1

Introduction

1. Corporate Finance – how decision making affects “value”.

2. Corporate finance is not a number “game”.

3. Focus: (a) practical issues that arise in valuation, (b) taxes, (c) incentives of different stakeholders.

2

Chapter 7 Risk, Return and the Cost of Capital

Final objective: Estimating the opportunity cost of capital.

Explain and calculate Expected return Security risk Diversification Portfolio risk beta.

3

Capital Budgeting Example

• Capital Budgeting Decision– Suppose you had the opportunity to buy a

tbill which would be worth $400,000 one year from today.• Interest rates on tbills are a risk free

7%.– What would you be willing to pay for this

investment?

$400,000 / (1.07) = $373,832

PV today:0 1 2

-$400,000

4

Cost of Capital

• Capital Budgeting Decision– Suppose you are offered a construction

deal with similar cost and payoff.– An important concept in finance is that a

risky dollar is worth less than a safe dollar. – You are told that the risk is quantified by

the cost of capital, which is 12%.

NPV= -350,000+400,000/1.12 = $7,142

5

Calculating Returns

Suppose you bought 100 shares of BCE one year ago today at $25. Over the last year, you received $20 in dividends (= 20 cents per share × 100 shares). At the end of the year, the stock sells for $30. How did you do?

6

Holding Period Returns

The holding period return is the return that an investor would get when holding an investment over a period of n years, when the return during year i is given as ri:

1)1()1()1(

return period holding

21

nrrr

7

0.1

10

1000

1957 1962 1967 1972 1977 1982 1987 1992 1997 2002

The Future Value of an Investment of $1 in 1957: Evidence from Canada

$42.91

$20.69

17.86$)1()1()1(1$ 200319581957 rrr

Common Stocks

Long Bonds

T-Bills

8

An Investment of $1 in 1900: US evidence

$1

$10

$100

$1,000

$10,000

$100,000

1900

1910

1920

1930

1940

1950

1960

1970

1980

1990

2000

Start of Year

Dol

lars

Common Stock

US Govt Bonds

T-Bills

15,578

14761

2004

9

$1

$10

$100

$1,000

1900

1910

1920

1930

1940

1950

1960

1970

1980

1990

2000

Start of Year

Dol

lars

Equities

Bonds

Bills

719

6.81

2.80

2004

Real Returns

An Investment of $1 in 1900: US evidence

10

How does this relate to cost of capital?

• Suppose there is an investment project which you know has the same risk as Standard and Poor’s Composite Index.

• What rate should you use?

11

Rates of Return 1900-2003

Source: Ibbotson Associates

-60%

-40%

-20%

0%

20%

40%

60%

80%

1900 1920 1940 1960 1980 2000

Year

Per

cent

age

Ret

urn

Stock Market Index Returns

12

Measuring Risk

1 14

1012

19

15

24

13

32

0

4

8

12

16

20

24

-50

to -

40

-40

to -

30

-30

to -

20

-20

to -

10

-10

to 0

0 to

10

10 t

o 20

20 t

o 30

30 t

o 40

40 t

o 50

50 t

o 60

Return %

# of Years

Histogram of Annual Stock Market ReturnsHistogram of Annual Stock Market Returns

13

Average Stock Returns and Risk-Free Returns

• The Risk Premium is the additional return (over and above the risk-free rate) resulting from bearing risk.

• One of the most significant observations of stock (and bond) market data is this long-run excess of security return over the risk-free return.

• The historical risk premium was 7.6% for the US.

14

Average Market Risk Premia (by country)

4.3 4.7 5.1 5.3 5.8 5.9 5.9 6.3 6.4 6.67.6 8.1 8.2 8.6

9.3 1010.7

0123456789

1011

Den

mar

k

Bel

giu

m

Sw

itze

rlan

d

Sp

ain

Can

ada

Irel

and

Ger

man

y

UK

Ave

rage

Net

her

lan

ds

US

A

Sw

eden

Sou

th A

fric

a

Au

stra

lia

Fra

nce

Jap

an

Ital

y

Risk premium, %

Country

15

Measuring Risk

Variance - Average value of squared deviations from mean. A measure of volatility.

Standard Deviation – Square root of variance. A measure of volatility.

16

Return Statistics

• The history of capital market returns can be summarized by describing the – average return

– the standard deviation of those returns

T

RRR T )( 1

1

)()()( 222

21

T

RRRRRRVARSD T

17

Average Standard Investment Annual Return Deviation Distribution

Canadian common stocks 10.64% 16.41%

Long Bonds 8.96 10.36

Treasury Bills 6.80 4.11

Inflation 4.29 3.63

Canada Returns, 1957-2003

– 60% + 60%0%

18

Risk Statistics

There is no universally agreed-upon definition of risk. A large enough sample drawn from a normal distribution looks like a bell-shaped curve.

19

Historically – Are Returns Normal?

S&P 500 Return Frequencies

0

2

5

11

16

9

1212

12

110

0

2

4

6

8

10

12

14

16

62%52%42%32%22%12%2%-8%-18%-28%-38%-48%-58%

Annual returns

Ret

urn

fre

qu

ency

Normal approximationMean = 12.8%Std. Dev. = 20.4%

20

Expected Return, Variance, and covariance

Consider the following two risky asset worlds. There is a 1/3 chance of each state of the economy and the only assets are a stock fund and a bond fund.

Rate of ReturnScenario Probability Stock fund Bond fund

Recession 33.3% -7% 17%Normal 33.3% 12% 7%

Boom 33.3% 28% -3%

21

Expected Return, Variance, and Covariance

Stock fund Bond Fund

Rate of Squared Rate of Squared

Scenario Return Deviation Return Deviation Recession -7% 3.24% 17% 1.00%Normal 12% 0.01% 7% 0.00%Boom 28% 2.89% -3% 1.00%Expected return 11.00% 7.00%Variance 0.0205 0.0067Standard Deviation 14.3% 8.2%

22

Rate of ReturnScenario Stock fund Bond fund Portfolio squared deviationRecession -7% 17% 5.0% 0.160%Normal 12% 7% 9.5% 0.003%Boom 28% -3% 12.5% 0.123%

Expected return 11.00% 7.00% 9.0%Variance 0.0205 0.0067 0.0010Standard Deviation 14.31% 8.16% 3.08%

The Return for Portfolios

The expected rate of return on the portfolio is a weighted average of the expected returns on the securities in the portfolio.

)()()( SSBBP rEwrEwrE

23

Rate of ReturnScenario Stock fund Bond fund Portfolio squared deviationRecession -7% 17% 5.0% 0.160%Normal 12% 7% 9.5% 0.003%Boom 28% -3% 12.5% 0.123%

Expected return 11.00% 7.00% 9.0%Variance 0.0205 0.0067 0.0010Standard Deviation 14.31% 8.16% 3.08%

The Variance of a Portfolio

24

Portfolio Risk

1

2

3

4

5

6

N

1 2 3 4 5 6 N

STOCK

STOCKTo calculate portfolio variance add up the boxes

25

Diversification

• The variance (risk) of the security’s return can be broken down into:– Systematic (Market) Risk– Unsystematic (diversifiable) Risk

The Effect of Diversification:– unsystematic risk will significantly diminish in

large portfolios– systematic risk is not affected by

diversification since it affects all securities in any large portfolio

26

Portfolio Risk as a Function of the Number of Stocks in the Portfolio

Nondiversifiable risk; Systematic Risk; Market Risk

Diversifiable Risk; Nonsystematic Risk; Firm Specific Risk; Unique Risk

n

In a large portfolio the variance terms are effectively diversified away, but the covariance terms are not.

Thus diversification can eliminate some, but not all of the risk of individual securities.

Portfolio risk

27

Beta and Unique Risk

beta

Expected

return

Expectedmarketreturn

10%10%- +

-10%+10%

stock

Copyright 1996 by The McGraw-Hill Companies, Ic

-10%

1. Total risk = diversifiable risk + market risk2. Market risk is measured by beta, the sensitivity to market changes

28

Beta and Unique Risk

Market Portfolio - Portfolio of all assets in the economy. In practice a broad stock market index, such as the S&P Composite, is used to represent the market.

Beta - Sensitivity of a stock’s return to the return on the market portfolio.

29

Definition of Risk When Investors Hold the Market Portfolio

• Researchers have shown that the best measure of the risk of a security in a large portfolio is the beta ()of the security.

• Beta measures the responsiveness of a security to movements in the market portfolio.

)(

)(2

,

M

Mii R

RRCov

30

Chapter 8Risk and Return

• Markowitz Portfolio Theory

• Risk and Return Relationship

• Validity and the Role of the CAPM

31

Markowitz Portfolio Theory

• Given a certain level of risk, investors prefer stocks with higher returns.

• Given a certain level of return, investors prefer less risk.

• By combining stocks into a portfolio, one can achieve different combinations of return & standard deviation.

• Correlation coefficients are crucial for ability to reduce risk in portfolio.

32

Markowitz Portfolio Theory

Exxon Mobil

Coca Cola

Standard Deviation

Expected Return (%)

40% in Coca Cola

Expected Returns and Standard Deviations vary given different weighted combinations of the stocks

33

Efficient Frontier

Example Correlation Coefficient = .4

Stocks % of Portfolio Avg Return

ABC Corp 28 60% 15%

Big Corp 42 40% 21%

34

Efficient Frontier

Standard Deviation

Expected Return (%)

Each half egg shell represents the possible weighted combinations for two stocks.

The composite of all stock sets constitutes the efficient frontier

35

Efficient Frontier

Example Correlation Coefficient = .4

Stocks % of Portfolio Avg Return

ABC Corp 28 60% 15%

Big Corp 42 40% 21%

Portfolio 28.1 17.4%

Let’s Add stock New Corp to the portfolio

36

Efficient Frontier

Example Correlation Coefficient = .3

Stocks % of Portfolio Avg Return

Portfolio 28.1 50% 17.4%

New CorpNew Corp 3030 50%50% 19% 19%

New Portfolio 23.43 18.20%

NOTE: Higher return & Lower risk

How did we do that? DIVERSIFICATION

37

Efficient Frontier

A

B

Return

Risk

AB

38

Efficient Frontier

A

BN

Return

Risk

AB

39

Efficient Frontier

A

BN

Return

Risk

ABABN

40

2-Security Portfolios - Various Correlations

100% bonds

retu

rn

100% stocks

= 0.2

= 1.0

= -1.0

41

Efficient Frontier

retu

rn

P

minimum variance portfolio

efficient frontier

Individual Assets

42

Riskless Borrowing and Lending

Now investors can allocate their money across the T-bills and a balanced mutual fund

100% bonds

100% stocks

rf

retu

rn

Balanced fund

CML

43

Market Equilibrium: CAPM

retu

rn

P

efficient frontier

rf

M

CML

44

100% bonds

100% stocks

retu

rn

First Optimal Risky Portfolio

Second Optimal Risky Portfolio

CML 0 CML 1

0fr

1fr

Changes in Riskfree Rate

45

Security Market LineReturn

.

rf

Risk Free

Return =

Efficient Portfolio

Market Return = rm

BETA1.0

46

Security Market LineReturn

BETA

rf

1.0

SML

SML Equation = rf + B ( rm - rf )

47

Risk & Expected Return

Exp

ecte

d re

turn

%3FR

%3

1.5

%5.13

5.1β i %10MR

%5.13%)3%10(5.1%3 iR

48

Estimating with regression

Sec

uri

ty R

etu

rns

Sec

uri

ty R

etu

rns

Return on Return on market %market %

RRii = = ii + + iiRRmm + + eeii

Slope = Slope = iiCharacte

ristic

Line

Characteris

tic Line

49

Estimates of Beta for Selected Stocks

Stock Beta

Research in Motion 3.04

Nortel Networks 3.61

Bank of Nova Scotia 0.28

Bombardier 1.48

Investors Group. 0.36

Maple Leaf Foods 0.25

Roger Communications

1.17

Canadian Utilities 0.08

TransCanada Power 0.08

50

CAPM versus Reality

1. Do investors care about mean and variance?

2. Is there a security that is risk-free?

3. Short selling?

4. Transaction costs?

5. Most important: homogeneous expectations?

51

Testing the CAPM

Avg Risk Premium 1931-2002

Portfolio Beta1.0

SML30

20

10

0

Investors

Market Portfolio

Beta vs. Average Risk Premium

52

Testing the CAPM

Avg Risk Premium 1931-65

Portfolio Beta1.0

SML

30

20

10

0

Investors

Market Portfolio

Beta vs. Average Risk Premium

53

Testing the CAPM

Avg Risk Premium 1966-2002

Portfolio Beta1.0

SML

30

20

10

0

Investors

Market Portfolio

Beta vs. Average Risk Premium

54

Invest in project

Chapter 9 (part 1)Capital Budgeting and Risk

Firm withexcess cash

Shareholder’s Terminal

Value

Pay cash dividend

Shareholder invests in financial

asset

Because stockholders can reinvest the dividend in risky financial assets, the expected return on a capital-budgeting project should be at least as great as the expected return on a financial asset of comparable risk.

A firm with excess cash can either pay a dividend or make a capital investment

55

Company Cost of Capital

• A firm’s value can be stated as the sum of the value of its various assets

PV(B)PV(A)PV(AB) valueFirm

56

Company Cost of Capital

10%nologyknown tech t,improvemenCost

COC)(Company 15%business existing ofExpansion

20%products New

30%Ventures eSpeculativ

RateDiscount Category

57

Company Cost of Capital (COC) is based on the average beta of the assets

The average Beta of the assets is based on the % of funds in each asset

Example1/3 New Ventures B=2.01/3 Expand existing business B=1.31/3 Plant efficiency B=0.6

AVG B of assets = 1.3

Company Cost of Capitalsimple approach

58

Company Cost of Capital

If the firm is all equity financed, A company’s cost of capital can be compared to the CAPM required return

Required

return

Project Beta1.26

Company Cost of Capital

13

5.5

0

SML

59

Example

• Suppose the stock of Stansfield Enterprises, a publisher of PowerPoint presentations, has a beta of 2.5. The firm is 100-percent equity financed.

• Assume a risk-free rate of 5-percent and a market risk premium of 10-percent.

• What is the appropriate discount rate for an expansion of this firm?

60

Example (continued)Suppose Stansfield Enterprises is evaluating the following non-mutually exclusive projects. Each costs $100 and lasts one year.

Project Project Project’s Estimated Cash Flows Next Year

IRR NPV at 30%

A 2.5 $150 50% $15.38

B 2.5 $130 30% $0

C 2.5 $110 10% -$15.38

61

Using the SML to Estimate the Risk-Adjusted Discount Rate for Projects

Pro

ject

IRR

Firm’s risk (beta)

SML

5%

Good projects

Bad projects

30%

2.5

A

B

C

62

Capital Structure - the mix of debt & equity within a company

Expand CAPM to include CS (common shares)

R = rf + B ( rm - rf )

becomes

Requity = rf + B ( rm - rf )

Capital Structure

63

Capital Structure & COC (company cost of capital)

COC = rportfolio = rassets

rassets = rdebt (D) + requity (E)

(V) (V)

Bassets = Bdebt (D) + Bequity (E)

(V) (V)

requity = rf + Bequity ( rm - rf )

IMPORTANT

E, D, and V are all market values

64

0

20

0 0.2 0.8 1.2

Capital Structure & COC

Expected return (%)

Bdebt Bassets Bequity

Rrdebt=8

Rassets=12.2

Requity=15

Expected Returns and Betas prior to refinancing

65

Suppose the Conglomerate Company has a cost of capital, based on the CAPM, of 17%. The risk-free rate is 4%, the market risk premium is 10%, and the firm’s beta is 1.3.

17% = 4% + 1.3 × [14% – 4%]

This is a breakdown of the company’s investment projects:1/3 Automotive retailer = 2.0

1/3 Computer Hard Drive Mfr. = 1.3

1/3 Electric Utility = 0.6

average of assets = 1.3

When evaluating a new electrical generation investment, which cost of capital should be used?

The Firm versus the Project

66

Capital Budgeting & Project RiskP

roje

ct

IRR

Firm’s risk (beta)

SML

17%

1.3 2.00.6r = 4% + 0.6×(14% – 4% ) = 10%

10% reflects the opportunity cost of capital on an investment in electrical generation, given the unique risk of the project.

10%

24% Investments in hard drives or auto retailing should have higher discount rates.

67

Capital Budgeting & Project Risk

Pro

ject

IR

R

Firm’s risk (beta)

SML

rf

FIRM

Incorrectly rejected positive NPV projects

Incorrectly accepted negative NPV projects

Hurdle rate

)( FMFIRMF RRβR

The SML can tell us why:

68

Theoretically, the calculation of beta is straightforward:

2)(

),(

M

im

M

Mi

σ

σ

RVar

RRCovβ

Problem 1: Betas may vary over time.

Measuring Betas

69

Measuring Betas

Dell Computer

Slope determined from plotting the line of best fit.

Price data: May 91- Nov 97

R2 = .10

B = 1.87

70

Measuring Betas

Dell Computer

Slope determined from plotting the line of best fit.

Price data: Dec 97 - Apr 04

R2 = .27

B = 1.61

71

Measuring Betas

General Motors

Slope determined from plotting the line of best fit.

R2 = .07

B = 0.72

Price data: May 91- Nov 97

72

Measuring Betas

General Motors

Slope determined from plotting the line of best fit.

GM

return (%)R2 = .29

B = 1.21

Price data: Dec 97 - Apr 04

73

Estimated Betas

Beta equity

Standard Error

Burlington Northern & Santa Fe 0.53 0.2

CSX Transportation 0.58 0.23Norfolk Southern 0.47 0.28

Union Pacific Corp 0.47 0.19Industry portfolio 0.49 0.18

74

Beta Stability

% IN SAME % WITHIN ONE RISK CLASS 5 CLASS 5 CLASS YEARS LATER YEARS LATER

10 (High betas) 35 69

9 18 54

8 16 45

7 13 41

6 14 39

5 14 42

4 13 40

3 16 45

2 21 61

1 (Low betas) 40 62

Source: Sharpe and Cooper (1972)

75

Using an Industry Beta

• It is frequently argued that one can better estimate a firm’s beta by involving the whole industry.

• If you believe that the operations of the firm are similar to the operations of the rest of the industry, you should use the industry beta.

• If you believe that the operations of the firm are fundamentally different from the operations of the rest of the industry, you should use the firm’s beta.

76

Problems with Industry Beta

One must make sure that the firm is comparable to other industry both in its operation and its financing.

Question: Consider Grand Sport, Inc., which is currently all-equity and has a beta of 0.90. The firm has decided to lever up to a capital structure of 50% debt and 50% equity. Since the firm will remain in the same industry, its asset beta should remain 0.90.

Assuming a zero beta for its debt, what should the equity beta be?

77

Beware of Fudge Factors

• Common practice to make adjustments to discount rate to offset worries.

Example:

1) A new drug won’t get FDA approval and won’t be able to go on the market.

2) Unexpected weather condition would hurt the crop.

78

Determinants of Beta

• Business Risk– Cyclicality of Revenues

– Operating Leverage

• Financial Risk– Financial Leverage

79

Cyclicality of Revenues

• Highly cyclical stocks have high betas.– Empirical evidence suggests that retailers

and automotive firms fluctuate with the business cycle.

– Transportation firms and utilities are less dependent upon the business cycle.

80

Operating Leverage

• The degree of operating leverage measures how sensitive a firm (or project) is to its fixed costs.

• Operating leverage increases as fixed costs rise and variable costs fall.

• Operating leverage magnifies the effect of cyclicality on beta.

• The degree of operating leverage is given by:

Salesin Change

Salesin Change

EBIT

EBITDOL

81

Operating Leverage

Volume

$

Fixed costs

Total costs

EBIT

Volume

Operating leverage increases as fixed costs rise and variable costs fall.

Fixed costs

Total costs

82

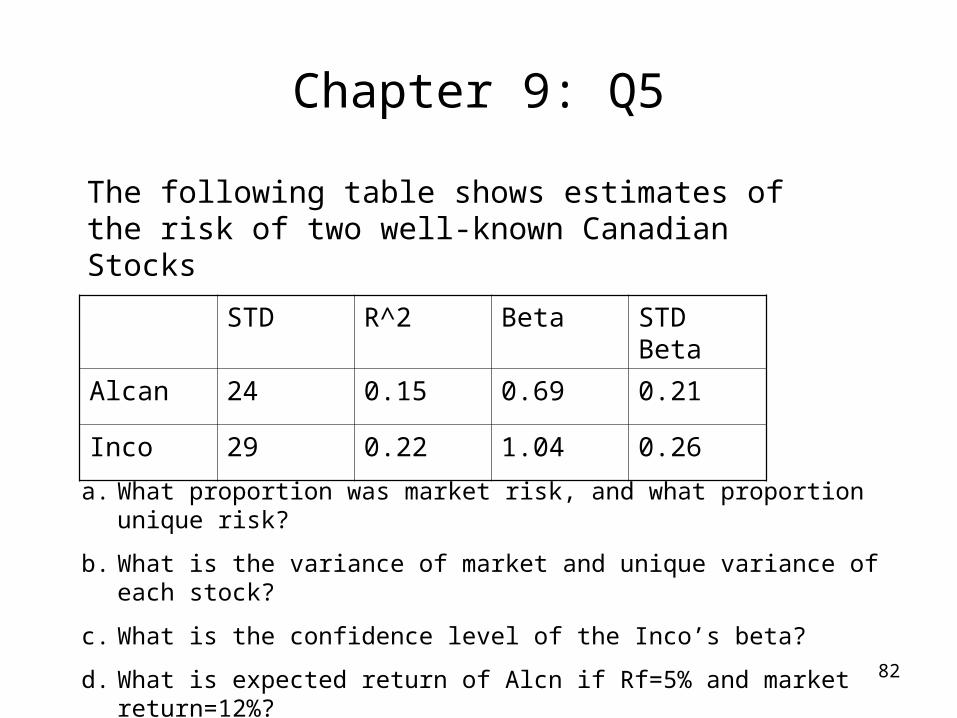

Chapter 9: Q5

The following table shows estimates of the risk of two well-known Canadian Stocks

STD R^2 Beta STD Beta

Alcan 24 0.15 0.69 0.21

Inco 29 0.22 1.04 0.26

a. What proportion was market risk, and what proportion unique risk?

b. What is the variance of market and unique variance of each stock?

c. What is the confidence level of the Inco’s beta?

d. What is expected return of Alcn if Rf=5% and market return=12%?

e. Suppose next year the market provides a zero return. What return to you expect for each stock?

83

Chapter 9: Q9You run a perpetual encabulator machine, which generates revenues averaging $20 million per year. Raw material costs are 50 percent of revenues. These costs are variable – they are always proportional to revenues. There are no other operating costs. The cost of capital is 9 percent. Your firm’s long-term borrowing rate is 6 percent. Now you are approached by Studebaker Capital Corp., which proposes a fixed-price contract to supply raw materials at $10 million per year for 10 years.

a. What happens to the operating leverage and business risk of the encabulator machine if you agree to this fixed-price contact?

b. Calculate the present value of the encabulator machine with and without the fixed-price contract?

84

Chapter 9 (part 2) Capital Budgeting and Risk

tf

tt

t

r

CEQ

r

CPV

)1()1(

85

Risk,DCF and CEQ

Example

Project A is expected to produce CF = $100 mil for each of three years. Given a risk free rate of 6%, a market premium of 8%, and beta of .75, what is the PV of the project?

86

Risk,DCF and CEQ

Example

Project A is expected to produce CF = $100 mil for each of three years. Given a risk free rate of 6%, a market premium of 8%, and beta of .75, what is the PV of the project?

%12

)8(75.6

)(

fmf rrBrr

240.2 PVTotal

71.21003

79.71002

89.31001

12% @ PV FlowCashYear

AProject

87

Risk,DCF and CEQ

ExampleProject B cash flow is 94.6, 89.6, 84.8 in year 1-3 respectively. However, these cash flows are RISK FREE. What is Project’s B PV?

240.2 PVTotal

71.284.83

79.789.62

89.394.61

6% @ PV FlowCashYear

Project B

240.2 PVTotal

71.21003

79.71002

89.31001

12% @ PV FlowCashYear

AProject

88

Risk,DCF and CEQ

240.2 PVTotal

71.284.83

79.789.62

89.394.61

6% @ PV FlowCashYear

Project B

240.2 PVTotal

71.21003

79.71002

89.31001

12% @ PV FlowCashYear

AProject

Since the 94.6 is risk free, we call it a Certainty Equivalent of the 100.

89

Risk,DCF and CEQ

ExampleProject A is expected to produce CF = $100 mil for each of three years. Given a risk free rate of 6%, a market premium of 8%, and beta of .75, what is the PV of the project?.. Now assume that the cash flows change, but are RISK FREE. What is the new PV?

The difference between the 100 and the certainty equivalent (94.6) is 5.7%…this % can be considered the annual premium on a risky cash flow

flow cash equivalentcertainty flow cashRisky

057.1

90

Long lived assets and discount rates

Example (from text): The scientists at Vegetron have come up with an electric mop and are ready to go ahead with pilot production. The preliminary phase will take one year and costs $125k. Management feels that there is only a 50% chance that the pilot production will be successful. If the project fails, the project will be dropped. If the project succeeds Vegetron will build a $1million plant that would generate an expected annual cash flow in perpetuity of $250k. Rf=7%, Risk Premium=9%. Regular projects of the firm have a beta of 0.33, however due to the 50% probability of failure management assumes a beta of 2 for the project.

1. What is NPV? 2. Is management correct about its approach for the NPV

calculation?

91

International Projects

• Investment projects abroad may be safer than similar domestic investments.

• Remember: Beta measures risk relative to investor’s portfolio (a good question would be to ask who is the investor of the company?)

• Not clear why home bias persists so strongly (perhaps information, transaction costs, etc.)

92

What is Liquidity?

• The idea that the expected return on a stock and the firm’s cost of capital are positively related to risk is fundamental.

• Recently a number of academics have argued that the expected return on a stock and the firm’s cost of capital are negatively related to the liquidity of the firm’s shares as well.

• The trading costs of holding a firm’s shares include brokerage fees, the bid-ask spread, and market impact costs.

93

Liquidity, Expected Returns, and the Cost of Capital

• The cost of trading an illiquid stock reduces the total return that an investor receives.

• Investors thus will demand a high expected return when investing in stocks with high trading costs.

• This high expected return implies a high cost of capital to the firm.

94

Liquidity and the Cost of Capital

Cos

t of

Cap

ital

LiquidityAn increase in liquidity, i.e., a reduction in trading costs, lowers a firm’s cost of capital.

95

Liquidity and Adverse Selection

• There are a number of factors that determine the liquidity of a stock.

• One of these factors is adverse selection.• This refers to the notion that traders with better

information can take advantage of specialists and other traders who have less information.

• The greater the heterogeneity of information, the wider the bid-ask spreads, and the higher the required return on equity.

96

What the Corporation Can Do

• The corporation has an incentive to lower trading costs since this would result in a lower cost of capital.

• A stock split would increase the liquidity of the shares.

• A stock split would also reduce the adverse selection costs thereby lowering bid-ask spreads.

• This idea is a new one and empirical evidence is not yet in.

97

What the Corporation Can Do

• Companies can also facilitate stock purchases through the Internet.

• Direct stock purchase plans and dividend reinvestment plans handled on-line allow small investors the opportunity to buy securities cheaply.

• The companies can also disclose more information, especially to security analysts, to narrow the gap between informed and uninformed traders. This should reduce spreads.

98

Summary and Conclusions• The expected return on any capital budgeting

project should be at least as great as the expected return on a financial asset of comparable risk. Otherwise the shareholders would prefer the firm to pay a dividend.

• The expected return on any asset is dependent upon .

• A project’s required return depends on the project’s .

• A project’s can be estimated by considering comparable industries or the cyclicality of project revenues and the project’s operating and financial leverage.

99

Jones Family Mini-Case

Executive summary:• The wildcat oil well is going to cost $5 million.• The Jones geologists says there’s only 30% chance of a dry hole.• If oil is found, the expectation is for 300 barrels of crude oil per day

(at a price of $25 per barrel)• Sales will start next year.• Production and shipping costs are $10 per barrel (Mr. Jones argues

that they are fixed).• Production will start declining at 5% every year.• Oil prices expected to grow at 2.5% per year, and pumping will

continue for 15 years.• The interest rate is 6%, the beta is 0.8, and the risk premium is 7%.

100

Chapter 10: Decision Trees• A fundamental problem in NPV analysis is

dealing with uncertain future outcomes.• There is usually a sequence of decisions in

NPV project analysis.• Decision trees are used to identify the

sequential decisions in NPV analysis.• Decision trees allow us to graphically represent

the alternatives available to us in each period and the likely consequences of our actions.

• This graphical representation helps to identify the best course of action.

101

Example of Decision Tree

Do not study

Study finance

Open circles represent decisions to be made.

Filled circles represent receipt of information

e.g., a test score in this class.

The lines leading away from the circles represent

the alternatives.

“C”

“A”

“B”

“F”

“D”

Pay wizard $1000?

102

Stewart Pharmaceuticals • The Stewart Pharmaceuticals Corporation is considering

investing in developing a drug that cures the common cold.• A corporate planning group, including representatives from

production, marketing, and engineering, has recommended that the firm go ahead with the test and development phase.

• This preliminary phase will last one year and cost $1 billion. Furthermore, the group believes that there is a 60% chance that tests will prove successful.

• If the initial tests are successful, Stewart Pharmaceuticals can go ahead with full-scale production. This investment phase will cost $1,600 million. Production will occur over the next four years.

103

Stewart Pharmaceuticals NPV of Full-Scale Production following Successful Test

Note that the NPV is calculated as of date 1, the date at which the investment of $1,600 million is made. Later we bring this number back to date 0.

Investment Year 1 Years 2-5

Revenues $7,000

Variable Costs (3,000)

Fixed Costs (1,800)

Depreciation (400)

Pretax profit $1,800

Tax (34%) (612)

Net Profit $1,188

Cash Flow -$1,600 $1,588

75.433,3$)10.1(

588,1$600,1$

4

1

t

tNPV

104

Stewart Pharmaceuticals NPV of Full-Scale Production following Unsuccessful Test

Note that the NPV is calculated as of date 1, the date at which the investment of $1,600 million is made. Later we bring this number back to date 0.

Investment Year 1 Years 2-5

Revenues $4,050

Variable Costs (1,735)

Fixed Costs (1,800)

Depreciation (400)

Pretax profit $115

Tax (34%) (39.10)

Net Profit $75.90

Cash Flow -$1,600 $475

461.91$)10.1(

90.475$600,1$

4

1

t

tNPV

105

Decision Tree for Stewart Pharmaceutical

Do not test

Test

Failure

Success

Do not invest

Invest

Invest

The firm has two decisions to make:To test or not to test.To invest or not to invest.

0$NPV

NPV = $0

mNPV 461.91$

mNPV 75.433,3$

106

Stewart Pharmaceutical: Decision to Test

• Let’s move back to the first stage, where the decision boils down to the simple question: should we invest?

• The expected payoff evaluated at date 1 is:

failuregiven

Payoff

failure

Prob.

successgiven

Payoff

sucess

Prob.

payoff

Expected

25.060,2$0$40.75.433,3$60.payoff

Expected

95.872$10.1

25.060,2$000,1$ NPV

• The NPV evaluated at date 0 is:

So we should test.

107

Real Options

• One of the fundamental insights of modern finance theory is that options have value.

• The phrase “We are out of options” is surely a sign of trouble.

• Because corporations make decisions in a dynamic environment, they have options that should be considered in project valuation.

108

Options

The Option to Expand• Static analysis implicitly assumes that the scale of the

project is fixed.• If we find a positive NPV project, we should consider the

possibility of expanding the project to get a larger NPV.• For example,the option to expand has value if demand

turns out to be higher than expected.• All other things being equal, we underestimate NPV if we

ignore the option to expand.The Option to Delay• Has value if the underlying variables are changing with a favourable trend.

109

The Option to Expand: Example

• Imagine a start-up firm, Campusteria, Inc. which plans to open private (for-profit) dining clubs on university campuses.

• The test market will be your campus, and if the concept proves successful, expansion will follow nationwide.

• Nationwide expansion, if it occurs, will occur in year four.

• The start-up cost of the test dining club is only $30,000 (this covers leaseholder improvements and other expenses for a vacant restaurant near campus).

110

Campusteria pro forma Income Statement

Investment Year 0 Years 1-4

Revenues $60,000

Variable Costs ($42,000)

Fixed Costs ($18,000)

Depreciation ($7,500)

Pretax profit ($7,500)

Tax shield 34% $2,550

Net Profit –$4,950

Cash Flow –$30,000 $2,550

We plan to sell 25 meal plans at $200 per month with a 12-month contract.

Variable costs are projected to be $3,500 per month.

Fixed costs (the lease payment) are projected to be $1,500 per month.

We can depreciate (straight line) our capitalized leaseholder improvements.

84.916,21$)10.1(

550,2$000,30$

4

1

t

tNPV

111

The Option to Expand: Valuing a Start-Up

• Note that while the Campusteria test site has a negative NPV, its negativity is relatively small.

• If we expand, we project opening 20 Campusterias in year four and the size of the project may grow 20 folds.

• The value of the project is in the option to expand. • If we hit it big, we will be in a position to score large.• We won’t know if this has value if we do not try. Thus, it

seems that we may want to take on this test project and see what it delivers.

112

Discounted Cash Flows and Options

• We can calculate the market value of a project as the sum of the NPV of the project without options and the value of the managerial options implicit in the project.

M = NPV + Opt

A good example would be comparing the desirability of a specialized machine versus a more versatile machine. If they both cost about the same and last the same amount of time the more versatile machine is more valuable because it comes with options.

113

The Option to Abandon: Example• The option to abandon a project has value if demand

turns out to be lower than expected.• Suppose that we are drilling an oil well. The drilling rig

costs $300 today and in one year the well is either a success or a failure.

• The outcomes are equally likely. The discount rate is 10%.

• The PV of the successful payoff at time one is $575.• The PV of the unsuccessful payoff at time one is $0.

114

The Option to Abandon: Example (continued)

Traditional NPV analysis would indicate rejection of the project.

NPV = = –$38.641.10

$287.50–$300 +

Expected Payoff

= (0.50×$575) + (0.50×$0) = $287.50

=Expected Payoff

Prob. Success

× Successful Payoff

+ Prob. Failure

× Failure Payoff

115

The Option to Abandon: Example

The firm has two decisions to make: drill or not, abandon or stay.

Do not drill

Drill

0$NPV

300$

Failure

Success: PV = $575

Sell the rig; salvage value

= $250

Sit on rig; stare at empty hole:

PV = $0.

Traditional NPV analysis overlooks the option to abandon.

116

• When we include the value of the option to abandon, the drilling project should proceed:

NPV = = $75.001.10

$412.50–$300 +

Expected Payoff

= (0.50×$575) + (0.50×$250) = $412.50

=Expected Payoff

Prob. Success

× Successful Payoff

+ Prob. Failure

× Failure Payoff

The Option to Abandon: Example (continued)

117

Valuation of the Option to Abandon

• Recall that we can calculate the market value of a project as the sum of the NPV of the project without options and the value of the managerial options implicit in the project. OptNPVM

Opt 64.3800.75$

Opt 64.3800.75$

64.113$Opt

118

The Option to Delay: Example

• Consider the above project, which can be undertaken in any of the next 4 years. The discount rate is 10 percent. The present value of the benefits at the time the project is launched remain constant at $25,000, but since costs are declining the NPV at the time of launch steadily rises.

• The best time to launch the project is in year 2—this schedule yields the highest NPV when judged today.

Year Cost PV NPV t

0 20,000$ 25,000$ 5,000$ 1 18,000$ 25,000$ 7,000$ 2 17,100$ 25,000$ 7,900$ 3 16,929$ 25,000$ 8,071$ 4 16,760$ 25,000$ 8,240$

2)10.1(

900,7$529,6$

Year Cost PV NPV t NPV 0

0 20,000$ 25,000$ 5,000$ 5,000$ 1 18,000$ 25,000$ 7,000$ 6,364$ 2 17,100$ 25,000$ 7,900$ 6,529$ 3 16,929$ 25,000$ 8,071$ 6,064$ 4 16,760$ 25,000$ 8,240$ 5,628$

119

Option issues to consider

Things to remember in these types of analysis: • Cost of the testing• Expected future cash flows given the outcome

of the test• Probability of success of the testing• Discount rate