1

Chapter 2

Introductio

n to Transaction Processing

COPYRIGHT © 2007 Thomson South-Western, a part of The Thomson Corporation. Thomson, the Star logo,

and South-Western are trademarks used herein under license

2

Objectives for Chapter 2

Broad objectives of transaction cyclesTypes of transactions processed by each

of the three transaction cyclesThe basic accounting records used in TPSThe traditional accounting records and

their magnetic equivalents Documentation techniquesBatch and real-time processing and the

impact of these technologies on transaction processing

3

Cycles

Revenue CycleExpenditure CycleConversion Cycle

4

SubCycles

Revenue Cycle: time lag between sub-cycles due to credit relations with customers : physical component (sales to customers) financial component (cash receipts from customers)

Expenditure Cycle: time lag between sub-cycles due to credit relations with suppliers: physical component (acquisition of goods from suppliers) financial component (cash disbursements to suppliers)

Conversion Cycle : production system (planning, scheduling, and control of

physical product through manufacturing process) cost accounting system (monitors flow of cost information

related to production)

5

Manual System Accounting Records

Documents: Source - used to capture and formalize

transaction data needed for transaction processing (ex: Customer PO)

Product - result of transaction processing (ex: check)

Turnaround - product document of one system that becomes source document for another system (ex: remittance advice)

6

Manual System Accounting Records (continued)

Journals - record of chronological entry special journals - specific classes of

transactions that occur in high frequency (ex: sales journal)

general journal - nonrecurring, infrequent, and dissimilar transactions

Ledger - book of financial accounts general ledger - shows activity for each

account listed on chart of accounts subsidiary ledger - shows activity by detail for

each account type (ex: A/R sub. ledger)

7

Audit Trail (manual)

SourceDocument

JournalGeneralLedger

FinancialStatements

SourceDocument

JournalGeneralLedger

FinancialStatements

8

Computer-Based Systems (CBIS)

Audit trail is less observable in computer-based systems than traditional manual systems.

Data entry and computer programs are physical trail.

Data are stored in magnetic files.

9

Computer FilesMaster File - generally contains

cumulative account data (e.g., general ledger and subsidiary ledgers)

Transaction File - temporary file containing transactions since last update (journals)

Reference File - contains relatively constant information used in processing (e.g., tax tables, service fees)

Archive File - contains past transactions for reference purposes (History)

10

Documentation Techniques

Five common documentation techniques:

1. Entity Relationship Diagram2. Data Flow Diagrams3. Document Flowcharts4. System Flowcharts5. Program Flowcharts6. Record Layout Diagrams

11

Documentation Techniques

Three documentation techniques we study this semester:

1. Entity Relationship Diagram2. Document Flowcharts3. System Flowcharts

12

Entity Relationship Diagram (ERD)

A documentation technique to represent relationship between entities in system.

13

Cardinality

represents the numerical mapping between entities: one-to-one one-to-many many-to-many

Depends

on

business

rules !!

Sales-person

Car

Customer

is assigned

Entity Relationship Entity

1 1

Examples of Cardinalities

Company A

Sales-person

Car

Customer

is assigned

Entity Relationship Entity

M1

Examples of Cardinalities

Company B

16

Customer Orderplaces

Entity Relationship Entity

M1

Examples of Cardinalities

17

Vendor Inventorysupplies

Entity Relationship Entity

M M

Examples of Cardinalities

18

Flowcharts

19

Keys to successful document flowcharting

Create logical functions (usually departments)

Symbol sizes are standardized Most are same size; a few are smaller

(on page & off page connectors; file-blue symbols on previous slide)

Drag documents along!! (Copy/paste)Don’t violate “sandwich rule”Very few shortcuts

20

Document Flowcharts

illustrate relationship among processes and documents that flow between them

clearly depict separation of functions in system

21

System Flowcharts

used to represent relationship between key elements--input sources, programs, and output products--of computer systems

depict type of media being used (paper, magnetic disks, and terminals)

some symbols same in both document and system flowcharts

22

Databases

23

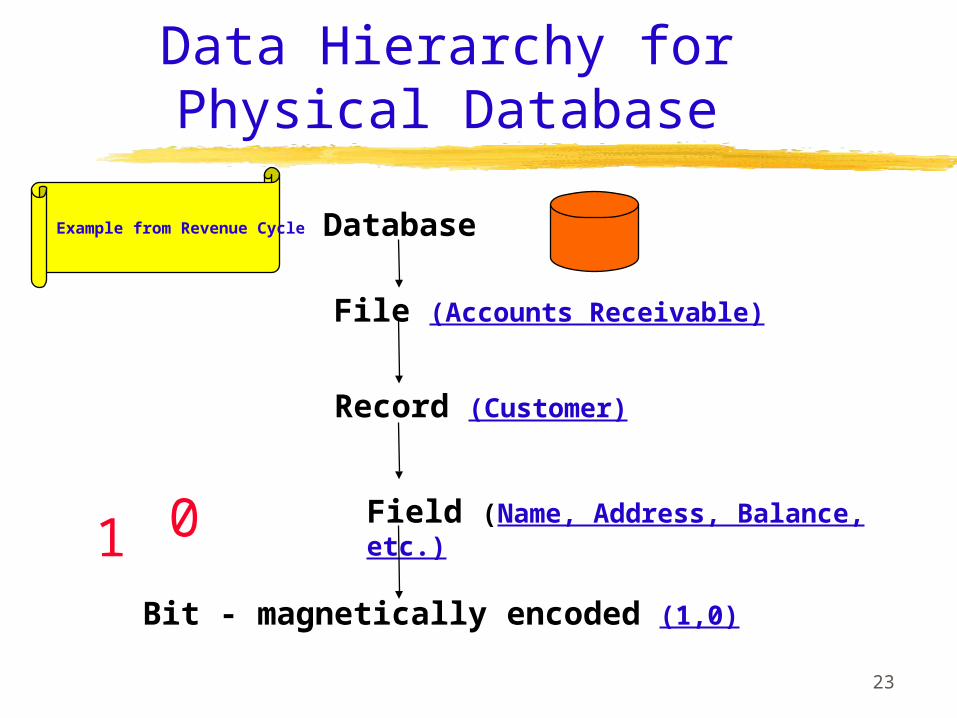

Data Hierarchy for Physical Database

Database

File (Accounts Receivable)

Record (Customer)

Field (Name, Address, Balance, etc.)

Bit - magnetically encoded (1,0)

1 0

Example from Revenue Cycle

24

Modern Systems versus Legacy Systems

Modern systems characteristics: client-server based and process transactions in real time use relational database tables have high degree of process integration and data

sharing some are mainframe based and use batch processing

Some firms still employ legacy systems for certain aspects of data processing; therefore accountants need to understand legacy systems.

Legacy systems characteristics: mainframe-based applications batch oriented early legacy systems use flat files for data storage later legacy systems use hierarchical and network

databases data storage systems promote a single-user

environment that discourages information integration

25

Data Structures

allow records to be located, stored, retrieved and allow movement through database. Two components: organization of file is physical

arrangement of records (how they are stored)

access method is technique used to locate records and to navigate through database or file (how they are retrieved)

26

Sequential Access Structure

All records lie in contiguous storage spaces in specified sequence arranged by primary key.

Data retrieval requires that all records before desired record must be read in order first.

Cannot directly access record.

27

Direct Access Structures

Records are stored at unique locations known as addresses.

Address tells operating system exact location of record on disk.

Allows access to record without going through all preceding records.

28

Database Backup Procedures

• Destructive updates leave no backup.• To preserve adequate records, backup procedures must be

implemented, as shown below: The master file being updated is copied as a backup. A recovery program uses the backup to create a pre-

update version of the master file.

29

CBIS

Two broad classes of systems: Batch systems Real-time systems

30

Batch Processing

A batch is group of similar transactions that are accumulated over time and processed together.

Time lag between event and processing.

31

Advantages of Batch Processing

Organizations can increase efficiency by grouping similar transactions into batches rather than processing each event separately.

Batch processing provides control over transaction process via control figures.

Although-tradeoff between batch size and errors.

32

Real-Time Systemsprocess transactions individually at

moment economic event occursno time lag between economic event and

processinggenerally require greater resources

than batch processing because they require dedicated processing capacity; (however, these cost differentials are decreasing)

oftentimes have longer systems development time (for internally developed systems)

33

Why Do So Many AISs Use Batch Processing?

Much AIS processing characterized by high-volume, independent transactions: recording cash receipts checks received in

mail Payroll

Processing of such high-volume can be done during an off-peak computer time (overnight).

34