in private commercial practice.Ms Sonya Catherine Furey BEc(Acc) LLM FCA Ms Furey was appointed Group Tax Manager in December 1999 and Company Secretary in December 2002. Prior to joining Futuris, Ms Furey held a management role at KPMG, Corporate Tax Consulting. Ms Furey holds a Bachelor of Economics (Accounting) from the Flinders University of South Australia and a Masters of Laws (Corporate and Commercial) from the University of Adelaide. She is also a Fellow of the Institute of Chartered Accountants and a Fellow of the Taxation Institute of Australia.

29

Corporate Governance

This statement discloses the key elements of the Company’s governance framework during the reporting period and to the date of this report.

The Board has in place a charter that consolidates the principles, policies and practices of its governance framework as refl ected in this statement (“Board Charter”).