Accounting Entries under GST for different situations

On 8th August 2017

ICAI Webcast < http://estv.in/icai/08082017/>

1

Accounting Entries under GST for different

situations

CA.VENUGOPAL GELLA

On 8th August 2017

Scope

• Introduction.

• Configuration.

• List of ledgers to be created.

• Outward Supply.

• Inward Supply.

• Entry to be passed after filing GST Returns i.e. Closing Entries.

• Transition entries to be passed

Introduction

• Technology or software is the backbone of GST

• Success or failure of implementation of GST isheavily dependent on technology

• GST will create a paradigm shift in how SmallBusiness “run their day to day business”

• Changes in the Accounting entries that one hasfollow to comply with GST Law.

Configurations of

Accounting Systems

Master Setup

• Inventory Item configuration.

• Item Name

• HSN Code/SAC code

• Tax Rate

• Unit of measurement

Master Setup...

• Sales Account

• Percentage wise

• Customer / Vendors Accounts (Multiple GSTIN)

• Name

• Address

• State

• GSTN

• PAN

• Purchases Accounts (Rate wise)

• Tax ledger (credit, liability, cash for CGST/SGST/IGST)

Master Setup…

• Transaction Time

• Select

• Revenue ledger

• Party ledger

• Item

• Enter Amount

• Tax Type ,

• Can We Make Automation?

• Place of Supply (important if it is different fromplace of recipient)

Master Setup...

• Expenses Accounting, Capturing Input tax

• Advance ledgers – Receipt voucher

• Refund vouchers

• Unregistered purchases - Invoice

• Payment vouchers

• Outstanding more than 180 days

• Credit Note & Debit Note

“Invoicing Under”

• Composition supplier?

• Warranty / Free Samples?

• Tax Invoice v/s. Bill of Supply?

• Composite supply/Mixed Supply?

• Buy one get one offers?

• Works contractor

• on immovable?

• on movable/AMC?

• Transportation charges GST Rate?

“Invoicing Under” :“BILL To , SHIP TO” Case

• Supply state – Maharashtra

• Bill to state – Maharashtra

• Ship to state—Tamil Nadu

• In the above example, Supply state & “Bill To” state are only relevant.

• If both states are same CGST & SGST shall be levied otherwise IGST shall be levied.

List of ledgers to be created - BSCurrent Assets / Duties & Liabilities Duties and taxes (Current liabilities)

Input CGST A/c 9% Output CGST A/c*

Input SGST A/c 9% Output SGST A/c*

Input IGST A/c 18% Output IGST A/c*

Provisional ITC CGST Ledger A/c GST on Advance

Provisional ITC SGST Ledger A/c

Provisional ITC IGST Ledger A/c Current Liability

Electronic Credit CGST Ledger A/c Electronic Liability Ledger CGST A/c

Electronic Credit SGST Ledger A/c Electronic Liability Ledger SGST A/c

Electronic Credit IGST Ledger A/c Electronic Liability Ledger IGST A/c

Electronic Cash CGST Ledger A/c

Electronic Cash SGST Ledger A/c Sundry Creditors (Group in tally)

Electronic Cash IGST Ledger A/c Registered

Cash/ Bank A/c Unregistered

Composition(* For each % you can create separately)

List of ledgers to be created - PnL

Outward Supply - Sales A/c Inward Supply - Purchases A/c

Local B2B sales A/c Purchases A/c

Local B2C sales A/c Exempt purchases A/c

Interstate B2B sales A/c Expense A/c

Interstate B2C sales A/c Inward Supply - Purchases A/c

Export Sales Purchases A/c

Exempt Sales {B2B / B2C + Local / Inter State}

RCM Sales {B2B / B2C + Local / Inter State}

eCom Sales {B2B / B2C + Local / Inter State}

Outward Supply

Outward Supply- Taxable SuppliesNature Dr/Cr Ledger a/c Amount Amount

Reporting

Table

B2B Dr

Cr

Cr

Cr

Debtors A/c

To Local B2B sales A/c

To 9% Output CGST A/c

To 9% Output SGST A/c

1,41,600

1,20,000

10,800

10,800

GSTR1>>

Table 4A

B2C S

Local

Dr

Cr

Cr

Cr

Debtors A/c

To Local B2C sales A/c

To 9% Output CGST A/c

To 9% Output SGST A/c

1,41,600

1,20,000

10,800

10,800

GSTR1>>

Table7A(1)

B2C S

Interstate

Dr

Cr

Cr

Debtors A/c

To Interstate B2C sales A/c

To 18% Output IGST A/c

1,41,600

1,20,000

21,600

GSTR1>>

Table 7B(1)

B2C L (>2.5

Lacs)

Dr

Cr

Cr

Debtors A/c

To Interstate B2C sales A/c

To 18% Output IGST A/c

2,95,000

2,50,000

45,000

GSTR 1>>

Table 5A

Exempt Supplies

Nature Dr/Cr Ledger a/c Amount Amount Reporting Table

Outward Supply – Exempt

Inter-state Sale

– B2B

Dr

Cr

Debtors A/c

To Exempt B2B sales-Interstate A/c

1,20,000

1,20,000

GSTR-1 >>

Table 8A

Local Sale – B2B Dr

Cr

Debtors A/c

To Exempt B2B sales-Local A/c

1,20,000

1,20,000

GSTR-1 >>

Table 8B

Inter-state Sale

– B2C

Dr

Cr

Debtors A/c

To Exempt B2C sales-Interstate A/c

{No Transaction Limit}

3,00,000

3,00,000

GSTR-1 >>

Table 8C

Local Sale – B2C Dr

Cr

Debtors A/c

To Exempt B2C sales-Local A/c

1,20,000

1,20,000

GSTR-1 >>

Table 8D

RCM Supplies Sec 9(3)

Nature Dr/Cr Ledger a/c Amount Amount Reporting Table

Outward Supply - Sales attracting RCM – Sec 9(3)

Local Sale – B2B Dr

Cr

Debtors A/c

To Local RCM B2B sales A/c

1,20,000

1,20,000

GSTR-1 >>

Table 4B

Local Sale – B2C Dr

Cr

Cr

Cr

Debtors A/c

To Local B2C sales A/c

To 9% Output CGST A/c

To 9% Output SGST A/c

1,41,600

1,20,000

10,800

10,800

GSTR1 >>

Table 7A(1)

Inter-state Sale –

B2B

Dr

Cr

Debtors A/c

To Inter State RCM B2B sales

A/c

1,20,000

1,20,000

GSTR-1 >>

Table 4B

Inter-state Sale –

B2C

Dr

Cr

Cr

Debtors A/c

To Interstate B2C sales A/c

To 18% Output IGSTA/c

1,41,600

1,20,000

21,600

GSTR1 >>

Table 7B(1)

Outward Supply-Supplies through E-commerce Operator

Nature Dr/Cr Ledger a/c Amount AmountReporting

Table

Local Sale –

B2B

Dr

Cr

Cr

Cr

Debtors A/c

To Local e-COM B2B sales A/c

To 9% Output CGST A/c

To 9% Output SGST A/c

1,41,600

1,20,000

10,800

10,800

GSTR-1 >>

Table 4C

Local Sale –

B2C S

Dr

Cr

Cr

Cr

Debtors A/c

To Local e-COM B2C sales A/c

To 9% Output CGST A/c

To 9% Output SGST A/c

1,41,600

1,20,000

10,800

10,800

GSTR-1 >>

Table 7A (1)

& 7A (2)

Inter State

Sale – B2C S

Dr

Cr

Cr

Debtors A/c

To Inter State e-COM B2C sales A/c

To 18% IGST A/c

1,18,000

1,00,000

18,000

GSTR-1 >>

Table 7B (1)

& 7B (2)

Inter State

Sale – B2C L

Dr

Cr

Cr

Debtors A/c

To Inter State e-COM B2C sales A/c

To 18% Output IGST A/c

2,95,000

2,50,000

45,000

GSTR-1 >>

Table 5B

Outward Supply- Export & SEZ

Nature Dr/Cr Ledger a/c Amount Amount Reporting Table

Outward Supply - For Exports

With payment

of duty

Dr

Dr

Cr

Cr

Debtors A/c

IGST Refund Due A/c.

To Sales (export) A/c

To 18% Output IGST A/c

2,00,000

36,000

2,00,000

36,000

GSTR 1 >>

Table 6A

With payment of

Duty

Without

payment of

duty

Dr

Cr

Debtors A/c

To Sales (export) A/c

1,25,000

1,25,000

GSTR 1 >>

Table 6A

Under LUT or Bond

Outward Supply - For SEZ

With payment

of duty

Dr

Dr

Cr

Cr

Debtors A/c

IGST Refund Due A/c.

To Sales (export) A/c

To 18% Output IGST A/c

2,00,000

36,000

2,00,000

36,000

GSTR 1 >>

Table 6B

With payment of

Duty

Without

payment of

duty

Dr

Cr

Debtors A/c

To Sales (export) A/c

1,25,000

1,25,000

GSTR 1 >>

Table 6B

Under LUT or Bond

Advances Received from CustomerNature Dr/Cr Journal Entry Amount Amount Reporting Table

Advance

received

Dr

Cr

Bank

To Advance Received

11800

11800

GSTR-1>>Table-11A (1)

Invoice Same

MonthAdvances Received and Invoice Raised in the same month, the Tax would be levied on

Supply no separate reporting for Advances is required.

Invoice not

raised in

same Month

Dr

Cr

Cr

GST on Advances

To 9% Output CGST

To 9% Output SGST

1800

900

900

GSTR-1>>Table-11A (1)

Invoice raised

Subsequently

Dr

Cr

18% IGST Output A

To GST on Advances

1800

1800

GSTR-1>>Table-11B (2)

Subsequent adjustment for advances

Nature Dr/Cr Journal Entry Amount Amount Reporting Table

B2B Dr

Cr

Cr

Cr

Debtors A/c

To Local B2B sales A/c

To 9% Output CGST A/c

To 9% Output SGST A/c

1,41,600

1,20,000

10,800

10,800

GSTR1 >>

Table 4A

Receipt Dr

Cr

Bank

To Debtors A/c

1,29,800

1,29,800 -

Advance

Adjusted

Dr

Cr

Advance Received

To Debtors A/c

11,800

11,800

GSTR-1 >>

Table-11B (1)

Dr

Dr

Cr

9% Output CGST A/c

9% Output SGST A/c

To GST on Advances

900

900

1800

GSTR-1 >>

Table 11B (1)

Credit Note / Debit NoteNature Dr/Cr Journal Entry Amount Amount Reporting Table

Credit Note

B2B

Dr

Dr

Dr

Cr

Local B2B sales A/c

9% Output CGST A/c

9% Output SGST A/c

To Debtors A/c

1,20,000

10,800

10,800

1,41,600

GSTR 1 >>

Table 9B

Credit Note

B2C L

Dr

Dr

Dr

Cr

Local B2C sales A/c

9% Output CGST A/c

9% Output SGST A/c

To Debtors A/c

1,20,000

10,800

10,800

1,41,600

GSTR 1 >>

Table 9B

Credit Note

B2C S

Dr

Dr

Dr

Cr

Local B2C sales A/c

9% Output CGST A/c

9% Output SGST A/c

To Debtors A/c

1,20,000

10,800

10,800

1,41,600

GSTR 1 >>

Table 10

Adjustments to

Past sales

Debit Note Dr

Cr

Cr

Cr

Debtors A/c

To Local B2B sales A/c

To 9% Output CGST A/c

To 9% Output SGST A/c

1,41,600

1,20,000

10,800

10,800

GSTR 1 >>

Table 9B

Inward Supply

Inward Supply- Registered Dealer

Nature Dr /Cr Ledger a/c Amount Amount Reporting Table

Purchase –

B2B

Dr

Dr

Dr

Cr

Purchases/Exepnses-B2B A/c

Input CGST A/c

Input SGST A/c

To Creditor A/c

1,00,000

14,000

14,000

1,28,000

GSTR-2>>

Table-3

Optional : Allow the accountant to take full Input tax credit regardless of T1,T2,T3;

this can be handled at the time of file GSTR -2

Inward Supply- URD

Nature Dr/Cr Ledger a/c Amount Amount Reporting Table

Purchases –

RCM 9(3)

Dr

Dr

Dr

Cr

Cr

Cr

Purchases/Expenses -RCM

Input CGST A/c

Input SGST A/c

To Creditor A/c

To 2.5% Output CGST A/c

To 2.5% Output SGST A/c

50,000

1,250

1,250

50,000

1,250

1,250

GSTR-2>>

Table-4A

Purchases-

URD

C2B – 9(4)

Dr

Dr

Dr

Cr

Cr

Cr

Purchases/Expenses -URD

Input CGST A/c

Input SGST A/c

To Creditor A/c

To 6% Output CGST A/c

To 6% Output SGST A/c

50,000

3,000

3,000

50,000

3,000

3,000

GSTR-2>>

Table-4B

Inward Supply- URD Contd….Nature Dr/Cr Ledger a/c Amount Amount Reporting Table

RCM Liability end of

the day

As per Notification

No.8/2017-Central

Tax (Rate), purchases

up to 5k is exempted

every day.

Dr

Dr

Cr

Cr

Input CGST A/c

Input SGST A/c

To 6% Output CGST A/c

To 6% Output SGST A/c

{Purchases are normally booked

without payment of taxes. Day

end the taxes are calculated and

liability is created}

3,000

3,000

3,000

3,000

GSTR-2

Table-4B

Import of Services

Dr

Dr

Cr

Cr

Expenses

Input IGST A/c

To Creditor A/c

To 12% IGST A/c

50,000

6,000 50,000

6,000

GSTR-2

Table-4C

Inward Supply- Import

Nature Dr/Cr Ledger a/c Amount Amount Reporting Table

Import of

Goods

Dr

Dr

Cr

Cr

Purchases

Input IGST

To Creditor A/c

To 12% IGST A/c

{ Track Bill of Entry }

50,000

6,000

50,000

6,000

GSTR-2

Table-5A& 5B

Inward Supply- (Composition/Nil/ Nontaxable)

Nature Dr/Cr Ledger a/c Amount Amount Reporting Table

Purchase from

Composition Dealer

Dr

Cr

Purchases/Expenses a/c

To Creditors a/c

1,000

1,000

GSTR-2>>

Table-7 (2)

Exempted / NIL /

NON-Taxable

Purchase

Dr

Cr

Purchases/Expenses a/c

To Creditors a/c

1,000

1,000

GSTR-2>>

Table-7 (3/4/5)

Inward Supply- Advances paid to Vendors

Nature Dr/Cr Ledger a/c Amount Amount Reporting Table

Advances Paid to

Registered Vendor Regular Payment entry

Advance Paid to

Unregistered

Vendor

Dr

Cr

Creditor a/c

To Bank

1,00,000

1,00,000

GSTR-2>>

Table-10A (1)

Payment Voucher Dr

Dr

Cr

Cr

Input CGST-RCM

Input SGST- RCM

To 2.5% Output CGST A/c

To 2.5% Output SGST A/c

2,500

2,500

2,500

2,500

GSTR-2>>

Table-10A (1)

GSTR – 3 5A (1)

URD Purchase

against advance

Dr

Cr

Purchases a/c

To Creditor

1,00,000

1,00,000

GSTR-2>>

Table-4B

Inward Supply- ISD related

Nature Dr/Cr Ledger a/c Amount Amount Reporting Table

ISD Purchase of

SERVICES

Dr

Dr

Dr

Cr

Expenses-B2B A/c

Input CGST A/c

Input SGST A/c

To Creditor A/c

1,00,000

14,000

14,000

1,28,000

GSTR-6>>

Table-3

(of ISD)

ISD Purchase of

MATERIALS

Dr

Cr

Expenses-B2B A/c

To Creditor A/c

(No Credit can be availed)

1,28,000

1,28,000

GSTR-6>>

Table-3

(of ISD)

ISD Credit Transfer

(Head Office) Dr

Cr

Cr

Branch Office A/c

To Input CGST A/c

To Input SGST A/c

28,000

14,000

14,000

GSTR-2>>

Table-8A

(of Branch)

OR

GSTR-6>>

Table-5

(of ISD)

Journal Entries after filing GST Returns

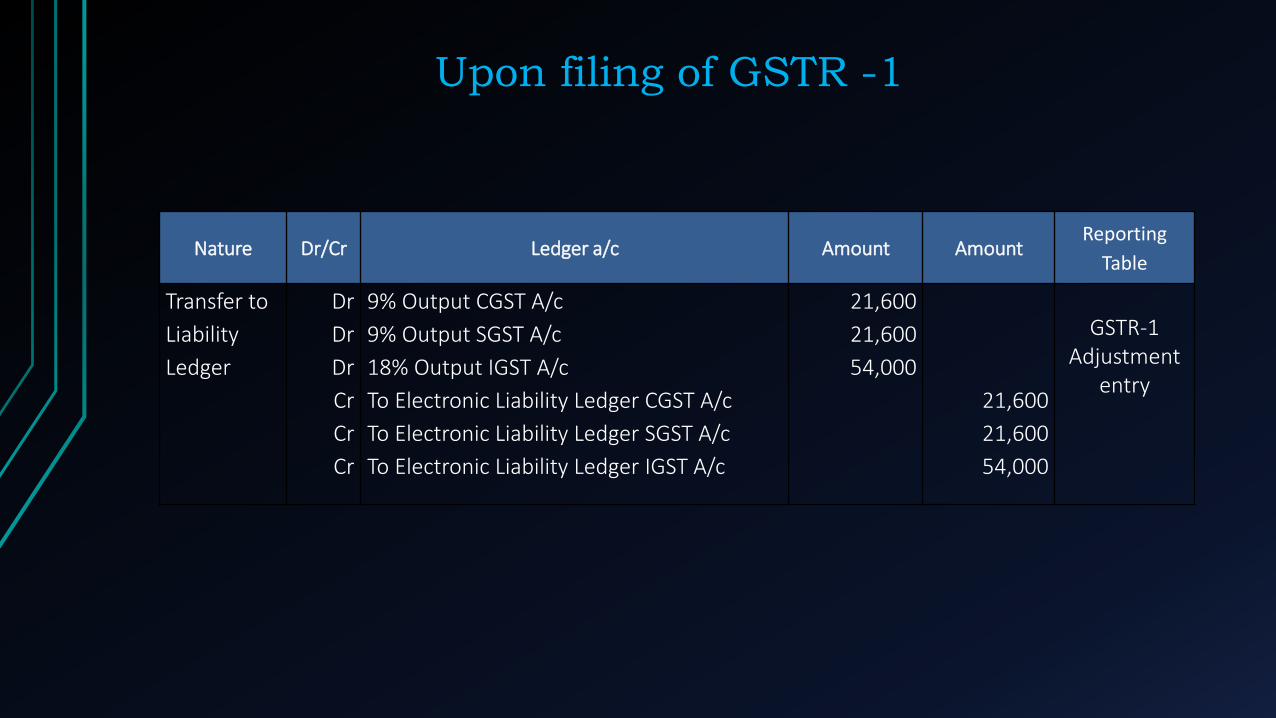

Upon filing of GSTR -1

Nature Dr/Cr Ledger a/c Amount AmountReporting

Table

Transfer to

Liability

Ledger

Dr

Dr

Dr

Cr

Cr

Cr

9% Output CGST A/c

9% Output SGST A/c

18% Output IGST A/c

To Electronic Liability Ledger CGST A/c

To Electronic Liability Ledger SGST A/c

To Electronic Liability Ledger IGST A/c

21,600

21,600

54,000

21,600

21,600

54,000

GSTR-1Adjustment

entry

Upon filing of GSTR -2Nature Dr/Cr Ledger a/c Amount Amount Reporting Table

Transfer to

Credit

Ledger

Dr

Dr

Dr

Dr

Cr

Cr

Cr

Electronic Credit CGST Ledger A/c

Electronic Credit SGST Ledger A/c

Electronic Credit IGST Ledger A/c

Expenses A/c { T1,T2,T3}

To Input CGST A/c

To Input SGST A/c

To Input IGST A/c

9,450

9,450

7,500

2,000

9,450

9,450

9,500

GSTR 2

Adjustment

entry

Basis

mismatch

Report

Dr

Dr

Dr

Cr

Cr

Cr

Provisional ITC CGST A/c

Provisional ITC SCGT A/c

Provisional ITC IGST A/c

To Electronic Credit CGST Ledger A/c

To Electronic Credit SGST Ledger A/c

To Electronic Credit IGST Ledger A/c

900

900

900

900

900

900

GSTR 2

Adjustment

entry

Inward Supply-Upon filing of GSTR -2 Contd…

Nature Dr/Cr Ledger a/c Amount Amount Reporting Table

Not attended

by supplier

Dr

Cr

Purchase/Expense a/c

To Provisional ITC XGST* A/c

900

900

Mismatch Report

Adjustment

Entry

Rectified by

supplier

Dr

Cr

Electronic Credit XGST Ledger A/c

To Provisional ITC XGST A/c

900

900

Mismatch Report

Adjustment

Entry

* XGST here shall mean CGST or SGST or IGST as applicable

Inward Supply-On Payment of Taxes

Nature Dr/Cr Ledger a/c Amount Amount Reporting Table

Transfer amount

to cash ledger

Dr

Dr

Dr

Cr

Electronic Cash CGST Ledger A/c

Electronic Cash SGST Ledger A/c

Electronic Cash IGST Ledger A/c

To Bank A/c

1,000

1,000

1,000

3,000Not Applicable

TDS / TCS Dr

Cr

Electronic Cash Ledger

To Govt / eCom Operator

Auto

populated Not Applicable

Inward Supply-Upon filing of GSTR -3

Nature Dr/Cr Ledger a/c Amount Amount Reporting Table

Transfer to

Credit Ledger

Dr

Dr

Dr

Cr

Cr

Cr

Cr

Cr

Cr

Electronic Liability Ledger CGST A/c

Electronic Liability Ledger SGST A/c

Electronic Liability Ledger IGST A/c

To Electronic Credit CGST Ledger A/c

To Electronic Credit SGST Ledger A/c

To Electronic Credit IGST Ledger A/c

To Electronic Cash CGST Ledger A/c

To Electronic Cash SGST Ledger A/c

To Electronic Cash IGST Ledger A/c

21,600

21,600

55,800

13,950

13,950

7,500

6,750

26,850

30,000

Adjustment

entry

Accounting for Transitional

Provisions & Data need to have

for filling TRAN-1 & TRAN -2

Transition Entries

Migration Entry 140(1)

38

Particulars Rs

Cenvat Credit in last Excise Returns 150

Input Tax Credit available in last VATreturns

250

Tax incidence of Non submitting ofstatutory forms (C form to be submitted forsale value of Rs.5,000/- )(5.5%-2%)

(175)

PRE GST POST GST

Particulars Rs

Input Credit available to CGST CreditLedger

150

Input Credit available to SGST CreditLedger

75(250-175)

Electronic Credit CGST Ledger Dr 150Electronic Credit SGST Ledger Dr 75

To CENVAT Credit A/c 150To Input Vat A/c 75

Migration Entry 140(2)

Particulars Rs

Cenvat Credit available for Capital Goods 250

Input Tax Credit availed so far 125

Balance credit not availed 125

PRE GST

Electronic Credit CGST Ledger Dr 125

To Input CENVAT A/c 125

Trader 140(3) Deemed Credit

Conditions:

• Used or intended to be used for taxable supply

• Eligible for credit under GST

• Goods should be excisable and not exempt or nil rate

• Pass on all the benefit to customer

• Documents evidencing procurement is available

Entry to be passed for sale of such goodsParty Account A/c Dr XXXTransitional Discount A/c Dr XX

To Sales @ 12% A/c XXXTo CGST Liability ledger A/c XXTo SGST Liability ledger A/c XX

Entry to be passed for taking creditCGST Credit Liability A/c XX

To Transitional discount A/c XX

Trader 140(3) Deemed Credit

Supply Value GST Rate Type of tax CGST paidIGST Paid

Deemed Credit rate

Deemed credit value

% on sale value

10000 5% CGST 250 0 40% of CGST 100 1.00%

10000 12% CGST 600 0 40% of CGST 240 2.40%

10000 18% CGST 900 0 60% of CGST 540 5.40%

10000 28% CGST 1400 0 60% of CGST 840 8.40%

10000 5% IGST 0 500 20% of IGST 100 1.00%

10000 12% IGST 0 1200 20% of IGST 240 2.40%

10000 18% IGST 0 1800 30% of IGST 540 5.40%

10000 28% IGST 0 2800 30% of IGST 840 8.40%

Example for above

Particulars Amount

Base Price 500

Add: CGST at 6 % 30

Add: SGST at 6% 30

Total Commercial Value 560

Less: Discount Eligible Credit at 40% of CGST i.e., Rs.30 (12)

Selling Price 548

On Sale

Party Account A/c Dr 548Transitional Discount A/c Dr 12

To Sales @ 12% A/c 500To CGST Liability ledger A/c 30To SGST Liability ledger A/c 30

Up on TRAN – 2

Electronic Credit CGST Ledger A/c 12To Transitional discount A/c 12