document of the world banksiteresources.worldbank.org/.../resources/cassenegal20072010.pdf ·...

TRANSCRIPT

Document of The World Bank

FOR OFFICIAL USE ONLY

Report No. 36608-SN

INTERNATIONAL DEVELOPMENT ASSOCIATION

AND

INTERNATIONAL FINANCE CORPORATION

COUNTRY ASSISTANCE STRATEGY

FOR

THE REPUBLIC OF SENEGAL

FOR THE PERIOD FY07-FY10

May 2, 2007

Poverty Reduction and Economic Management 4 Country Department AFCF1 Africa Region This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

ii

CURRENCY EQUIVALENTS (As of January 31, 2007)

Currency Unit = CFA Franc (CFAF) US$1 = CFAF 482

FISCAL YEAR January 1 – December 31

ABBREVIATION AND ACRONYMS

AAA Analytical and Advisory Activities AAP Africa Action Plan AFD Agence Française de Développement (French Development Agency) AFDB African Development Bank AG Accelerated Growth AGS Accelerated Growth Strategy APIX Agence de Promotion des Investissements et des Grands Travaux

(Investment Promotion and Infrastructure Agency) BASICS Basic Support for Institutionalizing Child Survival BCI Budget Consolidé de l’Investissement (Consolidated Investment Budget) BOAD West African Development Bank BOT Build-Operate-Transfer CAS Country Assistance Strategy CDD Community Driven Development CEM Country Economic Memorandum CESAG Centre Africain d'Etudes Supérieures de Gestion (Regional Training Institutions in Financial Management) CFAA Country Financial Accountability Assessment CIDA Canadian International Development Agency CPAR Country Procurement Assessment Report CPIA Country Policy and Institutional Assessment DFID Department for International Development (UK) DPL Development Policy Lending DTC3 Diphtheria Tetanus Whooping-cough 3 ECOWAS Economic Community of West African States EU European Union FDD Fonds de Dotation à la Décentralisation (Decentralization Fund) FAO Food and Agriculture Organization of the United Nations FECL Fonds d’Equipement des Collectivités Locales (Fund for Local Governments Equipment) FIAS Foreign Investment Advisory Service FMG/C Financial Management Group/Conference FSAP Financial Sector Assessment Program GDP Gross Domestic Product GEF Global Environment Facility GIRMaC Gestion des Ressources Marines et Côtières au Sénégal

(Integrated Marine and Coastal Resources Management Project) GNI Gross National Income GNP Gross National Product HIPC Heavily Indebted Poor Countries HIV/AIDS Human Immuno-deficiency Virus/Acquired Immune Deficiency Syndrome IBRD International Bank for Reconstruction and Development ICA Investment Climate Assessment ICS Integrated Controller’s System ICT Information and Communication Technology ICS Industries Chimiques du Sénégal (Chemical Industries of Senegal) IDA International Development Association IFAC International Federation of Accountants IFC International Finance Corporation IPP Independent Power Producer JICA Japan International Cooperation Agency

iii

KfW German Cooperation MCA Millennium Challenge Account MDG Millennium Development Goals MDRI Multilateral Debt Relief Initiative MIGA Multilateral Investment Guarantee Agency MOU Memorandum of Understanding MTEF Medium-term Expenditure Framework MW Megawatts NGO Non-Governmental Organization OECD Organization for Economic Co-operation and Development OED Operations Evaluation Department OMVS Organisation de la Mise en Valeur du Fleuve Sénégal (Senegal River Basin Organization) PAMU Projet d’Amélioration de la Mobilité Urbaine (Urban Mobility Improvement Project) PCG Partial Credit Guarantee PDMAS Programme de Développement des Marchés Agricoles (Agricultural Markets and Agribusiness Development

Project) PEFA Public Expenditure Financial Assessment PEP Private Enterprise Partnership PEQT Projet Education de Qualité pour Tous (Quality Education for All) PER Public Expenditure Review PHC Primary Health Care PIPP Private Investment Promotion Project PNDL Programme Nationale de Développement Local (National Local Development Program) PRECOL Projet de Renforcement et d’Equipement des Collectivités Locales (Local Authorities Development Program) PROGEDE Projet de Diffusion de l’Accès aux Services Electriques Ruraux

(Sustainable and Participatory Energy Management project) PRS Poverty Reduction Strategy PRSC Poverty Reduction Support Credit PRSP Poverty Reduction Strategy Paper PSAC Private Sector Adjustment Credit PSAOP Programme des Services Agricoles et des Organisations de Producteurs (Agricultural Services and Producer

Organization Project) PSD Private Sector Development REER Real Effective Exchange Rate ROSC Report on the Observance of Standards and Codes SENELEC Société Nationale d’Eau et d’Electricité (Electric Company of Senegal) SIP Small Investment Program SLM Sustainable Land Management SME Small and Medium Enterprise SOE State-owned Enterprise SSA Sub-Saharan Africa STEP-ILO International Labor Organization SYSCOA Système Comptable Ouest Africain (Integrated Financial Management Software) UNDP United Nations Development Programme UNESCO United Nations Educational, Scientific and Cultural Organization UNICEF United Nations Children's Fund USAID United States Agency for International Development WAAP West Africa Agricultural Productivity WAEMU West African Economic and Monetary Union WBG World Bank Group WBI World Bank Institute WDR World Development Report WHO World Health Organization

IDA IFC

Vice President Country Director

Sector Manager Task Team Leader

Obiageli Ezekwesili (AFRVP) Madani M. Tall (AFCF1) Antonella Bassani (AFTP4) Jacques Morisset (AFTP4)

Vice President Director Director Country Manager

Eduard Nassim (CAMVP) Thierry Tanoh (CAFDR) Richard Ranken (CEAHK) Aida der Hovanessian (DKRIFC)

iv

THE REPUBLIC OF SENEGAL

COUNTRY ASSISTANCE STRATEGY

TABLE OF CONTENTS

EXECUTIVE SUMMARY ...................................................................................................................................... VI 1. INTRODUCTION ................................................................................................................................................1 2. COUNTRY CONTEXT .......................................................................................................................................1

A. POLITICAL AND INSTITUTIONAL BACKGROUND ...............................................................................................1 B. RECENT ECONOMIC DEVELOPMENTS ...............................................................................................................2 C. MEDIUM-TERM OUTLOOK AND SUSTAINABILITY.............................................................................................4 D. POVERTY PROFILE AND UNEQUAL PROGRESS TOWARD MDGS .......................................................................4

3. SENEGAL’S MAIN DEVELOPMENT CHALLENGES.................................................................................7 A. IMPROVING PUBLIC SERVICE DELIVERY ..........................................................................................................8 B. ENHANCING PRIVATE SECTOR DEVELOPMENT ..............................................................................................13

4. SENEGAL’S LONG-TERM VISION AND MEDIUM-TERM PRIORITIES.............................................17 5. WORLD BANK GROUP ASSISTANCE.........................................................................................................20

A. LESSONS FROM PAST EXPERIENCES AND CONSULTATION STRATEGY..............................................................20 B. PROPOSED BANK PROGRAMS AND EXPECTED OUTCOMES .............................................................................21 C. DELIVERY OF THE BANK’S ASSISTANCE PROGRAM ........................................................................................36 D. LENDING AND THE AAA SUPPORT PROGRAM.................................................................................................38

6. COUNTRY RISK MANAGEMENT AND MONITORING ..........................................................................42 A. MAIN RISKS AND MITIGATION REMEDIES......................................................................................................42 B. PERFORMANCE MONITORING & EVALUATION ...............................................................................................44

7. CONCLUDING REMARKS.............................................................................................................................45

v

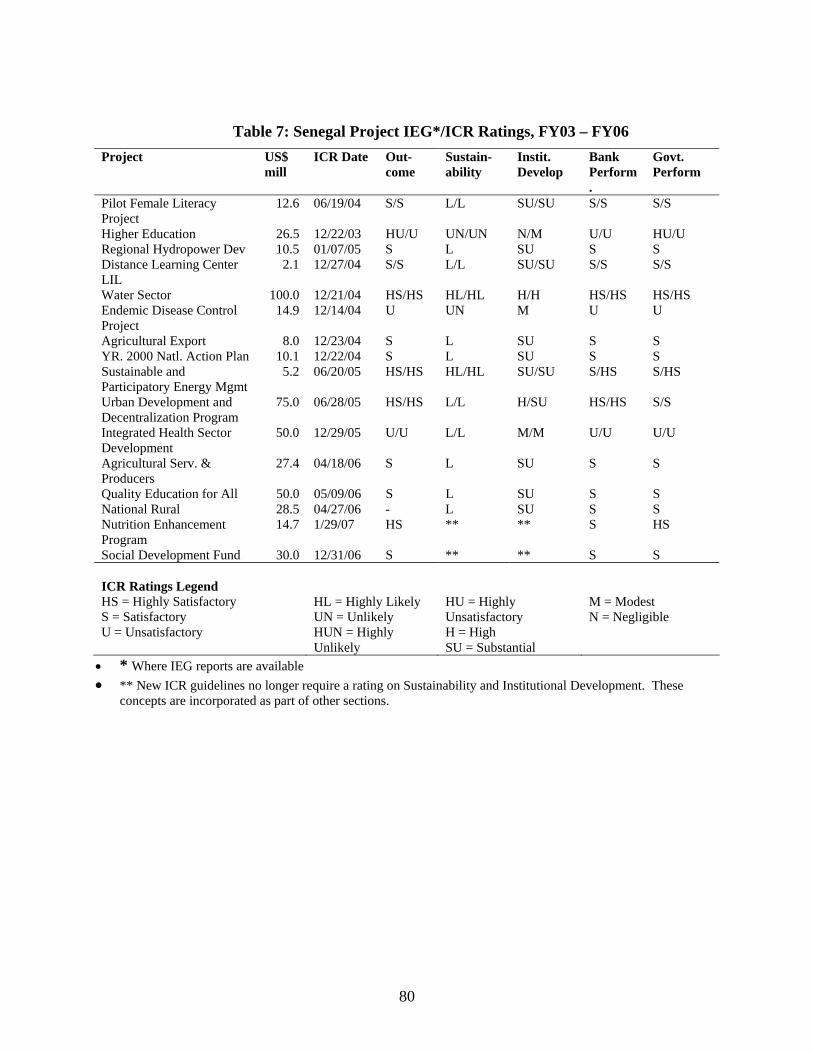

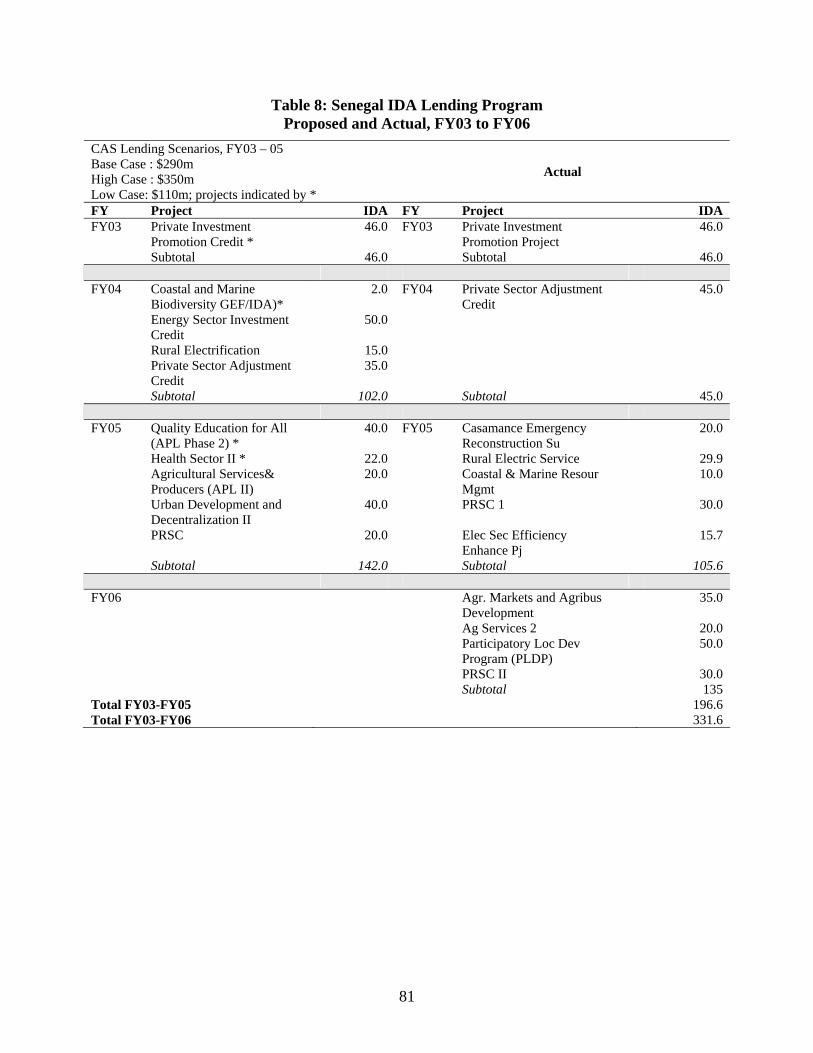

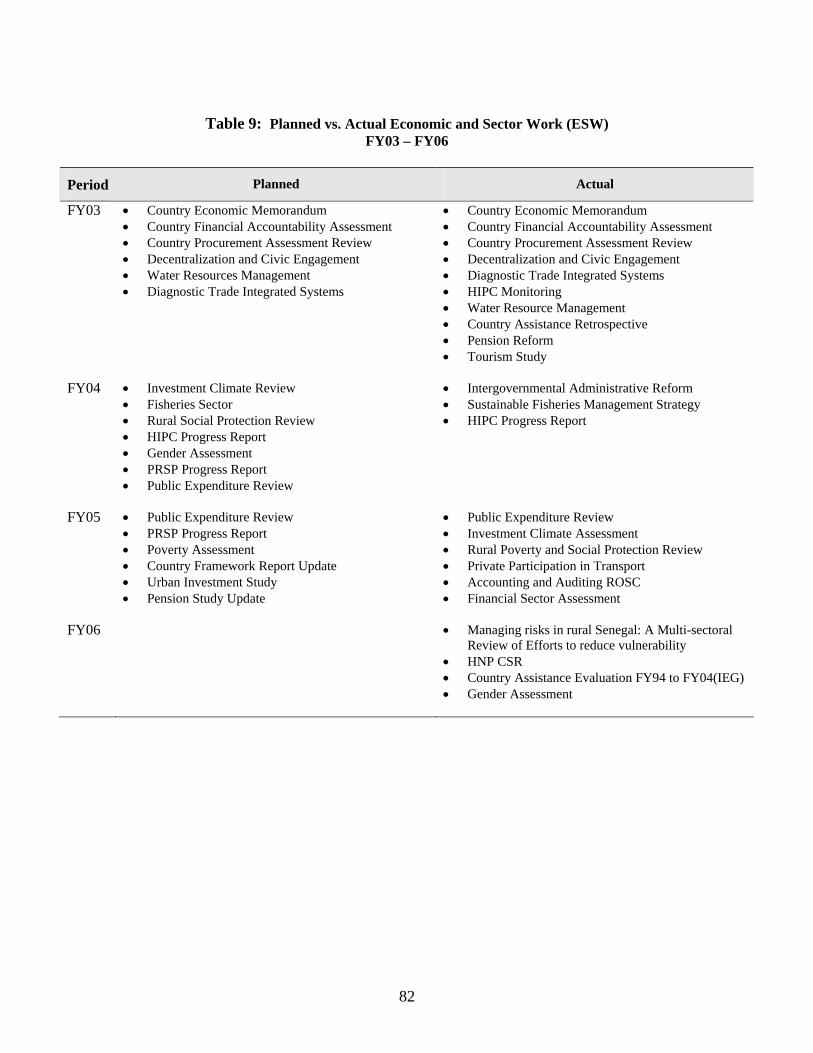

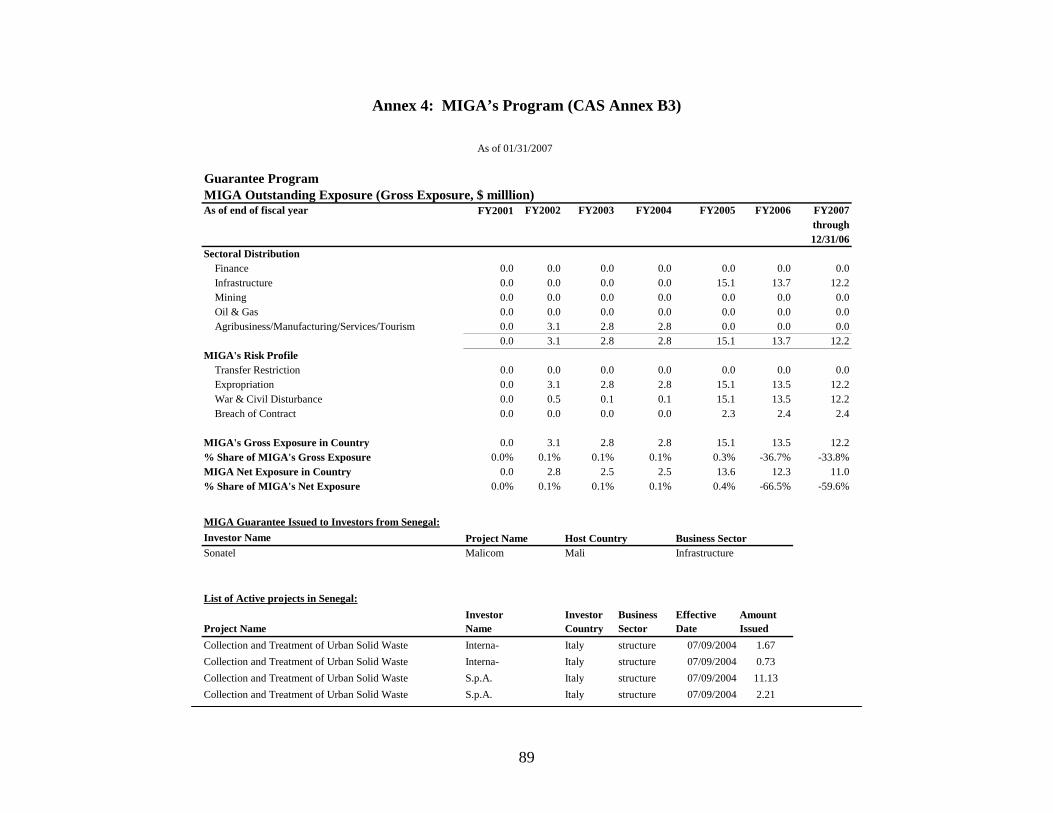

List of Annexes Annex 1: Results-Oriented CAS Matrix .................................................................................................. 47 Annex 2: CAS Completion Report FY03-FY06...................................................................................... 58 Annex 3: IFC Strategy (CAS Annex B8)................................................................................................. 84 Annex 4: MIGA’s Program (CAS Annex B3)......................................................................................... 89 Annex 5: Joint Fund-World Bank Debt Sustainability Analysis ............................................................. 92 Annex 6: CAS Consultations and Outreach........................................................................................... 104 Annex 7: CAS Harmonization and Coordination with Other Donors ................................................... 106 Annex 8: Senegal at a Glance (CAS Annex A2) ................................................................................... 111 Annex 9: Key Economic Indicators (CAS Annex B6) .......................................................................... 113 Annex 10: Key Exposure Indicators (CAS Annex B7) ........................................................................... 116 Annex 11: Operations Portfolio (IBRD/IDA and Grants) (CAS Annex B8)........................................... 117 Annex 12: Selected Indicators of Bank Portfolio Performance and Management (CAS Annex B2)...... 118 Annex 13: IBRD/IDA Program Summary (CAS Annex B3) .................................................................. 119 Annex 14: CAS Summary of Non-lending Services (Annex B4)............................................................ 120 Country Map IBRD 33475........................................................................................................................ 121 List of Tables Table 2.1: World Bank Institute (WBI) Governance Indicators in 2004-05................................................ 2 Table 2.2: Senegal Compared to the Rest of Sub-Saharan Africa ............................................................... 3 Table 5.1: Summary of CAS Results-Based Framework........................................................................... 33 Table 5.2: Proposed World Bank Group Program (Base Case)................................................................. 40 Table 5.3: Senegal in comparison of other Sub-Saharan Africa countries 2005 CPIA scores .................. 41 List of Figures Figure 3.1: Contributions to Economic Growth by Sector (2000-04)........................................................ 16 Figure 5.1: Ongoing and proposed IDA Lending Program up to FY10 .................................................... 42 List of Boxes Box 2.1: Street Children in Senegal............................................................................................................. 6 Box 3.1: Main Achievements in Public Financial Management and Remaining Issues............................ 12 Box 3.2: Constraints to Growth in Senegal: What do private investors tell us? ....................................... 14 Box 5.1: Gender Development in the CAS................................................................................................ 35

The following World Bank Staff contributed to the preparation of the CAS: Jacques Morisset (TTL), Francoise Perrot, Iradj Alikhani, Fily Sissoko, Bourama Diaite, Leif Jensen, Sidi Boubacar, Ronnie Hammad, Suzanne Otis, Adama El Hadj Toure, Renato Nardello, Vincent Palmade, Peter Mousley, Moctar Thiam, Moukim Temourov, Eric de Roodenbecke, Aissatou Diack, Julien Bandiaky, André Ryba, Ibou Diouf, Christian Diou, Michel Layec, Awa Seck, Isabelle Huynh, Yann Burtin, Tomas Vis, David Bridgman, Manievel Sene, Peter Kristensen, Yves-Andre Prevost, Sonia Plaza, Guy Darlan, Mademba Ndiaye, Lily Mulatu, Geraldo Martins, Demba Balde, Matar Fall, Antonio Estache, Raymond Bourdeaux, Deo Ndikumana, Aisha Kahn, Basma Ammaari, Elizabeth White, Menno Mulder-Sebanda, Philip English, Marc Blackden, Sambagor Gueye, Hawa Diop, Quentin Wodon, and Brice Jean-Marie Quesnel, Eduard Nassim (CAMVP)Thierry Tanoh (CAFDR) Richard Ranken (CEAHK) Aida der Hovanessian (DKRIFC). Judite Fernandes provided valuable assistance. Peer reviewers are: Gaiv Tata (FRM), Brian Ngo (PRMVP), and Jan Walliser (OPCS).

vi

EXECUTIVE SUMMARY

1. By historical and regional standards Senegal has achieved good economic results over the past decade even though its performance was weaker in 2006. Not only did GDP growth average almost 5 percent per year, but poverty in households also declined by almost 15 percentage points between 1994 and 2002. Nevertheless, Senegal remains a poor country, with a GDP per capita of US$710 in 2005, and major deficiencies in its infrastructure and human development. It also failed to report major improvements in man-made outcomes such as governance, ease of doing business, and technology development, which are crucial for a country that cannot rely on significant natural resources. 2. The Government is well aware that it needs to do more and better to reach its MDGs and reduce poverty by half by 2015. The implementation of the new Poverty Reduction Strategy (PRS), as well as of the Accelerated Growth Strategy (AGS), is expected to lead to higher economic growth rates, and to greater equity through improvements in the delivery of basic social services and in the protection of the most vulnerable population groups. The Government has also announced its intent to improve governance and strengthen participatory processes and decentralization. This medium-term vision has been approved by stakeholders in Senegal and is aligned with its Millennium Development Goals (MDGs). 3. The proposed outcome-based Country Assistance Strategy (CAS) for the period FY07-10 seeks to support Senegal’s effort in achieving its ambitious development agenda. It is the result of a participatory process through which the World Bank Group (WBG) aims to (i) optimize its experience in Senegal; (ii) align its support with the Government’s PRSP priorities and the Bank’s Africa Action Plan (AAP); and (iii) find synergies with partners. The new CAS recognizes that more efforts are needed to address the challenge of weak governance in Senegal, and introduces a “governance filter” comprising four core principles to ensure that governance considerations are mainstreamed into all WBG’s programs: (i) improve transparency and efficiency in the use of public resources; (ii) increase public sector accountability; (iii) strengthen and modernize the judicial system; and (iv) enhance mechanisms for private sector governance. This focus should help Senegal to close the gap with successful emerging countries. 4. The CAS program is selective by focusing on three pillars:

a. Pillar I: accelerated growth/wealth creation. Strengthening GDP growth to an annual rate of 7 percent, which is 1-2 percent higher than the historical average, is perceived by Senegal as one of its prerequisites for reaching MDGs. WBG support will include a series of IDA and IFC instruments organized to achieve the six following outcomes: (i) promoting a competitive investment climate; (ii) building and maintaining basic infrastructure for growth; (iii) facilitating access to financial resources by small and medium enterprises; (iv) promoting a modern and diversified agricultural sector; (v) fostering sustainable development and management of natural resources; and (vi) developing skilled labor and use of technology.

vii

b. Pillar II: human development/shared growth. Increasing access to social services and creating opportunities for poor and vulnerable groups, as growth performance is improved, is at the heart of Senegal’s PRS agenda. Improved equity is crucial, not only to ensure social and political stability, but also to achieve long-term economic growth. WBG assistance will include a mix of financial and analytical support in the education and health sectors, as well as in the area of the protection of vulnerable groups.

c. Pillar III: rural and urban synergies. The rapid pace of urbanization in Senegal —six out of ten people are projected to live in cities by 2015—raises a key challenge for the authorities who will need to find the right balance between urban and rural development. To support the Government, the WBG will shape its program around three major outcomes: (i) balancing the provision of infrastructure between urban and rural areas; (ii) reducing the vulnerability of immigrants and emigrants; and (iii) improving the quality of life of the population through better management of natural resources and improved access to water and sanitation.

5. As a tangible step toward achieving these medium-term outcomes, the proposed CAS recognizes the regional dimension of Senegal’s development as well as the importance of enhancing gender development and building local capacity. Several regional operations and analytical studies are envisaged in the energy sector, the promotion of the Senegal River area, the road sector, with the development of corridors with Mauritania and The Gambia, and social sectors through regional initiatives in health and education. Success in the development of Senegal will not only depend greatly on its capacity to provide women social protection and equal access to social services, but also to secure for them more and better jobs. Last, but not least, the focus on capacity building is justified because Senegal’s progress will be shaped by the quality of its labor force and entrepreneurs as well as the effectiveness of its public administration.

6. A focused lending program is proposed, in the range of US$420 million over the four-year CAS period, which will complement ongoing operations and seek to optimize WBG assistance given government priorities and partner programs. The proposed CAS program will aim at balancing WBG lending across the above three key pillars and the governance filter. It will seek to maximize Bank assistance in Senegal through: (i) the use of various financial instruments such as budget support, single investment projects, and community driven development initiatives; (ii) leveraging financial resources beyond the country IDA allocation through partnerships and donor coordination; and (iii) enhancing regional economic externalities.

7. The CAS includes a core program of AAA which aims at supporting the Government’s vision, and focuses on three main issues: (i) labor market and productivity; (ii) protection of vulnerable groups (notably youth and street children and activities in rural areas such as in the groundnut basin); and (iii) fiscal policies, expenditure efficiency, and civil service reforms. In collaboration with IFC and WBI, other analytical studies are expected to be carried out on the development of the knowledge economy, the regional housing finance market, and a review of the fiscal regime of financial operations.

viii

8. The program is designed to mitigate risks that could limit the effectiveness of WBG support. These risks can be grouped into three main categories: (i) lack of governance and vested interests; (ii) vulnerability to political and economic external shocks; and (iii) weak capacity for implementing reforms. The measurement of results is an essential component of improving mutual accountability and mitigating risks. The WBG will primarily depend on three complementary channels to monitor CAS progress over time. The first channel is the current PRSP institutional framework for the compilation and verification of results and milestones. The second channel consists of periodic portfolio reviews, in close coordination with the authorities and other partners. The third channel is to ensure that the strategic AAA program and intermediary outcomes (or milestones) help track results over time, including a CAS progress report in early FY09.

1. INTRODUCTION

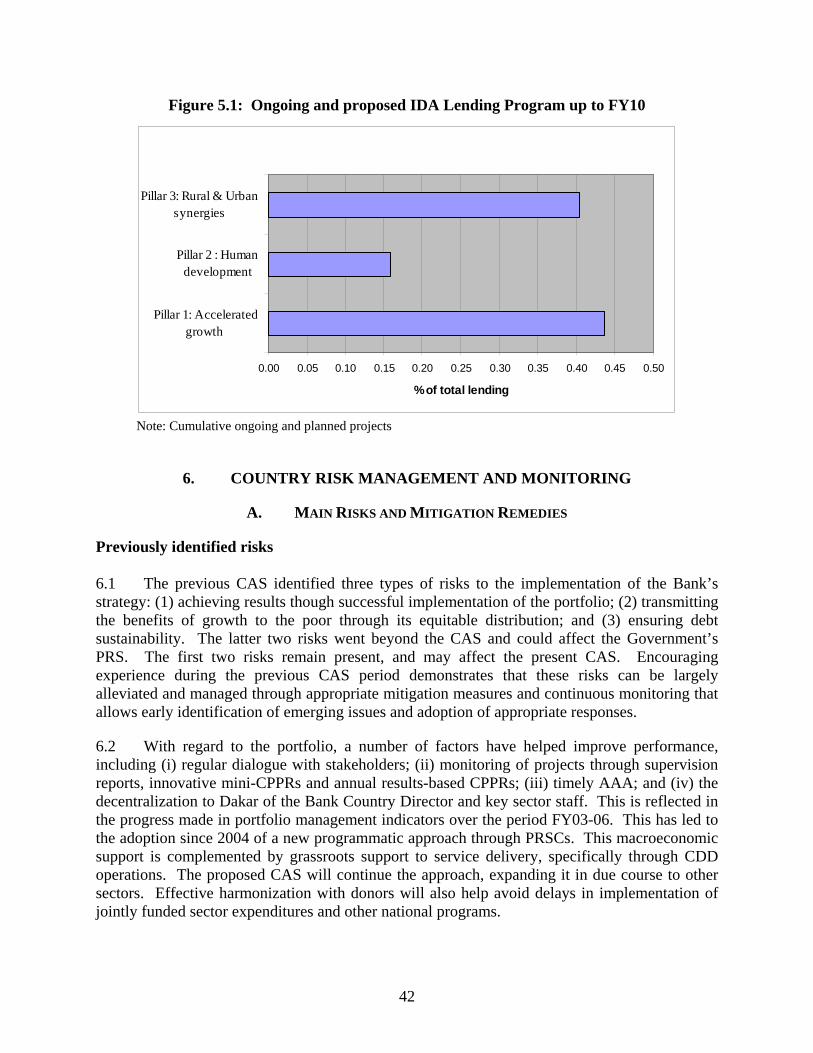

1.1 The proposed CAS activities are clustered around three pillars and one cross-sector governance filter. The three pillars are: (i) fostering economic growth through support to private sector development; (ii) improving human development through better delivery of social services, notably to the most vulnerable groups; and (iii) enhancing rural and urban synergies. Transparency will be mainstreamed in all programs and projects supported by the CAS to help improve public and private governance. The CAS will employ a selected mix of Bank and IFC financing instruments and a targeted program of WBG Analytical and Advisory Activities (AAA).

1.2 The proposed CAS is (i) based on the WBG experience since the early 1990s; (ii) oriented toward results; and (iii) aimed at supporting Senegal’s second generation Poverty Reduction Strategy (PRS) with the ultimate objective of attaining the Millennium Development Goals (MDGs). It reflects the various phases of the consultation process within the WBG and in Senegal.

2. COUNTRY CONTEXT

A. POLITICAL AND INSTITUTIONAL BACKGROUND

2.1 Senegal is located on the West Coast of Africa and is part of the West African Economic and Monetary Union (WAEMU). With a population estimated at about 10 million, its economy is dominated by a few strategic sectors, including groundnuts, fisheries, and services. The role of the agricultural sector has declined over time, from almost 15 percent of GDP in 1960 to 7 percent in 2004. The informal sector accounts for about 60 percent of GDP. Its rural economy frequently suffers from drought, and lacks access to basic services and infrastructure, leading to low productivity, high emigration and higher poverty rates in rural areas. As a result, it is estimated that almost half of the population lives in cities.1 This ratio is projected to increase up to 60 percent by 2015.

2.2 Over the past decades, Senegal has enjoyed a stable political climate, and has remained largely unaffected by regional instability. According to a recent World Bank study, every year one out of eight countries will suffer from an internal political conflict in Sub-Saharan Africa.2 By contrast, Senegal has shown a remarkable political stability since independence, which was strengthened by the successful transition to a new President in 2000 and the Casamance peace agreement at the end of 2004. This stability is viewed as the result of a relatively free and diverse media (with numerous newspapers and radios) and an active civil society (with hundreds of NGO), as well as the ability to preserve the historical social equilibrium between modern institutions and religious communities. Several indicators used by the international community such as World Bank Institute (WBI) governance indicators (Table 2.1) and the Freedom House ranking of civil liberties and political rights reflect the relatively good health of Senegalese institutions, and show that Senegal compares favorably to most 1 Including 30 percent in Dakar. 2 P. Collier et al., Breaking the Conflict Trap: Civil War and Development Policy, Washington, D.C., World Bank, New York: Oxford University Press, 2003.

2

African countries. However, the quality of its institutions still lags with respect to that prevailing in emerging and OECD countries.

2.3 The last few months have seen an increase in political activities linked to the preparation of the Presidential elections in February 2007 and the legislative elections scheduled in June 2007. Events such as shifts in the Cabinet’s composition, and disputes between the President and one of the former Prime Ministers, have led to some government spending irregularities, weaker budgetary controls by the judiciary and legislative powers, and fragile governance in public and quasi-public enterprises (see more details in para 2.6). Furthermore, the Government is now perceived as less efficient than a few years ago (the Government Effectiveness WBI indicator declined from 61.2 in 1998 to 49.8 in 2005). Helping Senegal reverse this trend will be at the center of the WBG agenda.

Table 2.1: World Bank Institute (WBI) Governance Indicators in 2004-05 Governance Indicator

Senegal

Percentile

Sub-Saharan Africa Average

Percentile

OECD Average

Percentile Voice and Accountability 53.1 32.7 91.3 Political Stability 41.4 33.4 82.5 Government Effectiveness 51.8 27.3 89.8 Regulatory Quality 41.8 28.8 91.5 Rule of Law 47.3 27.8 90.6 Control of Corruption 47.8 29.6 90.9

Source: Kaufmann D., A. Kraay, and M. Mastruzzi 2006: Governance Matters V: Governance Indicators for 1996-2005.

B. RECENT ECONOMIC DEVELOPMENTS

2.4 Today, Senegal is viewed as a good performer in Sub-Saharan Africa with its economy growing at a steady rate of about 5 percent since the devaluation in 1994. The Government has shown a capacity to generate economic growth, in spite of exogenous shocks (such as droughts and natural disasters). Inflation has remained well under control, at around 1-2 percent per year. The fiscal position has been strong, with an unprecedented low indebtedness and growing tax revenues. Similarly, the current account deficit has been over-financed by official and private capital inflows, resulting in substantial foreign exchange reserves equivalent to over 3 months of imports at end-2006. The monetary and exchange rate policies have been kept in line with regional agreements.

2.5 Senegal has received significant capital inflows over the past decade. It has continued to be one of the most assisted countries in the world (the level of official aid per capita exceeded US$100 in 2004). Furthermore, the growing number of Senegalese living in industrial countries (and the increasing facilities to send money across international borders) has generated a steady increase in remittances, estimated at around US$500 million in 2004,3 which have helped to

3 This figure does not include non-official transfers.

3

promote economic growth and social protection in Senegal.4 Overall, these two sources of foreign capital are now estimated to be equivalent to about 25 percent of GDP.

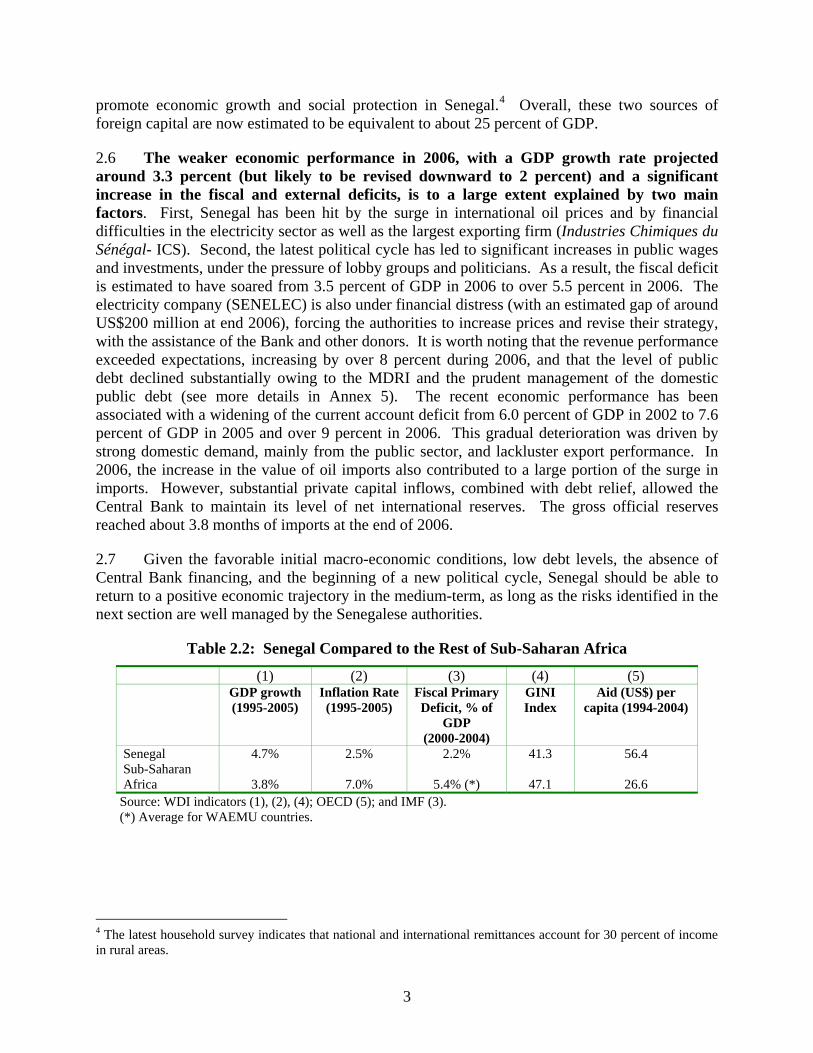

2.6 The weaker economic performance in 2006, with a GDP growth rate projected around 3.3 percent (but likely to be revised downward to 2 percent) and a significant increase in the fiscal and external deficits, is to a large extent explained by two main factors. First, Senegal has been hit by the surge in international oil prices and by financial difficulties in the electricity sector as well as the largest exporting firm (Industries Chimiques du Sénégal- ICS). Second, the latest political cycle has led to significant increases in public wages and investments, under the pressure of lobby groups and politicians. As a result, the fiscal deficit is estimated to have soared from 3.5 percent of GDP in 2006 to over 5.5 percent in 2006. The electricity company (SENELEC) is also under financial distress (with an estimated gap of around US$200 million at end 2006), forcing the authorities to increase prices and revise their strategy, with the assistance of the Bank and other donors. It is worth noting that the revenue performance exceeded expectations, increasing by over 8 percent during 2006, and that the level of public debt declined substantially owing to the MDRI and the prudent management of the domestic public debt (see more details in Annex 5). The recent economic performance has been associated with a widening of the current account deficit from 6.0 percent of GDP in 2002 to 7.6 percent of GDP in 2005 and over 9 percent in 2006. This gradual deterioration was driven by strong domestic demand, mainly from the public sector, and lackluster export performance. In 2006, the increase in the value of oil imports also contributed to a large portion of the surge in imports. However, substantial private capital inflows, combined with debt relief, allowed the Central Bank to maintain its level of net international reserves. The gross official reserves reached about 3.8 months of imports at the end of 2006.

2.7 Given the favorable initial macro-economic conditions, low debt levels, the absence of Central Bank financing, and the beginning of a new political cycle, Senegal should be able to return to a positive economic trajectory in the medium-term, as long as the risks identified in the next section are well managed by the Senegalese authorities.

Table 2.2: Senegal Compared to the Rest of Sub-Saharan Africa

(1) (2) (3) (4) (5) GDP growth

(1995-2005) Inflation Rate (1995-2005)

Fiscal Primary Deficit, % of

GDP (2000-2004)

GINI Index

Aid (US$) per capita (1994-2004)

Senegal 4.7% 2.5% 2.2% 41.3 56.4 Sub-Saharan Africa

3.8%

7.0%

5.4% (*)

47.1

26.6

Source: WDI indicators (1), (2), (4); OECD (5); and IMF (3). (*) Average for WAEMU countries.

4 The latest household survey indicates that national and international remittances account for 30 percent of income in rural areas.

4

C. MEDIUM-TERM OUTLOOK AND SUSTAINABILITY

2.8 The medium-term scenario is based on real GDP annual growth of about 5 percent and continued low inflation during 2007-11 (see Annex 9). This growth rate is at about the same level as the average growth rate since the devaluation of the CFAF in 1994, and consistent with the low base scenario presented by the authorities in the second Poverty Reduction Strategy Paper (PRSP-II). Its attainment would require the continuous implementation of sound macroeconomic policies, market-oriented structural reforms, and an efficient Government investment program. Private savings should increase moderately, facilitated by rising real per capita income and financial sector development. Reflecting these trends, the external current account deficit (including official transfers) would decline marginally from the projected 12 percent of GDP in 2006, to around 7.5 percent of GDP by 2010.

2.9 The medium-term outlook is subject to a number of downside risks, but could also be upgraded under specific conditions. On the one hand, Senegal’s economy remains vulnerable to exogenous shocks, including higher oil prices, severe droughts, locust invasion, and severe political strife in the WAEMU region. It will also be highly dependent on the ability of the authorities to address the current crisis in the energy sector and chemical industry (which still needs to be properly evaluated). The relative fragility of the current account deficit also emphasizes the need to promote private sector development, especially export-oriented activities, which is at the center of the new Accelerated Growth Strategy (AGS).5 On the other hand, the rapid implementation of the AGS may accelerate economic growth to the range of 7-8 percent assuming it creates better conditions for the development of private sector activities and thus stimulates higher private investment and exports. New private activities could also arise from opportunities in potential sectors such as tourism, Information and Communication Technology (ICT), and agriculture.

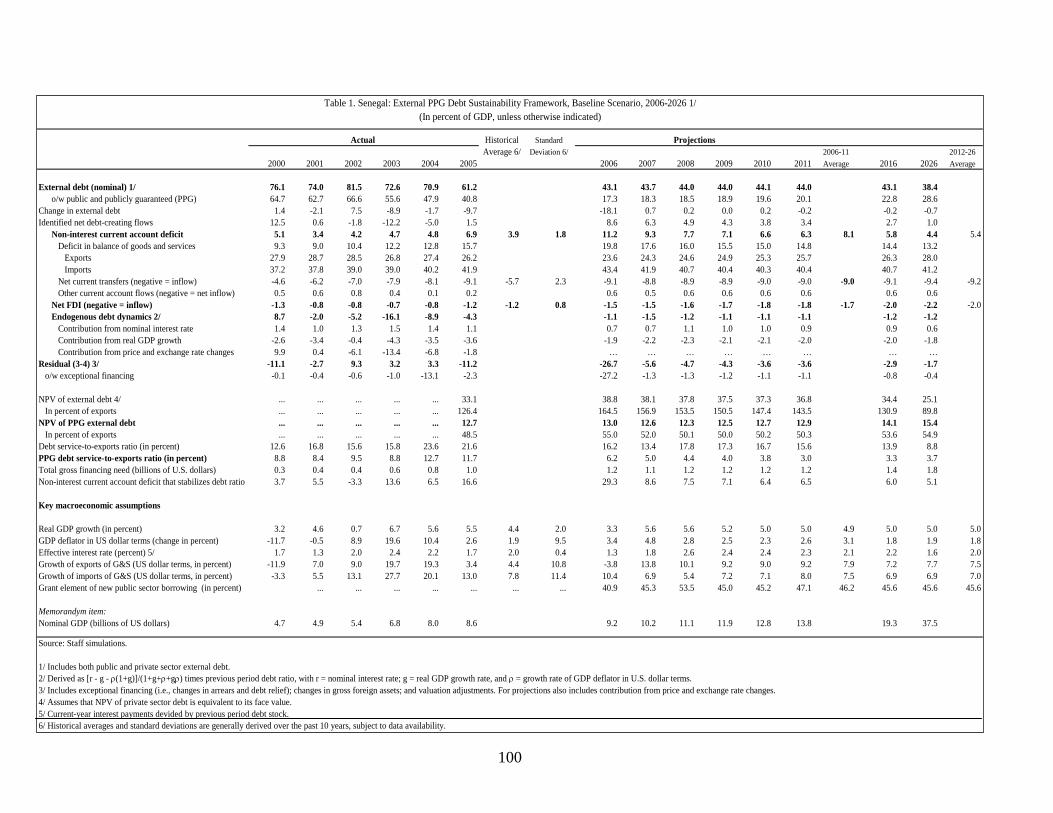

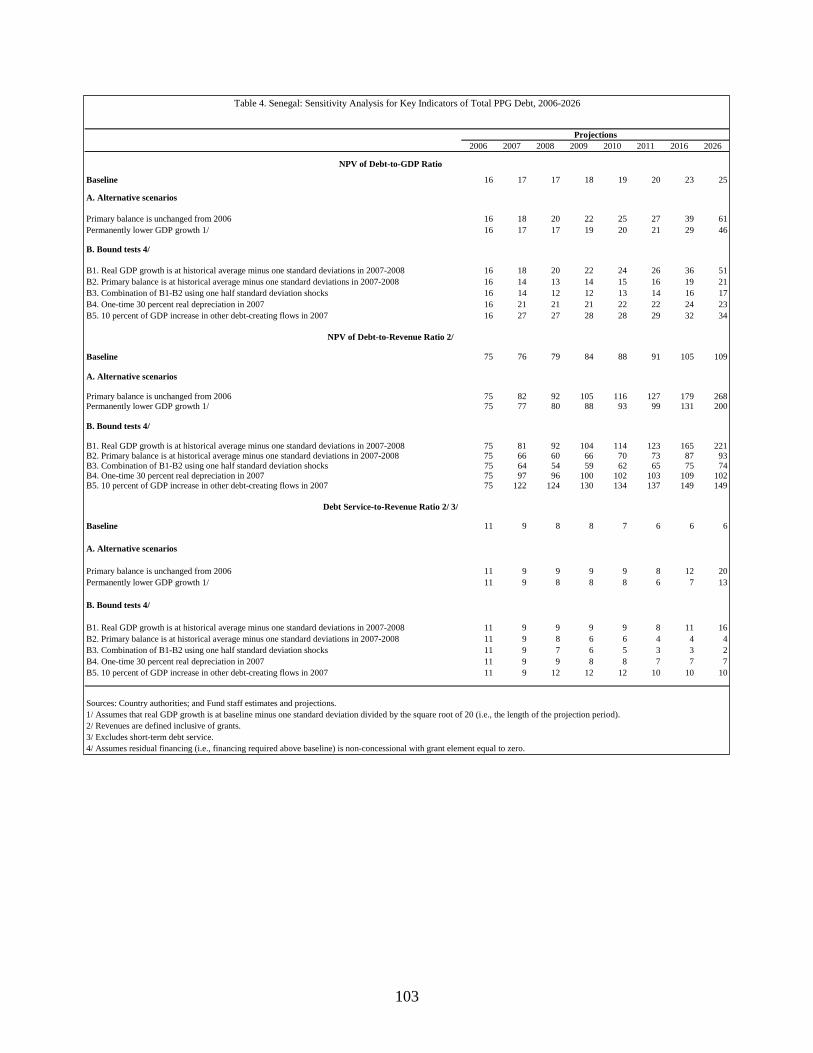

2.10 The second positive feature of the medium-term outlook is that Senegal has exited the recent enhanced HIPC Initiative and MDRI with a good basis for maintaining sustainable external debt levels over the medium term, especially if borrowing remains at concessional terms and the level of the fiscal deficit remains below 4 percent of GDP (see Annex 5 for details). The recent Debt-Sustainability Analysis (DSA) conducted jointly by the IMF and Bank staffs has shown that the level of public external debt was as low as 13 percent of GDP at the end of 2006. Public domestic debt is estimated at about 3 percent of GDP, of which two-thirds is long term. The DSA highlights the need for Senegal to continue to adopt strict fiscal discipline, a prudent strategy regarding borrowing.

D. POVERTY PROFILE AND UNEQUAL PROGRESS TOWARD MDGS

2.11 Senegal remains a poor country, with a GNI per capita of US$710 in 2005.6 The latest household survey indicates that the proportion of the population living in poverty decreased from 67.9 percent in 1994 (61.4 percent of households) to 57.1 percent in 2001 (48.5 percent of households), which represents a significant achievement by both historical and 5 A clear indication of the concentration of Senegal’s exports is that in 2002, the top five exports at the 8-digit Harmonized System level represented over 40 percent of total exports (petroleum, crude vegetable oil, phosphoric acid, lobster and shrimps). 6 World Bank’s Atlas methodology.

5

regional standards.7 This positive evolution needs to be qualified on three accounts: (i) the absolute number of poor households has nonetheless increased; (ii) poverty remains concentrated in rural areas as shown by the fact that the decrease was larger in Dakar and other urban centers than in rural areas; and (iii) perceptions of poverty show that two-thirds of households identify themselves as poor and one-third of poor and non-poor alike feel poverty has substantially increased in their community over the last five years.

2.12 The probability of being poor in Senegal is highly correlated with access to basic infrastructure services. The regions with the highest levels of poverty (Ziguinchor, Kolda, Kaoloack, and Diourbel) are those with the lowest access to water and sanitation and electricity. For the rural population, and for the poor in both the urban and rural areas, access gaps are large and reinforce their vulnerability. 8

2.13 Unequal human development is both the cause and the result of poverty. The average life expectancy does not exceed 56 years in Senegal, as both infant and maternal mortality rates are high (even in comparison to developing countries). The level of education is improving, notably in primary education, but secondary and tertiary education suffer from numerous problems, leading to low rates of return and high dropout rates.

2.14 Poverty in Senegal is also linked to the difficulty in finding jobs. Today, four out of ten potential workers are unemployed or underemployed in Senegal, and this proportion is even higher for young people who lack skills and experience. Part of the problem is rooted in the lack of dynamism of the private sector and the declining share of the agricultural sector in the economy (most notably the groundnut sector). Indeed, since 2000, private investment has declined in proportion of GDP and the number of new enterprises remains limited, at least in the formal sector, due to various obstacles such as the difficult access to electricity at a reasonable cost, the lack of transparency in the business environment, and the poor functioning of the judiciary system (as reflected by Senegal’s poor ranking in Doing Business).

2.15 Another determinant of poverty is the vulnerability of the rural population to external shocks (such as climatic conditions), which affects their income negatively. Such vulnerability has led to higher emigration rates toward cities, in particular Dakar, contributing in turn to the deterioration of living conditions in urban areas and to the emergence of new vulnerable groups (e.g., street children, see Box 2.1). These trends have created increasing concerns regarding food and water security, notably in booming urban areas, and sustainable economic growth in all regions. This situation has fueled higher illegal emigration flows toward industrial countries.

7 Fuller details on the results described in this section can be found in: La Pauvreté au Sénégal: de la dévaluation de 1994 à 2001-2002, Ministry of Economy and Finance and World Bank, January 2004 or PRSP Progress Report, Report N. 28813-SEN, April 28, 2004. 8 For more details, see Senegal, Poverty Assessment, 2003.

6

Box 2.1: Street Children in Senegal

2.16 Progress toward MDGs has been unequal due to the mixed performance of Senegal in addressing the main factors behind poverty and inequalities. As summarized in Table 2.3, Senegal is likely to reach its goals in terms of universal primary education and its combat against HIV/AIDS at the current pace of progress. Senegal is also well on track to achieve its MDGs in the urban water sub-sector, even though challenges remain in rural areas where about 3 million people still need access to water and sanitation services. Furthermore, recent actions in terms of nutrition and immunization programs (Diphtheria Tetanus Whooping-cough 3 (DTC3) coverage reached almost 80 percent in 2005) provide some encouraging signs of progress. The number of people utilizing HIV/AIDS voluntary counseling and treatment also increased significantly, from 9,900 in 2002 to 94,000 in 2006. However, major concerns remain with respect to the long-term objectives of eradicating extreme poverty, fighting malaria, and reducing infant and maternal mortality by 2015. Senegal is off- track on these goals.

Most observers agree that the number of street children increased significantly over the past two decades, but no data is available. Preliminary estimates of a 2006 census of street children in the metropolitan Dakar area put their number at over 10,000, and at least as many are likely to be found in other urban centers throughout the country and particularly in the southern regions (e.g., Kolda, Kaolak). These children are among the most vulnerable as they generally lack a caring and enabling environment providing the psycho-social support they need. Living in abject poverty, they are often malnourished, don’t go to school, are victims of violence and have no access to health care. Barefoot, in rags and tatters, they are now part of the urban landscape.

The vast majority of street children, mostly boys of 3-14 years, come from rural areas, and over a third come from other countries (Guinea Bissau especially). They include children entrusted to Koranic teachers by their parents (talibés) who are forced to beg for a living, children whose families live in the street, and children who have broken up with their families (e.g., runaways, victims of family violence, abandoned children). The talibés are by far the most numerous and visible group, easily recognized by the tomato cans they carry to collect alms. A 2006 survey suggests they actually spend very little time learning the Koran, and there are numerous cases of child trafficking disguised as Koranic schooling.

7

Table 2.3: Senegal’s Uneven Path Toward its MDGs

1990

2000

2003

2004/5 Goals 2015

Projected 2015

Goal 1: Eradicate extreme poverty and hunger Population below Poverty Line (%) 58 55.8 54 35 45 Prevalence of underweight children (under three years of age)

21 17.3

10 14

Goal 2: Achieve universal primary education Net primary enrollment ratio (% of relevant age group) 47.1 68.3 75.8 79.9 100 100 Primary completion rate, total (% of relevant age group) 42 46 44 48.3 100 53.4 Goal 3: Promote gender equality and empower women Ratio of girls to boys in primary and secondary education (%)

68.5 83.9 87.1 100 96.7

Goal 4: Reduce child mortality Immunization, DTC3 (% of children ages 12-23 months) 51 41 70 93 85 85 Infant mortality rate (per 1,000 live births) 90 80 78 61 30 45 Under age 5 mortality rate (per 1,000) 148 139 137 121 49 102 Goal 5: Improve maternal health Births attended by skilled health staff (% of total) 38 52 75 75 Maternal mortality ratio (modeled estimate, per 100,000 live births)

510 434 127.5 380

Goal 6: Combat HIV/AIDS, malaria, and other diseases Malaria Prevalence rate 40.7 Prevalence of HIV, total (% of population aged 15-49) 1 1.5 1.7 3 3 Goal 7: Ensure environmental sustainability Access to an improved water source (% of urban population)

66 78 90 95 95

Access to an improved water source (% of rural population)

65 82

Access to improved sanitation (% of urban population) 35 56 60 78 69 Access to improved sanitation (% of rural population) 19.1 59 Source: Government and World Bank

3. SENEGAL’S MAIN DEVELOPMENT CHALLENGES

3.1 Senegal has yet to fully live up to its development potential. At the current economic growth rate of 5 percent, it would take Senegal more than 12 years to reach a per capita income of US$1,000 (the level recorded today by countries such as the Philippines or Paraguay) or nearly 25 years to move ahead of Tunisia and Brazil (assuming that these countries were to remain at their present levels). Senegal’s development is hindered by serious deficiencies in terms of both human and infrastructure development. For example, electricity consumption per capita remains significantly lower in Senegal than the average in Sub-Saharan Africa. The road network is underdeveloped and of poor quality. Senegal was ranked at the 156th position by the United Nation Overall Human Development Index in 2006.

8

3.2 The international experience has revealed that one pre-requisite for success in a country such as Senegal, with limited natural resources, is to perform better than others through a combination of man-made achievements in four main areas: (i) transparency and governance; (ii) Government efficacy; (iii) ease in doing business; and (iv) capacity to adapt and adopt new technologies through innovation and human development.9 Senegal has not yet reported significant improvements in these four areas (see Table 3.1). Today it is ranked at approximately the same level as Ghana and Vietnam but lower than successful emerging countries in the world (Ireland, Singapore, and Estonia) and in Africa (Mauritius, Tunisia).

Table 3.1: Senegal Lags Behind Emerging Countries in Man-Made Areas for Economic Development (Country Ranking)

(1) (2) (3) (4) Countries

Transparency

Government Effectiveness

Ease of Doing Business

Technology Development

Singapore 5 1 1 17 Ireland 19 18 10 20 Estonia 27 39 17 15 Mauritius 51 62 32 69 Tunisia 43 66 80 72 Vietnam 107 117 104 92 Ghana 65 101 94 104 Senegal 78 97 146 103

Source: Transparency International (1), WBI (2) and (4), Doing Business (3) 3.3 The recent economic performance provides Senegal with the opportunity to break with its history of relatively mixed results in terms of growth, equity and poverty alleviation. Seizing this opportunity will require determined actions in two key areas: (i) improving public service delivery; and (ii) promoting private sector participation.

A. IMPROVING PUBLIC SERVICE DELIVERY

3.4 Senegal enjoys a historical opportunity to increase the role of its fiscal policy owing to the sound public management of the Central Government’s financial equilibriums in recent years, strengthened by the recent external debt relief.10 It would nonetheless be incorrect to believe that an expansive fiscal policy will necessarily trigger accelerated growth in Senegal. Experience over the past two decades shows that public spending and economic growth are not necessarily correlated or, at least, not as much as private investment because of persistent weaknesses in terms of allocative and operational efficiencies of public spending.11 If budgets

9 These four dimensions reflect the current literature on economic growth. The emphasis nowadays is given to the role of the quality of institutions (as reflected by Government effectiveness and transparency). This approach complements the more traditional view that has stressed the role of technology, human capital, and private investment (which are captured by technology and the business environment indicators). 10 Such an increase should stay within reasonable limits in order to avoid exaggerated pressures on the current account balance, which could deteriorate in the event of an overly ambitious fiscal policy. For details, see Public Expenditure Review, June 2005. 11 Allocative efficiency refers to the consonance of budgetary allocations with the strategic priorities of the country. Operational efficiency, on the other hand, refers to the provision of public services at a reasonable quality and cost.

9

are misallocated and/or misappropriated, the services that people need (and presumably desire) may not get adequate levels of funding. And, if funds are misappropriated, both the quality and quantity of services that are offered will suffer.

Improving the allocative efficiency of public spending

3.5 The Government has increasingly recognized that the lack of allocative efficiency of its spending is one of the main constraints to achieving its poverty reduction objectives. A recently completed Bank study on the effectiveness of public investment, prepared in close collaboration with the authorities, presents a selected set of areas for reforms.12

3.6 The first area is to consolidate public spending on infrastructure so as to close the infrastructure gap. Senegal lags in terms of the development and quality of its road and electricity networks, which are lower than the average in sub-Saharan Africa. The inadequate supply of infrastructure services has also contributed to the low productivity of the private sector, notably by raising transport and energy costs. World Bank estimates indicate that by modernizing the road network and electricity grid to the levels achieved by Botswana, Senegal could increase its annual growth rate by almost 3 percentage points.13

3.7 In response, the authorities have allocated an increasing share of expenditure to infrastructure, accounting for 40 percent of total investment in 2004 and 2005 versus 25 percent in 2000-03. Building new infrastructure has also become the centerpiece of the President’s vision, with the planned construction of a new airport and an industrial platform located about 30 kilometers from Dakar, which will help to decentralize activities away from the Dakar area. The adequate provision of infrastructure in rural areas will also help promote agricultural activities and reduce poverty, which is highly correlated with access to water and energy services.14

3.8 Fundamental issues remain to be addressed to meet the investment challenge in the infrastructure sector. Not only an increasing share of public resources needs to be allocated to providing and maintaining these services but it will also be necessary to attract private funds to preserve the fiscal space. Such an orientation has already been initiated in the energy and road sectors, but with mixed results over the past few years. The recent adoption of the BOT Law and the creation of the Infrastructure Council have provided the basic elements for boosting private sector participation in infrastructure projects in Senegal. Lastly, the authorities will have to improve their capacity to plan recurrent costs over time as well as to assess the expected impact of large infrastructure projects on the environment and land management.

3.9 Second, the Government will have to upgrade the intra-sectoral allocation of resources within the education and health sectors. The share of education and health expenditure in total public expenditures has increased significantly over the past few years, up by 0.9 and 0.5 percentage points of GDP respectively between 2000 and 2004. This effort has

12 For fuller details, see Senegal’s Public Expenditure Review, 2004 and Public Expenditure Review Update, op. cit. June 2005. 13 For more details, see Public Expenditure Review, 2005 and “Recent Development in Infrastructure”, the World Bank Group, Private Sector Unit, 2005. 14 Senegal: Moving out of Poverty, 2006 and “Water reforms in Senegal: A regional and Interpersonal Distributional Impact Analysis”, 2006.

10

begun to produce positive results as illustrated by the recent increases in primary gross enrollment (up from 67 percent in 2002 to 77 percent in 2004) and in immunization coverage (DTC3 rate up from 54 percent in 2002 to over 80 percent in 2005). Yet, this effort must be enhanced to help these sectors meet their MDGs. In the health sector, the Plan National de Développement Sanitaire, revised in late 2004, provides the roadmap for the next few years. The Government will continue to improve access and utilization of basic health services through the strengthening of outreach activities, the implementation of its infrastructure development plan, and the implementation of the regulatory and legal frameworks for private health service provision and funding. The Government will also need to reinforce priority actions in the areas of preventing infectious diseases and utilizing reproductive health services.

3.10 In the education sector, there have been important gains in achieving higher enrollment rates and gender parity in primary schools, including a higher registration rate for girls than for boys as first graders in 2005, with 91.5 percent admission into grade one (girls represented 51 percent of those admitted). The ratio of girls to boys has consistently improved, reaching 97.2 percent and 86.6 percent in primary and secondary education respectively in 2005. To consolidate this progress in terms of access to education, the Government must improve the quality of primary education. There is also a need to improve quality and performance of secondary education as well as to reduce inefficient expenditure policies (e.g., generalized scholarships to all university students). The authorities have started to give more attention to vocational training by developing new partnerships with the private sector. 3.11 The third area is to increase and harmonize budgetary support to vulnerable groups. In a country where about half of the population live in poverty and are de facto excluded from formal social protection systems, social inclusion is at the center of the development agenda. However, vulnerable groups have only received marginal attention from the Government, as recognized by the authorities in their last two PRSP Progress Reports. The recent review realized by the Bank has revealed that the existing lack of coordination across programs reduces their effectiveness, most notably in rural areas.15 As a result, the Government has developed a new Social Protection Strategy that was adopted at the end of 2005. It stresses three main objectives: (i) strengthening and extending existing social security systems; (ii) improving the prevention and management of major risks and catastrophes; and (iii) increasing social protection of the most vulnerable groups. The document also calls for better targeting of vulnerable groups and understanding the factors behind their vulnerability and exclusion. At this stage, the Government seeks to mobilize further internal and external funding so as to make significant progress toward protecting the most vulnerable groups in the country.

3.12 The last area emphasizes the need to improve the allocative efficiency of public spending not only across sectors but also across regions. Inequalities in the delivery of social goods and infrastructure are rooted in the unequal allocation of human and financial resources by regions. For example, a large proportion of teachers and health workers are located in the Dakar areas, at the expense of remote areas where needs are pressing. The Senegalese Government has initiated the decentralization of decision-making regarding the management of human and financial resources, including the strengthening of local Governments’ capacities and the gradual transfer of a number of responsibilities to local communities, especially in the education and 15 For more details, see “Rural Protection Strategy”, July 2005.

11

health sectors. Decentralized execution of the investment budget was initiated in the 2006 Budget Law for the health and education sectors. Nevertheless, Senegal remains a very centralized country with limited tax revenues for local Governments and financial transfers (FECL and FDD) equivalent to less than 1.5 percent of the central Government budget in 2005. Clearly, the decentralization process needs to be accelerated over the next few years.

Upgrading the operational efficiency of public spending

3.13 The lack of operational efficiency of public spending appears rooted in cumbersome and complex administrative and financial procedures. As a result, in June 2003, the Senegalese authorities approved two action plans supporting public expenditure management reforms (following recommendations of the Country Financial Accountability Assessment—CFAA and the Country Procurement Assessment Review—CPAR) and initiated their implementation with the support of donors, including the Bank and the IMF. Senegal has made significant progress in the areas of budget preparation and execution, notably in the priority sectors defined in the PRSP. However, significant upgrading is still needed in the areas of internal and external controls and of budget execution in agencies and state-owned enterprises. Similarly, efforts must be made to increase transparency in procurement of public contracts by upgrading the legal and institutional framework. Those weaknesses were most apparent in mid-2004, when a series of irregularities in infrastructure spending in a secondary city came to light, and seem to have been exacerbated by mismanagement and lack of transparency in parastatals in recent months, leading to the accumulation of debt. Such improvements will have to include local Governments (in view of the expected increasing decentralization) and public enterprises.

3.14 As part of their objective to improve the quality of public human resource management, the authorities have initiated civil service reform. They have recruited almost 15,000 new civil servants (as agreed upon with the IMF and the Bank), with an emphasis on the main sectors of the PRSP, including education, health, justice, tax collection, and security. Concurrently, the Government has initiated the implementation of a series of reforms in its remuneration policy aiming at (i) improving the competitiveness of public wages with respect to the private sector; (ii) simplifying procedures; and (iii) introducing performance-based incentives. The recent audit of the wage bill has revealed that the implementation of a new payment system is required to modernize the management of human resources in public administration. The Government will have to continue to experiment with new pilot projects, such as the one recently tested in 25 health facilities, to introduce performance-based incentives in key sectors such as health and education. The Government will need to strengthen its civil service by giving more attention to the development of adequate training programs, including training in partnership with the private sector. An effective fiscal policy requires an increase in labor productivity of the public sector over time.

12

Box 3.1: Main Achievements in Public Financial Management and Remaining Issues

The Bank’s fiduciary risk assessment rated public financial management as “moderate” in Senegal, in line with the result from the Government’s comprehensive evaluation of the CFAA and CPAR action plans carried out in June 2006. Overall, progress was judged encouraging, with 70 percent and 44 percent of the CFAA and CPAR actions respectively completed by end 2005. Major achievements were realized in terms of preparation and execution of the budget, notably through the use of programmatic budgets in key ministries and the gradual decentralization of budget execution from the Ministry of Economy and Finance to line ministries. The implementation of the software system SIGFIP was also perceived as a major step forward. On procurement, the first ever audit was published at end 2005 and key Ministries have started to develop annual plans to help streamline procedures and avoid concentration of contracts in the last quarter of the calendar year. With regard to controls, it was noted that the Treasury had been able to transfer all state accounts accumulated from 1997 to the Cour des comptes, eliminating the backlog accumulated over the years. In turn, the Cour des comptes has evaluated the state accounts for 1997, 1998 and 1999 and is on the pace to review remaining accounts during the next 18 months. The evaluation report recommended that the authorities should focus their efforts in the following areas: (i) improve wage and human resources management; (ii) harmonize procedures between projects funded on internal and external resources; (iii) accelerate the use of programmatic budgets in line Ministries; (iv) improve the preparation and execution of the investment budget; and (v) strengthen internal and external controls of agencies, public enterprises, and local governments. The authorities, and partners, were also encouraged to launch the Public Expenditure Financial Assessment (PEFA), as it should provide useful benchmarks for measuring progress in Senegal over time and compared to other countries. Such an exercise is expected to be completed by October 2007.

3.15 The Senegalese authorities need to be made more accountable for the use of public funds by strengthening checks and balances and by disseminating relevant information to media and interested parties. The Government needs to ensure that allocated resources reach their intended final beneficiaries. A recent tracking survey has reported that only 58 percent of teachers could be identified on active duty, raising doubts about the efficacy of the system to educate children. Similarly, leakages and inefficiencies are numerous in the health sector.16 Efforts to strengthen checks and balances are under way through the implementation of the CFAA/CPAR actions described earlier. The Treasury has finalized the consolidated state’s accounts and recently forwarded them to the General Accounting Court (clearing the significant backlog). The Court has reviewed these accounts for 1997-99 and a timetable was set up to send its avis de conformité to the National Assembly for the remaining years. The Court has relatively limited resources and a Multidonor Trust Fund is funding short term accountants to assist in accelerating the review. There is a need to strengthen the controls of independent agencies and public enterprises as emphasized in the recent Public Expenditure Review Update and the ROSC on corporate governance produced by IFC in early FY2007. The Government has also established a number of new institutions aimed at improving governance in both the public and private sector (e.g., Commission contre la Corruption, Infrastructure Council) but efforts are needed to make them more effective. Finally, the authorities have taken the initiative to strengthen information systems and further empower final beneficiaries, notably through the development of Community Driven Development (CDD) initiatives supported by the Bank.

16 For details, see “Senegal, Policies and Strategies for Accelerated Growth and Poverty Reduction”, A Country Economic Memorandum, April 3, 2003.

13

B. ENHANCING PRIVATE SECTOR DEVELOPMENT

3.16 The performance of the private sector has been uneven in Senegal as evidenced by the decrease in private investment from 17 percent of GDP in 2000 to 15 percent in 2004 and the relative stagnation of exports, around 27 percent of GDP. This lack of dynamism is also reflected at the micro level since labor productivity of manufacturing in Senegal, while high compared to neighboring countries, is estimated to have declined over the past two decades, and is today equivalent to one fifth or one third of those achieved in Korea and South Africa, respectively.17 Job creation has been minimal with the unemployment and under-employment rates stagnating at around 40 percent of the labor force. Such a performance needs to be turned around so that the private sector can play its expected pivotal role in the PRS agenda.

3.17 Policymakers face major challenges to improve Senegal’s investment climate and promote sector development. Streamlining bureaucracy and improving transparency are key challenges as illustrated by Senegal’s poor ranking in Doing Business Indicators and the Bank’s recent ROSC on accounting practices by the private sector.18 While some specific initiatives have been launched, a more concerted, broad based strategy is required. The Senegalese Government finalized its new Accelerated Growth Strategy in January 2007, which is part of the second-generation PRSP (see next section for details). This new approach is expected to help address further cross-sector issues related to the investment climate and promote five specific clusters that are perceived by the Government to have the highest comparative advantage for Senegal: (i) agribusiness; (ii) tourism; (iii) telecommunications and new technologies; (iv) textiles; and (v) fisheries.

3.18 Many surveys, diagnoses and studies, including those emanating from the Bank Group, have already helped to reach a consensus regarding the major constraints faced by the private sector in Senegal (Box 3.2).19 Building on recommendations from the Presidential Investors’ Councils, the authorities have improved the business environment by streamlining regulations concerning business registration and taxation. In January 2004, the National Assembly adopted reforms simplifying the corporate income tax and investment codes. The tax basis was broadened by eliminating several tax exemptions, and a single tax replacing the income tax, the value-added tax, patent contributions, and social security charges was introduced for small enterprises. The new investment code broadened the scope of eligible sectors to take into account PRSP priorities and it streamlined the system of investment incentives.

17 See “Senegal: Investment Climate Assessment”, World Bank, 2004. 18 World Bank, ROSC on auditing and accounting practices, 2005. 19 A non-exhaustive list of studies from the WBG on the business environment in Senegal includes: “Senegal, Investment Climate Assessment” (2004), FIAS studies on taxation and administrative barriers (1999, 2001, and 2003), MIGA’s studies on benchmarking (2005).

14

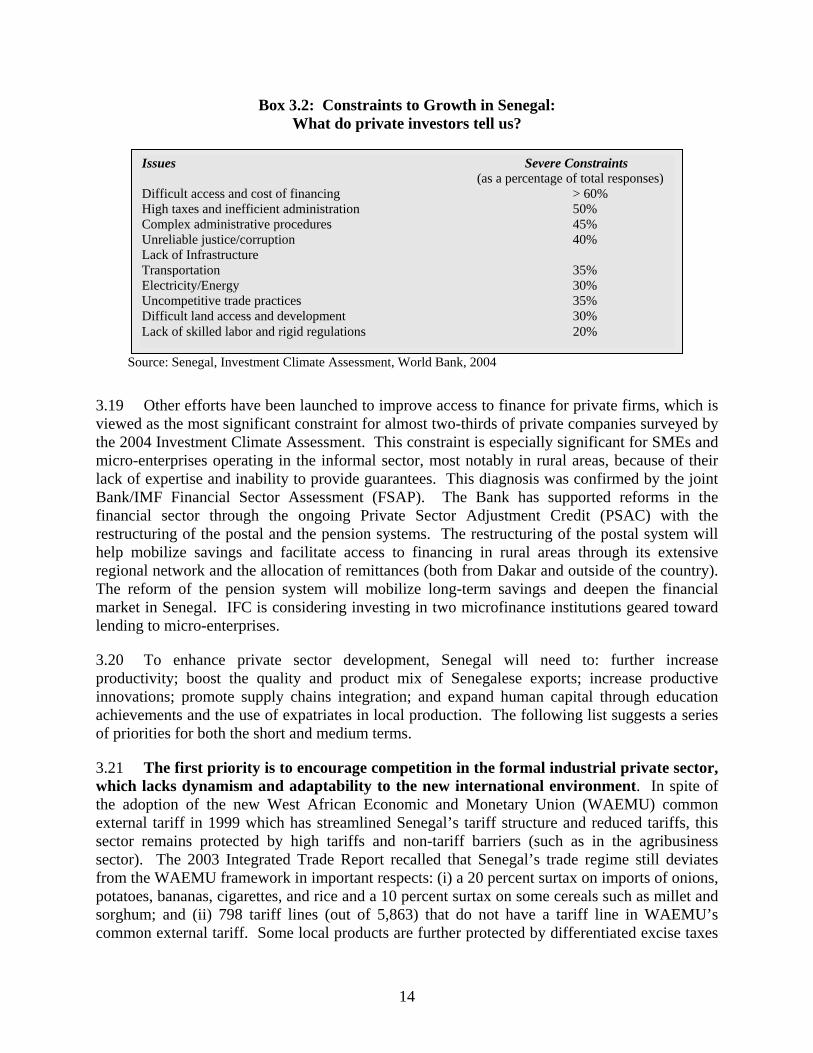

Issues Severe Constraints (as a percentage of total responses) Difficult access and cost of financing > 60% High taxes and inefficient administration 50% Complex administrative procedures 45% Unreliable justice/corruption 40% Lack of Infrastructure Transportation 35% Electricity/Energy 30% Uncompetitive trade practices 35% Difficult land access and development 30% Lack of skilled labor and rigid regulations 20%

Box 3.2: Constraints to Growth in Senegal: What do private investors tell us?

Source: Senegal, Investment Climate Assessment, World Bank, 2004

3.19 Other efforts have been launched to improve access to finance for private firms, which is viewed as the most significant constraint for almost two-thirds of private companies surveyed by the 2004 Investment Climate Assessment. This constraint is especially significant for SMEs and micro-enterprises operating in the informal sector, most notably in rural areas, because of their lack of expertise and inability to provide guarantees. This diagnosis was confirmed by the joint Bank/IMF Financial Sector Assessment (FSAP). The Bank has supported reforms in the financial sector through the ongoing Private Sector Adjustment Credit (PSAC) with the restructuring of the postal and the pension systems. The restructuring of the postal system will help mobilize savings and facilitate access to financing in rural areas through its extensive regional network and the allocation of remittances (both from Dakar and outside of the country). The reform of the pension system will mobilize long-term savings and deepen the financial market in Senegal. IFC is considering investing in two microfinance institutions geared toward lending to micro-enterprises.

3.20 To enhance private sector development, Senegal will need to: further increase productivity; boost the quality and product mix of Senegalese exports; increase productive innovations; promote supply chains integration; and expand human capital through education achievements and the use of expatriates in local production. The following list suggests a series of priorities for both the short and medium terms.

3.21 The first priority is to encourage competition in the formal industrial private sector, which lacks dynamism and adaptability to the new international environment. In spite of the adoption of the new West African Economic and Monetary Union (WAEMU) common external tariff in 1999 which has streamlined Senegal’s tariff structure and reduced tariffs, this sector remains protected by high tariffs and non-tariff barriers (such as in the agribusiness sector). The 2003 Integrated Trade Report recalled that Senegal’s trade regime still deviates from the WAEMU framework in important respects: (i) a 20 percent surtax on imports of onions, potatoes, bananas, cigarettes, and rice and a 10 percent surtax on some cereals such as millet and sorghum; and (ii) 798 tariff lines (out of 5,863) that do not have a tariff line in WAEMU’s common external tariff. Some local products are further protected by differentiated excise taxes

15

on imported and local products such as edible oils and cigarettes.20 In some sectors, collusive behaviors by a few dominant firms have produced significant costs for local consumers, raising prices above their international levels (for example, sugar, transportation, and groundnuts).21 Such behavior and weak governance have also led to financial mismanagement in key sectors (ICS mining and SENELEC electricity). At this stage, the Government will push for the elimination of the remaining specific taxes and non-tariff barriers in the sectors mentioned above and for improved governance in public and private enterprises.

3.22 To foster competition, the Senegalese Government has promoted the participation of new private operators, notably in the infrastructure sector. After two failed privatization attempts in 1995 and 1999, in March 2005 the authorities sold the groundnut processing and vegetable oil refining company (SONACOS) to the only bidder that made an offer. In the electricity sector, the Government concluded the process of selecting an independent private producer (IPP) to increase generation capacity by 67.5 Megawatts (MW) (equivalent to about 14.6 percent). In the future, the Government will promote higher private sector participation in infrastructure sectors (transports and energy). A necessary condition will be to improve the accounting and audit systems for public (and quasi public) enterprises and regulated private operators when there are residual monopoly powers. An effort will also be pursued to upgrade accounting and reporting practices in the private sector, along the lines suggested in the recent ROSC produced by the Bank.

3.23 The second priority is to support micro and small and medium enterprises, which account for more than half of the Senegalese economy. Perhaps the greatest challenge facing Senegal, as the country attempts to move from economic stability to accelerated growth with equity, is to generate sustainable sources of opportunity for the marginalized groups in society. This effort will require the expansion of micro-enterprises and small and medium firms, which are the main providers of jobs. Such firms face a variety of constraints, including lack of access to capital, weak technology and labor skills, and poor integration within supplier and distribution networks. Most small and medium-sized firms do not have access to property rights (including land) and to inexpensive conflict-resolution mechanisms, due to the lack of efficiency of the judiciary system and complex administrative procedures. There is no simple answer to these challenges but they have to be at the center of the new AGS.

3.24 The third priority is to optimize the perceived comparative advantage of the Senegalese economy in a few strategic sectors, and thus promote exports and/or job creation. The business principle is to push “what is already moving” and to give priority to the sectors that have contributed to two-thirds of GDP growth in the recent past. Those are by order of decreasing importance: communications, trade and financial services, real estate and construction, and agriculture and agribusiness (Figure 3.1). This focused approach has already been adopted in the AGS (at least for two sectors) and should be strengthened over the next few 20 For details, Senegal: Diagnostic Trade Integration Study, March 2003. 21 A recent Bank study indicates that the sugar sector in Senegal is under the monopoly of one company employing approximately 3,000 permanent employees (plus 2,000 temporaries), which benefits from relatively high protection levels. As a result, the consumer price of sugar is about US$1 per kilogram in Senegal, while it is US$0.4 in Sri Lanka and US$0.5 in The Gambia. Such a price differential has significant implications for poverty levels in Senegal since it is estimated that the number of people living in poverty would decline by 200,000 or by almost 2 percentage points if the sugar price were cut by half or equal to the one prevailing in The Gambia.

16

years. Over time, success in these sectors will spread over the rest of the economy, creating new synergies and investment opportunities.

Figure 3.1: Contributions to Economic Growth by Sector (2000-04)

0.0% 5.0% 10.0% 15.0% 20.0% 25.0%

Communication

Trade andfinancial services

Real estate andconstruction

Agriculture andagrobusiness

Source: World Bank

3.25 A stronger, more competitive agriculture sector combines the second and third priorities. Assisting small farmers and entrepreneurs in rural areas is essential because they are among the poorest segments of the population and the most exposed to climatic and natural shocks. As a result, these groups are the main sources of emigration toward urban centers, especially Dakar.22 The emergence of new exports (such as fresh vegetables of which exports boomed by 130 percent between 2003 and 2005) appears promising and should help diversify production and agricultural exports away from groundnuts. The recent increase in competitiveness of the agricultural sector in Senegal is nonetheless limited to a few locations (Niayes, Senegal River Valley, and Casamance regions) and products. It is also penalized by complex relationships between traditional and modern powers that make difficult access to land and discourage site development because of the lack of guarantees and financial resources. Furthermore, resource degradation is a growing challenge for Senegal, ranging from deforestation to land degradation associated with poor water resources management and the depletion of fish stocks. The Government has set out plans for addressing these issues and the Bank is currently finalizing its Country Environment Analysis, in close collaboration with donors and civil society.

3.26 The fourth priority is to increase the level of skills and technology used by the private sector in Senegal. As mentioned earlier, to be successful Senegal will have to boost and diversify its exports, suggesting that its local production in key sectors (such as ICT, exports, and agriculture) will have to be aligned with quality standards defined by consumers in industrialized markets. The recent knowledge assessment produced by World Bank Institute (WBI) on Senegal reveals that it ranked poorly even among other Sub-Saharan countries (see Table 3.1). Senegal has improved compared to 1995 but not as fast as other countries. Its main weaknesses appear to be related to the poor quality of its Research and Development (R&D) institutions and relatively 22 Rapport de la synthèse de la deuxième enquête sénégalaise auprès des ménages (ESAM-II), juillet 2004.

17

low education attainments. Fostering technological development will have to rely on a multi-faceted approach involving education establishments and research institutes, partnerships with private firms (local and foreign), and the State. A specific effort, supported by the World Bank, has been made by the Government to upgrade the National Fund for Agricultural Research (FNRAA) and to foster the links between the education system and the labor market. Concurrently, actions will have to be taken to upgrade the legal and institutional environments as well as to promote new channels for information and knowledge dissemination (notably through Senegalese expatriates, and partnerships with foreign universities and colleges).

3.27 The fifth and last priority is to take advantage of the presence of many Senegalese abroad (7 out of 10 Senegalese families report having one of their members living abroad). Senegal already benefits from significant remittances sent home by migrant workers and expatriates. While these funds help generate economic growth on a national scale by financing the purchase of consumer goods and real estate, they also represent a potential source of financing for more infrastructure projects and productive activities on a larger scale. A closer connection with the local banking system has to be developed to help monetize the economy since only 10 percent of the population is estimated to have a bank account today. The ongoing reform of the postal system and sustained growth of microfinance institutions will help achieve this goal. In parallel, actions should be taken to reverse the brain drain23 and to motivate expatriates to bring back new skills and technology to Senegal. The Government has started to focus on expatriates by launching a combined effort through the Ministry of Foreign Affairs and the Investment Promotion Agency (APIX).

4. SENEGAL’S LONG-TERM VISION AND MEDIUM-TERM PRIORITIES

4.1 The Senegalese Government is well aware that it needs to achieve more and better to address the above challenges in the next few years, and thus increase economic growth, create jobs, and reach the poor. This commitment is reflected in the second generation Poverty Reduction Strategy Paper (PRSP-II), which was presented to the Board on January 30, 2007, through which the authorities offer their vision for the next five years. At the outset, it is worth underscoring that this vision is well aligned with the MDGs agenda, and its formulation has benefited from inputs from donors, local Governments and representatives of the civil society as well as from the private sector.

4.2 Senegal’s medium-term vision is articulated around four pillars: (i) wealth creation; (ii) access to basic social services; (iii) protection of vulnerable groups; and (iv) greater transparency and participatory processes. The first three pillars were already included in the first PRSP, while the last one has emerged as a new priority for the authorities. Below is a presentation of the Government’s priority areas. These specific programs show what the Government is committed to accomplish.

4.3 By placing the Accelerated Growth Strategy (AGS) at the center of the first pillar of the PRSP-II, the authorities have rightly emphasized the need to encourage private sector-led growth and to expand and diversify exports. The AGS is based on two key objectives: (i)

23 An IMF study shows that 60 percent of African immigrants living in the US have a tertiary education (source: William J. Carrington and Enrica Detragiache, “How Extensive Is the Brain Drain?, Finance and Development”.

18

improving the overall investment climate in the economy by focusing on a series of cross-cutting issues (including in the areas of justice, taxes, infrastructure, and administrative barriers); and (ii) promoting the development of five cluster sectors with a presumed good export growth and job creation potential, including through measures to enhance sectoral competitiveness.24 In parallel, wealth creation will rely on the implementation of national sectoral strategies for the agricultural and livestock sectors aimed at promoting activities in rural areas. The PRSP-II discusses the large infrastructure projects that the Government plans to put in place over the next few years, including the Diamniadio industrial platform, the Dakar-Thiès highway, and the new airport. These projects will not only provide the necessary basis for private sector development, but will also help diversify economic activities away from Dakar and its suburbs (which account for about 80 percent of GDP on less than one percent of the national territory).

4.4 The second pillar based on human development will continue to promote access to basic social services by a growing share of the population. The implementation of the national strategies in the education and health sectors, as well as new commitments to enhance nutrition and access to sanitization and water are the key elements of the Government’s strategy.

4.5 The third pillar of the PRSP-II emphasizes the need to improve the lives of vulnerable groups, an area which has been neglected so far, and prescribes actions to ensure that these groups benefit from wealth creation and have better access to social services. Vulnerable groups are numerous and diverse in Senegal, including children, handicapped, elderly, and refugees. The recent finalization of the National Protection Strategy has helped build a consensus on a selected set of priorities, including the need to increase the coverage of existing safety nets, provide direct financial assistance to targeted groups, and improve the Government’s capacity to respond to natural catastrophes and shocks. Such a concerted approach has helped improve coordination between various stakeholders.