dole 2001 annual

TRANSCRIPT

Dole Food Company, Inc.Annual Report 2001

Food Operating DivisionsEurope and Africa

Belgium • Cameroon • Canary Islands • France • Germany • Ghana • Greece • Italy • Ivory Coast • KenyaNamibia • Netherlands • South Africa • Spain • Tunisia • Turkey • United Kingdom • Zimbabwe

Latin America and CaribbeanBermuda • Chile • Colombia • Costa Rica • Ecuador • Guadeloupe • Guatemala • Honduras

Jamaica • Martinique • Mexico • Peru Asia

China • Japan • New Zealand • Philippines • ThailandNorth America

Canada • United States: Arizona, California, Florida, Hawaii, Ohio, Washington

Food Marketing DivisionsEurope and Middle East

Albania • Algeria • Austria • Azerbaijan • Bahrain • Belarus • BelgiumBosnia • Bulgaria • Croatia • Czech Republic • Denmark • Estonia • Egypt • Finland • France • Georgia • Germany

Greece • Hungary • Iceland • India • Ireland • Israel • Italy • Jordan • Kazakhstan • Kuwait • Latvia • Lebanon • LithuaniaLuxembourg • Malta • Morocco • Netherlands • Norway • Oman • Poland • Portugal • Qatar • Romania • RussiaSaudi Arabia • Senegal • Slovakia • Spain • Sweden • Switzerland • Syria • Tajikistan • Tunisia • Turkey • Ukraine

United Arab Emirates • United Kingdom • UzbekistanLatin America and Caribbean

Argentina • Chile • Colombia • Costa Rica • Dominican Republic • Ecuador • GuatemalaHonduras • Mexico • Peru • Puerto Rico • Uruguay

AsiaChina • Hong Kong • Japan • New Zealand • Philippines • South Korea • Thailand

North America Canada • United States

Dole Worldwide Operations

SourcingRipening/DistributionMarketsCorporate

■

▲

●

◆

◆▲

▲▲

▲

▲

▲

▲

▲▲

▲

▲

Dole Food Company, Inc. Annual Report 2001 1

Cash Flow(EBITDA* in millions)

■ EBIT ■ Depreciation & Amortization

Shareholders’ Equity(in millions)

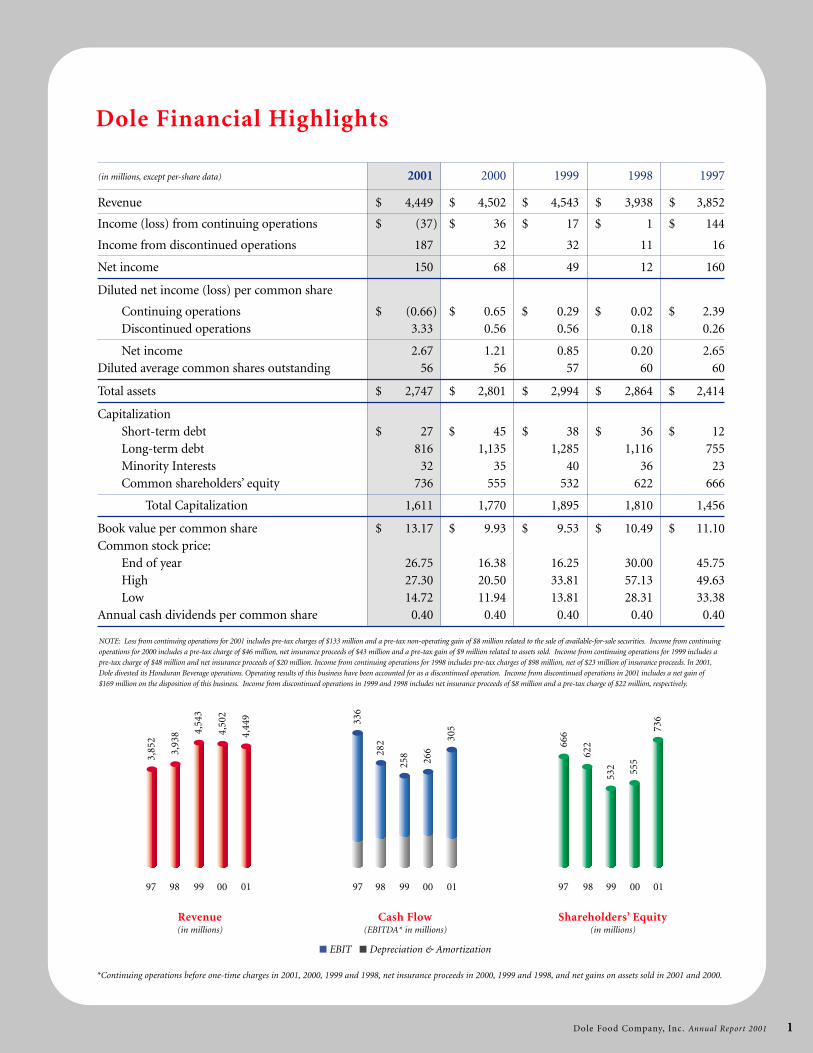

NOTE: Loss from continuing operations for 2001 includes pre-tax charges of $133 million and a pre-tax non-operating gain of $8 million related to the sale of available-for-sale securities. Income from continuing

operations for 2000 includes a pre-tax charge of $46 million, net insurance proceeds of $43 million and a pre-tax gain of $9 million related to assets sold. Income from continuing operations for 1999 includes a

pre-tax charge of $48 million and net insurance proceeds of $20 million. Income from continuing operations for 1998 includes pre-tax charges of $98 million, net of $23 million of insurance proceeds. In 2001,

Dole divested its Honduran Beverage operations. Operating results of this business have been accounted for as a discontinued operation. Income from discontinued operations in 2001 includes a net gain of

$169 million on the disposition of this business. Income from discontinued operations in 1999 and 1998 includes net insurance proceeds of $8 million and a pre-tax charge of $22 million, respectively.

Revenue(in millions)

97 98 99 00 01 97 98 99 00 01 97 98 99 00 01

*Continuing operations before one-time charges in 2001, 2000, 1999 and 1998, net insurance proceeds in 2000, 1999 and 1998, and net gains on assets sold in 2001 and 2000.

3,85

2

3,93

8 4,54

3

4,50

2

4,44

9 336

282

258

266

305

532 55

5

736

62266

6

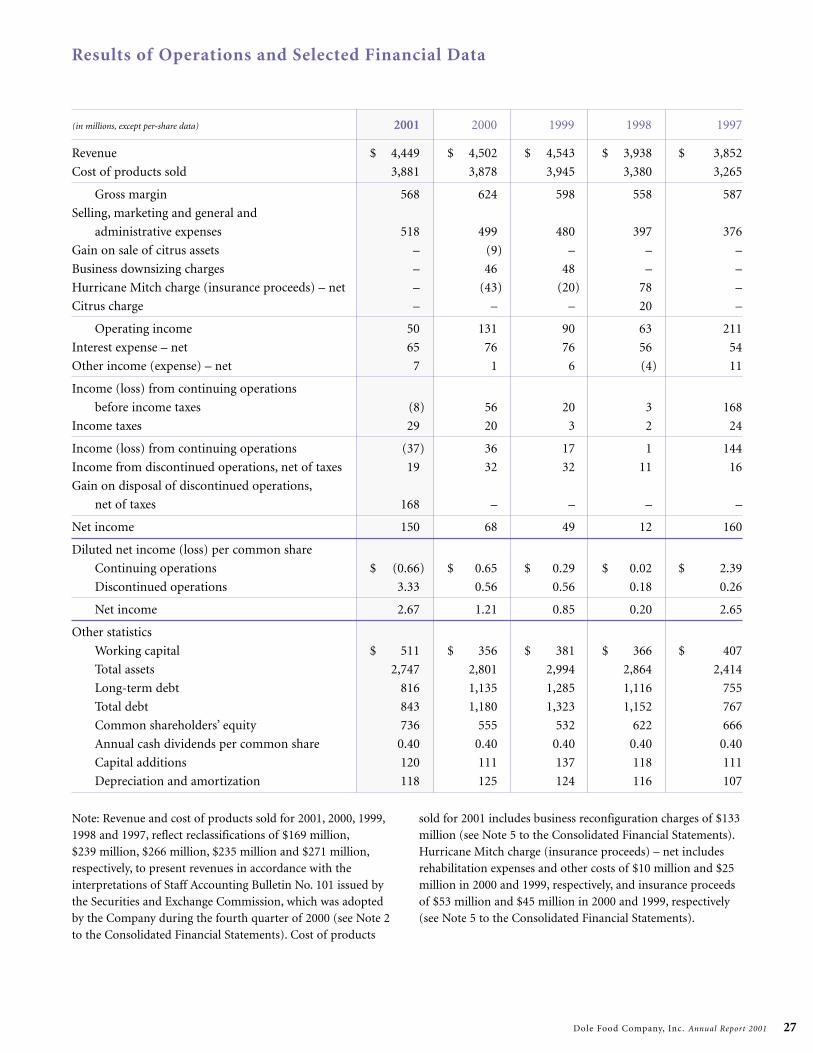

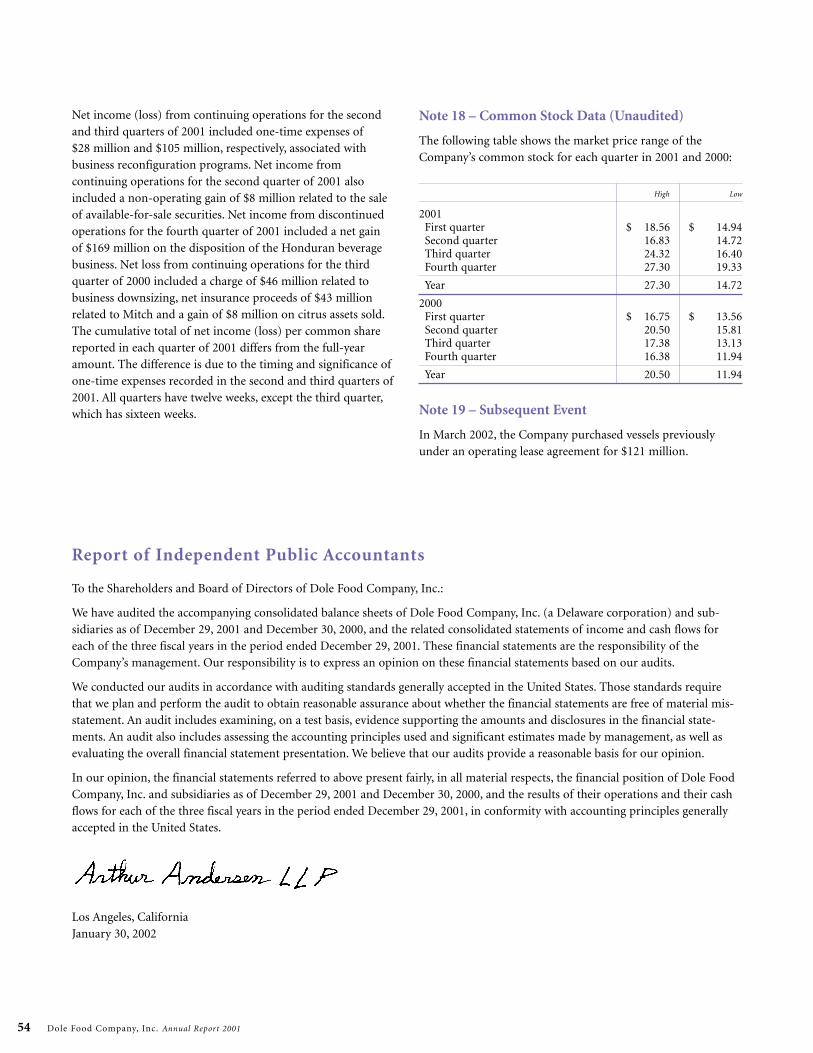

(in millions, except per-share data) 2001 2000 1999 1998 1997

Revenue $ 4,449 $ 4,502 $ 4,543 $ 3,938 $ 3,852

Income (loss) from continuing operations $ (37) $ 36 $ 17 $ 1 $ 144

Income from discontinued operations 187 32 32 11 16

Net income 150 68 49 12 160

Diluted net income (loss) per common share

Continuing operations $ (0.66) $ (0.65) $ 0.29 $ 0.02 $ 2.39Discontinued operations 3.33 0.56 0.56 0.18 0.26

Net income 2.67 1.21 0.85 0.20 2.65Diluted average common shares outstanding 56 56 57 60 60

Total assets $ 2,747 $ 2,801 $ 2,994 $ 2,864 $ 2,414

CapitalizationShort-term debt $ 27 $ 45 $ 38 $ 36 $ 12Long-term debt 816 1,135 1,285 1,116 755Minority Interests 32 35 40 36 23Common shareholders’ equity 736 555 532 622 666

Total Capitalization 1,611 1,770 1,895 1,810 1,456

Book value per common share $ 13.17 $ 9.93 $ 9.53 $ 10.49 $ 11.10Common stock price:

End of year 26.75 16.38 16.25 30.00 45.75High 27.30 20.50 33.81 57.13 49.63Low 14.72 11.94 13.81 28.31 33.38

Annual cash dividends per common share 0.40 0.40 0.40 0.40 0.40

Dole Financial Highlights

To Our Shareholders:

The year 2001 marks Dole

Food Company’s 150th year

in business. The humble

business partnership formed

by two missionaries in 1851,

commenced as a general store

in Hawaii, has become a

worldwide leader in the food industry with more

than 59,000 employees in more than 90 countries.

This past year, Dole embarked upon efforts to sig-

nificantly reduce costs at all levels and to dispose

of non-core and/or under-performing businesses.

The latter initiatives had begun in prior years, but

2001 was the year when significant accomplish-

ments were made in these efforts and we fully

expect that 2002 will be the year in which these

efforts are completed.

Financial Results

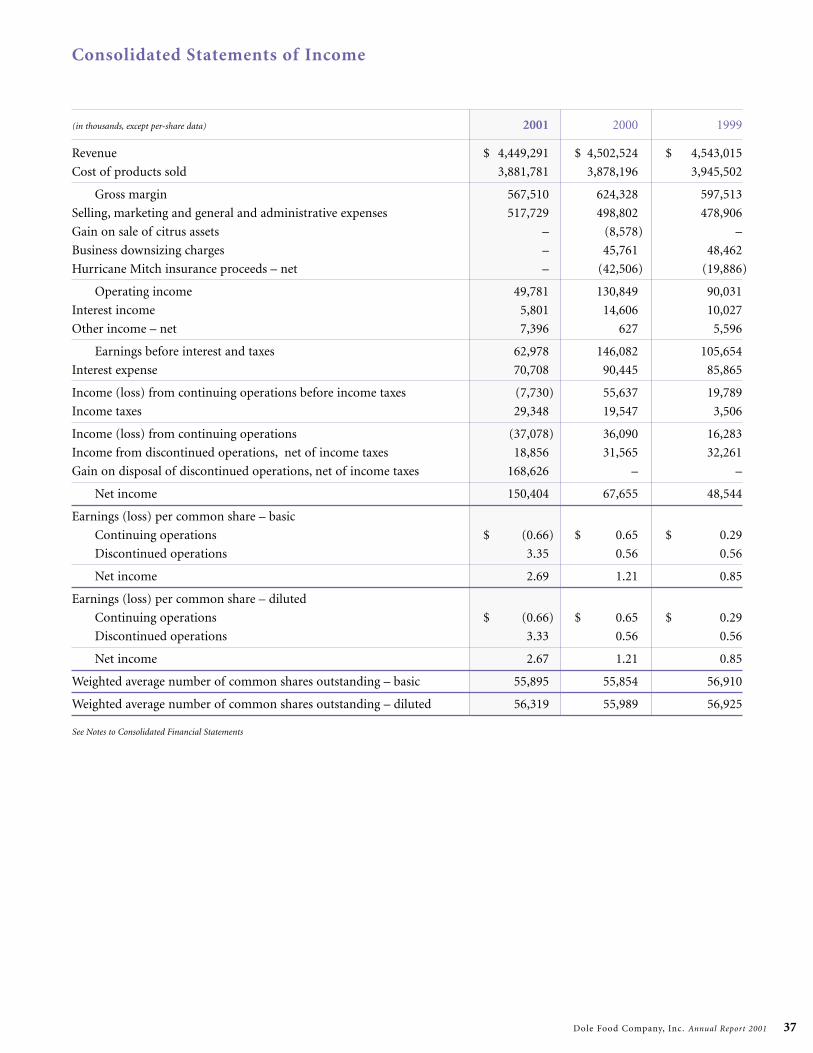

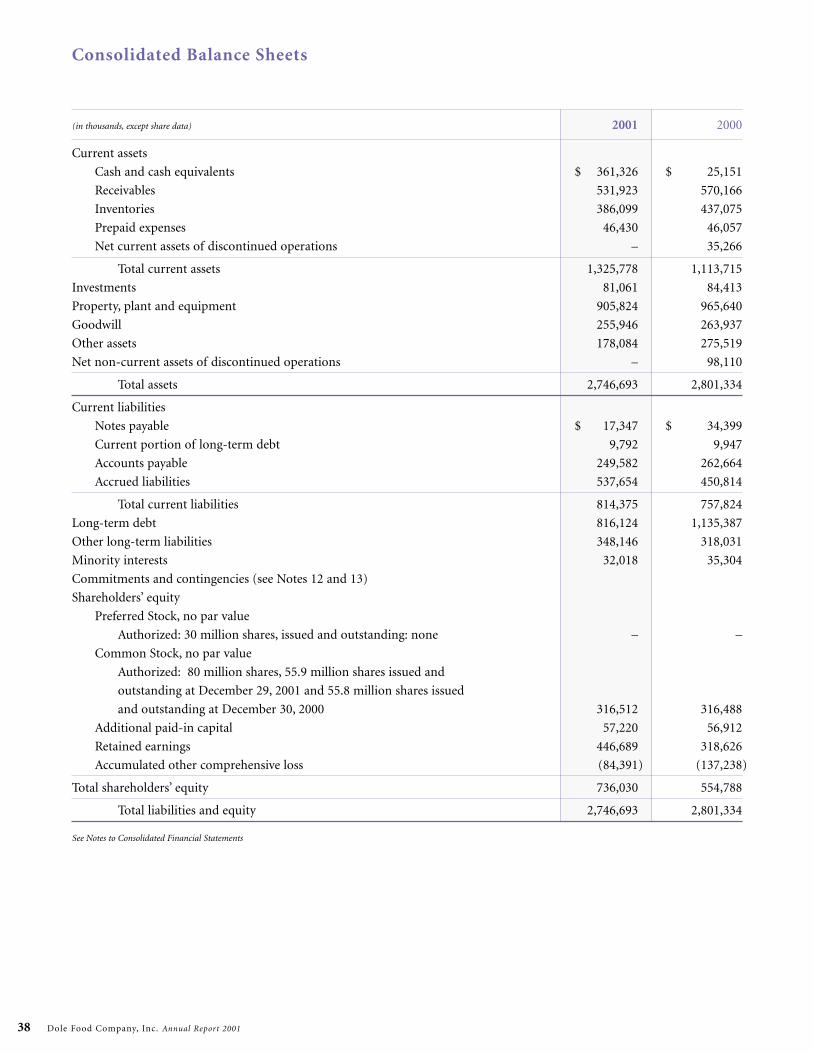

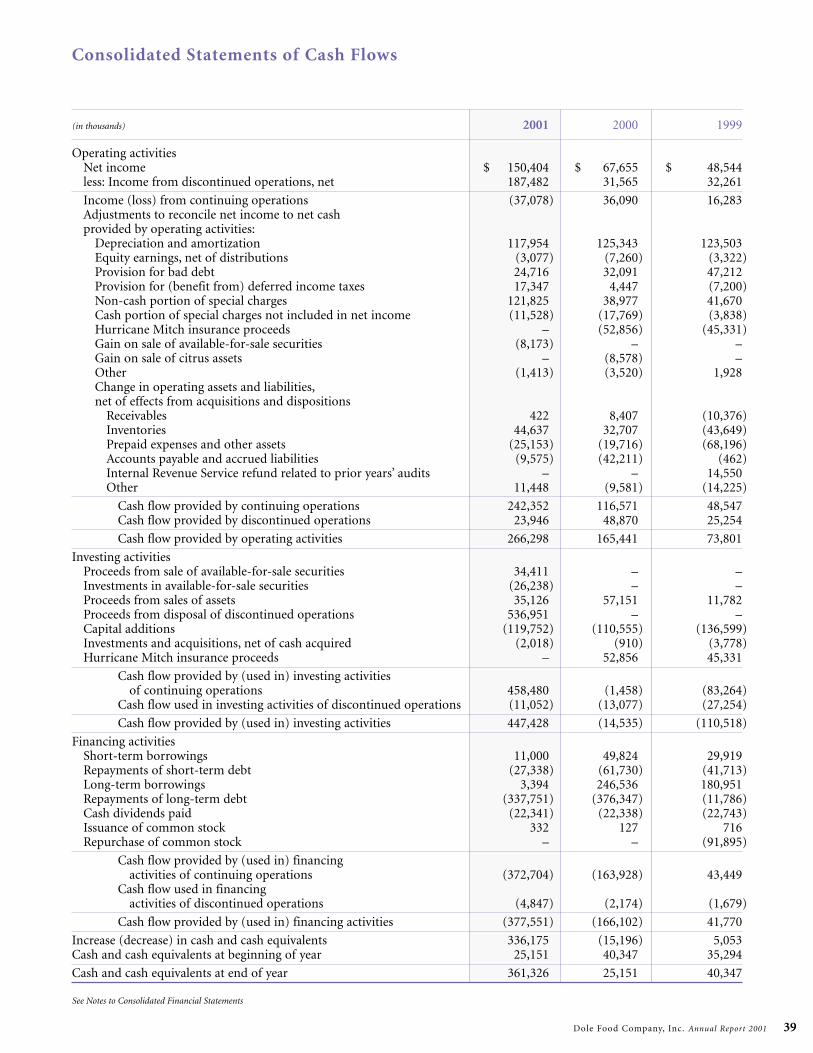

Revenues for 2001 of $4.5 billion were virtually

flat with 2000. Net income was $150.4 million or

$2.67 per share. These amounts reflect business

reconfiguration charges taken in the second and

third quarters totaling $122.1 million; a net gain

on sale of marketable securities in the second

quarter of $5.6 million; and a net gain of $168.6

million from the divestiture of our Honduran

Beverage business. These amounts also reflect

net income from discontinued operations (the

Honduran Beverage business). On a continuing

operations basis, full year 2001 net income was

$79.4 million, or $1.41 per share. This represents

an increase in net income from continuing opera-

tions of over 90% when compared to 2000 net

income from continuing operations of $41.3

million or 74 cents per share.

Full year 2001 earnings before interest, taxes,

depreciation and amortization (“EBITDA”) from

continuing operations totaled $305 million com-

pared to $266 million for 2000. At the end of the

year, net debt was $481.9 million, which is approx-

imately $670 million below net debt at the end of

2000. The reduction in 2001 has come primarily

from improved operating cash flows, enhanced

working capital management, and proceeds from

asset sales, primarily the Honduran Beverage oper-

ations. As a result, interest expense from continu-

ing operations was reduced to $70.7 million versus

$90.5 million for 2000. Capital spending for con-

tinuing operations totaled $120 million versus

$111 million for 2000. This included approximately

$27.1 million for Dole’s new fresh-cut flowers

distribution facility in Miami, Florida.

The year 2001 will forever be imprinted on our minds and the minds of the

world. The aftermath of the devastating terrorist attacks on the Pentagon and

World Trade Center has heightened our sense of patriotism for all Americans

who have so proudly united in support of our great nation. At Dole, our heart-

felt compassion goes out to the families, friends and associates of those lost on

September 11.

Dole Food Company, Inc. Annual Report 2001 2

David H. MurdockChairman of the Board andChief Executive Officer

Divestiture of Honduran Beverage Operations

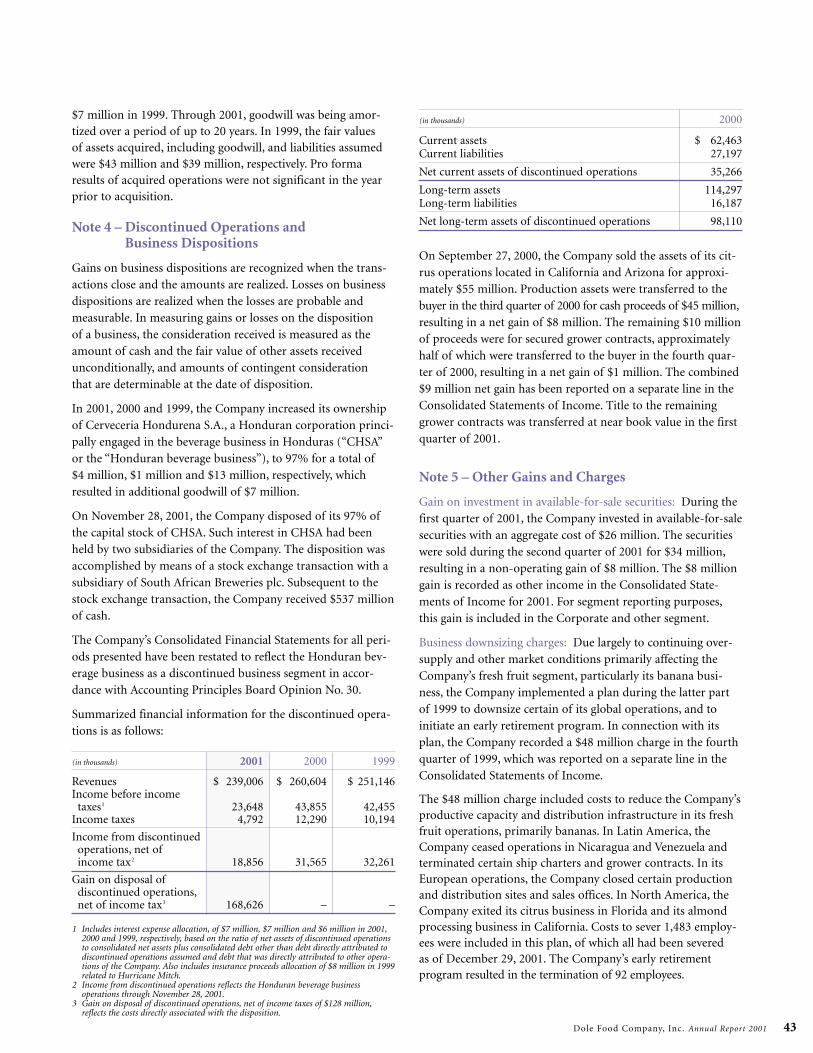

On November 28, 2001, Dole consummated the

divestiture of its 97% stake in the Cerveceria

Hondureña S.A. beverage operations located in

Honduras through a stock exchange transaction

with a subsidiary of South African Breweries plc.

Subsequent to the stock exchange transaction, Dole

received $537 million of cash, which resulted in a

net gain to the company of $168.6 million. The net

proceeds were immediately used to pay down debt.

The disposition of this business was in line with

Dole’s strategy of divesting itself of non-core assets.

We wish our long time Cerveceria Hondureña asso-

ciates much success with South African Breweries.

New Miami Facility

In December 2001, Dole’s Florida-based fresh-cut

flowers distribution operation moved into a new

328,000 square foot building. Approximately

200,000 square feet of this state-of-the-art facility

is refrigerated.

Management Changes

Our 150-year history and strong foundation affords

Dole the ability of being able to draw from an

experienced and competent management base.

In 2001, we were able to promote and reposition

from within our ranks several members of senior

and middle management.

Dole Food Company, Inc. Annual Report 2001 3

Dole Food Company Board of Directors(Seated, right to left): David H. Murdock, Lawrence A. Kern

(Standing, right to left): Zoltan Merszei, Lawrence M. Johnson, David A. DeLorenzo, E. Rolland Dickson, M.D., Mike Curb, Richard M. Ferry

In February 2001, Lawrence (Larry) A. Kern was

appointed President and Chief Operating Officer.

He was previously President of Dole’s highly

successful Fresh Vegetables business where he

pioneered its transformation from a commodity

vegetables operation to a balanced business with a

strong value-added revenue base complemented

by a right-sized commodity vegetables operation.

Eric M. Schwartz succeeded Mr. Kern as President

of Dole Worldwide Fresh Vegetables. He was previ-

ously Senior Vice President of Operations at this

division. Richard A. Harrah was appointed

President of Dole’s Latin American production

operations. He was previously Vice President of

Operations at Dole Fresh Flowers. Prior to joining

Dole, he had extensive experience in the banana

industry, serving in senior executive capacities in

the food industry. Scott Greenwood was appointed

President of Dole’s Fresh Flowers division. He

was previously Vice President of Sales for Dole

Packaged Foods. Michael J. Cavallero was promoted

to President of Dole North American Tropical

Fresh Fruit, previously serving that division as

Vice President of Sales and Marketing.

During 2001, David DeLorenzo retired as Vice

Chairman, having served the company in various

executive capacities for 31 years. His knowledge,

loyalty, dedication and integrity were instrumental

in making Dole a global leader in the industry.

Mr. DeLorenzo will continue to serve as a member

of the Board of Directors.

Financing Activities

In August 2001, Dole renewed its 364-day revolv-

ing credit facility for $200 million. Agents in the

facility are Bank of America and the Bank of Nova

Scotia. There have been no borrowings under this

facility. Toward the end of 2001, all of the out-

standing borrowings under the company’s $400

million, five-year revolving credit facility were

repaid, primarily with proceeds from the disposi-

tion of the Honduran Beverage business. As a

result, at year-end 2001, Dole’s reduced outstanding

borrowings only consist of $775 million of long-

term bonds and limited foreign borrowings.

Outlook

Having completed major cost-cutting initiatives in

2001 coupled with the divestiture of major non-

core and under-performing assets during the year,

Dole will focus on expanding its core businesses in

key markets. In 2002, management will continue

to dedicate efforts to completing the divestiture of

a few remaining non-core and under-performing

businesses but these efforts are largely behind us.

As there can be no substitute for being the low

cost provider to our markets, we will maintain our

focus on achieving a reduced cost structure. We

will also seek new opportunities both internally

and externally to expand our product offerings

and grow our revenue base. We begin 2002 with

confidence in our abilities to profitably grow our

core businesses while maintaining genuine con-

cern for the well-being of our people and the

consumer. Our realigned management team is

prepared for these challenges.

We would like to express our gratitude to our

employees, shareholders and customers for their

continued support and confidence.

Sincerely,

David H. Murdock

Chairman and Chief Executive Officer

Dole Food Company, Inc. Annual Report 2001 4

The Encyclopedia of

Foods: A Guide to

Healthy Nutrition

is a beautifully

photographed and

illustrated 500-page

book that is part of

Dole’s ongoing effort

to promote healthy,

nutritious foods and

lifestyles. The definitive resource on what to eat

for maximum health, the Encyclopedia provides

an overview of the principles of nutrition. The

foods that we eat play a major role in the prevention

and treatment of coronary artery disease, cancer,

stroke and diabetes, the four leading causes of

death in the United States. The role of nutrition in

other common medical conditions such as obesity,

high blood pressure and osteoporosis is discussed.

The Encyclopedia stresses and illustrates the

importance of the Food Guide Pyramid, health

implications of the various food groups as well as

nutrient contents, history and recommended uses.

An invaluable resource for linking food and

health, key features include:

• Narrative of the food groups – fruits, vegetables,

grains, high-protein foods, dairy foods, herbs,

spices, beverages, fats, oils and sweeteners.

• Overview of the basic principles of nutrition,

recommendations for nutrient intake, the role

of each nutrient and the US Dietary Guidelines

for Americans and how it translates into healthy

food selections.

• Creative ways to select, plan and prepare health-

ful meals, including two weeks of nutritionally

balanced menus and ways to modify favorite

family recipes to be healthful and delicious.

• Information on supplements, antioxidants,

phytochemicals, functional foods and new

food technology.

To order on-line, please go to www.dole.com.

The Encyclopedia of Foods: A Guide to Healthy

Nutrition is available for $19.95, plus $3.00

shipping and handling per book.

Dole Food Company, Inc. Annual Report 2001 5

Exercise for Health Healthy Prepared Meals Fiber and Vitamin Sources Food-Health Connection

Encyclopedia of Foods: A Guide to Healthy Nutrition

This book was prepared by medical and nutrition experts from the Mayo Clinic,

University of California Los Angeles and the Dole Food Company, Inc.

Dole Food Company, Inc. Annual Report 2001 6

During the year 2001, operat-

ing management made sig-

nificant strides in transform-

ing the Dole Food Company

from a production driven

company into a sales and

market driven one. This was

accomplished by undertaking

a review of our current customer base and focusing

only on those that were deemed to be strategically

important and profitable business partners. This

effort was further supported by a review of our

markets and the businesses in those markets,

which resulted in our initiating steps to exit

markets and businesses determined to be non-core

or under-performing. In addition, we focused on

dramatically reducing our costs worldwide.

As a result of these initiatives, total worldwide

revenues of $4.45 billion for 2001 were essentially

even with 2000. Revenues for 2001 were signifi-

cantly higher in most of our core businesses pri-

marily as a result of higher volumes and prices for

North American bananas, higher volumes and

prices for our Premium Select pineapple in North

America and Europe, increased volumes for our

North American packaged salads business consis-

tent with category growth, and increased volumes

of our FRUIT BOWLS® and FRUIT-N-GEL

BOWLS™ in North America. However, these

increases were offset by the impact on revenues

of asset sales and business shutdowns, which

accounted for approximately $140 million of

revenues in 2000 that were not realized in 2001.

The weak euro and yen to US dollar exchange rates

negatively impacted revenues by approximately

$85 million. Additional offsets included reductions

in our banana volumes to unprofitable markets in

Eastern Europe and lower year-over-year pricing in

our commodity vegetables business.

Earnings before interest and taxes (“EBIT”) from

continuing operations was $187 million, versus

$141 million for 2000. Improved EBIT in the

company’s fresh fruit segment, primarily due to

higher banana and fresh pineapple profits in

North America and Europe, was slightly offset by

losses in the California deciduous and Northwest

apples businesses, which the company is exiting.

EBIT was also higher in the company’s fresh veg-

etables segment as a result of category growth for

packaged salads which offset lower commodity

vegetables pricing, and in the packaged foods

segment as a result of increased FRUIT BOWL

and FRUIT-N-GEL BOWL sales volumes and

lower production costs. Earnings were lower in

the fresh-cut flowers segment, due to unfavorable

market conditions, which resulted in lower sales

volumes. Consulting fees relative to the cost

savings programs implemented during the year

served as a one-time partial offset to EBIT growth.

Operational Review

The year of 2001 was a year of change, challenge and achievement for the Dole

Food Company as we transformed into a more sales and marketing driven company.

We look to our key customers and vendors to be our strategic business partners.

Lawrence A. KernPresident andChief Operating Officer

We recently finished the strategic and operational

reviews of our North American banana and fresh-

cut flowers businesses, and have begun to imple-

ment changes. We completed the reviews of our

European, Latin American and Asian banana

operations some time ago, and implementation of

process enhancements are well on their way. Our

strategic sourcing and logistics and distribution

analyses are also complete and implementation is

nearing completion. To date, we have identified

100% of our goal of $200 million of annual

improvements to future operating results that

should be realized on a steady state basis by 2003.

These programs contributed approximately $93

million of pre-tax operating earnings, before off-

sets, during 2001. These programs also resulted in

$28 million of one-time pre-tax charges to income

in the second quarter and $105 million of pre-tax

charges in the third quarter of 2001. No additional

charges from these programs were made in the

fourth quarter and we expect that there will be no

further significant charges associated with these

programs in the future.

Of the $93 million in 2001 profit improvement,

approximately $25 million dropped through to

pre-tax income. The offsets of approximately

$68 million were mainly from the impact of lower

pricing for commodity vegetables, reduced sales

volumes for fresh-cut flowers, the effect of foreign

currency exchange, primarily from the yen, the

absence of earnings from the Honduran Beverage

business and consulting costs associated with the

strategic and operational reviews of our businesses.

The non-recurring portion of these offsets was

approximately $13 million. Therefore, excluding

the non-recurring offsets, about 40 percent of the

profit improvements added to pre-tax profit for 2001.

Dole Food Company, Inc. Annual Report 2001 7

Dole is the world’s largest producer and marketer of high-quality fresh fruit, fresh vegetables and fresh-cut flowers, and markets a growing line of packaged foods.

Dole Worldwide Product List

Dole Fresh VegetablesDole ArtichokesDole AsparagusDole Bell PeppersDole BroccoliDole Brussels SproutsDole Butter LettuceDole CarrotsDole CauliflowerDole CeleryDole CilantroDole Dry OnionsDole Green Leaf LettuceDole Green OnionsDole Iceberg LettuceDole Idaho PotatoesDole RadishesDole Red Leaf LettuceDole Romaine LettuceDole Sugar Peas

Dole Fresh-Cut VegetablesDole All American Salad KitDole American Salad BlendDole Chopped Romaine SaladDole Classic Cole SlawDole Classic Greek Salad KitDole Classic Iceberg SaladDole Classic Romaine SaladDole Caesar Salad KitDole Light Caesar Salad KitDole Creamy Garlic Caesar

Salad KitDole Romano Salad KitDole Sunflower Ranch

Salad KitDole European Salad BlendDole French Salad BlendDole Greener Selection®

SaladDole Hearts of Romaine

Mix Salad BlendDole Italian Salad BlendDole Just Lettuce™ SaladDole Leafy Romaine

Salad BlendDole Mediterranean

Salad Blend Dole Mediterranean Salad KitDole Organic Baby LettucesDole Organic Baby SpinachDole Organic Hearts of

Romaine MixDole Organic Spring Mix

with HerbsDole Peeled Mini-CarrotsDole Shredded CarrotsDole Shredded LettuceDole Shredded Red CabbageDole Spring Mix Salad BlendDole Triple Cheese Salad KitDole (Tuscany) ButterLettuce Salad BlendDole (Verona) Field Greens

Salad BlendDole Very Veggie™ Salad Blend

Pascual HermanosDole Santa (Grape) TomatoesDole Cherry TomatoesDole On-Vine TomatoesDole Plum TomatoesDole Little Gem Baby LettuceDole Rucola SaladDole Mini Leaf SaladDole Spring Onions

Dole Dried Fruit & NutDole Dates Chopped in

Resealable BagsDole CinnaRaisins® in

Resealable BagsDole Golden Seedless RaisinsDole Dates Pitted in

Resealable BagsDole Pitted Prunes CanisterDole Pitted Prunes in

Resealable BagsDole Seedless Raisins CanisterDole Seedless Raisins in

Resealable BagsDole Seedless Raisins Mini SnacksDole Seedless Raisins

Six Packs

SamanDole Golden RaisinsDole Mixed Fruit & NutDole Pitted PrunesDole Soft ApricotsEat Me Dried ApricotsEat Me Dried FigsEat Me Pitted PrunesEat Me Whole DatesSoelia AlmondsSoelia Dried ApricotsSoelia Dried FigsSoelia HazelnutsSoelia JA Whole DatesSoelia Pine NutsSoelia PistachiosSoelia Pitted DatesSoelia Pitted PrunesSoelia PrunesSoelia Soft ApricotsSoelia Soft FigsSoelia WalnutsSoelia Whole Nuts

Dole Fresh FruitDole ApplesDole ApricotsDole AvocadoDole BananasDole Banana Puree Dole CantaloupeDole CherriesDole ClementinesDole CoconutsDole CranberriesDole GrapefruitDole GrapesDole Honeydew Melon

Dole KiwiDole MangoesDole Morado BananaDole Native BananaDole NectarinesDole OrangesDole Organic BananasDole PeachesDole PearsDole PineappleDole Fresh-Cut

Pineapple ChunksDole Fresh-Cut

Pineapple SpearsDole Fresh-Cut

Pineapple CylindersDole Plantains Dole PlumsDole PomegranatesDole StrawberriesDole Super Sweet BananaDole Yucca

Dole Packaged FoodsDole Aloe Vera (Solid)Dole Apricot HalvesDole Apricot Snack CupDole Apricots in Juice

or SyrupDole Crushed Pineapple

in Juice or SyrupDole DatesDole Deciduous Fruit

Cocktail in Juice and SyrupDole Fruit Bowls® – PeachesDole Fruit Bowls – Mixed

FruitDole Fruit Bowls – Pineapple Dole Fruit Bowls – Tropical

Fruit Dole Fruit Bowls – Mandarin

Orange SegmentsDole Fruit Festival Snack CupDole Fruit-N-Gel Bowls™

Pineapple in Lime GelDole Fruit-N-Gel Bowls

Mandarin Orange inOrange Gel

Dole Fruit-N-Gel BowlsPeaches in Strawberry Gel

Dole FruiTango™ MandarinDole FruiTango PineappleDole FruiTango StrawberryDole FruiTango TropicalDole Guava HalvesDole Guava in SyrupDole Longans in SyrupDole Longans Snack CupDole Lychees in SyrupDole Lychees Snack CupDole Mandarin Orange

Fruit CupsDole Mandarin Orange

SegmentsDole Mandarin Orange

Segments, Easy Open

Dole Mango Cubes Snack Cup

Dole Mango Juice DrinkDole Mango Slices in

Blended Juice or SyrupDole MushroomDole Nata de Coco in SyrupDole Nata de Coco

with Jackfruit Snack CupDole Papaya in SyrupDole Peach Halves in SyrupDole Peach Slices - Easy OpenDole Peach Snack CupDole Peaches in Juice

and SyrupDole Pear Snack CupDole Pears in Juice and SyrupDole Pine Orange Banana

JuiceDole Pineapple Chunks

in Juice or SyrupDole Pineapple ConcentrateDole Pineapple Cubes

in SyrupDole Pineapple Fun Shapes®

– CosmicDole Pineapple Fun Shapes

– Sea CreaturesDole Pineapple Grapefruit

Juice DrinkDole Pineapple JuiceDole Frozen Pineapple JuiceDole Pineapple Juice DrinkDole Pineapple Lychee

Juice DrinkDole Pineapple Mandarin

Orange Banana JuiceDole Pineapple Orange JuiceDole Pineapple Orange

Juice BoxDole Pineapple Orange

Juice DrinkDole Pineapple Orange

Raspberry Juice BoxDole Pineapple Orange

Strawberry JuiceDole Pineapple Slices

in Juice or SyrupDole Pineapple Snack CupDole Pineapple Snack

Wedges, Easy OpenDole Pineapple Strawberry

Juice DrinkDole Pineapple Tidbits

for PizzaDole Pineapple Tidbits

in JuiceDole Pouch – Pineapple

Tidbits in SyrupDole PrunesDole RaisinsDole Rambutan in SyrupDole Rambutan Snack CupDole Rambutan with

Pineapple Snack Cup

Dole Red Papaya Chunksin Light Syrup

Dole Tomato SauceDole Tropical Fruit Cocktail

in Juice and SyrupDole Tropical Fruit Cocktail

in Syrup with Passion Fruit Juice

Dole Tropical Fruit Juice BoxDole Tropical Fruit SaladDole Tropical Fruit Salad,

Easy OpenDole Tropical-Pineapple

Juice BlendDole White AsparagusDole Yellow Papaya Chunks

in SyrupSeasons Pineapple JuiceSeasons Tropical Fruit Mix

Dole Fresh FlowersAchilleaAlstroemeriaAster ButterflyAster MatsumotoAster MontecasinoBouvardiaBupleurumCampanulasCarnationsChinese CarnationsCremonsDelphiniumFarm BouquetsFootball MumsFreesiaGerberaGerspiderGodetiasGypsophilaKangaroo PawsLeatherleafLimoniumLisianthusMicro PomponsMillion Stars GypsophilaMiniature CarnationsMonk’s HoodMumsPomponsRoses (Hybrid Tea)Roses (Micro)Rover Mums - Fall onlySnapdragonsSolidagoSolidasterSpider MumsSpray RosesStaticeStockSunflowersSweetheart RosesTree FernYarrow

Dole Food Company, Inc. Annual Report 2001 8

Dole Food Company, Inc. Annual Report 2001 9

North America

During 2001,

Dole bananas,

already the num-

ber one banana

brand in North

America, continued to grow in market share. Our

experienced and knowledgeable sales team worked

to solidify strong relationships with retail customers

and emphasized building new partnerships with

wholesalers. In the produce industry in North

America today, wholesale partners are key to our

distribution and expansion into independent

markets and chains that do not have their own

ripening facilities.

In early 2001, we expanded our fresh fruit product

line by introducing organic bananas under the

DOLE brand. The introduction proved successful,

as we have found that organic produce is a grow-

ing category throughout North America.

Although our food service airline business was some-

what affected by the September 11 tragedy, we were

still able to expand our bananas into new outlets. We

feel our success in the food service arena has much to

do with our innovative packaging designs that meet

the needs of food service accounts.

We continued to develop relationships with school

districts across the country, emphasizing Dole’s

commitment to nutrition education and the 5 A

Day message. While our new version of Dole’s

5 A Day nutrition education CD-ROM was get-

ting into classrooms, we were getting more Dole

bananas onto school breakfast and lunch menus.

In marketing, we continued to grow our brand

through promotions like the Dole Banana Shuffle,

tie-ins with major national brands and a sweep-

stakes that sent the winners on a trip to the Williams

World Classic Golf Tournament. In advertising, our

focus is to reach consumers with a nutrition message

that also portrays our products as fun.

Dole Fresh Fruit

Dole North America customers purchase more than eight million pounds of

Dole fresh fruit every day. Dole is the industry leader in growing, sourcing,

shipping and distribution of high-quality consistent product.

Product InnovationsOrganic Bananas and Premium Select Pineapple – In 2001, Dole Fresh Fruit

introduced DOLE branded organic bananas in North America. DOLE PREMIUM

SELECT® Pineapples were introduced into the North American market after years

of hard work by Dole’s research and development teams, whose exacting quality

standards resulted in cultivation, growth and shipping practices, which have pro-

vided Dole customers with the finest extra sweet pineapples available.

Dole Food Company, Inc. Annual Report 2001 10

Dole’s pineapple category grew in North America

over the past year. In Hawaii, Dole refocused on its

core business of pineapples while other less prof-

itable product lines were eliminated to redirect

all resources toward expanding the category. Our

other tropical product categories, such as melons

as well as cranberries, continue to grow.

Dole’s North American deciduous program

achieved record revenues and solidified the number

one position in the market for the 2001 season.

Dole improved its stone fruit market share

considerably over the previous year, ranking as

the market leader in Chilean stone fruit imports.

This program complements Dole’s Chilean grape

program, which is also number one in North

America. Dole continues to import a full line of

apples and pears from Chile and completed a very

successful introduction of DOLE branded avoca-

dos into North America.

Dole’s South African import program is relatively

small but has an optimistic outlook for growth in

the deciduous and citrus categories. South Africa

offers a full line of table grapes, including varieties

that are new to our overall program. South African

citrus imports enable us to offer an additional line

of products to our customers through the summer

months. These programs nicely parallel with and

add depth to our Chilean business and complement

our existing product line. We foresee continued

growth opportunities in this area.

Europe

Dole Europe dramatically improved its revenue

and profit performance during 2001 through a

restructuring of its banana business that eliminated

one-third of its overhead, consolidated shipping

services and concentrated activities on servicing

supermarkets directly.

Dole Europe also introduced new banana packaging

presentations for “Baby Bananas” and “Gourmet

Bananas” as well as single finger displays for con-

venience stores. Banana production and marketing

has also been expanded to consider the growing

demand for organically grown bananas. With these

new banana presentations, Dole Europe is working

with its retail partners to broaden product offer-

ings in order to appeal to the increasing demands

of our consumers.

The Dole Colombia and Dole Chile (not pictured) are the largest all-refrigerated container vessels in the world.

Dole Food Company, Inc. Annual Report 2001 11

Dole Food Company, Inc. Annual Report 2001 12

Fact from Encyclopedia of Foods Fruit is a valuable source of fiber, vitamin C, some of the B

vitamins, vitamin A, and other antioxidants and phytonutri-

ents. A diet that contains ample amounts of fruits and veg-

etables is associated with a reduced risk for cancer. There is

no evidence that mineral or vitamin supplements are better

than obtaining nutrients though whole foods.

Dole Europe’s ripening and distribution activity

reached almost $1 billion in revenue for 2001. Of

particular note, we have expanded our German

distribution to the Berlin area to better service

rapidly expanding retailers in the new German

capital, which may be the center of an expanded

European Union.

A major concern to European consumers is food

safety. Following concerns about various contamina-

tion incidents, retailers are demanding strict suppli-

er accountability. Dole is a leader in full traceability

of its supply chain. For example, Dole South Africa

has been recognized by some leading European

retailers as a reliable supplier with systems in place

to trace produce from the supermarket shelf back

to the tree or vine where it grew. Dole Europe is

expanding this capability throughout its businesses.

Complete accountability for each product will pro-

vide consumers with the comfort they desire.

Dole Europe’s mission is one of service to its retail

customers and satisfaction of consumer demand.

Asia

In Asia, Dole faced tough challenges due to weak

economic conditions in its primary markets and

the strength of the US dollar. In addition, the

Asian banana industry suffered from over-supply.

In order to address this situation, Dole Asia com-

pleted a restructuring of its operations including

reducing volumes from company as well as inde-

pendent grower farms, and downsizing adminis-

trative overhead. These steps have allowed Dole

Asia to re-focus on its strategy of innovative agri-

cultural excellence aligned with customer require-

ments for high quality fresh fruits and vegetables.

Dole Asia is confident that the significant expan-

sion of niche and value-added products form a

solid foundation for future profitable growth.

Latin America

Banana industry volumes were down year over

year by about 5% due to cooler than normal

weather in South America, which contributed to

overall better pricing in North America and

Europe. As part of Dole’s cost reduction and profit

improvement strategy, it exited unprofitable mar-

kets and, accordingly, adjusted its volume to meet

its core market requirements. Through increased

ship utilization and higher productivity from its

own farms, delivered costs significantly improved

in 2001. Dole bananas are grown on 15,000

hectares of Company owned farms and about

29,000 hectares of independent producers’ farms.

Dole’s new organic banana farm in Ecuador,

Nuevo Esperanza (New Hope), came into full

production bringing to North America the highest

quality organic bananas available in the market.

An independent grower program was also started

in Peru to provide additional volume of high

quality organic bananas.

Dole has expanded its Premium Select pineapple

operations in Latin America and now sources

from fully operational farms in Costa Rica,

Ecuador and Honduras.

All of Dole’s Latin American farming operations

became fully certified under an Environmental

Management System to ISO 14001 international

standards. Certifications oversee compliance of

applicable laws on worker safety and environmen-

tal protection by our farms and those of our inde-

pendent growers.

Over 22,000 Dole employees throughout Latin

America are dedicated to bringing to market the

highest quality and safest fresh fruit possible.

Dole Food Company, Inc. Annual Report 2001 13

Dole Food Company, Inc. Annual Report 2001 14

Earnings from

operations in

Dole’s fresh veg-

etables segment

were up due to

cost reduction

efforts and continued growth in revenues of the

packaged salads business. Dole’s retail packaged

salads not only maintained a leading market

share position, but growth exceeded that of this

category segment in the food industry. Dole Fresh

Vegetables continued to expand production and

distribution capabilities by completing significant

expansion projects in the Springfield, Ohio plant,

where a 30,000 square foot addition was added,

and the Yuma, Arizona facilities, where a 70,000

square foot addition is being added. Dole’s Yuma

production facility will transition from a five-

month seasonal operation to a year-round produc-

tion operation in the fall of 2002 to accommodate

the growth.

Dole Fresh Vegetables also continued to lead the

fresh-cut salad category in new product introduc-

tions. JUST LETTUCE™, a product containing a

mix of both iceberg and romaine lettuces, and

Hearts of Romaine Mix, have quickly become two

of the most popular salads in the premium salad

segments. New product development continues

to be a key driver in the growth of the segment,

accounting for over twenty percent of Dole’s

value-added volume growth year over year.

In the international markets, Dole also began

operation of its second green field production site

in Scandinavia. Helsingborg, Sweden, is the home

of the second fresh-cut plant now in operation

which provides DOLE branded retail salad prod-

ucts to the Sweden, Finland, and Denmark mar-

kets. The plants were designed with the same

stringent food safety requirements that were the

cornerstone of the North American facilities

design. Making multiple markets possible under

Hot New ProductsSalad Packages - Dole Fresh Vegetables led the category in new product intro-

ductions in 2001. JUST LETTUCE, introduced in January, is a new variety of

Premium Classics consisting of iceberg and romaine. It has become one of the

most popular salads in the category. Hearts of Romaine Mix was rolled out in

June, and quickly became one of our leading Salad Blends.

Dole Fresh Vegetables

In 2001, consumers purchased more Dole salads than any other brand. Dole’s

unit market share of the category was 37.3%. On average, consumers in the

United States buy 1,166,000 bags of Dole salads every day.

Dole Food Company, Inc. Annual Report 2001 15

Dole Food Company, Inc. Annual Report 2001 16

Fact from Encyclopedia of Foods Vegetables contribute significant amounts of vitamins,

minerals, soluble and insoluble fiber, and other phytonutri-

ents to our diets. The goal is to have at least three servings

of vegetables every day. Variety and different colors and

kinds of vegetables are important.

the DOLE brand, the actual packaging is printed

with trilingual instruction and labeling. Dole also

announced and has made plans for the divestiture

of Pascual Hermanos, which is a commodity busi-

ness located in Spain. With the exception of a

small citrus business, the divestiture plan calls for

Pascual Hermanos to be sold as an operating entity.

Offsetting improved results from packaged salads

in North America were divestiture costs relating

to the sale and or closure of non-performing

businesses in the deciduous segment and lower

commodity vegetable prices in North America.

Dole Fresh Vegetables ceased operations at its

Washington apple business. Most of the assets

of the apple business have either been sold or

are currently under escrow. Dole Fresh Vegetables

has also divested most of the assets associated

with the California Deciduous business.

Although commodity pricing was very strong,

results were below the record levels realized in

2000. Cost reduction efforts in the commodity

business were aggressive and helped in part to

offset cost increases in land rents, fertilizers, and

energy costs. Energy cost increases and supply

presented a significant challenge in 2001 and

continue to be at the forefront of challenges

ahead in the coming years.

Fresh Vegetables’ commodity program was suc-

cessful in obtaining marketing agreements leverag-

ing the DOLE brand in other commodities such as

potatoes. Dole Fresh Vegetables continues to offer

premium quality commodity vegetables to the

produce market, and is continuing to seek part-

nerships that will expand our vegetable presence

on the produce shelf.

In reference to food safety, The American Institute

of Baking, one of the nation’s leading independent

third party auditors for food safety practices, has

again rated both Dole value-added year-round

production facilities in California and Ohio as

“Superior”, which is the highest rating possible.

The Soledad plant initiated and completed a fif-

teen-month study with the Food and Drug

Administration on HACCP practices (Hazard

Analysis of Critical Control Points for food safety)

for the processing of pre-cut vegetables. Originally

developed by NASA, a HACCP program identifies

and eliminates any vectors of risk in a production

process so that food safety is proactive instead of

reactive. Examples that make up a HACCP pro-

gram include metal detectors on all production

lines, stainless steel construction of equipment for

ease of cleaning, and a comprehensive and docu-

mented daily sanitation program. The outcome of

the study was that, through information sharing

and hands-on training with Dole Fresh Vegetables

Quality Assurance personnel and FDA auditors,

there is a better understanding of the unique

pre-cut vegetable production process from both

a company and a regulatory standpoint.

Dole Food Company, Inc. Annual Report 2001 17

Dole prides itself on offering its customers and consumers the highestquality and widest variety of produce available in the market today. Itsworldwide team of growers, packers, processors, shippers and employees iscommitted to consistently providing premium products, while protectingthe environment in which its products are grown and processed.

Dole Food Company, Inc. Annual Report 2001 18

Operating results

in Dole’s pack-

aged foods busi-

ness increased,

primarily due to

higher volumes

of new products and lower production costs in the

company’s Asian processing plants. Our FRUIT

BOWLS continued to achieve excellent market

performance with a 40% market share for the year.

This was partly due to the successful launch of

Mandarin FRUIT BOWLS, which is now the

number two item in this category, right behind

Peaches. Additionally, the performance of our new

FRUIT-N-GEL BOWLS surpassed our expecta-

tions as well as exceeded those of our retailers.

Despite worldwide excess supply of pineapple and

concentrate in 2001, and price competition, Dole

maintained its overall revenue and market posi-

tion in these businesses. The marketing effort for

canned pineapple is focused on teaching consumers

how to eat more nutritiously by using this product

in their everyday meals and snacks. Looking for-

ward to 2002, the Thai pineapple industry, which

supplies about one third of the world’s canned

pineapple, is moving into a short supply cycle.

However, with dual sourcing capability (Phil-

ippines and Thailand), Dole is well supplied and

well positioned to gain market share. For canned

pineapple juice, the marketing effort is aimed at

delivering the message that Dole is 100% juice

and therefore a better-for-you alternative.

To further boost Dole’s presence in the marketplace,

a new product called 100% Juice FRUITANGO™

is being expanded into retail markets. This is a line

of single-serve, tropical juice blends in a “slim”

eight-ounce can, with four flavors: Pineapple,

Strawberry, Mandarin and Tropical. This product

tested extremely well in the club store channel,

and has since been expanded nationally. The retail

Dole Packaged Foods

FRUIT BOWLS continued to achieve excellent market performance with a 40%

market share for the year. Canned Pineapple and Pineapple Juice maintained

historical market shares of 52% and 46%, respectively.

Hot New ProductsFruit-N-Gel Bowls and FruiTango – The trend towards healthy snacking has

created a huge opportunity for Dole FRUIT BOWLS. In an effort to keep up

with this demand, Dole has quadrupled FRUIT BOWL capacity in the past two

years. We are now able to produce almost 500 million Bowls annually, enough

to provide two packages for every school age person in America.

Dole Food Company, Inc. Annual Report 2001 19

Dole Food Company, Inc. Annual Report 2001 20

Fact from Encyclopedia of Foods When it comes to eating at home, your meals can only be as

good as the food you have in your kitchen. Be sure you have

plenty of fruits, vegetables, and whole grains on hand so you

can translate your plan for healthful eating into enjoyable

and nutritious meals.

Dole Food Company, Inc. Annual Report 2001 21

expansion is being supported with television and

radio advertising, as well as in-store and local market

programs. This product is also getting a good

reception in the convenience store channel.

Given the success of the FRUIT BOWLS franchise,

six new items will be launched in the spring of

2002. Four of the items are single-serve and come

with a fork, for on-the-go consumption. These are

larger than the regular FRUIT BOWLS because

they are targeted specifically towards adults. The

four flavors are: Peaches, Pineapple, Mandarin

Orange and Tropical Fruit. These products are

expected to be particularly popular in convenience

stores. The other two items are reduced sugar

FRUIT-N-GEL BOWLS. These two products have

one-third less calories than regular FRUIT-N-GEL

BOWLS and come in the four-pack, four-ounce

cup format. The two flavors are: Pears in Kiwi-

Berry Gel, and Papaya in Peach Gel. These product

launches are supported by television advertising,

consumer promotion and public relations pro-

grams. In addition, significant resources have been

applied towards developing the next generation of

FRUIT BOWLS products.

With continued increasing demand for FRUIT

BOWLS, Dole is making additional investments

in its Asian canneries. These investments will go

toward state-of-the-art production equipment that

will ensure Dole’s position as industry innovator

and low cost producer. Dole is now packing as

many plastic cups as traditional cans.

With a broader line of convenience-oriented prod-

ucts, Dole is gaining expanded distribution in

non-grocery channels. This is important because

they are growing faster than the grocery channel,

some of the largest U.S. retailers are in these channels

and the costs of gaining new distribution in them

is less. In the last year, Dole has gained significant

new distribution in the drug, convenience store

and mass merchandiser channels, and has become

an increasingly dominant presence in the club

store snack cup business.

Aside from FRUIT BOWLS, new product develop-

ment efforts are underway for other value-added

packaging formats. A multi-serve, resealable plastic

bottle is being tested in a limited number of retail

channels, and a multi-serve pouch is being tested

in the foodservice sector. This packaging is intended

to deliver fruit to the end user in more convenient

and user-friendly ways, so as to increase overall

fruit consumption.

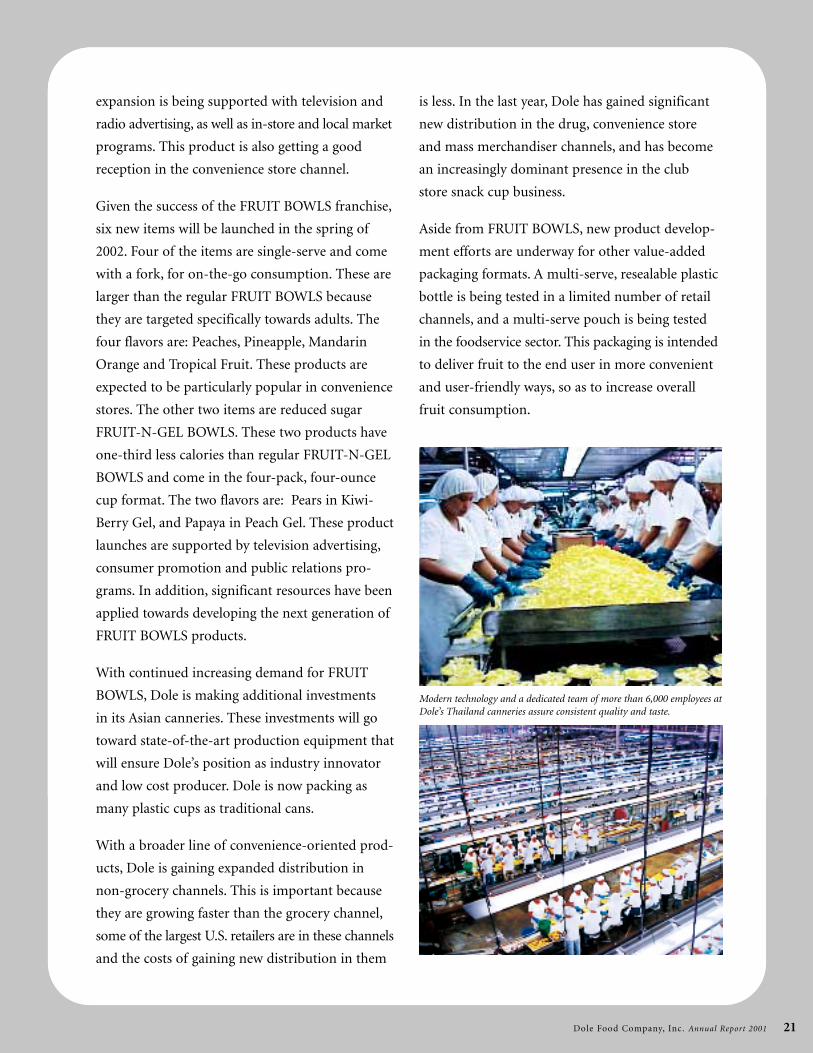

Modern technology and a dedicated team of more than 6,000 employees atDole’s Thailand canneries assure consistent quality and taste.

Dole Food Company, Inc. Annual Report 2001 22

We were some-

what disappoint-

ed with the per-

formance of our

fresh-cut flowers

segment during

the year, where we continued to experience inte-

gration challenges and unfavorable market condi-

tions. These have slowed our progress in reposi-

tioning this business. We are looking forward to

enhanced distribution efficiencies from our

Miami, Florida-based operations, which were

recently relocated into a new combined world-

wide divisional headquarters facility.

This new 328,000 square foot facility centralizes

production, warehousing and shipping opera-

tions, in addition to housing sales, marketing

and administrative offices. Located on 17 acres

in International Corporate Park, the new facility

began operations on December 17, 2001 with

300 employees, and will operate year-round. A

unique merchandising room showcases Dole’s 820

varieties of fresh-cut flowers, including 170 vari-

eties of roses, to prospective customers. Also, a

modern technical laboratory allows for continual

floral research and development. The consolida-

tion of operations from up to seven buildings at

peak holiday periods into one state-of-the-art

facility will streamline the handling of flowers

from production to distribution to receipt by our

customers. This will significantly improve cold-

chain management and tighten inventory control

and handling of product resulting in reduced

shrink costs and improved flower quality.

Within the facility, over 200,000 square feet is

refrigerated by a glycol ammonia system. This

system can control the variability in temperature

within one-half degree, which has been proven

to increase the vase life of fresh-cut flowers. This

expansive refrigerated space allows for no inter-

ruption in the cold chain, ensuring top quality

products to the customer. A receiving area of

Dole Fresh Flowers

We anticipate enhanced distribution efficiencies in 2002 from our new 328,000

square foot facility in Miami, Florida. Previously housed in seven separate

buildings, operations are now consolidated.

Our Top SellersDole Fresh Flowers is the largest rose importer of Colombia’s flowers and the

only importer with guaranteed daily deliveries by air. Immediately after har-

vesting, DOLE flowers are flown to the new Miami facility where tempera-

tures are maintained within one-half degree of required levels in all warehouse

and production operations. Maintaining the cold chain enables Dole to deliver

the freshest and healthiest flowers to the market.

Dole Food Company, Inc. Annual Report 2001 23

Dole Food Company, Inc. Annual Report 2001 24

Miami Facility FactsMiami is the U.S. gateway for the floral industry, since the majority of flowers for

commercial use are grown in South America. Dole Fresh Flowers grows its product

on nearly 20 farms throughout Colombia, Ecuador and Mexico. Nearly three mil-

lion stems of flowers pass through Dole’s new Miami facility every day during the

holiday season.

Dole Food Company, Inc. Annual Report 2001 25

30,000 square feet ensures incoming product is

handled with speed. Over 37,000 square feet is

dedicated towards production and processing of

bouquets and arrangements. Additionally, 135,000

square feet of warehouse and shipping space

allows for the handling of large quantities of

simultaneous orders.

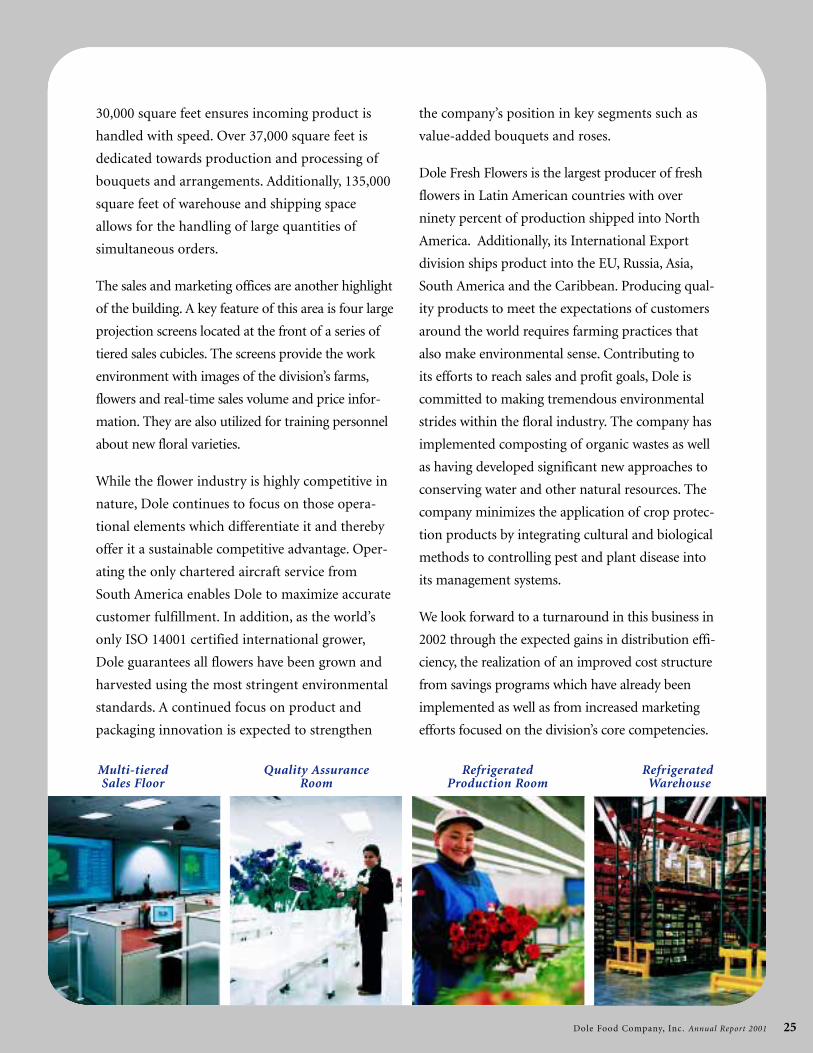

The sales and marketing offices are another highlight

of the building. A key feature of this area is four large

projection screens located at the front of a series of

tiered sales cubicles. The screens provide the work

environment with images of the division’s farms,

flowers and real-time sales volume and price infor-

mation. They are also utilized for training personnel

about new floral varieties.

While the flower industry is highly competitive in

nature, Dole continues to focus on those opera-

tional elements which differentiate it and thereby

offer it a sustainable competitive advantage. Oper-

ating the only chartered aircraft service from

South America enables Dole to maximize accurate

customer fulfillment. In addition, as the world’s

only ISO 14001 certified international grower,

Dole guarantees all flowers have been grown and

harvested using the most stringent environmental

standards. A continued focus on product and

packaging innovation is expected to strengthen

the company’s position in key segments such as

value-added bouquets and roses.

Dole Fresh Flowers is the largest producer of fresh

flowers in Latin American countries with over

ninety percent of production shipped into North

America. Additionally, its International Export

division ships product into the EU, Russia, Asia,

South America and the Caribbean. Producing qual-

ity products to meet the expectations of customers

around the world requires farming practices that

also make environmental sense. Contributing to

its efforts to reach sales and profit goals, Dole is

committed to making tremendous environmental

strides within the floral industry. The company has

implemented composting of organic wastes as well

as having developed significant new approaches to

conserving water and other natural resources. The

company minimizes the application of crop protec-

tion products by integrating cultural and biological

methods to controlling pest and plant disease into

its management systems.

We look forward to a turnaround in this business in

2002 through the expected gains in distribution effi-

ciency, the realization of an improved cost structure

from savings programs which have already been

implemented as well as from increased marketing

efforts focused on the division’s core competencies.

Multi-tiered Quality Assurance Refrigerated RefrigeratedSales Floor Room Production Room Warehouse

Dole Food Company, Inc. Annual Report 2001 26

Fresh Fruit Fresh Vegetables Packaged Foods Fresh-cut Flowers

Other OperatingSegments

Total

99 00 01 99 00 01

Fresh Fruit

99 00 01

Fresh Vegetables

99 00 01

Packaged Foods

99 00 01

Fresh-cut Flowers

99 00 01

Other OperatingSegments

Total OperatingSegments

99 00 01 99 00 01

Fresh Fruit

99 00 01

Fresh Vegetables

99 00 01

Packaged Foods

99 00 01

Fresh-cut Flowers

99 00 01

Other OperatingSegments

Total OperatingSegments

99 00 01 99 00 01

Fresh Fruit

99 00 01

Fresh Vegetables

99 00 01

Packaged Foods

99 00 01

Fresh-cut Flowers

99 00 01

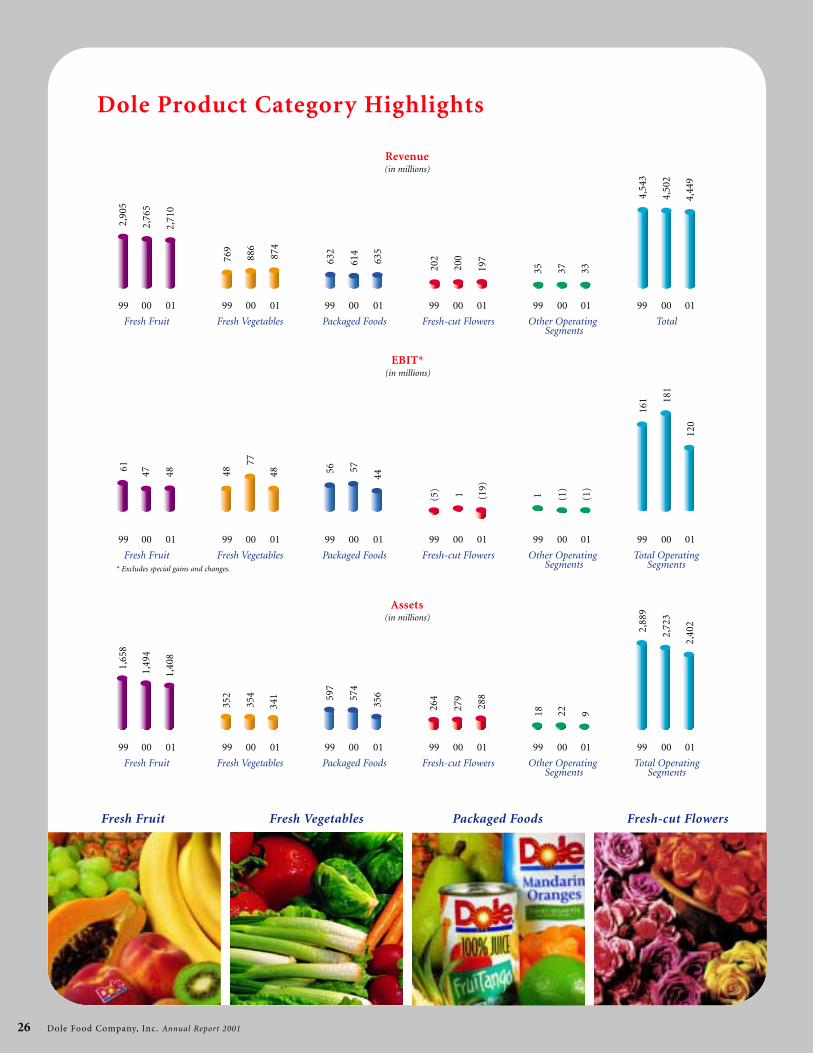

Dole Product Category Highlights2,

905

2,76

5

2,71

0

769

886

874

632

614

635

202

200

197

4,54

3

4,50

2

4,44

9

35 37 33

61 47 48 48

77

48 56 57

44

(5) 1 (19)

161 18

1

120

1,65

8

1,49

4

1,40

8

352

354

341 59

7

574

356

264

279

288

2,88

9

2,72

3

2,40

2

Revenue(in millions)

EBIT*(in millions)

Assets(in millions)

1 (1)

(1)

18 22 9

* Excludes special gains and changes.

Dole Food Company, Inc. Annual Report 2001 27

Results of Operations and Selected Financial Data

(in millions, except per-share data) 2001 2000 1999 1998 1997

Revenue $ 4,449 $ 4,502 $ 4,543 $ 3,938 $ 3,852

Cost of products sold 3,881 3,878 3,945 3,380 3,265

Gross margin 568 624 598 558 587

Selling, marketing and general and

administrative expenses 518 499 480 397 376

Gain on sale of citrus assets – (9) – – –

Business downsizing charges – 46 48 – –

Hurricane Mitch charge (insurance proceeds) – net – (43) (20) 78 –

Citrus charge – – – 20 –

Operating income 50 131 90 63 211

Interest expense – net 65 76 76 56 54

Other income (expense) – net 7 1 6 (4) 11

Income (loss) from continuing operations

before income taxes (8) 56 20 3 168

Income taxes 29 20 3 2 24

Income (loss) from continuing operations (37) 36 17 1 144

Income from discontinued operations, net of taxes 19 32 32 11 16

Gain on disposal of discontinued operations,

net of taxes 168 – – – –

Net income 150 68 49 12 160

Diluted net income (loss) per common share

Continuing operations $ (0.66) $ 0.65 $ 0.29 $ 0.02 $ 2.39

Discontinued operations 3.33 0.56 0.56 0.18 0.26

Net income 2.67 1.21 0.85 0.20 2.65

Other statistics

Working capital $ 511 $ 356 $ 381 $ 366 $ 407

Total assets 2,747 2,801 2,994 2,864 2,414

Long-term debt 816 1,135 1,285 1,116 755

Total debt 843 1,180 1,323 1,152 767

Common shareholders’ equity 736 555 532 622 666

Annual cash dividends per common share 0.40 0.40 0.40 0.40 0.40

Capital additions 120 111 137 118 111

Depreciation and amortization 118 125 124 116 107

Note: Revenue and cost of products sold for 2001, 2000, 1999,1998 and 1997, reflect reclassifications of $169 million,$239 million, $266 million, $235 million and $271 million,respectively, to present revenues in accordance with theinterpretations of Staff Accounting Bulletin No. 101 issued bythe Securities and Exchange Commission, which was adoptedby the Company during the fourth quarter of 2000 (see Note 2to the Consolidated Financial Statements). Cost of products

sold for 2001 includes business reconfiguration charges of $133million (see Note 5 to the Consolidated Financial Statements).Hurricane Mitch charge (insurance proceeds) – net includesrehabilitation expenses and other costs of $10 million and $25million in 2000 and 1999, respectively, and insurance proceedsof $53 million and $45 million in 2000 and 1999, respectively(see Note 5 to the Consolidated Financial Statements).

Dole Food Company, Inc. Annual Report 2001 28

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Washington. Programs initiated during the third quarter of2001 constituted $105 million of these one-time expenses andincluded costs associated with the planned divestiture of theCompany’s Pascual Hermanos fresh vegetables business inSpain and certain other non-core businesses in Europe, as wellas the downsizing of banana and flower operations in LatinAmerica and banana production in the Philippines. A majorityof the costs associated with these programs consisted of assetimpairments necessary to write certain assets down to fairvalue, less costs to sell. Also included in the $133 million ofexpense, were $42 million of accrued costs for employee sever-ance, contract terminations and other costs associated withdivestiture, closure and other reconfiguration activities. A totalof 3,179 employees in the Company’s operations are being severed under these plans, of which 1,234 have been severed as of December 29, 2001. The Company anticipates the $133million of charges to result in approximately $42 million oftotal cash payments, of which $11 million were incurred in2001 with the remainder to be incurred primarily in 2002.The Company does not expect any further significant businessreconfiguration charges associated with these programs in the future.

While the most significant accomplishments relative to recon-figuration of its operations were made in 2001, the Companydid commence plans to reconfigure its operations in earlieryears. Due largely to continuing oversupply and other marketconditions primarily affecting the Company’s fresh fruit seg-ment, particularly its banana business, the Company imple-mented a plan during the latter part of 1999 to downsize certain of its global operations, and to initiate an early retire-ment program. In connection with its plan, the Companyrecorded a $48 million charge in the fourth quarter of 1999,which was reported on a separate line in the ConsolidatedStatements of Income. The $48 million charge included costs to reduce the Company’s productive capacity and distributioninfrastructure in its fresh fruit operations, primarily bananas.In Latin America, the Company ceased operations in Nicaraguaand Venezuela and terminated certain ship charters and growercontracts. In its European operations, the Company closed certain production and distribution sites and sales offices.In North America, the Company exited its citrus business inFlorida and its almond processing business in California.Costs to sever 1,483 employees were included in this plan, ofwhich all had been severed as of December 29, 2001. TheCompany’s early retirement program resulted in the termina-tion of 92 employees.

In the third quarter of 2000, the Company initiated a plan tocontinue the downsizing of its fresh fruit operations, includingthe complete shutdown of certain activities. In connectionwith its plan, the Company recorded a $46 million charge,which was reported on a separate line in the ConsolidatedStatements of Income. The $46 million charge included coststo further reduce the Company’s existing productive capacityin its banana operations in Latin America and Asia, as well ascosts to shutdown its melon and citrus farming activities in

Overview

During 2001, Dole Food Company, Inc. and its consolidatedsubsidiaries’ (“the Company”) results of operations and finan-cial condition were favorably impacted by the following factors:

• The implementation of Company-wide cost savings initiatives,

• The continued review of non-core and underperformingbusinesses and the initiation of plans for their divestiture,

• Improved conditions in the banana business.

These factors were partially offset by weak foreign currencyexchange rates, primarily the yen.

During the first quarter of 2001, the Company undertook anextensive cost savings initiative and engaged the BostonConsulting Group to assist in performing strategic and opera-tional reviews of its banana and fresh-cut flowers businessesand in implementing programs to enhance profitability andachieve consolidated savings from global strategic sourcing andlogistics. The Company completed this review in the fourthquarter of 2001 and expects these critical assessments to resultin cost savings and improved market focus, which shouldenhance profitability. The Company’s cost-cutting activitiesmainly included the elimination of shipping services, exitingmore costly fruit sourcing arrangements and the consolidationof selling and general and administrative functions.

The Company expects to realize $200 million of annualimprovements to operating results on a steady state basis by2003 as a result of these initiatives.

For 2001, the Company realized approximately $93 million of savings, before offsets, when compared to operating resultsfor 2000. Offsets included the impact of lower pricing forcommodity vegetables, reduced sales volumes for fresh-cutflowers, the effect of foreign currency exchange primarily fromthe yen, the absence of earnings from the Honduran beveragebusiness and consulting costs associated with the strategic andoperational reviews of the Company’s businesses. Of the $93million of savings, approximately $25 million was recognizedin pre-tax income, after offsets. For 2002, the Company expectsan additional $66 million in profit improvements, with ananticipated favorable impact of $30 million on pre-tax income.This amount, combined with $13 million of 2001 one-timeoffsets that will not be present in 2002, should result inapproximately $43 million of incremental improvement in pre-tax profit as a result of these programs. The remaining $41million of savings is expected to be realized in 2003.

The business reconfiguration programs resulted in the recog-nition of $133 million of one-time expenses for the year.Programs initiated during the second quarter of 2001 generated$28 million of these one-time expenses and included the shut-down and related asset sales of the Company’s Californiadeciduous and Pacific Northwest apples operations, includingpackinghouses, ranches and orchards in California and

Dole Food Company, Inc. Annual Report 2001 29

Honduras and the downsizing of its distribution network in Europe. In its Latin American banana operations, theCompany closed select production sites, severed some employeearrangements, terminated some contracts with independentgrowers and divested its controlling interest in a productionjoint venture in South America. In its Asian banana opera-tions, the Company exited production on select agriculturallands and terminated some employees and contracts withindependent growers. In its European operations, theCompany reduced its sales force and administrative staff, pri-marily in northern Europe. A total of 4,880 employees in theCompany’s operations are being severed under these plans,of which 4,871 have been severed as of December 29, 2001.

In November 2001, the Company disposed of its 97% of thecapital stock of a Honduran corporation principally engaged inthe beverage business in Honduras, Cerveceria Hondurena S.A.(“the Honduran beverage business”). The disposition wasaccomplished by means of a stock exchange transaction with asubsidiary of South African Breweries, plc. Subsequent to thestock exchange transaction, the Company received $537 millionof cash. The proceeds from the divestiture have been used pri-marily to pay down debt. The Honduran beverage businessresults have been reported as discontinued operations throughNovember 28, 2001, the date of the disposition.

In the latter part of 1999, the Company first began a review ofits non-core assets and under-performing businesses with theintention to sell or liquidate those that fell outside of theCompany’s future strategic direction or that did not meetinternal economic return criteria. This review led to the divestiture of certain businesses as follows:

In 2000, the Company sold the assets of its citrus operationslocated in California and Arizona for approximately $55 mil-lion. Production assets were transferred to the buyer in thethird quarter of 2000 for cash proceeds of $45 million, result-ing in a net gain of $8 million. The remaining $10 million ofproceeds were for secured grower contracts, approximately halfof which were transferred to the buyer in the fourth quarter of2000, resulting in a net gain of $1 million. The combined $9 million net gain has been reported on a separate line in theConsolidated Statements of Income. Title to the remaininggrower contracts was transferred at near book value in the first quarter of 2001.

The Company also sold its Florida citrus and California almondoperations in 2000 and is currently pursuing the sale of itsdeciduous fruit businesses located in North America. In total,these sales are expected to generate gross proceeds of approxi-mately $95 million.

Furthermore, the Company is pursuing the sale of its PascualHermanos fresh vegetables business in Spain and other non-core businesses in Europe. No final determination as to expect-ed proceeds has been made.

In 2001, the Company began to benefit from the downsizing ofits operations in prior years. The banana business improved

primarily as a result of the Company’s significant cost savingactivities, higher banana volumes and pricing in NorthAmerica, and favorable local pricing in Europe partially offsetby the decline in the euro against the U.S. dollar. Managementanticipates that the North American and European marketimprovements will stabilize in the near term.

The Company continued to be negatively impacted by unfavor-able declines in foreign currency exchange rates. In 2001,the yen continued to weaken against the U.S. dollar, decreasing13% on an average basis during the year compared to theaverage in 2000. The euro also steadily declined, stabilizing inthe latter part of the year compared to the average in 2000.The Company has significant Japanese sales denominated inyen as well as European sales denominated in euro or curren-cies with exchange rates pegged to the euro. Product andshipping costs associated with a portion of these sales are U.S. dollar-denominated. The decline in the yen and euro in2001 negatively impacted the Company’s revenues and earningsbefore interest and taxes (“EBIT”) by approximately $85million and $35 million, respectively.

European Union Quota: The European Union (“EU”) main-tains banana regulations that impose quotas and tariffs onbananas. In April 2001, the EU reached agreements with theUnited States and Ecuador to implement a tariff-only importsystem no later than January 1, 2006. In the interim periodbeginning July 1, 2001, European companies that operated andbought bananas and sold them into the EU market during theyears 1994-1996 are eligible for banana import licenses. TheCompany’s earnings have not been negatively impacted by thenew interim regime, and it believes the ongoing impact of thisregime will not be dilutive to its current earnings levels.

Financial Instruments: As of December 29, 2001, theCompany’s derivative instruments, both free-standing andembedded, as defined by Statement of Financial AccountingStandards No. 133 (“FAS 133”), “Accounting for DerivativeInstruments and Hedging Activities,” as amended by FASBStatement of Financial Accounting Standards No. 138,“Accounting for Certain Derivative Instruments and CertainHedging Activities – An amendment of FASB Statement No.133,” consisted of foreign currency exchange forwards andcertain minor warrants in privately held companies.

The Company entered into foreign currency exchange forwardcontracts to reduce its risk related to anticipated working capitalcollections and payments denominated in foreign currencies.These contracts are denominated in Japanese yen, Britishpounds, Swedish krona and the euro and are designated ashedges under FAS 133. The Company’s foreign currencyexchange forwards, in an aggregate outstanding notionalamount of $171 million, were designated and effective as hedgesof the changes in fair values of recorded assets or liabilities or offuture cash flows. The ineffective portion of changes in fair val-ues of hedge positions, which was included in operating incomefor 2001, was not material. Unrealized net gains related to cash

Dole Food Company, Inc. Annual Report 2001 30

flow hedges totaling $15 million were included as a componentof accumulated other comprehensive loss as of December 29,2001. Settlement of these contracts will occur in 2002.

The counterparties to the foreign currency exchange forwardcontracts consist of a number of major international financialinstitutions. The Company has established counterparty guide-lines and regularly monitors its positions and the financialstrength of these institutions. While counterparties to hedgingcontracts expose the Company to credit-related losses in theevent of a counterparty’s non-performance, the risk would belimited to the unrealized gains on such affected contracts. TheCompany does not anticipate any such losses.

In 2000, the Company received stock warrants in two privatelyheld companies through which the Company sells a portion ofits products. The Company can, at its option, purchase twomillion shares upon public registration of the two privatelyheld companies at a weighted-average price of $5.75 per share.The Company estimated that the fair value of these warrantswas not significant as of December 29, 2001.

In the normal course of business, the Company entered intovarious commodity purchase and sale contracts. These con-tracts qualify as a normal purchase and sale under FAS 133 and are excluded from mark-to-market accounting.

In 1998, the Company had contracted to purchase Germanmarks primarily at fixed exchange rates to facilitate paymentfor the purchase of two German-made refrigerated containervessels. In the fourth quarter of 1999, in conjunction with thetermination of the Company’s purchase obligation, it enteredinto an operating lease for the vessels. In the fourth quarter of 1999, these currency exchange contracts were terminatedresulting in a pre-tax charge to operating income of approxi-mately $2 million.

Foreign Currencies: The Company distributes its products inmore than 90 countries throughout the world. Its internationalsales are usually transacted in U.S. dollars and major Europeanand Asian currencies. Certain costs are incurred in currenciesdifferent from those received from the sale of products. Resultsof operations may be affected by fluctuations in currencyexchange rates in both sourcing and selling locations. However,prior to 2001, the Company has, with minor exceptions, nothedged these exposures.

During 2001, the yen as well as the euro and related Europeancurrencies continued to weaken against the U.S. dollar.Subsequent to year-end, the euro and related European curren-cies have stabilized somewhat against the U.S. dollar, while theyen has continued to weaken significantly. As of March 1, 2002,the spot exchange rate between the yen and the U.S. dollar hadfallen 10% versus the average exchange rate in effect during2001. The Company has approximately $500 million of annualsales denominated in yen. Additionally, in 2001, the Companyincurred $14 million of foreign currency translation losses,which were recognized as a component of accumulated other

comprehensive loss in shareholders’ equity and included in thecalculation of comprehensive income. The Company currentlyestimates that a 1% change in value of the yen-to-U.S. dollarand the euro-to-U.S. dollar exchange rates would each impactEBIT by approximately $2 million. The ultimate impact offuture changes to these and other currency exchange rates on2002 revenues, operating income, net income, equity and com-prehensive income is not determinable at this time.

Euro Conversion: On January 1, 2002, twelve participatingmembers of the EU converted to the euro as their commonlegal currency. Aside from certain minor conversion efforts in2001, the Company has not experienced any significant impactsupon conversion. The Company also does not anticipate anysignificant impacts due to price transparency or other long-term competitive implications.

Related Party Transactions: The Company’s policy permits it tohave arms-length transactions with related parties.

David H. Murdock, the Company’s Chairman and ChiefExecutive Officer, owns Castle & Cooke, Inc. (“Castle”), a realestate and resorts business, as well as a transportation equip-ment leasing company, a private dining club and a privatecountry club, which supply products and provide services tonumerous customers and patrons. During fiscal 2001, 2000 and 1999, the Company paid Mr. Murdock’s companies anaggregate of approximately $2 million in each year.

In 1995, Castle issued to the Company a promissory note in the principal amount of $10 million, which was repaid inDecember 2000. The $10 million note bore interest at the rate of 7% per annum, payable quarterly. Castle incurred and paid $0.7 million of interest expense in both 2000 and1999 pursuant to the terms of the $10 million note.

The Company and Castle each hold a 50 percent interest in anairplane, which was formerly owned solely by the Company.Under a co-ownership agreement, the Company and Castleagreed that each party would be responsible for the direct costsassociated with its use of the airplane, and that all indirect costswould be equally shared.

At December 29, 2001, the Company was under contractualobligation for the delivery of a replacement aircraft. TheCompany’s share of the total aircraft cost of approximately $45 million is $30 million. The remaining cost of the aircraft is an obligation of Castle.

Critical Accounting Policies and Estimates

The preparation of the Consolidated Financial Statementsrequires management to make estimates and assumptions thataffect reported amounts. The estimates and assumptions areevaluated on an on-going basis and are based on historicalexperience and on other factors that management believes arereasonable. Estimates and assumptions include, but are notlimited to, the areas of customer and grower receivables, inven-tories, assets held for sale, useful lives of property, plant and

Dole Food Company, Inc. Annual Report 2001 31

equipment, intangible assets, marketing programs, incometaxes, self-insurance reserves, retirement benefits, and commit-ments and contingencies.

The Company believes that the following represent the areaswhere more critical estimates and assumptions are used in thepreparation of the Consolidated Financial Statements:

Grower advances: The Company advances funds to third partygrowers primarily in Latin America and Asia for various farm-ing needs. Some of these advances are secured with propertyor other collateral owned by the growers. The Companyrecords an allowance for these grower receivables based on estimates of the growers’ ability to repay advances and the fairvalue of the collateral. The Company monitors these receivableson a regular basis. If the financial condition of the growers orthe fair value of the collateral were to deteriorate, additionalallowances may be required.