Download - ABC Costing 03

8/8/2019 ABC Costing 03

http://slidepdf.com/reader/full/abc-costing-03 1/28

Activity Based Costing:A Tool to Aid Decision Making

8/8/2019 ABC Costing 03

http://slidepdf.com/reader/full/abc-costing-03 2/28

© The McGraw-Hill Companies, Inc., 2000 Irwin/McGraw-Hill

Activity Based Costing (ABC)

The objective of activity-basedcosting is tounderstand

overhead and theprofitability of

products andcustomers.

ABC is agood supplementto our traditional

cost system I agree!

8/8/2019 ABC Costing 03

http://slidepdf.com/reader/full/abc-costing-03 3/28

© The McGraw-Hill Companies, Inc., 2000 Irwin/McGraw-Hill

Ov erhead rates maybe based on acti v ity

at capacity.

Activity Based Costing (ABC)

Acti v ity-Based Costing

Both manufacturingand nonmanufacturing

costs may beassigned toproducts.

Some manufacturingcosts may be excluded

from product

costs.

There are a number of cost pools each of

which is allocatedusing a unique

measure of acti v ity.

Allocation bases oftendiffer from

traditional costingsystems.

8/8/2019 ABC Costing 03

http://slidepdf.com/reader/full/abc-costing-03 4/28

© The McGraw-Hill Companies, Inc., 2000 Irwin/McGraw-Hill

H ow Costs are Treated UnderActivity-Based Costing

Overhead Allocation

P lantwideOv erhead

Rate

DepartmentalOv erhead

Rates

Acti v ity BasedCosting

8/8/2019 ABC Costing 03

http://slidepdf.com/reader/full/abc-costing-03 5/28

© The McGraw-Hill Companies, Inc., 2000 Irwin/McGraw-Hill

P lantwide Overhead Rate

C ompanies tend to use direct labor direct labor as the overhead allocation base.

8/8/2019 ABC Costing 03

http://slidepdf.com/reader/full/abc-costing-03 6/28

© The McGraw-Hill Companies, Inc., 2000 Irwin/McGraw-Hill

A two stage process isnecessary because costs

are allocated to departmentsand then to products.

F inishing Department

Shipping Department

Painting Department

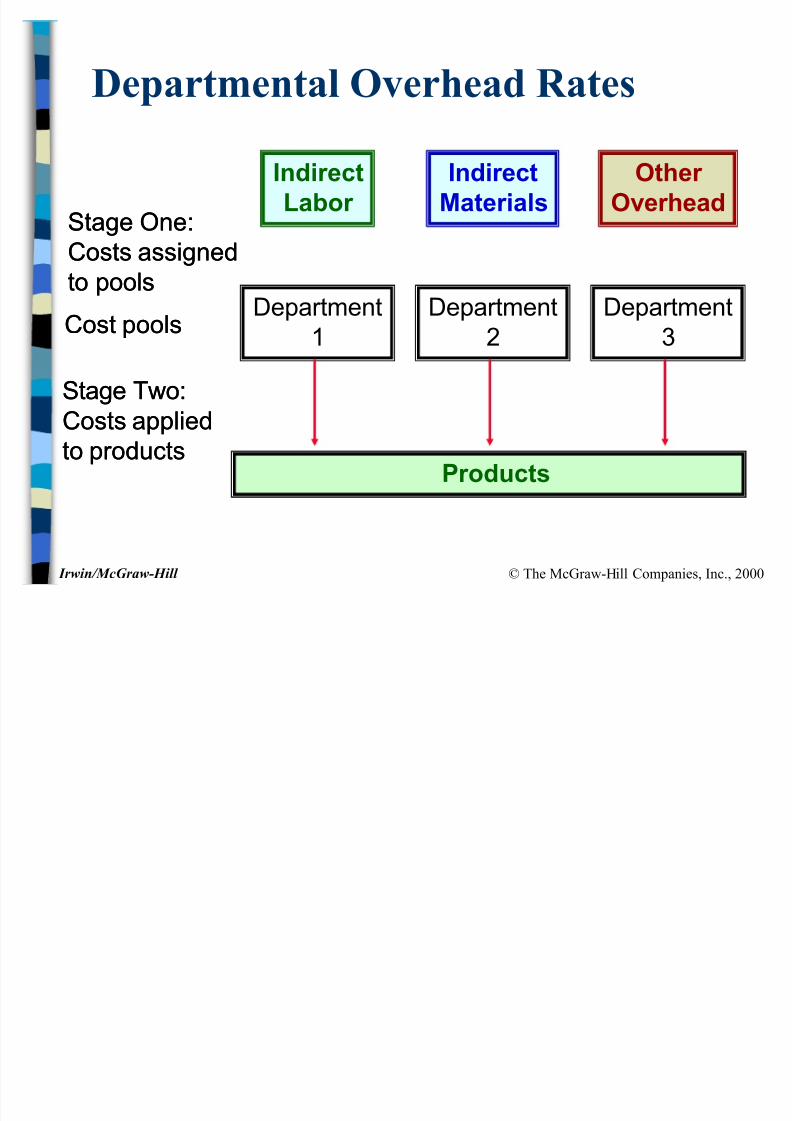

Departmental Overhead Rates

8/8/2019 ABC Costing 03

http://slidepdf.com/reader/full/abc-costing-03 7/28

© The McGraw-Hill Companies, Inc., 2000 Irwin/McGraw-Hill

Department1

Department2

Department3

C ost poolsC ost pools

IndirectLabor

IndirectMaterials

O ther Ov erhead

Stage One:Stage One:C osts assignedC osts assignedto poolsto pools

Departmental Overhead Rates

8/8/2019 ABC Costing 03

http://slidepdf.com/reader/full/abc-costing-03 8/28

© The McGraw-Hill Companies, Inc., 2000 Irwin/McGraw-Hill

Department1

Department2

Department3

C ost poolsC ost pools

Stage One:Stage One:C osts assignedC osts assignedto poolsto pools

P roducts

Stage Two:Stage Two:C osts appliedC osts appliedto productsto products

Departmental Overhead Rates

IndirectLabor

IndirectMaterials

O ther Ov erhead

8/8/2019 ABC Costing 03

http://slidepdf.com/reader/full/abc-costing-03 9/28

© The McGraw-Hill Companies, Inc., 2000 Irwin/McGraw-Hill

Department1

Department2

Department3

C ost poolsC ost pools

Stage One:Stage One:C osts assignedC osts assignedto poolsto pools

P roducts

Stage Two:Stage Two:C osts appliedC osts appliedto productsto products

Direct

Labor Hours

Machine

Hours

Raw

MaterialsC ost

Departmental Allocation Bases

Departmental Overhead Rates

IndirectLabor

IndirectMaterials

O ther Ov erhead

8/8/2019 ABC Costing 03

http://slidepdf.com/reader/full/abc-costing-03 10/28

© The McGraw-Hill Companies, Inc., 2000 Irwin/McGraw-Hill

Designing an ABC System

Cost O bjects(e.g., products

and customers)Acti v ities

Consumptionof Resources

Cost

8/8/2019 ABC Costing 03

http://slidepdf.com/reader/full/abc-costing-03 11/28

© The McGraw-Hill Companies, Inc., 2000 Irwin/McGraw-Hill

Designing an ABC System

Steps for Implementing AB CSteps for Implementing AB C

Identify and define activities and activity pools.Where possible, trace costs to activities and costobjects.

Assign costs to activity cost pools.C alculate activity rates.

Assign costs to cost objects.Prepare management reports.

8/8/2019 ABC Costing 03

http://slidepdf.com/reader/full/abc-costing-03 12/28

© The McGraw-Hill Companies, Inc., 2000 Irwin/McGraw-Hill

I dentifying Activity to I nclude

A part of the productionA part of the productionprocess for which managementprocess for which management

wants a separate reporting of thewants a separate reporting of thecosts of the acti v ity in v ol v ed.costs of the acti v ity in v ol v ed.

Unit-Le v elActi v ity

Batch-Le v elActi v ity

P roduct-Le v elActi v ity

Customer-Le v elActi v ityO rganization-

sustaining

Acti v ity

8/8/2019 ABC Costing 03

http://slidepdf.com/reader/full/abc-costing-03 13/28

© The McGraw-Hill Companies, Inc., 2000 Irwin/McGraw-Hill

I dentifying Activity to I nclude

Acti v ity Cost P oolActi v ity Cost P oolis a ³bucket´ in

which costs areaccumulated thatrelate to a single

activity in the AB C system.

$

$

$ $

$$

8/8/2019 ABC Costing 03

http://slidepdf.com/reader/full/abc-costing-03 14/28

© The McGraw-Hill Companies, Inc., 2000 Irwin/McGraw-Hill

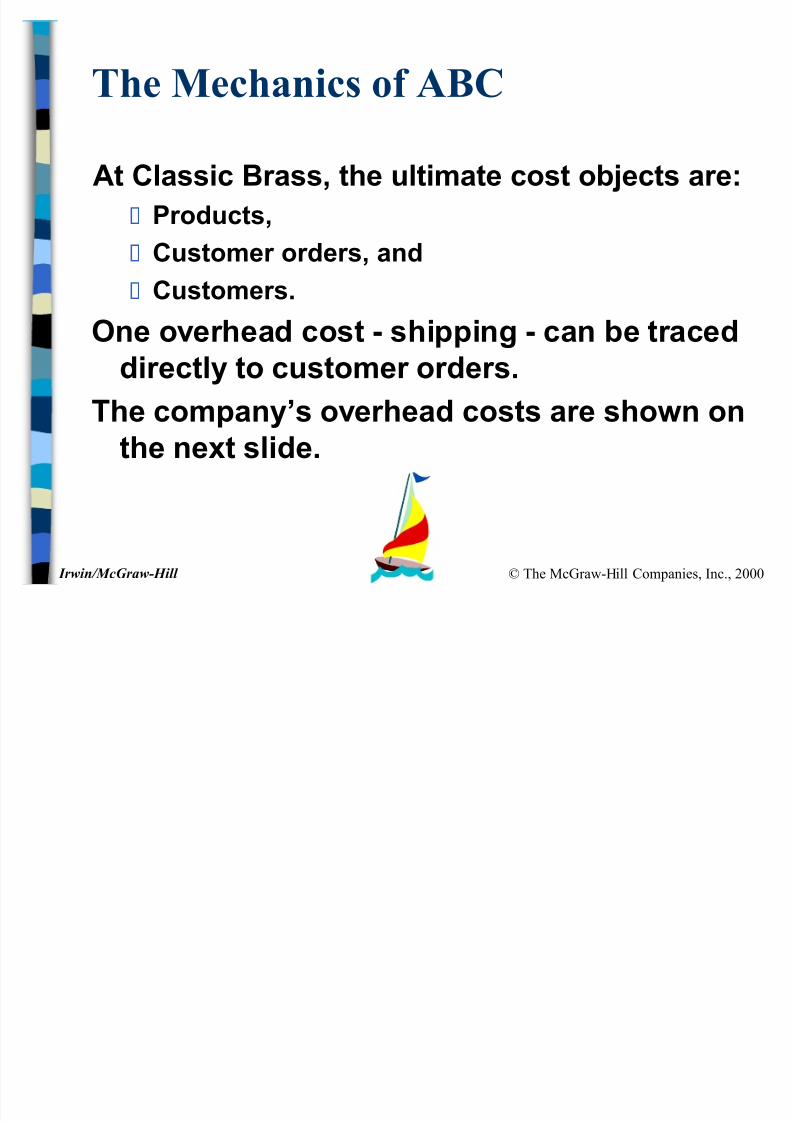

The Mechanics of ABC

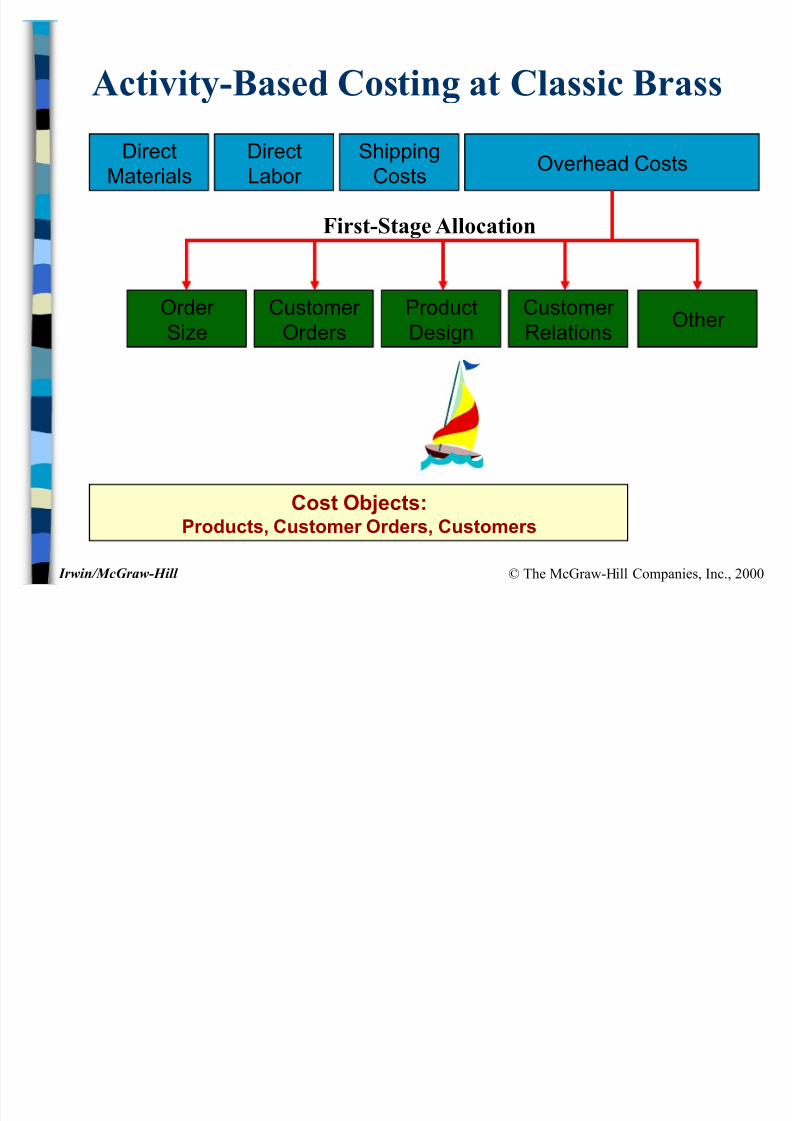

At Classic Brass, the ultimate cost objects are:P roducts,Customer orders, andCustomers.

O ne o v erhead cost - shipping - can be traceddirectly to customer orders.

The company¶s o v erhead costs are shown onthe next slide.

8/8/2019 ABC Costing 03

http://slidepdf.com/reader/full/abc-costing-03 15/28

© The McGraw-Hill Companies, Inc., 2000 Irwin/McGraw-Hill

Produc t on Depar t en tndirec t f ac tory wages 500,000$Fac tory equipmen t deprecia tion 300,000 Fac tory u tilities 120,000 Fac tory building lease 80,000 1,000,000$

Shipping cos ts traced to cus tomer orders 40,000 General Adminis tra tive Depar tmen tAdminis tra tive wages and salaries 400,000 Off ice equipmen t deprecia tion 50,000 Adminis tra tive building lease 60,000 510,000

Marke ting Depar tmen tMarke ting wages and salaries 250,000 Selling expenses 50,000 300,000

To tal overhead cos ts 1,850,000$

Overhead Cos ts a t Classic Brass(Manu f ac turing and NonManu f ac turing )

8/8/2019 ABC Costing 03

http://slidepdf.com/reader/full/abc-costing-03 16/28

© The McGraw-Hill Companies, Inc., 2000 Irwin/McGraw-Hill

Activity-Based Costing at Classic Brass

DirectMaterials

DirectLabor

ShippingC osts Overhead C osts

Traced $/ DLH Traced

Cost O bjects:P roducts, Customer O rders, Customers

8/8/2019 ABC Costing 03

http://slidepdf.com/reader/full/abc-costing-03 17/28

© The McGraw-Hill Companies, Inc., 2000 Irwin/McGraw-Hill

Activity-Based Costing at Classic Brass

DirectMaterials

DirectLabor

ShippingC osts

Order Size

C ustomer Orders

ProductDesign

C ustomer Relations

Other

Overhead C osts

Cost O bjects:P roducts, Customer O rders, Customers

F irst-Stage Allocation

8/8/2019 ABC Costing 03

http://slidepdf.com/reader/full/abc-costing-03 18/28

© The McGraw-Hill Companies, Inc., 2000 Irwin/McGraw-Hill

Activity-Based Costing at Classic Brass

DirectMaterials

DirectLabor

ShippingC osts

Cost O bjects:P roducts, Customer O rders, Customers

Order Size

C ustomer Orders

ProductDesign

C ustomer Relations

Other

Overhead C osts

F irst-Stage Allocation

Second-Stage Allocations

$/ MH $/ O rder $/ Design $/ Customer

Unallocated

8/8/2019 ABC Costing 03

http://slidepdf.com/reader/full/abc-costing-03 19/28

© The McGraw-Hill Companies, Inc., 2000 Irwin/McGraw-Hill

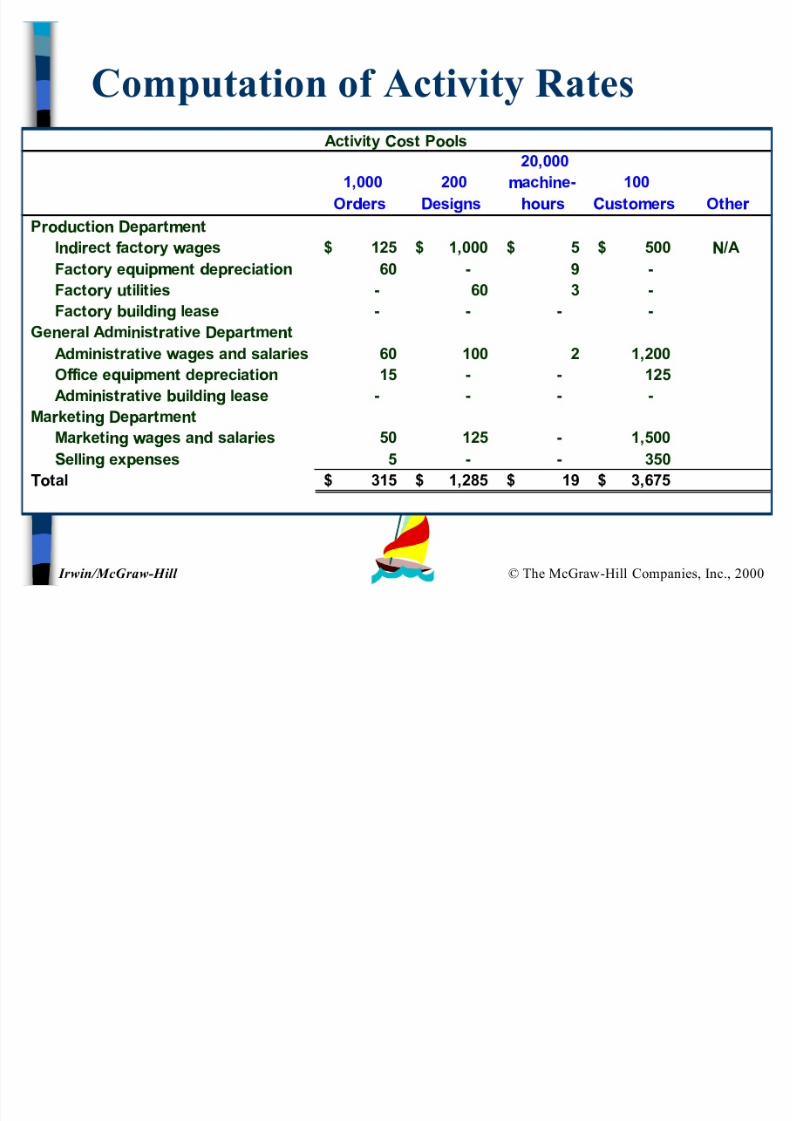

Assigning Costs to Activity Cost P ools

Customer Orders

ProductDesign

Order Size

Customer Relations Other Total

Production DepartmentIndirect factory wages 25% 40% 20% 10% 5% 100%Factory equipment depreciation 20% 0% 60% 0% 20% 100%Factory utilities 0% 10% 50% 0% 40% 100%Factory building lease 0% 0% 0% 0% 100% 100%

Shipping costs traced to customer order N/AGeneral Administrative Department

Administrative wages and salaries 15% 5% 10% 30% 40% 100%Office equipment depreciation 30% 0% 0% 25% 45% 100%Administrative building lease 0% 0% 0% 0% 100% 100%

Marketing DepartmentMarketing wages and salaries 20% 10% 0% 60% 10% 100%Selling expenses 10% 0% 0% 70% 20% 100%

Activity Cost Pools

Management at C lassic Brass believes overhead should bedistributed as follows:

8/8/2019 ABC Costing 03

http://slidepdf.com/reader/full/abc-costing-03 20/28

© The McGraw-Hill Companies, Inc., 2000 Irwin/McGraw-Hill

Customer Orders

ProductDesign

Order Size

Customer Relations Other Total

Production DepartmentIndirect factory wages 125,000$

Factory equipment depreciationFactory utilitiesFactory building lease

General Administrative DepartmentAdministrative wages and salariesOffice equipment depreciationAdministrative building lease

Marketing Department

Marketing wages and salariesSelling expenses

Total

Activity Cost Pools

Assigning Costs to Activity Cost P ools

Indirect factory wages $500,000Percent consumed by customer orders 25%

$125,000

Using the total costs and percentage consumption of overhead, costs are assigned to activity pools.

8/8/2019 ABC Costing 03

http://slidepdf.com/reader/full/abc-costing-03 21/28

© The McGraw-Hill Companies, Inc., 2000 Irwin/McGraw-Hill

Customer Orders

ProductDesign

Order Size

Customer Relations Other Total

Production DepartmentIndirect factory wages 125,000$

Factory equipment depreciation 60,000 Factory utilitiesFactory building lease

General Administrative DepartmentAdministrative wages and salariesOffice equipment depreciationAdministrative building lease

Marketing Department

Marketing wages and salariesSelling expenses

Total

Activity Cost Pools

Assigning Costs to Activity Cost P ools

Factory equipment depreciation $300,000Percent consumed by customer orders 20%

$ 60,000

Using the total costs and percentage consumption of overhead, costs are assigned to activity pools.

8/8/2019 ABC Costing 03

http://slidepdf.com/reader/full/abc-costing-03 22/28

© The McGraw-Hill Companies, Inc., 2000 Irwin/McGraw-Hill

Customer Orders

ProductDesign

Order Size

Customer Relations Other Total

Production DepartmentIndirect factory wages 125,000$ 200,000$ 100,000$ 50,000$ 25,000$ 500,000$

Factory equipment depreciation 60,000 - 180,000 - 60,000 00,000 Factory utilities - 12,000 60,000 - 48,000 120,000 Factory building lease - - - - 80,000 80,000

General Administrative DepartmentAdministrative wages and salaries 60,000 20,000 40,000 120,000 160,000 400,000 Office equipment depreciation 15,000 - - 12,500 22,500 50,000 Administrative building lease - - - - 60,000 60,000

Marketing Department

Marketing wages and salaries 50,000 25,000 - 150,000 25,000 250,000 Selling expenses 5,000 - - 5,000 10,000 50,000

Total 15,000$ 257,000$ 80,000$ 67,500$ 490,500$ 1,810,000$

Activity Cost Pools

Assigning Costs to Activity Cost P oolsU

sing the total costs and percentage consumption of overhead, costs are assigned to activity pools.

8/8/2019 ABC Costing 03

http://slidepdf.com/reader/full/abc-costing-03 23/28

© The McGraw-Hill Companies, Inc., 2000 Irwin/McGraw-Hill

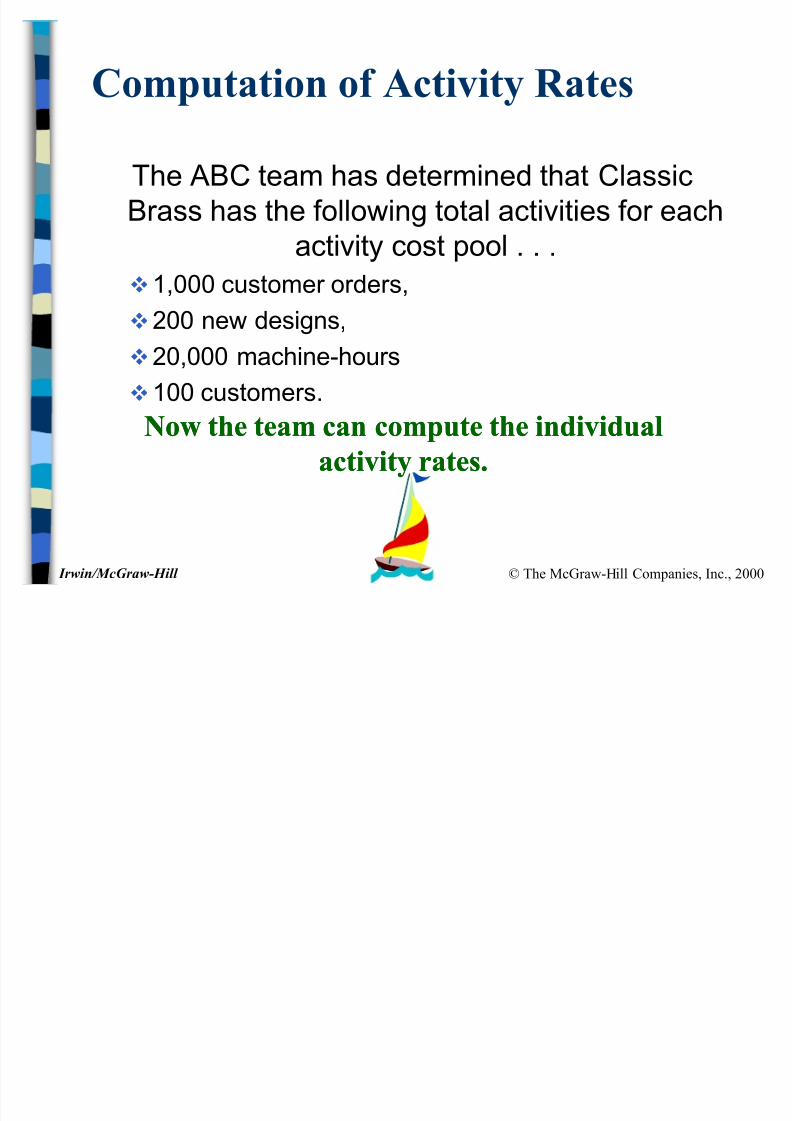

Computation of Activity Rates

The AB C team has determined that C lassicBrass has the following total activities for each

activity cost pool . . .1,000 customer orders,200 new designs,20,000 machine-hours100 customers.

N ow the team can compute the individualN ow the team can compute the individualactivity rates.activity rates.

8/8/2019 ABC Costing 03

http://slidepdf.com/reader/full/abc-costing-03 24/28

8/8/2019 ABC Costing 03

http://slidepdf.com/reader/full/abc-costing-03 25/28

8/8/2019 ABC Costing 03

http://slidepdf.com/reader/full/abc-costing-03 26/28

© The McGraw-Hill Companies, Inc., 2000 Irwin/McGraw-Hill

Difference Between ABC andTraditional P roduct Costs

AB C will ordinarily shiftbatch-level and

product-level

overhead costs fromhigh-volume

products produced inlarge batches to low-

volume productsproduced in small

batches.

8/8/2019 ABC Costing 03

http://slidepdf.com/reader/full/abc-costing-03 27/28

© The McGraw-Hill Companies, Inc., 2000 Irwin/McGraw-Hill

Difference Between ABC andTraditional P roduct Costs

U nder AB C bothmanufacturing andnonmanufacturing

costs may beassigned to products.

Organization-sustaining costs and

the costs of idlecapacity are not

assigned to products.

8/8/2019 ABC Costing 03

http://slidepdf.com/reader/full/abc-costing-03 28/28

© The McGraw-Hill Companies, Inc., 2000 Irwin/McGraw-Hill

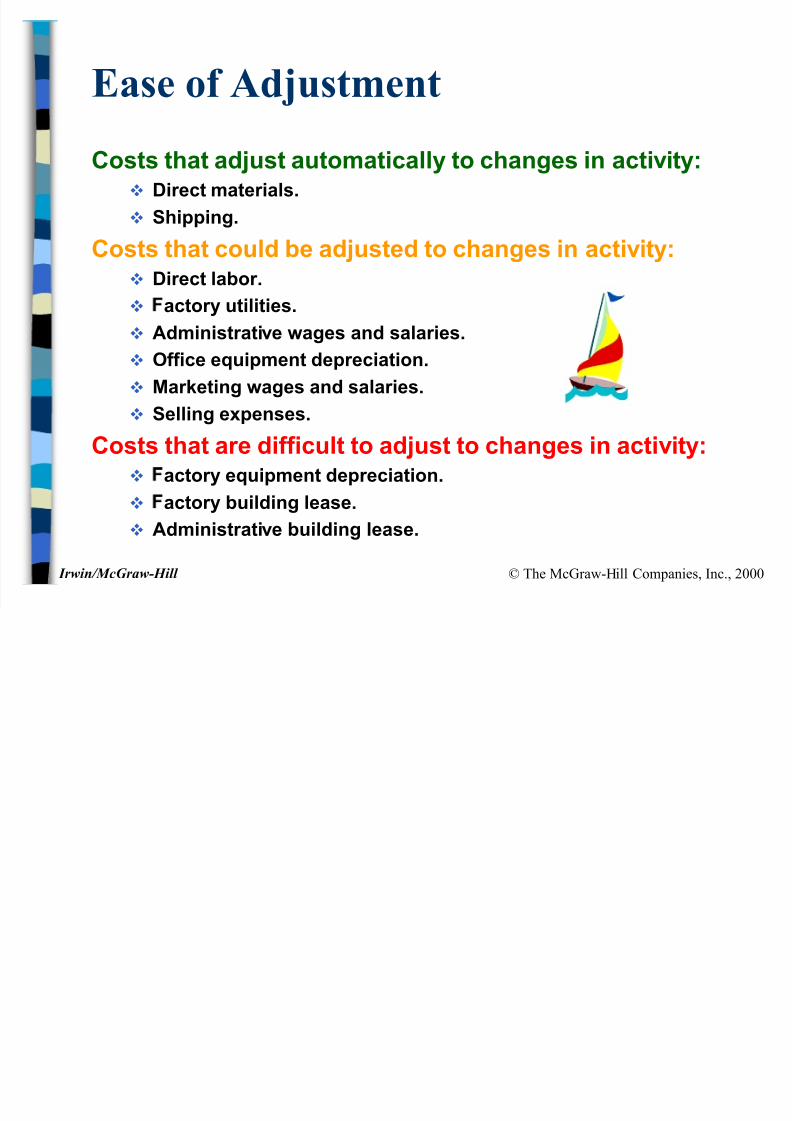

E ase of Adjustment

Costs that adjust automatically to changes in acti v ity:Direct materials.Shipping.

Costs that could be adjusted to changes in acti v ity:Direct labor.

actory utilities.Administrati v e wages and salaries.O ffice equipment depreciation.Marketing wages and salaries.

Selling expenses.Costs that are difficult to adjust to changes in acti v ity:

actory equipment depreciation.actory building lease.

Administrati v e building lease.