Download - 3/8/12

Economics for Leaders

3/8/12

BR: Explain how BR: Explain how “substitution” works“substitution” works

Today: Finish yesterdayToday: Finish yesterday

Consumers in Markets

desire for a product

willingness and ability to pay for it++

Demand =

Economics for Leaders

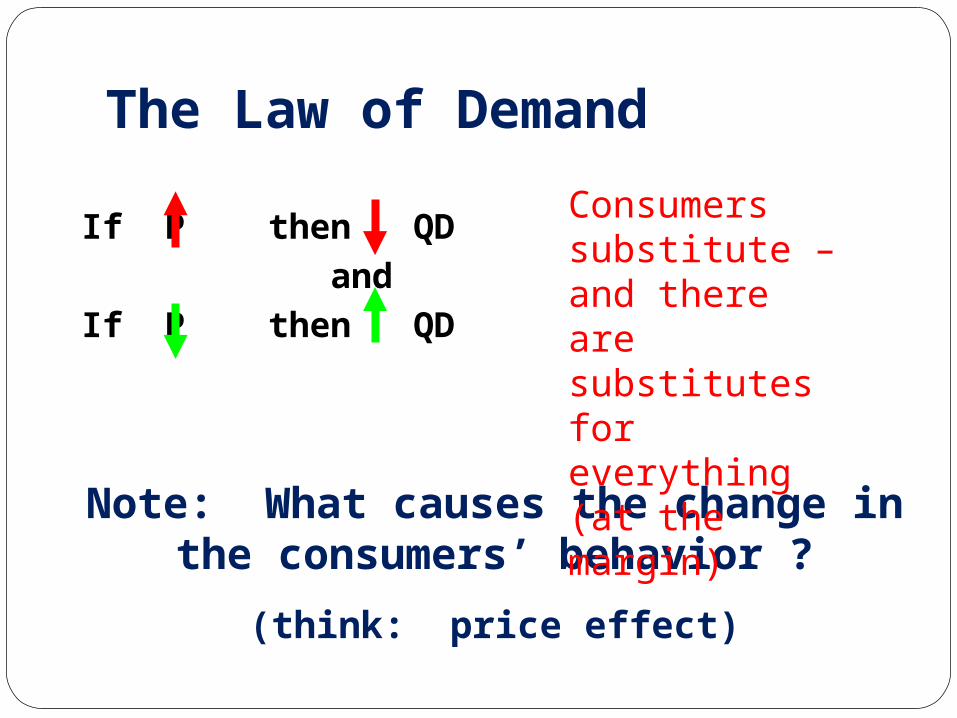

The Law of Demand

If P then QD andIf P then QD

Note: What causes the change in the consumers’ behavior ?

(think: price effect)

Consumers substitute – and there are substitutes for everything (at the margin)

Shifting Demand and Supply

What things besides price affect how much people buy?

Economics for Leaders

Price As An Incentive for Consumers

Price Qa Qb Qt

$35 3 3 6

$20 4 6 10

$13 5 10 15

$7 6 15 21

Demand for CDs

Economics for Leaders

Graphs: Pictures of Demand

Price

0 Quantity Demanded (QD)

How much will people buy at this price?

DaDb Dt

Economics for Leaders

The Law of Demand

If P then QD andIf P then QD

Note: What causes the change in the consumers’ behavior ?

(think: price effect)

Consumers substitute – and there are substitutes for everything (at the margin)

Economics for Leaders

Assumption:EVERYTHINGEVERYTHING

ELSEREMAINS

THESAME

Economics for Leaders

What If “Everything Else” DOESN’T Stay the Same?

Price Qa Qb Qt

$35 5 4 9

$20 7 7 14

$13 8 11 19

$7 10 16 26

Demand for CDs AFTER Something has changed: Your pay at your job doubles, for example.

Demand shifters

tastes and preferences numbers of consumers prices of substitutes

(coffee & tea)prices of complements

(peanut butter & jelly)expectations of future pricesincome

Demand shifters: examples

What will happen to the demand for hotdogs if the price of hotdog buns increases?

What will happen to the demand for hamburger if the price of hotdogs increases?

Consumers Are Only ½ the Market

SupplySupply

What Incentive Do Producers have to make (Any or More) of a Product?

Producers are in business to make…Producers will make more of a product only if that decision increases…

Marginal Benefits (MB) and Marginal Cost (MC)MB > MC this is good, so make moreMB < MC not good, so make less

PROFIT

PROFIT

Economics for Leaders

Price An Incentive for Producers

Price Qa Qb Qt

$7 5 3 8

$13 8 7 15

$20 11 9 20

$35 20 14 34

Producers of CDs

Economics for Leaders

The Law of Supply

If P then QS andIf P then QS

Note: What causes the change in the producers’ behavior ?

(think: price effect)

Remember: Producers can

substitute, too.

Economics for Leaders

Graphs: Pictures of Supply

Price

0 Quantity Supplied (QS)

How much will producers offer for sale at this price?

SaSb

St

Economics for Leaders

Assumption:EVERYTHINGEVERYTHING

ELSEREMAINS

THESAME

Shifting Supply

What besides price affects producers’ willingness to offer products for sale?

Economics for Leaders

What If “Everything Else” DOESN’T Stay the Same?

Price Qa Qb Qt

$7 3 2 5

$13 6 6 12

$20 9 8 17

$35 18 13 31

Supply of CDs AFTER Something has changed. Price of labor goes up by $2 per hour.

Supply shifters

costs of productionresource availability changestechnology changespolicies change (taxes, for example)

numbers of suppliers prices of production substitutes

producer could make more money producing other things (grow corn instead of soybeans, for example)In WW2 auto factories switched to making tanks

suppliers’ expectations about the future“prediction of bad hurricane season”“minimum wage is going to go up”

Supply shifters: Examples

What will happen to the supply of hotdogs if the price of hotdog buns increases? Why?

What will happen to the supply of DVDs if recording technology becomes more efficient? Why?

What will happen to the supply of new houses after a summer of terrible fires destroys many forest areas? Why?

Exit Slip:

1. What is the law of demand

2. Describe one example of how price can shift, demand can shift.

3. What roles do substitutes play in supply and demand (think margin)?

Equilibrium Price

The price at which the amount (quantity) people want to buy = the amount (quantity) producers

want to sell.

QD = QS

Market equilibrium

At market equilibrium, there is no force for change (ceteris paribus).

All those willing and able to buy at the market price were able to buy all they wanted.

All those willing and able to sell at the market price sold all they had.

The units sold brought at least as much value to the buyers as they cost the producers.

Everybody gained.

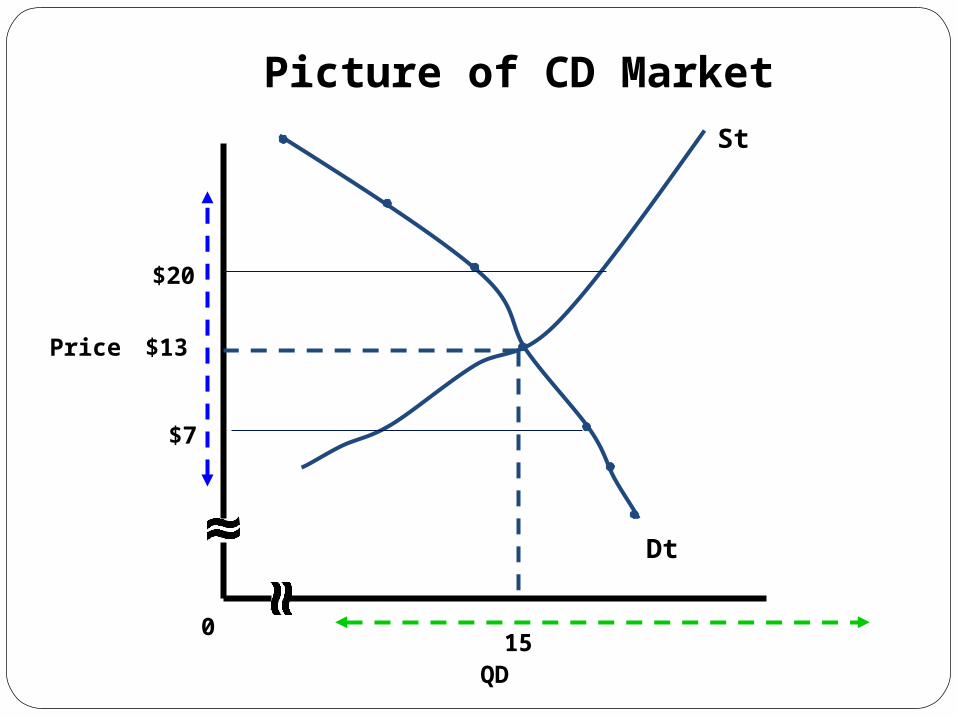

Economics for Leaders

Picture of CD Market

Price

QD

0

$13

15

Dt

St

$20

$7

Economics for Leaders

Shifts and changing equilibrium

Q

P

Q*

P*

D

S

S’

An deacrese in supply causes an increase in market price and a decrease in quantity demanded, ceteris paribus.

Q**

P**

Economics for Leaders

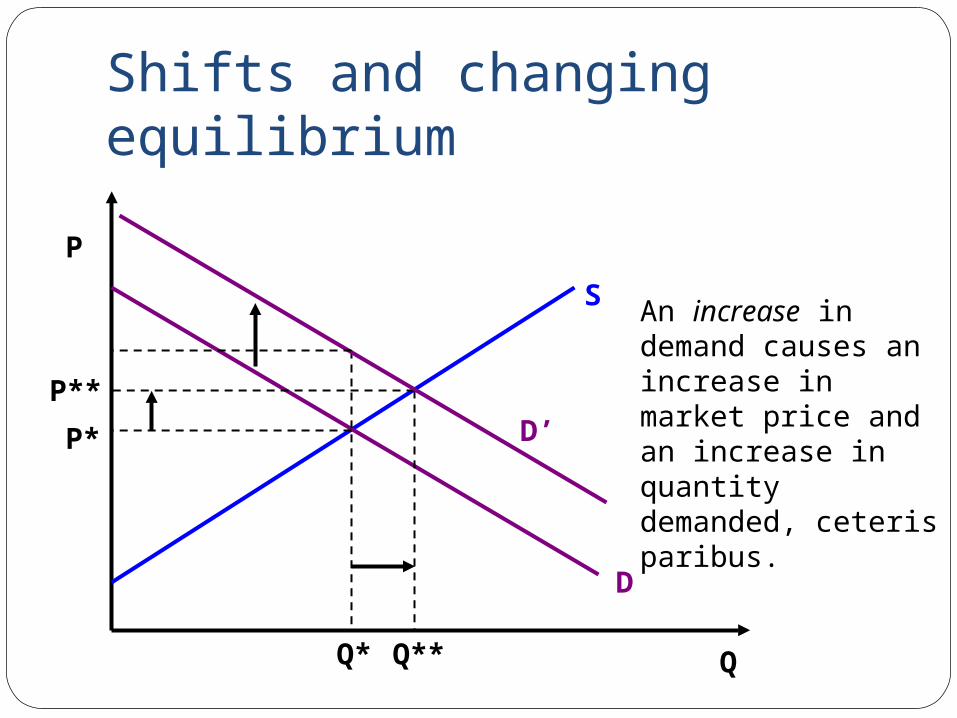

Shifts and changing equilibrium

Q

P

Q*

P*

D

S

D’

An increase in demand causes an increase in market price and an increase in quantity demanded, ceteris paribus.

Q**

P**

Economics for Leaders

1.Markets are dynamic.

2.Market prices aren’t set; they happen!

http://www.youtube.com/watch?v=Ng3XHPdexNM

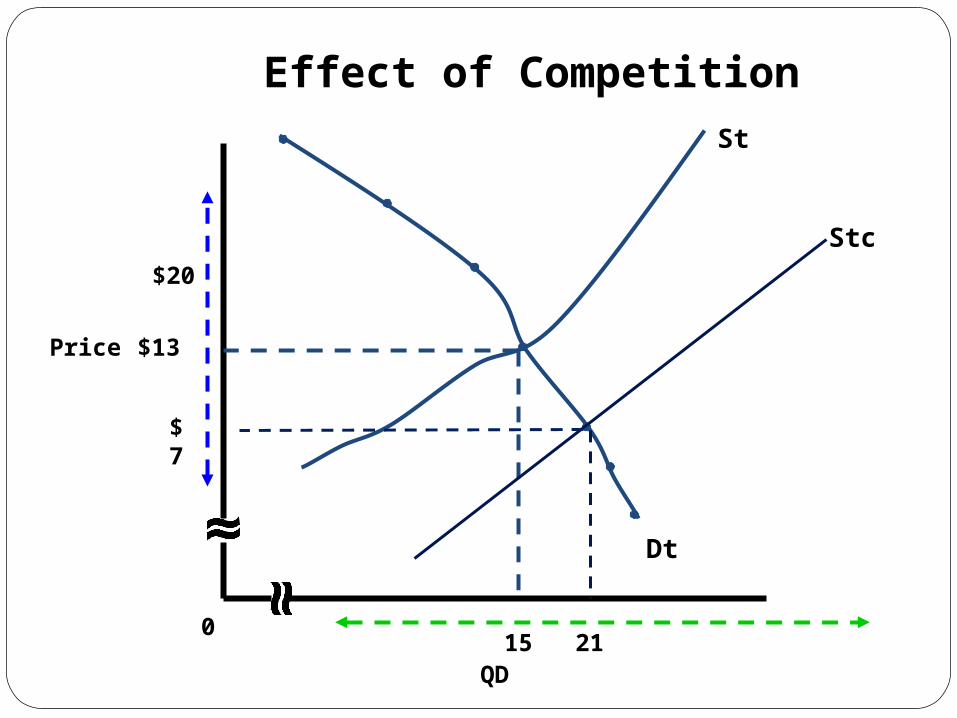

Economics for Leaders

Effect of Competition

Price

QD

0

$13

15

Dt

St

$20

$7

Stc

21

Economics for Leaders

Sellers Compete with Other Sellers

How do they compete?

Economics for Leaders

Buyers Compete with Other Buyers

How do they compete?

Economics for Leaders

Market Competition: Win-Win Outcomes

Both buyers and sellers value what they received more than what they gave up.

Economics for Leaders

ERP-4: Institutions are the “rules of the game” that influence choices.

Laws, customs, moral principles, superstitions, and cultural values influence people’s choices. These basic institutions controlling behavior set out and establish the incentive structure and the basic design of the economic system.

Economics for Leaders

Institutions necessary for well-functioning markets:

Property rights Rule of law

Economics for Leaders

1.They make more goods and services available at lower prices.

2.The presence of other competitors (actual or potential) provides incentives for innovation

3.Markets provides opportunities for the poor as workers.

4.Markets provides opportunities for the poor as entrepreneurs.

Open Markets Benefit the Poor

The “Big Ideas” from Lesson 3:

1. Open markets benefit both buyers and sellers by providing a low cost mechanism by which they can trade with one another

2. Open markets benefit the poor by encouraging economic growth

3. Open entry and exit with competition make markets efficient.

4. Money price rations goods in markets.5. Clearly defined property rights and rule of law are

necessary for this process to work

![[XLS] Web view1 2 3 4 5 6 7 8 9 10 11 12. 1 2 3 4 5 6 7 8 9 10 11 12. 1 2 3 4 5 6 7 8 9 10 11 12. 1 2 3 4 5 6 7 8 9 10 11 12. 1 2 3 4 5 6 7 8 9 10 11 12. 1 2 3 4 5 6 7 8 9 10 11 12](https://cdn.vdocuments.us/doc/165x107/5b1d62ed7f8b9ac6348b9098/xls-web-view1-2-3-4-5-6-7-8-9-10-11-12-1-2-3-4-5-6-7-8-9-10-11-12-1-2-3-4-5.jpg)