domiciles of alternative investment funds | current trends

TRANSCRIPT

www.nicsa.org

DOMICILES OF ALTERNATIVE INVESTMENT FUNDS – CURRENT TRENDS

21 April 2015

NICSA webinar sponsored by ALFI

www.nicsa.org

www.nicsa.org

• The following presentation analyses trends in choice of domicile for Alternative Investment Funds, prepared by Oliver Wyman for the Association of the Luxembourg Fund Industry (ALFI) in November 2014

• Alternative Investment Funds (AIFs) are defined as investment schemes that apply investment strategies typically not available to traditional mutual funds (e.g. UCITS). AIFs can be grouped into three main asset classes:– Hedge Funds– Private Equity funds– Real Estate funds

• The report examines only those domiciles attracting largest number of Alternative Investment Funds by number fund registrations and asset under management. These are:– The Cayman Islands– State of Delaware in the United States of America– Key AIF domiciles in the European Union: Luxembourg, Ireland and Malta– The Channel Islands comprising Jersey, Isle of Man and Guernsey– Other Caribbean Islands: Bermuda and British Virgin Islands (BVI)

• In order to ensure desired level of accuracy, the report uses publicly available information from local monetary authorities and industry associations (to the extent available), commonly used fund databases (e.g. Preqin, EurekaHedge, Monterey Insight). But since much data is not disclosed, this has been complemented by proprietary data and interviews with industry experts to derive estimates for AIF domicile choices

Introduction

www.nicsa.org

The number of Alternative Investment Funds has increased by 10% since 2010

www.nicsa.org

Domiciliation in the EU and the more traditional hubs of Delaware and Cayman Islands show the strongest growth

www.nicsa.org

Traditional offshore domiciles confirm their dominant role within the respective AIF asset classes

www.nicsa.org

In summary therefore, we see four main trends which we now examine in turn

www.nicsa.org

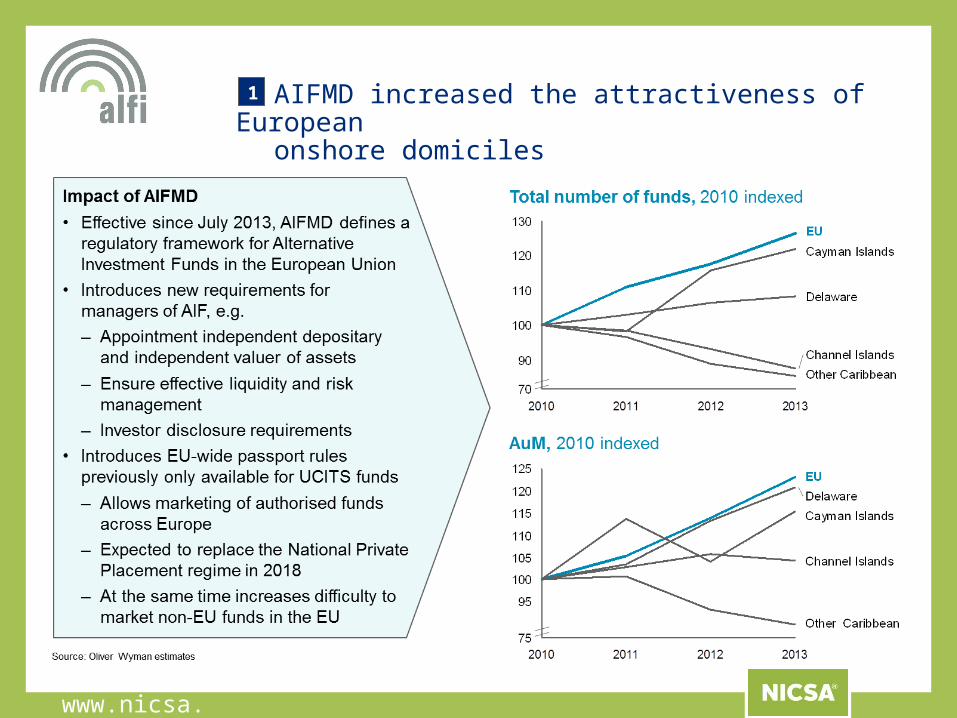

AIFMD increased the attractiveness of European onshore domiciles

1

www.nicsa.org

The three EU AIFs domiciles are all growing strongly, each with differing ‘sweet spots’

1

• Luxembourg with strong growth in Real Estate and Private Equity funds

– Number of RE and PE funds up by more than 35% since 2010 (estimate)

– Decreasing number of Hedge Funds and Fund of Funds since 2010

• Ireland with strong focus on Hedge Funds

– Large centre for Hedge Fund administration

– >60% growth in number of Hedge Funds since 2010

• Malta attracting niche markets within the hedge fund industry

– Focus on small funds, with Malta’s average fund size below €20m, compared with ~€80-120m for Luxembourg or Ireland

www.nicsa.org

Co-domiciliation is an increasingly favoured response for onshoring AIFs – evidence from Luxembourg and Ireland

1

www.nicsa.org

Demand for regulated AIFs triggered an increase in UCITS compliant replications of alternative investment strategies

2

www.nicsa.org

Moreover AIFs under regulated mutual fund structures also report significantly higher asset growth in the US through ’40 Act funds

2

www.nicsa.org

Domiciles offering ‘one-stop-shop’ solutions continue to attract funds at expense of domiciles with less well developed fund infrastructure

3

www.nicsa.org

The dominant position of traditionally successful domiciles seems entrenched

4

Cayman Islands has traditionally been seen as the global home of Hedge Funds and has strengthened that role over the last four years

www.nicsa.org

Around 60% of global offshore Hedge Fund assets are domiciled on the Cayman Islands

4

www.nicsa.org

Most Private Equity funds are domiciled in Delaware with Guernsey gaining some ground

4

www.nicsa.org

Delaware also remains an important domicile for Real Estate funds – with other Real Estate focused domiciles under pressure

4

www.nicsa.org

Summary of key success factors4

www.nicsa.org

Overall, we expect the demand for regulated AIFs to continue and the boundary between traditional AIFs and mutual funds to diminish yet further

www.nicsa.org

www.nicsa.org

Contacts at Oliver Wyman