do you cee? the internet and online advertising market in central and eastern europe

Post on 13-Sep-2014

4.628 views

DESCRIPTION

‘Do you CEE?’ report prepared by Gemius is the key publication for all industry experts in the region. Between 2010 and 2011 edition, International Marketing Director, Marta Klepka presents updated landscape of the internet in CEE. Which are the key countries for the industry in 2011? What kind of characteristic changes & reshuffles have been observed during the past year? What kind of knowledge base does a potential investor need not only to enter but also to conquer a new market? Use the set of internet best practices & business intelligence solutions to grow your business onlineTRANSCRIPT

Do You CEE? The internet and online advertising market in Central and Eastern Europe.

MARTA KLEPKA

Sofia, 26.10.2011

2 DO YOU CEE

The internet and online advertising market in Central and Eastern Europe

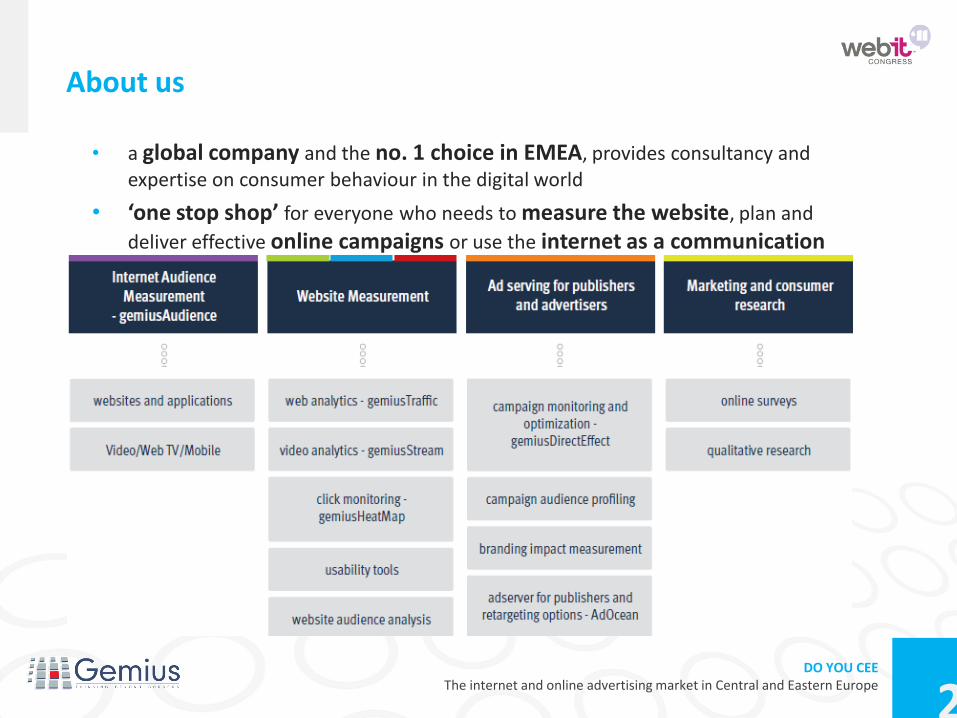

• a global company and the no. 1 choice in EMEA, provides consultancy and expertise on consumer behaviour in the digital world

• ‘one stop shop’ for everyone who needs to measure the website, plan and

deliver effective online campaigns or use the internet as a communication channel

About us

3 DO YOU CEE

The internet and online advertising market in Central and Eastern Europe

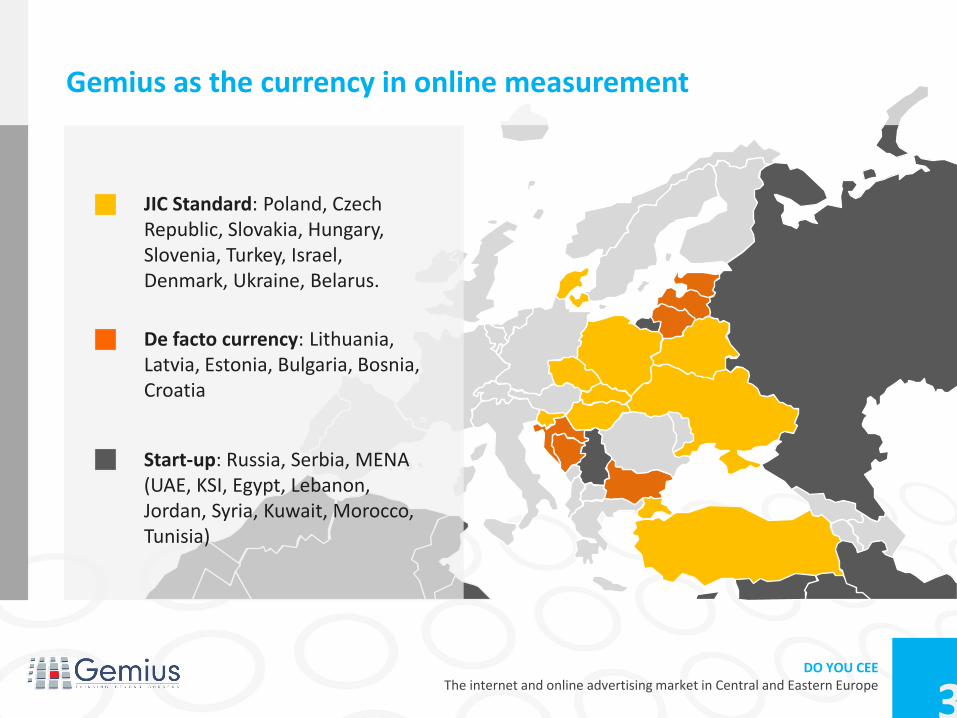

JIC Standard: Poland, Czech Republic, Slovakia, Hungary, Slovenia, Turkey, Israel, Denmark, Ukraine, Belarus.

De facto currency: Lithuania, Latvia, Estonia, Bulgaria, Bosnia, Croatia

Start-up: Russia, Serbia, MENA (UAE, KSI, Egypt, Lebanon, Jordan, Syria, Kuwait, Morocco, Tunisia)

Gemius as the currency in online measurement

4 DO YOU CEE

The internet and online advertising market in Central and Eastern Europe

Do You CEE? The internet and online advertising market in Central and Eastern Europe.

5 DO YOU CEE

The internet and online advertising market in Central and Eastern Europe

Size Potential Highlights

Adspends

Formats

Social

Mobile

Video

Size

6

Market size //

internet population in the CEE region (June 2011); source of data: Ukraine: gemiusAudience; Hungary: gemius/Ipsos Fusion Data; Latvia: gemiusAudience; Czech Republic: NetMonitor - SPIR - Mediaresearch & Gemius; Romania: Mercury Research; Slovakia: AIMmonitor - AIM – Mediaresearch & Gemius; Bulgaria: gemiusAudience (data collected using Synovate research);Poland: Megapanel PBI/Gemius; Slovenia:

gemusAudience; Turkey: IpsosKMG (data for July 2011); Russia: Gemius estimation based on FOM statistics/gemiusFusion Data; Estonia: gemiusAudience (data collected using TURU-UURINGUTE AS research); Lithuania: gemiusAudience; Croatia: Gemius/Valicon; Belarus: gemiusAudience; Romania: Euromonitor; Bosnia: gemiusAudience; Serbia: www.internetworldstats.com (June 2010) [age groups –

Lithuania, Poland: 7+; Czech Rep.: 10+; Croatia, Turkey: 12+; Estonia, Latvia,Hungary: 15+; Ukraine: 16+ Russia: 18+; Slovenia: 10-75; Slovakia: 14-79;Bosnia: 15-65; Bulgaria: 15-69; Belarus: 15-74]

INTERNET POPULATION (mm internet users / 2011)

The largest pure CEE

markets:

Russia (53.7 million internet users)

Poland (18.9 million internet users)

Turkey comes second in this ranking (24.5 million internet users)

0

10

20

30

40

50

60

Mill

ion

s

June 2010

June 2011

7

Market size //

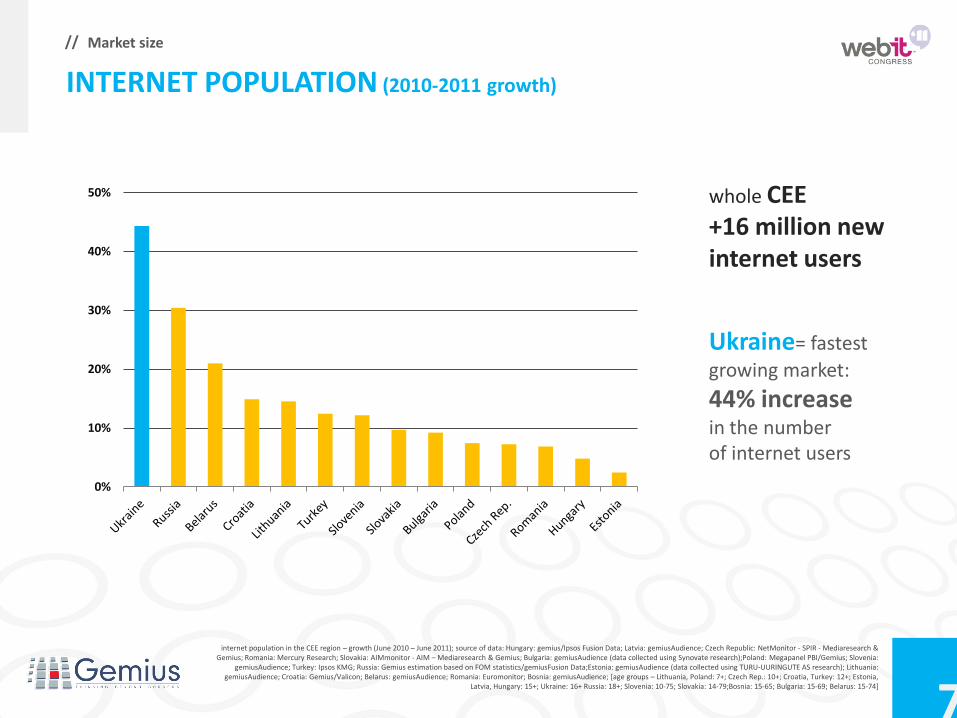

INTERNET POPULATION (2010-2011 growth)

whole CEE +16 million new internet users

Ukraine= fastest

growing market:

44% increase in the number of internet users

internet population in the CEE region – growth (June 2010 – June 2011); source of data: Hungary: gemius/Ipsos Fusion Data; Latvia: gemiusAudience; Czech Republic: NetMonitor - SPIR - Mediaresearch & Gemius; Romania: Mercury Research; Slovakia: AIMmonitor - AIM – Mediaresearch & Gemius; Bulgaria: gemiusAudience (data collected using Synovate research);Poland: Megapanel PBI/Gemius; Slovenia:

gemiusAudience; Turkey: Ipsos KMG; Russia: Gemius estimation based on FOM statistics/gemiusFusion Data;Estonia: gemiusAudience (data collected using TURU-UURINGUTE AS research); Lithuania: gemiusAudience; Croatia: Gemius/Valicon; Belarus: gemiusAudience; Romania: Euromonitor; Bosnia: gemiusAudience; [age groups – Lithuania, Poland: 7+; Czech Rep.: 10+; Croatia, Turkey: 12+; Estonia,

Latvia, Hungary: 15+; Ukraine: 16+ Russia: 18+; Slovenia: 10-75; Slovakia: 14-79;Bosnia: 15-65; Bulgaria: 15-69; Belarus: 15-74]

0%

10%

20%

30%

40%

50%

8

Market size //

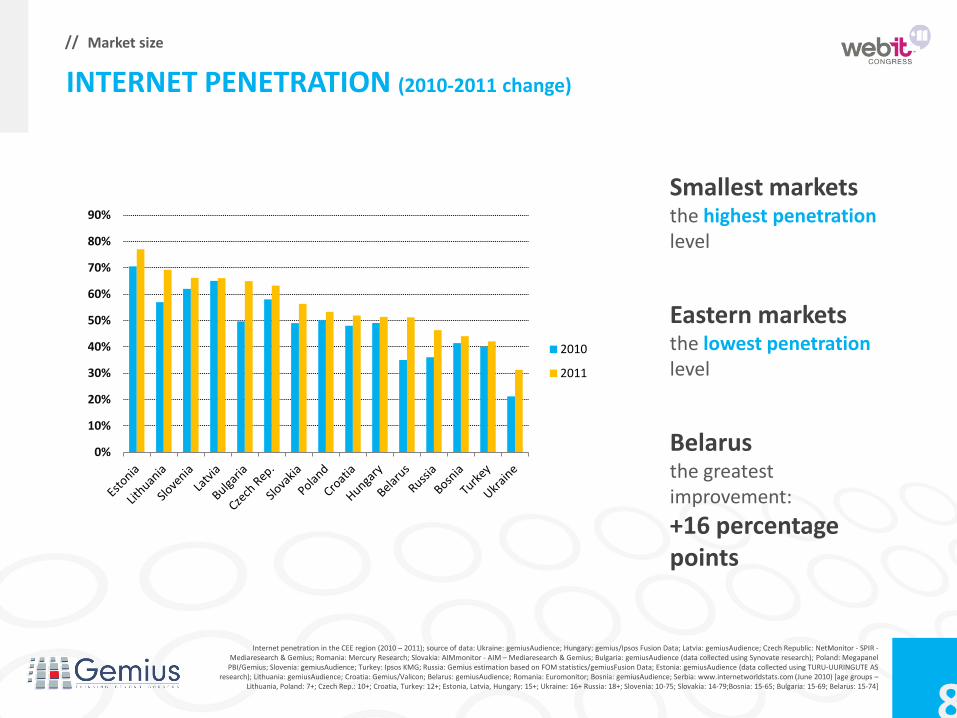

INTERNET PENETRATION (2010-2011 change)

Smallest markets the highest penetration level

Eastern markets the lowest penetration level

Belarus the greatest improvement:

+16 percentage points

Internet penetration in the CEE region (2010 – 2011); source of data: Ukraine: gemiusAudience; Hungary: gemius/Ipsos Fusion Data; Latvia: gemiusAudience; Czech Republic: NetMonitor - SPIR - Mediaresearch & Gemius; Romania: Mercury Research; Slovakia: AIMmonitor - AIM – Mediaresearch & Gemius; Bulgaria: gemiusAudience (data collected using Synovate research); Poland: Megapanel

PBI/Gemius; Slovenia: gemiusAudience; Turkey: Ipsos KMG; Russia: Gemius estimation based on FOM statistics/gemiusFusion Data; Estonia: gemiusAudience (data collected using TURU-UURINGUTE AS research); Lithuania: gemiusAudience; Croatia: Gemius/Valicon; Belarus: gemiusAudience; Romania: Euromonitor; Bosnia: gemiusAudience; Serbia: www.internetworldstats.com (June 2010) [age groups –

Lithuania, Poland: 7+; Czech Rep.: 10+; Croatia, Turkey: 12+; Estonia, Latvia, Hungary: 15+; Ukraine: 16+ Russia: 18+; Slovenia: 10-75; Slovakia: 14-79;Bosnia: 15-65; Bulgaria: 15-69; Belarus: 15-74]

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2010

2011

9

Market size //

BROADBAND PENETRATION

Data source: Eurostat

0

5

10

15

20

25

30

35

40

45

Bro

db

and

co

nn

ect

ion

s p

er

10

0 in

hab

itan

ts

Broadband penetration 2010

Only a few CEE markets reach

the EU average when it comes to

broadband penetration.

Some CEE markets are still much worse in these terms than even the worst Western markets.

2009 2010

10 DO YOU CEE

The internet and online advertising market in Central and Eastern Europe

Size Potential

Adspends

Formats

$

Social

Mobile

Video

Potential

Adspends $

Highlights

11

Market potential //

ONLINE ADSPENDS (mm € / 2009-2010 change)

Russians, Poles and Czechs spend

the biggest amount of money on internet advertising

Slovakia opens

the group of small markets

Data source: online adpends in the CEE region (2009-2010); source of data: IAB Europe, TNS LT, SPIR, ZenithOptimedia, Gemius. All countries except for Ukraine, Belarus and Serbia: gross values

€ 0

€ 100

€ 200

€ 300

€ 400

€ 500

€ 600

€ 700

€ 800

Mill

ion

s

2009

2010

12

Market potential //

0

10

20

30

40

50

60

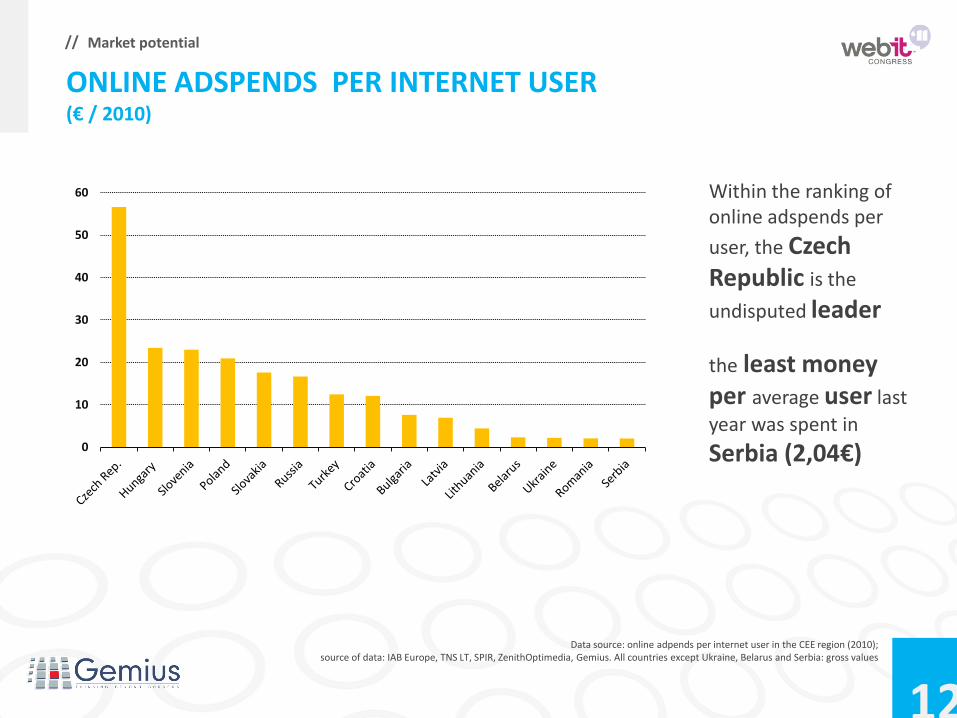

ONLINE ADSPENDS PER INTERNET USER (€ / 2010)

Within the ranking of online adspends per

user, the Czech Republic is the

undisputed leader

the least money per average user last

year was spent in

Serbia (2,04€)

Data source: online adpends per internet user in the CEE region (2010); source of data: IAB Europe, TNS LT, SPIR, ZenithOptimedia, Gemius. All countries except Ukraine, Belarus and Serbia: gross values

13

Market potential //

ONLINE AS SHARE OF TOTAL

Data source: ZenithOptimedia Group, AEF July 2011

The share of online in the total adspend in CEE countries is

much lower than in most countries of

Western Europe.

Still, it is comparable or higher than in the

Mediterranean markets, with Portugal serving the best example.

0%

5%

10%

15%

20%

25%

30%

35%

14 DO YOU CEE

The internet and online advertising market in Central and Eastern Europe

Size Potential

Adspends

Formats

$

Social

Mobile

Video

Potential

Formats

Highlights

15

Market potential //

Analysed Ads: Regular banners + rich media (Toplayer, Preroll, Expand, etc.) Source: gemiusDirectEffect 2011 H1

Share of campaigns using specific ad formats

53,0%

9,1%

7,4%

95,5%

6,9%

5,7%

2,0%

1,4%

88,1%

0,9%

0,6%

36,8%

13,0%

9,9%

6,2%

1,3%

0,7%

Regular Banners

Preroll

Expand

Regular Banners

Toplayer

Expand

Brandmark

Preroll

Regular Banners

Expand

Brandmark

Regular Banners

Preroll

Toplayer

Expand

Pop-up/Pop-under

Brandmark

Slo

vaki

a H

un

gary

C

zech

Rep

. P

ola

nd

16

Market potential //

Average CTR of specific ad formats

Analysed Ads: Regular banners + rich media (Toplayer, Preroll, Expand, etc.) Source: gemiusDirectEffect 2011 H1

0,28%

3,27%

1,52%

0,19%

4,20%

0,26%

2,31%

3,01%

0,20%

0,10%

1,16%

0,19%

1,54%

1,64%

0,50%

0,72%

0,82%

Regular Banners

Preroll

Expand

Regular Banners

Toplayer

Expand

Brandmark

Preroll

Regular Banners

Expand

Brandmark

Regular Banners

Preroll

Toplayer

Expand

Pop-up/Pop-under

Brandmark

Slo

vaki

a H

un

gary

C

zech

Rep

. P

ola

nd

17

Market potential //

Share of ad impressions by sector – Czech Rep.

gemiusAdMonitor

Source: gemiusDirectEffect 2011 H1

3 top industries are almost the same in all the measured countries: -Finance -Telecommunications - Automotive

-Only in Poland car industry was overtook by Entertainment/Trade and Personal Care/ Hygiene

29,2%

18,8%

10,8%

5,8%

5,6%

5,4%

4,9%

3,1%

2,3%

1,9%

1,5%

1,4%

1,2%

0,6%

0,1% 7,3%

Finance, Insurance, Brokerage Telecommunications Automotive Clothing & Accessories Travel, Tourism, Hotels & Restaurants Food Trade Personal Care and Hygiene Household Products Pharmaceuticals Beverages and Alcohol Household Equipment, Furniture And Decorations Computers and Audio Video Real Estate Leisure Time Other

18 DO YOU CEE

The internet and online advertising market in Central and Eastern Europe

Size Potential Highlights

Adspends

Formats

Social

Mobile

Video

Highlights

Video

19

Market highlights //

At present, the biggest part of the

current network traffic is video

And still growing! In Central and Eastern Europe, Internet video traffic will account for

47% of all consumer

Internet traffic in

2015, up from 27% in

2010.

Data source: Cisco VNI 2010

VIDEO ADSPENDS

20

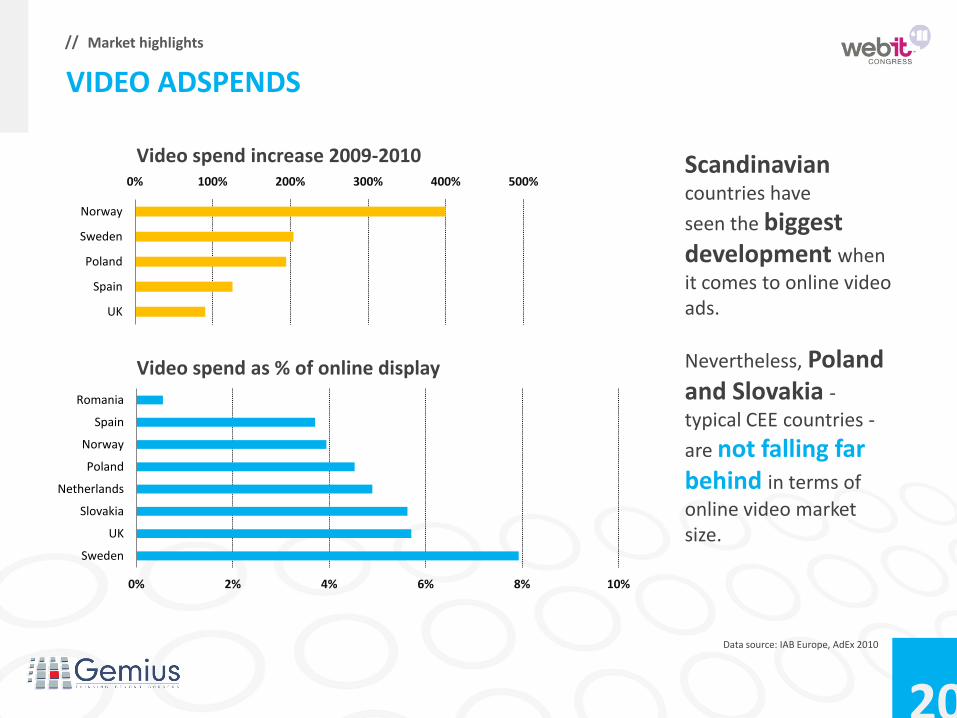

Market highlights //

Scandinavian countries have

seen the biggest development when

it comes to online video ads.

Nevertheless, Poland and Slovakia - typical CEE countries -

are not falling far behind in terms of

online video market size.

Data source: IAB Europe, AdEx 2010

VIDEO ADSPENDS

0% 100% 200% 300% 400% 500%

Norway

Sweden

Poland

Spain

UK

Video spend increase 2009-2010

0% 2% 4% 6% 8% 10%

Sweden

UK

Slovakia

Netherlands

Poland

Norway

Spain

Romania

Video spend as % of online display

21 DO YOU CEE

The internet and online advertising market in Central and Eastern Europe

Size Potential Highlights

Adspends

Formats

Social

Mobile

Video

Highlights

Mobile

22

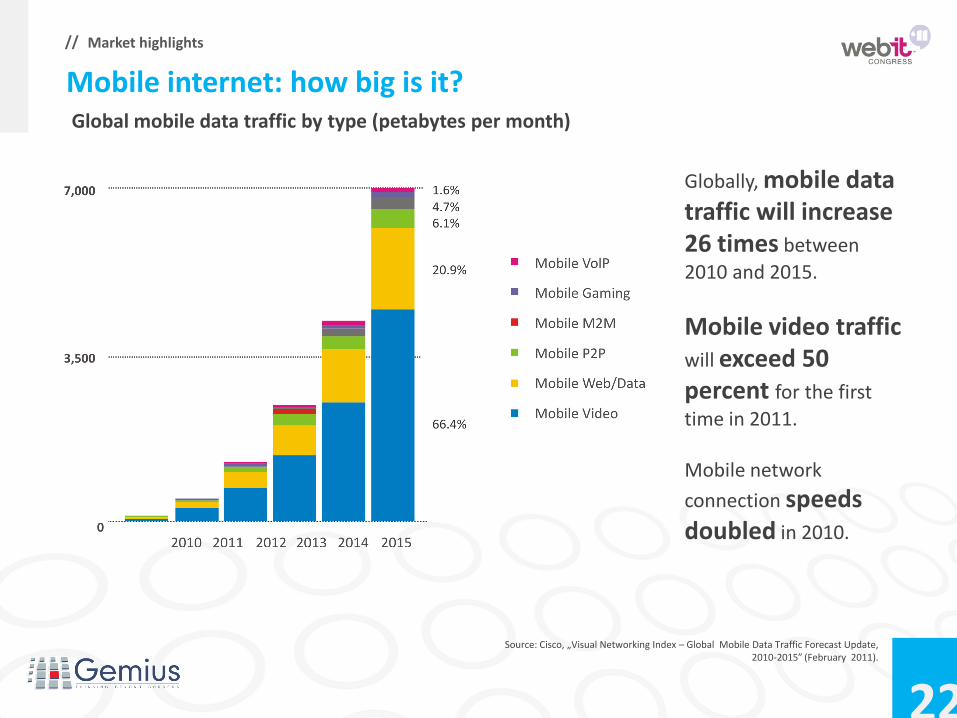

Market highlights //

Globally, mobile data traffic will increase 26 times between

2010 and 2015.

Mobile video traffic will exceed 50 percent for the first

time in 2011. Mobile network

connection speeds doubled in 2010.

Source: Cisco, „Visual Networking Index – Global Mobile Data Traffic Forecast Update, 2010-2015” (February 2011).

Global mobile data traffic by type (petabytes per month)

Mobile internet: how big is it?

23

Market highlights //

CEE – share of page views generated by visitors using mobile devices and PC computers

Mobile internet: how big is it?

1,5% Hungary

Page views - mobile devices

2,10%

Czech Republic 4,16%

Slovakia 7,21

% Denmark

1,96%

Ukraine 0,7% Bulgaria

Source of data: Gemius, gemiusTraffic (August 2011).

24

Market highlights //

0

5 000

10 000

15 000

2009 2010 2011 2012

Mobile search advertising Mobile display advertisings Mobile message advertising

Source: eMarketer (March 2008).

Total mobile adspends (mm$)

2007 2,695

2008 4,586

2009 7,375

2010 11,179

2011 15,250

2012 19,149

Mobile internet advertising spending worldwide: which formats? 2007-2012 (in millions)

25

Market highlights //

Source: Gemius, gemiusTraffic: Czech Republic, Bulgaria, Slovakia, Slovenia, Hungary, Poland, Russia, Ukraine (26.09.2011– 02.10.2011).

CEE – top 5 mobile devices (models) by website-averaged percentage share of page views generated on websites monitored by Gemius

21.1% Apple iPad

13.9% Apple iPhone

2.6% 2.2% 1.9%

Sam

su

ng

GT

-i9000

(Ga

lax

y S

)

Sa

ms

un

g G

T-i

91

00

(G

ala

xy S

II)

Preferences of mobile internet users: devices

HT

C D

es

ire

26

Market highlights //

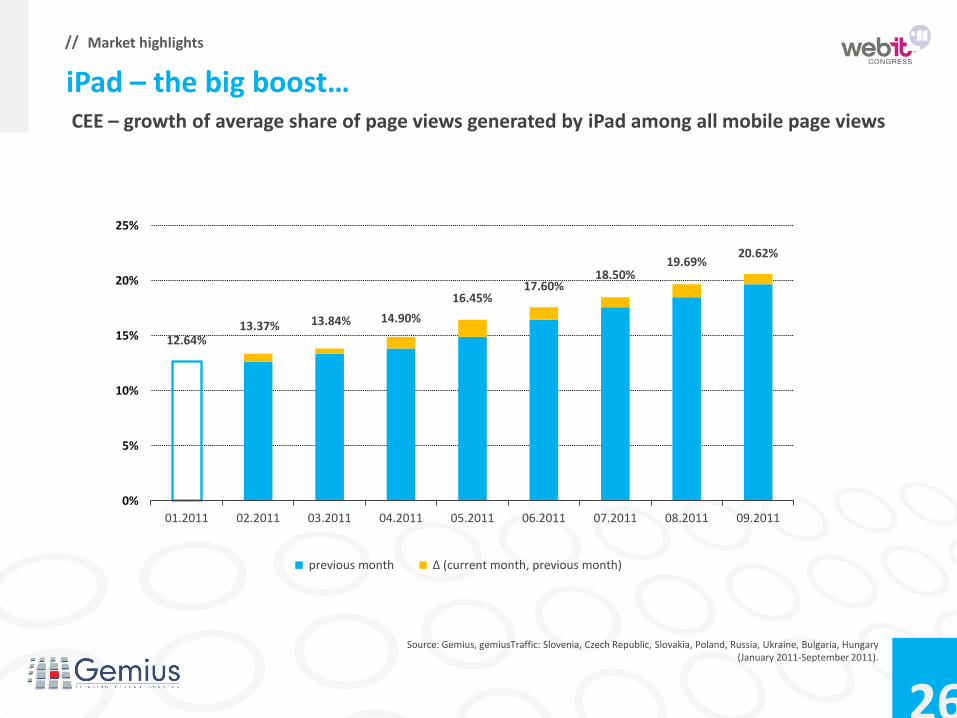

Source: Gemius, gemiusTraffic: Slovenia, Czech Republic, Slovakia, Poland, Russia, Ukraine, Bulgaria, Hungary (January 2011-September 2011).

) CEE – growth of average share of page views generated by iPad among all mobile page views

iPad – the big boost…

12.64% 13.37% 13.84% 14.90%

16.45% 17.60%

18.50% 19.69%

20.62%

0%

5%

10%

15%

20%

25%

01.2011 02.2011 03.2011 04.2011 05.2011 06.2011 07.2011 08.2011 09.2011

previous month ∆ (current month, previous month)

27

Market highlights //

The website-averaged percentage share of page views generated from iPad and iPhone on the selected markets

0%

5%

10%

15%

20%

25%

30%

35%

40%

Apple iPad, Q3 2011

Apple iPhone, Q3 2011

Source: Gemius, gemiusTraffic, Hungary, Denmark, Czech Republic, Bulgaria, Poland, Russia, Slovenia, Slovakia, Ukraine, Q3 2011.

28 DO YOU CEE

The internet and online advertising market in Central and Eastern Europe

Size Potential Highlights

Adspends

Formats

Social

Mobile

Video

Highlights

Social

29

Market highlights //

FACEBOOK USERS IN EUROPE (mm users / 2011)

Surprisingly, Turkey is Facebook’s biggest European market

Former East-block markets still have a growth potential for Facebook but local players remain strong.

Data source: www.socialbakers.com

0

5

10

15

20

25

30

35

April 2011

October 2011

30

Market highlights //

0

5

10

15

20

25

FACEBOOK USERS GROWTH IN THE LAST 6 MONTHS (%)

The Facebook’s pace of growth is

by far stronger in the east than in the west.

In Russia domestic social networks prevail.

Data source: www.socialbakers.com

31

Market highlights //

SOCIAL NETWORKS - Poland

The Polish giant, nk.pl, managed to

maintain a stable position for a year.

On the other hand,

Facebook is rapidly

gaining popularity – in a year it gained almost

50% users.

We will surely know the

winner in 2012.

Data source: Megapanel PBI/Gemius

0

2

4

6

8

10

12

14

Mill

ion

s R

U

Poland - clash of the social titans

nk.pl Group

facebook.com

32

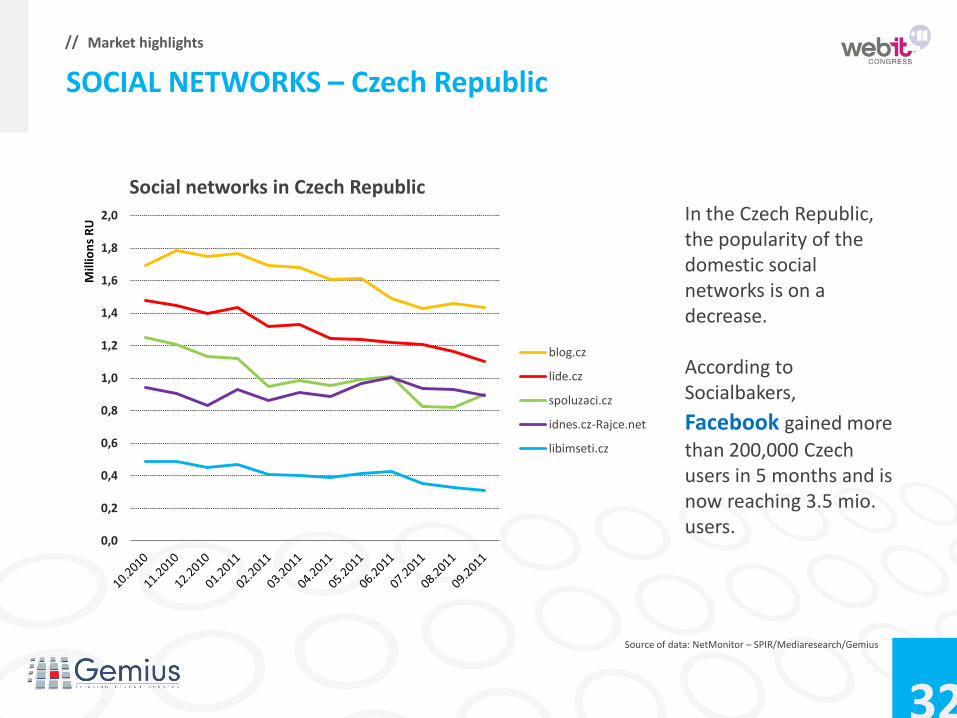

Market highlights //

Source of data: NetMonitor – SPIR/Mediaresearch/Gemius

In the Czech Republic, the popularity of the domestic social networks is on a decrease. According to Socialbakers,

Facebook gained more

than 200,000 Czech users in 5 months and is now reaching 3.5 mio. users.

SOCIAL NETWORKS – Czech Republic

0,0

0,2

0,4

0,6

0,8

1,0

1,2

1,4

1,6

1,8

2,0

Mill

ion

s R

U

Social networks in Czech Republic

blog.cz

lide.cz

spoluzaci.cz

idnes.cz-Rajce.net

libimseti.cz

33

Market highlights //

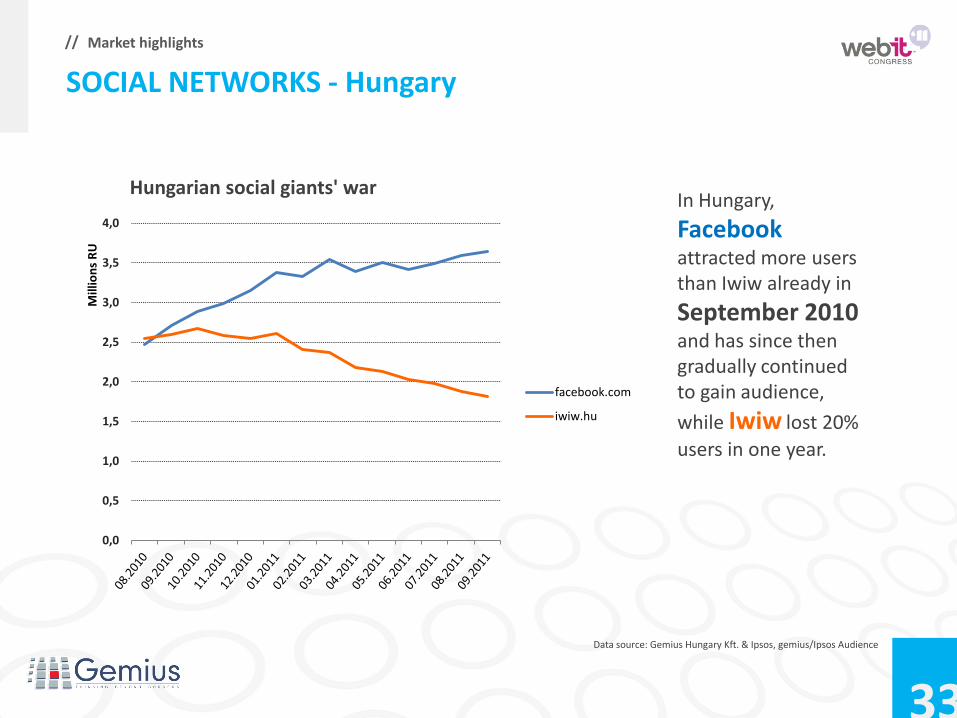

Data source: Gemius Hungary Kft. & Ipsos, gemius/Ipsos Audience

In Hungary,

attracted more users than Iwiw already in

September 2010 and has since then gradually continued to gain audience,

while Iwiw lost 20%

users in one year.

SOCIAL NETWORKS - Hungary

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

Mill

ion

s R

U

Hungarian social giants' war

facebook.com

iwiw.hu

34

Market highlights //

GOOGLE+

• Cost to build Google+ - 585 million USD • 500 employees engaged in the project

• 50 million users in 88 days

• Mark Zuckerberg is the most popular person on Google +

(almost 600,000 contacts)

Data source: Identyme.com

THANK YOU

Contact: Join us @: Facebook.com/GemiusGroup Twitter.com/Gemius Slideshare.net/Gemius_com YouTube.com/WwwGemiusCom

Marta Klepka

International Marketing Director [email protected]