Download - Annual report 2008 Volito Eng

VO

LITO

AB

| AN

NU

AL

RE

PO

RT

200

8

Volito AB, Södra Förstadsgatan 4, SE-211 43 Malmö tel +46 40 660 30 00 fax +46 40 660 30 20 e-mail [email protected] internet www.volito.se corporate identity number 556457-4639

Volito AB is an investment company operating within Aviation, Real Estate and Structured Finance. The company creates value through

long-term, active ownership based on genuine expertise within its lines of business. Value growth is generated both through current earnings and the increase

in value of the company’s investments.

Volito AB | GROUP PRESENTATION ANNUAL REPORT 2008

2003 Anita Nilsson Billgren

2004 K G Nilsson

2005 Martin Wickström

2006 Anders Österlin

2007 Björn Wessman

AddressesVolito ABSödra Förstadsgatan 4, SE-211 43 MalmöTel: +46 40 660 30 00 Fax: +46 40 660 30 20www.volito.se

Volito Aviation ABSödra Förstadsgatan 4, SE-211 43 MalmöTel: +46 40 660 30 00 Fax: +46 40 30 23 50www.volito.aero

Volito Fastigheter ABSödra Förstadsgatan 4, SE-211 43 MalmöTel: +46 40 664 47 00 Fax: +46 40 664 47 19www.volitofastigheter.se

Scandinavian Aviation Academy ABHässlögatan 20, SE-721 31 VästeråsTel: +46 21 80 28 00 Fax: +46 21 80 28 90www.bfsaa.se

Nordkap Bank AGThurgauerstrasse 54, CH-8050 Zürich, SchweizTel: +41 1 306 49 10 Fax: +41 1 306 49 11www.nordkapbank.com

CTT Systems AB (publ)Box 1042, SE-611 29 NyköpingTel: +46 155 20 59 00 Fax: +46 155 20 59 25www.ctt.se

Peab AB (publ)SE-260 92 FörslövTel: +46 431 89 000 Fax: +46 431 45 19 75www.peab.se

y bird painting essentially serves a

romantic tradition that is as equally

based on consciousness and enligh-

tenment as it is on the pursuit of the idyllic

and the escape from reality, and whose ideal

of beauty springs from the magical moment

of perfection. But, in a style that denounces

sentimentality and pathos as much as irony

and reflection lies the instrument that is

intended to overcome the gulf between the

painting’s elementary denominators, time

and timelessness.

Emanuel Bernstone, February 2009

Emanuel Bernstone was born in 1973

in Karlskrona. He trained at the Art

Academy in Düsseldorf, 1997-2003.

Following his studies, he has had a

number of exhibitions both in Sweden

and abroad. His work has been exhibi-

ted in cities such as Stockholm, Malmö

and Gothenburg. Abroad, his work has

been seen in Norway, Denmark,

Germany and the USA. He currently

lives and works in Berlin.

M

The Volito Group’s strength stems from the experience and dynamics of its staff and owners, and the capacity to adapt the business to new conditions” Johan Lundsgård CEO and President, Volito AB

Dynamics& experience

– THE VOLITO GROUP –

TH

E G

RO

UP

4

Business concept, structure and objective

VOLITO AB

AVIATION REAL ESTATE STRUCTURED FINANCE

V olito AB is a privately- owned investment company based in Malmö. The company runs operations in the areas of Aviation, Real Estate and Structured Finance. Volito structures its activities in operating subsidiaries and in other investments within its three business areas.

The Aviation business area covers the leasing of commercial jet aircraft, mainly Boeing 737 and Airbus 319/320, in the narrow-body segment. The leasing business is owned by the wholly-owned subsidiary, Volito Aviation AB, as well as by the partly owned (50%) VGS Aircraft Holding Ltd. The two companies are managed by Volito Aviation Services AB, which is 80% owned by Volito.

Aviation also includes SAA AB based in Västerås. The SAA Group runs training courses mainly for pilots, but also for other personnel in the aviation industry, and has operations in Sweden and the USA.

The Aviation business area also includes Volito’s holding in CTT Systems AB (publ). CTT develops and markets humidity control systems for commercial aircraft. The company’s most important products are the Zonal Drying and Cair brands. CTT Systems is listed on OMX Nordic Exchange Stockholm.

The Real Estate business area includes the wholly-owned Volito subsidiary, Volito Fastigheter AB. Volito Fastigheter focuses primarily on commercial real estate in the Malmö region. Real Estate also includes

Volito’s ownership in Peab AB (publ). Peab is active in the construction and civil engineering field and listed on OMX Nordic Exchange Stockholm.

Structured Finance encompasses Volito’s ownership in Nordkap Bank AG. Nordkap Bank offers structured financing solutions, and its customers are primarily in developing regions of the world. The bank runs its operations from Zürich, Switzerland.

Volito’s overall objective is to create long-term, balanced value growth for the shareholders. In 2008 Volito’s results were negatively affected due to the considerable fall in the stock market. Adjusted equity during the year has decreased by 26.2% (+21.7%). The Group’s adjusted equity on 31 December 2008 amounted to SEK 1 121.0 million (1 518.1).

5T

HE

GR

OU

P

2008 in brief• The Volito Group’s profit/loss before tax amounted to SEK -28.4 million (600.9).

• The Volito Group’s adjusted equity decreased by 26.2% to SEK 1 121.0 million (1 518.1).

• VGS Aircraft Holding Ltd (VGS) generated a profit before tax of USD 18.4 million in its first financial year.

• SAA returned to profitability after two loss-making years and reported a profit before tax of SEK 1.3 million (-5.0) for the full year.

• Volito has further increased its ownership in CTT Systems AB (publ) and owned 16.2% of the company at year-end.

• Volito Fastigheter reported one of its best profits ever before tax of SEK 48.1 million (27.0).

• Peab AB (publ) made an offer for Peab Industri AB (publ) during the year. After the implemented acquisition, Volito owns 5.24% of the capital and 2.54% of the votes in Peab AB (publ).

• Nordkap Bank reported a profit before tax for 2008 of CHF 1.5 million (11.5).

• The financial turbulence and falling share prices during the year have in general negatively affected the business climate in which Volito is active. In view of this, it is satisfying to note that the majority of Volito’s businesses have generated positive results.

• Johan Lundsgård took up his appointment as the new CEO and President on 1 September.

6

1 500

1 250

1 000

750

500

250

99 00 01 02 03 04 05 06 07 08

D espite the good results from the business area’s operations, Volito’s adjusted equity was negatively affected due to the falling share prices. On 31 December 2008, the Volito Group’s adjusted equity amounted to SEK 1 121.0 million, which represents a reduction of 26.2%.

Business area AviationThe global aviation industry had a troublesome year in 2008. In a changing and tough market, Volito Aviation has continued to generate good results. VGS Aircraft Holding Ltd (VGS), the Ireland-based aircraft leasing company jointly-owned with Goldman Sachs’, completed its first full financial year in 2008. During 2008 the company invested a total of USD 155 million in 6 aircraft that all match VGS’s criteria in terms of aircraft assets. In the same period VGS sold 8 aircraft and an aircraft engine for USD 82 million. The sales have generated combined capital gains of USD 6.4 million while also reducing the average age of the company’s remaining fleet. The sales were also made with an aim to decrease the exposure of VGS

relating to certain lessees and in this way reduce the risks in the company’s aircraft portfolio. The aircraft sold have also in part been models that do not fit in with the future strategy of VGS that was established when VGS was formed in 2007.

As a result of the worsening business climate, Volito Aviation implemented a cost-saving programme in autumn 2008 that aimed to cut costs and improve competitiveness.

The aviation school, SAA, has improved its results during the year and reported a profit. This positive development stems from a general improvement in quality within the business and the sale of Swiss company, Twinair.

CTT Systems received further orders in 2008 from both OEMs and airlines, and thereby strengthened its base for the coming years. However, an improvement in results will be deferred due to the delays that have affected Boeing in the launch of the new B 787. During the year Volito increased its ownership in CTT and

at year-end 2008 owned 16.2% of the votes and capital.

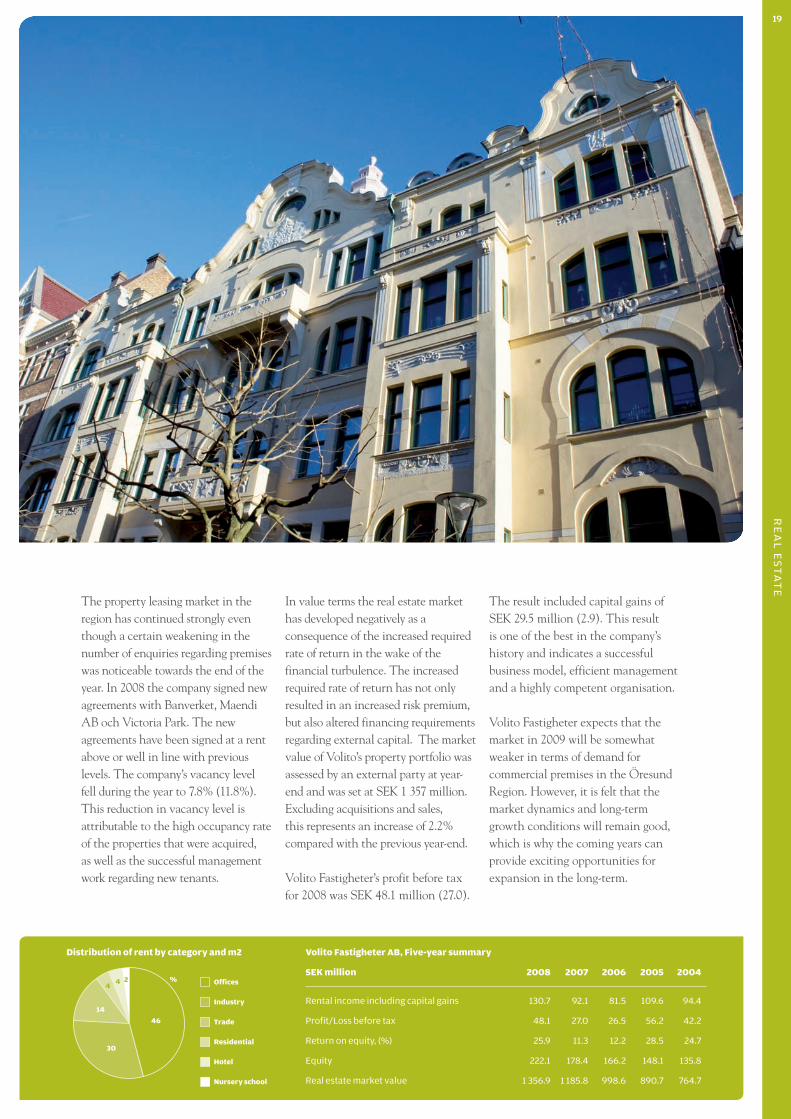

Business area Real EstateVolito Fastigheter’s result for 2008 were one of its best since the company was established in 1997. The company has both acquired and sold properties during the year. All transactions have had a strategic aim. The property leasing market in the Öresund Region continues to be strong, but property values have fallen as a result of the increased required rate of return in the wake of the financial crisis.

In the transactions carried out in 2008, Volito Fastigheter focused solely on Malmö and the surrounding area. My assessment is that Malmö will continue to be a highly attractive city seen from the perspective of the entire Öresund Region. Through an internal transaction the Delfinen property on Södra Förstadsgatan has been transferred from the Parent company, enabling Volito to bring together its property portfolio solely within the Volito Fastigheter Group – a structure that enhances the

Comments from the CEOThe financial turbulence and falling share prices that have been apparent during the year have had a generally negative impact on Volito’s business climate. In view of this, it is satisfying to note that the majority of Volito’s businesses have generated positive results.

SEK million The Volito Group, adjusted equity

7T

HE

GR

OU

P

efficiency of management, increases transparency and improves the business ratios within the Volito Group.

The property leasing market in the region has continued strongly even though a certain weakening in the number of enquiries regarding premises was noticeable towards the end of the year.

The real estate market has developed negatively during the year in value terms as a consequence of the increased required rate of return that the financial crisis has brought with it. The rise in required rate of return has not only resulted in an increased risk premium, but also altered financing requirements regarding external capital.

Volito Fastigheter expects that the market in 2009 will be somewhat weaker in terms of demand for commercial premises in the Öresund Region. However, it is felt that the market dynamics and long-term growth conditions will remain good, which is why the coming years can provide exciting opportunities for expansion from a long-term perspective.

Volito’s holdings in Peab AB (publ) and Peab Industri AB (publ) have developed positively during the year regarding the respective operations, but negatively in terms of value development.

Both Peab and Peab Industri had a high level of activities during the year which led to increased turnover(+8%) as well as operating

profit (+9%) for the whole of Peab now being consolidated as one group. The company’s order book continue to look robust, however a decline in incoming orders was noticeable in the latter part of the year.

The board of Peab decided in October to make an official bid for all the shares in Peab Industri. Three shares in Peab were offered for two shares in Peab Industri. The companies, which were split into two units in 2007, were consequently brought together again to form a joint group.

The construction industry was hit hard in terms of value development during the financial crisis of autumn 2008. During 2008 Volito’s holding in the two Peab companies lost 57% in value compared with the start of the year. As a comparison, the OMX

All Share Index fell by 40% in the same period.

Business area Structured FinanceNordkap Bank continued to develop positively during the first three quarters of 2008. The financial crisis and the emerging recession in 2008 have so far had only a small effect on the company. In the course of the fourth quarter a handful of customers suffered liquidity problems which resulted in increased provisions for potential credit losses.

The financial crisis and start of the recession have had fairly limited effects on the Volito Group’s results in 2008. We see a considerably weakened business climate in 2009 and the consequences for Volito are hard to predict at the present time. The Group is focusing on creating and maintaining cash flows from the business areas with an aim to ensure readiness to meet a weakening business climate.

Despite the concerns that mark the world economy at present, I have confidence in meeting the challenges that Volito faces. In conclusion, I would like to thank our customers, staff, business partners and owners for their good cooperation.

Johan LundsgårdCEO and PresidentJohan LundsgårdCEO and President

Definitions

Return on equityProfit/loss after tax in relation to average equity

Adjusted equityEquity and surplus values in real estate and listed shares with reduction for deferred tax

Return on adjusted equityChange in value on adjusted equity

Adjusted equity ratioAdjusted equity in relation to total assets including surplus values

“ The Group is focusing on creating and maintaining cash flows from the business areas with an aim to ensure readiness to meet a weakening business climate.“

The Volito Group, Ten-year summary

SEK million 2008 2007 2006 2005 2004 2003 2002 2001 2000 1999

Profit/Loss before taxes -28.4 600.9 144.5 79.0 30.7 70.7 -6.5 -13.7 80.6 77.8

Adjusted equity 1 121 1 518 1 273 935 663 563 497 496 445 365

Return on adjusted equity, (%) -23 22 37 42 19 14 0 12 21 39

Equity ratio, (%) 45 52 26 23 26 25 25 34 51 43

Assets 2 930 2 748 4 010 3 575 2 267 2 029 1 792 1290 736 754

8

9A

VIA

TIO

N

– VOLIT O AV I ATION –

Trust & execution

We earn our customers trust through diligent execution” Siggi Kristinsson CEO, Volito Aviation

300

250

200

150

100

50

A V I A T I O N A B

10

03 04 05 06 07 08

V GS Aircraft Holding (Ireland) Ltd (VGS), the Ireland-based aircraft leasing company jointlyowned with Goldman Sachs, completed its first full financial year in 2008. During the year the company invested a total of USD 155 million in 6 aircraft that are all well suited to fit VGS’s criteria in terms of aircraft assets. These were mainly Airbus 320-200 aircraft with an average age of around 6 years, which has reduced the average age of the VGS aircraft portfolio.

In the same period VGS sold 8 aircraft and an aircraft engine for USD 82 million. The sales have generated total capital gains of USD 6.4 million while also reducing the average age of the company’s remaining fleet. The sales were also made with an aim to decrease the exposure of VGS relating to certain lessees and in this way reducing the risks in the company’s

aircraft portfolio. The aircraft sold were also in part models that do not fit in with the future strategy of VGS that was established when VGS was formed in 2007.

At year-end VGS had an aircraft fleet of 41 aircraft with a book-value of USD 805 million. Liabilities linked to the fleet amounted at year-end to USD 574 million. The percentage of narrow-body aircraft in the fleet is 100% and there is a good spread of risk in geographical terms. The company has lessees in areas such as Europe, Central and South America, North America and Asia.

After the year’s completed transactions, VGS has a strong financial position and at year-end had liquid funds of USD 28.8 million. Furthermore, the company is now free of obligations regarding acquisitions and has an aircraft fleet that generates

a strong operative cash flow. In view of this background the company sees many interesting opportunities in 2009 in a market that for the foreseeable future will be characterised by downward pressure on prices and companies with a need to sell assets.

Volito Aviation Services AB (VAS) is the service and management company that manages the VGS fleet and the fleet that is wholly owned by Volito Aviation (see under summary ”Aircraft fleet, 31 December 2008”). The company has worked during the year to further refine its internal routines and processes. In addition, VAS was audited by the consulting firm SH&E in 2008. This was done to place yet another seal of quality on the organisation and to strategically prepare the company to also serve customers outside the Volito Group.

A year of dramatically altered market conditionsThe global aviation industry experienced a year of upheaval in 2008. The runaway oil prices in the first half of the year together with the financial turbulence in the autumn have led to extremely tough conditions for the world’s airlines. Volito Aviation has continued to generate good results under these conditions – a testament to the quality of the business plan.

SEK million Profit/Loss before tax

Direct and straight dealing, with a Swedish flavour. Great to experience this in the airline business” Pieter van Dijk, Transavia

11A

VIA

TIO

N

“I feel privileged to work with such a dedicated and professional team as my colleagues at VAS. The fact that some of the sales we carried through during the year were made in November, in the toughest possible market conditions, shows the organisation’s

strength and ability to adapt itself to new circumstances,” says Sigurdur Kristinsson, CEO of Volito Aviation.VGS made a profit before tax for 2008 of USD 18.4 million. This result represents a return on equity of 19%. The Volito Aviation AB Group

(which reports VGS as an associated company) made a profit before tax for 2008 of SEK 82.5 million (356.9) and a return on equity of 9.9% (54.7%). The results for 2007 included SEK 289.2 million that was related to the VGS transaction.

Volito Aviation AB, Five-year summary

SEK (USD) million 2008 2007 2006 2005 2004

Revenues 163.7(24.9) 321.6 (46.8) 396.1 (52.9) 210.8 (28.1) 98.9 (13.2)

Profit before tax 82.5(16.2) 356.9 (45.2) 103.2 (10..8) 8.8 (1.6) 12.0 (1.3)

Return on equity, (%) 9.9 54,7 26.7 3.1 15.3

Equity 532.1(52.4) 436.9 (50.5) 259.6 (27.3) 200.3 (21.3) 161.8 (15.0)

Assets 1 158.5(133.2) 976.9 (120.6) 2 669.5 (341.8) 2 466.2 (309.6) 1 171.8 (129.6)

Volito Aviation AB – 100% subsidiary of Volito ABand Volito’s holding company for aircraft leasing

The Goldman Sachs Group Inc – USA-basedinvestment bank and Volitos’ partner in VGS

Volito Aviation Services AB – Management company with responsibility for the aircraft fleet of VGS and Volito Aviation AB

Volito Aviation AG – Swiss holding company foraircraft leasing

VGS Aircraft Holding (Ireland) Ltd – Joint venture between Volito and Goldman Sachs with an aim to acquire, finance and lease out aircraft. As of 31 December 2008, VGS owned 41 aircraft.

Structure Volito Aviation

Argentina

12

The Aircraft Fleet, December 31st 2008

Geographical spread in 2008

USA

ARGENTINA

PANAMA

BRAZIL

Aircraft MSN/year Engine Model Registration Operator Lease Expiry

Fokker 50 20210/1991 PW100-125 PH-FZH Denim Air, The Netherlands March 2012

Fokker 50 20252/1992 PW100-125 PH-KXM Denim Air, The Netherlands March 2012

Boeing 737-33A 24094/1989 CFM56-3B2 LN-KKS Norwegian Air Shuttle, Norway April 2010

Boeing 737-4C9 25429/1992 CFM56-3C1 YR-BAD Blue Air, Romania March 2012

Boeing 737-4C9 26437/1992 CFM56-3C1 UR-GAV Ukraine International, Ukraine March 2012

Airbus 320-232 0872/1998 IAE V2527-A5 B-6256 Sichuan Airlines, China July 2011

Airbus 320-231 0230/1991 IAE V2500-A1 UR-DAB Donbassaero, Ukraine April 2012

Airbus 319-132 1074/1999 IAE V2524-A5 9V-SBA SilkAir, Singapore April 2010

Airbus 319-132 1098/1999 IAE V2524-A5 9V-SBB SilkAir, Singapore April 2010

Boeing 737-3L9 27061/ 1992 CFM56-3B2 9M-AAG Air Asia, Malaysia March 20 10

Airbus 319-132 1575/2001 IAE V2524-A5 PR-MBI TAM, Brazil March 20 14

Boeing 737-3G7 24009/1988 CFM56-3B1 N302AW US Airways, USA March 2011

Boeing 737-3G7 24010/1988 CFM56-3B1 N303AW US Airways, USA March 2010

Airbus 320-231 0308/1992 IAE V2500-A1 VT-EVS Indian Airlines (Nacil), India March 2010

Airbus 320-231 0314/1992 IAE V2500-A1 VT-EVT Indian Airlines (Nacil), India March 2010

Airbus 320-233 0558/1995 IAE V2527E-A5 F-HBAE Aigle Azur, France April 2009

Airbus 320-233 0561/1995 IAE V2527E-A5 F-HBAD Aigle Azur, France March 2009

Boeing 737-71Q 29047/1999 CFM56-7B HP-1369CMP COPA, Panama April 2010

Boeing 737-71Q 29048/1999 CFM56-7B HP-1370CMP COPA, Panama June 2010

Airbus A319-112 0629/1996 CFM56-5B6/2P CS-TTQ TAP, Portugal March 2012

Airbus A319-112 1068/1999 CFM56-5B6/2P F-GYFM CCM, France Nov 2014

Airbus A319-112 1145/1999 CFM56-5B6/2P F-GYJM CCM, France Oct 2014

Boeing 737-4J6 27171/1993 CFM56-3C1 VP-BQG Globus, Russia March 2014

Airbus 320-232 803/1998 IAE V2527-A5 N649AW US Airways, USA March 2013

13A

VIA

TIO

N

Owned by Volito Aviation AB Owned by VGS

GREAT BRITAIN

FRANCE

SPAIN

NORWAY

THE NETHERLANDS

UKRAINE

INDIA

ROMANIA

SINGAPORE

CHINA

MALAYSIA

PORTUGAL

ITALY

Aircraft MSN/year Engine Model Registration Operator Lease Expiry

Boeing 737-5Y0 24900/1991 CFM56-3C1 LV-BDV Aerolineas Argentinas, Argentina March 2011

Boeing 737-5Y0 25176/1991 CFM56-3C1 LV-BEO Aerolineas Argentinas, Argentina June 2011

Boeing 737-5Y0 24899/1991 CFM56-3C1 LV-BDD Aerolinas Argentinas, Argentina Feb 2011

Boeing 737-8K2 28373/1998 CFM56-7B PH-HZA Transavia, The Netherlands Dec 2009

Boeing 737-8K2 28374/1998 CFM56-7B PH-HZB Transavia, The Netherlands Dec 2010

Boeing 737-8K2 28375/ 1998 CFM56-7B PH-HZC Transavia, The Netherlands Dec 2010

Boeing 757-2Y0 26160/ 1993 RB211-535E4 G-FCLJ Thomas Cook, Great Britain April 2013

Boeing 757-2Y0 26161/1993 RB211-535E4 G-FCLK Thomas Cook, Great Britain April 2013

Airbus A319-112 1102/1999 CFM56-5B6/2P EI-DEY Meridiana, Italy Feb 2015

Airbus A319-112 1283/2000 CFM56-5B6/2P EI-DEZ Meridiana, Italy April 2015

Airbus A319-112 1305/2000 CFM56-5B6/2P EI-DFA Meridiana, Italy May 2015

Airbus A320-232 1652/2001 IAE 2527-A5 PR-MBQ TAM, Brazil Oct 2013

Airbus A320-232 1802/2002 IAE 2527-A5 PR-MBR TAM, Brazil Feb 2014

Airbus A320-232 1835/2002 IAE2527-A5 PR-MBS TAM, Brazil April 2014

Airbus A320-232 1591/2001 IAE2527-A5 PR-MBX TAM, Brazil June 2014

Airbus A320-232 1827/2002 IAE2527-A5 PR-MBZ TAM, Brazil Sep 2014

Airbus A320-232 1891/2002 IAE2527-A5 PR-MBY TAM, Brazil Oct 2014

Airbus 320-232 2531/2005 IAE V2527-A5 VT-KFF Kingfisher, India Sep 2012

Airbus 320-214 0426/1993 CFM56-5A EC-KBM Air Comet, Spain Dec 2011

Airbus 321-231 1276/2000 IAE V2531-A5 EC-HPM Spanair, Spain Nov 2014

MD-82 49269/1984 JT8-219 N249AA American Airlines, USA Dec 2013

MD-82 49270/1984 JT8-219 N251AA American Airlines, USA July 2014

Boeing 737-3T0 23942/1988 CFM56-3B1 N17356 Continental Airlines, USA Sep 2009

Acquired in 2009

14

Scandinavian Aviation Academy AB (SAA) continued its positive trend from 2007 during the year and reported a profit before tax of SEK 1.3 million (-5.0). The strong improvement has been driven mainly by continued positive developments relating to SAA’s operations in San Diego and the sale of the loss-making business, Twinair, in Switzerland.

The stability regarding the student base, organisation and quality of the business that was built up in 2007 at SAA in San Diego has also been reflected during the year in considerably improved profitability. An agreement was signed with an agent in 2008 concerning exclusivity for the Chinese market, which means that the majority of the company’s students will come from China in the coming years.

These students are assessed thoroughly before they go to the USA, which consequently makes it easier to achieve high efficiency in the training.

After a strategic assessment of the various companies within the SAA Group, a decision was made in March to sell SAA’s ownership share in Twinair. The company was deemed not to contribute anything substantial to SAA’s future development and strategy, while the operation took up much of the management’s time. The sale also contributed considerably to SAA’s improved profitability during the year.

SAA also performed well in 2008 in its role as a distributor for Cessna. A total of 8 aircraft were sold, a decrease compared with the 13 sold in the previous year. The lower volume is

attributable to the weaker demand that was noticeable in the latter part of the year.

After going through a period of profitability problems in 2006 and 2007, SAA now has a solid foundation in terms of profitability and management. The company has a strong name and a good product in a sector that can expect continued interesting developments in the future. In addition, the company has a competent business in terms of technical maintenance, which has potential for expansion in the coming years. These factors considered together mean that Volito views SAA’s continued development with great interest.

Aviation training

15A

VIA

TIO

N

CTT Systems AB took another major step forward in its development during 2008 when the company was chosen as the supplier for the forthcoming aircraft from Airbus, A350 XWB. CTT will supply both its systems for humidification and dehumidification for A350 XWB on an option basis. The transaction is a confirmation that CTT has become established in the OEM market among the world’s aircraft manufacturers following the order from Boeing that was received in 2005 relating to the B787.

Another important milestone was passed in September when Air New Zealand placed an order for 42 Zonal Drying systems for various aircraft types in its fleet. Air New Zealand is a company with a high profile in

the environmental area and chose CTT as part of moves to minimise its fuel consumption and thereby its environment-affecting CO2 emissions.

A further indication that CTT’s products are spearheading development in the field of aircraft humidity control was an order from the market’s VIP segment for the company’s Cair system to be installed on six aircraft. CTT has taken a clear leading role in this market segment, which indicates the quality delivered by the company’s products.

CTT’s profitability has been deferred further into the future due to the delays announced by Boeing regarding the B787. In addition to this, Boeing was hit by strikes during the autumn

of 2008 and delivery of the B787 to costumer is now expected in the first quarter of 2010. In May 2008, Volito increased its holding in CTT through the acquisition of a further 200 000 shares in the company. Volito’s holding after the acquisition amounted to 16.2% of the votes and capital in CTT. The acquisition of the shares shows Volito’s fundamental belief that CTT will generate good value growth in the future for its shareholders.

CTT’s share price decreased in 2008. All told, the share price fell by -48%. The trend for the OMX Small Cap over the same period was -46%.

Aviation technology

16

17R

EA

L E

ST

AT

E

– VOLIT O FA STIGHE TER –

Dialogue& proximity

The strength of Volito Fastigheter lies in the ability of its staff to maintain a good dialogue and work in close proximity to their tenants and business partners” Pelle Hammarstöm CEO, Volito Fastigheter

500

450

400

350

300

250

200

150

100

50 99 00 01 02 03 04 05 06 07 08

18

uring the year Volito Fastigheter acquired the properties Hamnen 22:2 and Delfinen 17. The combined purchase price for the two properties amounted to SEK 207 million. Hamnen is located close to Skeppsbron where Volito has built up a strong presence over the years. The area is deemed to be of special interest for the future due to the construction and establishment of the City Tunnel. Delfinen was acquired from Volito AB, the parent company of the Volito Group, and is located centrally on Södra Förstadsgatan in Malmö. The transaction regarding Delfinen refines Volito’s property portfolio and brings

it solely within the Volito Fastigheter Group – a structure that enhances the efficiency of management, increases transparency and improves the business ratios within the Volito Group.

“We felt it was right to acquire both these properties. The Hamnen acquisition further strengthens our presence around Skeppsbron, perhaps the most interesting location in Malmö when the City Tunnel is finished in 2010. We had previously managed Delfinen and it feels good to take on full ownership responsibility for the property. Delfinen further strengthens our cash flow while also providing possibilities for future

expansion, as the property was acquired without external financing,” says Pelle Hammarström, CEO of Volito Fastigheter.

Volito Fastigheter sold the Spjutet 2 property in Helsingborg. The sale generated a capital gain of SEK 29.5 million.

“For some time we have focused solely on Malmö and the surrounding area, so the sale felt like a natural step. In addition, we received a good price that further strengthens our financial position and situation,” states Pelle Hammarström.

Continued strong operating result in a weaker property marketThe result reported by Volito Fastigheter for 2008 were one of the strongest since the company was established in 1997. Volito Fastigheter’s profit before tax amounted to SEK 48.1 million (27.0). The result included capital gains of SEK 29.5 million (2.9). The company has both acquired and sold properties during the year. All transactions have had a strategic aim. The property leasing market in the Öresund Region continues to be strong, but property values have fallen somewhat as a result of the increased required rate of return in the wake of the financial crisis.

D

SEK million Adjusted equity

The premises in central Malmö offered us new possibilities. We definitely like the location” Georg Brunstam Hexpol AB

%

46

14

244

30

19R

EA

L E

ST

AT

E

The property leasing market in the region has continued strongly even though a certain weakening in the number of enquiries regarding premises was noticeable towards the end of the year. In 2008 the company signed new agreements with Banverket, Maendi AB och Victoria Park. The new agreements have been signed at a rent above or well in line with previous levels. The company’s vacancy level fell during the year to 7.8% (11.8%). This reduction in vacancy level is attributable to the high occupancy rate of the properties that were acquired, as well as the successful management work regarding new tenants.

In value terms the real estate market has developed negatively as a consequence of the increased required rate of return in the wake of the financial turbulence. The increased required rate of return has not only resulted in an increased risk premium, but also altered financing requirements regarding external capital. The market value of Volito’s property portfolio was assessed by an external party at year-end and was set at SEK 1 357 million. Excluding acquisitions and sales, this represents an increase of 2.2% compared with the previous year-end.

Volito Fastigheter’s profit before tax for 2008 was SEK 48.1 million (27.0).

The result included capital gains of SEK 29.5 million (2.9). This result is one of the best in the company’s history and indicates a successful business model, efficient management and a highly competent organisation. Volito Fastigheter expects that the market in 2009 will be somewhat weaker in terms of demand for commercial premises in the Öresund Region. However, it is felt that the market dynamics and long-term growth conditions will remain good, which is why the coming years can provide exciting opportunities for expansion in the long-term.

Volito Fastigheter AB, Five-year summary

SEK million 2008 2007 2006 2005 2004

Rental income including capital gains 130.7 92.1 81.5 109.6 94.4

Profit/Loss before tax 48.1 27.0 26.5 56.2 42.2

Return on equity, (%) 25.9 11.3 12.2 28.5 24.7

Equity 222.1 178.4 166.2 148.1 135.8

Real estate market value 1 356.9 1 185.8 998.6 890.7 764.7

Distribution of rent by category and m2

Offices

Industry

Trade

Residential

Hotel

Nursery school

1

15

12

2222

33

2

91

4411

3 52 4

ÖRESUND

KLAGSHAMN

N

2316141310

212019

6

78

11

5

MALMÖ

NN 17 18

20

Real estate holding 2008

Property Segeholm 10Address Ågatan 1Area 15 199 m2

Property Äpplet 15Address Generalsg 5Area 664 m2

Property Flygkameran 2Address Höjdroderg 7-9Area 1 376 m2

Property Diana 28Address Engelbrektsg 5Area 902 m2

Property Hangaren 2Address Flygplansg 1-3Area 2 200 m2

6

11

16

21

8

13

18

23

10

15

20

7

12

17

22

9

14

19

21R

EA

L E

ST

AT

E

Property Nejlikebuketten 4Address Derbyvägen 6Area 6 557 m2

Property Aegir 1Address Carlsgatan 1Area 7 610 m2

Property Flygledaren 7Address Hödroderg 22Area 1 971 m2

Property Runstenen 16Address Käglingevägen 37Area 3 068 m2

Property Medusa 3Address Carlsgatan 42Area 1 300 m2

Property Skytteltrafiken 2Address Nygårdsvägen 6Area 1 730 m2

Property Ran 9Address Jörgen Kocksg 1Area 7 904 m2

Property Hamnen 22:2Address Jörgen Kocksg 3Area 7 597 m2

Property Ran 4Address Skeppsbron 3Area 4 019 m2

Property Bronsdolken 27Address Stenyxegatan 25Area 2 221 m2

Property Kupolen 3Address Krossverksg 7-17Area 9 970 m2

Property Medusa 4Address Carlsgatan 44Area 7 201 m2

Property Lastbryggan 2Address Nygårdsvägen 4Area 1 158 m2

Property Härsjön 4Address Hålsjögatan 8Area 3 147 m2

Property Delfinen 17Address S Förstadsgatan 4Area 3 034 m2

Property Utgrunden 7Address Aspögatan 1Area 7 291 m2

Property Bronsdolken 26Address Stenyxegatan 25Area 3 423 m2

Property Ran 8Address Skeppsbron 7Area 1 084 m2

22

Volito’s holdings in Peab AB (publ) and Peab Industri AB (publ) have developed positively during the year regarding the respective operations, but negatively in terms of value development.

Both Peab and Peab Industri had a high level of activities during

the year which led to increased turnover(+8%) as well as operating profit (+9%) for the whole of Peab now being consolidated as one group. The company’s order book continue to look robust, however a decline in incoming orders was noticeable in the latter part of the year.

In October the board of Peab decided to make an official bid for all the shares in Peab Industri. Three shares in Peab were offered for two shares in Peab Industri. The companies, which were split into two units in 2007, were consequently brought together again to form a joint group.

Real Estate – other holdings

23R

EA

L E

ST

AT

E

The transaction means that Peab’s status is further strengthened through a higher equity ratio, increased cash flow and thereby an enhanced capability to both further develop the business and maintain good conditions to enable a continued stable return for shareholders.

The construction industry was hit hard in terms of value growth during the financial crisis of autumn 2008. In view of this, Volito’s holdings in the two Peab companies lost 57% (including received dividends) in value compared with the start of the year. As a comparison, the OMX Mid Cap Index fell by 40% in the same period.

24

25S

TR

UC

TU

RE

D F

INA

NC

E

– NOR DK A P BA NK AG –

Structure& perspective

Nordkap Bank AG has a long term perspective and remains committed in difficult times” Niklaus Hasler, CEO, Nordkap Bank AG

600

500

400

300

200

100

26

MSEK Loan and guarantee portfolio

I t was a year of unprecedented volatility with sharply falling commodity prices and declining inflation rates. What started as a mortgage crisis in the United States turned into a collapse of the world’s leading financial markets, creating a severe downturn in the real economy. These events affected the level of trust in free markets, risk controls, supervision, regulation and the overall efficiency of the financial industry.

During 2008, the loan portfolio of Nordkap Bank AG grew by 25% to CHF 539 million (432). Nordkap Bank AG performed well in the first three quarters of 2008 and it took advantage of attractive discounts available in the secondary loan market. However, in the course of the fourth quarter, the economic crisis started to affect the liquidity situation of a handful of Nordkap Bank’s borrowers and, as a consequence, Nordkap Bank AG

experienced payment delays and increased its provisions for potential credit losses from CHF 0.1 million to CHF 17.3 million. This increase in provisions turned the net profit into a loss of CHF 5.4 million (2007: net profit of CHF 7.2 million).

Challenging times for the fi nancial industryThe year 2008 was difficult for the entire financial services industry. The financial and economic crisis and the sharp drop in commodity markets is a big challenge for the customers of Nordkap Bank AG. In order to mitigate the impact of potential future loan losses, Nordkap Bank AG has initiated corrective measures and increased the loan loss provisions.

600

500

400

300

200

10004 05 06 07 08

CHF million Loan and guarantee portfolio

%

27S

TR

UC

TU

RE

D F

INA

NC

E

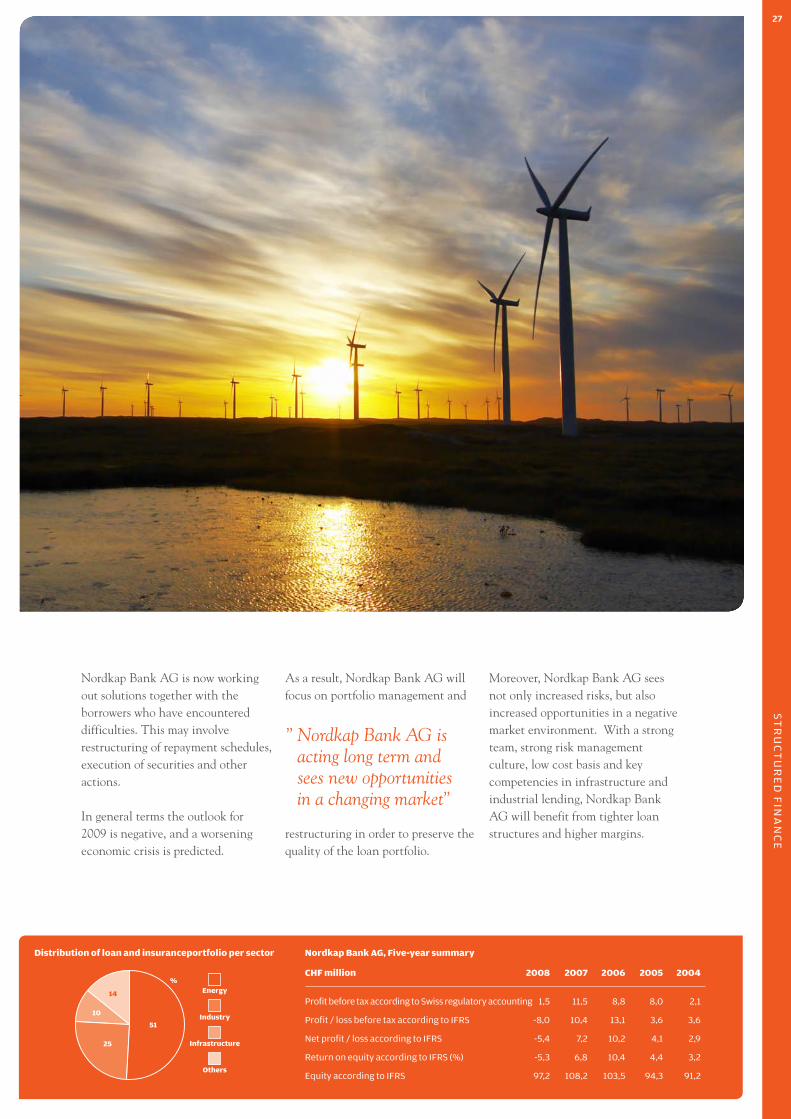

Nordkap Bank AG, Five-year summary

CHF million 2008 2007 2006 2005 2004

Profit / loss before tax -8,0 10,4 13,1 3,6 3,6

Net profit / loss -5,4 7,2 10,2 4,1 2,9

Return on equity (%) -5,3 6,8 10,4 4,4 3,2

Equity 97,2 108,2 103,5 94,3 91,2

Distribution of loan and insuranceportfolio per sector

Energy

Industry

Infrastucture

Others

Nordkap Bank AG is now working out solutions together with the borrowers who have encountered difficulties. This may involve restructuring of repayment schedules, execution of securities and other actions.

In general terms the outlook for 2009 is negative, and a worsening economic crisis is predicted.

As a result, Nordkap Bank AG will focus on portfolio management and

restructuring in order to preserve the quality of the loan portfolio.

Moreover, Nordkap Bank AG sees not only increased risks, but also increased opportunities in a negative market environment. With a strong team, strong risk management culture, low cost basis and key competencies in infrastructure and industrial lending, Nordkap Bank AG will benefit from tighter loan structures and higher margins.

” Nordkap Bank AG is acting long term and sees new opportunities in a changing market”

%

51

25

10

14

Nordkap Bank AG, Five-year summary

CHF million 2008 2007 2006 2005 2004

Profit before tax according to Swiss regulatory accounting 1,5 11,5 8,8 8,0 2,1

Profit / loss before tax according to IFRS -8,0 10,4 13,1 3,6 3,6

Net profit / loss according to IFRS -5,4 7,2 10,2 4,1 2,9

Return on equity according to IFRS (%) -5,3 6,8 10,4 4,4 3,2

Equity according to IFRS 97,2 108,2 103,5 94,3 91,2

Distribution of loan and insuranceportfolio per sector

Energy

Industry

Infrastructure

Others

8

9

6 75

4

3

2

1

28

N

Geographicalspread in 2008 ordkap Bank AG strives to spread risks as widely as possible, and therefore is active within a variety of sectors and different geographical areas.

The bank’s customers are mainly in the energy, industry and infrastructure sectors. Within the energy sector, which accounts for 51% of loans, the largest single segment is power generation, providing approx. 17% of the portfolio value.

The geographical spread covers all continents. The largest geographical markets are Eastern Europe (24%), North America (22%), Asia (15%) and Western Europe (13%).

24

25

30

32

3127

28

33

34

35

36

29

26

2319

1715

2221

2018

16

1413

1211

10

1 9 17 25 33

2 10 18 26 34

3 11 19 27 35

4 12 20 28 36

5 13 21 29

6 14 22 30

7 15 23 31

8 16 24 32

29

Canada

USA

Mexico

Belize

Costa Rica

Panama

Cayman Islands

Brazil

Argentina

Ireland

Great Britain

The Netherlands

Belgien

Luxembourg

Germany

Switzerland

Czech Republic

Croatia

Hungary

Bosnia-Herzegovina

Montenegro

Serbia

Romania

Lithuania

Finland

Ukraine

Turkey

Egypt

Saudi Arabia

Russia

Azerbaijan

Kazakhstan

Indonesia

Singapore

Philippines

Australia

ST

RU

CT

UR

ED

FIN

AN

CE

30

Board Member

Lennart Blecher, born 1955, Bachelor of LawsSenior Partner of EQT. Chairman of the Board at Brunswick Leasing Ltd. Chairman of the Board at Nordkap Bank AG, Zürich. Board Member of Volito Aviation AB, Volito Fastigheter AB and AIG Private Bank, Zürich.

Board Member

Bo Olsdal, born 1945, Master of ScienceBoard Member of Volito Aviation AB, Volito Fastigheter AB, SAA AB and Ste-Nic AB.

Chairman of the Board

Karl-Axel Granlund, born 1955, Master of ScienceChairman of the Board at Volito Aviation AB, Volito Fastigheter AB, CTT Systems AB (publ). Board Member of PEAB AB (publ) and others.

President and CEO

Johan Lundsgård, born 1953, EconomistBoard Member of Volito Aviation AB, Volito Fastigheter AB. Chairman of the Board at SAA AB. Board Member of Partnertech Karlskoga AB.

Board of Directors and Management

31

THE GROUP

Annual Report

Administration report

32-34

Consolidated income statement

35

Consolidated balance sheet

36-37

Pledged assets and

contingent liabilities

38

Summary of changes in equity

39

Cash flow statement

40

Supplement to cash flow statement 41-42

Accounting principles and notes

to the accounts

43-55

Signatures

55

Auditors’ report

57

Addresses

59

AN

NU

AL

RE

PO

RT

32

Administration reportThe business in brief

Volito AB (Corp. ID. No. 556457-4639) is the Parent company in a

Group that operates in the business areas Aviation, Real Estate and

Structured Finance. Aviation includes Volito Aviation (aircraft leasing),

SAA (training) and Volito’s holding in CTT Systems AB (publ). The Real

Estate business area consists of Volito Fastigheter, Volito’s holding

in Peab AB (publ) and the previous holding in Peab Industri AB (publ).

Structured Finance includes Volito’s ownership in Nordkap Bank AG.

The result before tax for the Parent company amounted to SEK

-54.8 million (206.1) and the result before tax for the Group was

SEK -28.4 million (600.9). The balance sheet total for the Parent

company at year-end was SEK 1 119.5 million (1 241.2) and for the

Group, SEK 2 929.7 million (2 747.9). The equity amounted to

SEK 574.8 million (668.0) and SEK 899.2 million (908.9) for

the Parent company and Group respectively.

AviationLeasing – Volito Aviation AB group

Volito Aviation was established in the spring of 2001 as a subsidiary of

Volito AB. The company runs operations in the leasing of commercial

jet aircraft in the narrow-body segment, mainly Boeing 737 and Airbus

319/320 aircraft.

In late 2006, Volito Aviation signed an agreement with Goldman Sachs

concerning the merger of their respective aircraft fleets into a jointly

owned company, VGS Aircraft Holding Ltd. (VGS), based in Ireland.

This transaction took the major part of 2007 to implement. The

transaction brought a realisation of parts of the value that has been

built up in Volito Aviation’s aircraft fleet.

During the year VGS invested USD 155 million (363) in 6 (18) new

aircraft and sold 8 aircraft and one aircraft engine for USD 82 million.

At year-end, VGS had a fleet of 41 aircraft. These have a total book

value of USD 805 million. Liabilities linked to the fleet amounted to

USD 574 million at year-end. The percentage of narrow-body aircraft

in the fleet is 100%, and there is a good spread of risk in geographical

terms. The company has lessees in areas such as Europe, Central and

South America, North America and Asia.

The fleet of VGS and Volito Aviation’s own fleet of five aircraft

are managed by Volito Aviation Services AB (VAS), a dedicated

management company that is principally owned by Volito Aviation

AB (80%). In 2008, VAS was audited by SH&E (a prominent global

consulting company in the aviation industry) in order to strategically

prepare the company to also serve customers outside the Volito

Group.

In addition to the investments made by VGS, Volito has upgraded its

own aircraft for a total of SEK 8.9 million.

Volito Aviation’s profit before tax for 2008 was SEK 82.5 million

(356.9). Of the previous year’s result, SEK 289.2 million was

attributable to the transaction with VGS.

Training – SAA AB group

SAA runs training courses for personnel in the aviation industry,

principally pilots, and has operations in Sweden and the USA.

SAA in San Diego has displayed considerably improved profitability

during the year. This is attributable to a large degree to the integration

work carried out in recent years, which has led to a more stable

organisation and better quality in the business. An agreement was

signed with an agent in 2008 regarding exclusivity for the Chinese

market, which means that the majority of the company’s students will

come from China in the next few years.

After a strategic assessment of the various companies within the SAA

group, a decision was made to sell SAA’s ownership share in Twinair.

The company was deemed not to contribute anything substantial to

SAA’s future development and strategy, while the operation took up

much of the management’s time.

The company acts as a distributor for Cessna. A total of 8 aircraft

(13) were sold, which generated SEK 2.3 million (3.2) in the form of

commissions. The lower volume compared with 2007 is attributable to

weaker demand in the latter part of the year.

The SAA group improved its results in 2008 and reported a profit

before tax of SEK 1.3 million (-5.0). The improvement is mainly due to

continued positive developments relating to SAA’s operations in San

Diego and the sale of the loss-making business Twinair in Switzerland.

Other holdings – CTT Systems AB (publ)

CTT is a Swedish technology company that develops and markets

humidity control systems for commercial aircraft. The company’s

shares are listed on OMX Nordic Exchange Stockholm.

CTT Systems AB (publ) took another major step in its development in

2008, as the company was chosen as the supplier for the forthcoming

aircraft from Airbus, A350 XWB. CTT will supply both its systems for

humidification and dehumidification for A350 XWB on an option basis.

In the autumn Air New Zealand placed an order for 42 Zonal Drying

systems for various aircraft types in its fleet. Air New Zealand is a

company with a high profile in the environmental area and chose CTT

as part of moves to minimise its fuel consumption and thereby its

environment-affecting CO2 emissions.

CTT’s profitability has been deferred further into the future due to the

delays announced by Boeing regarding the B787.

In May, Volito increased its holding in CTT through the acquisition of a

further 200 000 shares in the company. Volito’s ownership share after

the acquisition amounted to 16.2% of the votes and capital in CTT.

CTT’s share price declined in 2008. All told, the share price fell by 48%.

The fall in the OMX Small Cap over the same period was 46 %.

Real Estate Volito Fastigheter AB group

Volito Fastigheter AB is a wholly-owned subsidiary of Volito AB.

Volito Fastigheter is involved in the trade and management of real

estate in the Öresund Region. The company is focused on commercial

properties in the Malmö region.

During the year Volito Fastigheter acquired the properties Hamnen

22:2 and Delfinen 17. The combined purchase price for the two

properties (acquired via the acquisition of a subsidiary) amounted

to SEK 207.0 million. Hamnen is located close to Skeppsbron where

Volito has owned property for some time. The area is deemed to be

of special interest for the future due to the establishment of the City

Tunnel. Delfinen was acquired from Volito AB and is located centrally

in Malmö. The transaction regarding Delfinen refines Volito’s property

portfolio and brings it solely within the Volito Fastigheter group – a

structure that improves the efficiency of management and increases

transparency within the Volito Group.

The company sold the Spjutet 2 property in Helsingborg. The sale

generated a capital gain for the Group of SEK 27.6 million.

The market in the region has continued strongly, even though a

certain weakening in the number of enquiries regarding premises was

noticeable towards the end of the year. Volito Fastigheter signed

33

new agreements with Banverket, Meandi AB and Victoria Park. The

new agreements have been signed at a rent level above, or well in line

with, previous levels. The company’s vacancy level fell during the year

to 7.8% (11.8%). The reduction in vacancy level is attributable to the

high occupancy rate of the properties that were acquired, as well as

successful management work regarding new tenants.

In value terms the real estate market has displayed a downward trend

as a consequence of the increase in required rate of return that the

financial turbulence has brought with it. The increase in required

rate of return has resulted not only in an increased risk premium,

but also altered financing requirements regarding external capital.

The market value of Volito’s property portfolio was assessed by an

external party at year-end and was valued at SEK 1 357 million (1 186).

Excluding acquisitions and sales, this corresponds to an increase of

2.2% compared with the previous year-end.

Volito Fastigheter’s profit before tax for 2008 was SEK 48.1 million

(27.0). The result includes capital gains of SEK 29.5 million (2.9). The

return on adjusted equity for the year was 25.9% (11.3%).

Other holdings – Peab AB (publ) and Peab Industri AB (publ)

Peab and Peab Industri are companies active in the construction and

civil engineering field in the Nordic Region. Both companies’ shares

are listed on OMX Nordic Exchange Stockholm.

The board of Peab decided in October to make an official offer for all

the shares in Peab Industri. Three shares in Peab were offered for two

shares in Peab Industri. The companies, which were split into two units

in 2007, will consequently be brought together again to form a joint

Group.

Volito’s holding in Peab after the transaction stated above consists of

15 243 000 Series B shares in Peab AB (publ), which represents 5.24%

of the capital and 2.54% of the votes.

For Volito, the holding in Peab AB continues to be of a strategic

character. The company is looking at a number of real estate projects

at an early stage that would mean considerable expansion of the

company’s real estate activities. All these projects are linked to the

close cooperation that exists between Volito and Peab regarding real

estate development.

The construction industry was one of the sectors hardest hit in terms

of the value growth during the financial turbulence of autumn 2008.

Both Peab and Peab Industri have increased turnover (7% and 8%

respectively) and operating profit (7% and 9% respectively). The

companies’ order books continue to look robust, however a decline

in incoming orders was noted in the latter part of the year. The total

holding in both Peab companies at year-end had a market value of

SEK 329.2 million (819.2), which represents a value reduction of 57%

(taking into account the received dividend) for the year. This can be

compared to the OMX Mid Cap, which in the same period decreased

by 40%.

Structured Finance Nordkap Bank AG

Nordkap Bank is a Swiss commercial bank specialising in structured

financing solutions. Volito AG owns 40% of the shares in Nordkap Bank.

Nordkap Bank’s loan portfolio increased by 25% in 2008 to CHF 539

million (432). The bank performed well in the first three quarters,

gaining benefits from the attractive prices in the credit market. In Q4

the financial crisis began to have an effect on some of the bank’s loan

customers, who felt the impact of sharply falling commodity prices.

This resulted in delays in payments from customers and has led to

increased provisions for feared customer losses at Nordkap Bank.

For 2008 Nordkap Bank reported a profit before tax of CHF 1.5 million

(11.5). The return on equity was 2.0% (10.6%). Within the Volito Group,

Nordkap Bank’s profit/loss is translated in accordance with IFRS. The

consolidated loss for the Nordkap Holding Group in accordance with

IFRS was CHF 8.2 million (4.6).

Other holdingsVolito has ownership shares in AB Nordsidan, Galenica AB, Itesco AB,

Simcenter Copenhagen A/S and a number of other small companies.

During the year Volito sold its shares in Saint Victor s.a.r.l. The

combined value of the remaining holdings for the Group amounted at

year-end to SEK 22.1 million (19.1).

The Parent companyThe loss before tax for the Parent company was SEK 54.8 million

(profit 206.1).

During the year Volito AB sold the property Delfinen 17 to Volito

Fastigheter. The transaction generated a capital gain of SEK 42.7

million.

Peab’s decision to buy back Peab Industri has resulted in a capital loss

of SEK 132.9 million. The capital loss relating to Kattegat Invest AB,

which owned 475 000 shares in Peab Industri amounted to SEK

16.9 million.

TaxTax-exempt dividend on the holding in Peab AB

Volito AB has successfully concluded the process concerning tax

exemption on dividends and capital gains relating to the holding in

Peab AB. In April 2008 the Administrative Court of Appeal judged that

the dividend on the holding is tax exempt for the income years 2001

and 2002. Thereafter, the Swedish Tax Board decided in accordance

with these rulings relating to the income year 2004. (The Swedish Tax

Board had previously approved tax exemption for the income years

2003 and 2005. The years 2006 and 2007 have never been called into

question.)

Between the years 2000-2008 Volito received dividends from Peab

AB of SEK 67.3 million. Together with the tax-exempt dividends and

capital gains in the subsidiary, Kattegat Invest AB of SEK 33.8 million,

the Volito Group has received dividends and made capital gains

totalling just over SEK 100 million during the years in question.

Deficit in Dean Aviation Company LLC

For the financial years 1999 and 2002 Volito has claimed a deduction

for the deficit in the subsidiary, Dean Aviation Company LLC.

The deduction was called into question by the National Tax Board.

In 2004, The County Administrative Court approved the deficit. The

National Tax Board appealed in the Administrative Court of Appeal,

which in December 2008 ruled in the National Tax Board’s favour.

Volito AB has decided to apply for leave to appeal in the Supreme

Administrative Court.

Due to the fact that the possibility of a leave to appeal is uncertain,

the company has decided to report the tax that resulted from the

judgment in the Administrative Court of Appeal, together with the

interest on this tax, as expenses and liabilities as of 31 December 2008.

The tax has been estimated at SEK 34.5 million and the interest at SEK

15.6 million.

AN

NU

AL

RE

PO

RT

34

Important leasing agreementsVolito Aviation’s aircraft fleet is leased out under operational leasing

agreements. The period during which aircraft are leased out ranges

from one to four years, see note 6.

Volito Fastigheter has an occupancy rate of 92.2 % (88.2%). The

breakdown of leases is 96% commercial properties and 4% residential.

The commercial rental income is divided between 169 contracts in a

number of different sectors. For more information, see notes 6 and 21.

Important events after the end of the financial year There are no significant events after the end of the financial year.

Expectations concerning future developments We see a considerably worsened business cycle for 2009 and the

consequences for Volito are hard to predict at present. All three

business areas Aviation, Real Estate and Structured Finance have strong

cash flows, sound capital structures, competent managements and good

market positions, which means that preparedness is good when facing

a more uncertain future. Volito deems that the prevailing uncertainty

concerning future global economic developments ought to generate

business opportunities that benefit the Volito Group in the long term.

In view of its strong financial position and an aircraft fleet that

generates a strong operative cash flow, Volito Aviation sees

interesting opportunities in a market that for the foreseeable future

will be marked by downward pressure on prices and companies with a

need to sell assets.

Volito Fastigheter expects that in 2009 the market will be somewhat

weaker in terms of demand for commercial premises. However, it is

felt that the market dynamics and long-term growth conditions will

remain good, which is why the coming years can provide exciting

opportunities for expansion in a longer perspective.

It is feared that the ongoing financial crisis will worsen. As a result of

this, Nordkap Bank will focus on consolidating and structuring its loan

management with an aim to maintain the quality of its loan portfolio.

Nordkap Bank also sees new business opportunities in the changing

market. With a competent team, a strict risk management culture

and cost-effective organisation, Nordkap Bank will be able to gain

advantages from a tighter loan market with higher margins.

Financial risksIn its business activities the Volito Group is exposed to various types

of financial risks. Financial risks relate to changes in exchange rates

and interest rates that affect the company’s cash flow, profit and

thereby associated equity. The financial risks also include credit and

refinancing risks.

Exposure applying to the different operations is presented quarterly

for the respective companies’ boards, which make current decisions

regarding risk management based on the market situation and

macroeconomic information, see note 36.

Currency exposure

In its business activities the Volito Group is exposed to risks relating to

exchange rate changes principally through its involvement in aircraft

leasing. Income from the leasing business is set and paid in USD. This

exposure is counterbalanced to a large degree in that interest and

amortisation are similarly USD-based.

The results of VGS are reported as a share in an associated company.

Exchange rate differences related to translation of VGS are posted in

the equity.

The Volito Group’s holding in Nordkap Bank AG is partly hedged

against changes in the CHF exchange rate through certain borrowings

in CHF. However, a certain amount of the holding is exposed to

changes in the CHF exchange rate. Exchange rate differences related

to translation of the company are posted in the equity.

The board of Volito has decided to accept the exposure to USD and

CHF according to the above, as this exposure in itself constitutes a risk

diversification within the Volito Group. The extent of this exposure will

be decided according to continuous review.

Interest rate exposure

The Volito Group is exposed to changes mainly in short-term interest

rates through its involvement in Volito Fastigheter AB and SAA

groups. The Parent company, Volito AB, also has risk exposure relating

to short-term interest rates.

Taken together, the Volito Group’s total loans exposed to short-term

interest rates amount to approx. SEK 948 million.

The Volito Group manages part of its interest rate risks using interest

rate swaps. Hedging relating to 41.8% of the debt portfolio of the

Volito Fastigheter AB group is being managed with swaps, something

that gives the company a higher degree of flexibility in terms of future

debt management. See note 36.

Refinancing risks

The Volito Group depends on a functioning credit market. The Group

has a need to continuously refinance parts of its business, see note

39. The Group has a satisfactory equity ratio and loan capacity. It is

therefore Volito’s assessment that there is at present no problem

concerning the credit that is due for refinancing.

Volito’s employees The Volito Group is a relatively small organisation that handles large

capital amounts. The well-being and continuous development of the

Group’s employees are hence of vital importance for the long term

prosperity of the Group.

Volito uses employment conditions as the primary tool for attracting

suitable and talented people. A number of events are organised within

the Group’s various companies to further strengthen the team spirit

and loyalty among people working at Volito.

During the year Johan Lundsgård was appointed CEO of the Volito

Group. Johan has a background as a CEO of various industrial companies.

Previously to joining the company, he was President of Finnveden.

Proposed allocation of the company’s profit The Board of Directors and CEO propose that the profit available for

disposal, SEK 309 794 097.28 is allocated as follows (SEK K):

Dividend, [2 440 000 at SEK 8.25 per share] 20 130

Carried forward 289 664

Total 309 794

The proposed dividend reduces the Group’s equity ratio to 50% from

51%. The equity ratio is prudent, in view of the fact that the company’s

activities continue to operate profitably. Liquidity in the Group is

likewise expected to be maintained at a similarly secure level.

The Board’s understanding is that the proposed dividend will not

hinder the company in carrying out its duties in the short or long term

nor from conducting necessary investments. The proposed dividend

can thus be seen in accordance with sections 2 and 3 of Paragraph 3 of

ABL 17 (prudence principle).

For further information on the company’s income and position, refer

to the subsequent income statements and balance sheets, and related

notes to the accounts.

35A

NN

UA

L R

EP

OR

T

Income Statement The Group The Parent Company

Note Amounts in SEK K 2008 2007 2008 2007

2 Net sales 381 208 530 694 11 639 10 315

3 Income affecting comparability – 110 003 – –

4 Other operating income 51 314 15 937 42 719 855

1, 6 432 522 656 634 54 358 11 170

Operating expenses

5 Other external expenses -163 086 -148 380 -13 691 -12 612

7 Personnel costs -108 659 -91 095 -13 135 -13 673

8 Depreciation and write-downs of tangible

and intangible fixed assets -44 192 -147 697 -633 -670

9 Expenses affecting comparability – -73 219 – –

10 Other operating expenses -2 153 -6 497 -1 149 –

Operating profit/loss 114 432 189 746 25 750 -15 785

Result from financial income and expenses

11 Profit/loss from participations in group companies - 11 634 36 495 12 205

12 Profit/loss from participations in associated companies 33 377 -11 500 -7 344 -23 640

13 Profit/loss from other securities and

receivables held as fixed assets -91 735 276 736 -81 475 246 573

14 Interest income and similar income 15 131 27 356 12 331 9 095

15 Interest expenses and similar expenses -99 620 -142 136 -42 938 -22 386

16 Items affecting comparability - 249 042 – –

Profit/loss after financial items -28 415 600 878 -57 181 206 062

Appropriations

Reversed accelerated depreciations – – 2 341 –

17 Profit/loss before tax -28 415 600 878 -54 840 206 062

18 Taxes 20 768 -91 607 11 714 -30 845

Minority interests’ participation in profit/loss for the year -35 583 -117 805 – –

PROFIT/LOSS FOR THE YEAR -43 230 391 466 -43 126 175 217

36

Balance Sheet The Group The Parent Company

Note Amounts in SEK K 2008-12-31 2007-12-31 2008-12-31 2007-12-31

ASSETS Fixed assets

Intangible fixed assets

19 Other intangible assets 1 035 1 680 – –

20 Goodwill 2 369 4 025 – –

3 404 5 705 – –

Tangible fixed assets

21 Real estate 976 704 892 020 – 38 432

22 Aircraft 261 222 280 804 – –

23 Aircraft inventories 405 573 – –

24 Equipment, tools and installations 15 208 10 021 3 142 2 977

Construction in progress and advance

25 payments relating to tangible fixed assets 1 830 3 686 – –

1 255 369 1 187 104 3 142 41 409

Financial fixed assets

26 Participations in group companies – – 540 543 535 203

27 Receivables from group companies – – 91 979 74 031

28 Participations in associated companies 385 963 287 525 10 569 18 509

29 Receivables from associated companies 508 207 413 326 – –

30 Other securities held as fixed assets 439 341 544 251 408 167 500 967

31 Deferred tax assets 45 104 47 171 25 561 25 616

32 Pre-paid borrowing expenses 3 409 5 134 – 1

33 Other long-term receivables 7 073 6 076 1 342 625

1 389 097 1 303 483 1 078 161 1 154 952

Total fixed assets 2 647 870 2 496 292 1 081 303 1 196 361

Current assets

Inventories etc.

Raw materials and necessities 3 833 3 081 6 8

3 833 3 081 6 8

Current receivables

Accounts receivable – trade 10 651 7 404 14 1 281

Receivables from group companies 65 2 865 33 746 18 996

Receivables from associated companies 107 658 52 902 288 19 059

Income tax receivables 12 475 9 664 – 379

Other receivables 4 848 8 180 578 1 905

34 Prepaid expenses and accrued income 11 304 24 241 827 845

147 001 105 256 35 453 42 465

35 Short-term investments 1 477 998 1 477 998

Cash and bank balances 129 561 142 224 1 234 1 377

Total current assets 281 872 251 559 38 170 44 848

1 TOTAL ASSETS 2 929 742 2 747 851 1 119 473 1 241 209

37A

NN

UA

L R

EP

OR

T

Balance Sheet The Group The Parent Company

36

36

36

Note Amounts in SEK K 2008-12-31 2007-12-31 2008-12-31 2007-12-31

EQUITY AND LIABILITIES

37 Equity

Restricted equity

Share capital (2 440 000 shares at nom. SEK 100) 244 000 122 000 244 000 122 000

Issue with option 3 003 5 005 3 003 5 005

Restricted reserves/Statutory reserve 85 622 80 985 18 002 16 000

Non-restricted equity

Non-restricted reserves/Profit brought forward 609 779 309 490 352 920 349 764

Net profit/loss for the year -43 230 391 466 -43 126 175 217

899 174 908 946 574 799 667 986

Minority interests 312 020 228 697 – –

38 Untaxed reserves

Accumulated accelerated depreciation – – – 2 342

– – – 2 342

Provisions

31 Provisions for deferred taxes 80 919 144 766 – 44 495

Other provisions – 93 – –

80 919 144 859 – 44 495

Long-term liabilities

39 Other liabilities to credit institutes 749 097 504 375 350 000 82 106

41 Other liabilities 71 955 33 693 – –

821 052 538 068 350 000 82 106

Current liabilities

39 Liabilities to credit institutes 575 382 595 071 84 473 156 991

40 Bank overdraft facilities 40 412 159 467 34 885 138 691

Advance payment from customers 4 946 12 939 – –

Accounts payable - trade 16 385 15 460 1 027 1 760

Liabilities to Parent company 242 822 177 822

Liabilities to Group companies – – 17 195 118 322

Liabilities to associated companies 17 054 23 271 240 240

Income tax liabilities 79 144 42 455 33 322 –

Other liabilities 8 360 17 422 536 12 232

42 Accrued expenses and deferred income 74 652 60 374 22 819 15 222

816 577 927 281 194 674 444 280

TOTAL EQUITY AND LIABILITIES 2 929 742 2 747 851 1 119 473 1 241 209

38

Pledged Assets and Contingent Liabilities The Group The Parent Company

Amounts in SEK K 2008-12-31 2007-12-31 2008-12-31 2007-12-31

Pledged assets

For own liabilities and provisions

Property mortgages 698 855 731 355 – 44 000

Chattel mortgages 36 130 36 130 10 000 10 000

Shares 377 454 469 710 351 240 458 886

Shares in subsidiaries 193 339 193 359 295 610 290 030

Receivables 26 000 26 000 – –

Aircraft mortgages 146 884 147 548 – –

Other 1 000 1 000 1 000 1 000

Total pledged assets 1 479 662 1 605 102 657 850 803 916

Contingent liabilities

Guarantees for Group companies – – 134 357 55 367

Guarantees for associated companies 5 400 5 400 5 400 5 400

Tax case relating to claimed deductible deficiency – 58 155 – 58 155

Ongoing tax case relating to claimed deductible deficiency 38 771 36 224 – –

Claim for tax-fee capital gain – 4 578 – –

Tax case relating to claim

for tax-free dividend – 7 116 – 4 185

Claim for tax-free dividend 1 696 – 1 509 –

Other contingent liabilities 200 200 200 200

Total contingent liabilities 46 067 111 673 141 466 123 307

The Group

For the financial years 1999 and 2000, Volito has claimed a deduction for the deficiency in the subsidiary, Dean Aviation Company LLC. The deduction was

called into question by the Swedish Tax Authority. The County Administrative Court approved the deficiency, but the Swedish Tax Authority appealed to the

Administrative Court of Appeal, which in December 2008 ruled in the Swedish Tax Authority’s favour. Volito has decided to apply for leave to appeal to the

Supreme Administrative Court. Due to the fact that the possibility of a leave to appeal is uncertain, the company has decided to report the tax that resulted

from the judgments in the Administrative Court of Appeal, together with the interest on this tax, as expenses and liabilities as of 31 December 2008. With

this disappears the contingent liability that was reported for the named tax and interest.

The Swedish Tax Authority has filed a claim in the County Administrative Court that the deductible deficiency as of 31 December 2004 in an acquired

company should not be permitted according to the law on tax avoidance. Utilised and valued deductible deficiencies amount to SEK 140 million, which cor-

responds to SEK 39 million in deferred taxes.

Volito AB has successfully concluded the process concerning tax exemption on dividends and capital gains relating to the holding in Peab AB. In April 2008

the Administrative Court of Appeal judged that the dividend on the holding is tax exempt for the income years 2001 and 2002. Thereafter, the Swedish Tax

Authority decided in accordance with these rulings relating to the income year 2004. (The Swedish Tax Authority had previously approved tax exemption

for the income years 2003 and 2005. The years 2006 and 2007 have never been called into question.)

In 2008 the Volito Group received SEK 6.1 million in dividends from Peab Industri AB. Volito asserts that, like the holding in Peab AB, this holding is busi-

ness-contingent, which means the dividends are exempt from tax. As the claim that the holding in Peab Industri AB is business-contingent has not yet been

reported to the Swedish Tax Authority the issue has not been adjudicated. If the company is denied exemption from tax, no taxable income arises, as the

deductible deficiency from 2007 covers the received dividend.

The Parent Company

For the financial years 1999 and 2000, Volito has claimed a deduction for the deficiency in the subsidiary, Dean Aviation Company LLC. The deduction was

called into question by the Swedish Tax Authority. The County Administrative Court approved the deficiency, but the Swedish Tax Authority appealed to the

Administrative Court of Appeal, which in December 2008 ruled in the Swedish Tax Authority’s favour. Volito has decided to apply for leave to appeal to the

Supreme Administrative Court. Due to the fact that the possibility of a leave to appeal is uncertain, the company has decided to report the tax that resulted

from the judgment in the Administrative Court of Appeal, together with the interest on this tax, as expenses and liabilities as of 31 December 2008. With

this disappears the contingent liability that was reported for the named tax and interest.

Volito AB has successfully concluded the process concerning tax exemption on dividends and capital gains relating to the holding in Peab AB. In April 2008

the Administrative Court of Appeal judged that the dividend on the holding is tax-exempt for the income years 2001 and 2002. Thereafter, the Swedish Tax

Authority decided in accordance with these rulings relating to the income year 2004. (The Swedish Tax Authority had previously approved tax exemption

for the income years 2003 and 2005. The years 2006 and 2007 have never been called into question.)

In 2008 Volito received SEK 5.7 million in dividends from Peab Industri AB. Volito asserts that, like the holding in Peab AB, this holding is business-contin-

gent, which means the dividends are exempt from tax. As the claim that the holding in Peab Industri AB is business-contingent has not yet been reported

to the Swedish Tax Authority the issue has not been adjudicated. If the company is denied exemption from tax, no taxable income arises, as the deductible

deficiency from 2007 covers the received dividend.

39A

NN

UA

L R

EP

OR

T

Summary of Changes in Equity The Group The Parent Company

Restricted Non-restricted Restricted Non-restricted

Amounts in SEK K Share capital reserves equity Share capital reserves equity

Balance carried forward according to

balance sheet of 31 December 2006 122 000 74 502 348 283 122 000 21 005 368 525

Movements between unrestricted

and restricted equity – 10 133 -10 133 – – –

Profit/loss for the year – – 391 466 – – 175 217

Dividend – – -30 500 – – -30 500

FX/translation diff for the year – 1 355 1 840 – – –

Group contribution – – – – – 16 304

Tax effects on Group contribution – – – – – -4 565

Equity as of 31 December 2007 122 000 85 990 700 956 122 000 21 005 524 981

Movements between unrestricted

and restricted equity – 2 635 - 2 635 – – –

Profit/loss for the year – – - 43 230 – – -43 126

Dividend – – -40 260 – – -40 260

Bonus Issue 122 000 – -122 000 122 000 – -122 000

Buy-back of option – – -14 475 – – -14 475

FX/translation diff for the year – – 88 193 – – –

Group contribution – – – – – 6 492

Tax effects on Group contribution – – – – – -1 818

Equity as of 31 December 2008 244 000 88 625 566 549 244 000 21 005 309 794

Note 37 contains further information on equity.

40

Cash Flow Statement The Group The Parent Company

Amounts in SEK K 2008-12-31 2007-12-31 2008-12-31 2007-12-31

Operating activities

Profit/loss after financial income and expenses -28 415 600 878 -57 181 206 062

Adjustments for items not included in cash flow, etc 102 276 -374 260 67 082 -208 105

73 861 226 618 9 901 -2 043

Income taxes paid -14 601 -11 949 -326 -518

Cash flow from operating activities before

changes in working capital 59 260 214 669 9 575 -2 561

Cash flow from changes in working capital

Increase(-)/Decrease(+) in inventories -752 1 332 2 6

Increase(-)/Decrease(+) in current receivables -69 956 15 537 -1 551 -7 687

Increase(+)/Decrease(-) in current liabilities -6 245 -5 669 -27 507 11 345

Cash flow from operating activities -17 693 225 869 -19 481 1 103

Investment activities

Acquisition of subsidiaries -79 559 -33 513 – –