Widespread Excess Capacity in Manufacturing

ManufacturingCapacity Utilization

Source: Federal Reserve Board

Capacity Utilization By Industry

Industry Percent Chg.Dec.

2007Oct. 2009

Primary metal 86 57 -29 Machinery 79 57 -22 Motor vehicles/parts 70 51 -19 Wood product 68 51 -18 Fabricated metal 80 63 -17 Plastics/rubber 83 68 -16 Computer/electronic 76 63 -13 Paper 84 75 -9 Aerospace 84 76 -8 Electric power 85 79 -7 Mining 91 84 -7 Chemical 79 73 -6 Petroleum/coal prds 87 83 -4 Food 82 81 -1

Global Exports Bottoming Out

United States and World Exports of Goods, Inflation-Adjusted

Source: CPB Netherlands Bureau for Economic Policy Analysis

Nonfinancial Corporations Have Surplus Cash

Nonfarm Nonfinancial Financing Gap*

Source: Federal Reserve Board*Capital expenditures less the sum of US internal funds and inventory valuation adjustment

Diverging Business Investment Patterns in 2010

Business Investment, Inflation-Adjusted

Source: U.S. Bureau of Economic Analysis , MAPI Simulation of IHS Global Insight ModelF=Forecast

Nonresidential Construction Continues To Decline

Nonresidential Construction

Type Percent Change

2009 2010 2011

Nonresidential Structures -18 -16 +1

Commercial and Health Care -30 -21 +24

Manufacturing +27 -30 -18

Other Structures -9 -13 0

Construction By Type

Source: Left – U.S. Bureau of Economic Analysis, Right – MAPI Simulation of IHS Global Insight Model

Most Industries Are In Recession Phase Relative To One Year Ago

Source: MAPI

Cyclical Position of Business Investment Industries in Third Quarter 2009

Capital Equipment Industries Were Pulled Into Recession

Percent Change Percent Change

Industry 2009 2010 2011 Industry 2009 2010 2011

Elec. Equip. exceptAppliances -12 2 9

MetalworkingMachinery -24 0 12

Architec. & Structural Metals -18 -9 3 Industrial Machinery -35 4 18ConstructionMachinery -28 1 8

Commercial, Service &Other -17 1 13

Engines & Turbines -29 1 24 Forging & Stamping -20 3 13

Agricultural Equipment -9 -3 5Aerospace Products & Parts 1 2 8

Drilling Equipment -21 -6 4 Ship & Boat Building -13 -1 -2

Source: Federal Reserve Board, MAPI Simulation of IHS Global Insight Model

Investment-Related Manufacturing Production

Forward-Looking Manufacturing Indicators Improve

Manufacturing Production and Purchasing Managers’ Production Indexes

Source: Federal Reserve Board, Institute for Supply Management

U.S., Japanese, and Canadian Manufacturing Recovering From Severe Recession

Industrial Production By Country

Source: Left – OECD, Right – Consensus Forecasts, MAPI

Industrial Production By Country

Country Percent Change

2009 2010

United States -10 +4

Canada -12 +2

Japan -22 +11

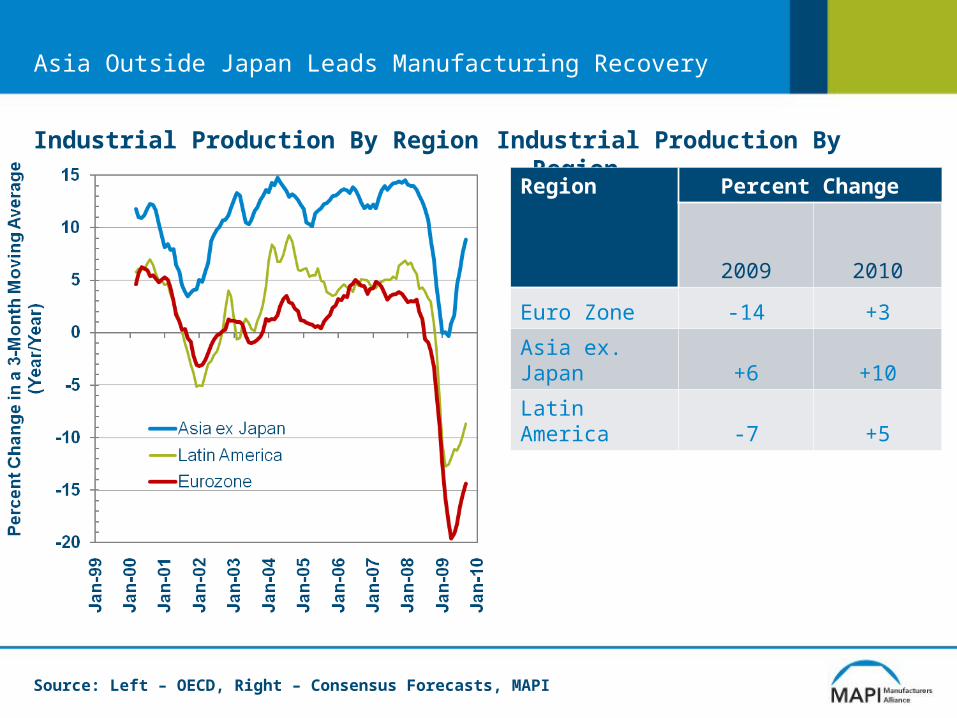

Asia Outside Japan Leads Manufacturing Recovery

Industrial Production By Region

Source: Left – OECD, Right – Consensus Forecasts, MAPI

Industrial Production By Region

Region Percent Change

2009 2010

Euro Zone -14 +3

Asia ex. Japan +6 +10

Latin America -7 +5

A Severe Global Recession Followed By Strong Initial Recovery

World Industrial Production

Source: CPB Netherlands Bureau for Economic Policy Analysis, Consensus Forecasts, MAPI

World Industrial Production