1

The Millennium Development Goals – bankable pledge or

sub-prime asset?

UNESCO Future Forum - 2 March 2009Kevin Watkins and Patrick Montjourides

2

Presentation

The MDGs – Where we are today

The impact of the financial crisis

Risks for the MDGs

Responses to the crisis

3

The pre-crisis MDGs – the ‘good news’ report

Extreme poverty – down by 320 million since 2000 (more than 1980-1999)

Child mortality - 3 million fewer deaths Education - 28 million more children in school and

progress on gender disparity Clean water – access improving Aid – Up from around $70 to $104bn 1999-2005

4

The bad news – Part 1

Most countries are off track for most targets Income poverty – much of South Asia and sub-Saharan

Africa missing goals Child mortality – ‘2 million death deficit’ by 2015 Maternal mortality – zero progress zone (10,000 deaths a

week) Education – At least 30 million off track (persistent gender

disparities) Forgotten goals:

Nutrition – one-in-three children stunted and nearly 1 billion total malnourished

Literacy – 11% decline since (circa) 1990, but 776 million adults affected

International cooperation - Aid $50bn pledged by 2010 but $30bn pipeline deficit and no deal on trade

5

The bad news – Part 2

The bad news was getting worse ITYBL (In the year before Lehman)

Rising food and energy costs:

pushing another 125 million driven into extreme poverty during 2006/2007 (WFP 2008)

deepening poverty levels (World Bank 2009)

increasing child malnutrition by 44 million (2006/2008)

adding 10 million to unemployment (ILO 2009)

Donors back-tracking on aid commitments – aid fell by 4.5% in 2006 and 8% in 2007 (OECD 2008)

6

Equity as a barrier to MDG progress

Higher growth but rising inequality weakening the

conversion of growth to poverty reduction – Vietnam

versus Kenya

Child mortality falling far more slowly among the poor

(who account for most child deaths)

Education inequalities holding back progress

Gender disparities magnified by poverty

The lesson – equity matters for the MDGs

7

Presentation

The MDGs – Where we are today

The impact of the financial crisis

Risks for the MDGs

Responses to the crisis

8

The impact of the financial crisis

Started in US housing and financial markets – but hitting the fourth-fifths of humanity in developing countries

has implications for all MDGs: financial markets in New York and London are linked to education and child mortality in the world’s poorest countries

Impacts on the poor do not make the same headlines as mortgage re-possessions, bank-bailouts, and employment in rich countries but the impacts will be large, sustained and leave a legacy of

human development setbacks

how large and sustained will depend on national and international policy choices

9

Transmission mechanisms

Economic growth prospects – deteriorating by the day Slower growth will impact through diverse channels

• Reduced opportunities for income generation and employment• Restricted opportunities for trade• Pressure on key government budgets• More limited and worse quality public service provision• Lower remittances• Pressure on aid budgets

Country effects will vary depending on:• impacts• distribution of shocks• capacity for fiscal stimulus• Policy choice – adjustments can be pro-poor or anti-poor

10

Putting the brakes on economic growth

The most visible impact of the financial crisis is on economic growth prospects.

All developing regions heading for slowdown, or possible reversals

Forecasts are being revised downwards on a daily basis

We are heading from a benign to malign economic growth environment

11

Advanced economies

Emerging and Developing regions apr-2008

oct-2008

nov-2008

jan-2009

Source: International Monetary Fund data

-2,0

0,0

2,0

4,0

6,0

8,0

10,0

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

GD

P an

nual

gro

wth

rate

(%)

-3,0

-1,0

1,0

3,0

5,0

7,0

9,0

2006 2007 2008 2009 2010

GD

P an

nual

gro

wth

rate

(%)

Good news recovery projections – not to be taken too seriously

The economic downturn

The deteriorating picture for 2009

12

janv-09

avr-08oct-08

nov-08

0

2

4

6

8

10

12

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

GD

P gr

owth

rat

e (%

)Sub-saharan Africa

janv-09

avr-08oct-08nov-08

0

2

4

6

8

10

12

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

GD

P gr

owth

rat

e (%

)

Developping Asia

In sub-Saharan Africa:• Growth reduction represents $72bn or $85 per capita• Impact below the poverty line (390 million people)

- $18bn or $46 per capita- Loss represents 20% of

average income

2008 2009

China 9 6,7India 7,3 5,1Argentina 6,5 0,01Indonesia 6,1 3,5Brazil 5,8 1,8South Africa 3,1 1,3Mexico 1,8 -0,3Turkey 1 -1,5

Source: International Monetary Fund

Economic growth rate – regional & country variations

Latin America and Caribbean

janv-09

avr-08oct-08nov-08

0

2

4

6

8

10

12

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

GD

P gr

owth

rat

e (%

)

Middle East

janv-09

avr-08oct-08nov-08

0

2

4

6

8

10

12

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

GDP

grow

th ra

te (%

)

13

Growth reversals linked to wider macro-economic problems

International trade• Terms of trade for commodity exporters are deteriorating (sub-

Saharan Africa and Latin America affected; Zambian government revenues from copper could fall from $415m to less than $200m )

• Steep decline in exports and trade-related employment (East Asia)

• Prospect of protectionist backlash

Private capital flows collapsing• $929 in 2008 but projected $165bn 2009 (net outflow of bank

lending)

• East Asia and Latin America most affected

• Impacts on credit, investment and employment

Remittances• $305bn in 2008 and more stable, but..

• 6% decline projected for 2009

• Some countries (Mexico) already in decline

14

Fiscal space matters for pro-poor adjustment – and it’s shrinking fast

Rich countries responding to crisis through large fiscal interventions, some developing countries following suit (United States 7% of GDP / China 10%)

But most developing countries, especially the poorest, lack fiscal capacity to respond to crisis

New ‘fiscal space indicator’ establishes threshold for:

• Fiscal deficits (3%)

• Government debt-to-GDP (+20%)

• Revenue-to-GDP (+13%)

• Aid-to-GDP (+5%)

15

Most developing countries lack fiscal capacity to respond to crisis

0

10

20

30

40

50

60

70

80

90

100

Middle-Income countries

Low-Income countries

Total number of countries

Num

ber

of

coun

trie

s

Sources: International Monetary Fund, World Bank, GMR team calculations

• 43 out of 48 low-income countries with data lack fiscal space

• 55 out of 87 middle-income countries lack fiscal space

Countries with low fiscal space

16

Presentation

The MDGs – Where we are today

The impact of the financial crisis

Risks for the MDGs

Responses to the crisis

17

Low fiscal space increases MDG risks - education

Countries at the bottom end of the global distribution for opportunity in education face serious constraints

Countries with distance to travel to EFA goals face prospect of economic slowdown with limited government capacity to respond

• World Bank lists 43 countries facing ‘high exposure’ to crisis

• 32 have distance to travel to universal primary education (UPE)

• 27 have limited fiscal space

18

Bangladesh Guinea Nepal

Benin India Nicaragua

Bhutan Iraq* Niger

Burkina Faso Lao PDR Nigeria

Burundi Lesotho Pakistan

Cambodia Madagascar Rwanda

Chad Malawi Senegal

Djibouti* Mali Togo

Eritrea Mauritania Yemen*

Ethiopia Mozambique

Low-income country with low fiscal space

Low Education Development Index (EDI) countries (29)

Low EDI countries at major risk

Sources: International Monetary Fund, World Bank, GMR team calculations* No data available

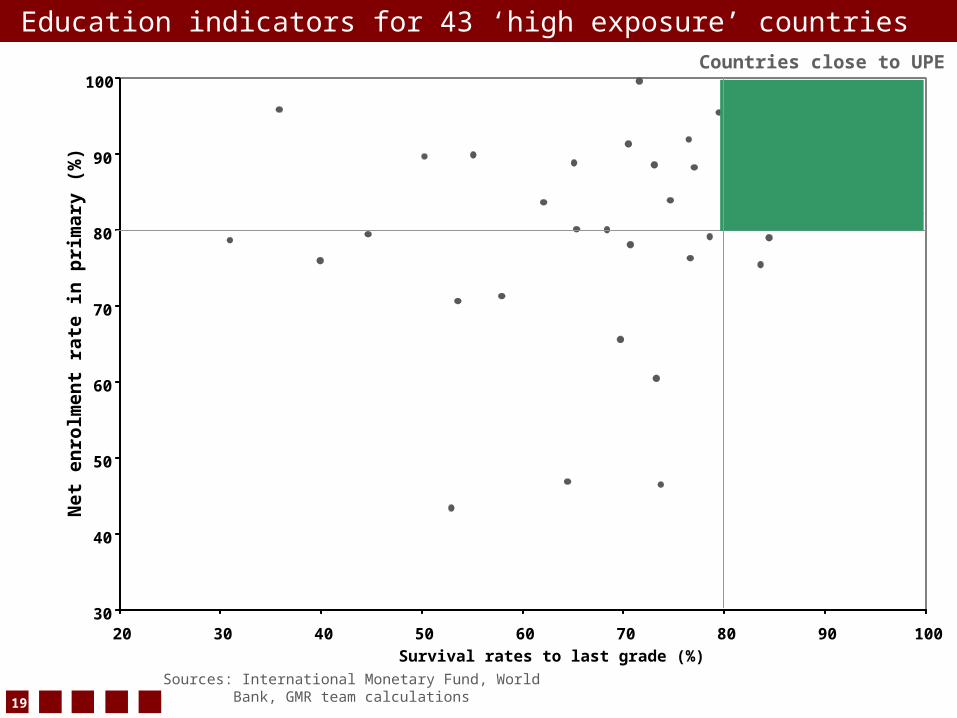

19

Education indicators for 43 ‘high exposure’ countries

30

40

50

60

70

80

90

100

20 30 40 50 60 70 80 90 100

Survival rates to last grade (%)

Net

en

rolm

ent

rate

in

pri

mar

y (%

)

Sources: International Monetary Fund, World Bank, GMR team calculations

Countries close to UPE

20

Bangladesh

Benin

Bhutan

Cambodia

Burkina FasoEritrea

Ethiopia

India

Madagascar

Mali

MauritaniaMozambique

Niger

Nepal

Nicaragua

PakistanSenegal

Togo

Rwanda

Most ‘high exposure’ countries face severe fiscal constraints

Kenya

Lao PDR

30

40

50

60

70

80

90

100

20 30 40 50 60 70 80 90 100

Survival rates to last grade (%)

Net

en

rolm

ent

rate

in

pri

mar

y (%

)

Sources: International Monetary Fund, World Bank, GMR team calculations

Countries close to UPE

Countries with low fiscal space

21

Potential MDG casualties

Impacts will be highly variable Past ‘economic shock’ analysis point to diverse effects

(Ferreira and Schady 2008):• Poorest countries register ‘pro-cyclical’ effects - nutrition, health and

education indicators worsen after crisis

• Middle-income countries ‘pro-cyclical’ in health, counter-cyclical on school attendance

Unlike the rich, the poor lack insurance and coping capacity

‘Tipping point’ effects can convert short-term shocks into legacy of long-term poverty: nutrition-health-education cycles

22

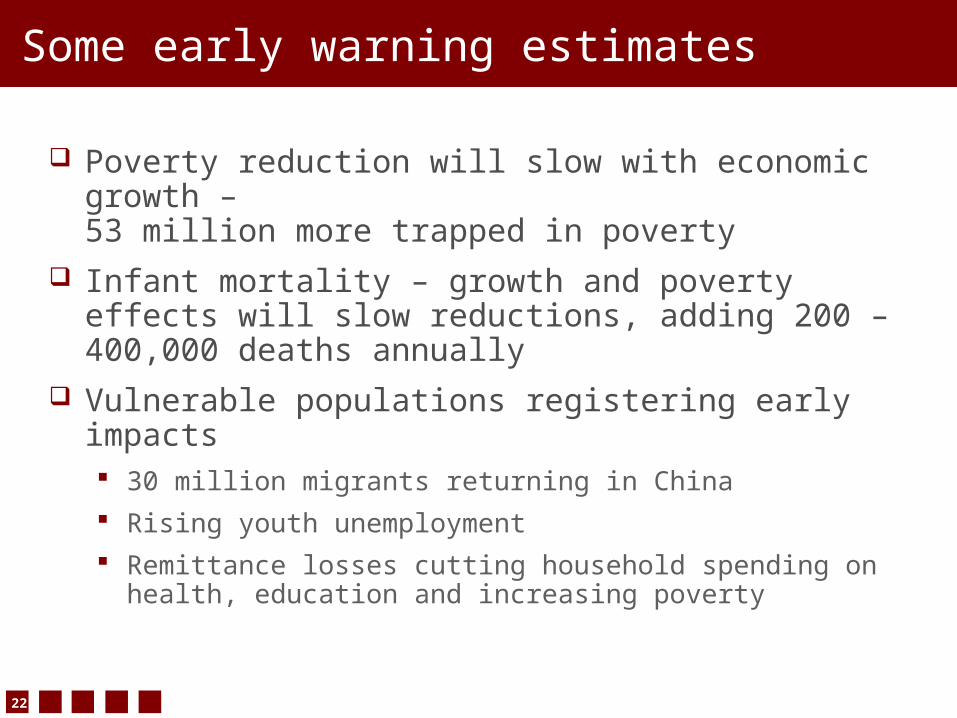

Some early warning estimates

Poverty reduction will slow with economic growth – 53 million more trapped in poverty

Infant mortality – growth and poverty effects will slow reductions, adding 200 – 400,000 deaths annually

Vulnerable populations registering early impacts 30 million migrants returning in China

Rising youth unemployment

Remittance losses cutting household spending on health, education and increasing poverty

23

Aid contagion effects

Fiscal pressure, rising unemployment, and bank rescues will weaken political support for aid

Past episodes highlight threat – aid budgets cut after Japanese real stock bubble burst in 1990 and Nordic crisis in 1991

• 6-9 year recover in Norway and Sweden

• No recovery in Japan and Finland

‘Target-based’ aid commitments will cut budgets• EU countries are ‘committed’ to 0.56 Aid/GNI by 2010

• Growth adjusted loss in 2010 is $4.6bn

Aid- dependent countries facing acute threats

24

Current level of aid to basic education

0

2

4

6

8

10

12

Aid to basic education in low-income countries (LIC)

EFA financing gap

versus aid to banks during a crisis

The development financing gap

$US billons

Sources: International Monetary Fund, GMR

25

0

50

100

150

200

250

300

350

400

$US

billo

nsAid to basic education in low-income countries (LIC)

EFA financing gap

Lower bound estimate of MDGs financing

versus aid to banks during a crisis

Bank capital funded by

public monies

The development financing gap

Sources: International Monetary Fund, GMR

26

Presentation

The MDGs – Where we are today

The impact of the financial crisis

Risks for the MDGs

Responses to the crisis

27

Responses – financial governance

Need for large and rapid financial transfers to developing countries to limit contagion

Globalise fiscal stimulus• Estimated level of $400bn pa (1% GDP of rich countries) for

developing countries (Lin 2009)

IMF should be taking the lead but is an under-resourced rich-man’s club

• Need for $500bn+ rights issues to support developing countries and less EU/US voice in governance

• Key role for G20 meeting in April 2009

28

Responses to the crisis – aid

Developed countries need to affirm and deliver on 2005 commitments

EU ‘adjustment commitment’ of $4.6bn

For aid to play counter-cyclical role it has to be delivered this year – front-loading is vital

Stop talking and fast-track Fast Track Initiative support in education

Avoid multiple ‘innovations’ and fragmented delivery

29

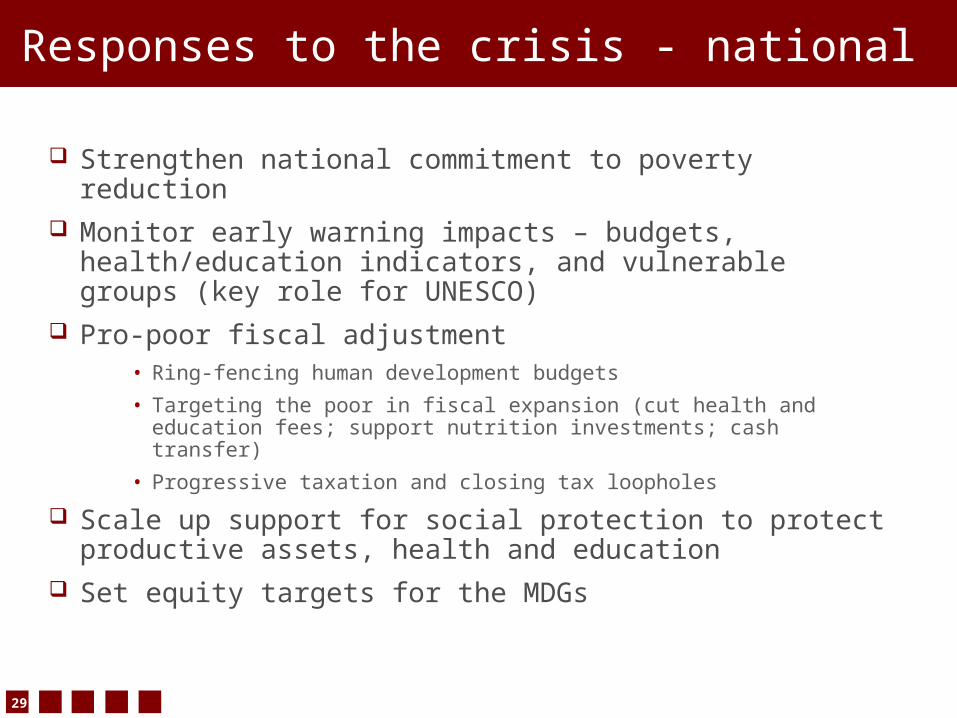

Responses to the crisis - national

Strengthen national commitment to poverty reduction Monitor early warning impacts – budgets,

health/education indicators, and vulnerable groups (key role for UNESCO)

Pro-poor fiscal adjustment • Ring-fencing human development budgets

• Targeting the poor in fiscal expansion (cut health and education fees; support nutrition investments; cash transfer)

• Progressive taxation and closing tax loopholes

Scale up support for social protection to protect productive assets, health and education

Set equity targets for the MDGs

30

Conclusion

The world’s poor are not responsible for the current crisis – ethical imperatives matter

Investments in global poverty reduction, health and education can support recovery – economic imperatives are also important

The MDG crisis represents a challenge to political leaders in rich countries and international development agencies

The threat is an opportunity to demonstrate that international cooperation can deliver change we can believe in.