213

CHAPTER VI

Analysis of Economic Value Added (EVA)

and Market Value Added (MVA)

Maximizing shareholders value is becoming the new corporate

standard in India. The corporates, which give the lowest preference to the

shareholders’ inquisitiveness, are now bestowing the utmost inclination to it.

Shareholder’s wealth in terms of the returns they receive depends on their

investment. The returns can either be in the form of dividends or in the form

of capital appreciation or both. Capital appreciation in turn depends on the

subsequent changes in the market value of the shares. This market value of

shares is influenced by a number of factors, which can be company specific,

industry specific and macro-economic in nature1.

An important goal of financial management is to maximise the wealth

of the organisation, highest capital employees wealth and consequently

enhance the value of the firm. Shareholder’s wealth is traditionally reflected

by either standard accounting parameters (such as profits, earnings and cash

flow from operations) or financial ratios (including earnings per share, return

on capital employed, return on net worth, net profit margin, operating profit

margin etc). All these indicators fail to measure the true economic worth due

to manipulative accounting techniques to state higher or lower earnings,

depending on non-meaningful decision on how to record revenues or

expenses. Standard accounting principles fail to reflect the varying cost of

capital among the business within a company or the difference in risk in the

case of alternative business strategies in the earnings.

1. Mangala, Deepa and Joura Simpy, (2002) Linkage between economic value added and

market value: An Analysis in Indian context, Indian Management Studies, Journal,

pp-55-56.

214

This financial information is used by managers, shareholders and other

interested parties to asses their firm’s current performance, and also by

stakeholders to predict its future performance. The question that then arises is,

whether these measures of corporate performance are linked to the

expectation of the shareholders or not. The problem with their performance

measure is the lack of a proper benchmark for comparison. To help corporate

to generate value for shareholders, value-based management system has been

developed. Indeed, value based management, which seeks to integrate finance

hypothesis with strategic economic philosophy, is considered as one of the

most significant contributions to corporate financial planning2.

Over the past several years, an alternative performance measure called

the Economic Value Added (EVA) has been gaining acceptance around the

globe and has also been acknowledged by institutional firms as a credible

performance measure in order to overcome the limitations of accounting

based measures of financial performance. Joel M stern and G. Bennett

Stewart & co., introduced a modified concept of economic profit in 1990, in

the name of Economic Value Added (EVA) as a measure of business

performance. Stern Stewart has claimed that EVA, as a tool of financial

management, is neither ‘just a phenomenon’ nor is it united to ‘for profit’

organizations. Economic value added has been put to use for management

performance evaluation, and more than just a measure of performance, it is

the framework for a complete financial management (for improving scarce

capital allocation; and valuation of a target company at the time of

acquisition).

EVA as a tool of financial performance measurement

Shareholders value creation is the new buzzword today and Economic

Value Added (EVA) is its most popular measure. In simple terms EVA is 2. MC Taggart, James et al., (1994). The Value imperative, Free Press; New York, PP 4-6.

215

nothing but returns generated above cost of capital. It is the Net Operating

Profit After Tax (NOPAT) minus an appropriate change for the opportunity

cost of all capital invested (WACC) in an organization. EVA is an estimate of

“economic profit” or the amount by which earnings exceed or fall short of the

required minimum rate of return that shareholders and lenders could get by

investing capital in other securities of analogous risk3.

EVA as a tool of financial measurement enlightens whether the

operating profit is enough to cover the cost of capital. Shareholders must earn

sufficient returns for the risk they have taken in investing their funds in

companies’ capital. According to business standard-KPMG, if a company’s

EVA is negative, the firm is destroying shareholder’s wealth even though it

may be reporting a positive and growing earning per share and return on

capital employed4. The EVA framework, which is becoming more and more

admired tool for measuring the financial performance of corporate, offers a

consistent approach to set goals and measure performance, communicate with

investors, evaluate strategies, allocate capital valuing acquisitions and

determine incentive bonuses. It is one of the several on going initiatives for

new corporate.

The evaluation and growth of the concept EVA, which may be

realistically in young age in the west has been going through its childhood in

country like India. It may be quite an emerging concept in the minds of Indian

corporate policy makers and managers. Hence this chapter examines in detail

the EVA of selected automobile industry. It consists of sub-parts like EVA-

based ranking of selected companies, industry-wise and sector-wise trends in

EVA-based ranking. Results and discussion on statistically established trends.

3. Jaishweta, (2003). Godrej Retools for Value, Business Standard, P. 6.

4. Purikh, Parag, (2002). The Universe of Wealth Creation, PPFAS-Financial Advisory

Services Ltd-Online P. 2.

216

217

218

This chapter also examines the linear regression analysis in the midst of

Market Value Added (MVA) and other traditional financial variables like

EVA, EPS, ROCE, NOPAT and RONW of sample companies. It also

discusses multiple regression analysis and MVA and other financial variables

of sample companies sector-wise.

EVA of selected companies

EVA-based performance framework not only provides a far more

accurate report card on corporate financial performance than conventional

measures, but also has considerable implications for companies on how to

make strategic decisions and manage the healthier financial performance in

their pursuit of shareholder value. EVA created by the selected automobile

industry during the study period is depicted in Table 6.1. The table shows that

out of twelve industry, eleven industry has generated positive EVA during the

study period except in the year 1998-99, 2002-03, 2004-05 and one company

has destroyed their shareholder’s wealth completely.

It may be observed from Table 6.1 that Ashok Leyland Ltd and Eicher

Motors Ltd out of twelve companies have been generating the positive EVA

all the way throughout the period of study. On the other hand, Daewoo

Motors India Ltd is the only company which has been annihilating the wealth

of shareholders right through the period except in the year 1995-96. Tata

Motors Ltd, Bajaj Auto Ltd, Maharastra Scooters India Ltd created positive

EVA during the major part of eleven years period. Rest of the companies

slightly showed instability on their front.

On the whole the Table 6.1 concludes that about one-third (4 out of

12), of the sample companies have been able to govern affirmative EVA

during period under study whereas remaining companies are feasible to

append a very little to the value of shareholders.

219

220

Table 6.3

EVA-Sector-Wise Trends (1995-96-2005-06)

S.No Industry Mean

(Rs.in.crores) CV CAGR

1. Ashok Leyland Ltd 241.06 0.28 4.14

2. Tata Motors Ltd 233.21 4.22 -6.89

3. Eicher Motor Ltd 22.21 0.66 8.54

4. Swaraj Mazda Ltd 12.05 0.46 5.20

Commercial Vehicles Sector 127.33 2.03 -2.71

5. Hindustan Motors Ltd 10.19 9.73 -6.15

6. Mahindra and Mahindra Ltd 149.55 3.24 -3.10

7. Maruthi Udyog Ltd 49.14 22.16 -22.32

8. Daewoo Motors India Ltd -62.34 1.17 -0.77

Passenger Cars and Multiutility

Vehicles Sector 36.63 11.38 -17.85

9. Bajaj Auto Ltd 541.65 1.36 -12.57

10 Maharastra Scooters Ltd 25.90 1.67 -3.23

11. TVS Motors India Ltd 45.97 3.00 -17.28

12. Hero Honda Motors Ltd 201.02 0.92 24.94

Two and Three Wheelers Sectors 203.65 0.92 -2.21

Whole Automobile Industry 122.54 1.86 -6.15

Source: Computed

221

EVA based ranking of selected companies

Table 6.1 also presents EVA-based ranking of sample companies. It is

evident from the table that companies like Tata Motors Ltd, Ashok Leyland

Ltd are toping in the list during the study period. On the other hand

companies like Hindustan Motors Ltd and Daewoo Motors India Ltd have

been loosing the grounds. Rest of the companies have indexed unsteady

position during the study period.

EVA based frequencies distribution of sample companies are shown in

Table 6.2. It is clear from that seven companies in 1998-99, 2002-03, two in

2003-04 and one company in 2004-05, 2005-06 are reporting negative EVA

and the remaining companies are generating positive EVA during the study

period. It is also observed that more than 33 1/3 per cent of the companies

have added to the economic value between Rs.100-500 crores during the

study period and only two companies in 1995-96, three in 1997-98, four in

1999-2000, two in 2001-02 and one in 2002-03 reported an EVA of over

Rs.500 crores.

Sector wise trends in EVA

Table 6.3 presents sector wise EVA of sample companies. It is evident

from Table 6.3 that the mean EVA generated for the automobile industry is

Rs.122.54 crores during the study period. The mean EVA generated is highest

in two and three wheelers sectors followed by commercial vehicles sectors

and passenger cars and multiutility vehicles sector. Two and three wheelers

sector and commercial vehicles sector should perform well in this regard

because their average is more than the industry average. It is also evident

from the table that all selected sectors and whole industry witnessed very high

fluctuation in their EVA during the study period. Table 6.3 further reported

that the commercial vehicles, passenger cars and multi-utility vehicle sector

and few of two and three wheelers sectors and whole industry registered

negative compound annual growth rate of EVA during the study period.

222

223

The economic value added of selected industry under commercial

vehicles sector during the study period is presented in Table 6.3. The mean

EVA was highest in Ashok Leyland Ltd followed by Tata Motors Ltd, Eicher

Motors Ltd and Swaraj Mazda Ltd. All the industry under the sector had

registered very high fluctuation in their EVA during the study period. It is

also evident from the table that Tata Motors Ltd registered negative

compound annual growth rate of EVA during the study period.

Table 6.3 also depicts the EVA generated by the selected companies

under passenger cars and multiutility vehicles sector during the study period.

It portrays that Daewoo Motors India Ltd showed negative EVA throughout

the study period. The mean of Mahindra and Mahindra Ltd was highest

followed by Maruthi Udyog Ltd and Hindustan Motors Ltd. All the

companies registered very high fluctuation in their EVA during the study

period. All the companies witnessed negative compound annual growth rate

of EVA.

The EVA generated by the companies under two and three wheeler

sector during the study period is presented in Table 6.3. It is evident from the

table that the mean of Bajaj Auto Ltd was highest followed by Hero Honda

Motors Ltd, TVS Motors Company Ltd and Maharastra Scooters Ltd. All the

companies registered very high fluctuation in their EVA during the study

period. The compound annual growth rate of all companies was negative

except Hero Honda Motors Ltd during the study period.

The sector wise paired test provides the value of t test in Table 6.4. The

table exhibits that there has been significant deviation (at 5% level) in the

EVA of respective years except for the year 2001-2002 to 2004-2005.

224

225

Comparison of EVA and conventional method of financial performance

Analysing the corporate performance of Indian automobile industry

based on Return On Capital Employed (ROCE) the conventional benchmarks

and on the new “trendier” one i.e., EVA, the results can be well exhibited in

Table 6.5. From the table, it can be inferred that Indian automobile industry

depicts a ROCE picture in terms of return on capital employed. The mean

value of return on capital employed of automobile industry during the study

period 24.51 per cent i.e., for every Rs.100 investment, the return is Rs.24.51

whereas EVA as a percentage of capital employed is only 7.04 i.e for every

Rs.100 investment the company has added value of Rs.7.04. The same picture

is reflected as in case of all three sectors. Thus, the comparison shows that

divergence is less existent between the performance results given by

traditional measure and EVA. However, the traditional measures do not

reflect the real value addition to shareholders wealth and thus EVA has to be

measured to have an idea about the shareholders value addition.

Market Value Added (MVA) of selected companies

The MVA explains the value added to a particular equity share over its

book value. It informs how much value has been added in the economic value

of the shareholders. In view of that, a company with an objective of pleasing

to the eyes of the shareholders wealth should endeavor to take advantage of

its MVA. MVA can be estimated by subtracting the book value of shares from

the market value of shares. It is silent that EVA helps in pushing up the MVA

of an organisation. Thus, EVA can be considered as an internal measure and

MVA as the external measure of a company’s financial performance.

Table 6.6 presents MVA calculation of selected companies of Indian

automobile industry. On the base of the table, it may be observed that out of

12 companies, 11 companies have registered positive MVA throughout the

226

227

228

study period. It indicates that the market value of these companies is

dominating over the book value. On the other hand, Hindustan Motors Ltd

(1997-98, 1999-00 to 2001-02), Daewoo Motors India Ltd (1997-98, 1999-00

to 2003-04) have registered negative MVA during the study period. It shows

that the book value of these companies is dominated over the market value.

MVA based ranking of selected companies

Table 6.6 also provides MVA based ranking. Glancing all the way

through the table, it is noticed that all companies like Maruthi Udyog Ltd,

Bajaj Auto Ltd, Hero Honda Motors Ltd, Tata Motors Ltd, Ashok Leyland

Ltd are topping the list and on the other side companies like Daewoo Motors

India Ltd, Swaraj Mazda Ltd and Maharastra Scooters India Ltd, are

struggling in terms of MVA over the period.

Sector wise trends MVA

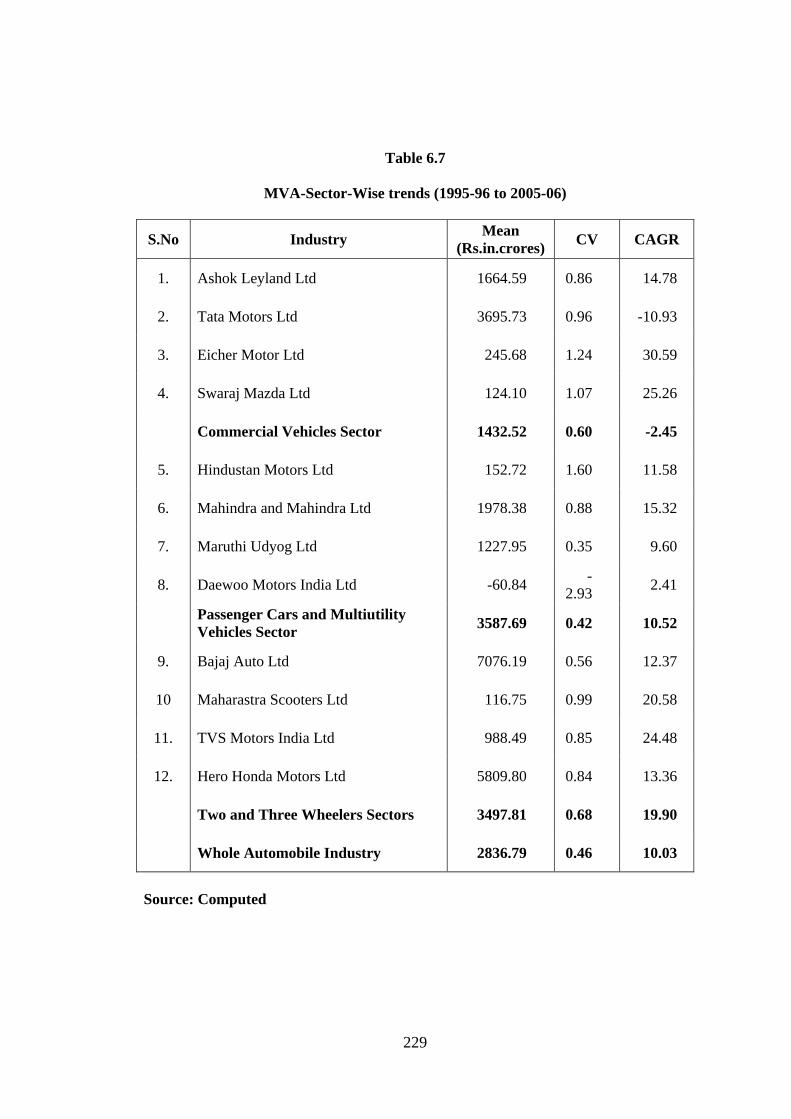

Table 6.7 portrays whole automobile industry and sector wise

information pertaining to MVA. It is evident from Table 6.7 that among the

three sectors, passenger cars and multiutility vehicles sector have been

generating highest market value added throughout the study period. This was

due to better market value added of Maruthi Udyog Ltd and Mahindra and

Mahindra Ltd. It was followed by two and three wheeler sector. Table 6.7 also

shows that all the selected sectors of automobile industry have been

generating aggregate MVA throughout the period. The growth of MVA is

consistent in case of passenger cars and multiutility vehicles whereas less

consistent in case of commercial vehicles and two and three wheelers sector.

Table also brings out that only the commercial vehicles sector had registered

negative compound annual growth rate of MVA during the study period.

229

Table 6.7

MVA-Sector-Wise trends (1995-96 to 2005-06)

S.No Industry Mean

(Rs.in.crores) CV CAGR

1. Ashok Leyland Ltd 1664.59 0.86 14.78

2. Tata Motors Ltd 3695.73 0.96 -10.93

3. Eicher Motor Ltd 245.68 1.24 30.59

4. Swaraj Mazda Ltd 124.10 1.07 25.26

Commercial Vehicles Sector 1432.52 0.60 -2.45

5. Hindustan Motors Ltd 152.72 1.60 11.58

6. Mahindra and Mahindra Ltd 1978.38 0.88 15.32

7. Maruthi Udyog Ltd 1227.95 0.35 9.60

8. Daewoo Motors India Ltd -60.84 -

2.93 2.41

Passenger Cars and Multiutility

Vehicles Sector 3587.69 0.42 10.52

9. Bajaj Auto Ltd 7076.19 0.56 12.37

10 Maharastra Scooters Ltd 116.75 0.99 20.58

11. TVS Motors India Ltd 988.49 0.85 24.48

12. Hero Honda Motors Ltd 5809.80 0.84 13.36

Two and Three Wheelers Sectors 3497.81 0.68 19.90

Whole Automobile Industry 2836.79 0.46 10.03

Source: Computed

230

231

The market value added of selected companies under commercial

vehicles sector during the study period is also presented in Table 6.7. This

table reveals that the mean MVA of Tata Motors Ltd were the highest

followed by Ashok Leyland Ltd, Eicher Motors Ltd and Swaraj Mazda Ltd.

Table 6.7 brings out that all the selected companies under the commercial

vehicles sector had registered very high fluctuations in their MVA during the

study period.

Table 6.7 presents MVA of selected companies under passenger cars

and multiutility vehicles sector. The table shows that the companies like

Maruthi Udyog Ltd and Mahindra and Mahindra Ltd are top in the list and it

was followed by Hindustan Motors Ltd and Daewoo Motors India Ltd. All the

selected companies except Maruthi Udyog Ltd has registered very high

fluctuation in their MVA during the study period. Table 6.7 brings out values

relating to compound annual growth rate of MVA selected companies. It is

evident from the table that all the companies had registered positive growth,

rate of MVA during the study period.

Table 6.7 brings out the values relating to MVA of selected companies

under two and three wheelers. Table 6.7 showed that Bajaj Auto Ltd, Hero

Honda Motors Ltd are comparatively top in the list. On the other hand,

Maharashtra Scooters Ltd are struggling on their front with regard to MVA

during the study period. It is also noticed that all the selected companies have

registered very high fluctuations in their MVA during the study period. The

analysis of compound annual growth rate of MVA showed mixed trend

during the study period.

The sector-wise paired test provided the value of the t test in Table 6.8.

The table exhibits that there has been no significant deviation in MVA in

respect of years except for the year 1995-96, 2003-04 and 2004-05.

232

MVA vis-a-vis other financial variables-Linear Regression and Multiple

Regression Analysis

In this section an attempt to find the relevance of Stern and Stewart’s

claim that MVA of the firm is largely positive association with or driven by

its EVA generating capacity and other financial variables like EPS, ROCE,

NOPAT and RONW. Based on the sample of 12 companies of Indian

automobile industry for a period of 11 years, the analysis of this section is

divided into two parts: in the first part, the linear regression analysis between

dependent and particular selected independent variables (s) has been

examined and in the second part multiple regression analysis between MVA

and other financial variables has been looked at for the selected sectors of

automobile industry during the study period.

Linear Regression Analysis of MVA and selected Financial Variables

In this section, results of correlation co-efficient, linear regression,

Durbin-Watson Model, F-Statistics and t-statistics have been determined

between dependent variable (MVA) and Independent variables. The values

hence obtained have their particular statistical sense. The regression co-

efficient for independent variables like EVA, EPS, ROCE, NOPAT and

RONW so worked out portray the temperament of association between the

dependent and particular independent variable. The F statistics and t statistics

so calculated determine the level of significance and insignificance being

associated between the variables. Durbin-Watson Model allows the researcher

to establish the auto-correlation, if any between dependent and independent

variable (the desirable value is two and any value more than two signifies

negative auto-correlation and vice-versa); values of adjusted R2 indicate the

extent of variation in the dependent variable which may be explicated by

independent variables and the standard error speaks about the limits within

which the estimated value as the dependent variable is expected to lie.

233

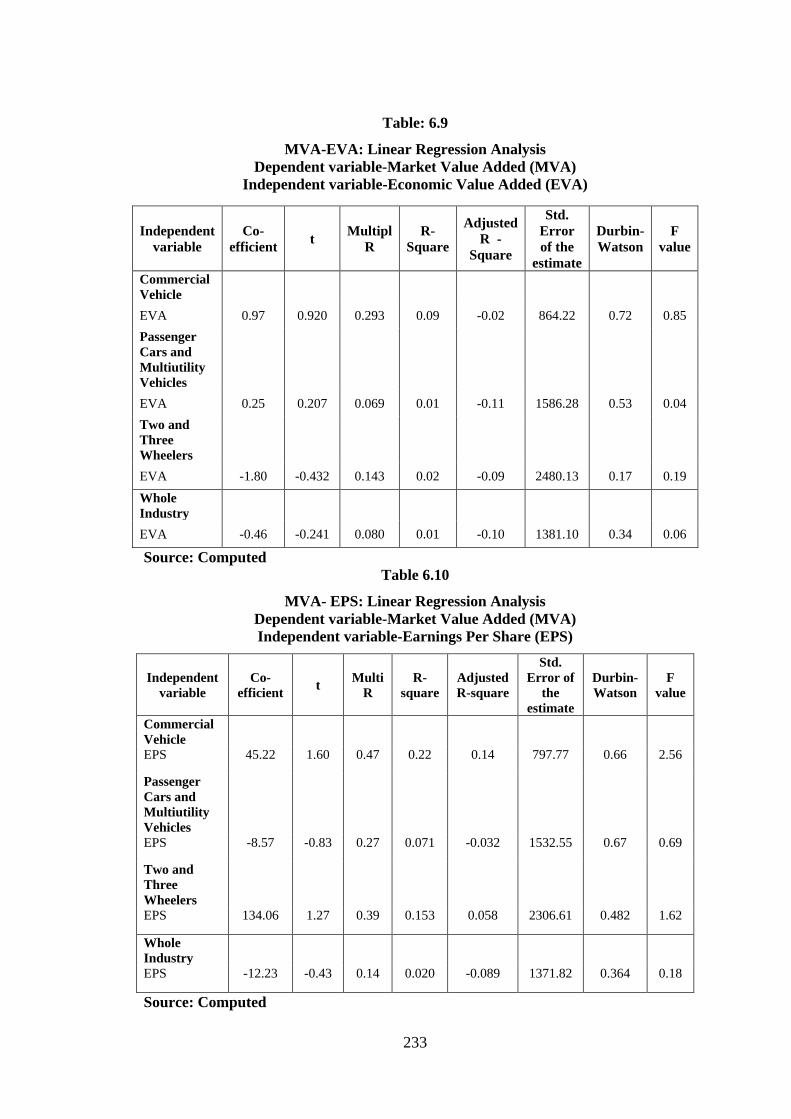

Table: 6.9

MVA-EVA: Linear Regression Analysis

Dependent variable-Market Value Added (MVA)

Independent variable-Economic Value Added (EVA)

Independent

variable

Co-

efficient t

Multipl

R

R-

Square

Adjusted

R -

Square

Std.

Error

of the

estimate

Durbin-

Watson

F

value

Commercial

Vehicle

EVA 0.97 0.920 0.293 0.09 -0.02 864.22 0.72 0.85

Passenger

Cars and

Multiutility

Vehicles

EVA 0.25 0.207 0.069 0.01 -0.11 1586.28 0.53 0.04

Two and

Three

Wheelers

EVA -1.80 -0.432 0.143 0.02 -0.09 2480.13 0.17 0.19

Whole

Industry

EVA -0.46 -0.241 0.080 0.01 -0.10 1381.10 0.34 0.06

Source: Computed

Table 6.10

MVA- EPS: Linear Regression Analysis

Dependent variable-Market Value Added (MVA)

Independent variable-Earnings Per Share (EPS)

Independent

variable

Co-

efficient t

Multi

R

R-

square

Adjusted

R-square

Std.

Error of

the

estimate

Durbin-

Watson

F

value

Commercial

Vehicle

EPS 45.22 1.60 0.47 0.22 0.14 797.77 0.66 2.56

Passenger

Cars and

Multiutility

Vehicles

EPS -8.57 -0.83 0.27 0.071 -0.032 1532.55 0.67 0.69

Two and

Three

Wheelers

EPS 134.06 1.27 0.39 0.153 0.058 2306.61 0.482 1.62

Whole

Industry

EPS -12.23 -0.43 0.14 0.020 -0.089 1371.82 0.364 0.18

Source: Computed

234

MVA-EVA Analysis

Table 6.9 offers the explanation about the regression on analysis

between MVA and EVA during the study period for the whole automobile

industry and its three sectors. Table 6.9 provides the values of R, R-square

and adjusted R2 for the whole industry 0.080, 0.01, -0.10 respectively. It

sounds that there exists poor relationship between MVA and EVA in

automobile industry, as the value of R-square is negative. Interestingly, the t

and F statistics give the identical results but both of them lead to insignificant

association between the variables under reference. It is evident from the table

that the overall result in passenger cars and multiutility vehicles does not

differ from whole industry and statistical association between MVA and EVA

is again insignificant. Tables 6.9 suggest that the adjusted R2 value is negative

in all cases in all the selected sectors of Indian automobile industry.

MVA-EPS Analysis

The linear regression analysis between MVA and EPS is presented in

Table 6.10 for the study period. It is evident from the Table 6.10 that the

correlation co-efficient between MVA and EPS during the study period is

0.14 and the value of R-Square and adjusted R-Square is very low and may

not be adequate for the fitness of the model. The t and F statistics suggest that

the association between MVA and EPS of automobile industry is not

significant and EPS does not suitably explain MVA. It is evident from the

table that the correlation co-efficient between MVA and EPS in passenger

cars and multiutility vehicles is 0.27 and the adjusted R-Square value is

negative. This shows the poor fitness of the model. Both t statistics and F

statistics certify that the association between these two variables is

insignificant as presented in the table. The t and F statistics are resulting

identical values and secured that EPS of commercial vehicles sector has been

able to describe MVA in better term than the other sectors. The overall results

showed that EPS is positively associated with MVA in all the three sectors

and the whole industry during the study period.

235

Table: 6.11

MVA-ROCE: Linear Regression Analysis

Dependent Variable: Market-Value Added (MVA)

Independent Variable: Return on capital employed (ROCE)

Independent

variable

Co-

efficient t

Multiple

R

R-

square

Adjusted

R-

Square

Std.

Error of

the

estimate

Durbin-

Watson

F

value

Commercial

Vehicle

ROCE 10.493 0.380 0.126 0.02 -0.09 896.80 0.72 0.14

Passenger

Cars and

Multiutility

Vehicles

ROCE 6.359 0.125 0.042 0.01 -0.11 1588.68 0.55 0.02

Two and

Three

Wheelers

ROCE 47.853 0.659 0.214 0.05 -0.06 1353.34 0.34 0.43

Whole

Industry

ROCE -125.179 -0.968 0.307 0.10 -0.01 2384.55 0.35 0.94

Source: Computed

Table 6.12

MVA-NOPAT: Linear Regression Analysis

Dependent Variable: Market-Value Added (MVA)

Independent Variable: Net operating profit after tax (NOPAT)

Independent

variable

Co-

efficient t

Multi

R

R-

square

Adjusted

R-square

Std.

Error of

the

estimate

Durbin-

Watson

F

value

Commercial

Vehicle

NOPAT 3.167 1.745 0.503 0.253 0.170 781.38 0.652 3.045

Passenger

Cars and

Multiutility

Vehicles

NOPAT 9.042 3.758 0.782 0.611 0.568 992.03 0.702 14.12

Two and

Three

Wheelers

NOPAT 18.422 13.997 0.978 0.956 0.951 525.12 2.360 195.92

Whole

Industry

NOPAT 10.478 8.942 0.948 0.899 0.888 440.71 1.201 79.96

Source: Computed

236

MVA-ROCE Analysis

Table 6.11 offers the explanation about the regression analysis between

MVA and ROCE during the study period for the whole automobile industry

and its three sectors. Table 6.11 provides the values of R, R-Square and

adjusted R-Square which are 0.307, 0.10, -0.01 respectively. It sounds that the

value is very low and may not be adequate for the fitness of the model. The

results of whole industry are similar to passenger cars and multiutility

vehicles. Table 6.11 suggests that the variables are clearly correlated in two

and three wheelers but the adjusted R-Square value is negative. However, in

case of passenger cars and multiutility vehicles and commercial vehicles

sector the value of R, R-Square and adjusted R-Square showed that the values

have resulted in poor relationship between MVA and ROCE in these sectors.

The overall results showed that ROCE is negatively associated with MVA in

all the whole industry during the study period.

MVA-NOPAT Analysis

Linear regression analysis between MVA and NOPAT is presented in

Table 6.12. In Table 6.12 the statistical association between MVA and

NOPAT of all the three sectors and the whole industry are provided. The table

reveals that the value of R, R-Square and adjusted R-Square are high and it

may be adequate for the fitness of the model in case of whole industry,

passenger cars and multiutility vehicles sector and two and three wheelers

sector. The t and F statistics also suggest that the association between MVA

and NOPAT is significant and NOPAT is suitable to explain the MVA of

these sectors and the whole industry during the study period. The table reveals

that the value of adjusted R-Square is very low and it may not be adequate for

the fitness of the model, the t and F statistics also suggest that the association

between the MVA and NOPAT is not significant. The overall analysis

showed that NOPAT is positively associated with MVA in all the three

sectors and whole industry.

237

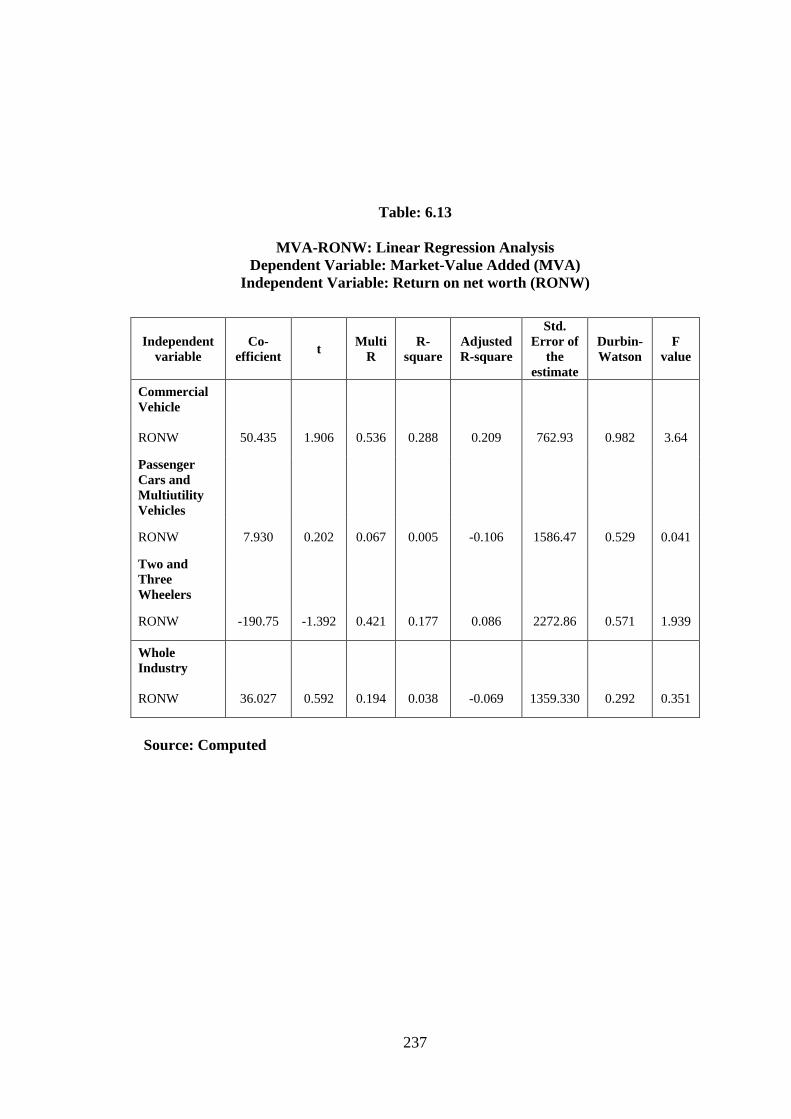

Table: 6.13

MVA-RONW: Linear Regression Analysis

Dependent Variable: Market-Value Added (MVA)

Independent Variable: Return on net worth (RONW)

Independent

variable

Co-

efficient t

Multi

R

R-

square

Adjusted

R-square

Std.

Error of

the

estimate

Durbin-

Watson

F

value

Commercial

Vehicle

RONW 50.435 1.906 0.536 0.288 0.209 762.93 0.982 3.64

Passenger

Cars and

Multiutility

Vehicles

RONW 7.930 0.202 0.067 0.005 -0.106 1586.47 0.529 0.041

Two and

Three

Wheelers

RONW -190.75 -1.392 0.421 0.177 0.086 2272.86 0.571 1.939

Whole

Industry

RONW 36.027 0.592 0.194 0.038 -0.069 1359.330 0.292 0.351

Source: Computed

238

MVA and RONW Analysis

Table 6.13 tenders the elucidation concerning the regression analysis

between the MVA and RONW during the study period. The table 6.13

provides the values of R, R-Square and adjusted R-Square. Table 6.13

suggests that variables are clearly correlated in the whole industry,

commercial vehicles and two and three wheelers sectors and adjusted R-

Square value is positive in two cases. In passenger cars and multiutility

vehicles the value of R, R-Square, adjusted R-Square value is positive in two

cases. In passenger cars and multiutility vehicles the vale of R, R-square,

adjusted R-Square are 0.067, 0.005 and -0.106 respectively. It sounds that

there exists poor relationship between MVA and RONW in passenger cars

and multiutility vehicles sector. The t and F statistics also give identical

results but both of them lead to insignificant association between them. The

overall analysis showed that RONW is negatively associated with MVA only

in case of two and three wheelers sectors during the study period.

MVA vis-à-vis other financial variables-Multiple Regression Analysis

The evidence of the majority of empirical study regarding EVA

suggests that there is a positive relationship between EVA and MVA.

However, when the explaining power of EVA versus traditional performance

measures regarding return is considered, the results are mixed. This is in

continuation with the analysis made in the previous past, an attempt has been

made in this part to find out sector-wise trends as far as the factors affecting

MVA are concerned. The purpose of this analysis whether a particular

independent variable or a set of variables emerges as the most explanatory

variable of the MVA during the study period. In order to meet this objective,

multiple regression analysis has been considered on sector-wise and whole

industry during the study period. The results of multiple regression analysis

are presented in this section.

239

Table: 6.14

Determinants of Market Value Added-Multiple Regression Analysis

(Automobile Industry)

Dependent Variable: Market Value Added (MVA)

Independent variable Co-efficients t-value Significant /

Not significant

Constant 2113.97 4.101

EVA 0.14 1.983 Significant**

EPS 28.76 3.773 Significant*

ROCE 128.89 2.648 Significant*

NOPAT 11.16 5.588 Significant*

RONW 100.48 2.234 Significant*

R2 = 0.98

Adj R2 = 0.97

F = 55.91

DW = 1.88

EVA-Economic Value Added; EPS - Earnings Per share;

ROCE-Return on capital employed; NOPAT-Net operating profit after tax;

RONW-Return on Net worth.

* - significant at 0.05 level; ** - significant at 0.10 level

Source: computed.

Table: 6.15

Determinants of Market Value Added-Multiple Regression Analysis

(Commercial Vehicles)

Dependent Variable: Market Value Added (MVA)

Independent variable Co-efficient t-value Significant /

Not significant

Constant 464.51 1.880

EVA 0.66 2.910 Significant*

EPS 38.87 2.864 Significant*

ROCE 108.88 3.157 Significant*

NOPAT 1.63 1.534 Significant**

RONW 150.79 3.671 Significant*

R2 = 0.81

Adj R2 = 0.63

F = 4.38

DW = 3.09

EVA-Economic Value Added; EPS - Earnings Per share;

ROCE-Return on capital employed; NOPAT-Net operating profit after tax;

RONW-Return on Net worth.

* - significant at 0.05 level ; ** - significant at 0.10 level

Source: computed.

240

Whole Industry

Table 6.14 brings out the determinants of market value added for

whole automobile industry during the study period. It is observed from the

Table 6.14 that all the selected independent variables exerts significant

influence on MVA of automobile industry during the study period. Co-

efficient of determination, R2 in the case 0.98 implies that changes in MVA

are predicted by these independent variables to the extent of 98 per cent. It is

also evident from the table that ROCE is found in strong association with

MVA followed by RONW, EPS, NOPAT and EVA. From the value of

adjusted R2 and F value regression results, it can be concluded that all the

selected independent variables well explain the MVA of automobile industry

during the study period.

Commercial Vehicles

Table 6.15 portrays the results of multiple regression analysis for

commercial vehicles sector. It is revealed from the table that the co-efficient

of determination, R2 value which is 0.81 implies that change in MVA can be

predicted by these independent variables to the extent of 81 per cent only. It is

also found that RONW is strongly associated with MVA followed by ROCE,

EPS, NOPAT and EVA during the study period. The value of F statistic and

adjusted R2 showed the good fitness of the model.

Passenger Cars and Multiutility Vehicles

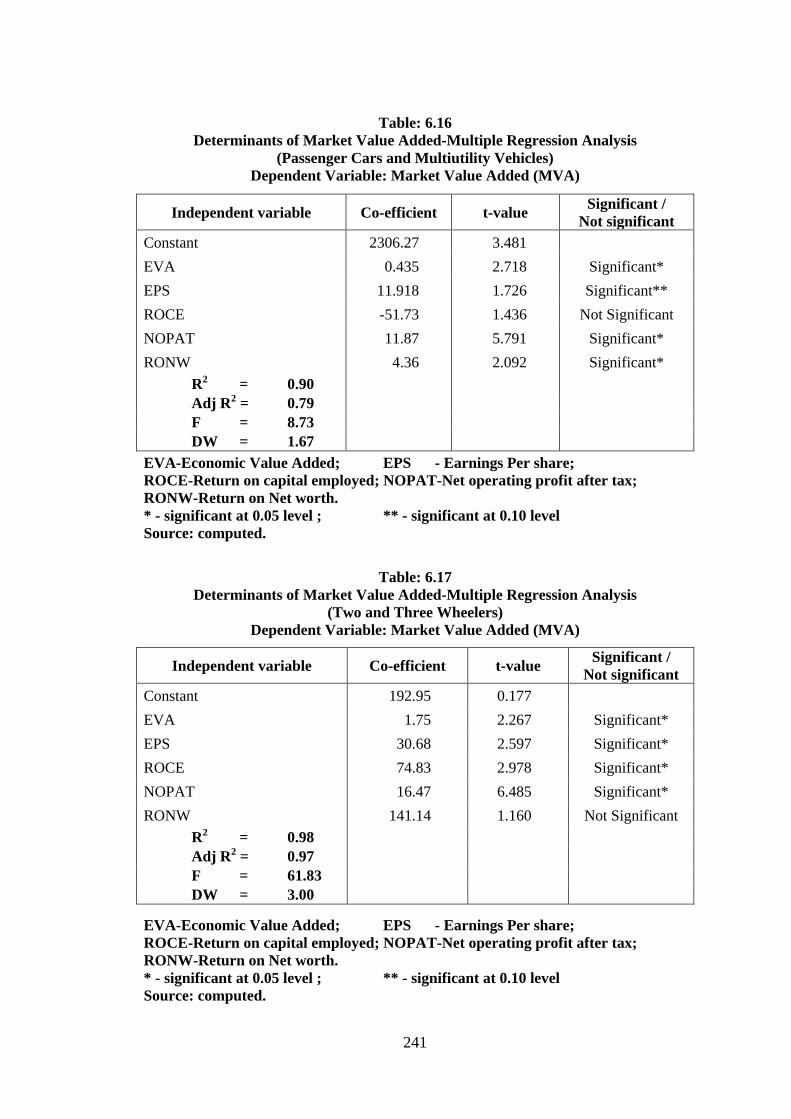

Table 6.16 gives an account of multiple regression analysis between

MVA and other financial variables in respect of passenger cars and

multiutility vehicles sector. The result provided by this table witnessed that

the variables noticed significantly associated with MVA are EPS, NOPAT,

RONW and EVA. The co-efficient of determination, R2 in this case is 0.90

implying that change in MVA is predicted by these independent variables to

the extent of 90 per cent. The value of R2 and F shows the good fitness of the

model.

241

Table: 6.16

Determinants of Market Value Added-Multiple Regression Analysis

(Passenger Cars and Multiutility Vehicles)

Dependent Variable: Market Value Added (MVA)

Independent variable Co-efficient t-value Significant /

Not significant

Constant 2306.27 3.481

EVA 0.435 2.718 Significant*

EPS 11.918 1.726 Significant**

ROCE -51.73 1.436 Not Significant

NOPAT 11.87 5.791 Significant*

RONW 4.36 2.092 Significant*

R2 = 0.90

Adj R2 = 0.79

F = 8.73

DW = 1.67

EVA-Economic Value Added; EPS - Earnings Per share;

ROCE-Return on capital employed; NOPAT-Net operating profit after tax;

RONW-Return on Net worth.

* - significant at 0.05 level ; ** - significant at 0.10 level

Source: computed.

Table: 6.17

Determinants of Market Value Added-Multiple Regression Analysis

(Two and Three Wheelers)

Dependent Variable: Market Value Added (MVA)

Independent variable Co-efficient t-value Significant /

Not significant

Constant 192.95 0.177

EVA 1.75 2.267 Significant*

EPS 30.68 2.597 Significant*

ROCE 74.83 2.978 Significant*

NOPAT 16.47 6.485 Significant*

RONW 141.14 1.160 Not Significant

R2 = 0.98

Adj R2 = 0.97

F = 61.83

DW = 3.00

EVA-Economic Value Added; EPS - Earnings Per share;

ROCE-Return on capital employed; NOPAT-Net operating profit after tax;

RONW-Return on Net worth.

* - significant at 0.05 level ; ** - significant at 0.10 level

Source: computed.

242

Two and Three wheelers

Table 6.17 describes the results of multiple regressions for

determinants of MVA for two and three wheelers sector during the study

period. It is explicit from the table that all the independent variables are

significantly associated with MVA of two and three wheelers sector during

the study period. Co-efficient of determination, R2 in this case in 0.98

implying that changes in MVA is predicted by selected independent variables

to the extent of 97 per cent. RONW is strongly associated with MVA

followed by ROCE, EPS, NOPAT and EVA. The value of t, F and R2 sounds

the good fitness of the model.