Accounting for Merchandising Business

ACG 2021: Chapter 5

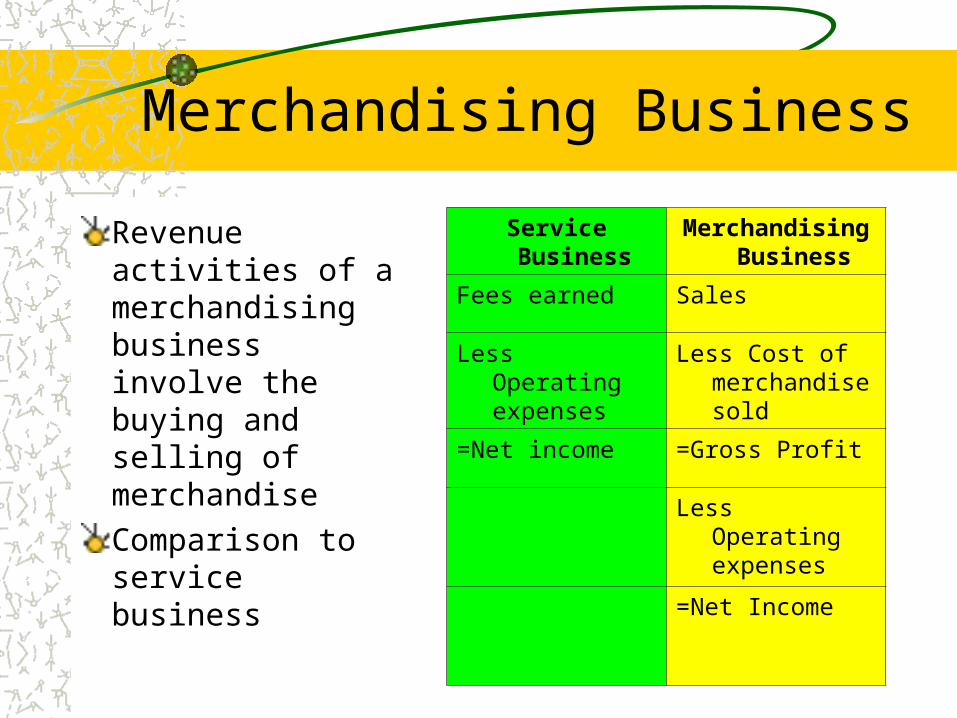

Merchandising Business

Revenue activities of a merchandising business involve the buying and selling of merchandiseComparison to service business

Service Business Merchandising Business

Fees earned Sales

Less Operating expenses

Less Cost of merchandise sold

=Net income =Gross Profit

Less Operating expenses

=Net Income

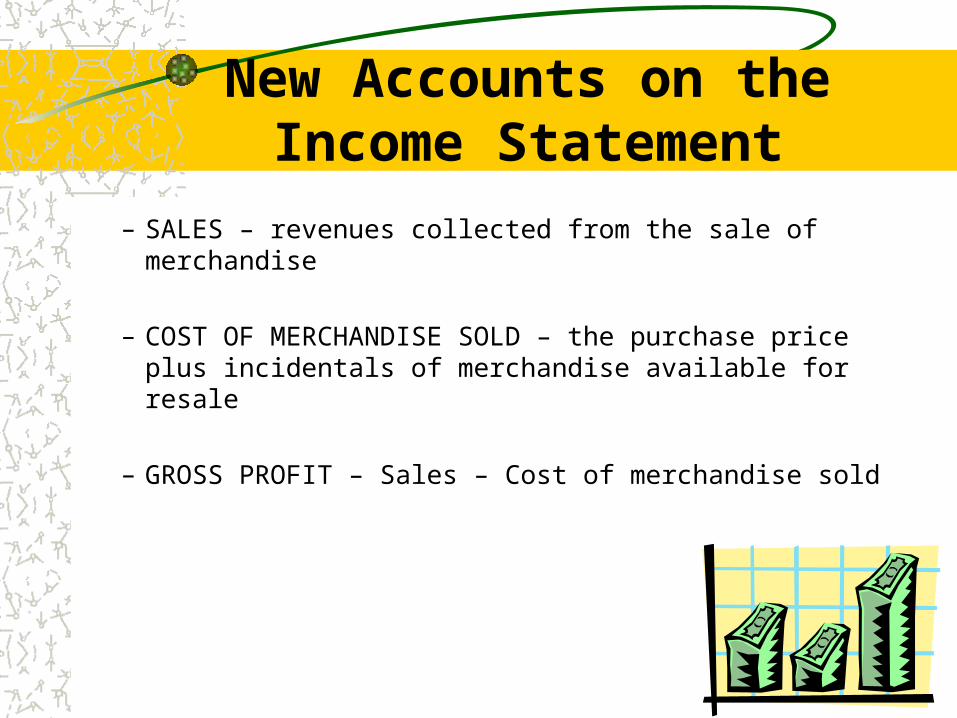

New Accounts on the Income Statement

– SALES – revenues collected from the sale of merchandise

– COST OF MERCHANDISE SOLD – the purchase price plus incidentals of merchandise available for resale

– GROSS PROFIT – Sales – Cost of merchandise sold

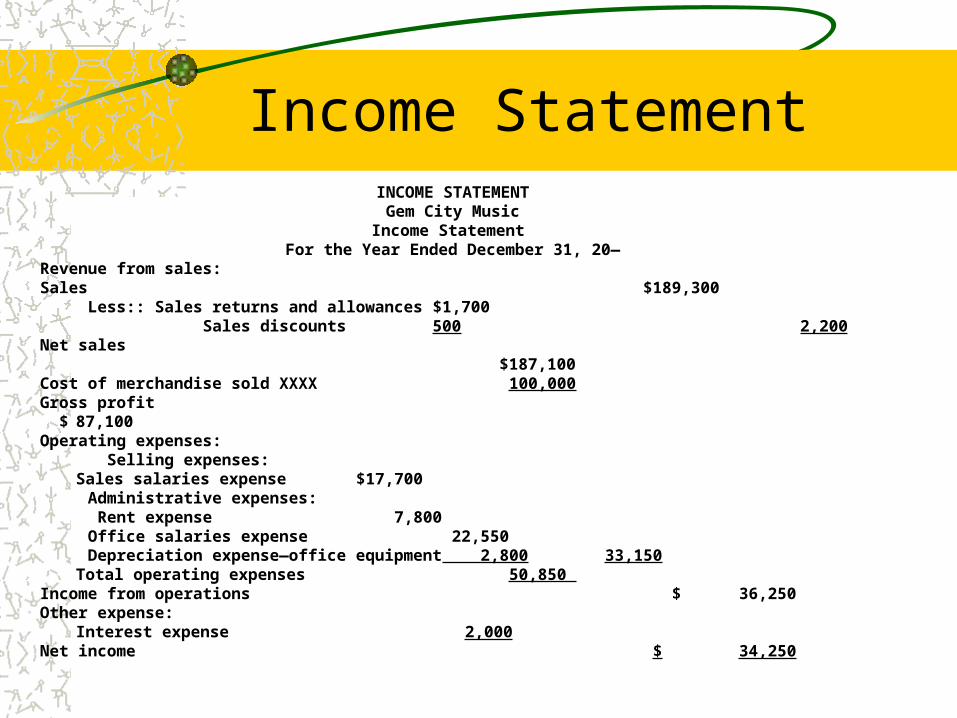

Income StatementINCOME STATEMENT

Gem City MusicIncome Statement

For the Year Ended December 31, 20—Revenue from sales:Sales $189,300 Less:: Sales returns and allowances $1,700 Sales discounts 500 2,200Net sales $187,100Cost of merchandise sold XXXX 100,000Gross profit $ 87,100Operating expenses: Selling expenses:

Sales salaries expense $17,700 Administrative expenses: Rent expense 7,800 Office salaries expense 22,550 Depreciation expense—office equipment 2,800 33,150

Total operating expenses 50,850 Income from operations $36,250Other expense:

Interest expense 2,000Net income $ 34,250

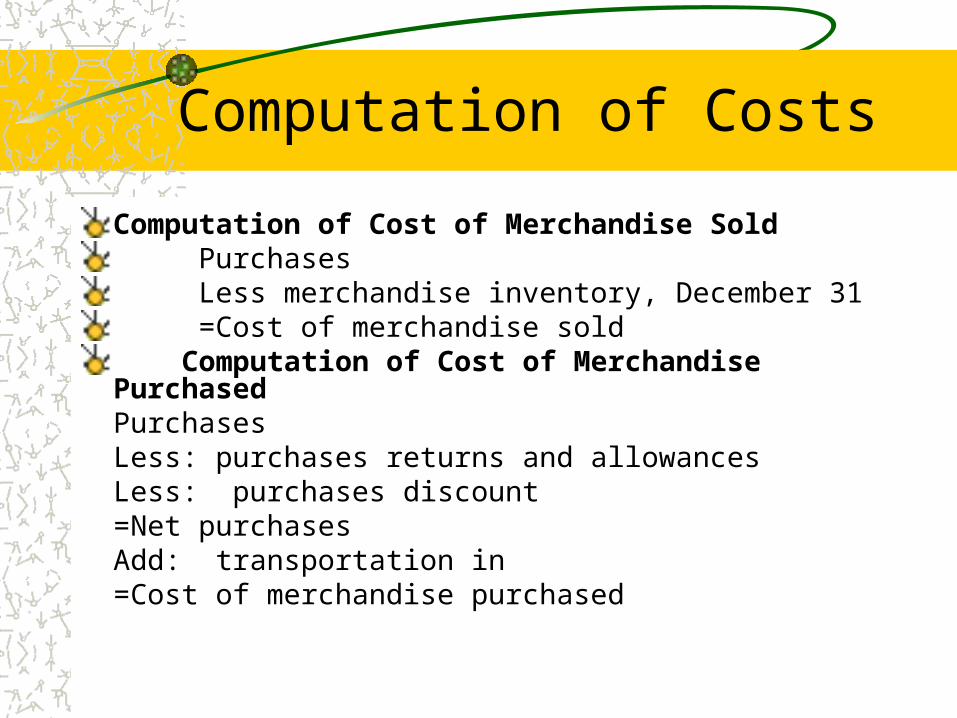

Computation of Costs

Computation of Cost of Merchandise SoldPurchasesLess merchandise inventory, December 31=Cost of merchandise sold

Computation of Cost of Merchandise PurchasedPurchasesLess: purchases returns and allowancesLess: purchases discount=Net purchasesAdd: transportation in=Cost of merchandise purchased

Balance Sheet Accounts

Merchandise inventory – merchandise on hand at the end of an accounting period.

Merchandising Terms

Sales – total amount charged to customers for merchandise soldSales returns and allowances – are granted by the seller to customers for damaged or defective merchandiseSales discount – are granted by the seller to customers for earlyNet sales = Sales –returns - discount

Merchandising Terms

Cost of goods sold– Cost of merchandise sold to customers

Purchases discounts– Offered by the seller to buyer– For early payment

Purchases allowances and returns– Buyer may receive a reduction in the intial price at

which the merchandise is purchased.

Merchandising Terms

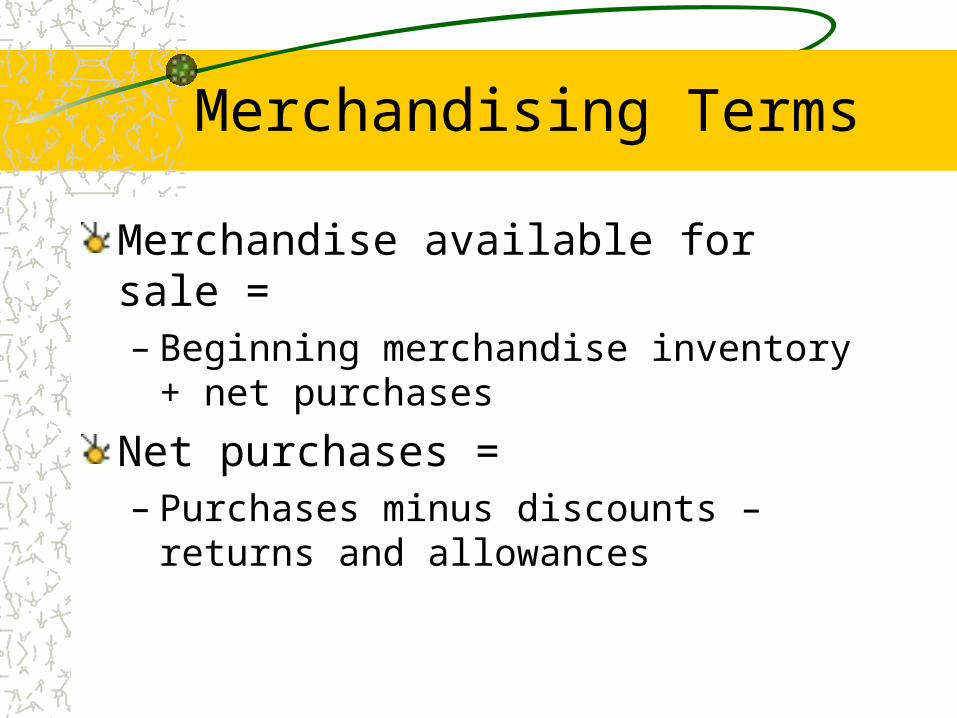

Merchandise available for sale =– Beginning merchandise inventory + net purchases

Net purchases =– Purchases minus discounts – returns and

allowances

Accounting for Sales

Under the perpetual inventory system, all sales require the reporting of the removal of inventory from the books at the same time.

Accounting for Sales

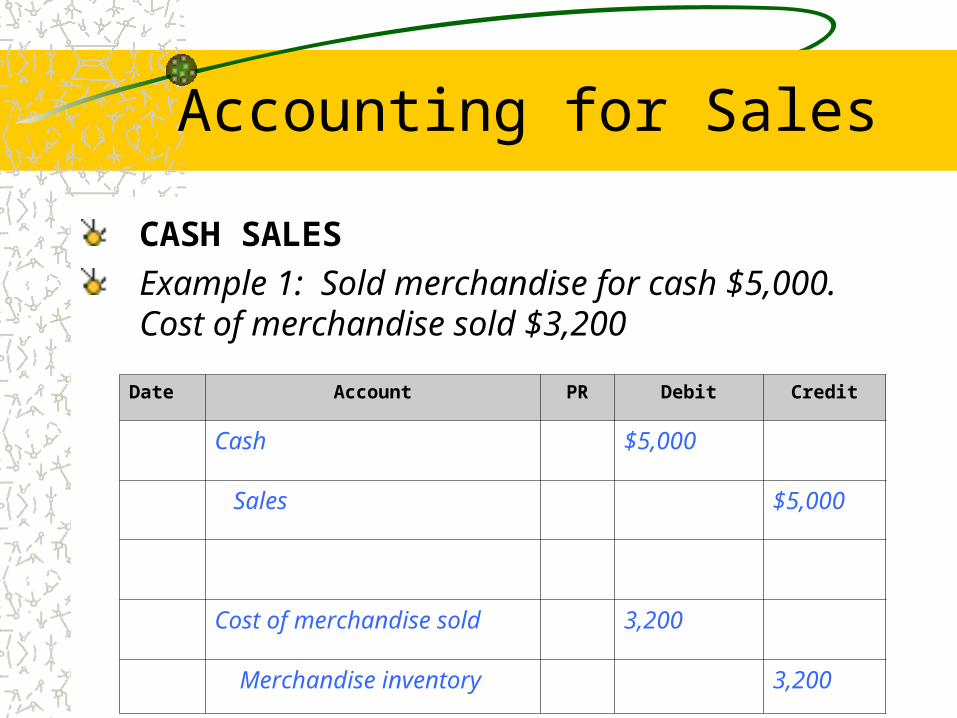

CASH SALES

Example 1: Sold merchandise for cash $5,000. Cost of merchandise sold $3,200

Date Account PR Debit Credit

Cash $5,000

Sales $5,000

Cost of merchandise sold 3,200

Merchandise inventory 3,200

Credit sales

Bank cards– Master card– Visa– Monies directly deposited

in business account– Requires a debit to CASH

Service charge must be later recorded as expense

Bank cards

Example 9: Sold merchandise on VISA $10,000. Cost of merchandise sold is $4,000. Credit card expense is 3% of sales.

Date Account PR Debit Credit

Cash $10,000

Sales $10,000

Cost of merchandise sold 4,000

Merchandise inventory 4,000

Credit card expense 300

Cash 300

Bank cards

Example 3: Sold merchandise on VISA $6,000. Cost of merchandise sold is $3,000. Credit card expense is 3% of sales.

Example 10

Cash 6,000 Sales 6,000

Cost of merchandise 3,000 Merchandise inventory 3,000Credit card expense 180 Cash 180

Credit sales

Two types:– American express– On account

Results in debit to ACCOUNTS RECEIVABLE

Sales of Account

Example 4: Sold merchandise on account $6,000. Cost of merchandise sold is $3,000. Date Account PR Debit Credit

Accounts receivable $6,000

Sales 6,000

Cost of merchandise 3,000

Merchandise inventory 3,000

Recap

Under the perpetual inventory system, all sales transactions consist of at least two entries.

The first entry records the sale at the selling price with a debit to how it will be paid and credit to sales.

The second entry records the merchandise leaving the business with a debit to cost of merchandise sold and credit to merchandise inventory for the cost of the merchandise.

Sales discounts

A reduction in the price of the good for early payment.This account is a contra – SALESUpon payment of the account receivable, if the payment is within the discount period, we record the discount.Credit terms – terms of when payments for merchandise are to be made.– Net 30 days – full amount due in 30 days– 2/10 – 2% discount if paid within 10 days

Example on Sales Discount

Example 5: Sold merchandise on account $5,000, terms 2/10, n/30. Cost of merchandise sold is $4,000.

Sales $5,000Discount 2%Discount $ $100

Sales $5,000Less discount 100Net amount 4,900

Sales discount

Date Account PR Debit Credit

Cash 4900

Sales discount 100

Accounts receivable 5000

Sales Returns and Allowances

Merchandise sold may be returned to the sellerMerchandise sold may be reduced in price due to defectsThis account is CONTRA – salesIncreases with a debit

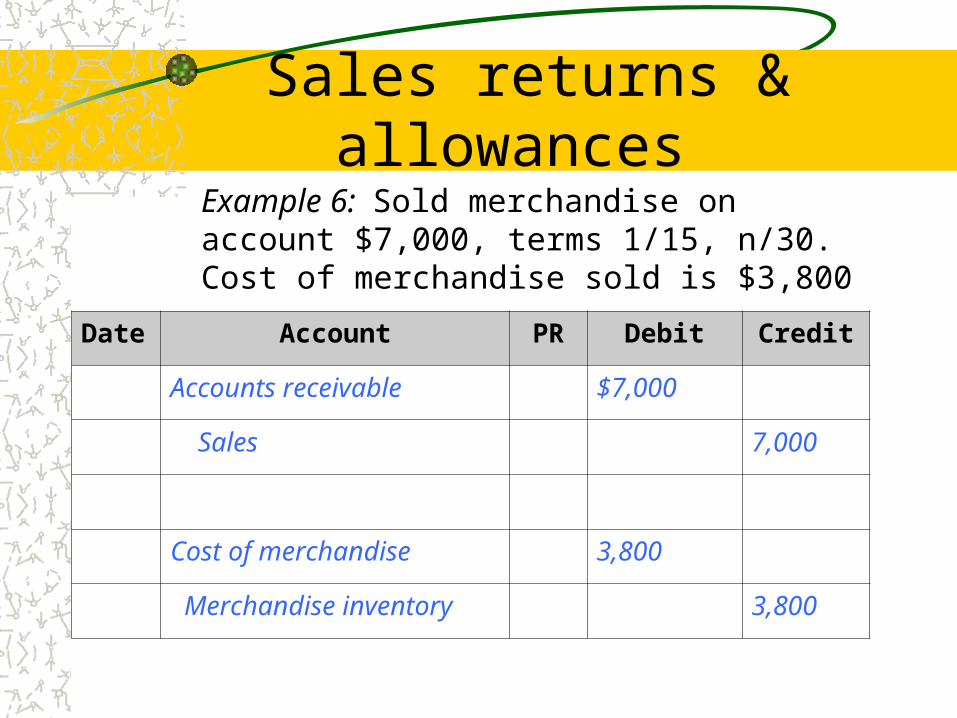

Sales returns & allowances Example 6: Sold merchandise on account $7,000, terms 1/15, n/30. Cost of merchandise sold is $3,800

Date Account PR Debit Credit

Accounts receivable $7,000

Sales 7,000

Cost of merchandise 3,800

Merchandise inventory 3,800

Sales returns & allowances

Return merchandise with sales price of $2,000 and cost of $1,000.

Date Account PR Debit Credit

Sales returns 2,000

Accounts receivable 2,000

Merchandise inventory 1,000

Cost of merchandise sold 1,000

Recap of Sales Example

Example 7: ABC Merchandising had the following transactions:Sold merchandise and received payment by VISA at $6,000, cost of merchandise sold is $4,000.Sold merchandise on account for $7,500 with credit terms 1/10, n/30. Cost of the merchandise is $4,500.Sold merchandise on account for $4,000, cost of merchandise is $2,500.Received a return of the merchandise in (c ) of sales price of $2,000 and cost of $1,750.Received payment within the discount period for merchandise in (b).Received payment for merchandise in (c ).

Accounting for Purchases

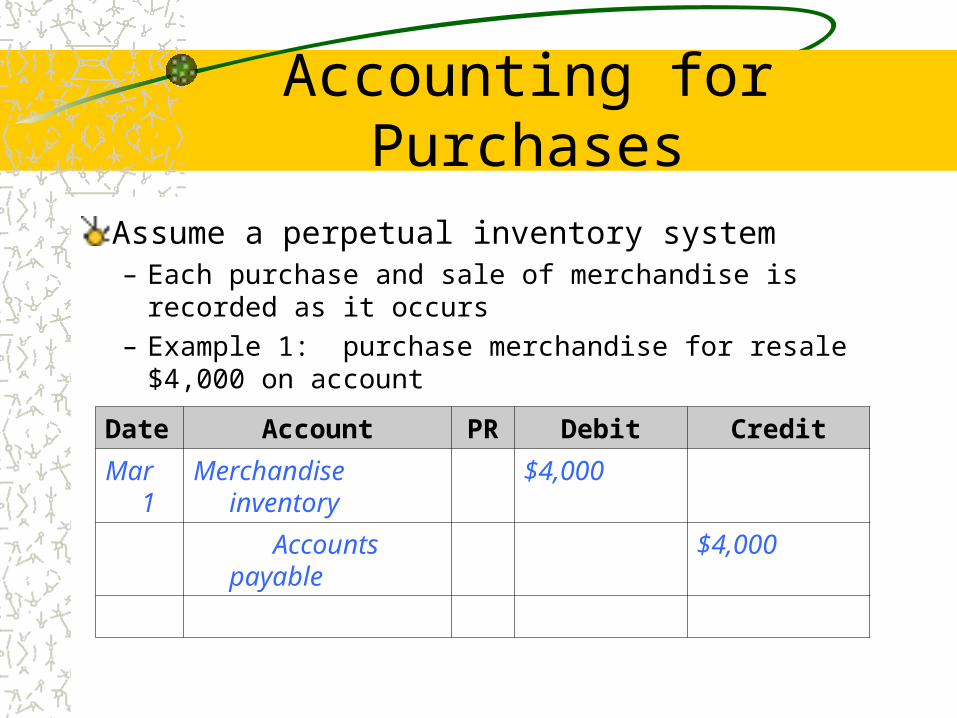

Assume a perpetual inventory system– Each purchase and sale of merchandise is recorded as it occurs– Example 1: purchase merchandise for resale $4,000 on

account

Date Account PR Debit Credit

Mar 1 Merchandise inventory $4,000

Accounts payable $4,000

Purchases Discount

Credit terms– Purchases discounts are

discounts taken by the buyer for early payment of an invoice.

– These discounts reduce the cost of the merchandise purchased.

– Should be taken when offered if not it is a LOSS to the business.

Purchase discount

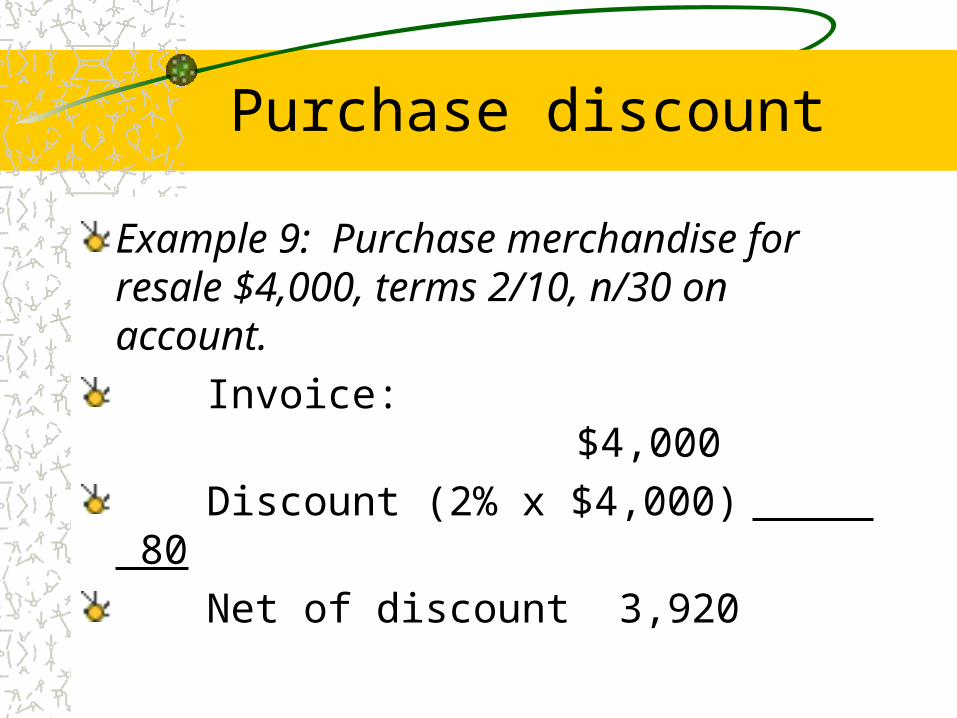

Example 9: Purchase merchandise for resale $4,000, terms 2/10, n/30 on account.

Invoice: $4,000Discount (2% x $4,000) 80Net of discount 3,920

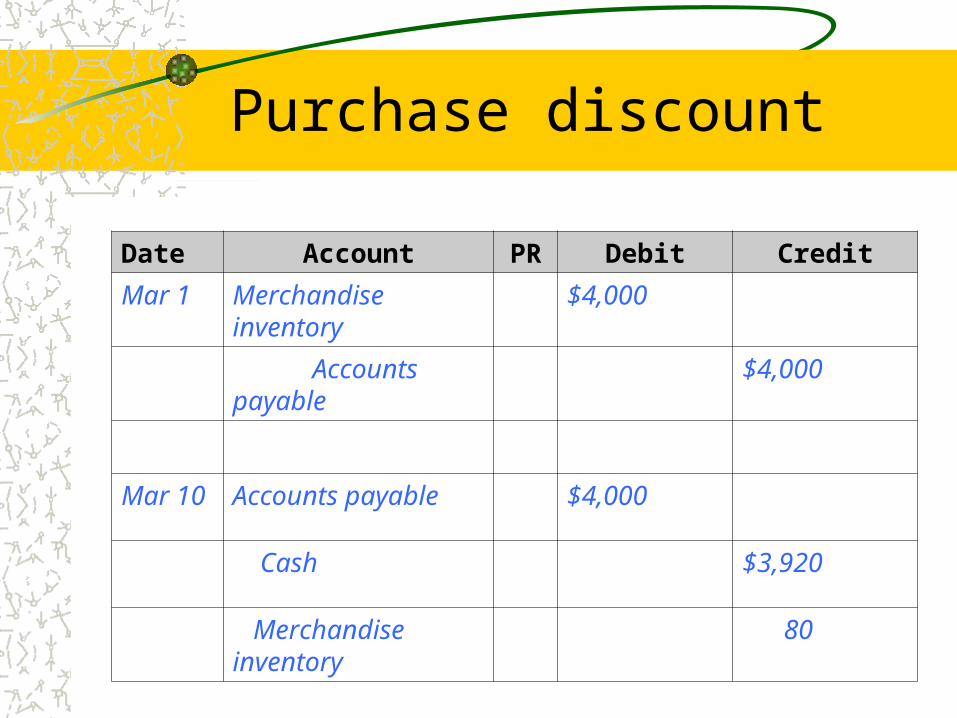

Purchase discount

Date Account PR Debit Credit

Mar 1 Merchandise inventory $4,000

Accounts payable $4,000

Mar 10 Accounts payable $4,000

Cash $3,920

Merchandise inventory

80

Purchase Discount

Reduction of the cost of the merchandise is reflected in the merchandise inventory account.

Example 10: Purchase merchandise for resale $6,000, terms 1/15, n/30 on account.

Purchases Returns and Allowances

Purchase returns – merchandise is returned to the sellerPurchase allowances – price adjustmentDebit memorandum – notification of the return or allowance by seller

Purchases Returns and Allowances

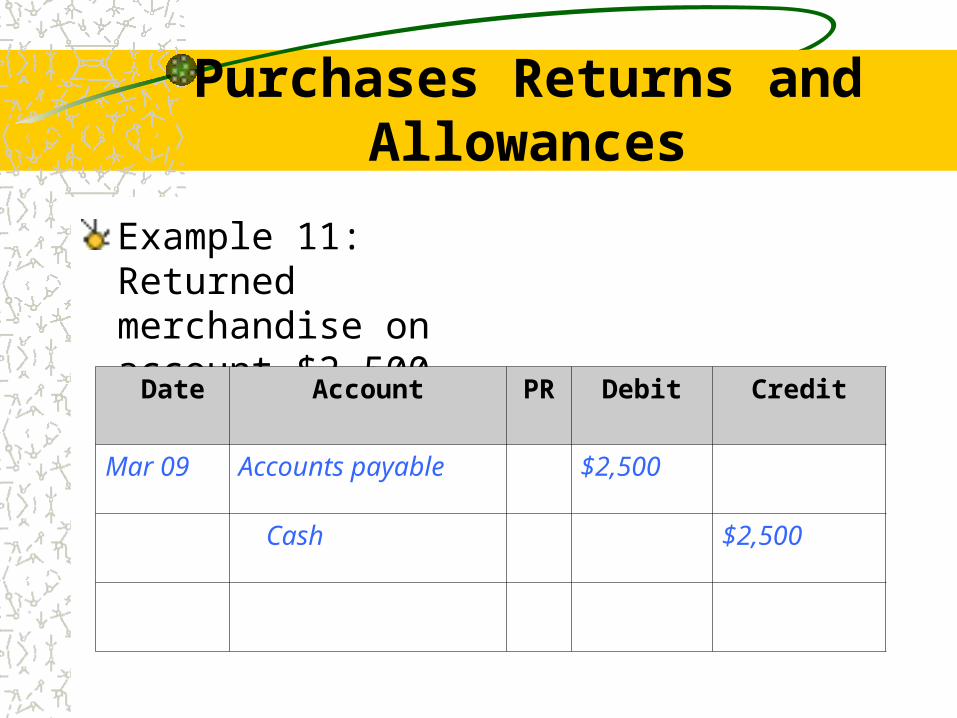

Example 11: Returned merchandise on account $2,500.

Date Account PR Debit Credit

Mar 09 Accounts payable $2,500

Cash $2,500

Example

Example 12: Purchased merchandise of $8,000 on terms 2/10,n/30. Ennis pays the original invoice less a return of $2,500 within the discount period. Record the above entries

Recap of Purchases Example

Example 7: ABC Merchandising had the following transactions:Purchased merchandise and received payment by VISA at $6,000.Purchased merchandise on account for $7,500 with credit terms 1/10, n/30. Purchased merchandise on account for $4,000.Return of the merchandise in (c ) of sales price of $2,000.Paid within the discount period for merchandise in (b).Paid for merchandise in (c ).

Transportation Costs

The terms of a sale should indicate when the ownership of the merchandise passes to the buyer.

• This point determines which party, the buyer or the seller must pay the transportation costs.

Transportation Costs

– FOB – shipping point• The ownership of the merchandise passes to the buyer

when the seller delivers the merchandise to the transportation company.

• Buyer pays the transportation costs

Example 13: Purchased merchandise for $4,000 with shipping costs of $50 FOB shipping point.

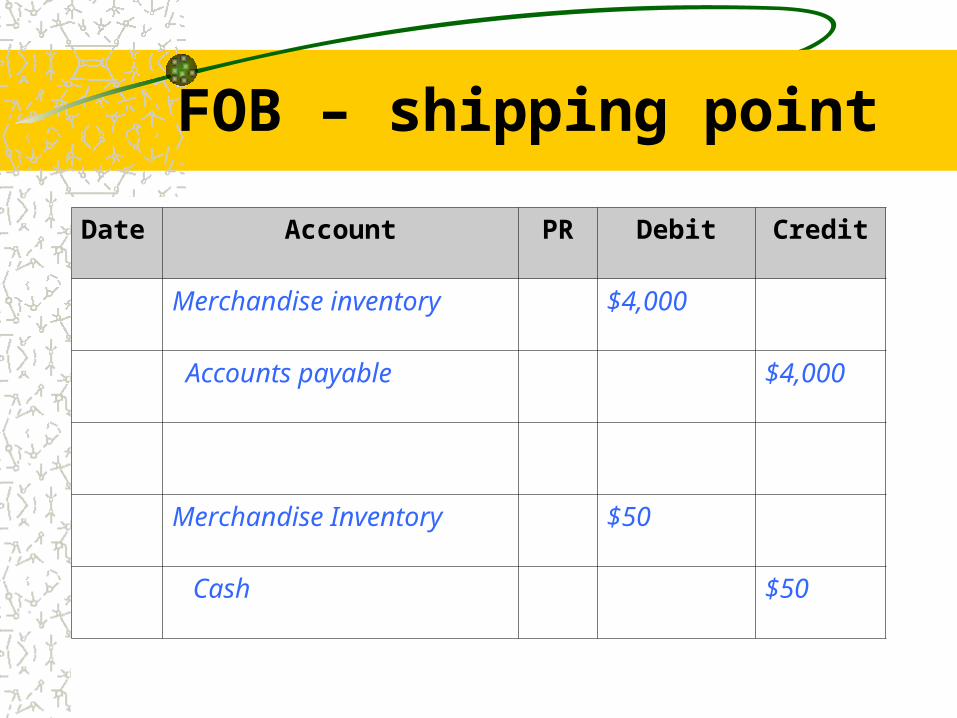

FOB – shipping point

Date Account PR Debit Credit

Merchandise inventory $4,000

Accounts payable $4,000

Merchandise Inventory $50

Cash $50

Transportation Costs

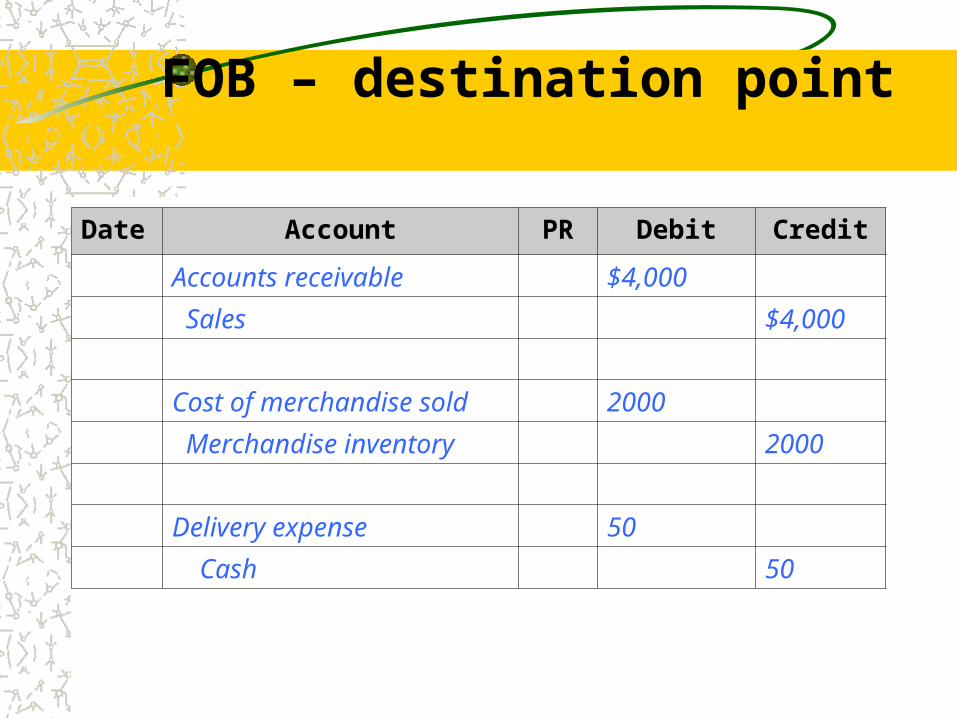

– FOB – destination point• The ownership of the merchandise passes to the buyer

when the seller delivers the merchandise to the buyer.• Seller pays the transportation costs

Example 14: Sold merchandise for $4,000 with shipping costs of $50 FOB destination. Cost of merchandise sold is $2,000.

FOB – destination point

Date Account PR Debit Credit

Accounts receivable $4,000

Sales $4,000

Cost of merchandise sold 2000

Merchandise inventory 2000

Delivery expense 50

Cash 50

Transportation costs

FREIGHT TERMSFOB FOBShipping Point

DestinationOwnership (title)passes to buyerwhen merchandise Delivered to Receivedis freight carrier by buyer

Transportationcosts are paidby Buyer Seller

Risk of loss duringtransportationbelongs to Buyer Seller

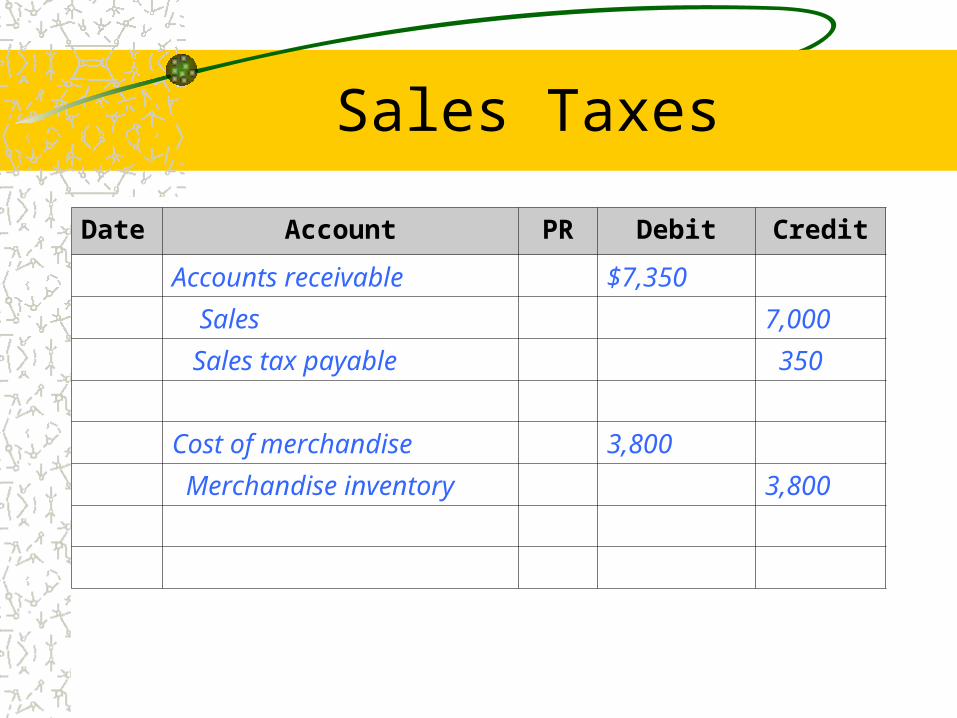

Sales Taxes

Liability to the businessCreate a SALES TAX PAYABLE account

Example 15: Sold merchandise on account $7,000, plus 5% sales tax. Cost of merchandise sold is $3,800.

Sales Taxes

Date Account PR Debit Credit

Accounts receivable $7,350

Sales 7,000

Sales tax payable 350

Cost of merchandise 3,800

Merchandise inventory 3,800

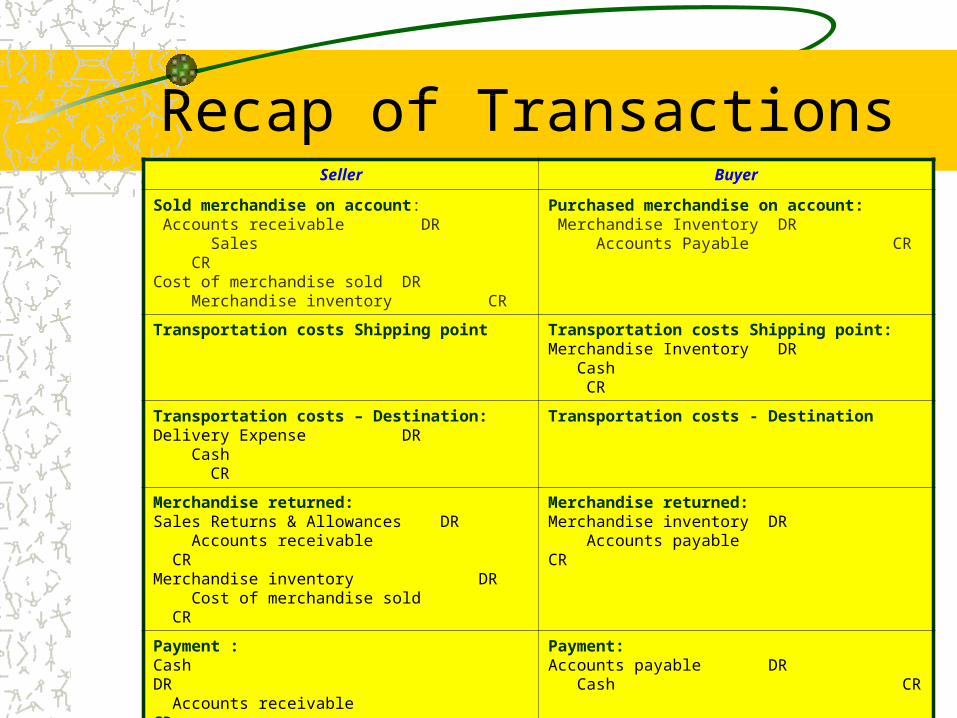

Recap of TransactionsSeller Buyer

Sold merchandise on account: Accounts receivable DR Sales CRCost of merchandise sold DR Merchandise inventory CR

Purchased merchandise on account: Merchandise Inventory DR Accounts Payable CR

Transportation costs Shipping point Transportation costs Shipping point:Merchandise Inventory DR Cash CR

Transportation costs – Destination:Delivery Expense DR Cash CR

Transportation costs - Destination

Merchandise returned:Sales Returns & Allowances DR Accounts receivable CRMerchandise inventory DR Cost of merchandise sold CR

Merchandise returned:Merchandise inventory DR Accounts payable CR

Payment :Cash DR Accounts receivable CR

Payment:Accounts payable DR Cash CR

Payment with discount:Cash DRSales discount DR Accounts receivable CR

Payment with discount:Merchandise inventory DR Cash CR

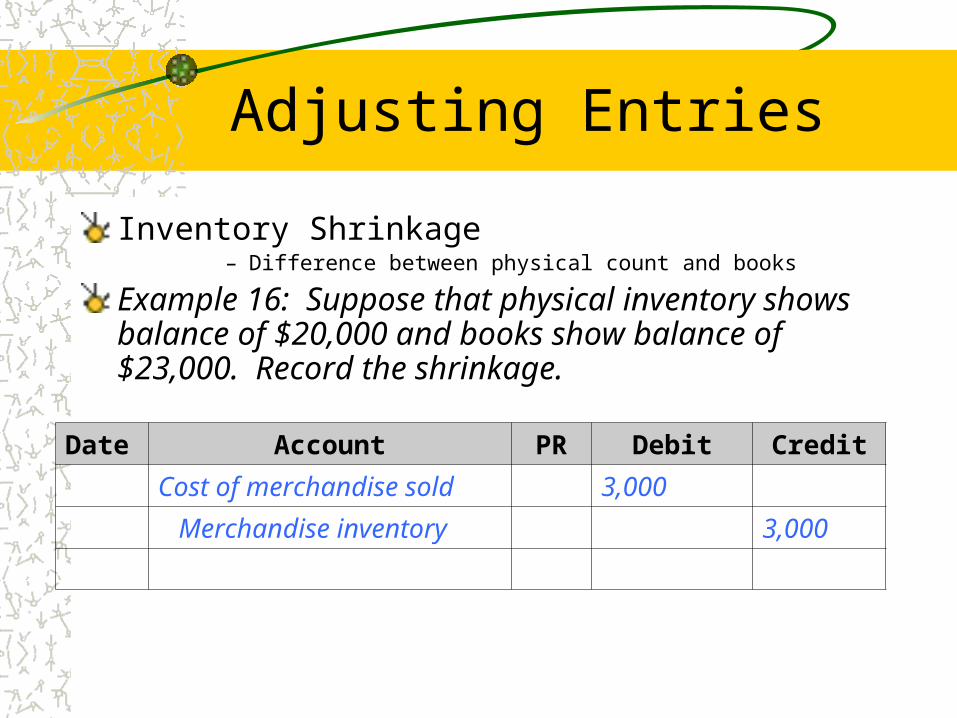

Adjusting Entries

Inventory Shrinkage– Difference between physical count and books

Example 16: Suppose that physical inventory shows balance of $20,000 and books show balance of $23,000. Record the shrinkage.

Date Account PR Debit Credit

Cost of merchandise sold 3,000

Merchandise inventory 3,000

Closing Entries

– Accounts that must be closed• Sales• Rent revenue• Sales returns and allowances• Sales discounts• Cost of merchandise sold• All expenses and revenues• Dividends