domestic mergers companies act 2014 - mason …€¦ · chair john gulliver, tax partner and head...

TRANSCRIPT

Domestic Mergers – Companies Act 2014

14 June 2017

Chair John Gulliver, Tax Partner and Head of Tax Speakers Liam Brazil, Corporate Partner Kevin Foley, Audit & Assurance Partner, Grant Thornton Maura Dineen, Tax Partner

2

Introduction

Domestic Mergers

• Summary Approval Procedure (“SAP”)

• Court Approval

• Merger Accounting

• Tax

Questions

Conclusion

3

Irish Structure

4

Irish plc/Ltd/DAC

Irish Subsidiary

Irish Target

Classic Demerge and Sell

5

Irish plc/Ltd/DAC

Irish Subsidiary

DemergerCo

Irish Target

Business

Domestic Mergers

Liam Brazil, Corporate Partner Mason Hayes & Curran

Domestic Mergers

• Chapter 3 of Part 9 of the Companies Act 2014 (Chapter 3)

• Term “merger” has an exhaustive statutory meaning

• Three different types:

• a merger by acquisition;

• a merger by absorption; and

• A merger by formation of a new company

7

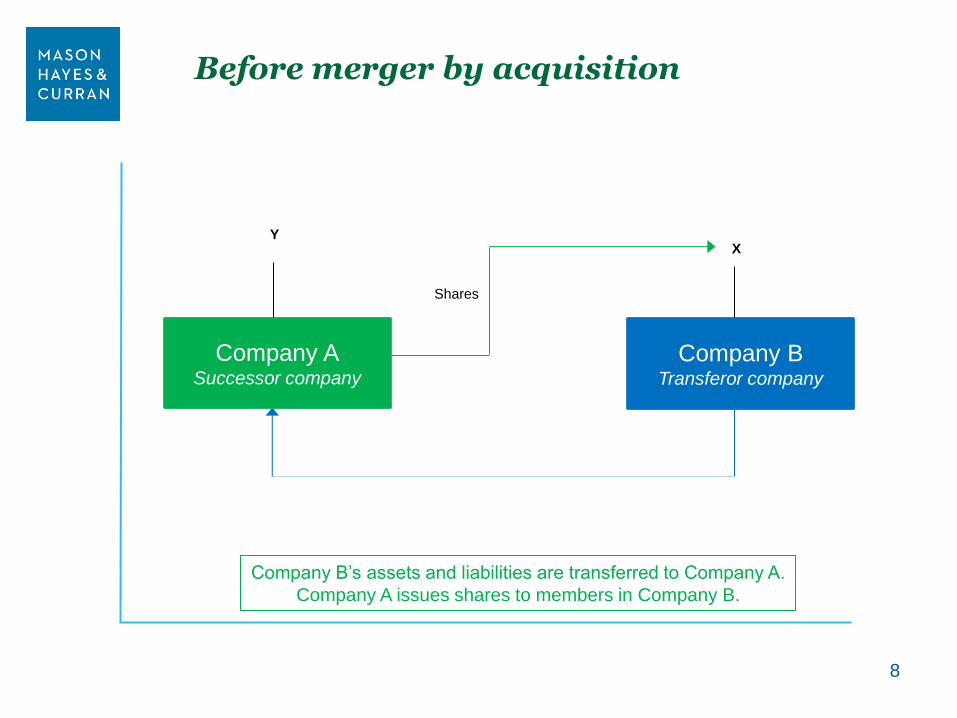

Before merger by acquisition

8

Company B’s assets and liabilities are transferred to Company A.

Company A issues shares to members in Company B.

Shares

Y X

Company A Successor company

Company B Transferor company

After merger by acquisition

9

X X Y

Company B

dissolved

Company A owns all assets

and liabilities of Company B

Before merger by absorption

10

Company A transfers all its assets and liabilities to Company B.

No issue of shares as consideration as Company B is sole

shareholder in Company A.

Assets and

liabilities 100% of shares held by Company B

Company A Transferor company

Company B Successor company

After merger by absorption

11

Company A is dissolved and all assets and liabilities are vested

in Company B.

Assets and

liabilities

Company A Dissolved

Company B Successor company

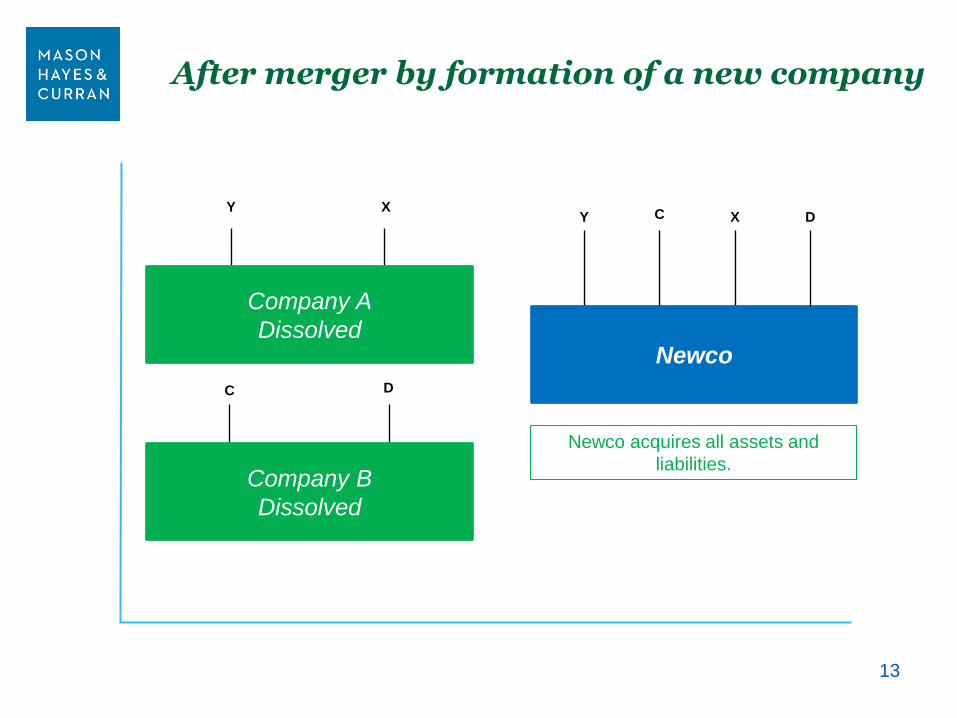

Before merger by formation of a new company

12

Companies A and B transfer all of their assets and liabilities to

Newco.

Newco Successor company

X Y

Assets and liabilities Company A

Transferor company

Assets and liabilities Company B

Transferor company

C D

After merger by formation of a new company

13

X Y

Newco

Company A

Dissolved

X Y

Newco acquires all assets and

liabilities.

C

Company B

Dissolved

D

D C

Types of companies that can merge

• For a Chapter 3 Merger

• No merging company can be a plc

• One company must be a private company limited by shares

• So:

─ LTDs can merge with other LTDs

─ LTDs can merge with DACS

─ LTDs can merge with UCs

─ LTDs can merge with CLGs

─ Combination of the above so long as one LTD

14

Merger Process

• Each type of Merger can be effected by:

• Utilising the Summary Approval Procedure (SAP); or

• Applying to the High Court for an order

Principal documents common to both:

• Common Draft Terms of Merger (CDT)

• Directors’ Explanatory Report

• Expert’s Report

15

Common draft terms of merger

• The CDT must be approved in writing by the directors

• Must include mandatory details including:

• Details of the transferor company

• Details of the successor company

• Except in the case of a merger by absorption:

• share exchange ratio

• the proposed terms of allotment of shares in the successor

company

• date from which shareholders will be able to participate in profits in

successor company

16

Common draft terms of merger cont.

• The date from which the transactions of the transferor company are to

be treated for accountancy purposes as being those of the successor

company

• The rights to be conferred by the successor company on members of

the transferor company or companies

• Information on the evaluation of the assets and liabilities to be

transferred to the successor company

• The dates of the financial statements of the transferor companies used

for the purpose of preparing the CDT

17

Directors’ Explanatory Report

• It must at a minimum explain:

• the CDT

• the legal and economic grounds for and implications of the

proposed merger

• the organisation and management structures

• recent and future commercial activities and the financial

interests of the holders of shares and other securities

• Not required for merger by absorption or if the requirement is

waived by voting shareholders

18

Expert’s Report

• No requirement to prepare one for a merger by absorption

• Other exceptions available for other types of merger

• Where required – each merging company must appoint a qualified

person:

• to examine the CDT

• to report on the CDT to the shareholders of the merging companies

19

Registration and Publication

• Deliver to the CRO within 30 days of the approval of the

CDT:

• a copy of the approved CDT

• a notice of the prescribed form DM1

• Filings and publication are not necessary if using the SAP

• Notice of the delivery must be published in the CRO

Gazette and one national daily newspaper

20

Inspection

• Inherent protection in the merger procedure

• CDT and other relevant documents must be available for

inspection at the registered office of each merging company

for a period of 30 days before the passing of the resolution

to approve the merger

21

SAP v Court Approval

• A merger cannot proceed unless it is approved by:

• virtue of SAP under Chapter 7 of Part 4; or

• the procedure laid down in Part 3 which involves obtaining a

court order confirming the merger

• There are important differences between the SAP and court

approval procedures

22

SAP - General

• Restricted Activity

• unanimous resolution (written resolution)

• declaration of solvency (at a board meeting)

• On the passing of the unanimous resolution the merger is

effective from the date specified in the CDT or any

supplemental document

23

SAP –declaration of solvency

• Declaration of solvency:

• relates to all merging companies and successor

company

• diligence

• filing in the CRO no later than 21 days after the merger

has been effected

• CRO obliged to dissolve the transferor companies on

delivery of the declaration to the CRO. Timing crucial

with respect to the effective date of the merger

24

SAP – section 209

• Declaration has no effect unless accompanied by a

supplemental document:

• confirming the CDT provides for such particulars of

each relevant matter to enable each of the prescribed

effects provisions to operate without difficulty in relation

to the merger; or

• specifying such particulars of each relevant matter as

will enable each of those effects provisions to operate

without difficulty

25

SAP – prescribed effects

• Prescribed effects provisions means a reference to section

480(3)(a) – (i)

• These provisions set out what the effects a court order

confirming a merger will have

• These provisions apply to a SAP by virtue of section 472(2)

26

SAP – prescribed effects cont’d

• Section 480(3) provides that by operation of law, for

example:

• all assets and liabilities transfer

• the transfer companies are dissolved

• all legal proceedings continue in the name of the successor

company

• contracts, agreements and instruments continue in the name

of the successor company

• all money due, owing or payable by transferor company

become obligations of the successor company

27

Court approval procedure

• Subject to some exceptions, a special resolution required

• Directors under a statutory obligation to advise members

and directors of successor company of any changes to the

assets and liabilities between the date of the CDT and the

general meeting

• Purchase of minority shares

• Protection of creditors

• Holders of securities

28

Court approval procedure

• The court may make an order hence its discretionary

• Merger effective from the date the court appoints

• The effects of the merger – Section 480(3)(a)-(i)

• Registration of title to assets by the successor company

• keepers of registers

• Property Registration Authority

29

Court approval procedure

• Certified copy of the court order sent to the Registrar by an

officer of the court

• The Registrar shall:

• register the certified copy of the order and register the

dissolution of the transferor company or companies;

and

• within 14 days after the date of that delivery –publish in

the CRO Gazette the fact that a copy of an order of the

court has been received

30

Liability of directors

• Both civil and/or criminal sanctions exist

• Civil

• misconduct

• untrue statement (defence)

• Re SAP - directors may be personally liable where they

make a declaration without having reasonable grounds

for the opinion as to the company’s solvency

31

Liability of directors cont’d

• Criminal

• untrue statement (defence)

• Category 2 offence:

• on summary conviction – €5,000 fine or

imprisonment for a term not exceeding 12 months

or both

• on conviction or indictment – a fine up to €50,000

or imprisonment for a term not exceeding 5 years

or both

32

Key Points and Issues

• SAP v the Court approval procedure:

• circumstances will dictate

• view that SAP best suited to a merger by absorption

• SAP less complex and more efficient from a cost and time perspective

• court – greater credibility

• declaration of solvency – potential personal liability for directors

• Registration of title of properties using the SAP procedure

• Employees – TUPE applies

• Non Irish law governed contracts

• Personal Rights - Scheme of Arrangement (In re Citi Hedge

Fund Services (Ireland) Limited [2013] IEHC 287)

33

Merger Accounting

Kevin Foley, Audit & Assurance Partner Grant Thornton

© 2017 Grant Thornton Ireland. All rights reserved.

Merger accounting

June 2017

Overview

© 2017 Grant Thornton Ireland. All rights reserved.

Domestic mergers

• Part 9, Ch 3 of Companies Act 2014

- sections 461 - 484

(Part 17 of Ch 9 re PLCs)

• FRS 102 s 19.29 – 19.32

IFRS – no specific guidance on common

control combinations; therefore

–Predecessor value method; or

–Acquisition method (IFRS 3)

© 2017 Grant Thornton Ireland. All rights reserved.

Accounting requirements

• No fair value adjustment

• Results included from start of accounting

period; prior period is restated

• Difference between the nominal value of the

shares issued plus the FV of any other

consideration given, and the nominal value of

the shares received in exchange recognised

in reserves and via SOCIE

© 2017 Grant Thornton Ireland. All rights reserved.

Accounting disclosures

For each combination:

• Names of combining entities

• The fact that merger accounting has been

adopted

• Date of combination

• Accounting policy choice

© 2017 Grant Thornton Ireland. All rights reserved.

Example

• Companies both have year ended 31 December 20X1. The date of merger is 31

March 20X2 for all examples.

• Assume all shares have €1 nominal value – A has 1m shares issued and B has

700k issued.

Company A (€m) Company B (€m)

PPE €6.2 €5.4

Tr debtors €0.7 €3.2

Due from B €0.5 -

Cash €1.0 €1.1

Tr creditors -€3.1 -€2.3

Due to A - -€0.5

€5.3 €6.9

Share cap €1.0 €0.7

Share prem €1.2 €2.0

SH funds brought forward €2.7 €2.8

Profit for 3 months to March X2 €0.4 €0.5

Cap redemp. reserve - €0.9

€5.3 €6.9

© 2017 Grant Thornton Ireland. All rights reserved.

Method 1 – Merger by acquisition

• A acquires B by issuing shares to members of B

• No cash payment

• 2 €1 shares in A for each €1 share in B are issued to

members of B

© 2017 Grant Thornton Ireland. All rights reserved.

Method 1 – Merger by acquisition

Company A (€m) Company B (€m) Merger adjustment Company AB (€m)

At 31 March X2 At 31 March X2 At 31 March X2

PPE €6.2 €5.4 €11.6

Tr debtors €0.7 €3.2 €3.9

Due from B €0.5 - -€0.5 -

Cash €1.0 €1.1 €2.1

Tr creditors -€3.1 -€2.3 -€5.4

Due to A - -€0.5 €0.5 -

€5.3 €6.9 €0.0 €12.2

Share cap €1.0 €0.7 -€0.7 €1.0

€1.4 €1.4

Share prem €1.2 €2.0 -€2.0 €1.2

SH funds brought forward €2.7 €2.8 €5.5

Profit for 3 months to March X2 €0.4 €0.5 €0.9

Cap redemp. reserve - €0.9 -€0.9 -

Merger reserve €2.2 €2.2

€5.3 €6.9 €0.0 €12.2

© 2017 Grant Thornton Ireland. All rights reserved.

Method 2 – Merger by absorption

• B is the wholly owned subsidiary of A

• A absorbs B

• No shares issued

© 2017 Grant Thornton Ireland. All rights reserved.

Method 2 – Merger by absorption Company A (€m) Company B (€m) Merger adjustment Company AB (€m)

At 31 March X2 At 31 March X2 At 31 March X2

PPE €6.2 €5.4 €11.6

Tr debtors €0.7 €3.2 €3.9

Due from B €0.5 - -€0.5 -

Cash €1.0 €1.1 €2.1

Tr creditors -€3.1 -€2.3 -€5.4

Due to A - -€0.5 €0.5 -

€5.3 €6.9 €0.0 €12.2

Share cap €1.0 €0.7 -€0.7 €1.0

Share prem €1.2 €2.0 -€2.0 €1.2

SH funds brought forward €2.7 €2.8 €5.5

Profit for 3 months to March X2 €0.4 €0.5 €0.9

Cap redemp. reserve - €0.9 -€0.9 -

Merger reserve €3.6 €3.6

€5.3 €6.9 €0.0 €12.2

© 2017 Grant Thornton Ireland. All rights reserved.

Method 3 – Merger by formation

• NewCo is created

• NewCo issues shares in exchange for the assets and

liabilities of both A and B

• €1 share in NewCo issued in exchange for each

share in A or B

• No cash payment

© 2017 Grant Thornton Ireland. All rights reserved.

Method 3 – Merger by formation

Company A (€m) Company B (€m) Merger adjustment NewCo (€m)

At 31 March X2 At 31 March X2 At 31 March X2

PPE €6.2 €5.4 €11.6

Tr debtors €0.7 €3.2 €3.9

Due from B €0.5 - -€0.5 -

Cash €1.0 €1.1 €2.1

Tr creditors -€3.1 -€2.3 -€5.4

Due to A - -€0.5 €0.5 -

€5.3 €6.9 €0.0 €12.2

Share cap €1.0 €0.7 -€1.7 €0.0

€1.7 €1.7

Share prem €1.2 €2.0 -€3.2 €0.0

SH funds brought forward €2.7 €2.8 €5.5

Profit for 3 months to March X2 €0.4 €0.5 €0.9

Cap redemp. reserve - €0.9 -€0.9 -

Merger reserve €4.1 €4.1

€5.3 €6.9 €0.0 €12.2

Tax Issues

Maura Dineen, Tax Partner Mason Hayes & Curran

Merger by absorption

48

Company A transfers all its assets and liabilities to Company B.

No issue of shares as consideration as Company B is sole

shareholder in Company A.

Assets and

liabilities 100% of shares held by Company B

Company A Transferor company

Company B Successor company

Merger = transfer of assets and liabilities

• Like any asset purchase agreement/business transfer agreement

• No tax legislation for domestic merger

• Analyse assets transferring

49

Tax Implications

transferor company

Capital Gains Tax

shareholder – successor company

Stamp duty operation of law?

end of taxable period

Corporation Tax payment dates

capital allowances/losses

50

Tax Implications

VAT Transfer of business relief

Payroll Revenue confirmation – no P45’s

Practical Issues filing/PAYE

any rulings?

Revenue clearances?

51