2015 Global Macro and Multi-Asset Outlook

MMXV

1

For Professional Investors and Advisors only

40% of German bonds currently in issue have a negative yield to maturity.

Apple’s market cap of $650 billion is almost $200 billion larger than the market cap.

of all Eurozone banks.

There are currently 2.5 billion people who need more water than they have access

to. This will rise to 6 billion by 2050 according to the OECD and UN forecasts.

The S&P 500 index has moved step for step with the US Federal reserve balance

sheet since 2009. In October 2014 the Fed announced it was ending Quantitative

easing.

There is 30x more gold than palladium on the planet.

All the platinum ever mined would fit into an average sized living room.

One in every six people in the world is Indian and one in five is Chinese. Developing

economies make up 84% of the world’s population.

80% of the world’s GDP is supported by 0 interest rate policies.

German house prices are down in real terms from 25 years ago.

2015 Global Macro and Multi-Asset Outlook

Equities: We expect mixed performance from

equities. We forecast that US equities will deliver

negative returns based on premium valuations, a

strong USD and a relatively less accommodative

central bank. We anticipate a sharp rally in

European banks, and strength from European

equities with foreign revenues. Large cap. US

technology and European pharmaceuticals are

well positioned for 2015. Europe and emerging

Asia trade at most compelling valuations

Fixed Income: We expect capital losses from

sovereign fixed income with greater than five

years to maturity. Emerging market inflation linked

bonds offer significant real yields, and in euro

terms will likely be 2015’s best performing fixed

income sector. 2014 marked the end of the 30

year fixed income bull market

Currencies: EUR will be the carry trade currency

of choice. The zero interest rate policy and

expansion of ECB’s balance sheet, eventually

through explicit quantitative easing will push

EUR/USD to 1.09 by the end of 2015. JPY will

continue to lose value vs. the USD but strengthen

vs. euro.

Real Estate: We are bullish of listed residential

property companies in Germany. The zero interest

rate policy of the ECB is appropriate for the

Eurozone but will fuel a property bubble in

Germany.

Commodities: We expect positive real yields on

US 10 year bonds will continue to keep negative

pressure on gold prices, while palladium and

platinum will benefit from increased industrial

demand and uncertain supply dynamics.

Alternatives: 2018 Dividend futures on the Euro

Stoxx 50 are trading 50% below consensus

estimates and 15% below 2014 dividend levels.

We expect these futures to deliver very strong

performance in 2015.

Selected forecast returns for 2015 (%)

Source: Plurimi Investment Managers (PIM). Forecasts are based on closing 2/12/2014 values. Expected returns are based on PIM’s proprietary models utilising a combination of valuation, growth, momentum and quality factors.

Current

2015 y/e

forecast

2015 Return (With yield)

S&P 500 2070 2015 -1%

FTSE 100 6717 7000 7%

Euro Stoxx 50 3248 3350 7%

Nikkei 17720 18500 6%

DJ 600 Banks 144 170 23%

Russel 2000 1177 1110 -5%

Euro50 2018

Dividends 108 118 9%

German Residential 100 112 12%

US S&P Utilities 463 430 -5%

EUR/USD 1.24 1.09 -12%

USD/JPY 120 125 +3%

German 10 Year 0.8 1.4 -5%

US 10 Year 2.3 2.6 -1%

UK 10 Year 2.0 2.6 -2%

Brent Oil $70/bbl $80/bbl 5%*

Gold $1200/oz $1070/oz -11%

Platinum $1203/oz 1220/oz 2%

Palladium $804/oz $865/oz 8%

2

The 800 million euro expansion of the ECB’s

balance sheet will be the most important factor

driving asset class performance in 2015.

FX will be a major component of returns in 2015,

helping assets priced in euros and yen.

Over the next market cycle major asset classes

will produce nominal and real returns that are

significantly lower than historic levels.

2015 Outlook

2015 Outlook

2014 Review

During 2014 we saw the global economy grow by approximately 3% with about 3% inflation. These numbers

are in line with 25 year global averages, but regionally there were significant divergences. The Eurozone saw

growth of less than 1%, the US grew slightly more than 2%, the UK grew by 3% and the Chinese economy

continued to expand by about 7.5%. Developed economies experienced inflation at slightly more than 1% while

emerging markets saw inflation rates of about 5%.

Developed central bank monetary policy was without exception accommodative in 2014, however in the fourth

quarter of 2014 the US Federal Reserve (Fed) ended quantitative easing (QE) supported by solid economic

data. In sharp contrast, the European Central Bank (ECB) announced plans to significantly expand its balance

sheet and the Bank of Japan (BoJ) responded to slower-than-desired inflation dynamics with an acceleration of

its programme of qualitative and quantitative easing (QQE).

Policy Outlook

We expect central bank policy will continue to be the most important driver of asset class returns in 2015 and

for several years to come. Of all policies the most important for investors is the end of the Fed’s balance sheet

expansion and the rebuilding of the ECB’s balance sheet. ECB President Mario Draghi has suggested EUR

800 million will be added to the ECB’s balance sheet to get back to its early 2012 levels. An accommodative

stance on monetary policy is needed in Europe as Germany seems unlikely to loosen its current budget plans

leaving the onus on monetary policy to reflate the Eurozone economy.

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

4500000

5000000

01/03/1999 01/03/2002 01/03/2005 01/03/2008 01/03/2011 01/03/2014 01/03/2017

FEDBalance

ECBBalance

ECB and Federal Reserve Balance Sheets ($ Millions)

Based on ECB

announcement

in October

2014

If explicit

quantitative

easing is

undertaken

Key Investment Chart for 2015

Source: Bloomberg, Plurimi Investment Managers estimates

The ECB saw its balance sheet contract

in 2012 and 2013. We believe this was

the unintended consequence of interest

rate policies which led to early repayment

of the ECB’s long-term refinancing

operations (LTRO) by euro-zone banks.

The shrinking balance sheet was

essentially a tightening of monetary

conditions and led to a very strong euro

in 2012 and 2013, despite the very poor

economy and financial conditions within

the Eurozone. The effect of the trillion

dollar expansion of the ECB balance

sheet should not be underestimated. The

impact will offset the previous contraction

and we expect improved financial

conditions in the Eurozone, in a similar

scale to those regions which have

implemented significant QE over previous

years.

“We will do whatever it takes” Mario Draghi July 2012

This is what it takes….

3

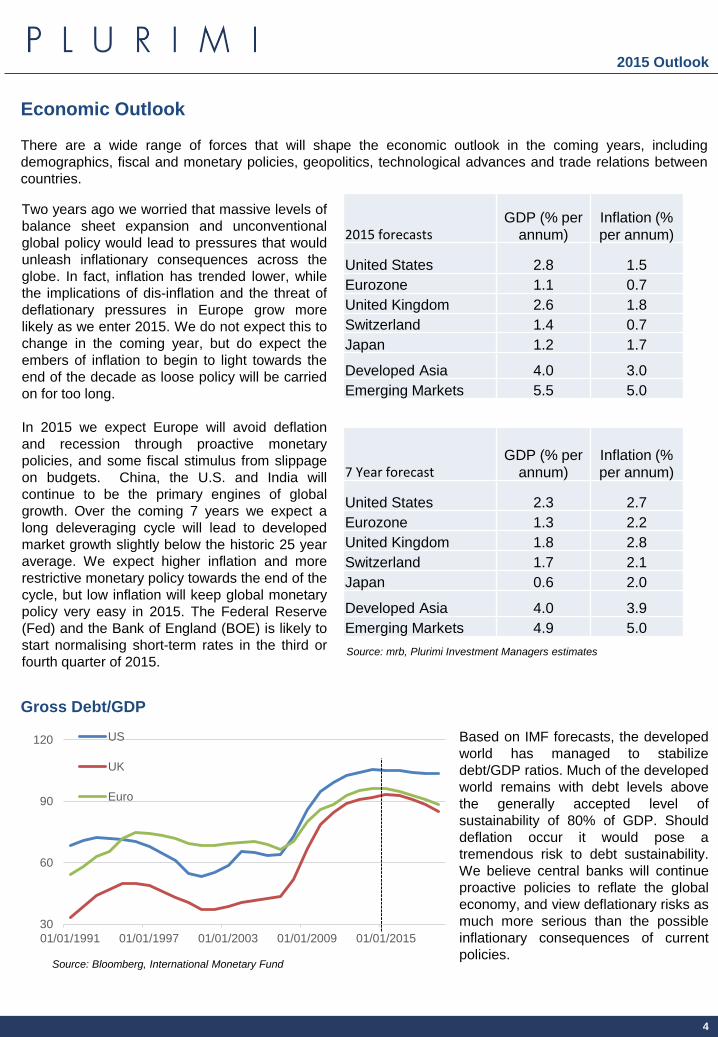

Economic Outlook

There are a wide range of forces that will shape the economic outlook in the coming years, including

demographics, fiscal and monetary policies, geopolitics, technological advances and trade relations between

countries.

7 Year forecastGDP (% per

annum)

Inflation (%

per annum)

United States 2.3 2.7

Eurozone 1.3 2.2

United Kingdom 1.8 2.8

Switzerland 1.7 2.1

Japan 0.6 2.0

Developed Asia 4.0 3.9

Emerging Markets 4.9 5.0

Two years ago we worried that massive levels of

balance sheet expansion and unconventional

global policy would lead to pressures that would

unleash inflationary consequences across the

globe. In fact, inflation has trended lower, while

the implications of dis-inflation and the threat of

deflationary pressures in Europe grow more

likely as we enter 2015. We do not expect this to

change in the coming year, but do expect the

embers of inflation to begin to light towards the

end of the decade as loose policy will be carried

on for too long.

In 2015 we expect Europe will avoid deflation

and recession through proactive monetary

policies, and some fiscal stimulus from slippage

on budgets. China, the U.S. and India will

continue to be the primary engines of global

growth. Over the coming 7 years we expect a

long deleveraging cycle will lead to developed

market growth slightly below the historic 25 year

average. We expect higher inflation and more

restrictive monetary policy towards the end of the

cycle, but low inflation will keep global monetary

policy very easy in 2015. The Federal Reserve

(Fed) and the Bank of England (BOE) is likely to

start normalising short-term rates in the third or

fourth quarter of 2015.

2015 forecastsGDP (% per

annum)

Inflation (%

per annum)

United States 2.8 1.5

Eurozone 1.1 0.7

United Kingdom 2.6 1.8

Switzerland 1.4 0.7

Japan 1.2 1.7

Developed Asia 4.0 3.0

Emerging Markets 5.5 5.0

30

60

90

120

01/01/1991 01/01/1997 01/01/2003 01/01/2009 01/01/2015

US

UK

Euro

Source: Bloomberg, International Monetary Fund

Based on IMF forecasts, the developed

world has managed to stabilize

debt/GDP ratios. Much of the developed

world remains with debt levels above

the generally accepted level of

sustainability of 80% of GDP. Should

deflation occur it would pose a

tremendous risk to debt sustainability.

We believe central banks will continue

proactive policies to reflate the global

economy, and view deflationary risks as

much more serious than the possible

inflationary consequences of current

policies.

Gross Debt/GDP

4

2015 Outlook

Source: mrb, Plurimi Investment Managers estimates

Economic and Policy Outlook

Our expectation is that the global economic expansion will continue but remain relatively subdued and

deflationary pressures will continue to exist within the Eurozone. We expect central banks will only normalise

policy once they are absolutely convinced we are on the path to sustainable growth, meaning short term

interest rates will remain near zero for most of 2015. All of this sounds very good for fixed income. However the

most important component is the starting yield. Risk aversion has remained at elevated levels following the

financial crisis. Economic and policy uncertainty has led investors to keep significant amounts of cash un-

invested and made them reluctant to rotate into growth assets. Defensive yield plays, have pushed government

bond yields to record lows. Such low yields increase the odds of capital losses in 2015, and make the

possibility of positive real returns over a market cycle close to non-existent.

Mario Draghi’s message to the world could not be clearer. Faced with the need to halt persistently decelerating

inflation, Mr. Draghi has shown a clear willingness on the part of the ECB to help the Eurozone

economies. Over the past two years the ECB has shifted its focus from stabilizing the financial system and

saving the monetary union from collapse to combating weak growth and excessively low inflation. Zero interest

rates influenced by private sector weakness is of benefit to the broader financial system.

Economic anxiety has made corporates hesitant to increase capital spending in recent years, despite the

rebound in corporate profits and record low borrowing rates. There is evidence that this is improving, led by

capital spending in the U.S. Central bank policy is addressing private sector deleveraging pressures and the

financial systems. The non-financial business sector is generally healthy and the ultra-accommodative policy

should begin to create longer-term capital spending projects as the economic expansion within the US

continues to gain traction.

Summary

• Modest acceleration in global growth to slightly above 3%.

• Cheap oil and policy fuelling growth.

• Global Inflation to remain subdued.

• China to slow but will remain second biggest contributor to global growth.

The growth picture in Japan and the Euro area remain vulnerable but we expect both these economies to

perform better in 2015. Easing financial conditions will be designed to increase lending, lower oil prices and

increasingly competitive currency dynamics will facilitate growth. Despite our somewhat optimistic view we do

acknowledge there is a real downside risk scenario in the Eurozone and deflationary pressures will remain.

Should the ECB fail to deliver on its balance sheet expansion pledges or slow its reflationary policies, our

expectations for some growth in the Eurozone would change.

China’s housing and credit imbalances are of particular risk to their overall economic performance and it is

against these risks that portfolio protection may prove to be most useful.

Key Risks

• ECB failing to deliver.

• Europe’s inability to avert further deterioration.

• Adverse geopolitical developments.

• China slowing more than expected.

5

2015 Outlook

Equity Outlook

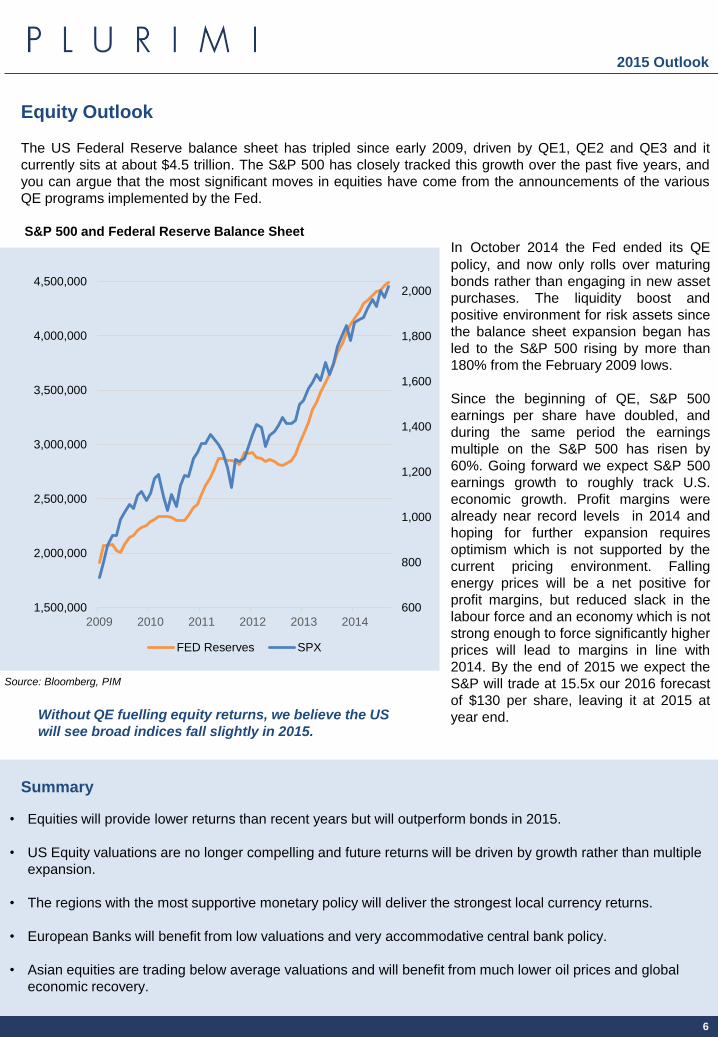

The US Federal Reserve balance sheet has tripled since early 2009, driven by QE1, QE2 and QE3 and it

currently sits at about $4.5 trillion. The S&P 500 has closely tracked this growth over the past five years, and

you can argue that the most significant moves in equities have come from the announcements of the various

QE programs implemented by the Fed.

S&P 500 and Federal Reserve Balance Sheet

600

800

1,000

1,200

1,400

1,600

1,800

2,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

2009 2010 2011 2012 2013 2014

FED Reserves SPX

In October 2014 the Fed ended its QE

policy, and now only rolls over maturing

bonds rather than engaging in new asset

purchases. The liquidity boost and

positive environment for risk assets since

the balance sheet expansion began has

led to the S&P 500 rising by more than

180% from the February 2009 lows.

Since the beginning of QE, S&P 500

earnings per share have doubled, and

during the same period the earnings

multiple on the S&P 500 has risen by

60%. Going forward we expect S&P 500

earnings growth to roughly track U.S.

economic growth. Profit margins were

already near record levels in 2014 and

hoping for further expansion requires

optimism which is not supported by the

current pricing environment. Falling

energy prices will be a net positive for

profit margins, but reduced slack in the

labour force and an economy which is not

strong enough to force significantly higher

prices will lead to margins in line with

2014. By the end of 2015 we expect the

S&P will trade at 15.5x our 2016 forecast

of $130 per share, leaving it at 2015 at

year end.Without QE fuelling equity returns, we believe the US

will see broad indices fall slightly in 2015.

• Equities will provide lower returns than recent years but will outperform bonds in 2015.

• US Equity valuations are no longer compelling and future returns will be driven by growth rather than multiple

expansion.

• The regions with the most supportive monetary policy will deliver the strongest local currency returns.

• European Banks will benefit from low valuations and very accommodative central bank policy.

• Asian equities are trading below average valuations and will benefit from much lower oil prices and global

economic recovery.

Summary

6

2015 Outlook

Source: Bloomberg, PIM

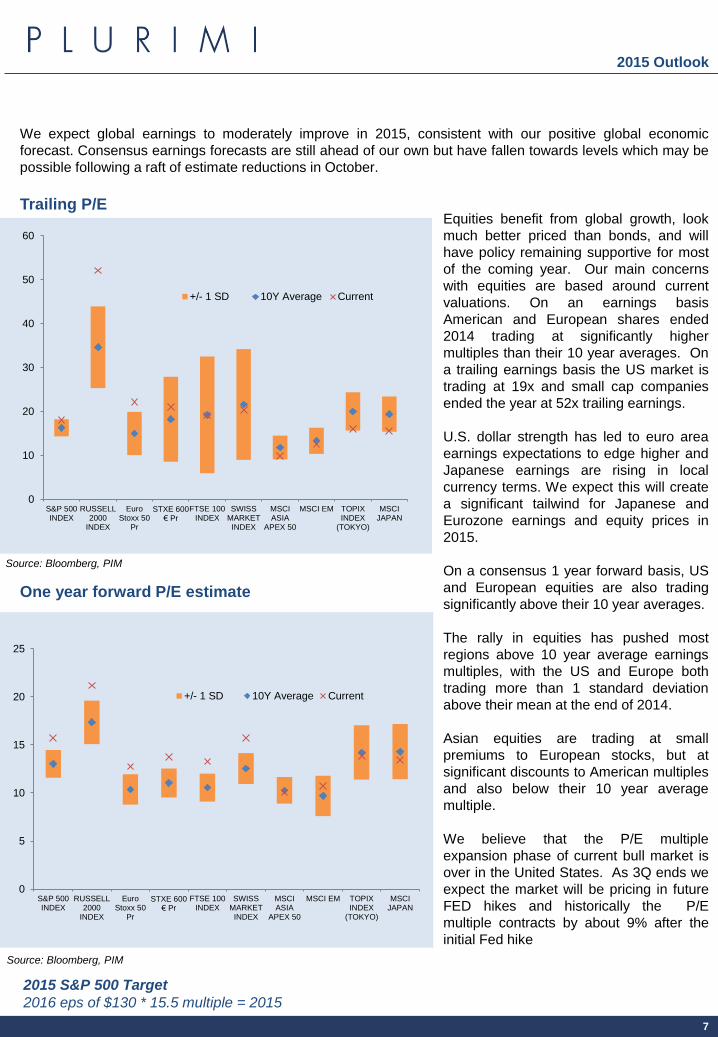

We expect global earnings to moderately improve in 2015, consistent with our positive global economic

forecast. Consensus earnings forecasts are still ahead of our own but have fallen towards levels which may be

possible following a raft of estimate reductions in October.

0

10

20

30

40

50

60

S&P 500INDEX

RUSSELL2000

INDEX

EuroStoxx 50

Pr

STXE 600 € Pr

FTSE 100INDEX

SWISSMARKETINDEX

MSCIASIA

APEX 50

MSCI EM TOPIXINDEX

(TOKYO)

MSCIJAPAN

+/- 1 SD 10Y Average Current

0

5

10

15

20

25

S&P 500INDEX

RUSSELL2000

INDEX

EuroStoxx 50

Pr

STXE 600 € Pr

FTSE 100INDEX

SWISSMARKETINDEX

MSCIASIA

APEX 50

MSCI EM TOPIXINDEX

(TOKYO)

MSCIJAPAN

+/- 1 SD 10Y Average Current

Equities benefit from global growth, look

much better priced than bonds, and will

have policy remaining supportive for most

of the coming year. Our main concerns

with equities are based around current

valuations. On an earnings basis

American and European shares ended

2014 trading at significantly higher

multiples than their 10 year averages. On

a trailing earnings basis the US market is

trading at 19x and small cap companies

ended the year at 52x trailing earnings.

U.S. dollar strength has led to euro area

earnings expectations to edge higher and

Japanese earnings are rising in local

currency terms. We expect this will create

a significant tailwind for Japanese and

Eurozone earnings and equity prices in

2015.

On a consensus 1 year forward basis, US

and European equities are also trading

significantly above their 10 year averages.

The rally in equities has pushed most

regions above 10 year average earnings

multiples, with the US and Europe both

trading more than 1 standard deviation

above their mean at the end of 2014.

Asian equities are trading at small

premiums to European stocks, but at

significant discounts to American multiples

and also below their 10 year average

multiple.

We believe that the P/E multiple

expansion phase of current bull market is

over in the United States. As 3Q ends we

expect the market will be pricing in future

FED hikes and historically the P/E

multiple contracts by about 9% after the

initial Fed hike

Trailing P/E

One year forward P/E estimate

2015 S&P 500 Target

2016 eps of $130 * 15.5 multiple = 2015

7

2015 Outlook

Source: Bloomberg, PIM

Source: Bloomberg, PIM

Multiples of book values also show US equities trading above 10 year averages, while Europe and Asia are

below historic multiples. Trading at almost 2.8x book value, the S&P will need to deliver very high returns on

equity for an extended period of time to justify these multiples.

0.6

1.1

1.6

2.1

2.6

3.1

S&P 500INDEX

RUSSELL2000

INDEX

EuroStoxx 50

Pr

STXE 600 € Pr

FTSE 100INDEX

SWISSMARKET

INDEX

MSCIASIA

APEX 50

MSCI EM TOPIXINDEX

(TOKYO)

MSCIJAPAN

+/- 1 SD 10Y Average Current

Low interest rates and record profit

margins have created an environment

where the market is trading significantly

above book value in The U.S.

At 2.8 x book the S&P must maintain

record profit margins, and continue to

grow earnings at near double digit rates.

Fair Value P/B = (ROE – growth)/(Cost of

Equity– growth)

We are sceptical that earnings growth

will significantly outstrip economic

growth and as the Fed eventually moves

towards higher rates we expect a

reversion toward the mean on global

P/B ratios.

1 year forward P/B estimate

The macro forces that are likely to prevail over the cyclical horizon favour Asian and European equities over

their U.S. counterparts, and the Eurozone is likely to be a prime beneficiary of this coming rotation.

Japan

Europe

UK

US

Excess Profit (PoE-CoE)

3 6 9 12

0.2

1.0

0.4

0.6

0.8

Log of P/B vs. Excess Profit

Equities expensive

Equities Cheap

We expect global equities to generate

a total return of 7% in local currency

terms in 2015. Global valuations are in

line with historic norms, but slightly

overvalued in regions which have

already engaged in balance sheet

expansion. We expect regions now

beginning or in the midst of this

process will see the best performance.

Earnings growth will be strongest in

Japan and Continental Europe, as

both regions benefit from

currency weakness.

7

2015 Outlook

Source: Bloomberg, PIM

Source: Bloomberg, PIM

Fixed Income Outlook

Government bonds have had a strong 2014 after selling off in 2013. We believe this reflects the tug of war

between global deleveraging, disinflation, excess savings, a strengthening global economy and expected

policy moves resulting in higher interest rates in the US and UK next year.

On Fed policy the market is currently priced for the Fed to start hiking in Q4 and raise the policy rate to 0.5-

0.6% by the end 2015 and 1.5% by the end of 2016. Consensus is below the “Fed dots” and we also believe

short term rates will not be raised as quickly as the Fed dots indicate. We do however, expect 10 year US

bond yields to rise over the coming year at rate slightly faster than forward pricing. Despite the recent growth

scare, most current data suggests that the global economic expansion is continuing and may even be

strengthening. This will put upward pressure on real bond yields.

10-Year Government Bond Yield (%)

Fair Value Measure** (%)

8

2

4

6

10

1990 2000 2010

Poor value

Good value

Fixed income generally does not offer many compelling investment opportunities, however we expect corporate

bonds will outperform government bonds in 2015. High yield spreads have widened since the June lows. Given

our positive economic views we expect to see high-yield spreads fall back to where they bottomed in mid 2014.

Investment grade spreads are less compelling, but should still narrow on the back of stronger growth and this

will be more than offset by rising government yields.

An improving global trade cycle will encourage EM bond spreads to narrow further. Inflation linked bonds from

emerging markets offer real yields of almost 3%. 2015 may not see emerging market currencies appreciate

meaningfully vs. the USD, but over the longer term higher economic growth, better demographics and lower

levels of debt will all lead to currency appreciation.

We expect the first Fed rate

hike to occur in Q4 2015, and

signal the beginning of the

end for ultra-accommodative

policy, and the end of the 30

bond bull market.

8

2015 Outlook

Source: Bloomberg, MRB, PIM

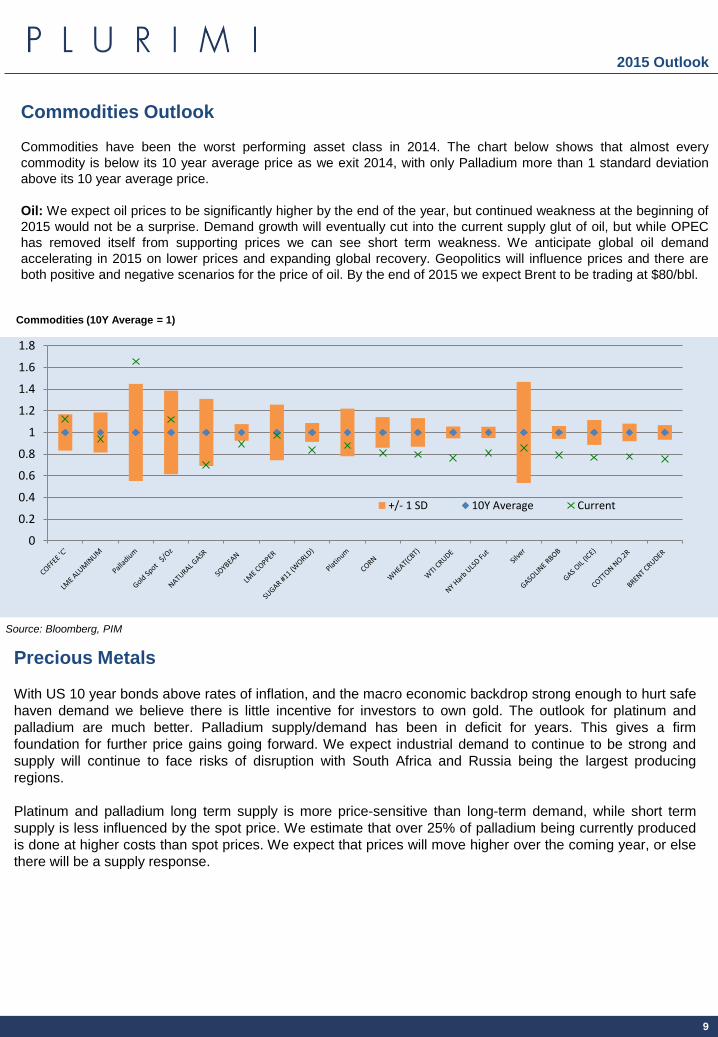

Commodities Outlook

Commodities have been the worst performing asset class in 2014. The chart below shows that almost every

commodity is below its 10 year average price as we exit 2014, with only Palladium more than 1 standard deviation

above its 10 year average price.

Oil: We expect oil prices to be significantly higher by the end of the year, but continued weakness at the beginning of

2015 would not be a surprise. Demand growth will eventually cut into the current supply glut of oil, but while OPEC

has removed itself from supporting prices we can see short term weakness. We anticipate global oil demand

accelerating in 2015 on lower prices and expanding global recovery. Geopolitics will influence prices and there are

both positive and negative scenarios for the price of oil. By the end of 2015 we expect Brent to be trading at $80/bbl.

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

Commodities (10Y Average = 1)

+/- 1 SD 10Y Average Current

Precious Metals

With US 10 year bonds above rates of inflation, and the macro economic backdrop strong enough to hurt safe

haven demand we believe there is little incentive for investors to own gold. The outlook for platinum and

palladium are much better. Palladium supply/demand has been in deficit for years. This gives a firm

foundation for further price gains going forward. We expect industrial demand to continue to be strong and

supply will continue to face risks of disruption with South Africa and Russia being the largest producing

regions.

Platinum and palladium long term supply is more price-sensitive than long-term demand, while short term

supply is less influenced by the spot price. We estimate that over 25% of palladium being currently produced

is done at higher costs than spot prices. We expect that prices will move higher over the coming year, or else

there will be a supply response.

9

2015 Outlook

Source: Bloomberg, PIM

100

110

120

130

140

150

160

170

180

2014 2015 2016 2017 2018 2019 2020

Future

Consensus

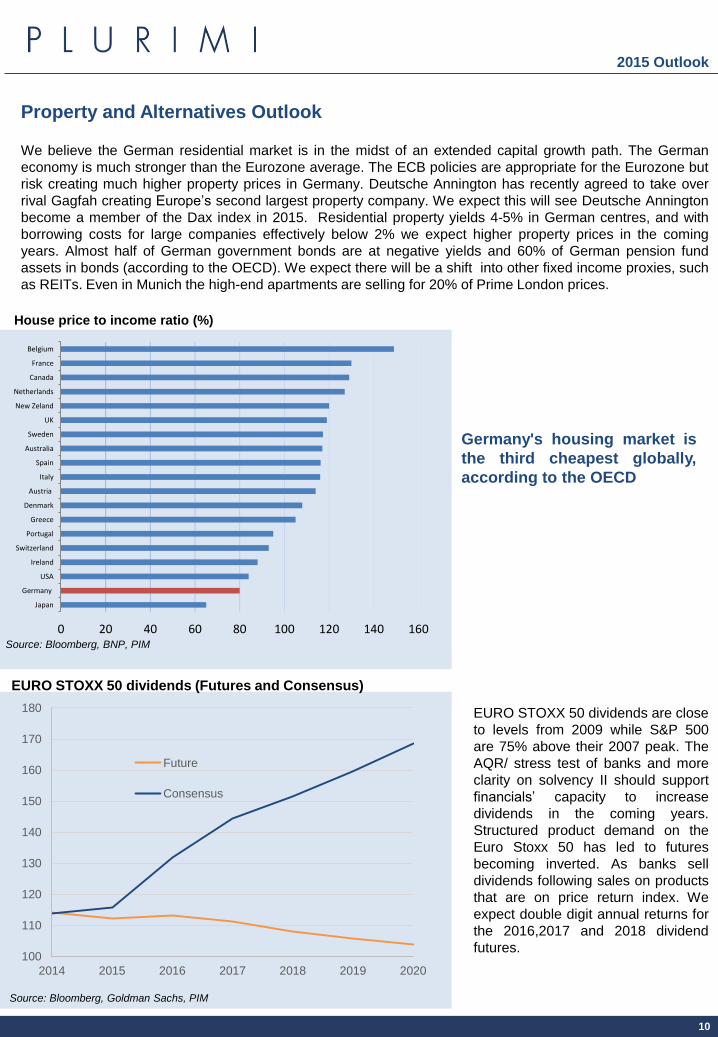

EURO STOXX 50 dividends are close

to levels from 2009 while S&P 500

are 75% above their 2007 peak. The

AQR/ stress test of banks and more

clarity on solvency II should support

financials’ capacity to increase

dividends in the coming years.

Structured product demand on the

Euro Stoxx 50 has led to futures

becoming inverted. As banks sell

dividends following sales on products

that are on price return index. We

expect double digit annual returns for

the 2016,2017 and 2018 dividend

futures.

Germany's housing market is

the third cheapest globally,

according to the OECD

0 20 40 60 80 100 120 140 160

Japan

Germany

USA

Ireland

Switzerland

Portugal

Greece

Denmark

Austria

Italy

Spain

Australia

Sweden

UK

New Zeland

Netherlands

Canada

France

Belgium

House price to income ratio (%)

Property and Alternatives Outlook

We believe the German residential market is in the midst of an extended capital growth path. The German

economy is much stronger than the Eurozone average. The ECB policies are appropriate for the Eurozone but

risk creating much higher property prices in Germany. Deutsche Annington has recently agreed to take over

rival Gagfah creating Europe’s second largest property company. We expect this will see Deutsche Annington

become a member of the Dax index in 2015. Residential property yields 4-5% in German centres, and with

borrowing costs for large companies effectively below 2% we expect higher property prices in the coming

years. Almost half of German government bonds are at negative yields and 60% of German pension fund

assets in bonds (according to the OECD). We expect there will be a shift into other fixed income proxies, such

as REITs. Even in Munich the high-end apartments are selling for 20% of Prime London prices.

10

2015 Outlook

Source: Bloomberg, BNP, PIM

Source: Bloomberg, Goldman Sachs, PIM

EURO STOXX 50 dividends (Futures and Consensus)

13

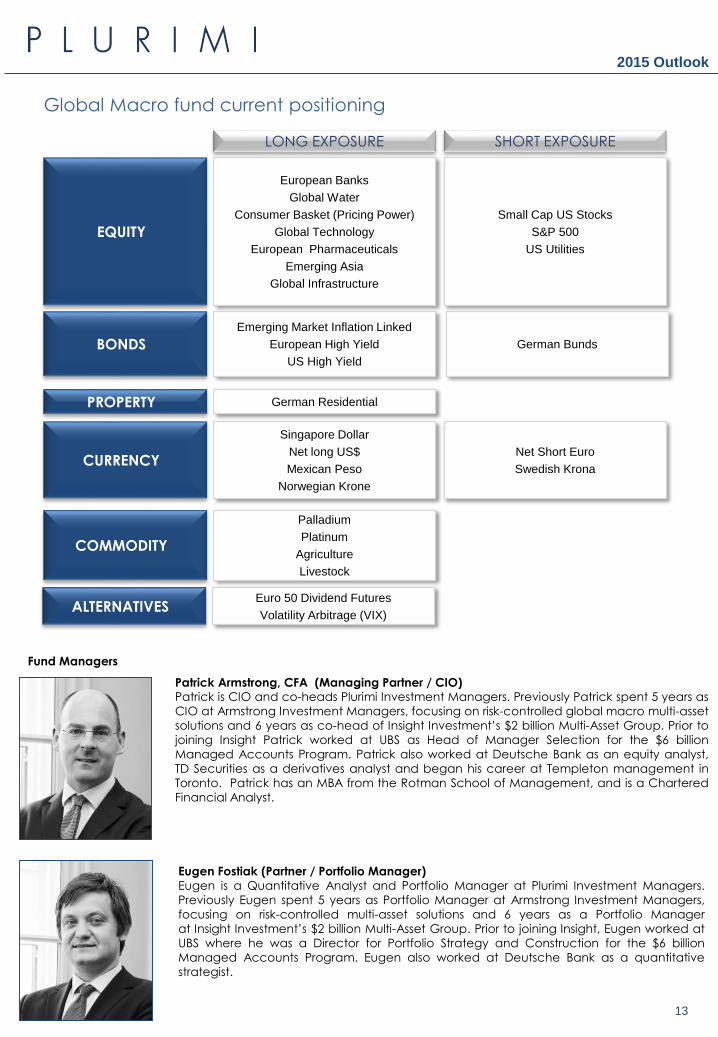

LONG EXPOSURE SHORT EXPOSURE

EQUITY

BONDS

ALTERNATIVES

PROPERTY

CURRENCY

COMMODITY

European Banks

Global Water

Consumer Basket (Pricing Power)

Global Technology

European Pharmaceuticals

Emerging Asia

Global Infrastructure

Small Cap US Stocks

S&P 500

US Utilities

Emerging Market Inflation Linked

European High Yield

US High Yield

Euro 50 Dividend Futures

Volatility Arbitrage (VIX)

German Residential

Singapore Dollar

Net long US$

Mexican Peso

Norwegian Krone

Net Short Euro

Swedish Krona

Palladium

Platinum

Agriculture

Livestock

Global Macro fund current positioning

2015 Outlook

German Bunds

Fund Managers

Patrick Armstrong, CFA (Managing Partner / CIO)Patrick is CIO and co-heads Plurimi Investment Managers. Previously Patrick spent 5 years as

CIO at Armstrong Investment Managers, focusing on risk-controlled global macro multi-asset

solutions and 6 years as co-head of Insight Investment’s $2 billion Multi-Asset Group. Prior to

joining Insight Patrick worked at UBS as Head of Manager Selection for the $6 billion

Managed Accounts Program. Patrick also worked at Deutsche Bank as an equity analyst,

TD Securities as a derivatives analyst and began his career at Templeton management in

Toronto. Patrick has an MBA from the Rotman School of Management, and is a Chartered

Financial Analyst.

Eugen Fostiak (Partner / Portfolio Manager)

Eugen is a Quantitative Analyst and Portfolio Manager at Plurimi Investment Managers.

Previously Eugen spent 5 years as Portfolio Manager at Armstrong Investment Managers,

focusing on risk-controlled multi-asset solutions and 6 years as a Portfolio Manager

at Insight Investment’s $2 billion Multi-Asset Group. Prior to joining Insight, Eugen worked at

UBS where he was a Director for Portfolio Strategy and Construction for the $6 billion

Managed Accounts Program. Eugen also worked at Deutsche Bank as a quantitative

strategist.

Utilities

Tech

MaterialsIndustrial

Staples

Discretionary

Energy

Health

Financial

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0 2 4 6 8 10 12 14 16 18 20

US Equity Valuations by Sector

Excess Profitability (RoE - CoE)

log (

P/B

V)

11

2015 Outlook

APPENDIX

Source: Bloomberg, PIM

The US market has moved from 8 out of 9 sectors trading

below fair value in 2008 to 3 out of 9 in 2014.

Within the US we are long technology which has seen higher

profitability match higher valuations, while utilities have

seen valuations increase while excess profit has fallen

slightly.

NOTES

13

Issued by Plurimi Investment Managers (“PIM”), a trading name of Plurimi Wealth LLP

which is authorized and regulated by the Financial Conduct Authority with FCA number

466728. This presentation is aimed at "Investment Professionals" as described in Article

19 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2001 (as

amended). It is aimed mainly at "authorised" and "exempt" persons as defined in The

Financial Services and Markets Act 2000. Any other recipients of this presentation

should disregard its contents and should not rely on it. The information contained in this

presentation is given without any liability whatsoever to PIM or any of its related entities

or their respective members or officers, and is not intended to constitute legal, tax or

accounting advice or opinion. No representation or warranty, expressed or implied, is

made as to the accuracy, completeness or thoroughness of the content of the

information. The recipient should consult with its own legal, tax or accounting advisers as

to the accuracy and application of the information contained herein and should conduct

its own due diligence and other enquiries in relation to such information. The information

in this presentation has not been independently verified by PIM. PIM disclaims any

responsibility for any errors or omissions in such information, including the financial

calculations, projections and forecasts set forth herein. No representation or warranty is

made by or on behalf of PIM that any projection, forecast, calculation, forward-looking

statement, assumption or estimate contained in this presentation should or will be

achieved. This presentation does not carry any right of publication. This presentation is

incomplete without reference to, and should be viewed solely in conjunction with, the oral

briefing provided by PIM. Neither this presentation nor any of its contents may be

reproduced or used for any other purpose without the prior written consent of PIM.

Disclaimer

This fact sheet is aimed at authorised and expert persons only under the Financial Services and Markets Act 2000 and members of the public should disregard its contents. Clients

should be informed of the risks of investing. The value of your investment may fall as well as rise and is not guaranteed. Past performance is not an indicator of future performance. Full

details of the risks can be found in the Fund Prospectus which can be obtained from PIM. Nothing in this document should be construed as investment advice. Issued by Plurimi

Investment Managers (“PIM”), a trading name of Plurimi Wealth LLP which is authorized and regulated by the Financial Conduct Authority with FCA number 466728.

11 Waterloo Place, London, SW1Y 4AU United Kingdom +44 (0) 207 484 3340 [email protected] www.plurimi.com