1

Math 479

Casualty Actuarial Mathematics

Fall 2014University of Illinois at Urbana-Champaign

Professor Rick Gorvett

Session 8: Ratemaking II

September 18, 2014

2

Last Time

• Ratemaking I

– Overall concept

– Two foundational techniques

• Pure premium method

• Loss ratio method

3

Agenda

• Ratemaking II

– Trend vs development – is there overlap?

– Relativities

– Parallelogram method

4

Loss Trendvs

Loss Development

5

Relationship to Reserving

• Developing losses to their projected ultimate values is a core concept

• But now, we add consideration of trend

• Why?– Historically, suppose that AY 2010 claims will

develop for (let’s say) ten years– Suppose that for ratemaking purposes, we are

estimating AY 2015– Note: AY 2015 may also be expected to develop

for ten years, but starting 5 years later

6

Loss Trend

• In our example, if we use AY 2010 losses as a basis for our “what if” scenario (“what if 2010 losses are representative of what losses might occur in 2015”), we must acknowledge that, in 2015, they will occur at a cost level that applies 5 years later

• Use historical patterns of losses (e.g., frequency and severity) to estimate and project loss “trend” or “inflation”

7

Trend vs Development

• Is there “overlap” here? Are the trend and development processes somewhat redundant?

• Answer: No.• There are two “time periods” in the ratemaking

process– (1) Average accident date for the experience

period, to average accident date for the future policies which will be written under the new projected rates

– (2) From the occurrence period of the losses to their final ultimate values

8

Relativities

9

Ratemaking “Relativities”

• Three main kinds of relativities– Classification– Territorial– Increased limits

• Classification ratemaking– One class is the “base class” (relativity = 1.00)– Rates for other classes are keyed off of the base

class rate• Class rate = base rate × class relativity factor

– More on this in the “Risk Classification” section

10

Ratemaking “Relativities” (cont.)

• Territorial ratemaking– Very similar to classification ratemaking,

conceptually and procedurally

• Increased limits factors– Basic limits premium or loss cost

• E.g., $100,000 per occurrence limit– Calculate premiums or loss costs for higher policy

limits by multiplying the basic limits value by the appropriate increased limits factor (ILF)

– Often, trending and/or developing is performed on a basic limits (and perhaps other limits) basis

11

Parallelogram

Technique

12

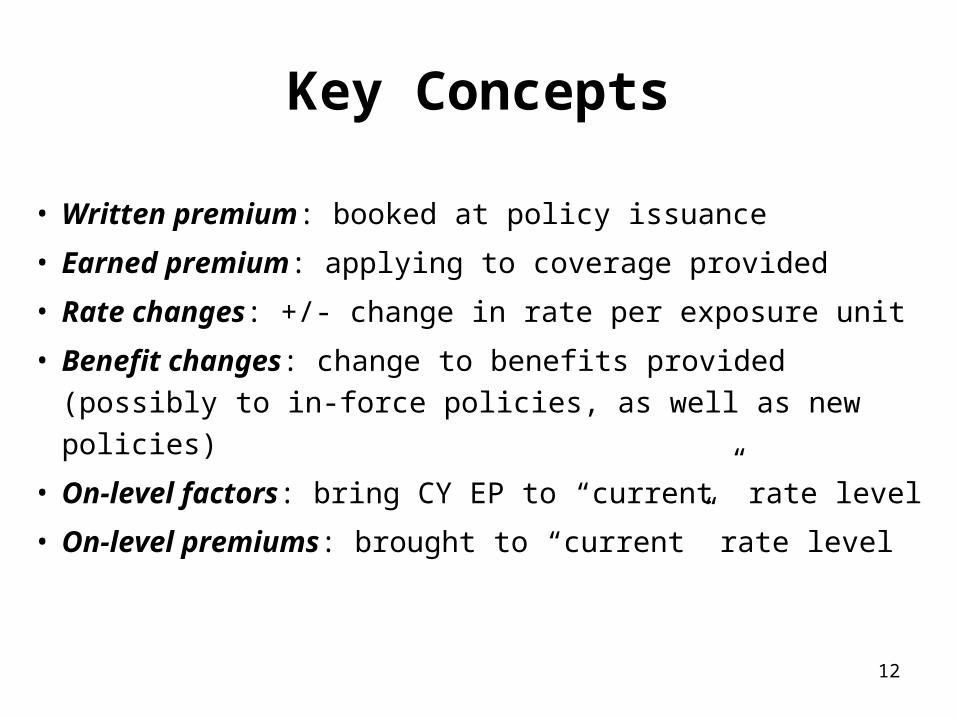

Key Concepts

• Written premium: booked at policy issuance

• Earned premium: applying to coverage provided

• Rate changes: +/- change in rate per exposure unit

• Benefit changes: change to benefits provided (possibly

to in-force policies, as well as new policies)

• On-level factors: bring CY EP to “current” rate level

• On-level premiums: brought to “current” rate level

13

Parallelogram Method

2008 2009

+20% rate change on July 1, 2008

What is the on-level factor to bring 2008 CY EP to a 2009 rate-level basis?

1.000

1.200

14

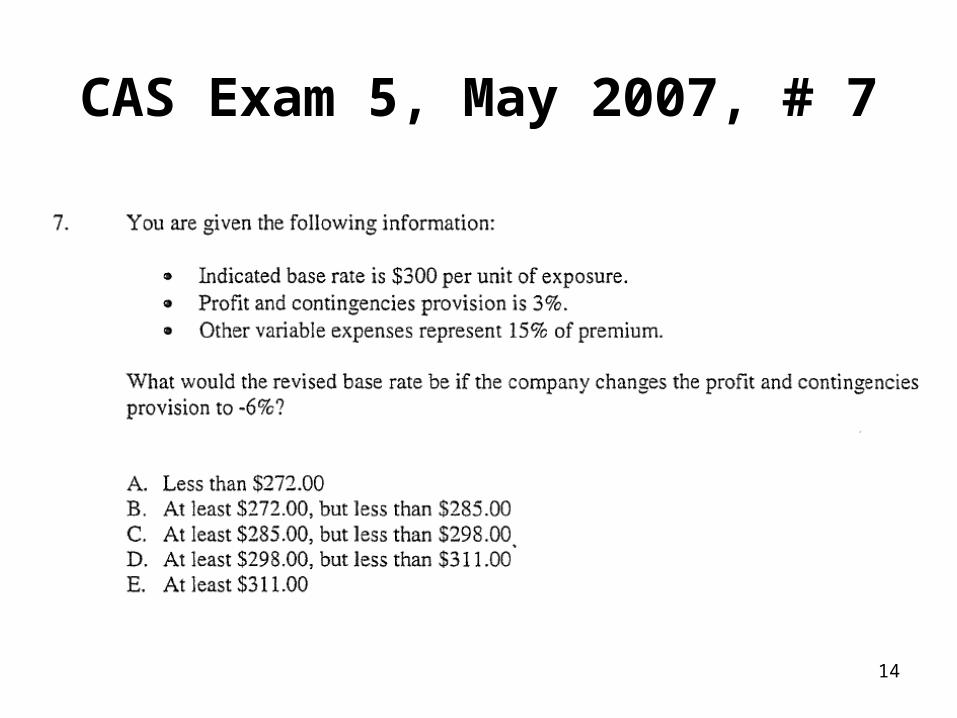

CAS Exam 5, May 2007, # 7

15

CAS Exam 5, May 2007, # 8

16

CAS Exam 5, May 2008, # 24

17

CAS Exam 5, May 2008, # 27

18

CAS Exam 5, May 2007, # 34

19

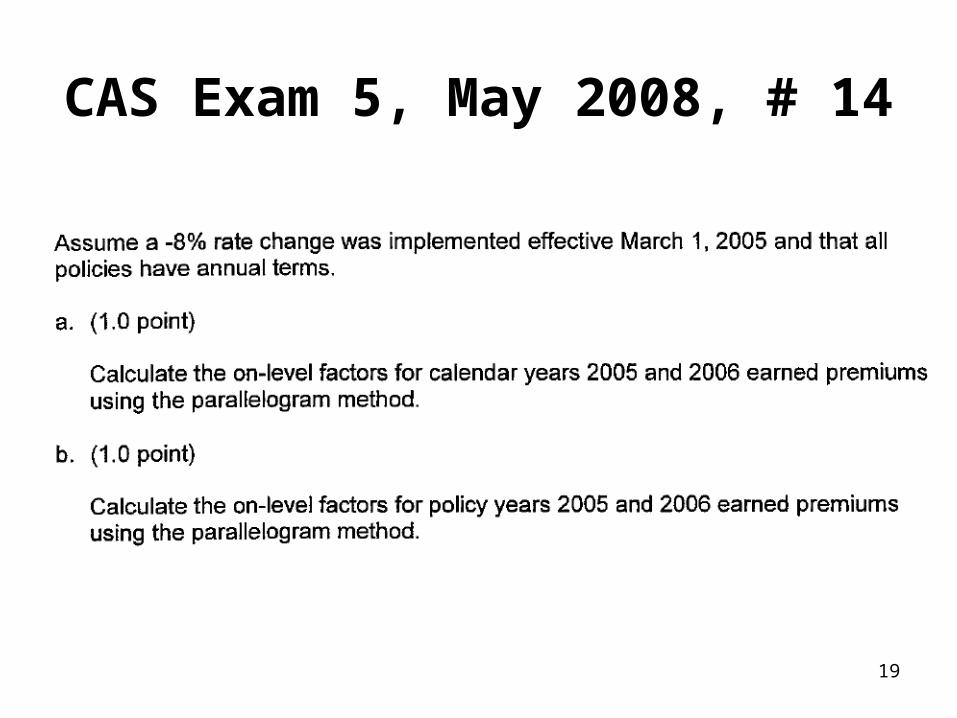

CAS Exam 5, May 2008, # 14

20

CAS Exam 5, May 2007, # 37

21

Next Time

• Ratemaking III

– Exposure bases

– Putting it all together