Bailouts, Bankruptcies and Bailouts, Bankruptcies and D&O UnderwritingD&O Underwriting

MODERATOR:

Marc London, MBA, Senior Vice President, Marsh USA

PANELISTS:

David Bradford, MBA, Executive Vice President & Editor-In-Chief, Advisen, Ltd.

Vincent J. Dowling, Jr., Managing Partner, Dowling & Partners Securities, LLC

Stephen R. Guglielmo, Lead Underwriter, HCC Global Financial Products

Michael Karmilowicz, Vice President, Hartford Financial Products

David Lynders, MBA, Vice President, Axis Capital

Christine S. Montelbano, MBA, Regional Vice President, Travelers Bond & Financial Products

Jeremy Perler, CFA, CPA, Co-Head of CFRA Accounting Research, RiskMetrics Group

Salvatore Pollaro, MBA, Executive Vice President, Zurich North America, Specialties`

2009 D&O2009 D&O SymposiumSymposium

Bankruptcies and Securities Bankruptcies and Securities Class Action SuitsClass Action Suits

Dave Bradford

Executive Vice President

Advisen Ltd.

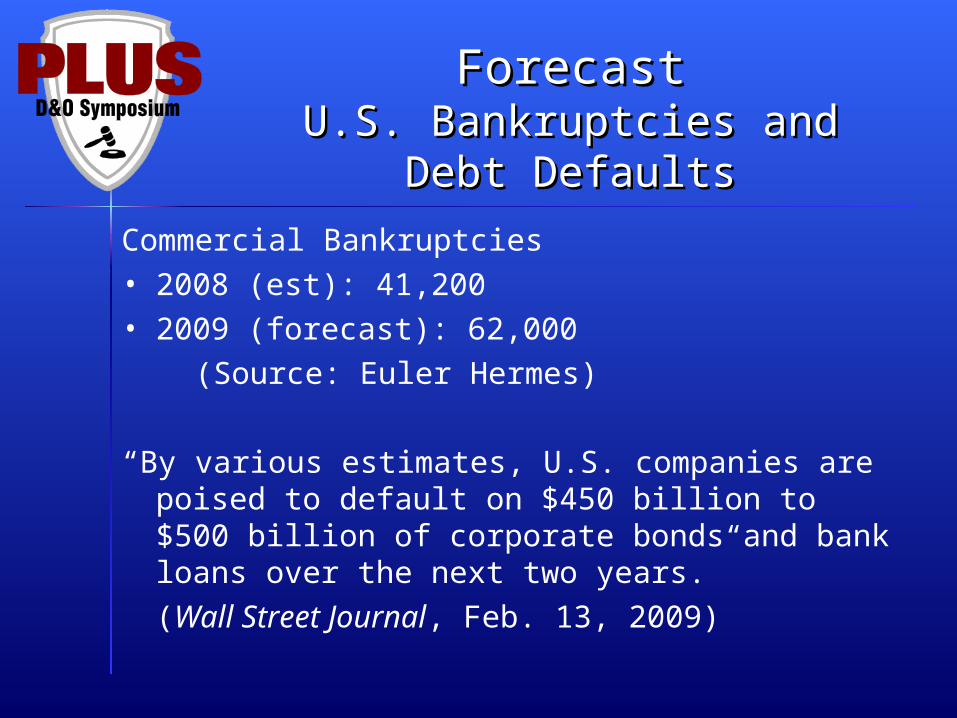

ForecastForecastU.S. Bankruptcies and Debt U.S. Bankruptcies and Debt

DefaultsDefaults

Commercial Bankruptcies• 2008 (est): 41,200• 2009 (forecast): 62,000

(Source: Euler Hermes)

“By various estimates, U.S. companies are poised to default on $450 billion to $500 billion of corporate bonds and bank loans over the next two years.”

(Wall Street Journal, Feb. 13, 2009)

Commercial Bankruptcy Commercial Bankruptcy FilingsFilings

0

10000

20000

30000

40000

50000

60000

Source: U.S. Bankruptcy Courts

Bankruptcies & SCASBankruptcies & SCAS

0

10000

20000

30000

40000

50000

60000

0

100

200

300

400

500

600

SCAS Comm Bankruptcies

All Commercial Bankruptcy FilingsAll Securities Class Action Suits Filed

Sources: Advisen MSCAd, U.S. Bankruptcy Courts

Bankruptcies & SCASBankruptcies & SCASLarge Public Bankruptcy Filings

All Securities Class Action Suits Filed

0

20

40

60

80

100

120

0

100

200

300

400

500

60019

95

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

SCAS Lg Pub Bankrupt

Sources: Web BRD, Advisen MSCAd

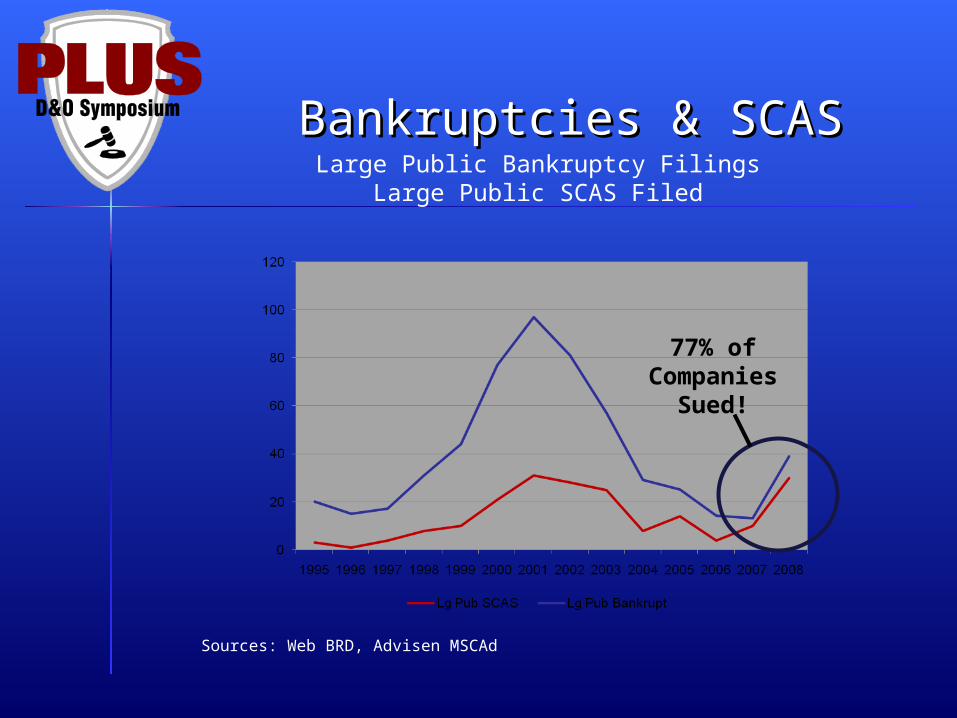

Bankruptcies & SCASBankruptcies & SCASLarge Public Bankruptcy Filings

Large Public SCAS Filed

Sources: Web BRD, Advisen MSCAd

Bankruptcies & SCASBankruptcies & SCASLarge Public Bankruptcy Filings

Large Public SCAS Filed

Sources: Web BRD, Advisen MSCAd

77% ofCompanies

Sued!

Who Has Failed?Who Has Failed?Large Public Company Bankruptcies

Sources: Web BRD, Advisen AMF

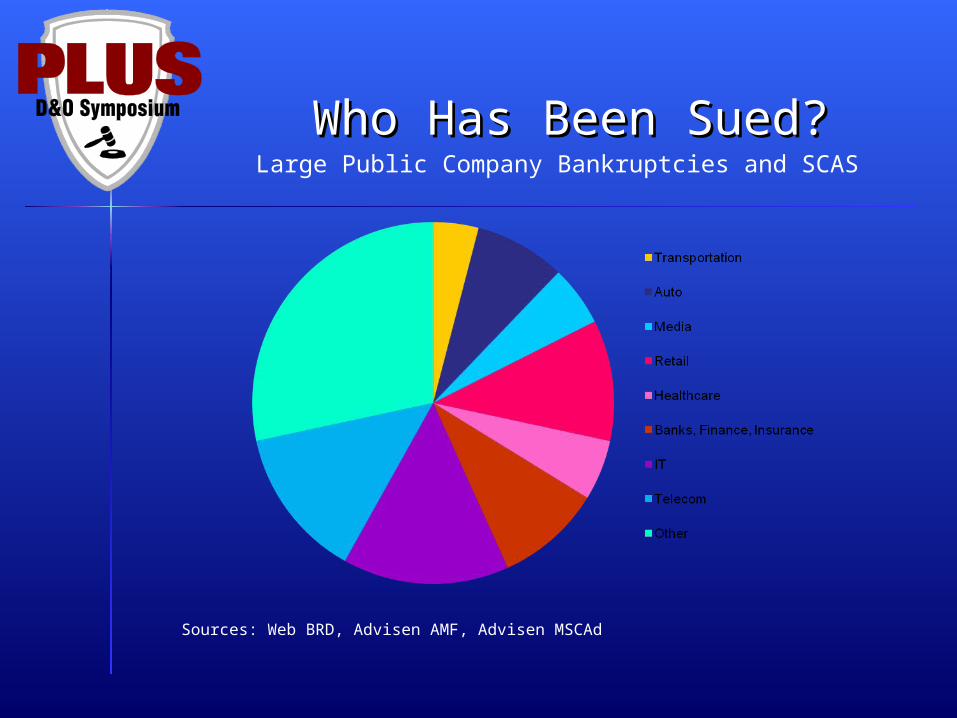

Who Has Been Sued?Who Has Been Sued?Large Public Company Bankruptcies and SCAS

Sources: Web BRD, Advisen AMF, Advisen MSCAd

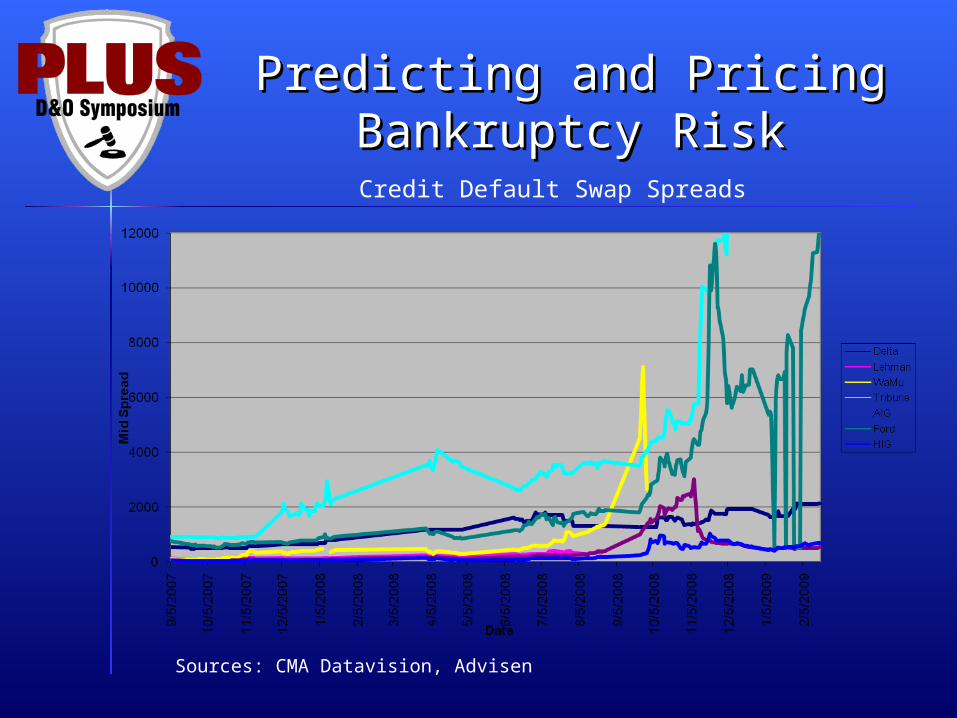

Predicting and Pricing Predicting and Pricing Bankruptcy RiskBankruptcy Risk

Credit Default Swap Spreads

Sources: CMA Datavision, Advisen

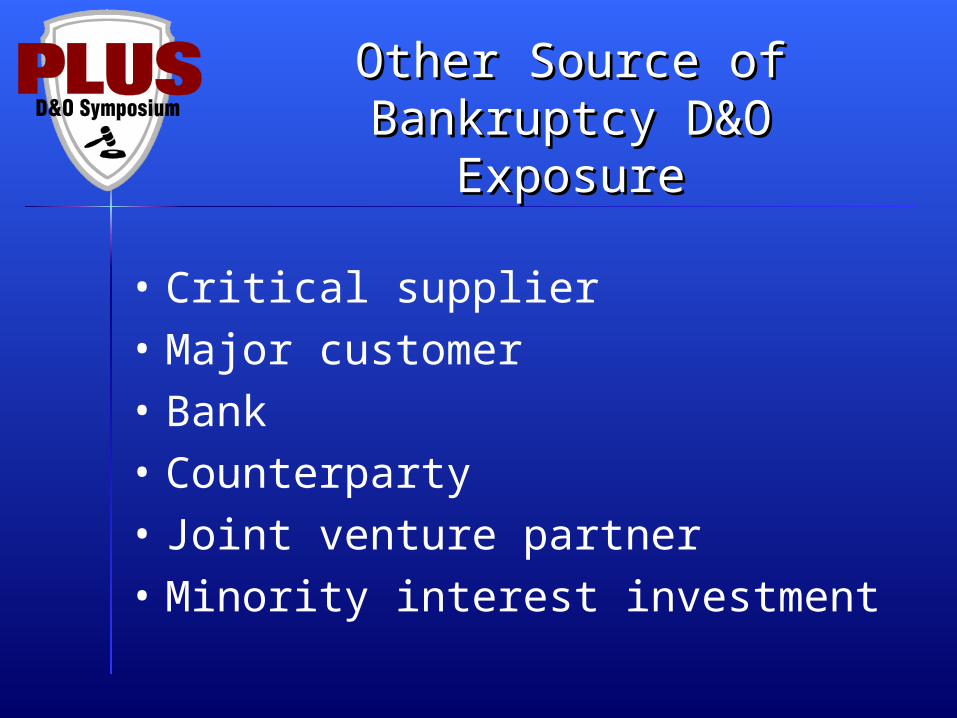

Other Source of Other Source of Bankruptcy D&O ExposureBankruptcy D&O Exposure

• Critical supplier

• Major customer

• Bank

• Counterparty

• Joint venture partner

• Minority interest investment

Economy Under Stress!Economy Under Stress!

• Auto sales, industrial production, consumer spending, and confidence measures at, or near, record lows

• S&P 500 down 38% in 2008

• 3.6 million U.S. jobs lost

• U.S. economy to contract 0.5% - 1.3%

New York City ~ February 25 & 26, 2009

The New WorldThe New World

Vincent J. Dowling, Jr.

Dowling & Partners Securities

Capital Lost In 2008Capital Lost In 2008

• The Net Result = We Estimate Of $55-75BB Of Capital Lost in ‘08 Investment Losses

• 50-75% Of Excess Capital Lost During 2008

$125 $100

$75

$43

$27 $27

$25$6

$25$5

$6

$70

$0

$25

$50

$75

$100

$125

Excess Capital @ YE07

H1-08 Change In Surplus

Excess Capital @ 6/30

Q3 A/T Op. Earnings, Ex. Cats

Q3 A/T Cats Q3 Investment/Other

losses

Excess Capital @ 9/30

Q4E Change (Range)

Est. Excess Capital @ YE07

US P&C INDUSTRY: 2008 CHANGE IN EXCESS CAPITALBased On Midpoint Of D&P's $100BB-150BB XS Capital Assumption At YE07

Increase

Decline

Industry Surplus GrowthIndustry Surplus Growth

$0

$100

$200

$300

$400

$500

$600

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

A

2008

E

2009

E

2010

E

P&C Industry Statutory Surplus ($, MM)

Stat Surplus

NPW

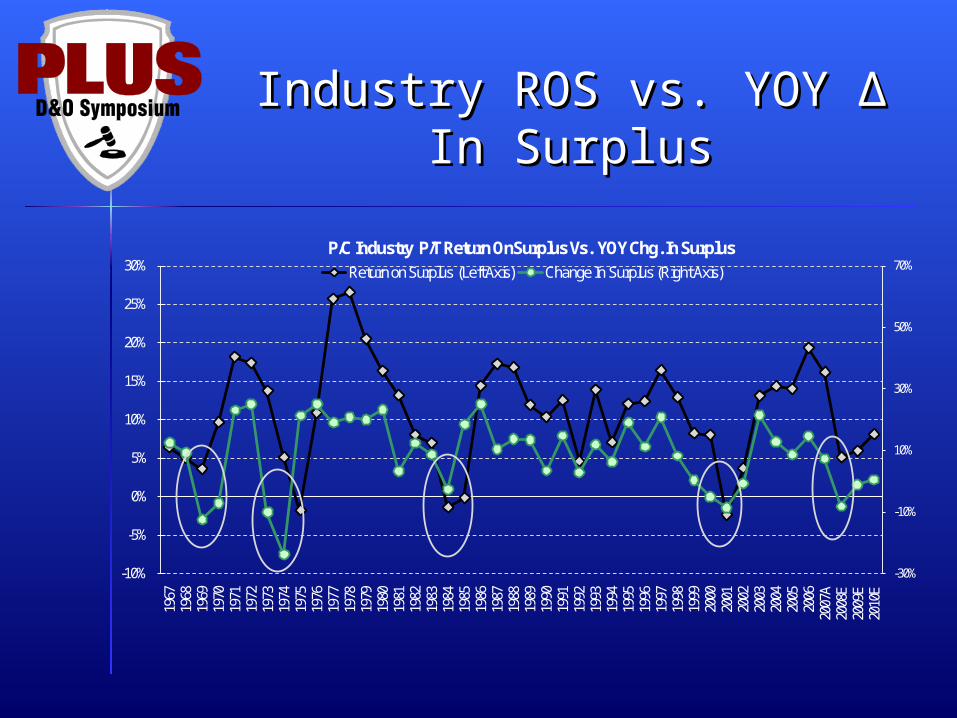

Industry ROS vs. YOY ∆ In Industry ROS vs. YOY ∆ In SurplusSurplus

-30%

-10%

10%

30%

50%

70%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

A20

08E

2009

E20

10E

P/C Industry P/T Return OnSurplus Vs. YOY Chg. In SurplusReturn on Surplus (Left Axis) Change In Surplus (Right Axis)

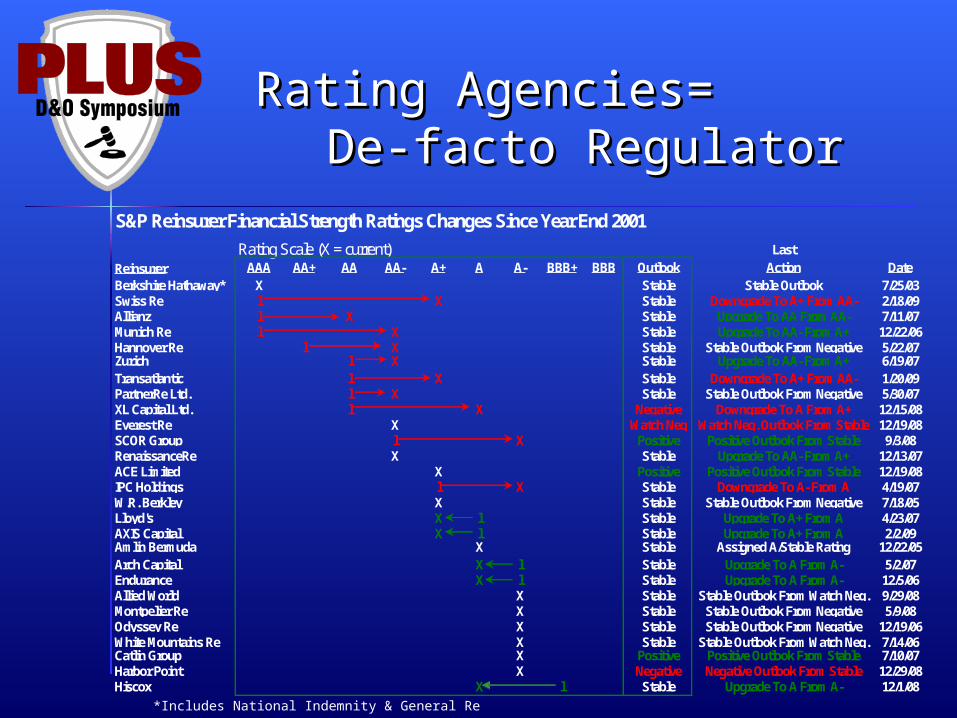

S&P Reinsurer Financial Strength Ratings Changes Since Year End 2001

Rating Scale (X = current) Last

Reinsurer AAA AA+ AA AA- A+ A A- BBB+ BBB Outlook Action DateBerkshire Hathaway* X Stable Stable Outlook 7/25/03Swiss Re l X Stable Downgrade To A+ From AA- 2/18/09Allianz l X Stable Upgrade To AA From AA- 7/11/07Munich Re l X Stable Upgrade To AA- From A+ 12/22/06Hannover Re l X Stable Stable Outlook From Negative 5/22/07Zurich l X Stable Upgrade To AA- From A+ 6/19/07Transatlantic l X Stable Downgrade To A+ From AA- 1/20/09PartnerRe Ltd. l X Stable Stable Outlook From Negative 5/30/07XL Capital Ltd. l X Negative Downgrade To A From A+ 12/15/08Everest Re X Watch Neg Watch Neg. Outlook From Stable 12/19/08SCOR Group l X Positive Positive Outlook From Stable 9/3/08RenaissanceRe X Stable Upgrade To AA- From A+ 12/13/07ACE Limited X Positive Positive Outlook From Stable 12/19/08IPC Holdings l X Stable Downgrade To A- From A 4/19/07W.R. Berkley X Stable Stable Outlook From Negative 7/18/05Lloyd's X l Stable Upgrade To A+ From A 4/23/07AXIS Capital X l Stable Upgrade To A+ From A 2/2/09Amlin Bermuda X Stable Assigned A/Stable Rating 12/22/05Arch Capital X l Stable Upgrade To A From A- 5/2/07Endurance X l Stable Upgrade To A From A- 12/5/06Allied World X Stable Stable Outlook From Watch Neg. 9/29/08Montpelier Re X Stable Stable Outlook From Negative 5/9/08Odyssey Re X Stable Stable Outlook From Negative 12/19/06White Mountains Re X Stable Stable Outlook From Watch Neg. 7/14/06Catlin Group X Positive Positive Outlook From Stable 7/10/07Harbor Point X Negative Negative Outlook From Stable 12/29/08Hiscox X l Stable Upgrade To A From A- 12/1/08

Rating Agencies= De-Rating Agencies= De-facto Regulatorfacto Regulator

*Includes National Indemnity & General Re

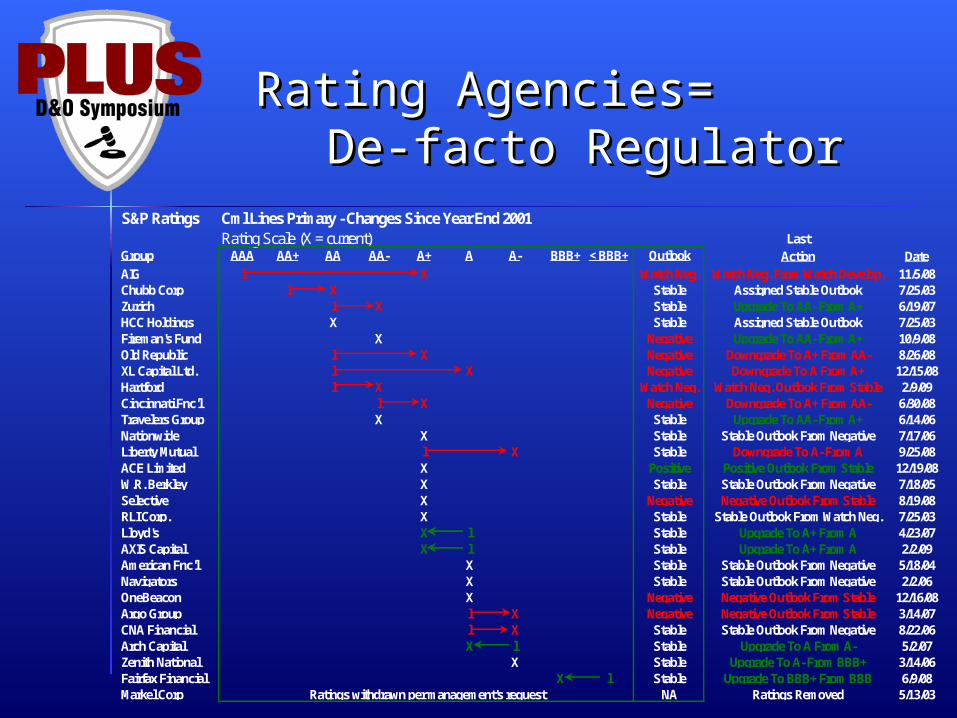

Rating Agencies= De-Rating Agencies= De-facto Regulatorfacto Regulator

S&P Ratings Cml Lines Primary - Changes Since Year End 2001Rating Scale (X = current) Last

Group AAA AA+ AA AA- A+ A A- BBB+ < BBB+ Outlook Action DateAIG l X Watch Neg. Watch Neg. From Watch Develop. 11/5/08Chubb Corp l X Stable Assigned Stable Outlook 7/25/03Zurich l X Stable Upgrade To AA- From A+ 6/19/07HCC Holdings X Stable Assigned Stable Outlook 7/25/03Fireman's Fund X Negative Upgrade To AA- From A+ 10/9/08Old Republic l X Negative Downgrade To A+ From AA- 8/26/08XL Capital Ltd. l X Negative Downgrade To A From A+ 12/15/08Hartford l X Watch Neg. Watch Neg. Outlook From Stable 2/9/09Cincinnati Fnc'l l X Negative Downgrade To A+ From AA- 6/30/08Travelers Group X Stable Upgrade To AA- From A+ 6/14/06Nationwide X Stable Stable Outlook From Negative 7/17/06Liberty Mutual l X Stable Downgrade To A- From A 9/25/08ACE Limited X Positive Positive Outlook From Stable 12/19/08W.R. Berkley X Stable Stable Outlook From Negative 7/18/05Selective X Negative Negative Outlook From Stable 8/19/08RLI Corp. X Stable Stable Outlook From Watch Neg. 7/25/03Lloyd's X l Stable Upgrade To A+ From A 4/23/07AXIS Capital X l Stable Upgrade To A+ From A 2/2/09American Fnc'l X Stable Stable Outlook From Negative 5/18/04Navigators X Stable Stable Outlook From Negative 2/2/06OneBeacon X Negative Negative Outlook From Stable 12/16/08Argo Group l X Negative Negative Outlook From Stable 3/14/07CNA Financial l X Stable Stable Outlook From Negative 8/22/06Arch Capital X l Stable Upgrade To A From A- 5/2/07Zenith National X Stable Upgrade To A- From BBB+ 3/14/06Fairfax Financial X l Stable Upgrade To BBB+ From BBB 6/9/08Markel Corp Ratings withdrawn per management's request NA Ratings Removed 5/13/03

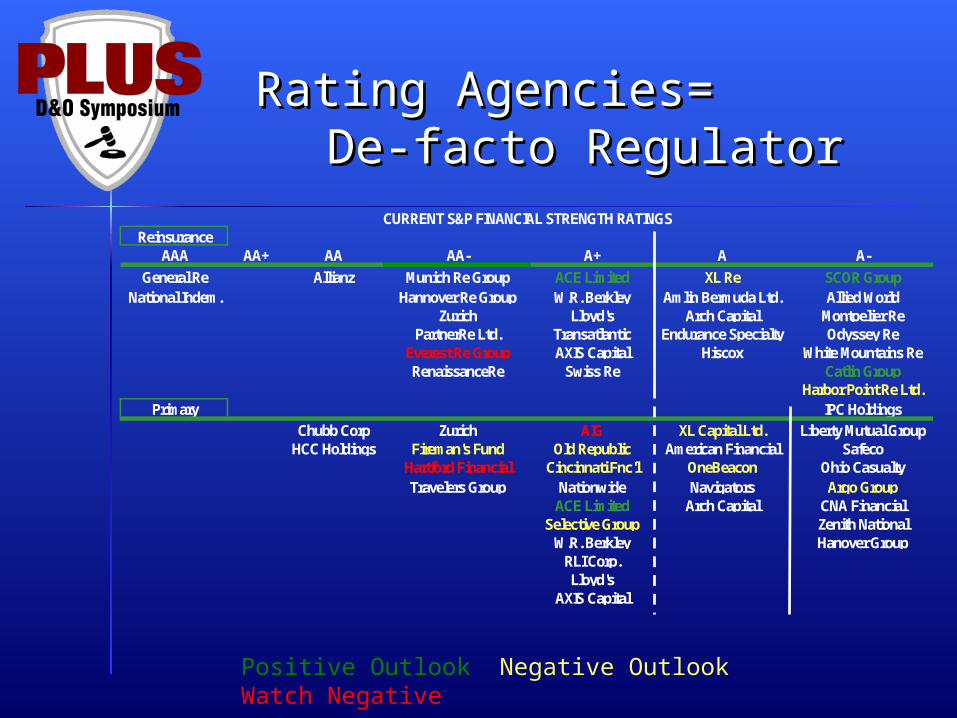

ReinsuranceAAA AA+ AA AA- A+ A A-

General Re Allianz Munich Re Group ACE Limited XL Re SCOR GroupNational Indem. Hannover Re Group W.R. Berkley Amlin Bermuda Ltd. Allied World

Zurich Lloyd's Arch Capital Montpelier RePartnerRe Ltd. Transatlantic Endurance Specialty Odyssey Re

Everest Re Group AXIS Capital Hiscox White Mountains ReRenaissanceRe Swiss Re Catlin Group

Harbor Point Re Ltd.Primary IPC Holdings

Chubb Corp Zurich AIG XL Capital Ltd. Liberty Mutual GroupHCC Holdings Fireman's Fund Old Republic American Financial Safeco

Hartford Financial Cincinnati Fnc'l OneBeacon Ohio CasualtyTravelers Group Nationwide Navigators Argo Group

ACE Limited Arch Capital CNA FinancialSelective Group Zenith National

W.R. Berkley Hanover GroupRLI Corp.Lloyd's

AXIS Capital

CURRENT S&P FINANCIAL STRENGTH RATINGS

Rating Agencies= De-Rating Agencies= De-facto Regulatorfacto Regulator

Positive Outlook Negative Outlook Watch Negative

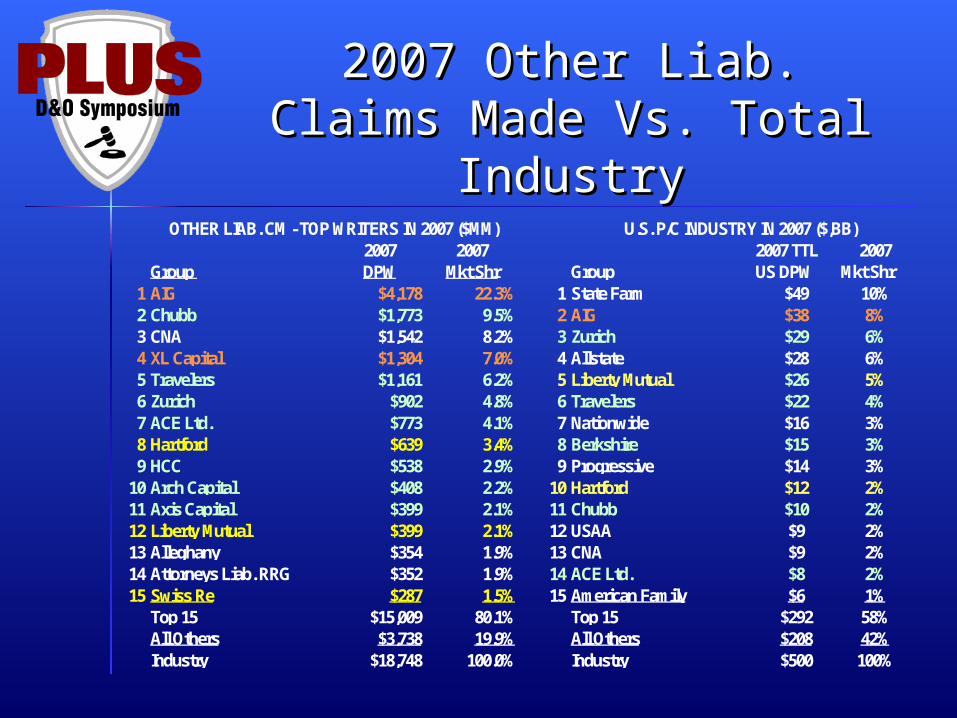

2007 Other Liab. Claims 2007 Other Liab. Claims Made Vs. Total IndustryMade Vs. Total Industry

2007 2007Group DPW Mkt Shr

1 AIG $4,178 22.3%2 Chubb $1,773 9.5%3 CNA $1,542 8.2%4 XL Capital $1,304 7.0%5 Travelers $1,161 6.2%6 Zurich $902 4.8%7 ACE Ltd. $773 4.1%8 Hartford $639 3.4%9 HCC $538 2.9%

10 Arch Capital $408 2.2%11 Axis Capital $399 2.1%12 Liberty Mutual $399 2.1%13 Alleghany $354 1.9%14 Attorneys Liab. RRG $352 1.9%15 Swiss Re $287 1.5%

Top 15 $15,009 80.1%All Others $3,738 19.9%Industry $18,748 100.0%

OTHER LIAB. CM - TOP WRITERS IN 2007 ($MM)2007 TTL 2007

Group US DPW Mkt Shr1 State Farm $49 10%2 AIG $38 8%3 Zurich $29 6%4 Allstate $28 6%5 Liberty Mutual $26 5%6 Travelers $22 4%7 Nationwide $16 3%8 Berkshire $15 3%9 Progressive $14 3%

10 Hartford $12 2%11 Chubb $10 2%12 USAA $9 2%13 CNA $9 2%14 ACE Ltd. $8 2%15 American Family $6 1%

Top 15 $292 58%All Others $208 42%Industry $500 100%

U.S. P/C INDUSTRY IN 2007 ($,BB)

Other Liab. Claims Made Other Liab. Claims Made Soft vs. Hard BlockSoft vs. Hard Block

66.1%

68.2% 71.0% 73.7%

68.9%

65.6%65.3%

63.3%64.4% 66.9%

86.6%

107.5%108.4%

104.8%

94.8%

63.5%

53.2%55.8%

63.5%

45%

55%

65%

75%

85%

95%

105%

115%

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

INDUSTRY "OTHER LIABILITY CLAIMS MADE" AY LOSS RATIO PICKSInitial Vs. Current NET Loss Picks

Initial L. Ratio Pick Current L. Ratio Pick

"SOFT MARKET" BLOCK

"HARD MARKET" BLOCK

New York City ~ February 25 & 26, 2009

Underwriting D&O: Underwriting D&O: Key Accounting Issues for 2009Key Accounting Issues for 2009

Jeremy Perler, CFA, CPAJeremy Perler, CFA, CPA

RiskMetrics GroupRiskMetrics Group

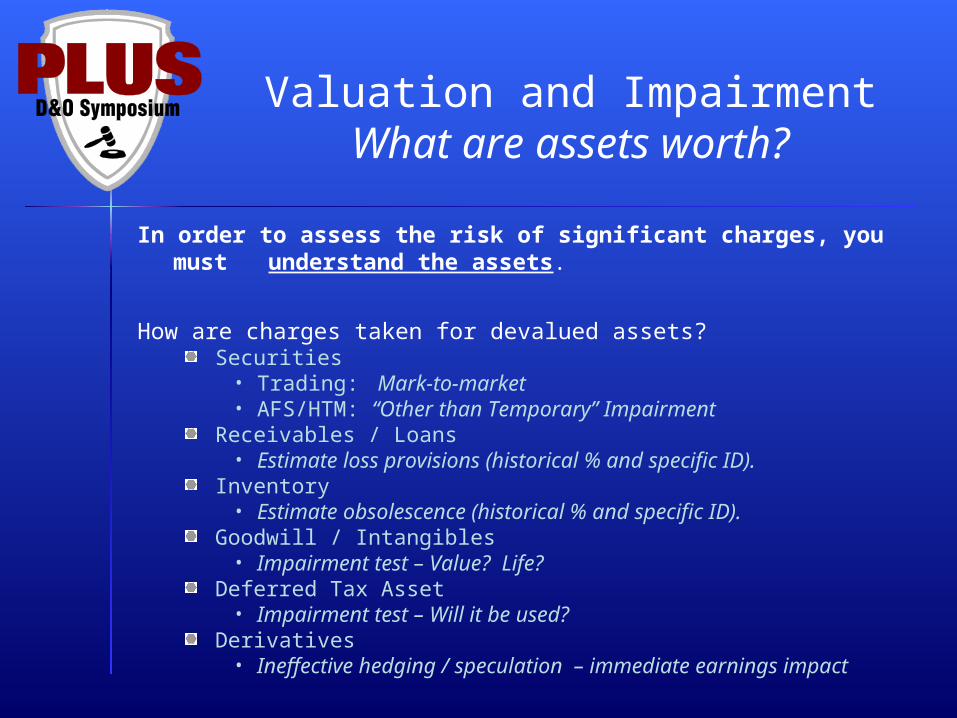

Valuation and ImpairmentWhat are assets worth?

In order to assess the risk of significant charges, you must understand the assets.

How are charges taken for devalued assets?Securities

• Trading: Mark-to-market• AFS/HTM: “Other than Temporary” Impairment

Receivables / Loans• Estimate loss provisions (historical % and specific ID).

Inventory• Estimate obsolescence (historical % and specific ID).

Goodwill / Intangibles• Impairment test – Value? Life?

Deferred Tax Asset• Impairment test – Will it be used?

Derivatives• Ineffective hedging / speculation – immediate earnings impact

Aggregate Balance Sheet of US Commercial Banks (Q2'08)

HTM Securities, 0.47%

AFS Securities,13.84%

Consolidated Loans, 48.37%

Other Assets, 20.98%

Goodwill & Intangibles, 3.87%

Trading Securities,12.48%

Valuation and ImpairmentWhat are assets worth?

Snapshot of an Average Bank’s Balance Sheet

Intense focus on M2M securities (12.5%) distracts from the bigger problem: Loans (48%) are in bad shape.

Valuation and ImpairmentWhat are assets worth?

Understand the business! What is happening in the loan portfolio?

Credit quality is deteriorating:

Reserves are increasing, but not enough to cover nonperforming loans:

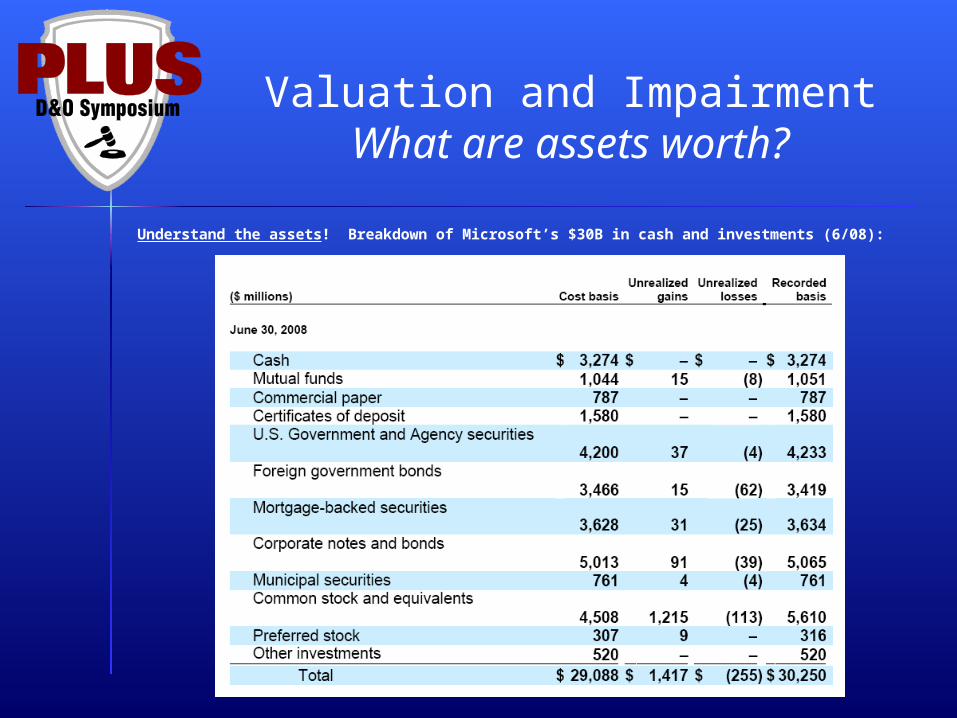

Valuation and ImpairmentWhat are assets worth?

Understand the assets! Breakdown of Microsoft’s $30B in cash and investments (6/08):

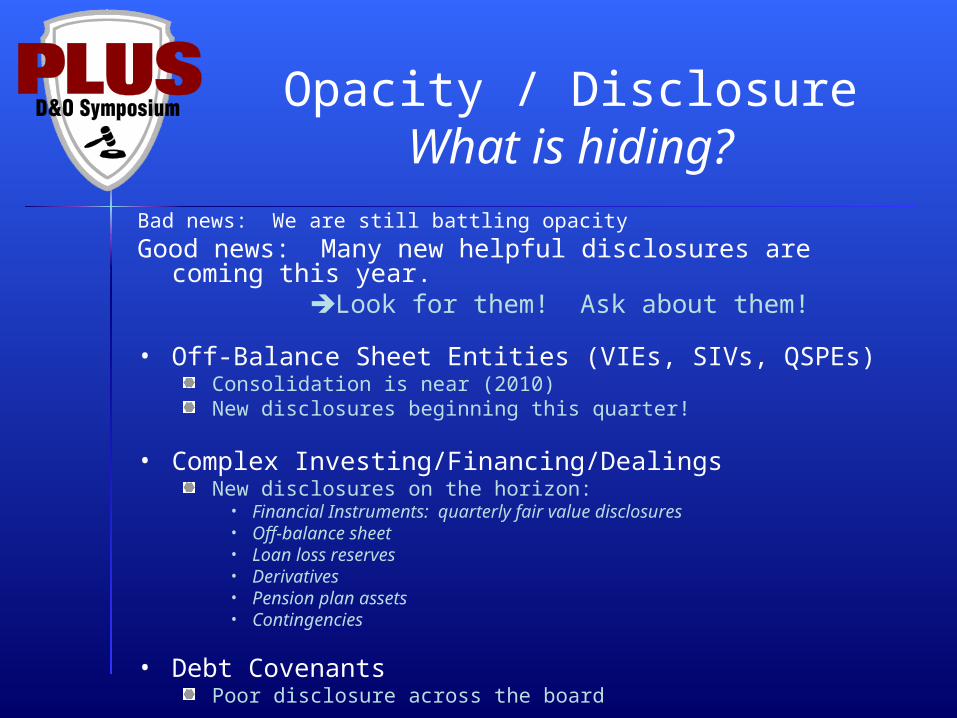

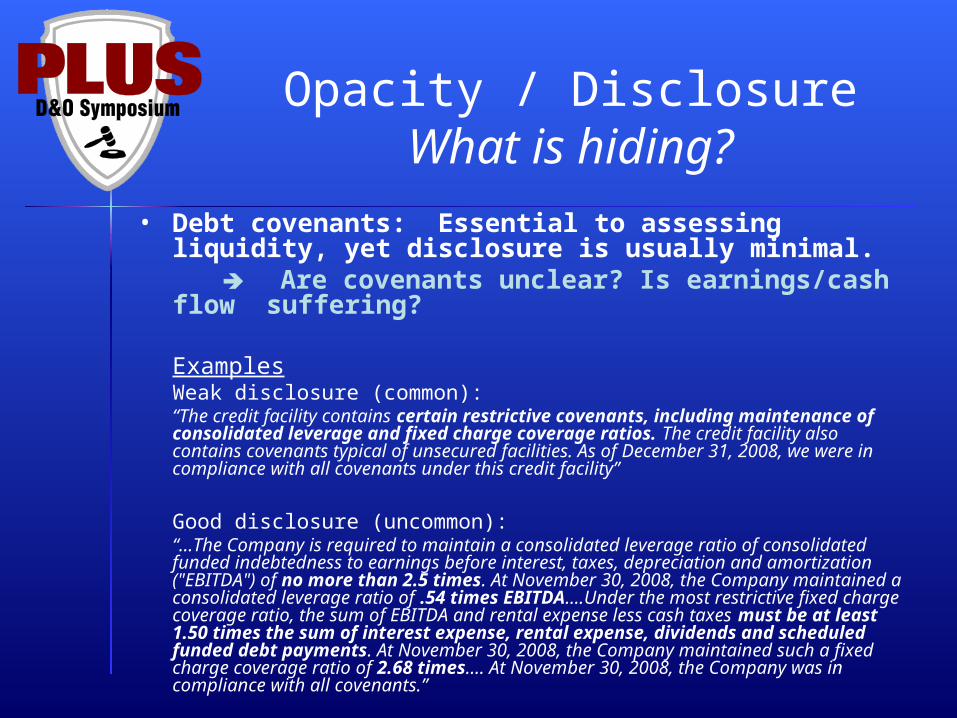

Opacity / DisclosureWhat is hiding?

Bad news: We are still battling opacity

Good news: Many new helpful disclosures are coming this year. Look for them! Ask about them!

• Off-Balance Sheet Entities (VIEs, SIVs, QSPEs)Consolidation is near (2010)New disclosures beginning this quarter!

• Complex Investing/Financing/DealingsNew disclosures on the horizon:

• Financial Instruments: quarterly fair value disclosures• Off-balance sheet• Loan loss reserves• Derivatives• Pension plan assets• Contingencies

• Debt CovenantsPoor disclosure across the board

Opacity / DisclosureWhat is hiding?

• Debt covenants: Essential to assessing liquidity, yet disclosure is usually minimal. Are covenants unclear? Is earnings/cash flow suffering?

ExamplesWeak disclosure (common):“The credit facility contains certain restrictive covenants, including maintenance of consolidated leverage and fixed charge coverage ratios. The credit facility also contains covenants typical of unsecured facilities. As of December 31, 2008, we were in compliance with all covenants under this credit facility”

Good disclosure (uncommon):“…The Company is required to maintain a consolidated leverage ratio of consolidated funded indebtedness to earnings before interest, taxes, depreciation and amortization ("EBITDA") of no more than 2.5 times. At November 30, 2008, the Company maintained a consolidated leverage ratio of .54 times EBITDA….Under the most restrictive fixed charge coverage ratio, the sum of EBITDA and rental expense less cash taxes must be at least 1.50 times the sum of interest expense, rental expense, dividends and scheduled funded debt payments. At November 30, 2008, the Company maintained such a fixed charge coverage ratio of 2.68 times…. At November 30, 2008, the Company was in compliance with all covenants.”

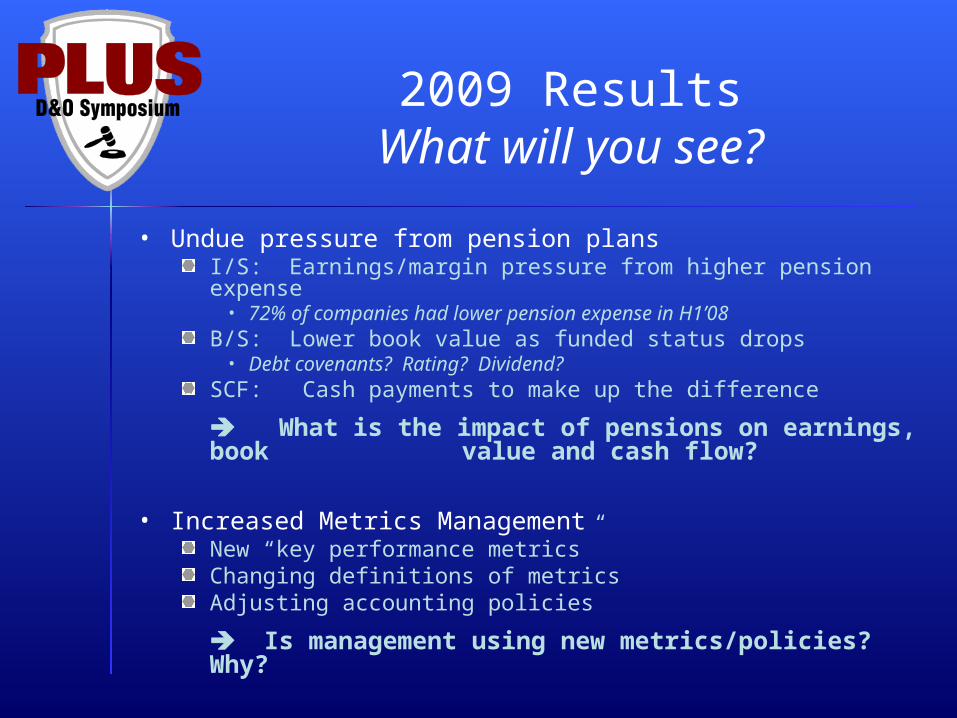

2009 ResultsWhat will you see?

• Undue pressure from pension plansI/S: Earnings/margin pressure from higher pension expense

• 72% of companies had lower pension expense in H1’08 B/S: Lower book value as funded status drops

• Debt covenants? Rating? Dividend? SCF: Cash payments to make up the difference

What is the impact of pensions on earnings, book value and cash flow?

• Increased Metrics Management New “key performance metrics”Changing definitions of metricsAdjusting accounting policies

Is management using new metrics/policies? Why?