1

Chapter 6Trade-Off Between Risk &

Return

Chapter 7

Risk, Return, and the CAPM

2

Today’s Chapter 6 & 7 Topics

Historical Trade-Off between Risk and Return

Historical Risk Premiums

Calculation of Historical Return and Risk

Portfolio Return and Risk

Calculation of Probabilistic Expected Return & Risk

Risk Diversification Unsystematic &

Systematic Risk

3

Risk and Return

Valuing risky assets - a task fundamental to financial management

Three-step procedure for valuing a risky asset

1. Determine the asset’s expected cash flows2. Choose discount rate that reflects asset’s risk3. Calculate present value (PV cash inflows - PV

outflows)

The three-step procedure is called discounted cash flow (DCF) analysis.

4

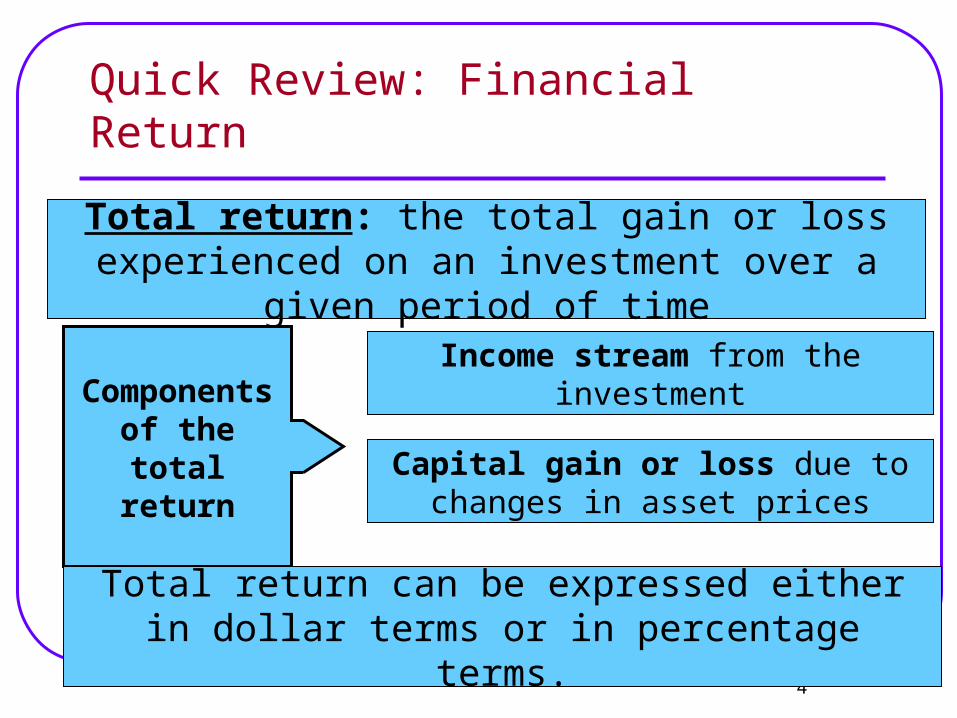

Quick Review: Financial Return

Total return: the total gain or loss experienced on an investment over a given

period of time

Components of the

total return

Income stream from the investment

Capital gain or loss due to changes in asset prices

Total return can be expressed either in dollar terms or in percentage terms.

5

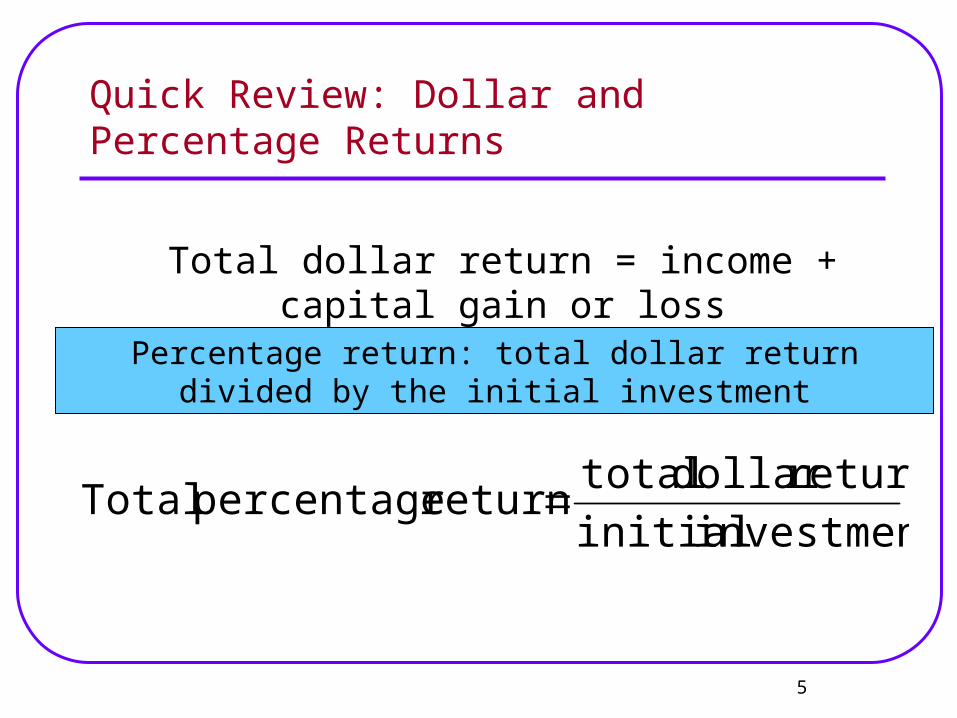

Quick Review: Dollar and Percentage Returns

Total dollar return = income + capital gain or loss

Percentage return: total dollar return divided by the initial investment

investment initialreturndollar total

return percentage Total

6

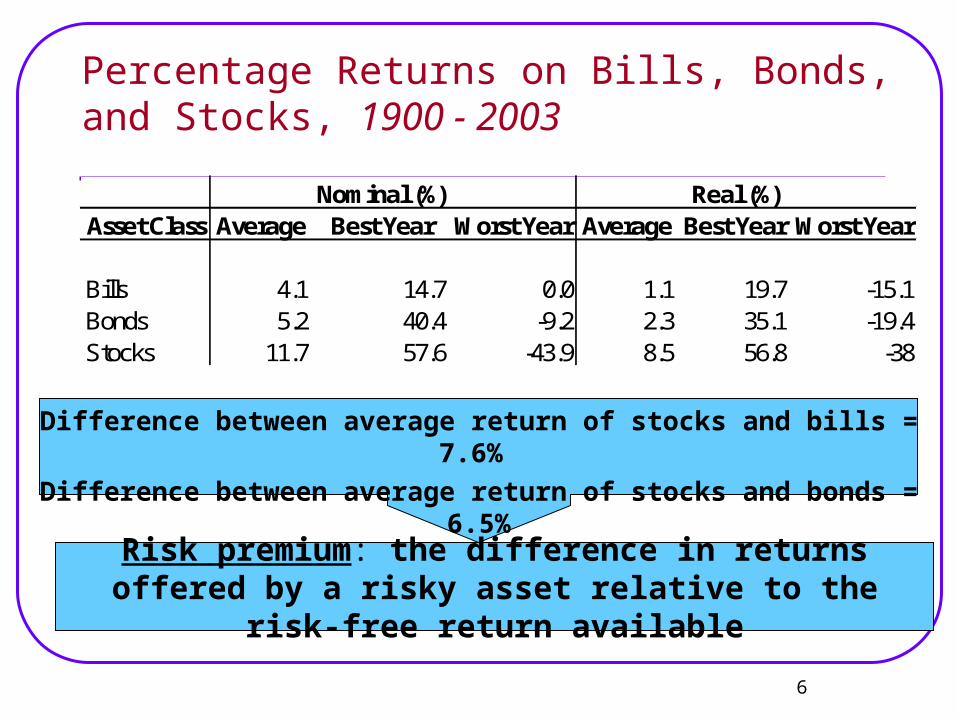

Percentage Returns on Bills, Bonds, and Stocks, 1900 - 2003

Difference between average return of stocks and bills = 7.6%

Difference between average return of stocks and bonds = 6.5%

Risk premium: the difference in returns offered by a risky asset relative to the risk-free return

available

Nominal (%) Real (%)Asset Class Average Best Year Worst Year Average Best Year Worst Year

Bills 4.1 14.7 0.0 1.1 19.7 -15.1Bonds 5.2 40.4 -9.2 2.3 35.1 -19.4Stocks 11.7 57.6 -43.9 8.5 56.8 -38

7

Variability of Stock Returns

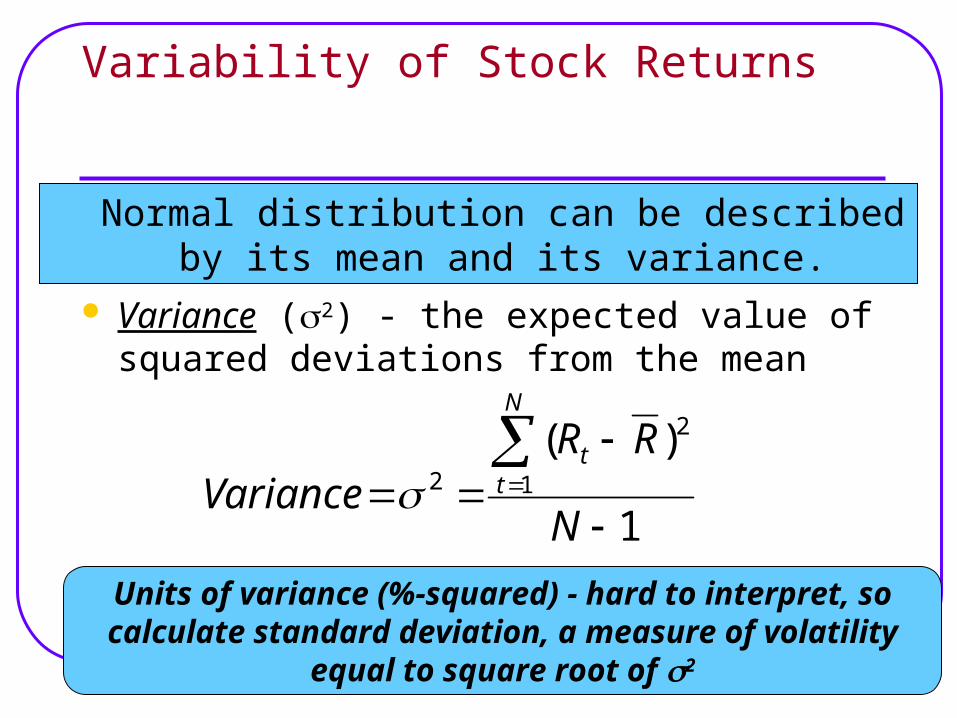

Normal distribution can be described by its mean and its variance.

Variance (2) - the expected value of squared deviations from the mean

1

)(1

2

2

N

RRVariance

N

tt

Units of variance (%-squared) - hard to interpret, so calculate standard deviation, a

measure of volatility equal to square root of 2

8

Volatility of Asset Returns

Asset Average(%) Std. Dev. (%) Average(%) Std. Dev. (%)

Equities 11.7 20.1 8.5 20.4Bonds 5.2 8.2 2.3 10Bills 4.1 2.8 1.1 4.7

Nominal Returns Real Returns

Asset classes with greater volatility pay higher average returns.

Average return on stocks is more than double the average return on bonds, but stocks are 2.5 times more volatile.

9

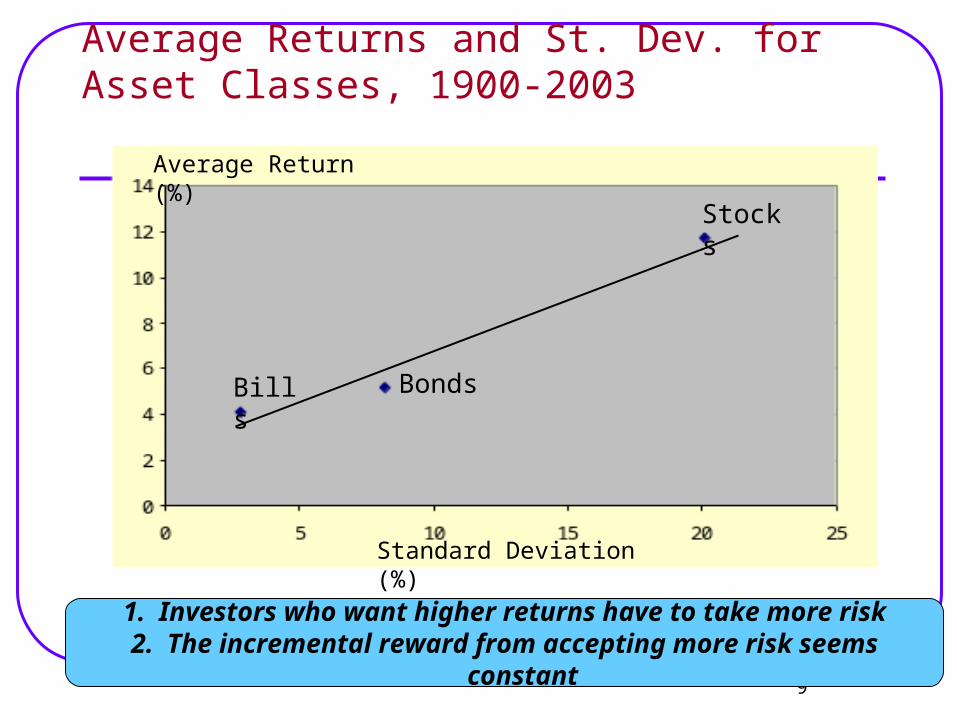

Average Returns and St. Dev. for Asset Classes, 1900-2003

1. Investors who want higher returns have to take more risk

2. The incremental reward from accepting more risk seems constant

Bills Bonds

Stocks

Average Return (%)

Standard Deviation (%)

10

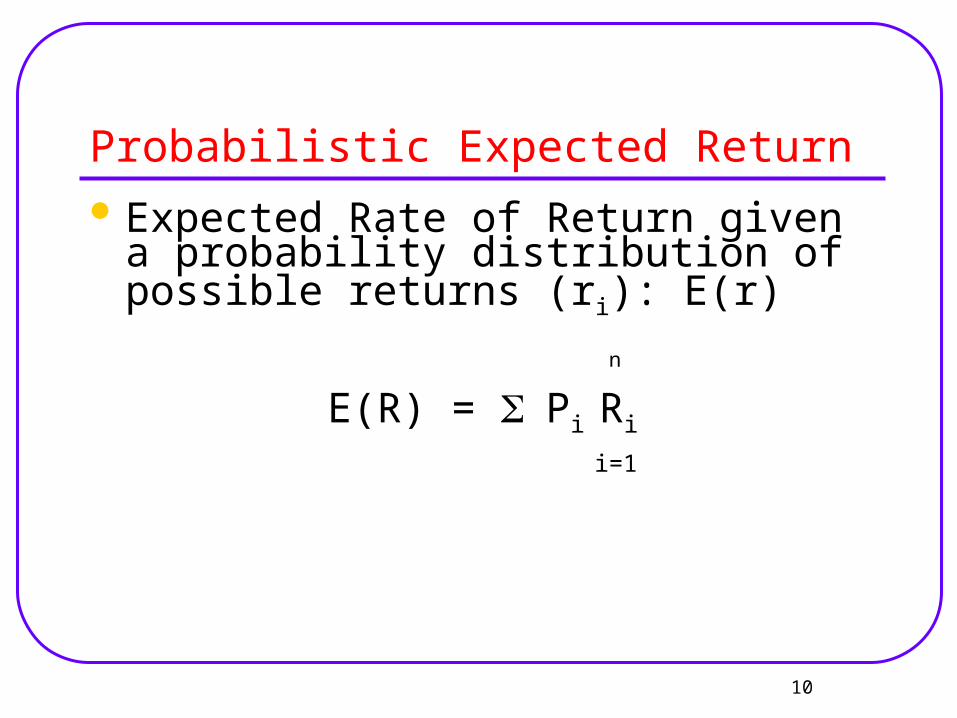

Probabilistic Expected Return Expected Rate of Return given a

probability distribution of possible returns (ri): E(r)

n

E(R) = Pi Ri

i=1

11

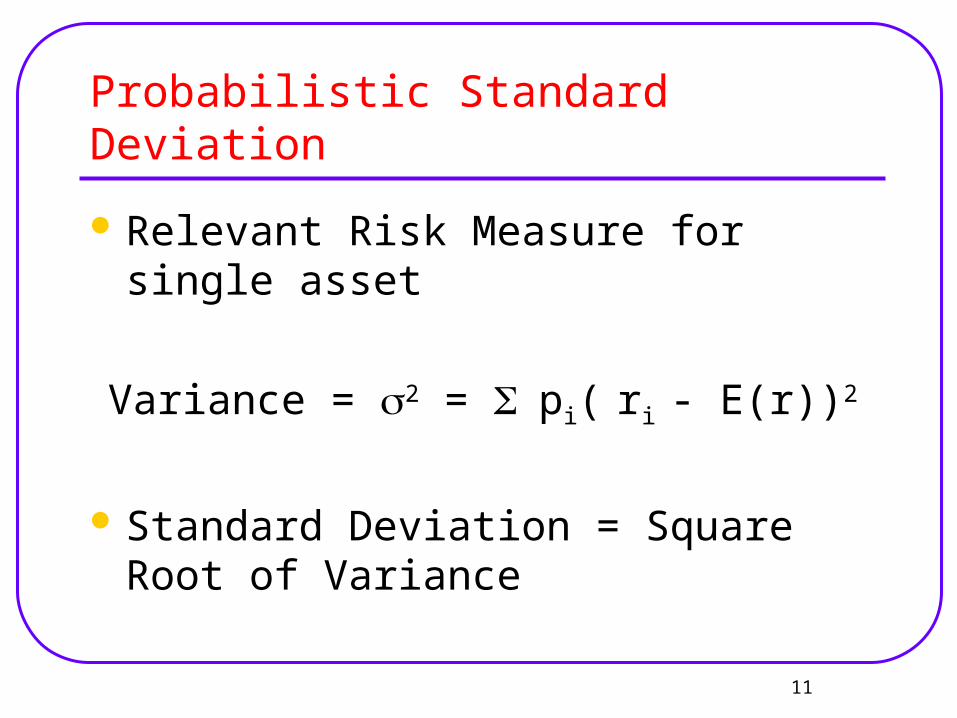

Probabilistic Standard Deviation

Relevant Risk Measure for single asset

Variance = 2 = pi( ri - E(r))2

Standard Deviation = Square Root of Variance

12

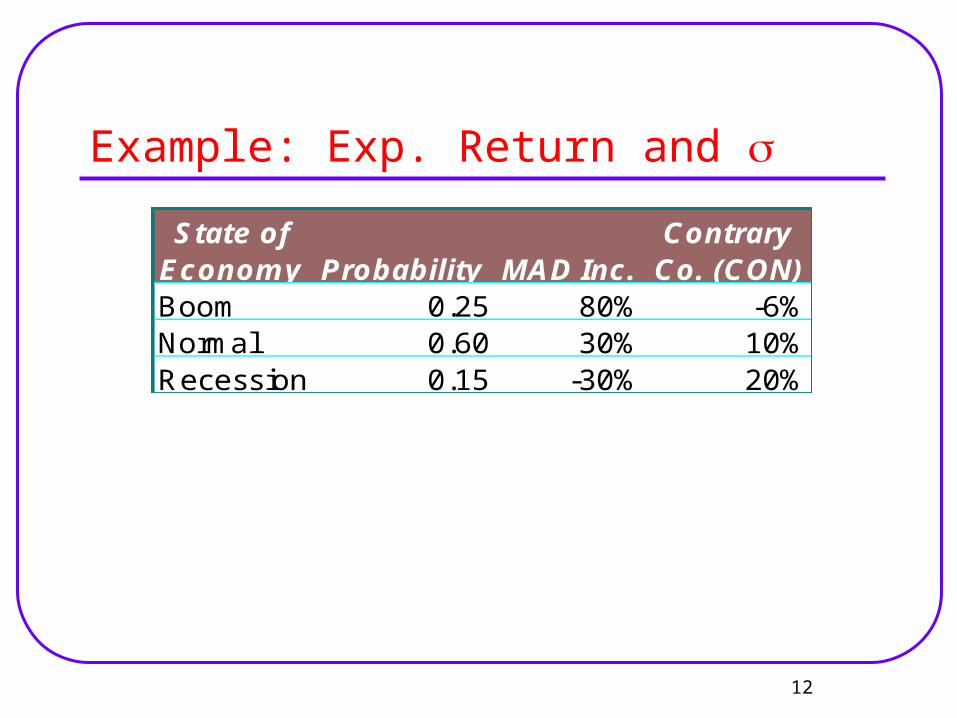

Example: Exp. Return and

State of ContraryEconomy Probability MAD Inc. Co. (CON)Boom 0.25 80% -6%Normal 0.60 30% 10%Recession 0.15 -30% 20%

13

Example: Standard Deviation

14

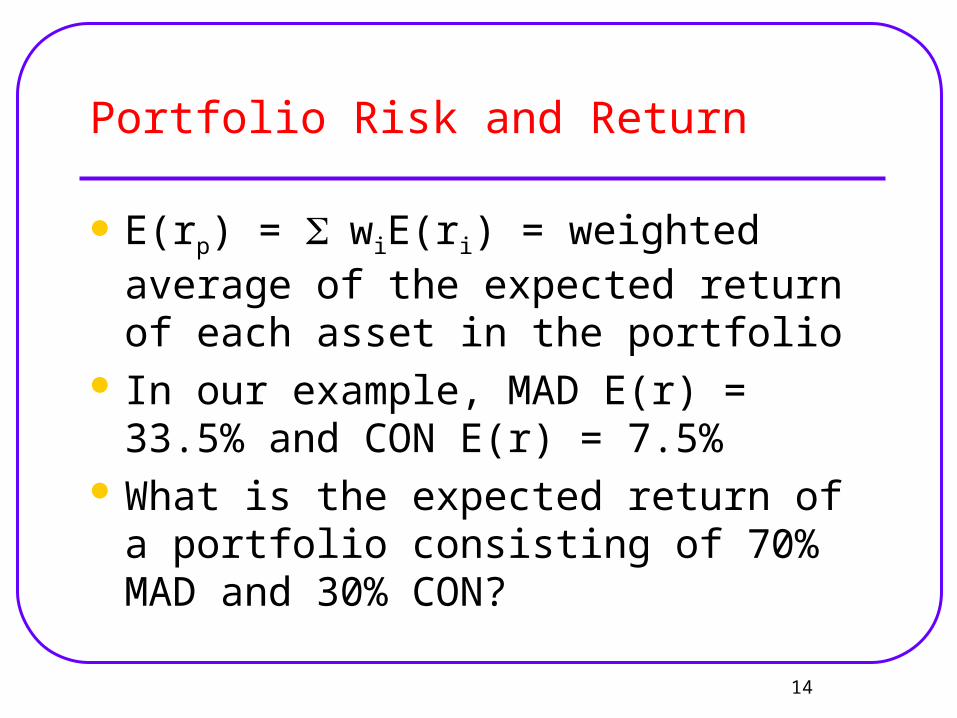

Portfolio Risk and Return

E(rp) = wiE(ri) = weighted average of the expected return of each asset in the portfolio

In our example, MAD E(r) = 33.5% and CON E(r) = 7.5%

What is the expected return of a portfolio consisting of 70% MAD and 30% CON?

15

Risk and Diversification

Portfolio rate

of return=

fraction of portfolio

in first assetx

rate of return

on first asset

+fraction of portfolio

in second assetx

rate of return

on second asset

E(rp) = wiE(ri) = .7(33.5%) + .3(7.5%) = 25.7%

((

((

))

))

16

Portfolio Risk

Looking at a 2-asset portfolio for simplicity, the riskiness of a portfolio is determined by the relationship between the returns of each asset over different scenarios or over time.

This relationship is measured by the correlation coefficient( ): -1<= < =+1

Lower = less portfolio risk compared to the weighted average of the standard deviations.

17

Example 70% MAD, 30% CON Portfolio State of Contrary MAD-CONEconomy Probability MAD Inc. Co. (CON) PortfolioBoom 0.25 80% -6% 54.2%Normal 0.60 30% 10% 24.0%Recession 0.15 -30% 20% -15.0%

18

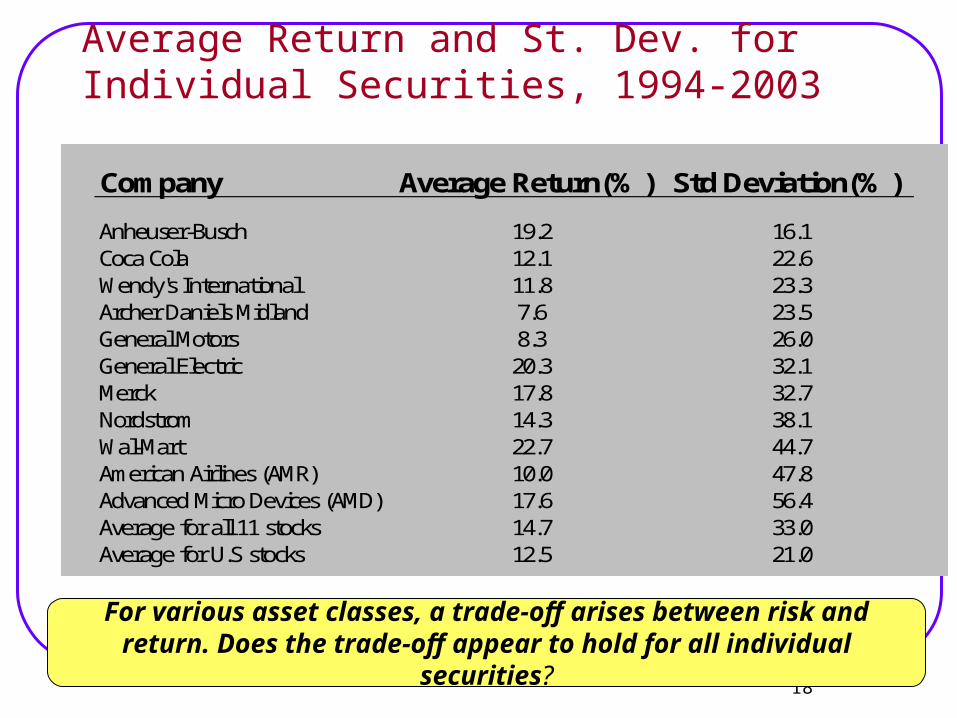

Average Return and St. Dev. for Individual Securities, 1994-2003

For various asset classes, a trade-off arises between risk and return. Does the trade-off appear to hold for all

individual securities?

Company Average Return(%) Std Deviation(%)

Anheuser-Busch 19.2 16.1Coca Cola 12.1 22.6Wendy's International 11.8 23.3Archer Daniels Midland 7.6 23.5General Motors 8.3 26.0General Electric 20.3 32.1Merck 17.8 32.7Nordstrom 14.3 38.1Wal-Mart 22.7 44.7American Airlines (AMR) 10.0 47.8Advanced Micro Devices (AMD) 17.6 56.4Average for all 11 stocks 14.7 33.0Average for U.S stocks 12.5 21.0

19

Average Return and St. Dev. for Individual Securities, 1994-2003

Average Return (%)

Standard Deviation (%)

Wal-MartAnheuser-Busch

Archer Daniels Midland

American Airlines

No obvious pattern here

20

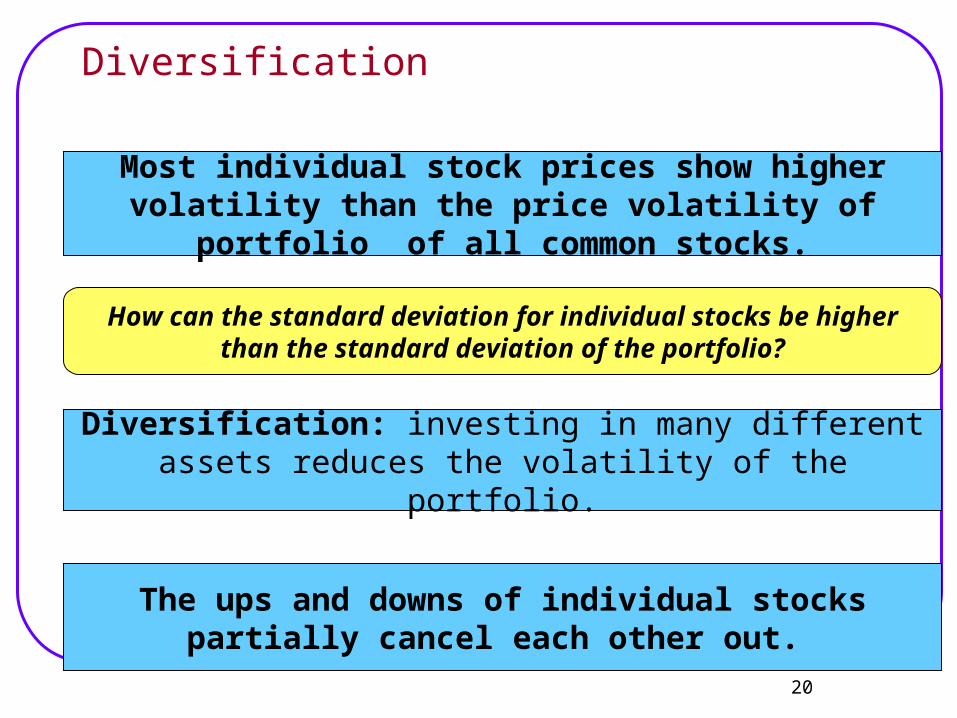

Diversification

Most individual stock prices show higher volatility than the price volatility of portfolio

of all common stocks.

How can the standard deviation for individual stocks be higher than the standard deviation of the portfolio?

Diversification: investing in many different assets reduces the volatility of the portfolio.

The ups and downs of individual stocks partially cancel each other out.

21

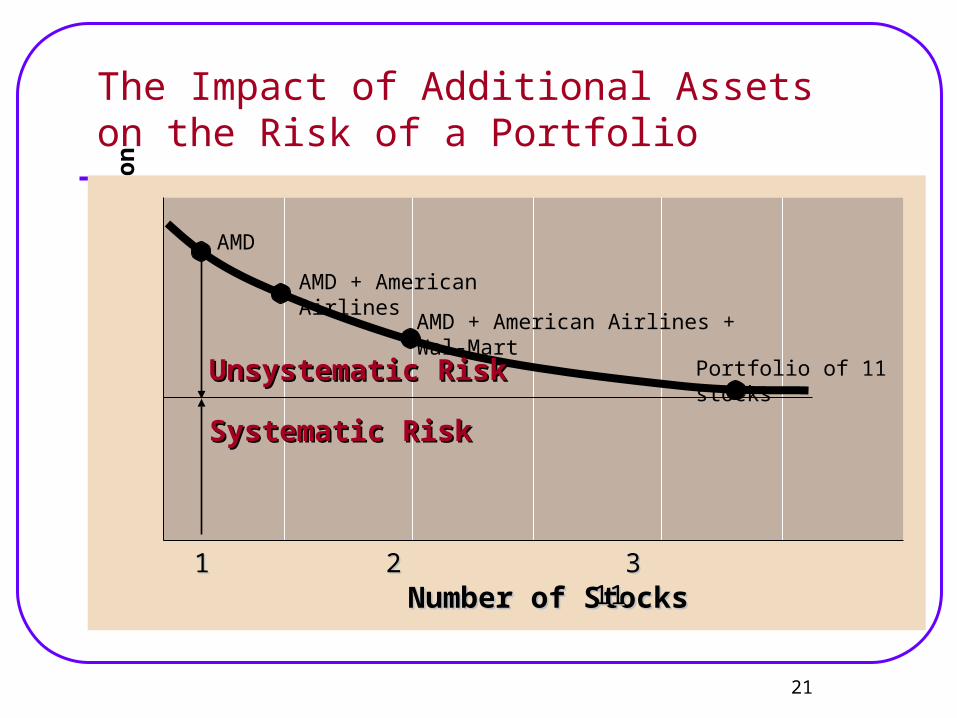

The Impact of Additional Assets on the Risk of a Portfolio

Po

rtfo

lio

Sta

nd

ard

Dev

iati

on

Number of StocksNumber of Stocks

Systematic RiskSystematic Risk

1 2 3 111 2 3 11

Portfolio of 11 stocks

AMD

Unsystematic RiskUnsystematic Risk

AMD + American Airlines

AMD + American Airlines + Wal-Mart

22

Diversification reduces portfolio volatility, but only up to a point. Portfolio of all stocks still

has a volatility of 21%.

Systematic risk: the volatility of the portfolio that cannot be eliminated through

diversification.

Unsystematic risk: the proportion of risk of individual assets that can be eliminated

through diversification

What really matters is systematic risk….how a group of assets move together.

Systematic and Unsystematic Risk

23

Systematic and Unsystematic Risk

The tradeoff between standard deviation and average returns that holds for asset classes

does not hold for individual stocks.

Because investors can eliminate unsystematic risk through diversification, market rewards

only systematic risk.

Standard deviation contains both systematic and unsystematic risk.