Jerry Luftman Ph.D.

SIM VP Chapter Relations & Academic Affairs, & NJ Chapter President Emeritus

Professor & Executive Director

Global Institute for IT Management

www.globaliim.com

201-787-9509

2012 IT TRENDS

Economy

Globalization

Sourcing Models

(+ aging workforce, Millennials)

Natural Disasters

Politics

New Markets

Terrorism/War(s)

Big Data/BI

Mobile, Social NW

Consumerization,

BYOD, Apps

Cloud/Virtualization

THE

PERFECT STORM

IT

Global Institute for IT Management

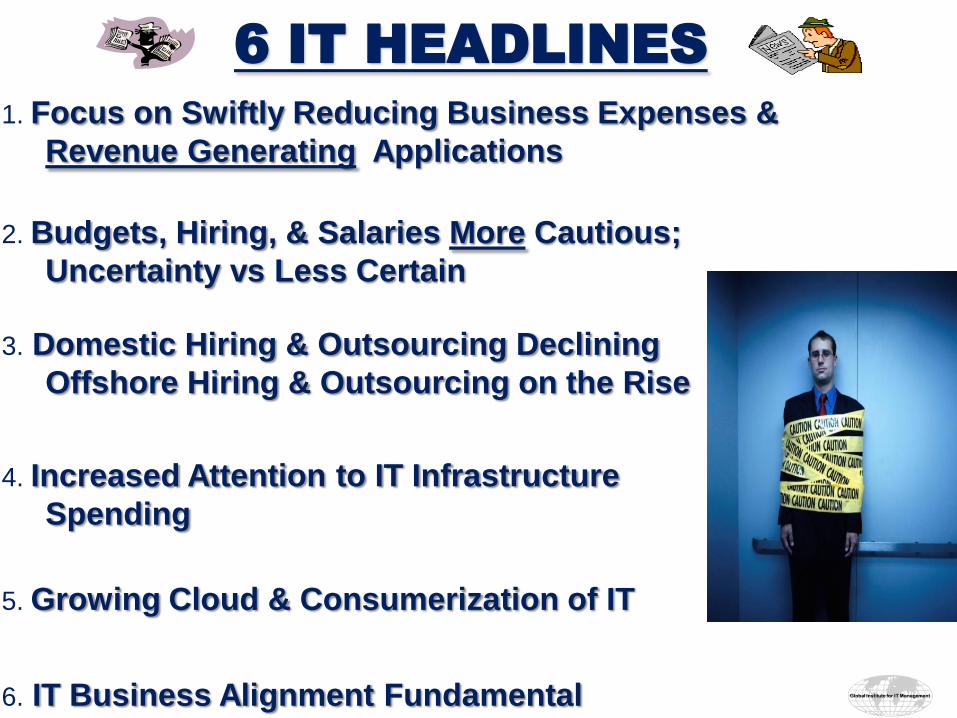

6 IT HEADLINES

1. Focus on Swiftly Reducing Business Expenses &

Revenue Generating Applications

4. Increased Attention to IT Infrastructure

Spending

5. Growing Cloud & Consumerization of IT

2. Budgets, Hiring, & Salaries More Cautious;

Uncertainty vs Less Certain

3. Domestic Hiring & Outsourcing Declining

Offshore Hiring & Outsourcing on the Rise

6. IT Business Alignment Fundamental

TOP 10 2012 IT MANAGEMENT CONCERNS

1 (4) Business Productivity and Cost Reduction

2 (1) Business & IT alignment

3 (2) Business Agility & Speed to Market

4 (9) Revenue Generating IT innovations

5 (10) IT Cost Reduction

6 (5) IT Strategic Planning

7 (3) Business Process Management & Reengineering

8 (7) Enterprise Architecture/ Infrastructure Capability

9 (8) Security and Privacy

10 (6) IT Reliability and Efficiency

(2011)

1 (1) Big Data, Business Intelligence

2 (2) Cloud Computing (SaaS, PaaS, IaaS)

3 (3) Enterprise Resource Planning (ERP) systems

4 (8) Collaborative and Workflow tools

5 (5) Customer Relationship Management (CRM)

6 (4) Mobile and Wireless Applications

7 * BYOD (Bring Your Own Device)

8 (9) (EAI/EAM) Enterprise Application Integration/Management

9

(16) Business Process Management Systems

10 * Apps Development

TOP 5 APPLICATIONS &

TECHNOLOGIES 2012

(2011) New* OFF: Virtualization, Continuity Planning

2012 IT BUDGET (ACTUAL)

2012

52%

2012 = 2011

2012 < 2011

2012 > 2011

47.9%

2012 IT BUDGET (ACTUAL)

2012 (2011) (2010) (2009) (2008)

(2007)

52% (44%)

(39%)

2012 = 2011 17.6% (27%) (31%) (23%) (28%) (17%)

2012 < 2011 34.5% (17%) (35%) (52%) (26%) (22%)

2012 > 2011

47.9% (56%) (34%) (25)% (46%)

(61%)

2013 IT BUDGET(PROJECTED)

(2011) 54.2% (52.1%)

2013 = 2012; 32.4%

(17.6%)

2013 < 2012; 21.8%

(34.5%)

2013 > 2012; 45.8%

(47.9%)

2012 IT BUDGET ALLOCATION

(ACTUAL) 2012 (2011) (2010) (2009)

(2008)

*Hardware, Network , Software (outsourced a new choice added to 2011)

60 (59) % on people; but revenue down

IT staff is 6.5% of overall staff

Hardware, Network, Software, Facilities,

Depreciation (In-House); 24%

(32%) (32%) (33%)

Hardware, Network , Software

(Outsourced-Domestic);

14%

Hardware, Network, Software

(Outsourced-Offshore); 2%

Internal Staff - Domestic; 33%

(38%) (43%) (39%)

(35%)

Internal Staff - Offshore; 6%

(2%) (3%) (4%)

Outsourced Staff - Domestic; 8%

(3%) (7%) (8%)

Outsourced Staff - Offshore; 3%

(2%) (5%) (4%)

Consulting Services; 9%

(11%) (10%) (12%)

*

*

(12%)

36% Outsourced

31% Domestic

5% Offshore

(28%)

(18.2%)

*

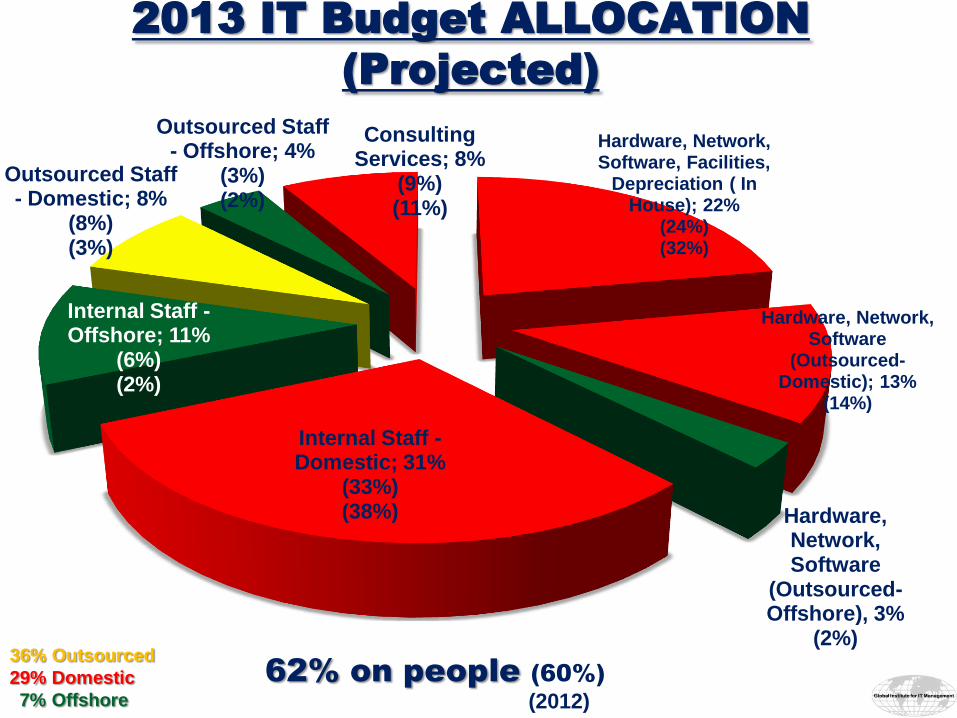

2013 IT Budget ALLOCATION

(Projected)

(2012)

62% on people (60%)

Hardware, Network, Software, Facilities,

Depreciation ( In House); 22%

(24%) (32%)

Hardware, Network, Software

(Outsourced-Domestic); 13%

(14%)

Hardware, Network, Software

(Outsourced-Offshore), 3%

(2%)

Internal Staff - Domestic; 31%

(33%) (38%)

Internal Staff - Offshore; 11%

(6%) (2%)

Outsourced Staff - Domestic; 8%

(8%) (3%)

Outsourced Staff - Offshore; 4%

(3%) (2%)

Consulting Services; 8%

(9%) (11%)

36% Outsourced

29% Domestic

7% Offshore

IT Budget allocation for Offshore Outsourcing

0

1

2

3

4

5

6

7

1.7

4.2 4.0

3.3

4.0

5.0 5.0%

2% 1% 5%

2.0%

2005 2006 2007 2008 2009 2010 2011 2013 (project)

2012

7.0%

2012 OFFSHORE OUTSOURCING

BUDGET ALLOCATED BY GEOGRAPHY

(2011)

India; 43% (58%)

China; 2% (10%)

Brazil; 2% (2%)

Caribbean; 0% (4%)

Mexico; 5% (5%)

Western EU; 13% (6%)

Eastern EU; 6% (4%)

Phillipines; 12% (4%)

Russia; 1% (3%)

Other, 16%

PERCENTAGE OF 2012 BUDGET ALLOCATED

TO INTERNAL CLOUD

> 10%

12%

(20%)

1 - 5%

40%

(21%)

Average: 5% (6% )

(2011)

0-1%; 37% (43%)

1-2; 20% (6%)

2-3; 7% (5%)

3-4; 2% (5%)

4-5; 11% (5%)

6-10; 11% (17%)

11-15; 4% (6%)

16-20; 1% (4%)

21-25; 3% (4%)

>25%; 4% (6%)

PERCENTAGE OF 2012 BUDGET

ALLOCATED TO EXTERNAL CLOUD

> 5%

16%

(19%)

Average: 4% (5%)

1 - 5%

43%

(40%)

(2011)

0-1%; 41% (41%)

1-2; 19% (16%)

2-3; 7% (6%)

3-4; 3% (9%)

4-5; 14% (15%)

6-10; 10% (8%)

11-15; 1% (5%)

16-20; 1% (5%)

21-25; 1% (0%)

>25%; 3% (1%)

0.00

2.00

4.00

6.003.60 3.60 3.50 3.82 3.83 3.87 3.55

4.94

3.84 Avg.

2005 2006 2008 2007 2009 2012 2010 2011

PERCENTAGE OF CORPORATE

REVENUE ALLOCATED TO IT BUDGET

IT BUDGET AS PERCENT OF REVENUE BY

INDUSTRY CLASSIFICATION

Information Technology 13.67% 10.19%

Finance/Banking 8.12% 6.67%

Transportation 6.1% 4.00%

Manufacturing 2.0% 1.70%

Government-State/Local 2.75% 9.45%

Business Services 12.12% 4.37%

Education 4.78% 4.04%

Aerospace 9.37% 2.50%

Data Processing Services 11.5% 10.19%

Insurance 8.16% 6.67%

3.55 Average

2011 2012

4.94

0.00

2.50

5.00

7.50 5.80 6.41 7.11 5.20 5.50 5.51 5.23

2012 IT STAFF TURNOVER RATE

5.82% Avg.

2006 2007 2008 2009 2012 2010 2011

2012 = 2011 29%

2012 > 2011

60%

2012 < 2011 11%

2012 IT STAFF SALARIES

(ACTUAL)

(2011: 67%)

(2010: 42%)

(2009: 34%)

(2008: 78%)

(2011: 26%)

(2010: 41%)

(2009: 47%)

(2008: 18%)

(2011: 8%)

(2010: 17%)

(2009: 19%)

(2008: 4%)

89%

(93%)

(96%)

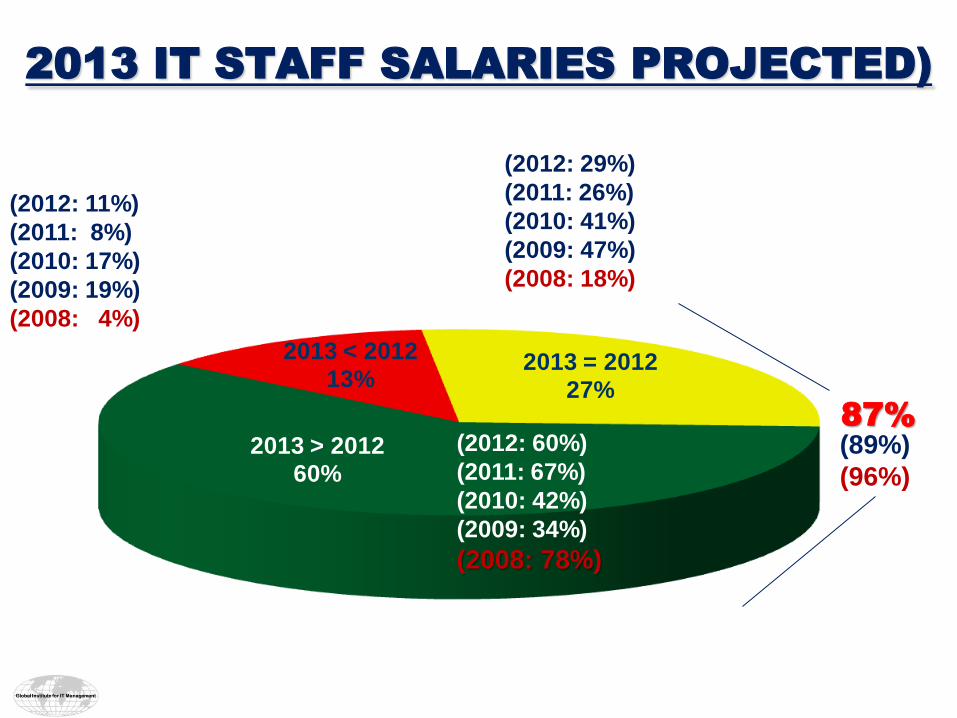

2013 = 2012 27%

2013 > 2012 60%

2013 < 2012 13%

2013 IT STAFF SALARIES PROJECTED)

(2012: 60%)

(2011: 67%)

(2010: 42%)

(2009: 34%)

(2008: 78%)

(2012: 29%)

(2011: 26%)

(2010: 41%)

(2009: 47%)

(2008: 18%)

(2012: 11%)

(2011: 8%)

(2010: 17%)

(2009: 19%)

(2008: 4%)

87%

(89%)

(96%)

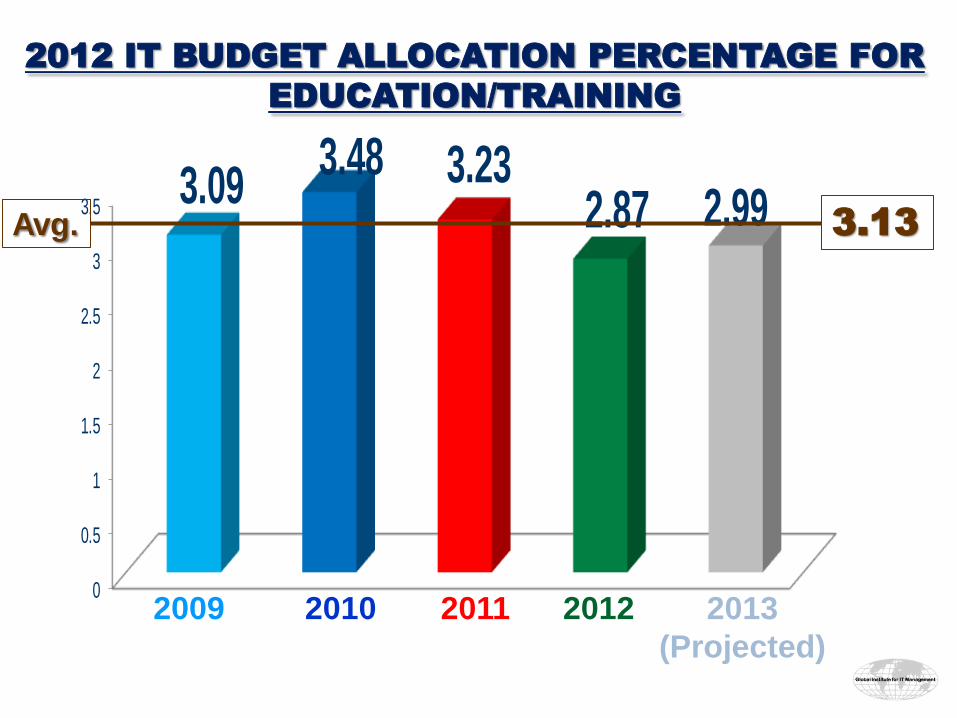

2012 IT BUDGET ALLOCATION PERCENTAGE FOR

EDUCATION/TRAINING

0

0.5

1

1.5

2

2.5

3

3.53.09

3.48 3.23 2.87 2.99

2009 2010 2011 2013

(Projected)

3.13 Avg.

2012

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

CEO CFO COO BUE Other

27%

19% 10%

2%

CIO OR SENIOR IT EXECUTIVE

REPORTS TO

43% 27% 16% 7% 7% Avg.

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

200

5

20

06

20

07

20

08

20

09

20

10

20

11

20

12

200

5

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

43%

0.00

1.00

2.00

3.00

4.00

5.00

6.00

3.60 4.10 4.30

4.60 5.10

4.45

5.96

HOW LONG (YEARS) HAS YOUR CIO (OR

SENIOR IT EXECUTIVE) HELD THEIR

POSITION?

4.59 Avg.

2006 2008 2007 2009 2012 2010 2011

> NFL Quarterback CEO: 8 years (Booz)

0%

5%

10%

15%

20%

25%

30%

HOW CIOS SPEND THEIR TIME

2007: 78% 2008: 82% 2009: 72% 2012: 77% 2010: 74%

7% 8% 7% 10% 11%

22%

13%

4% 6%

15%

Average: *77%

7% 8% 10%

1%

11%

24%

13%

8% 6%

12%

*Non Technical Time:

*

* *

*

* * *

2011: 77%

0%

10%

20%

30%

40%

50%

60%

70%

Within yourcompany's ITorganization

Outside yourcompany from an

external ITorganization

Within yourcompany butoutside of IT

Outside yourcompany from an

organizationoutside of IT

38%

54%

4% 4%

31%

61%

4% 3%

37%

54%

5% 5%

YOUR CURRENT CIO WAS HIRED FROM

2010 2011 2010 2011 2010 2011 2010 2011 2012 2012 2012 2012

2012 IT ORGANIZATION

0%

10%

20%

30%

40%

50%

60%

70%

80%

61%

5%

26%

6% 2%

61%

3%

33%

3% 1%

2006 2007 2008 2009 2012 2010 2011

Never Sometimes Always

CIO 2% 8% 90%

CEO 21% 57% 22%

CFO 9% 61% 30%

COO 34% 43% 23%

Bus. Unit Exec 19% 69% 12%

Other IT Exec 15% 49% 36%

ENGAGED IN ALLOCATION OF IT INFRASTRUCTURE RESOURCES

ENGAGED IN ALLOCATION OF IT APPLICATION RESOURCES

Never Sometimes Always

CIO 2% 12% 86%

CEO 22% 53% 25%

CFO 8% 61% 31%

COO 31% 47% 22%

Bus. Unit Exec 16% 85% 19%

Other IT Exec 13% 56% 31%

TOP IT METRICS

2013 2012

Projects delivered on time 1 1

Project ROI 2 4

Projects delivered on budget 3 2

SLA targets 4 3

Productivity improvement 5 6

Increased customer/client satisfaction 6 5

Revenue growth 7 7

Innovation/new ideas 8 10

Increases in new products/services 9 8

Improved decision making 10 9

ROE 11 12

Industry specific measurements 12 11

Lower error rates 13 13

Earnings per share 14 14

WHY DISCUSS IT-BUSINESS

ALIGNMENT? STILL

6. How do you know if your alignment is “appropriate”?

7. Can we move from a descriptive vehicle to a prescriptive

vehicle?

4. In search of mythical silver bullet

2. Too often considered just IT aligned with the business

3. Semantics: alignment vs fused, linked, integrated, fit,

harmony, converged, matched, melded, interwoven…

5. Focusing on infrastructure/architecture

1. Consider their organizations are not misaligned

Global Institute for IT Management

·

·

·

·

·

·

-

·

-

-

- Inter -

-

IT BUSINESS ALIGNMENT MATURITY CRITERIA

PARTNERSHIP

•Business Perception of IT Value

•Role of IT in Strategic Business

Planning

•Shared Goals, Risk,

Rewards/Penalties

•IT Program Management

•Relationship/Trust Style

•Business Sponsor/Champion

SCOPE &

ARCHITECTURE

•Traditional, Enabler/Driver,

External

•Standards Articulation

•Architectural Integration:

- Functional Organization

-Enterprise -Inter enterprise

•Architectural Transparency,

Agility, Flexibility

•Manage Emerging Tech.

SKILLS

by Business

•Liaison(s) effectiveness

COMMUNICATIONS

•Understanding of Business

by IT

•Understanding of IT

•Inter/Intra organizational

Learning/Education

•Protocol Rigidity

•Knowledge Sharing

COMPETENCY/VALUE

MEASUREMENTS

•IT Metrics

•Business Metrics

•Balanced Metrics

•Service Level Agreements

•Benchmarking

•Formal Assessments/Reviews

•Continuous Improvement

GOVERNANCE

•Organization Structure

•IT Investment Management

•Prioritization Process

•Business Strategic Planning

•IT Strategic Planning

•Budgetary Control

•Steering Committee(s)

•Cultural Locus of Power

•Change Readiness

•Innovation, Entrepreneurship

•Management Style

•Career crossover;

training/education

•Hiring and retaining

Interpersonal Environment •Social, Political, Trusting

Global Institute for IT Management

HIGHEST ELEMENTS Averages

LOWEST ELEMENTS Averages

1. Career Crossover 2.79

2. Change Readiness 2.84

3. Knowledge Sharing 2.86

4. Balanced Metrics 2.88

5. Understanding of IT by business 2.89

3.09 3.09

1. Demonstrated Contribution of IT to Business 3.48

2. Protocol Rigidity 3.36

3. Prioritization Process 3.32

4. Business Sponsor/Champion 3.23

Global Institute for IT Management

SAM Performance Framework

Communic.

Competency

Governance

Partnership

Tech Scope

Skills/HR

Strategic

Alignment

Maturity

Performance

Global Institute for IT Management

Outsourcing

22%

Decentralized

5%

Matrixed

25%

Centralized

Networked

30%

17%

Federated/Hybrid

2.98

3.60

2.69

2.87

Alignment Maturity 3.09

3.67

Global Institute for IT Management

Organization Structure

CIO Reporting Structure

President,

Chairman,

CEO

56 % 30 %

9 %

5 %

COO

CFO

Business

Unit Exec

3.45

3.36

3.25

3.01

Alignment Maturity 3.09 Global Institute for IT Management

• Technical Leadership Certificates

17. Big Data/Business Intelligence/Knowledge Mgt

18. Managing Cloud Computing

19. IT Infrastructure Integration

20. IT Security Management

21. Managing Social Networking/Mobile Computing

22. Project Management

23. Software Engineering

24. Technology Enabled Learning

• General Management Certificates 25. Effective English Business Communications

26. IT Business/Management Considerations (e.g.,

finance, organizational behavior, accounting,

statistics, economics, leadership)

Foundation

& IT Management

Certificates

26

• See our web: www.globaliim.com

1. 4 course IT Foundation Certificate (Mini MBA)

• Leadership

• Managing IT Trends & Emerging Technologies

• IT Resource Management

• IT Strategy

• Executive Certificates

2-9. IT in Industry (e.g., Finance, Pharmaceutical,

Healthcare, Manufacturing, Telecom,

Government, Transportation, Petro)

10. IT for the Business Executive

11. IT Human Resource Considerations

12. IT Management Consulting

13. Business Process Management

14. Supply Chain Management

15. Managing IT Legal Issues

16. Managing IT Vendors & Outsourcing (also for

non-IT)

Global Institute for IT Management