A SURVIVAL THEORY OF INTERNET FIRM DURATION

Robert J. Kauffman Director, MIS Research Center

Professor and Chair, Information and Decision Sciences Phone: (612) 624-8562; Fax: (612) 626-1316

Email: [email protected]

Bin Wang Doctoral Program, Information and Decision Sciences

Phone: (612) 624-6041; Fax: (612) 626-1316 Email: [email protected]

Carlson School of Management, University of Minnesota

Minneapolis, MN 55455

Last Revised: November 20, 2003 ____________________________________________________________________________

ABSTRACT

More than 5000 Internet firms have failed since the beginning of 2000. One common perception is that the downturn in the economy drove many firms out of business. However, why are some firms still alive while others are not? In this research, we examine the impact of various industry, firm and e-commerce-related drivers on Internet firm survival from the multiple perspectives of accounting and finance, information systems (IS), economics and organizational theory research. We analyze a panel data set of 115 public Internet firms using three different techniques: logit, nonparametric survival analysis and the semiparametric Cox proportional hazards model. The use of these econometric methods permits us to answer key research questions and cross-validate results. We characterize the survival rates throughout the lifetimes of the public Internet firms in our sample. Our results reveal that selling digital goods or services, entry of additional Internet firms via IPOs in the stock market, a larger firm size and a lower leverage (in terms of total debt/total assets) reduced the likelihood of failure. KEYWORDS: Duration modeling, binary choice model, econometrics, electronic commerce,

empirical methods, Internet firms, logit, morphing strategies, survival analysis. _____________________________________________________________________________________

ACKNOWLEDGEMENTS. We thank Dennis Ahlburg, Rajiv Banker, Alina Chircu, Eric Clemons, Qizhi Dai, Gordon Davis, Rajiv Dewan, Alok Gupta, Jungpil Hahn, Yuji Honjo, Bao-Jun Jiang, M.S. Krishnan, Zining Li, Hank Lucas, Brian McCall, Fred Riggins, Pervin Shroff, Eric Walden, Chuck Wood and participants of the “Competitive Strategy and Information Technology” mini-track at HICSS-36, the 2002 Workshop on Information Systems and Economics, the Information and Decision Sciences workshop at the Carlson School of Management of the University of Minnesota and the Computer and Information Systems department at the University of Michigan Business School for their valuable input on related versions of this paper. We also thank Tim Miller, CEO of Webmergers.com, for access to Internet firm bankruptcy and shutdown data. All errors of fact or interpretation are the sole responsibility of the authors. Rob Kauffman thanks the MIS Research Center for partial support.

1

INTRODUCTION

Fueled by advances in information technologies (IT) in the 1990s, Internet firms emerged to

facilitate online transactions, and leverage unique characteristics that set them apart from

traditional bricks-and-mortar businesses. The emergence of Web portal sites, online financial

service Web sites, and business-to-business (B2B) e-intermediaries has allowed new market

entrants to benefit from the emerging digital channel to deliver information and provide services

that were not previously available. But how can we explain the survival of Internet firms?

Although the information systems (IS) literature has examined IT and firm performance from

perspectives such as productivity (Brynjolfsson and Hitt 1996) and organizational form and

market structure (Clemons and Reddi 1993, Malone et al. 1987), it lacks findings on the survival

of IT-focused firms, in spite of the many Internet firm failures observed since 2000. According

to Webmergers.com (2003), mergers and acquisitions, about 5,000 Internet companies shut down

their sites or were acquired during the three-year period after the first quarter of 2000. Our

intended contribution to the IS literature is a survival theory of Internet firm duration and the

drivers behind the firm failures that were observed, as well as a means to identify the critical

factors for survival to optimize their resource allocation. We examine the impact of the

characteristics for traditional businesses on Internet firm survival, and also unique characteristics

of Internet firms, such as the product types or services a firm provides. This allows us to extend

our understanding on how advances in IT and the extent to which they are used to create unique

product offerings and reduce operational costs affect firm performance.

We answer the following research questions:

� How can different theories contribute to IS knowledge on IT-focused firm performance?

� What theory can we use to distinguish healthy Internet firms from those near bankruptcy?

2

� What are the key industry, firm and e-commerce-related variables that influence the

survival of Internet firms, and what are their relative explanatory capabilities?

� How can different modeling formulations contribute to a richer understanding of the

competition and firm survival in the digital marketplace?

While research on firm survival can be conducted at different levels, our intended

contribution is at the firm to business process level where there are identifiable firm

characteristics that can affect survival. By analyzing the duration of 115 public Internet firms

after their initial public offerings (IPOs) using a combination of the logit model and survival

analysis econometrics, the current research obtained four major results. First, the failure of

publicly-traded Internet firms mainly occurred between one and five years after they floated

IPOs in the stock market. The reason we compare firms starting from IPO issuance is because, in

survival analysis, observations are compared based on age, not on calendar time. Second, it was

not who the customers are but what kind of products or services an Internet firm provides that

mattered. Third, additional Internet firm IPOs actually reduced the likelihood of bankruptcy for

existing Internet firms. Finally, our use of different estimation models suggests the different

dimensions of the dynamics of Internet firm survival and allowed us to cross-validate our results.

THEORETICAL BACKGROUND

We next identify relevant theoretical underpinnings of the performance of IT-focused firms.

Accounting and Financial Research on Business Failure

Various financial ratios and cash flow components have been used to predict business failure.

Positing that the short-term financial management performance is related to bankruptcy, the

accounting and finance literature have used financial ratios such as return on investment (ROI),

capital turnover, financial leverage, short-term liquidity, cash position, inventory turnover and

3

receivable turnover to classify failed and non-failed firms (Gentry et al. 1984). However, this

research has been criticized for the lack of theoretical support since significant variables are

selected from a set of 20 to 40 financial ratios and the results are usually sample-dependent. To

correct for this problem, Gentry et al. (1985, 1987) developed models based on funds flow

components. They argue that since the net cash inflows of a firm should be the same as its net

cash outflows, we can examine the level and speed of the cash flow components and diagnose

the financial health of the firm. Their results suggest that dividends, investment and receivables

can be used to classify healthy and failed firms. But Casey and Bartczak (1985) and Gombola et

al. (1987) report no significant relationship between cash flow components and bankruptcy,

while Mossman et al. (1998) find that cash flow-based models have a higher predictive power

two or three years prior to bankruptcy, but predict less well any earlier.

Organizational Ecology Literature on Industry Evolution

The organizational ecology literature provides a framework to understand the evolutionary

process that firms experience in their industry contexts involving legitimacy and competition

(Hannan and Carroll 1992, Hannan et al. 1998). When a population of firms is young, it lacks

external legitimacy due to the small number of firms in the industry. As more firms enter and

the density of firms in the industry increases, industry legitimacy increases, resulting in a

temporarily lower mortality rate. However, as density continues to increase, competition also

intensifies, which results in reduced new firm entry and increased mortality. And, as one industry

grows and becomes institutionalized and its ties with other industries and networks supporting its

operations become stronger, changes in density no longer have as strong an impact on legitimacy

as they did earlier. But firms in one population increasingly find themselves competing with

other firms in the same niche as an industry matures.

4

Economics Research on Industry Evolution and Business Failure

Economics serves as a general theoretical backdrop for understanding firm competition and

exit behavior. It allows us to identify relevant industry and firm-related factors that affect

Internet firm survival. Nelson and Winter (1982) propose an evolutionary theory of organization

change and industry transformation. Contrary to neoclassical micro-theory which assumes

rational individuals, the authors argue that managers are boundedly rational and make decisions

based on standard organizational routines instead of “true” value maximization. Firms also

exhibit search behavior, which leads to modifications in their routines. The industry, sector and

competitors constitute the selection environment the firm faces. Nelson and Winter identify a

feedback loop wherein the rich get richer and the poor get poorer. As a result, we observe

increased industry concentration.

Economists also have explored industry evolution and market structure with a “product life

cycle” (PLC) perspective (Gort and Klepper 1982, Klepper 1996). As technologies evolve,

many industries exhibit similar patterns. First there is an increase in the number of firms in the

industry, followed by a sharp decline, and then the number of firms levels off. Early on, there

are many firms entering and innovating to provide different versions of the industry’s product.

Even though these firms are usually small, their mortality rate is low because prices are high. As

more firms enter and industry output increases, prices drop. But as the industry grows, chances

for innovation diminish and dominant product designs emerge. Firms compete based on

minimum efficient scale (MES) and the less efficient firms fail. Eventually, the entry and the

exit of firms reach equilibrium and we see a relatively stable number of firms in the industry.

Economists also analyze drivers of survival over shorter periods and for different industries.

Both the industry that the firm competes in and the economic descriptors of the firm and its

5

operations can affect the survival outcome. Industry-related factors include the technological

regime of the industry and rate of new firm entry. Audretsch (1991) reports that new startups are

more likely to survive in industries with an entrepreneurial regime, where it is possible to create

innovation advantages over established firms. Startups are more prone to fail in a routinized

regime, where incumbents have scale economies and startups face high initial setup costs, in

accord with PLC theory. Honjo (2000) finds that Japanese manufacturing startups are less likely

to survive in industries with higher rate of new firm entry. High entry rates may point to low

entry barriers (Geroski and Schwalbach 1991), resulting in fiercer competition.

Firm-related factors that can affect business survival include financial capital, startup size,

post-entry firm size, and founding time. A larger startup size can enhance a manufacturer’s

chance of survival due to the smaller gap between its size and the industry’s MES, allowing the

firm to benefit from economy of scale (Audretsch and Mahmood 1995). Honjo (2000) finds that

when financial capital and post-entry firm size are tested independently, both have beneficial

impacts, reducing the failure rate for Japanese manufacturers. However, when both variables are

tested in the same model, only financial capital is significant. It seems that the reported

relationship between larger firm size and reduced failure rate actually reflects the impact of

financial capital. Larger firms tend to have more abundant resources—“deeper pockets”—and

are more resistant to financial pressures that result in bankruptcy. Honjo also finds that firms

that are founded right before or after a market crash are more likely to fail.

Factors such as a larger firm size, older age at IPO, a higher initial IPO ROI, more IPOs co-

occurring in the market, and a higher percentage of the firm owned by insiders can enhance a

firm’s likelihood of survival after its IPO issuance (Hensler et al. 1997). But firms that issued

IPOs when stock prices are high and those facing higher risks, as specified in their IPO

6

prospectus, tend to fail more. Also, firms in the optical and pharmaceutical industries are more

likely to survive than computer and data, wholesale, restaurant, and airline firms.

IS and E-Commerce Research on the Efficacy of Different Internet Firm Business Models

Research on the performance differences of traditional and Internet firms informs us on how

IT gives Internet firms unique characteristics that can affect their competitiveness. Barua et al.

(2000) study the relationship between firm productivity and the products or services an Internet

firm provides. They examine digital Internet firms that sell digital products or services and are

able to directly use the Internet as the delivery channel, and physical Internet firms that sell

physical goods or services utilizing the digital channel but deliver their products via physical

channels. Digital product Internet firms achieve higher productivity benefits. Negligible

marginal production costs for digital goods and low e-delivery costs make digital firms better

able to achieve lower operational costs and higher productivity than physical firms.

Day et al. (2003) identify two types of business-to-business (B2B) e-markets. Breakthrough

markets use the Internet to facilitate creation of new products or services and markets. Examples

are portal sites and online auctions. In re-formed markets, the structure, function and purpose of

the market do not change. The Internet merely enhances existing business practices. B2B e-

markets and online banking are examples. Most e-markets lie on a continuum between the two

types. New startups are more likely to survive when they compete in breakthrough markets.

Incumbents are more likely to catch up and dominate in re-formed markets.

While the labels used differ, the above-mentioned research both capture an essential aspect of

Internet firms: how well they utilize the digital channel to create competitive advantage (Porter

1985). Digital product Internet firms can use this channel to reduce operating costs, and build a

cost advantage over physical firms. Firms that create breakthrough markets are able to deliver

7

unique value to their customers and serve brand new markets untouched by traditional

businesses. Also, firms that operate closer to breakthrough markets tend to provide digital goods

or services while firms closer to re-formed markets serve physical products. For example, portal

and online auction sites disseminate information and provide a virtual community where buyers

and sellers can trade. Firms in re-formed markets, such as e-tailers, have to physically deliver

their products and hence are physical firms.

Subramani and Walden (2001, 2002) study commerce initiative announcements and stock

prices. They distinguish two types of Internet firms: B2C firms with consumer customers, and

B2B firms with business customers. Their results suggest that B2C firm e-commerce

announcements yielded higher returns to shareholders than those of B2B firms in 1998

(Subramani and Walden 2001) but lower returns than for B2B e-commerce announcements

during 1999 and 2000 (Subramani and Walden 2002). Due to the e-commerce market hype that

existed from 1998 to 2000, we interpret these results as primarily capturing investor psychology.

Nevertheless, their research suggests differences in the market valuation of Internet firms.

Hypotheses

Our goal in this research is to build a theory on the performance of Internet firms, a group of

firms that have IT at the core of their businesses. Based on the literature, we identified industry,

firm and e-commerce-related factors that affect the survival of a typical business. To support a

test of our theory, we will build a model that is comprehensive enough to include variables in the

above three categories, yet parsimonious enough to make meaningful data analysis possible with

a data set on publicly-traded firms. Not all of the variables from prior research are relevant for

e-commerce and digital intermediation. For example, we observe no meaningful variation in the

technological regime of the industry, but we include other variables that have been most often

8

used, such as financial capital and firm size. We next state our research hypotheses. Similar to

Chen and Hitt (2002) and Lim and Benbasat (2000), we specify our hypotheses in both the null

and positive forms based on our theory-driven expectations about the likely significance of the

variables and their signs.

Prior research on business failure indicates that the new firm entry rate can influence startup

firm survival due to fiercer competition. Due to lack of industry definitions for the digital

marketplace and unavailable new firm entry rates for Internet sector industries, we approximate

this variable using the rate of Internet firm IPOs. A limitation of this operationalization is that

we cannot differentiate industries. However, we capture the key aspect of competition in market

capital among all Internet firms, which is essential to publicly-traded firms in the stock market.

□ HYPOTHESIS 1 (THE NEW FIRM ENTRY RATE HYPOTHESIS): Internet firms are less likely to survive when the rate of new firm entry in the digital marketplace, measured by the number of new IPOs in the stock market, is high.

Firm size is frequently used as a control variable in IS research. We state its impact in a

hypothesis due to the economics literature’s reading on the influence of firm size on survival as

derived from the difference between a firm’s size and the industry MES. PLC theory suggests

that larger firms are more likely to survive in mature industries. In young industries where

innovation opportunities are high, small firms are equally likely to survive. So for young

Internet firms, we hypothesize no relationship between firm size and firm survival.

□ HYPOTHESIS 2 (THE FIRM SIZE HYPOTHESIS): There is no relationship between an Internet firm’s size (in terms of the number of employees) and its likelihood of survival.

Although the results on the impact of firm size vary, the availability of financial capital

seems to enhance the survivability of firms in most of the research that we reviewed. As a result,

we hypothesize a positive relationship between financial capital and Internet firm survivalability.

□ HYPOTHESIS 3 (THE FINANCIAL CAPITAL HYPOTHESIS): Internet firms with more financial capital are more likely to survive.

9

A firm’s leverage (the ratio of total debt to total assets) is an indicator of its financial

solvency. First, it predicts bankruptcy in prior research. For Internet firms, excessive debt is an

indicator of greater risk for future performance since highly levered firms are riskier. High debt

ratio may block loan funding, which may hinder the firm’s growth. Second, Internet firms are

still in early development. Many are struggling to become profitable. So they tend to

accumulate debt. If a firm cannot reach profitability before it reaches an alarmingly high debt

ratio level, it may seek bankruptcy protection. Third, the amount of cash-on-hand and “burn rate”

have been frequently referred to as the reasons many Internet firms failed. Barron’s magazine

predicted that many Internet firms would fail because their cash was running out (Willoughby

2000). A higher debt ratio can makes it more difficult for a firm to raise additional funds, so we

expect it to affect survivability.

� HYPOTHESIS 4 (THE LEVERED FIRM HYPOTHESIS): Internet firms that are more highly levered (with a higher ratio of total liabilities to total assets) are more likely to fail.

Advances in IT give firms new ways to provide physical and digital goods and services.

Internet firms sell digital goods with negligible marginal production and lower delivery costs

compared to physical Internet firms. The cost savings will enhance their profits, which will

influence their survival rate. Digital product Internet firms more often compete in break-through

rather than re-formed markets. The value they provide to customers and the lack of competition

from traditional firms will enhance their viability. Physical firms more often compete in re-

formed markets with traditional firms. We expect them to be less likely to survive.

□ HYPOTHESIS 5 (THE DIGITAL PRODUCTS HYPOTHESIS): Internet firms that sell digital goods are more likely to survive than Internet firms that sell physical goods.

Though Subramani and Walden (2001, 2002) identified differences between stock price

returns for e-commerce initiative announcements, their results are sensitive to market

perceptions. We collected data between 1996 and early 2003—a longer period that expands

10

beyond the 1998 to 2000 period in prior studies, and includes observations from before and after

the DotCom crash in mid-2000. Expanding the timeline of our data allows us to minimize (to the

extent that is possible) the impact of the market turbulence on our results. In addition to B2C

and B2B firms, we use “B2B&C firms,” that serve both consumer and business customers. We

do not hypothesize a specific direction for the differences in survivability for different firm

types. Our analysis may reveal which type of firm is better positioned to compete.

� HYPOTHESIS 6 (THE TARGET MARKET HYPOTHESIS): Internet firms targeting different markets, including B2C, B2B and B2B&C, have the same likelihood of survival.

The hypotheses we develop allow us to build a survival theory for IT and Internet firm

performance. We next provide details on our empirical tests of these hypotheses.

ECONOMETRIC METHODS

Our empirical analysis involves two steps. We first develop a baseline model for

distinguishing between healthy and failing Internet firms. We then model Internet firm survival

in “IPO time,” to support age- and calendar time-based analyses. Our methods are intended to

triangulate to support a rich and in-depth understanding of Internet firm survival.

The Logit Model

The logit model, one in a family of discrete choice models, is widely used in economics,

social sciences and epidemiology to handle dependent variables that are not continuous.

Model Setup and Parameter Estimation. The vector of variables, x, will determine the

probability of a specific choice, through its estimated parameters, β, such that Prob(y=1) =

F(β’x). For a binary dependent variable, the probability of the other choice then becomes

Prob(y=0) = 1-F(β’x). Note here that F(β’x) is a cumulative density function. In logit models,

11

F(β’x)’s corresponding density function, f(β’x), takes the form of a logistic distribution, which

results in )(1

)1( '

'

xβ'Λ=+

==x

x

eeyobPr

β

β

, a logistic cumulative distribution function.1

With choices of y = (y1, y2, …, yn) for n observations in the sample, the joint probability is:

ii yn

i

yn )](F[)](F[))y,...,y,y((obPr −

=

−== ∏ 1

121 1 i

'i

' xβxβy . (1)

Taking the logarithm, the coefficients can be estimated with maximum likelihood methods.

For goodness-of-fit, we calculate the model χ2, -2 times the difference between model log

likelihood with only an intercept and a model with an intercept and independent variables

(Powers and Xie 2000). Larger values of χ2 indicate greater predictive power for the variables.

Interpreting Coefficients. Logit marginal effects are βxβxβx

x '' )](1)[(]|[ Λ−Λ=∂

∂ yE ,

calculated at the means of the independent variables. The odds ratio is often used to interpret

logit model coefficients. The odds of an outcome is the ratio of the probability that the outcome

will occur over the probability that it will not. For binary dependent variables, the odds of y = 1

is )1(1

)1()0()1(

===

==

yobPr-yobPr

yobPryobPr . The odds ratio is the impact of a variable on the odds of an

outcome. A coefficient estimate of βi for the ith independent variable makes odds ratio exp(βi).

If the model gives a coefficient estimate of -0.5 for Product (coded 1 for digital product Internet

firms, 0 for physical ones), then the odds ratio is exp(-0.5) = 0.61. This suggests the probability

ratio of bankruptcy versus survival for digital product Internet firms (i.e., Product=1) is 0.61 of

the corresponding probability ratio for physical ones (i.e., Product=0). Thus the likelihood of 1 For probit models, f(β’x) is the standard normal distribution. The logistic and normal distributions are similar, except that the logistic distribution has heavier tails. Logit and probit tend to give similar predictions if values in the β’x matrix are in the intermediate range. If the values of the β’x matrix are very small (or large), logit will give higher (or lower) probabilities for y = 0 as compared to probit (Greene 2002). Logit permits interpreting the coefficient estimates using the odds ratios, in addition to the marginal effects (Agresti 2002). We use logit as the primary model to predict Internet firm bankruptcy and liquidation, but also obtained similar results using probit.

12

observing bankruptcy should be smaller for digital product Internet firms than physical ones.

Duration Modeling and Survival Analysis

Survival analysis is widely used in public health to study the effectiveness of medical

treatments on patients and in criminology to examine patterns in criminal recidivism. The

occurrence of an event is a failure process that starts from a certain point in time, such as birth or

the start of a treatment. Four concepts are essential. Duration is the time that has elapsed since

the start of observation until the occurrence of the event of interest or the end of the study period,

if the event does not occur and the subject is still at risk. Such an observation is said to be right-

censored. Given an individual is at risk right before time t, the hazard rate is the instantaneous

failure rate at time t. The survival function is the probability that the firm’s duration will exceed

t. It also reflects the proportion of individuals in the population that will have a survival time

longer than t (Le 1997). Survival analysis is based on a stochastic failure process, so

observations are usually compared based on individual durations, rather than calendar time.

Age-based firm comparisons eliminate a learning effect associated with firm age. We use

nonparametric and semiparametric survival analysis to compare firms with the same number of

quarters that elapsed since their IPOs. We use the Kaplan-Meier (KM) estimator, a

nonparametric survival analysis technique, to construct survival functions for sample firms.

Then, we use the Cox (1975) proportional hazards model to test the impact of explanatory

variables on Internet firm survival. We also use a calendar time-based semiparametric survival

analysis, so we can control for the impact of market conditions. The strength of this multi-

method approach is that it allows us to visually construct curves that depict the survival patterns

for Internet firms and then examine what drives observed Internet firm bankruptcy and survival.

The KM Estimator. This nonparametric statistic calculates a survival function for sample

13

data (Le 1997), using ∏≤

−=

t)q(t )q(t

)q(t)q(tt n

dnS , where t(q) is the time (number of quarters after IPO

occurred) when a bankruptcy or a liquidation event was observed, and nt(q) is the number of firms

that are still in operation up until time t(q) and, hence, are still at risk at time t(q). dt(q) is the

number of firms that filed for bankruptcy or were liquidated at time t(q). The survival rates at

different times can be plotted against firm duration, resulting in Kaplan-Meier curves.

The Cox Proportional Hazards Model. For a firm at time t, its hazard function has a

nonparametric baseline hazard h0 (t) (similar to a regression constant) that depends only on time

t, and a parametric part that reflects the impact of independent variables on the hazard rate,

)exp()(),( 0 xββx, 'thth = . h0 (t) is the baseline hazard. It is the same for all firms at the same

age t. The independent variables x differ across firms over time. They include industry, firm

and e-commerce-related factors. β is the vector of parameters we will estimate.

We can obtain the cumulative baseline hazard function (Le 1997) as H0(t)= ∫t

dyyh0 0 )( . The

partial likelihood function is

ic

I

i))i(t(Rj

)exp()exp(

)(PL ∏∑=

∈

=1 t(i)j,

't(i)i,

'

xβxβ

β , where I is the sample size (with

each firm denoted by i) and t(i) is firm i’s duration (Hosmer and Lemeshow 1999). With t(i) we

select those periods of time when a firm is observed to fail. R(t(i)) is the set of firms at risk of

failing at t(i), when firm i fails. It includes all firms with durations that are the same or longer

than the duration of firm i.2 xi,t(i) is the vector of independent variables for firm i at the time it

fails, and xj,t(i) is the vector of the time-varying covariates for firm j that are at risk of failure. ci is

0 if observation i is censored, and 1 otherwise. The baseline hazard gets canceled out. An

2 We distinguish between t(i) used in the PL function and t(q) used in the KM estimator. t(i) denotes firm i’s duration. t(q) refers to points in time before t and when Internet firm bankruptcies or liquidations were observed.

14

intercept is unnecessary because variations in the hazard rate that are the same for all firms at the

same age are absorbed into the baseline hazard.3

SAMPLE AND MODELS

We next discuss data collection and specify the estimation forms of the empirical models.

Data Collection and Sample

Our definition of an Internet firm is like Barua et al.’s (2000): a “DotCom” generates all of

its revenues though the Internet. Barua et al. (2001) reduced the cutoff point to 95%,

recognizing that Internet firms also receive revenues though traditional channels such as phone

or fax. We use 90% as the cutoff and include well known firms that most will think are Internet

firms. We only admit Barua et al.’s (1999) Layers 3 and 4 firms to our sample. Layer 3 firms are

electronic intermediaries that provide online marketplaces to facilitate buyers and sellers to meet

and conduct transactions. Layer 4 firms are e-commerce firms that engage in online selling of

products or services. Our data consists of publicly-traded Internet firms; financial data for

private firms were unavailable. We eliminated firms that went public as traditional firms but

later became Internet firms. Their success will be explained differently than for firms founded as

Internet firms. Our data come from multiple data sources such as COMPUSTAT, Mergent

Online, corporate filings with the Securities and Exchange Commission (SEC) and the EDGAR

Online IPO Express database. We retained firms that generated more than 90% of their revenues

on the Internet. We eliminated firms with revenues allocated between the channels, when

information on relative portions was missing. Our sample consists of 115 publicly-traded

Internet firms. Descriptive statistics and a decomposition based on target market and outcome

3 The PL function assumes no tied duration data, i.e., no two firms filed for bankruptcy or were liquidated at the same duration after IPO. Depending on the number of ties, an adjustment to the PL function is necessary to account for the conjoint probability of observing two or more events at the same time. Our results reflect this adjustment.

15

status are shown in Tables 1 and 2. Due to missing data in the last quarter of data available, two

firms were cut. The estimation sample is 113 firms for logit and 115 firms for the Cox model. 4

Table 1. Descriptive Statistics

FIRM TYPE

NUMBER OF OBS.

DURATION (QUARTERS)

QUARTERLY REVENUES

($MM)

FIRM SIZE (# EMPLOYEES)

Mean Std. Dev. Mean Std. Dev. Mean Std. Dev. B2C 70 11.17 4.89 50.52 128.60 550 1214 B2B 13 11.77 5.31 29.63 67.36 259 217 B2B&C 32 11.94 4.82 22.78 32.03 376 523 TOTAL 115 11.45 4.89 40.00 103.79 464 981

Table 2. Sample Decomposition Based on Target Market and Status

STATUS TOTAL BANKRUPTCY/LIQUIDATION SURVIVAL TARGET

MARKET Count Frequency (%) Count Frequency (%) Count Frequency (%)

B2C 10 8.70 60 52.17 70 60.87 B2B 1 0.87 12 10.43 13 11.30 B2B&C 4 3.48 28 24.35 32 27.83 TOTAL 15 13.04 100 86.96 115 100.00

Variables

Dependent Variables. The binary dependent variable in our logit model is 1 if the Internet

firm went bankrupt or was liquidated during our sample period, and 0 otherwise. There are two

dependent variables in the Cox model. Duration is the number of quarters that has elapsed from

the time an Internet firm went IPO till the time of its bankruptcy filing or liquidation, or the end

of the study period if the firm is still alive. The binary indicator, Status, is 1 if the firm went

bankrupt or was liquidated, and 0 otherwise. Table 3 summarizes the definitions of our model.

4 These two companies are included in the Cox regression because this econometric analysis technique uses data on firm lifetime, not just the last quarter.

16

Table 3. Definitions of Model Variables

VARIABLE DEFINITION

Dependent Variable—Logit Model � Status 1 if bankrupt or liquidated, 0 otherwise

Dependent Variables—Cox Proportional Hazards Model

� Duration Number of quarters from the IPO date to time of bankruptcy, liquidation, or the end of the study period, whichever occurs sooner

� Status 1 if bankrupt or liquidated, 0 otherwise

Independent Variables—Industry-Related � IPOEntry Number of Internet firm IPOs in the quarter Independent Variables—Firm-Related � FirmSize Natural logarithm of the number of employees � FinCapital Amount of financial capital the firm possesses (in million of dollars) � DebtRatio Total liabilities as a percentage of total assets (in percent) Independent Variables—E-Commerce-Related � Product 1 if firm sells digital goods or services, 0 if physical goods or services � B2C 1 if the firm is a B2C firm, 0 otherwise � B2B 1 if the firm is a B2B firm, 0 otherwise Independent Variables—Control � InterestRate Six-month U.S. treasury bill interest rate (in percent)

Independent Variables. The independent variables we employ are the same across the logit

and Cox proportional hazards models. Based on our review of the literature, we have industry,

firm and e-commerce-related factors as our explanatory variables. The industry-related variable

is Rate of New Firm Entry and is operationalized as the number of Internet firm IPOs in each

quarter. Firm-related factors include Firm Size, Financial Capital and Debt Ratio. We

operationalize Firm Size as the natural logarithm of the number of employees of the firm.

Financial Capital is the difference between a firm’s assets and liabilities, measured in millions

of dollars. As is common in studies of financial condition, to control for inflation we adjusted

financial capital using the Producer Price Index to 1982 dollars. Debt Ratio measures a firm’s

total liabilities as a percentage of its total assets and is an indicator of a firm’s financial solvency.

The e-commerce-related variables are Product and Target Market. Product is a dummy

17

variable that takes the value of 1 for firms selling digital products or services (e.g., financial

service and portal sites) and 0 for firms selling physical goods such as books, CDs and DVDs.

We have three types of Internet firms in our sample: B2C, B2B, and B2B&C firms. They are

coded with two dummy variables for Target Market: B2C and B2B. The variable B2C is 1 for

B2C firms and 0 otherwise, and the variable B2B is 1 for B2B firms and 0 otherwise. For

B2B&C firms, the values for the above two dummy variables are both zero as our base case.

Control Variable. Following Audretsch and Mahmood (1995), we include Interest Rate as

a control variable in our models for the influence of the macroeconomy. It is operationalized as

the six-month U.S. Treasury Bill interest rate. We tested to see whether it would be appropriate

to include the unemployment rate in our model, but decided not to do it because it had a -.78

correlation with Interest Rate, which would tend to destabilize our coefficient estimates.

Econometric Issues. In our sample, Firm Size is only reported annually, so it will be the

same for the four quarters in the same year. We lag our explanatory variables by one quarter to

predict the survival outcome of the firm in the next quarter. Because many firms did not report

operational results for the quarter immediately before their bankruptcy, we use two-quarter-

lagged data for financial capital and debt ratio. We report the descriptive statistics of our

independent and control variables in Table 4. No two variables have a correlation higher than

.60. Tables 5 and 6 display appropriately-lagged correlation matrices for the independent and

control variables. The Belsley Kuh Welsch condition indices (Greene 2002) are both less than

20 for the variables, which eliminates multicollinearity as a problem.

In our empirical models, the Product variable represents a choice that most Internet firms in

our sample made when they were established. A colleague who commented on this research

suggested that there may be an endogeneity issue: firms with smarter management teams may

18

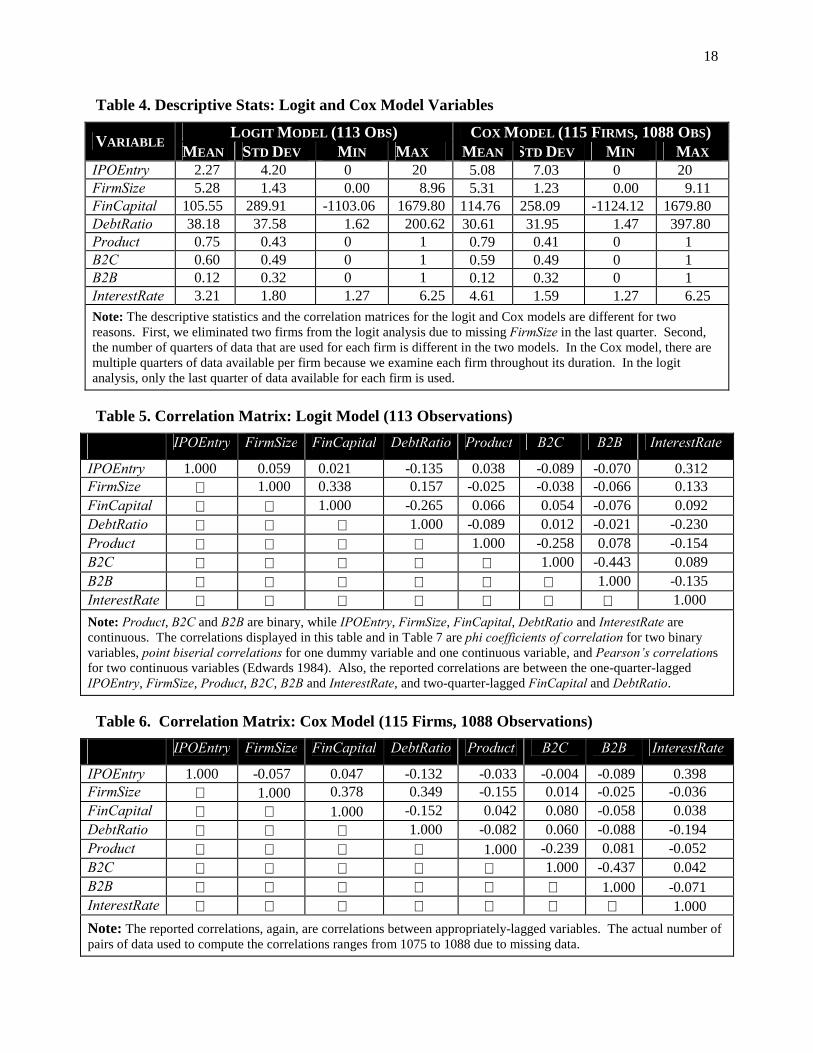

Table 4. Descriptive Stats: Logit and Cox Model Variables

LOGIT MODEL (113 OBS) COX MODEL (115 FIRMS, 1088 OBS) VARIABLE MEAN STD DEV MIN MAX MEAN STD DEV MIN MAX IPOEntry 2.27 4.20 0 20 5.08 7.03 0 20 FirmSize 5.28 1.43 0.00 8.96 5.31 1.23 0.00 9.11 FinCapital 105.55 289.91 -1103.06 1679.80 114.76 258.09 -1124.12 1679.80 DebtRatio 38.18 37.58 1.62 200.62 30.61 31.95 1.47 397.80 Product 0.75 0.43 0 1 0.79 0.41 0 1 B2C 0.60 0.49 0 1 0.59 0.49 0 1 B2B 0.12 0.32 0 1 0.12 0.32 0 1 InterestRate 3.21 1.80 1.27 6.25 4.61 1.59 1.27 6.25 Note: The descriptive statistics and the correlation matrices for the logit and Cox models are different for two reasons. First, we eliminated two firms from the logit analysis due to missing FirmSize in the last quarter. Second, the number of quarters of data that are used for each firm is different in the two models. In the Cox model, there are multiple quarters of data available per firm because we examine each firm throughout its duration. In the logit analysis, only the last quarter of data available for each firm is used.

Table 5. Correlation Matrix: Logit Model (113 Observations) IPOEntry FirmSize FinCapital DebtRatio Product B2C B2B InterestRate

IPOEntry 1.000 0.059 0.021 -0.135 0.038 -0.089 -0.070 0.312 FirmSize 1.000 0.338 0.157 -0.025 -0.038 -0.066 0.133 FinCapital 1.000 -0.265 0.066 0.054 -0.076 0.092 DebtRatio 1.000 -0.089 0.012 -0.021 -0.230 Product 1.000 -0.258 0.078 -0.154 B2C 1.000 -0.443 0.089 B2B 1.000 -0.135 InterestRate 1.000 Note: Product, B2C and B2B are binary, while IPOEntry, FirmSize, FinCapital, DebtRatio and InterestRate are continuous. The correlations displayed in this table and in Table 7 are phi coefficients of correlation for two binary variables, point biserial correlations for one dummy variable and one continuous variable, and Pearson’s correlations for two continuous variables (Edwards 1984). Also, the reported correlations are between the one-quarter-lagged IPOEntry, FirmSize, Product, B2C, B2B and InterestRate, and two-quarter-lagged FinCapital and DebtRatio.

Table 6. Correlation Matrix: Cox Model (115 Firms, 1088 Observations) IPOEntry FirmSize FinCapital DebtRatio Product B2C B2B InterestRate

IPOEntry 1.000 -0.057 0.047 -0.132 -0.033 -0.004 -0.089 0.398 FirmSize 1.000 0.378 0.349 -0.155 0.014 -0.025 -0.036 FinCapital 1.000 -0.152 0.042 0.080 -0.058 0.038 DebtRatio 1.000 -0.082 0.060 -0.088 -0.194 Product 1.000 -0.239 0.081 -0.052 B2C 1.000 -0.437 0.042 B2B 1.000 -0.071 InterestRate 1.000 Note: The reported correlations, again, are correlations between appropriately-lagged variables. The actual number of pairs of data used to compute the correlations ranges from 1075 to 1088 due to missing data.

19

have chosen to provide digital products and services, and firms that made this decision are more

likely to survive because of their better management. Though there is this possibility of

endogeneity, we believe it is not a major concern in our analysis for two reasons. First, firms

typically choose their primary product and service offerings and the industry they want to

compete in prior to deciding to launch a stock IPO. Our sample of Internet firm observations

began with their IPOs, a time by which the firms’ product and industry choices should have been

established already. Since these are pre-established, they are also exogenous (Judge et al. 1980).

Second, the market hype for physical Internet firms in late 1990s was equally high as reflected

by the press coverage and the amount of funding many Internet firms received. Examples

include Amazon.com, Webvan.com, and grouping buying sites such as Mercata.com and

Mobshop.com. Though many of these firms failed later, they were perceived as implementing

equally innovative and promising business models on the Internet at the time of their founding

and IPOs. This suggests that the market had no clear picture about the potential of these firms.

Estimation Forms of the Empirical Models

Based on the above definitions of our model variables and after applying appropriate lags for

the independent and control variables, the econometric models that we will test are as follows:

Logit: x

x

te

eyProb '

'

1)1(

β

β

+== (2)

where 242312110 −−−− ++++= tttt DebtRatioFinCapitalFirmSizeIPOEntry βββββxβ '

18171615 22 −−−− ++++ tttt teInterestRaBBCBoductPr ββββ (3)

Cox Proportional Hazard: 2312110 exp[)()( −−− ++= ttt FinCapitalFirmSizeIPOEntrythth βββ

]teInterestRaBBCBoductPrDebtRatio ttttt 1817161524 22 −−−−− +++++ βββββ (4)

20

We use one quarter of data per firm to predict survival in the logit model. We use two-

quarter-lagged financial capital and debt ratio and one-quarter-lagged data for the other

variables. In the Cox proportional hazards model, we also analyze the process through which the

independent variables vary across firms over time and how that affects survivability.

RESULTS

We first report the base case logit results. Then we discuss the survival analysis results.

Logit Model Results

The results of the logit model estimation are presented in Table 7.

Table 7. Logit Model Results (113 Observations)

PARAMETER ESTIMATES

STD. DEVS.

χχχχ2 ODDS RATIO

MARGINAL EFFECT

HYPOTHESIS TEST

Constant (β0) -2.875 1.863 2.382 IPOEntryt-1 (β1) -0.539 0.270 3.993** 0.583 -0.013 H1(N) FirmSizet-1 (β2) -0.479 0.257 3.462* 0.620 -0.011 H2(N) FinCapitalt-2 (β3) 0.001 0.001 1.179 1.001 0.00004 H3(N) DebtRatio t-2 (β4) 0.037 0.011 10.934*** 1.037 0.001 H4(Y) Productt-1 (β5) -1.538 0.856 3.228* 0.215 -0.056 H5(Y) B2Ct-1 (β6) -0.509 0.895 0.323 0.601 -0.013 B2Bt-1 (β7) -1.129 1.543 0.536 0.323 -0.018

H6(Y)

InterestRatet-1 (β8) 0.923 0.268 11.850*** 2.518 0.022 Note: Model χ2=35.17, 8 d.f., p=0.0001. Full data set of 113 Internet firms. Time period for analysis is from July 2000 to March 2003. Significance levels: * = p < 0.10; ** = p < 0.05; *** = p < 0.01. B2C and B2B code for different Internet firm target markets as binary variables, with B2B&C as the base case. Hypothesis: Y=supported, N=not supported.

Overall, the model exhibits reasonable goodness-of-fit (model χ2 = 35.17, 8 d.f., p < .01).

The significant variables are IPOEntry, FirmSize, DebtRatio, Product and InterestRate. The

estimated parameter for IPOEntry is negative and significant with a smaller than one odds ratio

and a negative marginal effect on bankruptcy (β1= -0.539, p < .05, odds ratio=0.583, marginal

effect = -0.013). The odds ratio estimate of 0.583 suggests as the number of Internet firm IPOs

increased by one, the odds of bankruptcy or liquidation (i.e., the probability ratio of bankruptcy

or liquidation versus survival) decreased by 41.7%. When calculated at the means of the

21

independent and control variables in our sample, one more Internet firm IPO reduced the

incumbent public Internet firm’s probability of bankruptcy or liquidation by 1.3%. The New

Firm Entry Rate Hypothesis (H1) is not supported. FirmSize has a negative and significant

parameter estimate with a smaller than one odds ratio and a negative marginal effect (β2 =

-0.479, p < .10, odds ratio = 0.620, marginal effect = -0.011). The Firm Size Hypothesis (H2) is

not supported. An increase of one in the natural logarithm of a public Internet firm’s number of

employees, the odds of bankruptcy or liquidation decreases to 62.0% of its original value. In

addition, the marginal effect, calculated at the means of the independent and control variables,

indicates the probability of bankruptcy or liquidation decreased by 1.1% as the natural logarithm

of a firm’s number of employees increases by one. These results indicate, for the public Internet

firms in our sample, their likelihood of bankruptcy or liquidation decreased as their firm sizes

increased. The estimated parameter for DebtRatio is positive and significant with a larger than

one odds ratio and a positive marginal effect on bankruptcy (β4= 0.037, p < .01, odds

ratio=1.037, marginal effect = 0.001). So our Levered Firm Hypothesis (H4) is supported. The

odds ratio of 1.037 indicates when a firm’s total liabilities as a percentage of its total assets

increased by 1%, the odds of bankruptcy or liquidation increased by 3.7%. As a result, an

Internet firm was more likely to fail when it carried a higher percentage of debt compared to its

total assets. The marginal effect is small. With each 1% increase in leverage during the sample

period of this study, the probability of failure for a public Internet firm increased by just .1%.

The parameter for Product also is negative and significant, with a smaller than one odds ratio

and a negative marginal effect on the likelihood of firm failure (β5 = -1.538, p < .10, odds

ratio=0.215, marginal effect = -0.056). Thus, the Digital Products Hypothesis (H5) is supported.

This result indicates that an Internet firm that sold digital goods had an odds of bankruptcy or

22

liquidation that was 21.5% of that of a physical product Internet firm. In addition, it had a 5.6%

lower probability of failing during the study period than that for the latter. The effect of

InterestRate during this period was positive and significant with a larger than one odds ratio and

a negative marginal effect on failure (β8 = 0.923, p < .01, odds ratio = 2.518, marginal effect =

0.022). This indicates an Internet firm’s odds of failure increased by 151.8% and its failure

probability increased by 2.2% with each 1% increase in the interest rate in our sample.

FinCapital and the intercept are not significant, and the Internet firm target market types, B2C

and B2B, show no significant differences from the base case of B2B&C firms. The null Target

Market Hypothesis (H6) is supported, while the Financial Capital Hypothesis (H3) is not.

Concordant-Discordant Pairs. An indicator of the predictive accuracy of a logit model is

the balance of concordant and discordant pairs (Agresti 2002). Concordant pairs are firms with

predicted outcomes of bankruptcy or liquidation, for which either bankruptcy or liquidation is

actually observed, or the predicted outcome of survival is confirmed by the observed outcome of

a firm that is still in business. Otherwise, we get a discordant pair. The predicted outcome of

bankruptcy or survival is the result of a comparison of the predicted probability of bankruptcy to

a probability threshold p, which ranges from 0 to 1. If the predicted probability of bankruptcy is

greater than p, the observation has a predicted outcome of bankruptcy. Otherwise, it has a

predicted outcome of survival. Table 8 summarizes the predictive validity of our logit model

based on different threshold probability values. Sensitivity is the conditional probability that a

firm has a predicted outcome of bankruptcy given that bankruptcy or liquidation is observed.

Specificity is the conditional probability that the predicted outcome is survival when it occurs.

23

Table 8. Classification Table for the Logit Model

CONCORDANT DISCORDANT PROB LEVEL Bankruptcy Survival Bankruptcy Survival

CORRECT(%)

SENSITIVITY (%)

SPECIFICITY(%)

0.0 15 0 98 0 13.3 100.0 0.0 0.1 10 77 21 5 77.0 66.7 78.6 0.2 9 80 18 6 78.8 60.0 81.6 0.3 9 84 14 6 82.3 60.0 85.7 0.4 7 85 13 8 81.4 46.7 86.7 0.5 4 89 9 11 82.3 26.7 90.8 0.6 2 93 5 13 84.1 13.3 94.9 0.7 1 93 5 14 83.2 6.7 94.9 0.8 0 96 2 15 85.0 0.0 98.0 0.9 0 97 1 15 85.8 0.0 99.0 1.0 0 98 0 15 86.7 0.0 100.0

Note: 98 firms survived; 15 failed. With an unbalanced sample, logit predicts survival better than failure. This is typical with an unbalanced sample (Cramer 1999). The appropriate method is for the analyst to select a probability cutoff point based on the tradeoff between the predictive accuracies of the two outcomes.

Receiver Operating Characteristic Curve. We can plot sensitivity against one minus

specificity for different probability thresholds, resulting in a receiver operating characteristic

(ROC) curve (Agresti 2002). Sensitivity represents the true positive rate of the logit model; one

minus specificity measures the false positive rate. An ROC curve summarizes the predictive

power of a logit model for all possible probability cutoff points. The larger the area under the

ROC curve, the better the predictive power. We plot the ROC curve for our logit model in

Figure 1. The area under the ROC curve has the same value as the concordance index, and

usually ranges between .5 (random guessing) and 1 (perfect predictive power). Our model has a

concordance index of .917, indicating reasonably good fit with the data.

24

Figure 1. The Receiver Operating Characteristic Curve Analysis for the Logit Model

Results from the KM Curve Analysis

Our nonparametric survival analysis involves plotting the KM curve for all 115 Internet firms

in our sample and the decomposed KM curves for different types of Internet firms. See Figures

2 and 3. Circles on the curves show censored observations. (Remember: firm duration begins

when its stock IPO, i.e., the start of the stochastic failure process.)

Figure 2. The KM Curve for All Publicly-Traded Internet Firms (115 Firms)

The KM curve for all 115 firms in Figure 2 is an aggregate presentation. It reveals that the

majority of the failures for Internet firms have occurred between Quarters 6 and 18 in their

25

lifetimes. The period between Year 1 to Year 5 after an Internet firm has gone public is critical

to its longer-term survival. After that, however, the plateau in the KM curve suggests that no

bankruptcy or liquidation outcomes have occurred after Quarter 18. In addition, we observe that

the failures during Years 1 to 4 were gradual: the firms do not appear to have failed all at the

same age since they went public. However, the two big steps in between Quarters 16 and 18

indicate a sharp decrease in survival rate of Internet firms during Year 5. Although this is not a

perfect match for failures in calendar time terms (e.g., late 2000 and 2001), nevertheless, it is

reasonable to recognize that by the time five years had gone by, many of these firms were feeling

the effects of the downturn in interest in the digital economy.

Figure 3. KM Curves for Internet Firms Targeting Different Markets (115 Firms)

Decomposition of the aggregate KM curve as shown in Figure 3 for Internet firms with

different markets suggests that the survival functions for publicly-held B2C, B2B and B2B&C

firms may be different. For example, starting from their IPOs, the KM curves for B2C and

B2B&C firms are similar before their sixth quarter of existence. At Quarter 6, when the

bankruptcies and liquidations start to emerge, the two KM curves start to diverge. B2C firms

26

experienced problems after their sixth quarter which lasted until the eleventh quarter, after which

no B2C firms failed in our sample due to bankruptcy or liquidation. The failure of B2B&C firms

was gradual in the beginning. From Quarters 16 to 18, B2B&C firms experienced a sharp drop

in survival rate: 30% failed 16 to 18 quarters after their IPOs. After that time though, the

B2B&C firms experienced no more bankruptcies or liquidations. For B2B firms, the failure

occurred early at the end of Year 1. After that, no B2B firm bankruptcies or liquidations were

observed in our sample of Internet firms.

We next report results from the Cox regression, which enables us to quantify the impact of

the various factors as well as target market over a longer period of time.

Results from the Cox Proportional Hazards Model

We present our age-based Cox proportional hazard model results in Table 9. (See Table 9.)

Here we distinguish between the hazard ratio, a statistic that is similar to the marginal effects on

failure in the logit model, and the hazard rate, the instantaneous failure rate at time t assuming a

firm is still at risk up until that time. The hazard ratio depicts the marginal impact of a one-unit

increase of an explanatory variable on the hazard rate. The hazard ratio is written as exp(βi),

where βi is the estimated coefficient for an explanatory variable xi. Overall, our model has a

likelihood ratio statistic of 28.55 and is significant at the .01 level.

The significant variables are IPOEntry, FirmSize, DebtRatio and Product. The estimated

parameter for IPOEntry is negative and significant with a hazard ratio of less than one (β1 =

-0.362, p < .10, hazard ratio= 0.696). The hazard ratio of 0.696 suggests with each additional

new Internet firm IPO, the hazard rate of an existing public Internet firm due to bankruptcy or

liquidation reduced to 69.6% of its original value. The New Firm Entry Rate Hypothesis (H1) is

not supported. FirmSize has a negative and significant parameter estimate with a smaller than

27

one hazard ratio (β2 = -0.425, p < .05, hazard ratio= 0.654). The null Firm Size Hypothesis (H2)

is not supported. The hazard ratio statistic suggests as FirmSize, measured as the natural

logarithm of the number of employees, increased by one, a public Internet firm’s hazard rate

decreased to 65.4% of its original value. The estimated parameter for DebtRatio is positive and

significant with a larger than one hazard ratio (β4 = 0.032, p < .01, hazard ratio= 1.032). The

Levered Firm Hypothesis (H4) is supported. These results indicate that when a firm’s total debt

as a percentage of its total assets increases by 1%, its hazard rate increases by 3.2%. This is

consistent with the results from the logit model, where we found that the debt ratio could help us

distinguish healthy Internet firms from those close to bankruptcy. For an Internet firm that is

still in its early stages of development, maintaining a manageable debt level is crucial to the

financial solvency and hence, the survivability of a firm.

Table 9. Cox Model Results (115 Firms with 15 Bankruptcies/Liquidations)

VARIABLE PARAMETER ESTIMATE

STANDARD DEVIATION

χχχχ2 HAZARD RATIO

HYPOTHESIS TEST

IPOEntryt-1 (β1) -0.362 0.217 2.801* 0.696 H1(N) FirmSizet-1 (β2) -0.425 0.219 3.770** 0.654 H2(N) FinCapitalt-2 (β3) 0.002 0.001 2.096 1.002 H3(N) DebtRatio t-2 (β4) 0.032 0.008 14.292*** 1.032 H4(Y) Productt-1 (β5) -1.503 0.595 6.379** 0.223 H5(Y) B2Ct-1 (β6) -0.364 0.687 0.281 0.695 B2Bt-1 (β7) -0.285 1.178 0.059 0.752

H6(Y)

InterestRatet-1 (β8) 0.300 0.221 1.838 1.350 Note: Estimation without an intercept constant, so β0 omitted. Likelihood ratio statistic for model significance: 28.55, p = 0.0004; significance levels for explanatory variables: * = p < 0.10; ** = p < 0.05; *** = p < 0.01. Full data set of 115 firms. Time period covered is second quarter 1996 to first quarter of 2003. The binary variables B2C and B2B code for the target market types of Internet firms, with B2B&C as the base case. Hypothesis: Y=supported, N=not supported.

The parameter estimate for Product is negative and significant with a hazard ratio smaller

than one (β5 = -1.503, p < .05, hazard ratio= 0.223). The hazard ratio statistic indicates that the

hazard rate for Internet firms selling digital goods or services was 22.3% of those that sold

28

physical products. The Digital Products Hypothesis (H5) is supported. This corroborates the

result found in Barua et al. (2000). Apparently, Internet firms selling digital products or services

experience considerably lower hazard rate due to the close to zero marginal production cost and

much lower delivery costs associated with the use of the Internet.

Even though B2C and B2B firms in our sample have lower hazard rates compared to the base

case of B2B&C firms, neither indicator is significant. The Target Market Hypothesis (H6) is

supported. This result indicates when the confounding effects of the other variables are

eliminated, the target market itself does not affect survivability. While short-term stock returns

might reflect market perceptions about the valuations of different types of Internet firms

(Subramani and Walden 2001, 2002), the market an Internet firm serves does not appear to have

been a determinant of survivability in the long run. FinCapital and InterestRate are not

significant either. Thus, we have no evidence to suggest that the Financial Capital Hypothesis

(H3) is supported. This result suggests that differences among the firms in terms of amount of

financial capital they possess are not large enough to give any Internet firm a survival advantage.

Because of the dramatic change in market conditions during our sample period, it is possible

that InterestRate and IPOEntry are not able to completely capture the impact of the

macroeconomy. To further explore this issue, we also performed a calendar time-based

semiparametric survival analysis where we compare the hazard rates of the Internet firms during

the same calendar quarter. It allows us to tease out the impacts of the macroeconomic

environment and investor psychology during different periods, and permits us to focus on the

firm and e-commerce related drivers of survival. We eliminate IPOEntry and InterestRate since

there was no variation in these two variables among firms in the same calendar quarter. We

obtained similar results to the age-based survival analysis in terms of both the parameter

29

estimates and their significance levels, where FirmSize, DebtRatio and Product are found to be

significant. These results provide stronger support for our age-based analysis where we find the

existence of firm size, debt ratio and product effects of Internet firm survival.

DISCUSSION

Our empirical analysis on the performance of IT-focused firms and the drivers of Internet

firm survival has the following four major findings. The KM curves for all the firms in our

sample and the decomposed KM curves for different target markets give a visual representation

of the survival pattern. The plateaus in the curves show that after surviving the initial

competition, an Internet firm faced a reduced risk of failure. This selection process started one

year after IPO and continued for four years. For B2B and B2C firms, bankruptcies and

liquidations occurred early on, between Years 1 and 3 after IPO. But failure occurred later for

B2B&C firms: about one third failed during Year 5 after their IPOs. Also, B2B firms had the

highest survival rate at the end, while B2B&C firms had the lowest. This reveals the importance

of strategic planning during the first five post-IPO years. Today, managers at Internet firms

should establish a core and profitable business offering before undertaking risky expansion.

Second, the results from our logit and age- and calendar time-based Cox proportional hazards

models are consistent and suggest factors such as Internet firm IPOs in the stock market, the

types of products or services an Internet firm provides, its size and leverage ratio are factors that

can affect its survival. Additional Internet firm IPOs can reduce an incumbent public Internet

firm’s likelihood of bankruptcy or liquidation. This is a counter-intuitive result since additional

IPOs present existing public Internet firms with competition for market capital. A possible

interpretation is that during our sample period, abundant financial capital in the stock market

induced more Internet firms to go public. The beneficial effect of a prosperous stock market

30

outweighed the negative impact of fiercer competition due to higher rates of new firm entry,

which resulted in a higher likelihood of survival. For our sample of 115 Internet firms, most of

them released IPOs in 1999 and the first quarter of 2000, a period during which the market

following of Internet stocks was high. Indeed, many Internet firms did IPOs to “cash out” and

take advantage of the amount of financial capital available in the stock market. This is evident in

a study by Croson et al. (2001), who find that many B2B firms made their market entry decisions

based on the potential of excessive returns from IPOs in the stock market. Hence, IPO entry may

be picking up the effect of the abundance of market capital and investors’ willingness to invest in

Internet stocks. When more market capital is available and market sentiments are positive,

existing Internet firms are more apt to survive—what we call the “Internet gold rush effect.”

Even though we suggest a smaller number of Internet firm IPOs leads to increased likelihood

of failure, the reverse can also be true. However, we do not believe this is the case in our data

analysis for two reasons. First, we used one-quarter-lagged IPOEntry to predict firm failure.

Even though we cannot predict 100% causality, this temporal separation gives us stronger

support for the direction of the relationship between Internet firm failure and IPO entry. Second,

our data suggest Internet firm IPOs responded to changes in market condition faster than Internet

firm failures. Internet firm IPOs dropped from 17 in Quarter 1 to 6 in Quarter 2 of 2000, while

the number of Internet firm failures remain as zero in both quarters. Failure started to occur in

Quarter 3 when the number of Internet firm IPOs reduced to one. Had the causality been in the

reverse direction, failure should be the first sign of a change rather than the number of IPOs.

The products or services that a firm provides can also affect its viability in the e-marketplace.

Specifically, the selling of digital goods or services, such as contents and financial services, can

reduce a firm’s likelihood of failure compared to the selling of physical goods, such as clothing,

31

books, CDs and DVDs. This result is consistent with Barua et al.’s (2000) findings. They report

that digital product Internet firms benefit from higher productivities than their physical

counterparts, due to the higher level of digitization of business processes. Because of the overlap

between the types of products or services a firm provides and the market it competes in, our

results suggest two possible reasons for the difference. First, many digital product Internet firms

compete in breakthrough markets and are able to create brand new products and services for their

customers. The ability to serve markets that were not served before gives these firms

competitive advantage and enhances their survivability. Second, for Internet firms selling digital

goods or services, the ability to deliver the products or services directly via the Internet can

greatly reduce the operational costs the firms incur. These results demonstrate that innovative

use of IT to create unique product or service offerings and reduce operational costs can greatly

enhance an Internet firm’s likelihood of survival. Although physical firms are at a disadvantage,

they can also streamline their business processes to take advantage of the Internet. For example,

e-tailers can use the Internet to integrate their supply chain and reduce their procurement cost.

Communication with the customers via email or live chat online can reduce the demand on call

centers and hence reduce operational costs.

Larger public Internet firms have a higher likelihood of survival, corroborating results in

Hensler et al. (1997) and Honjo (2000), where larger firms are seen to be less likely to fail. This

result suggest that even though Internet firms are still young, the competition intensified quickly

and firms started competing on size early on in the life cycle of the digital marketplace. A large

firm size, which might reflect a firm’s access to resources, protects it from turbulence in the

digital marketplace and helps it to recover from inferior short-term financial performance.

32

A lower debt load can enhance an Internet firm’s likelihood of survival. During the DotCom

boom from 1998 to 2000, many Internet firms equated market share to future profitability. In

order to become the market leader, they borrowed big, spent big and priced below cost to attract

potential customers, which resulted in big losses and a price-sensitive customer base that will

disappear once the prices are no longer appealing. The high debt ratios the firms experienced

resulted from the need for capital to build robust systems solutions, the need to spend heavily to

build brand awareness and continuous losses from operations, so these firms were pushed toward

bankruptcy. For Internet startups, maintaining a steady growth plan and focusing on the most

profitable customers are essential for achieving profitability and building competitiveness.

Third, the hazard rates for public Internet firms targeting different markets are the same.

Though investors in the stock market were more attentive to B2C Internet firms in 1998 and

1999 and to B2B firms in 2000, the market a public Internet firm served was not a determinant of

its hazard rate from 1996 to 2003. This result confirms our Target Market Hypothesis (H6).

Hence, our empirical analysis reveals it is not who the customers are but what products or

services an Internet firm provides that matters. B2B, B2C and B2B&C firms can take equal

advantage of the digital channel if they sell digital products or services via the Internet.

Fourth, the logit results suggest that bankruptcy increases when interest rates climb. This

result corroborates what we have observed in the economy recently. The stock market crash in

March 2000 and the large-scale failure in the DotCom sector triggered a slowdown in the general

economy, leading to in a series of interest rate cuts by the Federal Reserve Bank. As an indicator

(Granger 1989), interest rates lag the economic cycle and Internet firm bankruptcies and

liquidations we observed during the past couple of years. So this resulted in a positive

relationship between interest rate and Internet firm bankruptcy in our logit model. However, in

33

our Cox model, interest rate was not significant. Why? Possibly because data from a longer

period of time were used. For logit, only the last quarter of data available for each firm was used

and the sample period was from June 2000 to March 2003. All data available for firms were

used in the Cox model and the sample period there was from April 1996 to March 2003.

We illustrate the trend in interest rate and the number of public Internet firm bankruptcies

and liquidations in Figure 4. During the period from mid-2000 to 2002, a higher interest rate was

associated with a larger number of Internet firm bankruptcies and liquidations. However, if we

consider a longer time period, the association between a higher interest rate and a higher number

of Internet firm bankruptcies after 2000 evened out. Hence, our hazard model did not detect any

relationship between interest rate and bankruptcy. These results reveal the logit’s sensitivity to

anomalies in a shorter time frame. Examining just one quarter of data for each firm can help us

predict whether it will fail in the next period. But it is better to test with data for each firm over a

longer period to avoid mistaken inferences derived from any observable short-term effects.

Figure 4. Comparison of Internet Firm Bankruptcies/Liquidations and Interest Rate

CONCLUSION

Drawing upon multiple theories, we develop and test a survival theory of Internet firm

34

duration. Our research extends the IS knowledge on IT and firm performance in that we

approach this issue from a survival angle. By identifying unique characteristics that distinguish

Internet firms from traditional businesses, we are able to examine how the extent to which IT is

used to create unique product offerings and reduce operational costs affect survival. We employ

the logit model, and also perform nonparametric and semiparametric survival analyses on a

sample of public Internet firms. The use of multiple models allows us to cross-validate our

results. We also sketch out the Internet firm bankruptcy and liquidation rates at the different

stages of their lifetimes. Our results suggest that Internet firms that sell digital products or

services are more likely to survive due to unique value offered to customers and reduced

operational costs. Our research also reveals the importance of maintaining a low debt ratio, since

many Internet firms are new startups and still are unable to avoid operating losses. Finally,

during our sample period, a vibrant capital market, as indicated by the large number of Internet

firm IPOs, and a large firm size also reduced an Internet firm’s likelihood of failure.

Our research has the following limitations. First, as most Internet firms are still relatively

young, our results may not adequately characterize the ways they reach outcomes in the later

periods of their business life cycles. The initial boom and the subsequent large-scale failure in

the Internet sector further restrict the generalizability of our results. However, we believe a

study like ours can help both the academic community and business professionals to better

understand the turbulence in the digital marketplace during the past three years. In addition,

results from our research can also help managers to identify the drivers for survival and direct

their attentions and resources to the most crucial levers to maintain a healthy business. Second,

because we only have public Internet firms in our sample, the results may not readily generalize

to private Internet firms. However, it is extremely difficult to obtain financial information about

35

private firms. We leave for future research small-scale analysis of the performance and survival

of private Internet firms and comparisons between them and public firms.

REFERENCES

Agresti, A. 2002. Categorical Data Analysis. Wiley, New York, NY. Audretsch, D. B. 1991. New firm survival and the technological regime. Review of Economics and Statistics 73(3) 441-450. Audretsch, D. B., T. Mahmood. 1995. New firm survival: New results using a hazard function. Review of Economics and Statistics 77(1) 97-103. Barua, A., J. Pinnell, J. Shutter, A. B. Whinston. 1999. Measuring the Internet economy: An exploratory study. Working Paper, Center for Research on E-Commerce, McComb School of Business, University of Texas at Austin, Austin, TX. Barua, A., J. Pinnell, J. Shutter, A. B. Whinston, B. Wilson. 2001. Measuring the Internet economy. Working Paper, Center for Research on E-Commerce, McComb School of Business, University of Texas at Austin, Austin, TX. Barua, A., A. B. Whinston, F. Yin. 2000. Not all dot coms are created equal: An exploratory investigation of the productivity of Internet based companies. Working Paper, Center for Research on E-Commerce, McComb School of Business, University of Texas at Austin, Austin, TX. Brynjolfsson, E., L. M. Hitt. 1996. Paradox lost? Firm-level evidence on the returns to information systems spending. Management Science 42(4) 541-568. Casey, C., N. Bartczak. 1985. Using operating cash flow data to predict financial distress: Some extensions. Journal of Accounting Research 23(1) 384-401. Chen, P. Y., L. M. Hitt. 2002. Measuring switching costs and the determinants of customer retention in internet-enabled businesses: A study of the online brokerage industry. Information Systems Research 13(3) 255-274. Clemons, E. K., S. P. Reddi. 1993. The impact of information technology on the organization of economic activity: The "move to the middle" hypothesis. Journal of Management Information Systems 10(2) 9-35. Cox, D. 1975. Partial likelihood. Biometrika 62(2) 269-275. Cramer, J. S. 1999. Predictive performance of the binary logit model in unbalanced samples. Journal of the Royal Statistical Society: Series D (The Statistician) 48(1) 85-94.

36