ACQUISITIONS & GRANTS OFFICE

Personal Property Lease Determination Worksheet Training

This training presents the Acquisitions and Grants Office’s (AGO) policy and procedures related to Leases and the

Lease Determination Worksheet.

This is not the policy and procedures of Ernst & Young, LLP.

Objectives

• To obtain a better understanding of leases including:– Terminology;– Applicable laws and regulations; and– Classification.

• To obtain a working knowledge of the lease determination worksheet, including:– Part A and Part B; and– Related appendices.

Why are we here?

• Leases are an integral part of NOAA’s financial statements.

• Therefore, leases are subject to the Chief Financial Officer’s (CFO) Act and audit.

• Completion of the worksheet is necessary to comply with regulations – Office of Management and Budget (OMB)– Federal Accounting Standards Advisory Board

(FASAB)– CFO Act

Definition

• Lease:– An agreement conveying the right to use

property, plant, or equipment usually for a stated period of time. (FASB 13, paragraph 1)

• Also includes:– Licenses– Permits– Memorandums of Understanding (MOUs)– Interagency service agreements

Two Different Regulations

• Budget:– Concerned with scoring.– OMB Circular No. A-11, Appendix B, Scoring Lease-

Purchases and Leases of Capital Assets

• Accounting:– Concerned with correctly reflecting the asset on

financial statements.– SFFAS 6, Accounting for Property, Plant, and

Equipment (FASAB)– FAS 13, Accounting for Leases, and related

amendments (FASB)

Lease Scoring

• Budget Authority – the authority provided by law to incur financial obligations that will result in outlays

• Outlays - a payment to liquidate an obligation; measure of Government spending.

Funding

• Anti-Deficiency Act:– Requires adequate budget authority before

entering into a contract or other obligation for payment.

• OMB:– Requires full funding or budget authority for an

useful segment or an entire project, which could be several contracts.

Budgeting for Leases

• Operating Lease:– Ownership of the asset remains with owner (Lessor).– The lease does not contain a bargain-price purchase

option.– Term of lease doesn’t exceed 75% of economic life of

asset.– The PV of minimum lease payments does not exceed

90% of asset’s “fair market value” (see A-11 definition) at inception of the lease.

– General purpose asset (not built for Government-specific purpose).

– Private sector market for asset.

Budgeting for Leases (cont.)

• Lease-purchase: Lease that transfers ownership.– Without substantial private risk.– With substantial private risk.

• Capital Lease: Any lease other than a lease-purchase that does not meet the criteria of an operating lease.

• OMB does not mention anything about skipping criteria if the lease is in the last 25% of the useful life.

• No specifics related to the type of property leased.

Accounting for Leases

• Criteria for Capital Leases:– Transfers ownership of the property at the end

of the lease.– Option to purchase property at a bargain price.– Lease term is equal to or greater than 75% of

estimated economic life.– Present value of minimum lease payments,

excluding executory costs, equals or exceeds 90% of fair value of the property.

Accounting for Leases (cont.)

• Operating Leases:– Does not assume the risks of ownership of the

property.– Does not meet any of the four criteria for a

capital lease.

• If the lease is in the last 25% of its useful life, then criteria 3 & 4 (from the previous slide) do not apply.

Types of Leases

Budget Accounting

Type of Lease: OMB FASAB FASB

Capital Lease Yes Yes Yes

Lease-Purchase Yes No No

Operating Lease Yes Yes Yes

Capital and Operating Leases: A Research Report (FASAB – Oct. 2003)

NOAA Regulations

• Capitalization threshold– $200,000

• Depreciable useful life– 2 years

• Types of Leases– Operating– Capital, but not capitalizable– Capital and capitalizable

Differences

• Number of criteria to determine lease type

• Types of leases

• Interest Rates:– Date– Treasury or Contractor

• Bargain Purchase Option

Lease Determination Worksheet

• Necessary to address the regulations and the CFO Act.

• Two parts to the worksheet to address each regulation.– Part A addresses budgeting.– Part B addresses accounting.– Each part is divided into sections (e.g. A.1,

A.1, B.1, B.2)• Each section addresses a specific topic or criteria

(e.g. economic life, net present value, etc.)

Worksheet (cont.)

• Completed by Requisitioner or COTR

• Reviewed by AGO Headquarters

• Needs to be completed when total lease payments over the life of the lease (including option years) is greater than $200,000.

• Lease Handbook provides detail instructions on completing the worksheet.

Worksheet (cont.)

• Part A (Budget) of the worksheet is to be completed:– Pre-award

• Could be several times during the process, but definitely during the final negotiations

– At time of award– Post award, if change to financial structure of

lease occurs (i.e. change in lease term, change in payment stream)

Worksheet (cont.)

• Part B (Accounting) of the worksheet is to be completed:– Pre-award

• During the final negotiations

– At time of award– Post award, if change to financial structure of

lease occurs

Worksheet (cont.)

• Excel spreadsheet

• Separate tabs for each part and appendix

• Ability to link data

• Formulas are already in the spreadsheet, as applicable

• Yellow highlights denote cells to be filled in

Information Needed

• Lease begin date• Date contract/lease

signed by Government

• Lease end date• Number of option

years• Economic useful life• Improvements/

upgrades

• Lease payment stream

• Interest rate• Fair market value• Transfer of

ownership?• Bargain Purchase

option?

LDW – Part ALease Information

• Requisition Number

• Solicitation Number

• Description of Leased Property– Including manufacturer and model number– Including Line/Staff/Corporate Office

LDW – Part ALease Information (cont.)

• Revision– Provide explanation if revisions

• New information (i.e. modification to lease)• Error in previous worksheet

– Date of revision

LDW – Section A.1General Information

• Real versus Personal Property

• Leases with another Federal agency– Reasonable assertion of effort

LDW – Section A.2Economic Useful Life

• Multiple Assets within lease– Sum of present values of lease payments for

each asset discounted back to the date that the asset is delivered

– Recommend individual worksheet for each asset if they are different pieces of property and have different delivery dates

LDW – Section A.2Useful Life (cont.)

• Dates– Lease beginning date or date of first payment– Date contract/lease signed– Lease end date, including all option periods– Base term– Option years, including increments– Total lease term

LDW – Section A.2Useful Life (cont.)

• Age of asset

• NOAA’s suggested economic useful life

• Renovations/upgrades– Years that renovations/upgrades extend the

useful life.

• Estimated remaining economic useful life

• One of the six lease criteria

LDW – Section A.3Present Value Calculation

• Payment Periods– Annually, quarterly, monthly

• Annuity Due/Ordinary Annuity– Payment at the beginning or the end of the

period

• Payment Amounts– Executory costs (taxes, maintenance, and

insurance)– Appendix A (example on next slide)

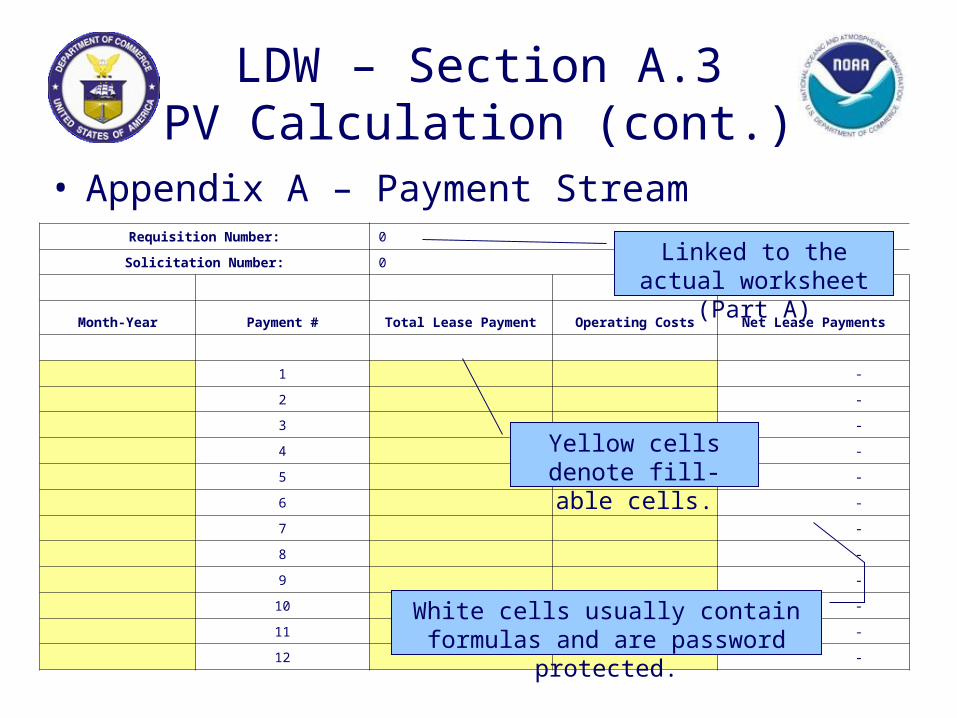

LDW – Section A.3PV Calculation (cont.)

• Appendix A – Payment StreamRequisition Number: 0

Solicitation Number: 0

Month-Year Payment # Total Lease Payment Operating Costs Net Lease Payments

1 -

2 -

3 -

4 -

5 -

6 -

7 -

8 -

9 -

10 -

11 -

12 -

Yellow cells denote fill-able

cells.

Linked to the actual worksheet (Part A)

White cells usually contain formulas and are password

protected.

LDW – Section A.3PV Calculation (cont.)

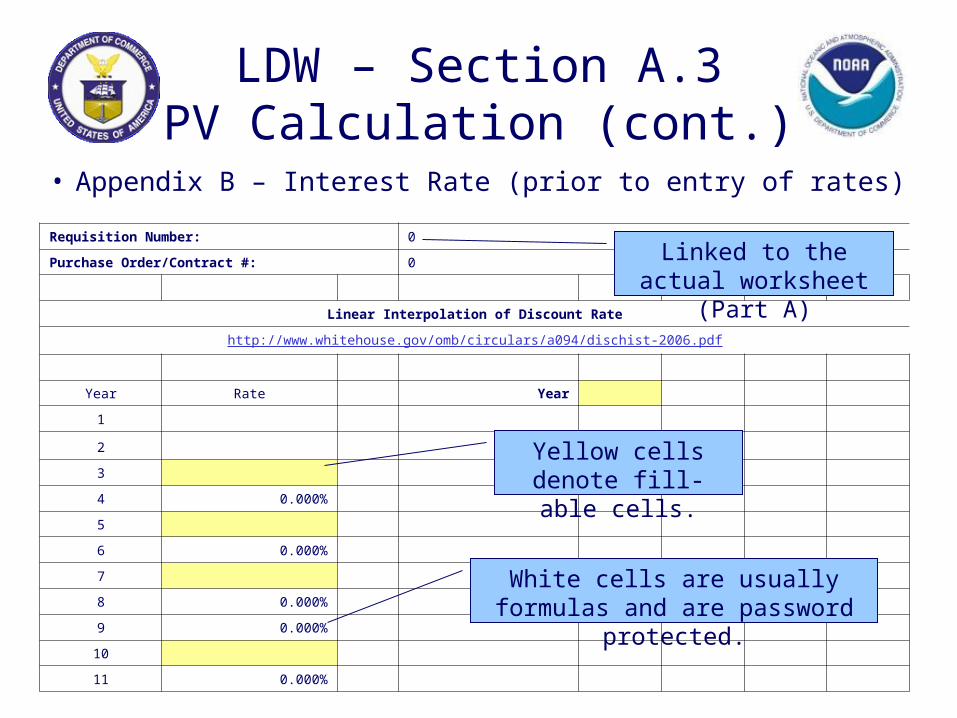

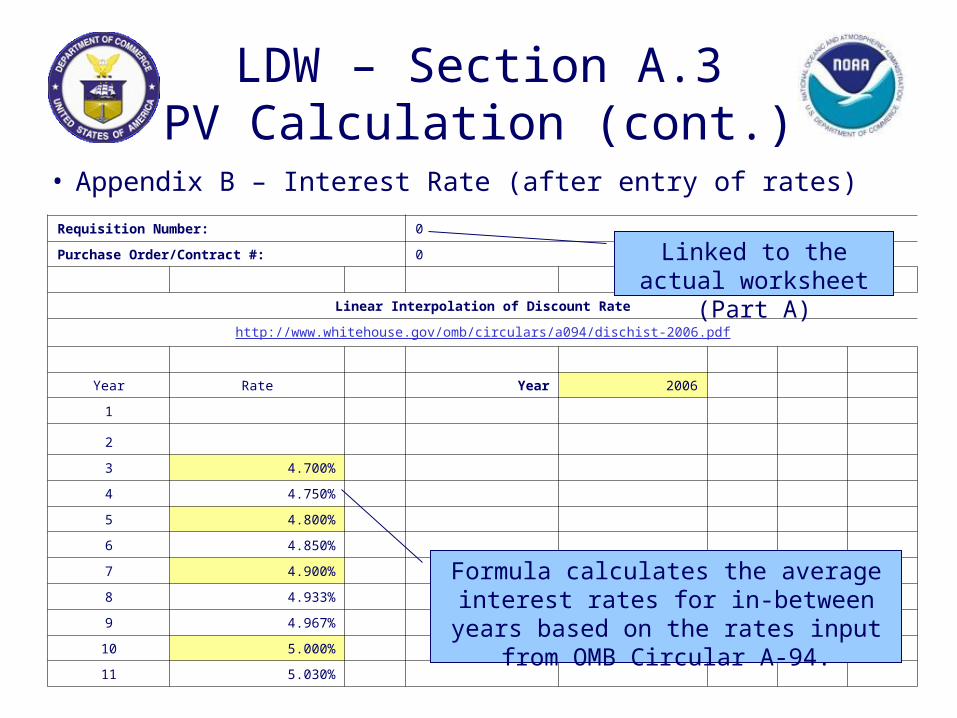

• Interest Rate (www.whitehouse.gov/omb)– Date lease signed– Appendix B

• FMV– Usually quote, GSA schedule or catalog price– Appendix C

• Blank spreadsheet• Use if need to add several costs together to

determine the FMV

LDW – Section A.3PV Calculation (cont.)

• Appendix B – Interest Rate (prior to entry of rates)Requisition Number: 0

Purchase Order/Contract #: 0

Linear Interpolation of Discount Rate

http://www.whitehouse.gov/omb/circulars/a094/dischist-2006.pdf

Year Rate Year

1

2

3

4 0.000%

5

6 0.000%

7

8 0.000%

9 0.000%

10

11 0.000%

Linked to the actual worksheet (Part A)

Yellow cells denote fill-able

cells.

White cells are usually formulas and are password protected.

LDW – Section A.3PV Calculation (cont.)

• Appendix B – Interest Rate (after entry of rates)Requisition Number: 0

Purchase Order/Contract #: 0

Linear Interpolation of Discount Rate

http://www.whitehouse.gov/omb/circulars/a094/dischist-2006.pdf

Year Rate Year 2006

1

2

3 4.700%

4 4.750%

5 4.800%

6 4.850%

7 4.900%

8 4.933%

9 4.967%

10 5.000%

11 5.030%

Linked to the actual worksheet (Part A)

Formula calculates the average interest rates for in-between years based on the rates input from OMB

Circular A-94.

LDW – Section A.3PV Calculation (cont.)

• Net present value– Value of the lease payments in terms of

today’s money– How much would it cost NOAA if NOAA had

bought the property instead of leased it

LDW – Section A.3PV Calculation (cont.)

• Calculation of present value– Appendix D

• Ability to link to payment stream

– Hints:• Remaining balance should equal zero for the last

payment• Net present value (NPV) should equal the total of

the principal payments

• One of the six lease criteria

LDW – Section A.3PV Calculation (cont.)

• Appendix D - Top Section – Linked to the worksheet.– No input necessary.

Requisition #:

Lease End Date: 1/0/1900 % of Fair Market Value: #DIV/0!Lease Start/ Acceptance Date: 1/0/1900 Fair Market Value: -$

0 Interest Rate: 0.00%Purchase Order/ Contract #: 0 Present Value of Net Rent: -$

Linked to the actual worksheet (Part A)

LDW – Section A.3PV Calculation (cont.)

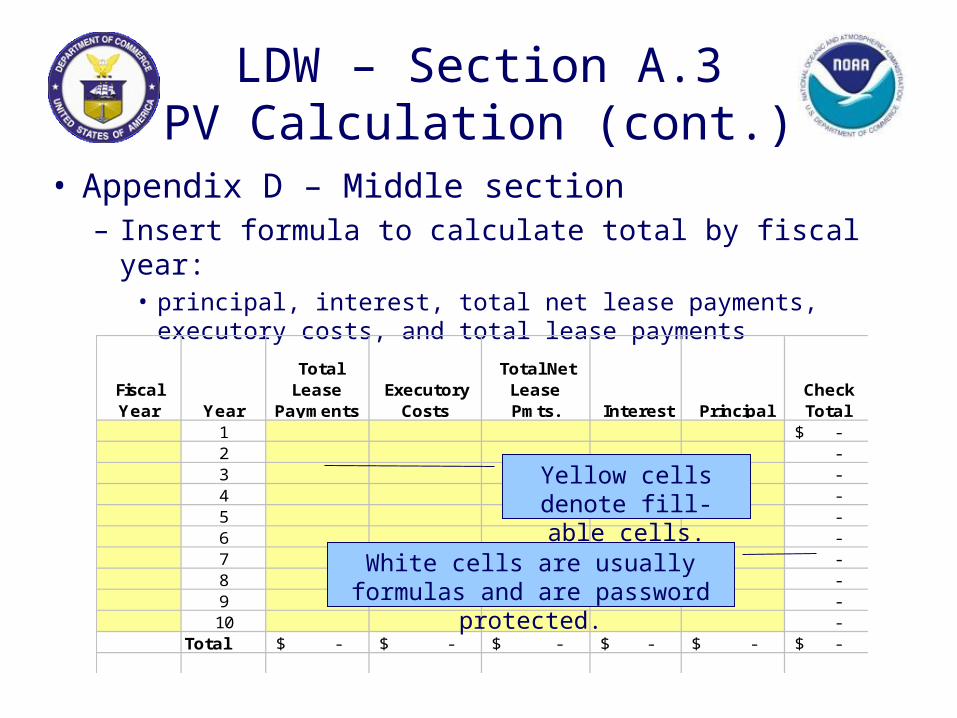

• Appendix D – Middle section – Insert formula to calculate total by fiscal year:

• principal, interest, total net lease payments, executory costs, and total lease payments

Fiscal Year Year

Total Lease

Payments Executory

Costs

Total Net Lease Pmts. Interest Principal

Check Total

1 -$ 2 - 3 - 4 - 5 - 6 - 7 - 8 - 9 - 10 -

Total -$ -$ -$ -$ -$ -$

Yellow cells denote fill-able

cells.White cells are usually formulas

and are password protected.

LDW – Section A.3PV Calculation (cont.)

• Appendix D – Bottom Section – Calculation of net present value

• Based on lease payments included in Appendix A

Interest RateMonthly Interest Rate 0.00%

Month - Year

Month Number

Total Lease

Payments

Executory

Costs

Net Monthly Lease

Monthly Interest Pmts.

Monthly Principal Pmts.

Remaining Balance

-$ 1 -$ -$ -$ -

120 - - - - Total -$ -$ -$ -$ -$

Net Present Value -$

Yellow cells denote fill-able

cells.

White cells are usually formulas and are password protected.

LDW – Section A.4Capital or Operating

• Lease Criteria– Transfer ownership– Bargain purchase option– Special purpose

• Built on government land• Unique specification of NOAA

– Private Sector market– Economic useful life (Section A.2)– Present value (Section A.3)

LDW – Section A.5Lease-Purchase

• Determine whether lease-purchase is with or without substantial risk

• Substantial Risk:– Defined in terms of how governmental in

nature is the project• Less governmental in nature, higher private sector

risk

• Five questions to determine if lease-purchase is with or without substantial risk

LDW – Section A.6-9Budget Authority & Outlays

• Now determined what type of lease, remaining sections of the worksheet determine the budget authority and outlays for each type of lease

LDW – Section A.6Lease-Purchase w/ Risk

• Up-front budget authority = amount equal to asset cost (net present value); annual = amount equal to imputed interest costs

• Outlays = Scored over lease term in an amount equal to the annual lease payments.

LDW – Section A.7Lease-Purchase w/o Risk

• Contact NOAA AGO Headquarters if need to complete this section– Very complicated

LDW – Section A.8Operating Lease

• Cancellation clause– Fiscal fund clause

• Up-front budget authority = amount equal to total payments under the full term of the lease or amount sufficient to cover first year lease payments plus cancellation costs

• Outlays = Scored over lease term in an amount equal to the annual lease payments.

LDW – Section A.9Capital Lease

• Up-front budget authority = amount equal to asset cost (net present value); annual = amount equal to imputed interest costs

• Outlays = Scored over lease term in an amount equal to the annual lease payments.

Budget Authorityand Outlays

Transaction Budget Authority Outlays

Lease-purchase without substantial risk

Up front – amount equal to asset cost;

annual – amount equal to imputed interest costs

Amount equal to asset cost scored over the construction period in proportion to the distribution of the contractor’s costs; amount equal to imputed interest costs recorded on an annual basis over lease term.

Lease-purchase with substantial risk

Up front – amount equal to asset cost;

annual – amount equal to imputed interest costs

Scored over lease term in an amount equal to the annual lease payments.

Budget Authorityand Outlays (cont.)

Transaction Budget Authority Outlays

Capital lease Up front – amount equal to asset cost;

annual – amount equal to imputed interest costs

Scored over lease term in an amount equal to the annual lease payments.

Operating lease Up-front – amount equal to total payments under the full term of the lease or amount sufficient to cover first year lease payments plus cancellation costs

Scored over lease term in an amount equal to the annual lease payments.

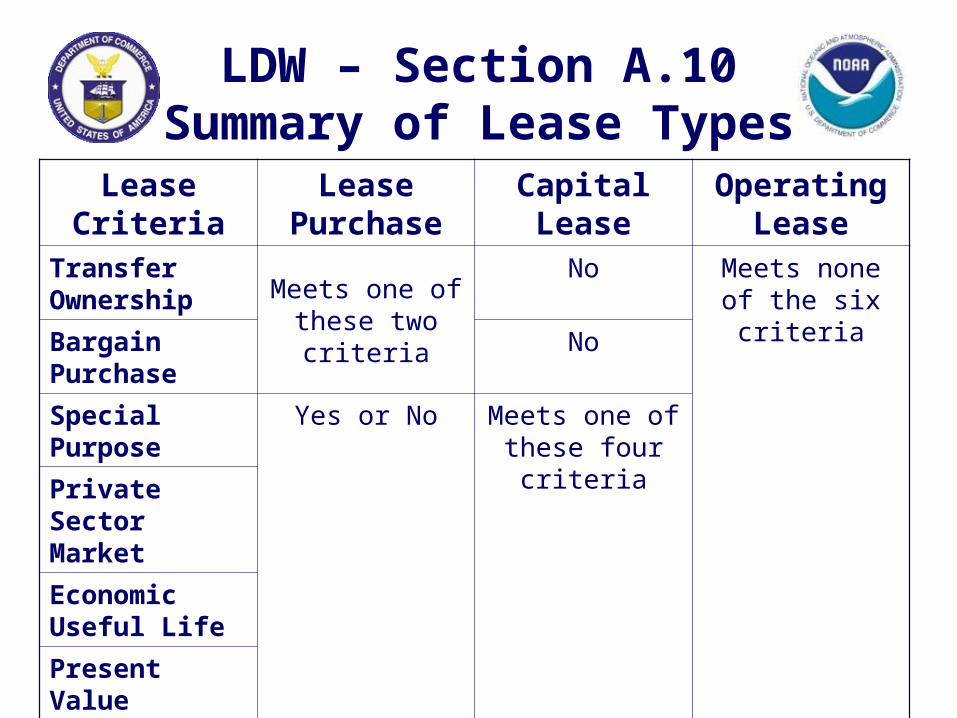

LDW – Section A.10Summary of Lease Types

Lease Criteria

Lease Purchase

Capital Lease

Operating Lease

Transfer Ownership Meets one of

these two criteria

No Meets none of the six criteria

Bargain Purchase

No

Special Purpose

Yes or No Meets one of these four

criteriaPrivate Sector Market

Economic Useful Life

Present Value

LDW – Section A.11Submission to OMB

• Requirement to submit to OMB certain types of leasing and non-routine financing proposals for review of the scoring impact.

• Answer 14 questions

LDW – Section A.12Final Determination

• Conclusion

• Signed and dated by:– Preparer– Headquarters Review– Program Office Review– Line Office Budget– Contracting Officer– Head Contracting Officer

LDW – Part BOverview

• Linked to data input in Part A– Requisition number– Purchase order/contract number– Description of leased property– Explanation for revisions

LDW – Section B.1General Information

• Indeterminable lease term

• Fiscal funding clause

LDW – Section B.2Economic Useful Life

• Dates– Lease beginning date or date of first payment– Date contract/lease signed– Lease end date, including all option periods– Base term– Option years, including increments– Total lease term

LDW – Section B.2Useful Life (cont.)

• Age of asset

• NOAA’s suggested economic useful life

• Renovations/upgrades– Years that renovations/upgrades extend the

useful life.

• Estimated remaining economic useful life

• Beginning of term in last 25% of useful life

• One of the four lease criteria

LDW – Section B.3Present Value Calculation

• Payment Periods– Annually, quarterly, monthly

• Annuity Due/Ordinary Annuity– Payment at the beginning or the end of the

period

• Payment Amounts– Executory costs (taxes, maintenance, and

insurance)– Appendix E (similar to Appendix A)

LDW – Section B.3PV Calculation (cont.)

• Appendix E – Payment StreamRequisition Number: 0

Solicitation Number: 0

Month-Year Payment # Total Lease Payment Operating Costs Net Lease Payments

1 -

2 -

3 -

4 -

5 -

6 -

7 -

8 -

9 -

10 -

11 -

12 -

Yellow cells denote fill-able

cells.

Linked to the actual worksheet (Part B)

White cells usually contain formulas and are password

protected.

LDW – Section B.3PV Calculation (cont.)

• Interest Rate – Lower of Treasury (www.whitehouse.gov/omb) or

Contractor’s interest rate– Date lease begins or acceptance date– Appendix F (similar to Appendix B)

• FMV– Usually quote, GSA schedule or catalog price– Appendix G (similar to Appendix C)

• Blank spreadsheet• Use if need to add several costs together to determine the

FMV

LDW – Section B.3PV Calculation (cont.)

• Appendix F – Interest Rate (prior to entry of rates)Requisition Number: 0

Purchase Order/Contract #: 0

Linear Interpolation of Discount Rate

http://www.whitehouse.gov/omb/circulars/a094/dischist-2006.pdf

Year Rate Year

1

2

3

4 0.000%

5

6 0.000%

7

8 0.000%

9 0.000%

10

11 0.000%

Linked to the actual worksheet (Part B)

Yellow cells denote fill-able

cells.

White cells are usually formulas and are password protected.

LDW – Section B.3PV Calculation (cont.)

• Appendix F – Interest Rate (after entry of rates)Requisition Number: 0

Purchase Order/Contract #: 0

Linear Interpolation of Discount Rate

http://www.whitehouse.gov/omb/circulars/a094/dischist-2006.pdf

Year Rate Year 2006

1

2

3 4.700%

4 4.750%

5 4.800%

6 4.850%

7 4.900%

8 4.933%

9 4.967%

10 5.000%

11 5.030%

Linked to the actual worksheet (Part B)

Formula calculates the average interest rates for in-between years based on the rates input from OMB

Circular A-94.

LDW – Section B.3PV Calculation (cont.)

• Calculation of present value– Appendix H (similar to Appendix D)– Hints:

• Remaining balance should equal zero for the last payment

• Net present value (NPV) should equal the total of the principal payments

• One of the four lease criteria

LDW – Section B.3PV Calculation (cont.)

• Appendix H - Top Section – Linked to the worksheet.– No input necessary.

Requisition #:

Lease End Date: 1/0/1900 % of Fair Market Value: #DIV/0!Lease Start/ Acceptance Date: 1/0/1900 Fair Market Value: -$

0 Interest Rate: 0.00%Purchase Order/ Contract #: 0 Present Value of Net Rent: -$

Linked to the actual worksheet (Part B)

LDW – Section B.3PV Calculation (cont.)

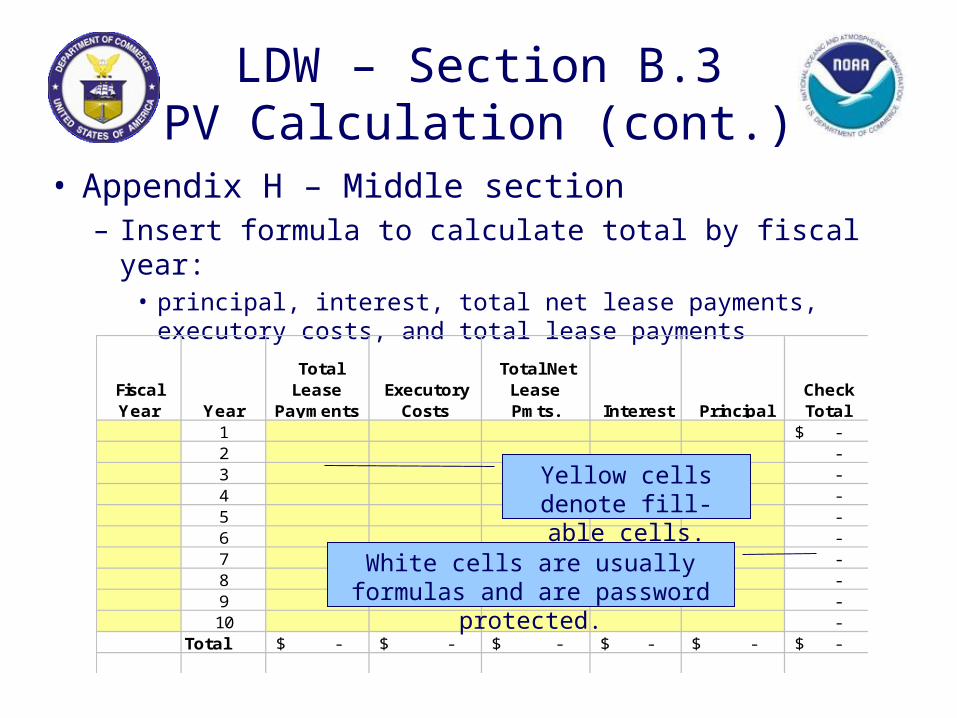

• Appendix H – Middle section – Insert formula to calculate total by fiscal year:

• principal, interest, total net lease payments, executory costs, and total lease payments

Fiscal Year Year

Total Lease

Payments Executory

Costs

Total Net Lease Pmts. Interest Principal

Check Total

1 -$ 2 - 3 - 4 - 5 - 6 - 7 - 8 - 9 - 10 -

Total -$ -$ -$ -$ -$ -$

Yellow cells denote fill-able

cells.White cells are usually formulas

and are password protected.

LDW – Section B.3PV Calculation (cont.)

• Appendix H – Bottom Section – Calculation of net present value

• Based on lease payments included in Appendix E

Interest RateMonthly Interest Rate 0.00%

Month - Year

Month Number

Total Lease

Payments

Executory

Costs

Net Monthly Lease

Monthly Interest Pmts.

Monthly Principal Pmts.

Remaining Balance

-$ 1 -$ -$ -$ -

120 - - - - Total -$ -$ -$ -$ -$

Net Present Value -$

Yellow cells denote fill-able

cells.

White cells are usually formulas and are password protected.

LDW – Section B.4Capital or Operating

• Lease Criteria– Transfer ownership– Bargain purchase option– Economic useful life (Section B.2)– Present value (Section B.3)

LDW – Section B.5 NOAA Capitalization

• If capital:– Useful life is remaining economic useful life

• Transfer ownership• Bargain purchase option

– Useful life is lease term• Economic useful life (Section B.2)• Present value (Section B.3)

• Capital but not-capitalizable– Less than or equal to two years– Cost less than $200,000

• Major class of asset

LDW – Section B.6 Future Payments

• Schedule– Link to table from Appendix H

• Funded versus unfunded (budget)

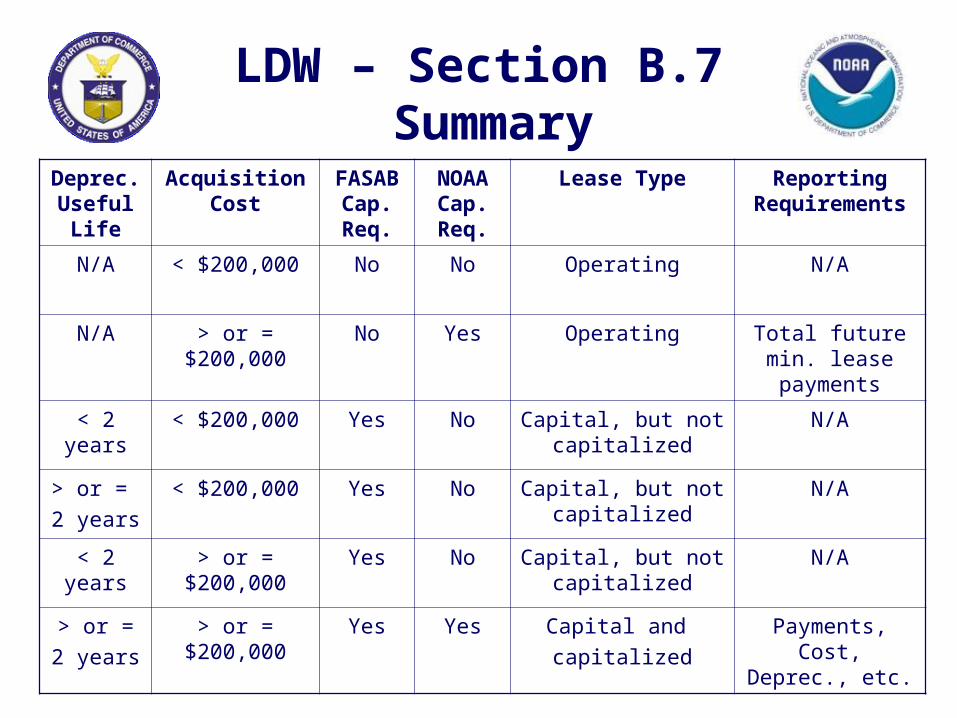

LDW – Section B.7 Summary

Deprec. Useful

Life

Acquisition Cost

FASAB Cap. Req.

NOAA Cap. Req.

Lease Type Reporting Requirements

N/A < $200,000 No No Operating N/A

N/A > or = $200,000

No Yes Operating Total future min. lease payments

< 2 years < $200,000 Yes No Capital, but not capitalized

N/A

> or =

2 years

< $200,000 Yes No Capital, but not capitalized

N/A

< 2 years > or = $200,000

Yes No Capital, but not capitalized

N/A

> or =

2 years

> or = $200,000

Yes Yes Capital and

capitalized

Payments, Cost, Deprec., etc.

LDW – Section B.8Final Determination

• Conclusion

• Signed and dated by:– Preparer– Headquarters Review– Program Office Review– Line Office Budget– Contracting Officer– Head Contracting Officer

• Distribution

Supporting Documentation

• Document! Document! Document!

• Verbal information is okay– Document name, title, company, date of

conversation, and telephone number

• Document on LDW where in lease (page number or paragraph obtained information from, if not straightforward)

Modifications

• Any remaining budgetary resources prior to modification should be used to offset cost of new contract– No remaining budgetary resources if not scored up

front at the time the lease was signed (capital lease or lease purchase)

• Budget authority = difference in the NPV of the new contract and the remaining term of the original contract– Both present values should be calculated using

Treasury rates at time the contract is amended

Actual Worksheet

• Let’s Review!!

• Part A– Appendix A – D

• Part B– Appendix E – H

Miscellaneous

• If you have questions or are uncertain about anything, contact AGO Headquarters.– Patricia Coleman (

[email protected])– Temujene Makua (

[email protected])– Richard Parkerson (if Patricia and Temujene

are unavailable)([email protected])

Where to Get Worksheet & Handbook

• AGO website – http://www.ago.noaa.gov/– Click “Acquisition” on left side.– Click “Policies” on left side.– Scroll down to:

• Personal Property Lease Handbook• Personal Property Lease Determination Worksheet

Where to Get More Information

• OMB website, specifically OMB A-11• FASAB website

– FASAB SFFAS No. 6– Research report on Capital and Operating

Leases (October 2003)

• FASB website, specifically FAS 13• AGO – contacts on previous page• Ernst & Young – Heather Potter

Questions/Comments