do changes in dividend policy signal the future …repository.um.edu.my/830/1/do changes in dividend...

TRANSCRIPT

DO CHANGES IN DIVIDEND POLICY SIGNAL THE FUTURE OR THE PAST?

LIM WEI LING

FACULTY OF BUSINESS AND ACCOUNTANCY UNIVERSITY OF MALAYA

NOVEMBER 2008

Do Changes in Dividend Policy Signal the Future or the Past?

Lim Wei Ling

Bachelor of Business Administration Universiti Kebangsaan Malaysia

2001

Submitted to the Graduate School of Business Faculty of Business and Accountancy

University of Malaya, in partial fulfilment of the requirements for the Degree of Master of Business Administration

November 2008

ii

ABSTRACT

This research study investigates whether Malaysian Main Board companies pursue

changes in dividends to convey information on the future profitability of the

companies by studying on a total of 2,679 firm-year observations from year 1998 to

2007. The Ordinary Least Square regression results show that Main Board listed

companies do not use dividends as a signalling tool to convey information on the

future prospect of the companies. In fact, positive and significant relationship is found

to be stronger between changes in dividends in year T=0 with concurrent changes in

earnings in year T=0, which is consistent with the previous findings by Benartzi,

Michaely and Thaler (1997) and Nissim and Ziv (2001). Further, regression analysis

on sub-samples of firm-year observations categorized by the period of stable

dividends before the dividend change events (2 years, 3 years and 4 years) shows no

relationship exists between the stability of dividends before dividend change events

with the extent of dividend signalling. No relationship is found between size of

dividend change, size of dividend yield with the extent of dividend signalling.

Multiple regression by incorporating industry dummies in the regression equation

shows that no difference in changes in earnings between the 3 major sectors

(Industrial, Trading/Service and Consumer) when there are changes in dividends,

indicating that industry effect does not have any influence on the extent of dividend

signalling of the companies.

iii

ACKNOWLEDGEMENTS

I would like to express my gratitude to my supervisor of my research project,

Ybhg. Professor Dato' Dr. Mansor for his patience, support and guidance given on my

research area on dividend signalling. Despite the difficulties encountered in my

research due to meticulous works involved and constraints in getting complete

financial database needed in this study, I am glad to be able to complete my research

on time under the intellectual guidance and share of research experiences by Professor

Dato’ Dr. Mansor.

Million of thanks to my beloved family for their unconditional supports and

understanding despite of my less time with them due to my busy schedule for both

work and research project. Appreciation is also dedicated to my superior and

colleagues at work for their support and understanding during my entire MBA course

period.

Special thanks to Mr CG Teh, Mr KL Ooi and Ms Shirley Lo who have

provided their professional insights on dividend signalling in Malaysia. Being top

management involved in the dividend decision of three Main Board listed companies,

their feedbacks are really useful in explaining the reasons of dividend signalling not

applicable in Malaysia.

Last but not least, I would also like to express my appreciation to my fellow

MBA coursemates who have accompanied me for the whole MBA course with joy

and unforgettable memories. Special thanks to Mr Cheong Kok Loong who has

provided his assistance and support to me during my journey of completing this

research study.

iv

TABLE OF CONTENTS ABSTRACT……………………………………………………………………. ii ACKNOWLEDGEMENTS…………………………………………………… iii LIST OF SYMBOLS AND ABBREVIATIONS…………………………….. viii CHAPTER 1: INTRODUCTION……………………………………………………………... 1 1.1 PURPOSE AND SIGNIFICANCE OF THE STUDY…………………. 1 1.2 OBJECTIVE AND SCOPE OF THE STUDY…………………………. 2 1.3 LIMITATION OF THE STUDY ………………………………………. 4 1.4 ORGANISATION OF THE STUDY…………………………………... 5 CHAPTER 2: LITERATURE REVIEW…………………………………….. 6 2.1 WHAT IS DIVIDEND POLICY……………………………………….. 6 2.2 THE DIVIDEND SIGNALLING THEORY…………………………… 12

2.2.1 Previous literatures that support earnings and past dividends determine current dividends…………………………………… 15

2.2.2 Previous literatures that support changes in dividends do not provide signals to the market…………………………………… 17

2.2.3 Previous literatures that support changes in dividends provide signals to the market…………………………………………… 20

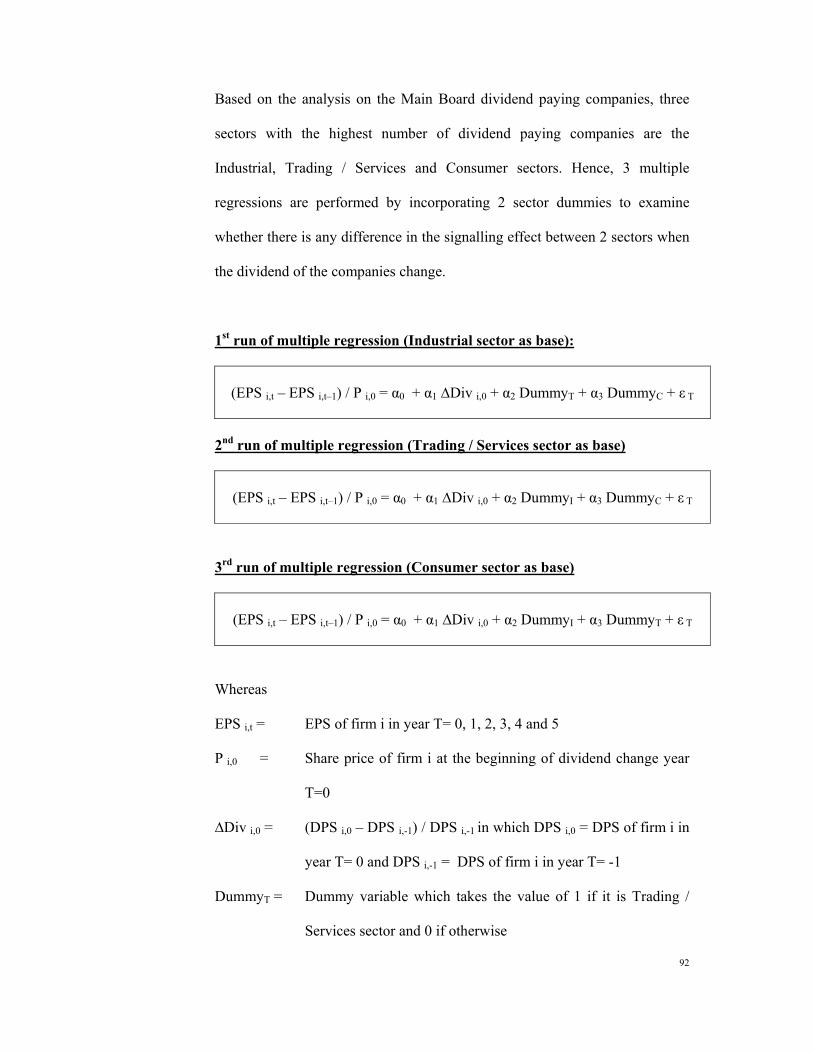

CHAPTER 3: RESEARCH METHODOLOGY……………………………. 23 3.1 DEVELOPMENT OF THE HYPOTHESES…………………………… 23 3.2 SELECTIONS OF MEASURES……………………………………….. 27

3.2.1 Measure of unexpected earnings………………………………... 28 3.2.2 Measure of changes in dividends……………………………….. 29

3.3 SAMPLING DESIGN…………………………………………………... 30 3.4 DATA COLLECTION PROCEDURE…………………………………. 31 3.5 DATA ANALYSIS TECHNIQUES……………………………………. 32

3.5.1 Data Filtering…………………………………………………… 32 3.5.2 Assumptions adopted in the regression analysis……………… 33 3.5.3 Analysis on the relationship between changes in dividends in

year 0 with changes in earnings in the concurrent year and subsequent 5 years ……………………………………………... 34

3.5.4 Analysis on the extent of dividend signalling with the influence of industry effect using multiple regression…………………….. 36

CHAPTER 4: RESEARCH RESULTS……………………………………… 37 4.1 SUMMARY STATISTICS……………………………………………... 37

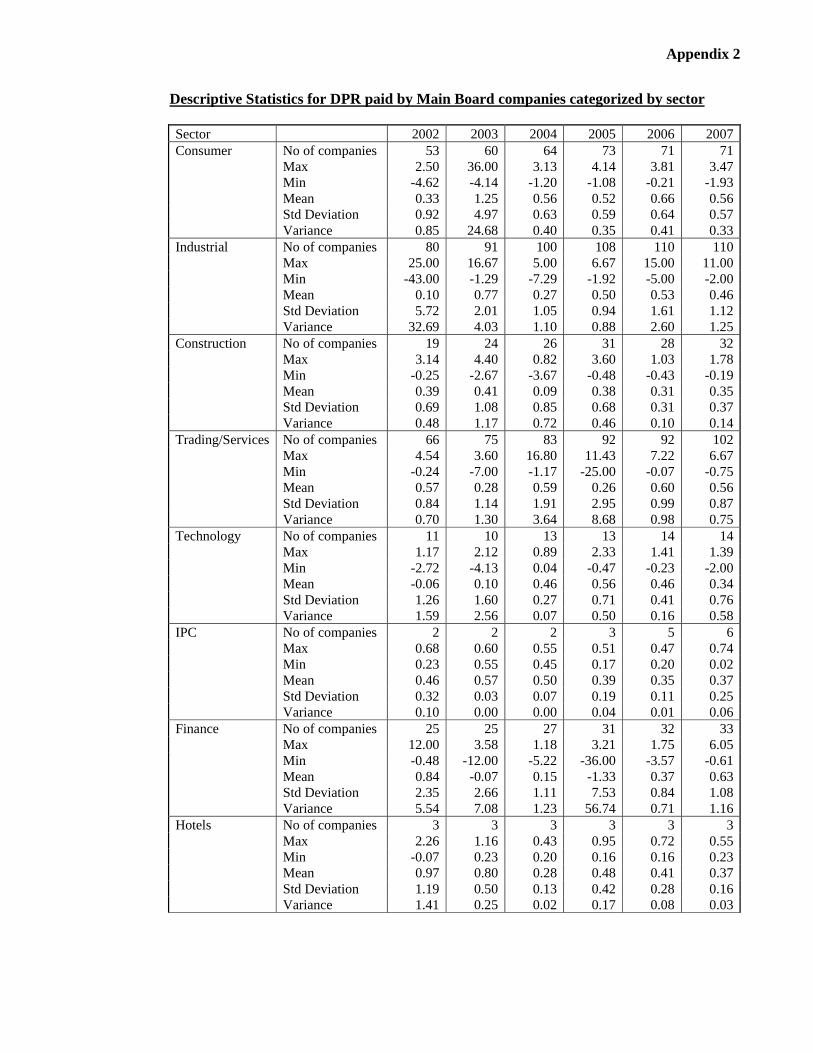

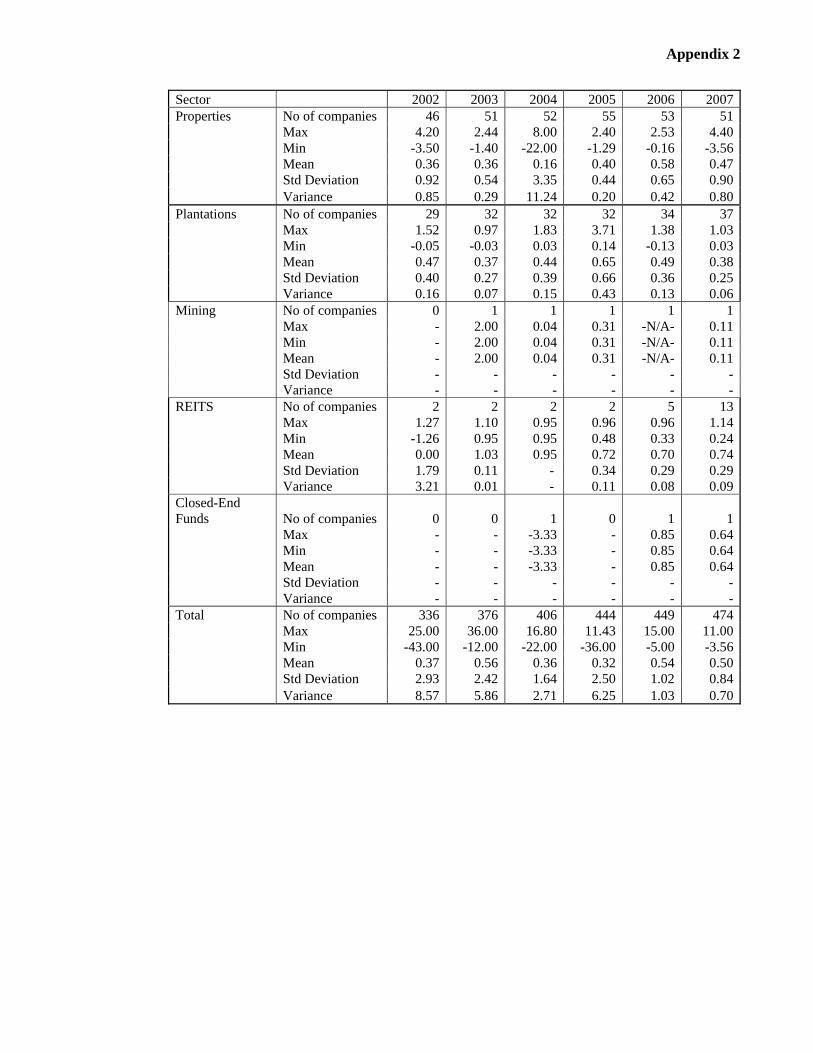

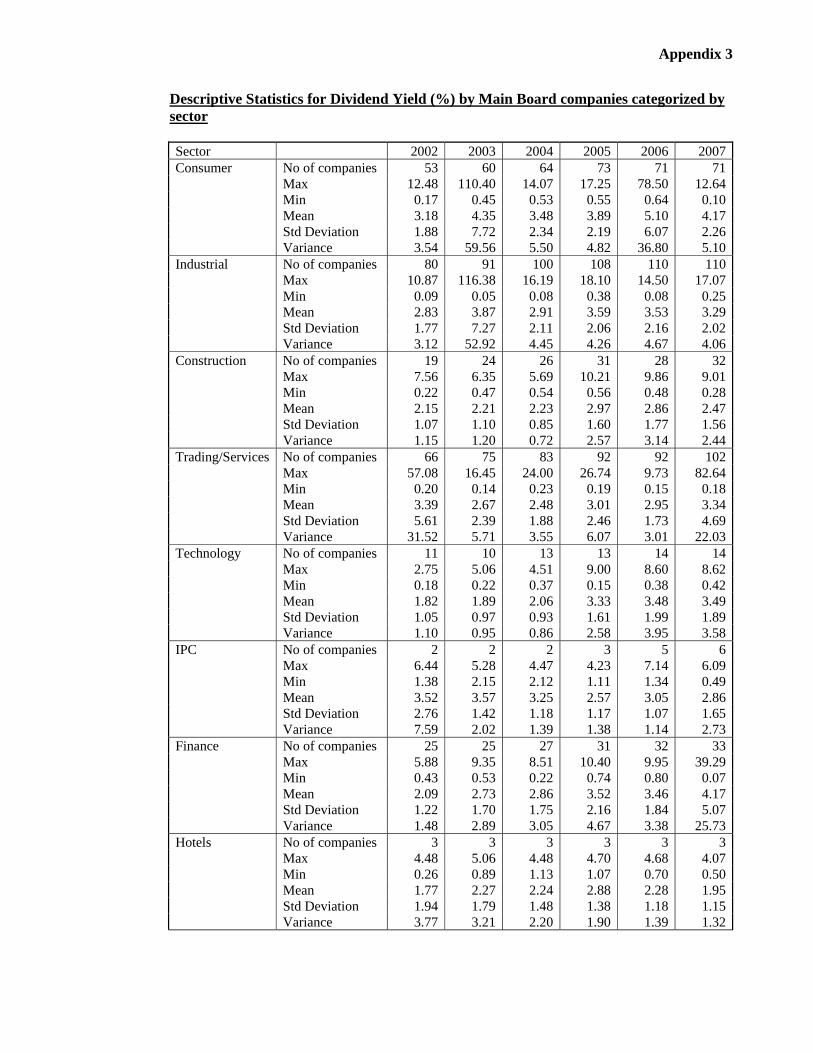

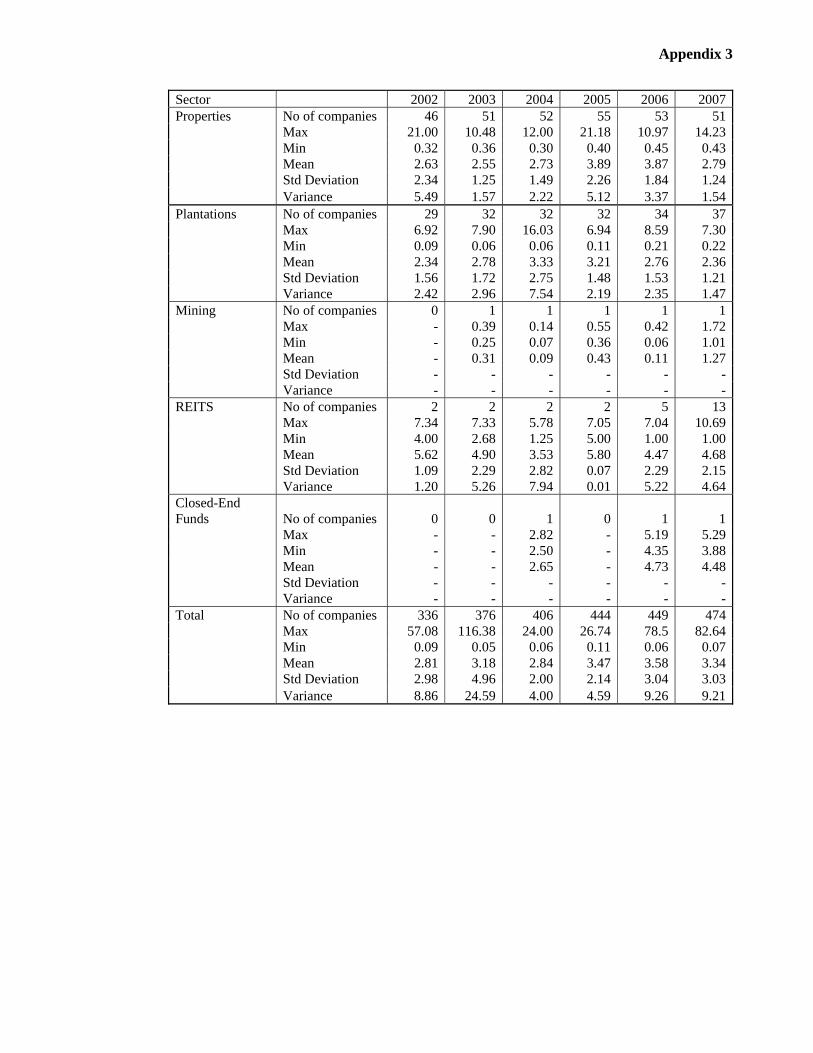

4.1.1 Overall Dividend Payment Trend of Main Board Listed Companies in Bursa Malaysia…………………………………... 39

4.1.2 Descriptive summary on the selected samples………………….. 53 4.2 ANALYSIS OF MEASURES………………………………………….. 62

4.2.1 Analysis of Regression Result on All Firm-Year Observations... 66 4.2.2 Analysis of Regression Result on Each Individual Year

Observations From Year 1998 to 2007…………………………. 70 4.2.3 Analysis of Regression Result on Dividend Change Events

During the Financial Crisis Period (1998-2001) and Post-Financial Crisis Period (2002-2007)……………………………. 81

4.2.4 Analysis of Regression Result on Dividend Change Events Occurred After Stable DPS for Consecutive 2 years, 3 years and 4 years…………………………………………………………... 85

v

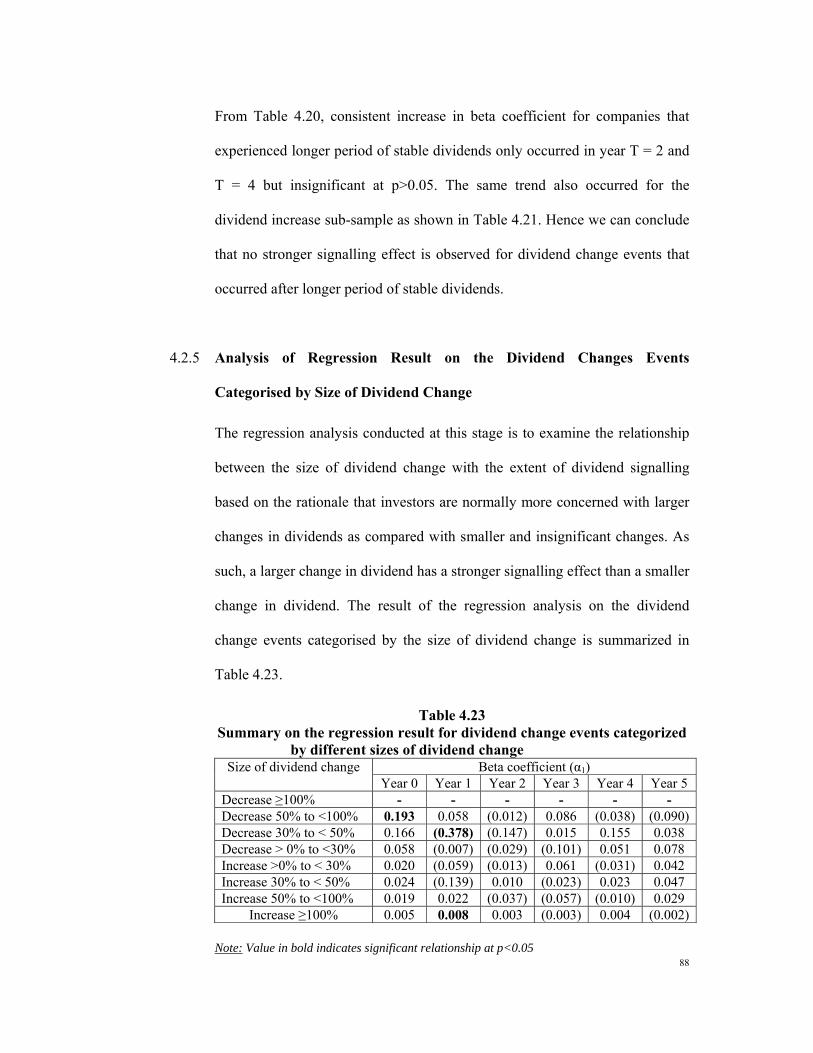

4.2.5 Analysis of Regression Result on the Dividend Change Events Categorized by Size of Dividend Change……………………… 88

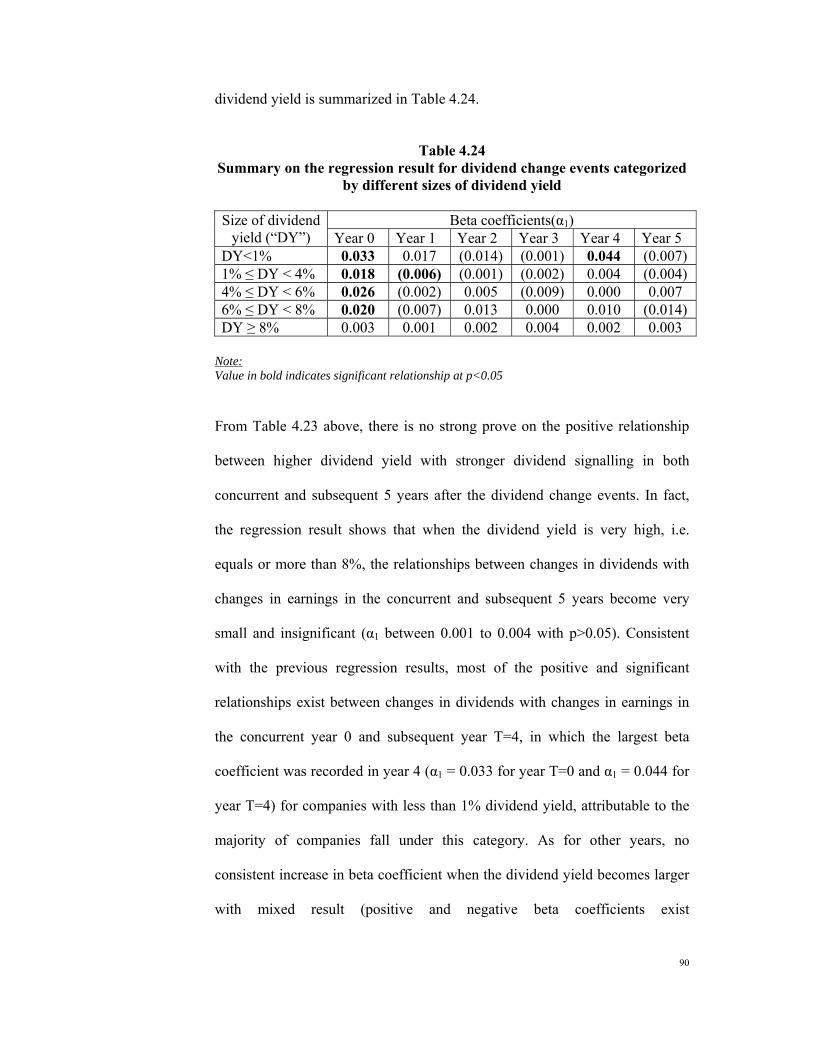

4.2.6 Analysis of Regression Result on Dividend Change Events Categorized by Size of Dividend Yield………………………… 89

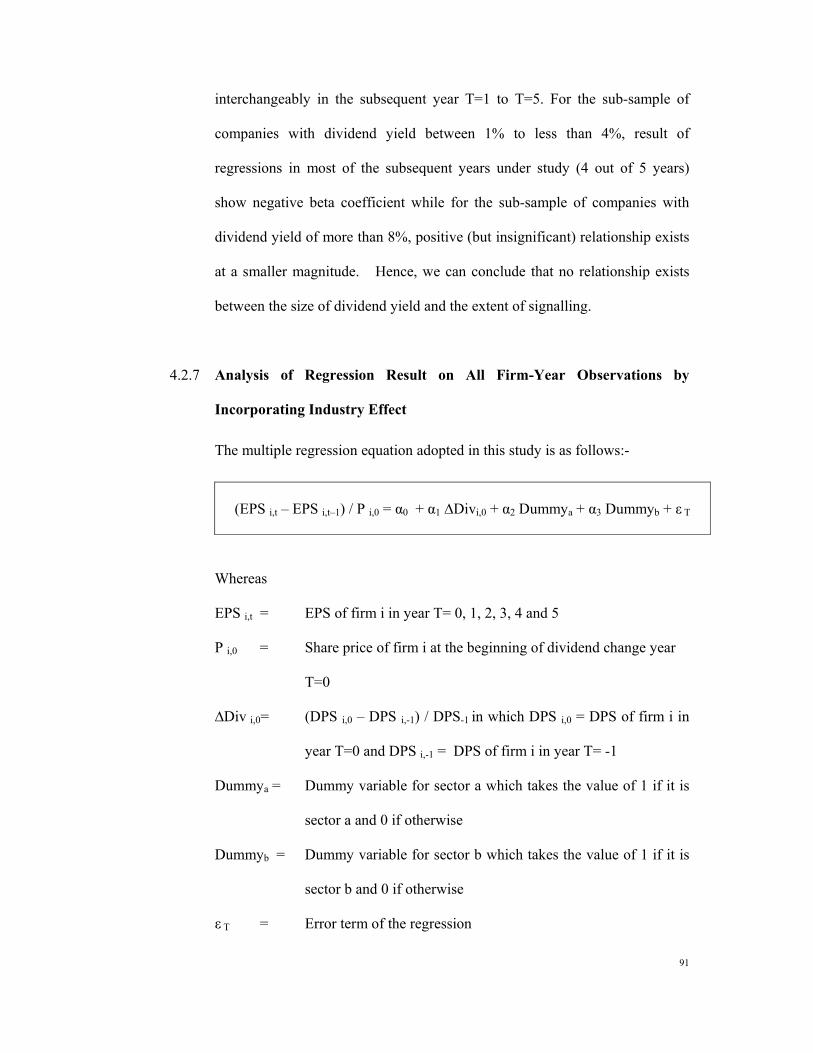

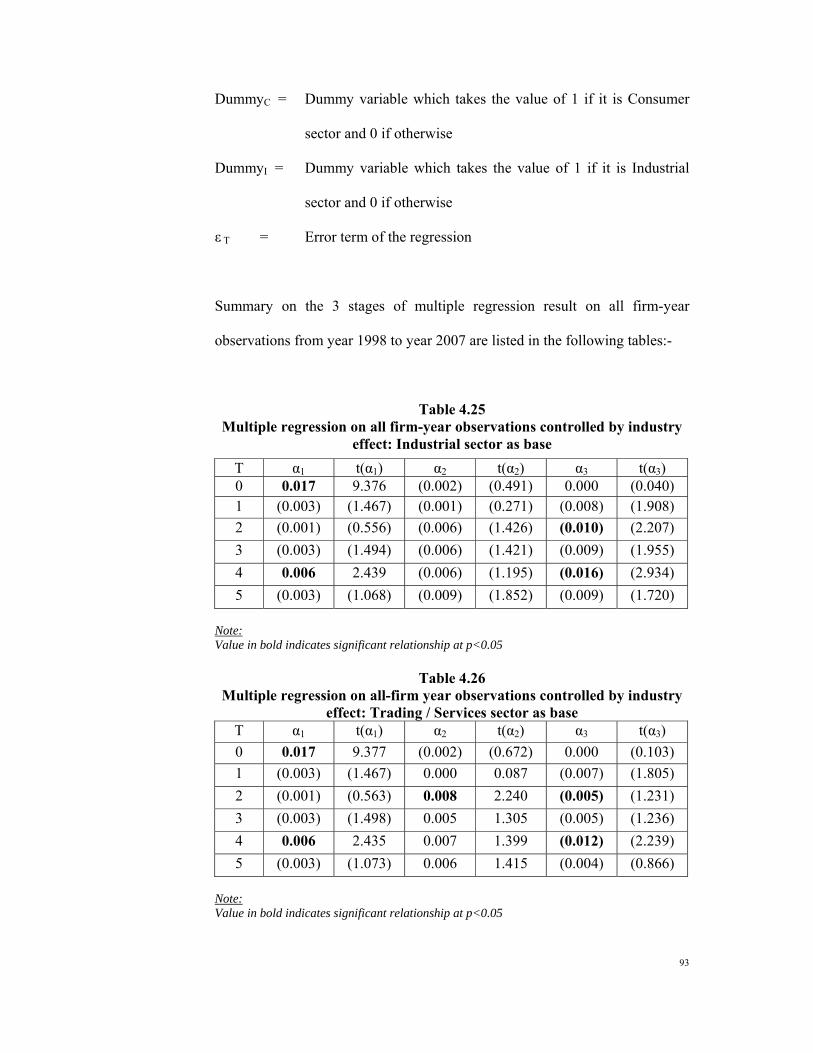

4.2.7 Analysis of Regression Result on All Firm-Year Observations by Incorporating Industry Effect……………………………….. 91

4.3 SUMMARY OF RESEARCH RESULTS……………………………… 97 CHAPTER 5: CONCLUSIONS AND RECOMMENDATIONS…………... 109 5.1 CONCLUSION…………………………………………………………. 109 5.2 SUGGESTIONS FOR FUTURE RESEARCH ………………………... 117 REFERENCES………………………………………………………………… 119 APPENDICES

vi

LIST OF FIGURES Figure 4.1

Composition of dividend paying and non-dividend paying companies in the Main Board of Bursa Malaysia (2002-2007)…… 37

Figure 4.2

Dividend paying companies in the Main Board of Bursa Malaysia (by sector), 2002-2007…………………………………………….. 40

Figure 4.3 Type of dividend changes for dividend paying companies (2002-2007)……………………………………………………………….. 41

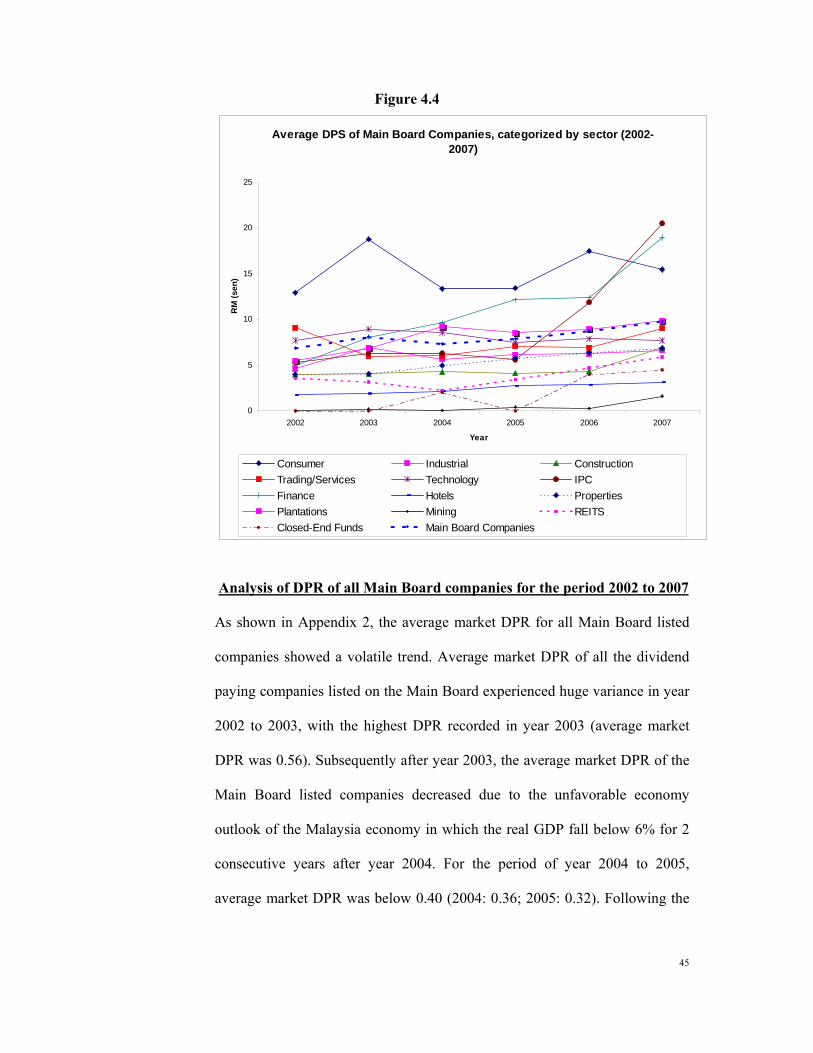

Figure 4.4 Average DPS of Main Board Companies, categorized by sector (2002-2007)………………………………………………………... 45

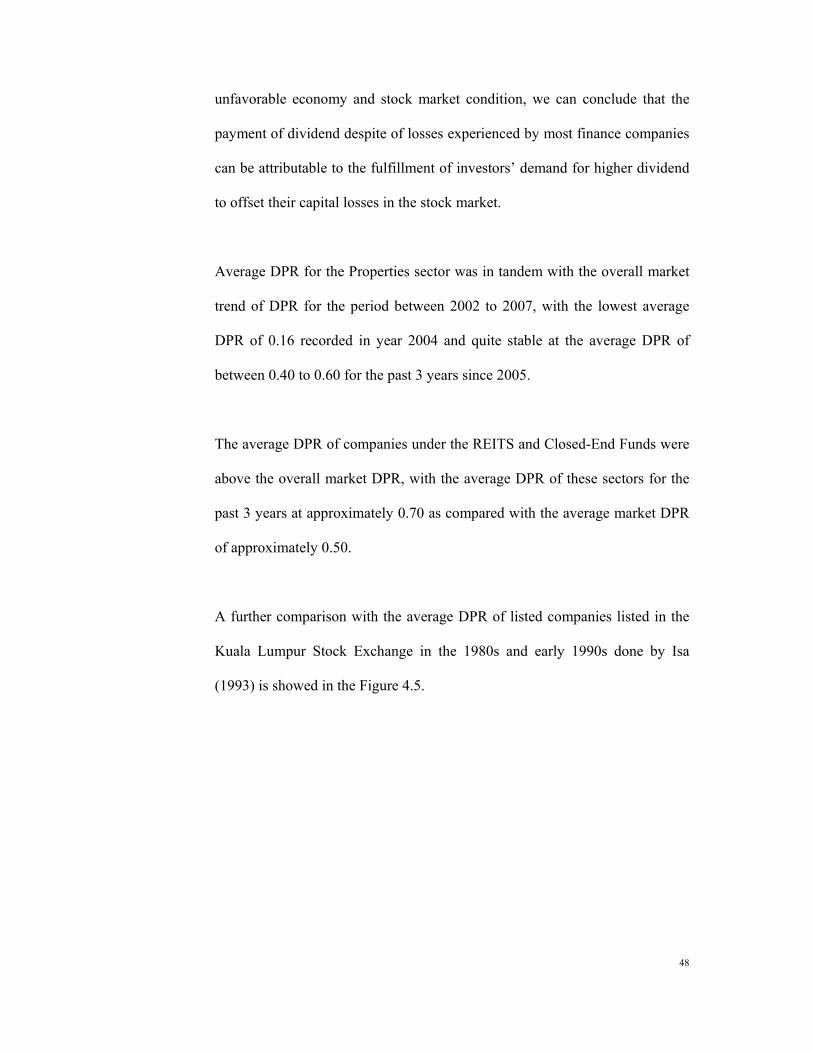

Figure 4.5 Average DPR of listed companies between 1981-2007…………… 49 Figure 4.6

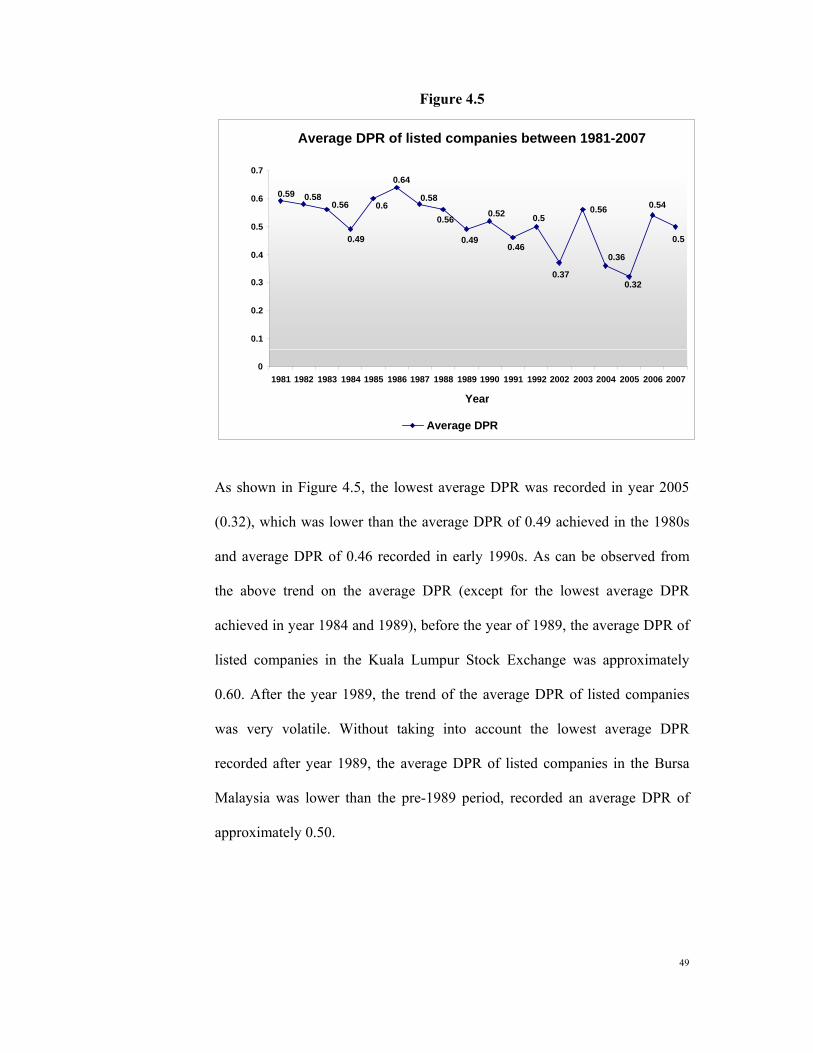

Average Dividend Payout Ratio of Main Board Companies categorized by sector (2002-2007)………………………………… 50

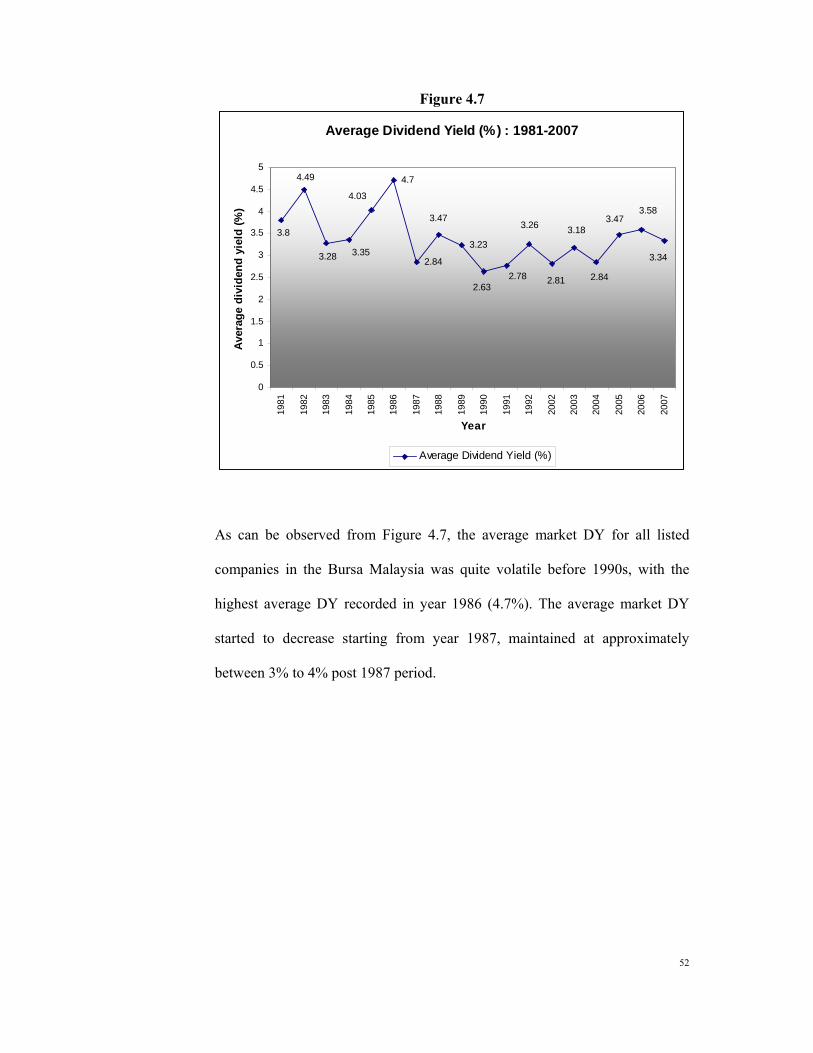

Figure 4.7 Average Dividend Yield (%): 1981-2007…………………………. 52 Figure 4.8

Average Dividend Yield of Main Board Companies categorized by sector (2002-2007)………………………………………………… 53

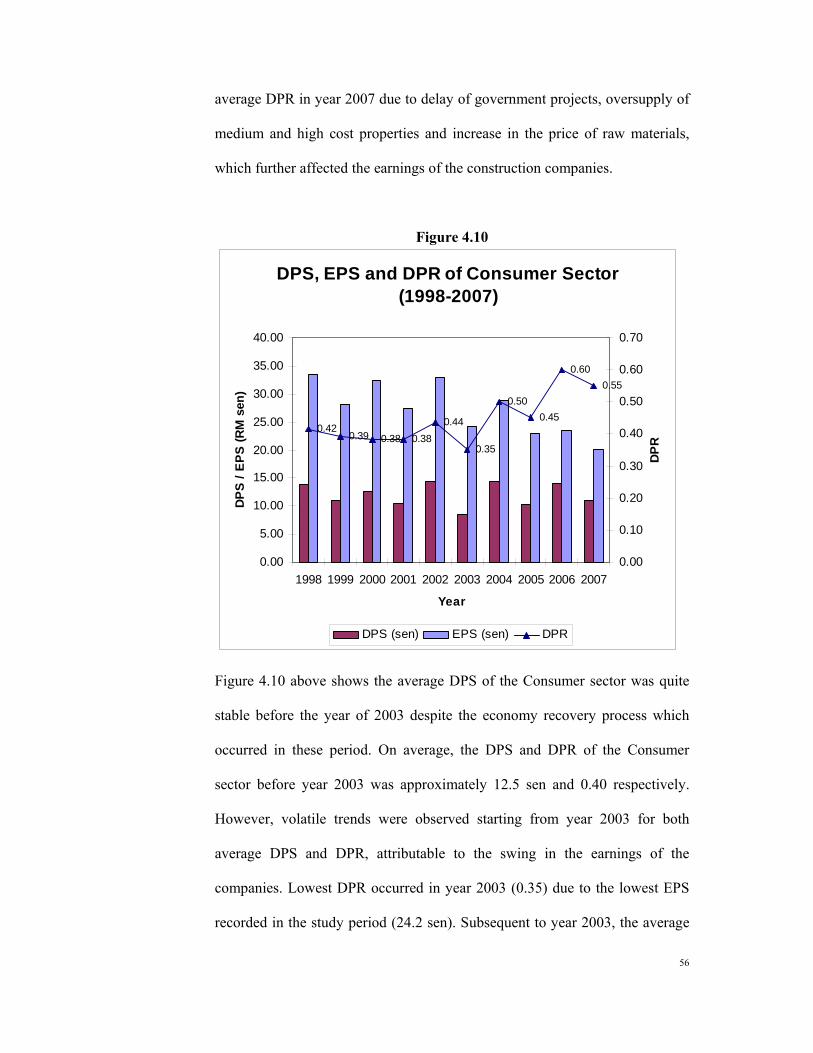

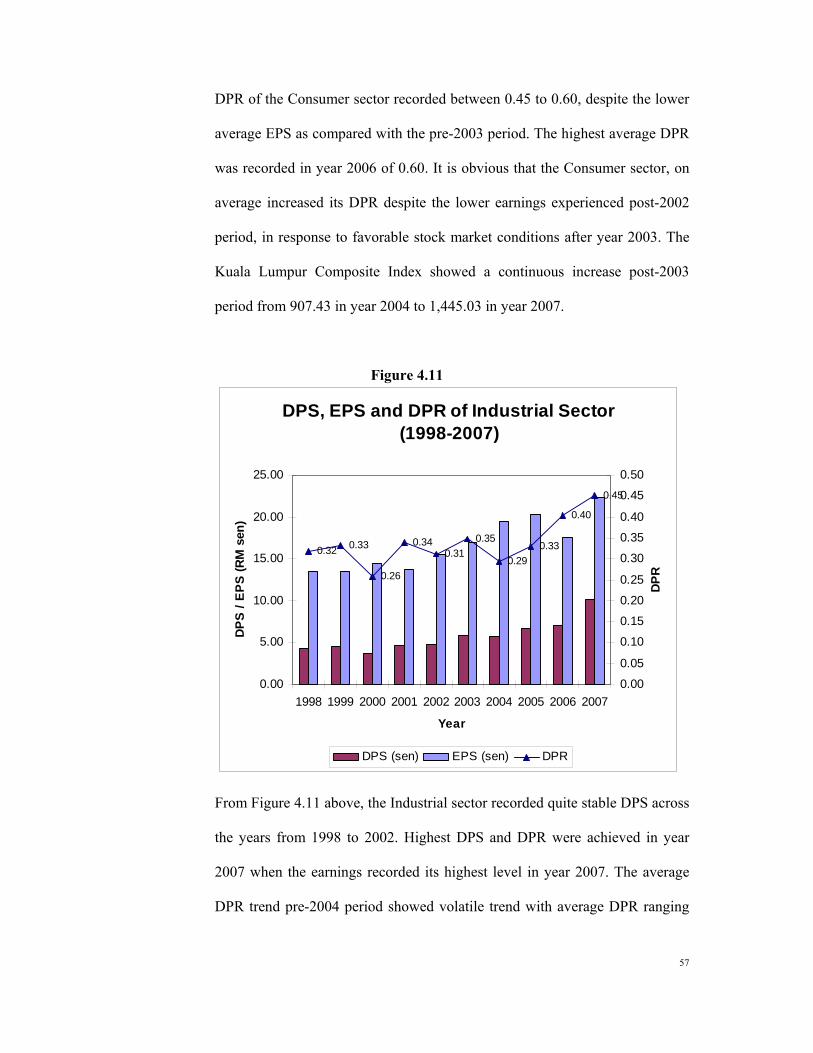

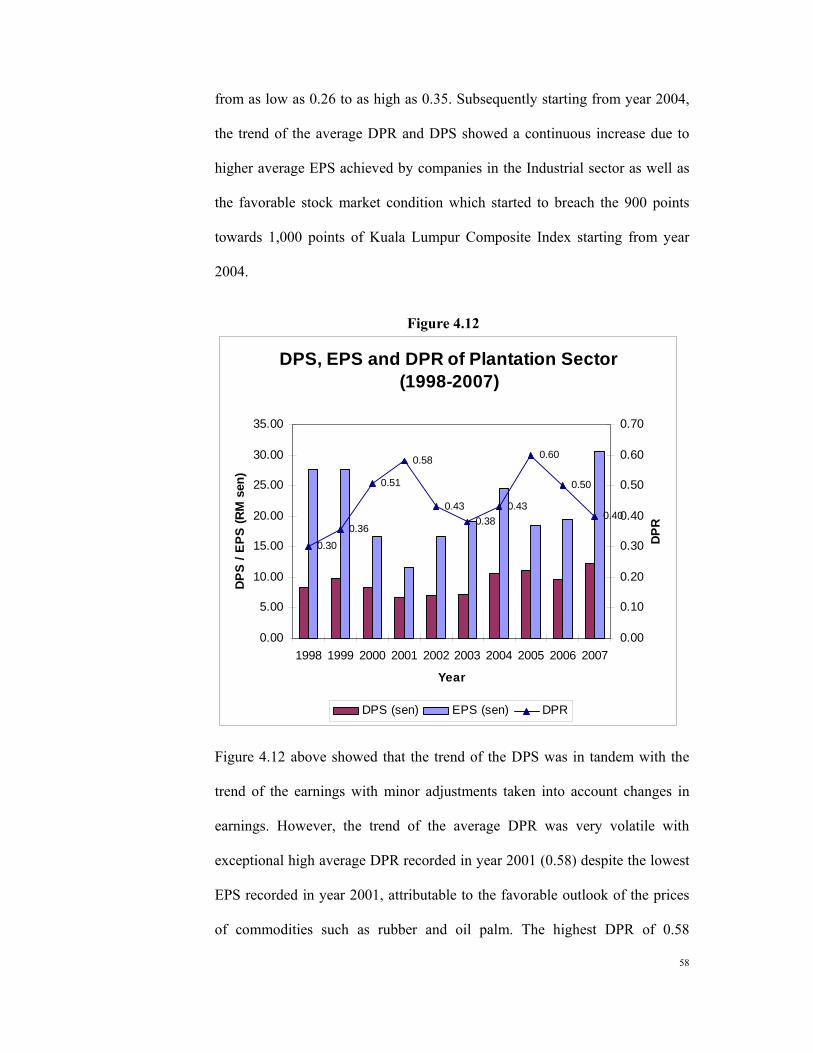

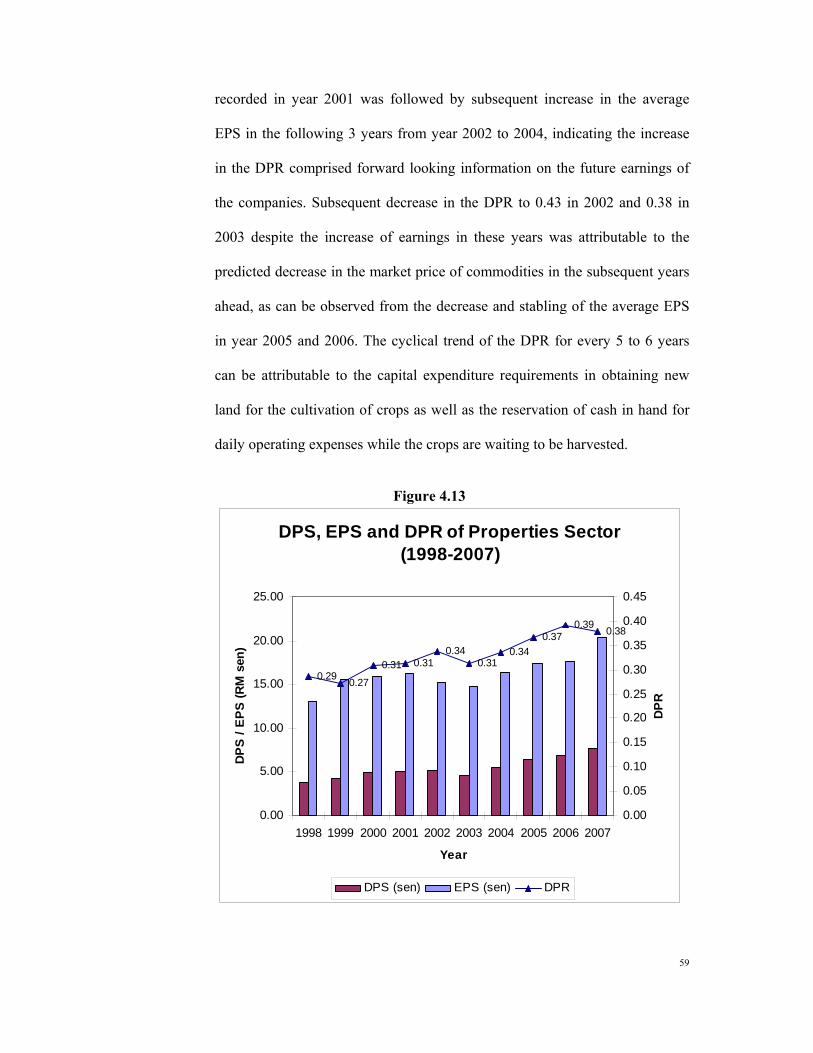

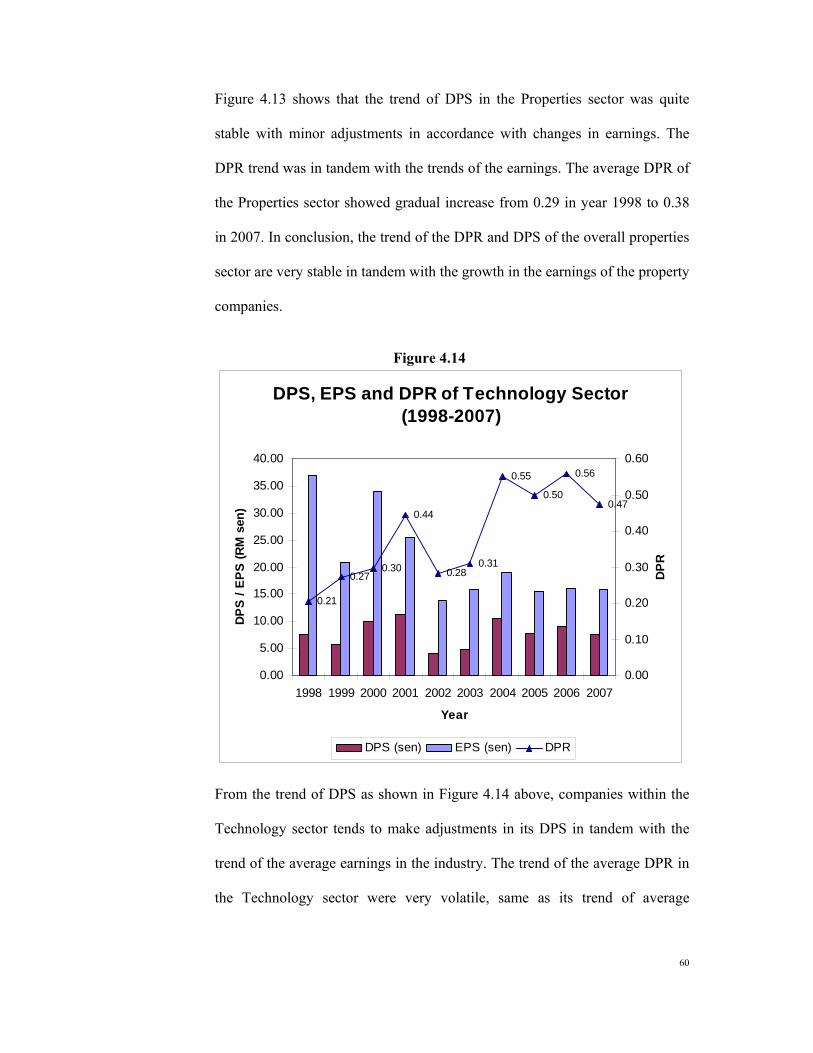

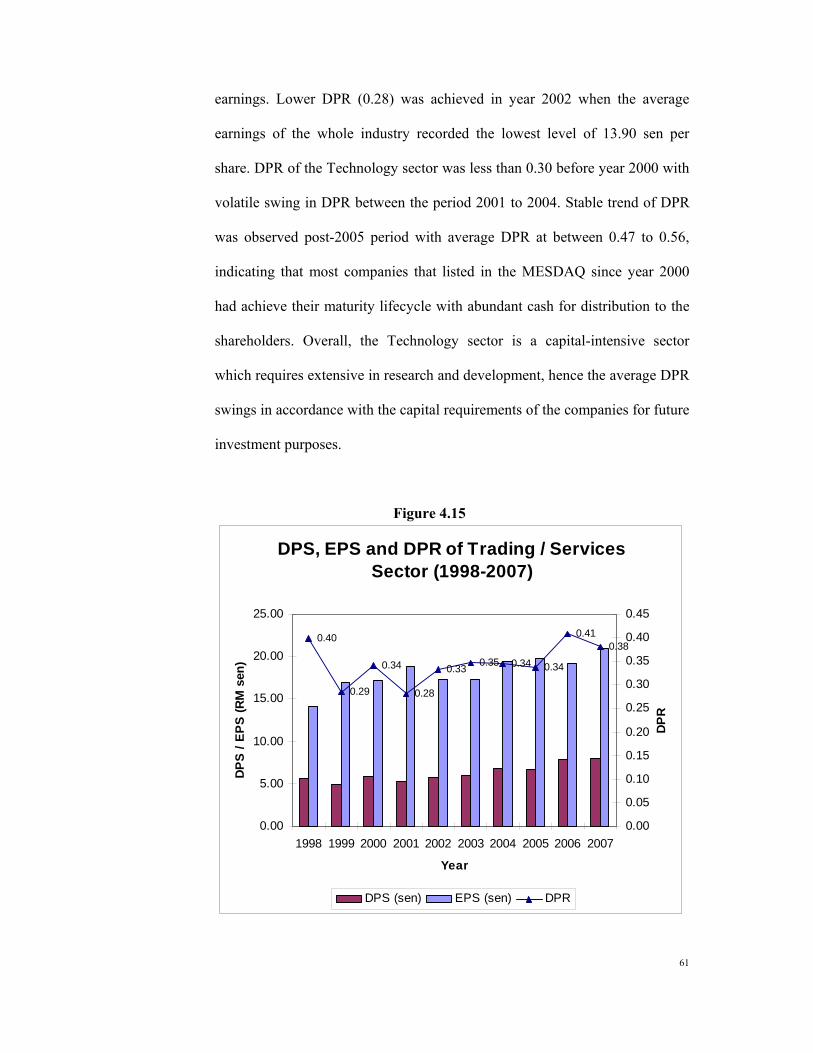

Figure 4.9 DPS, EPS and DPR of Construction Sector (1998-2007)…………. 55 Figure 4.10 DPS, EPS and DPR of Consumer Sector (1998-2007)……………. 56 Figure 4.11 DPS, EPS and DPR of Industrial Sector (1998-2007)…………….. 57 Figure 4.12 DPS, EPS and DPR of Plantation Sector (1998-2007)……………. 58 Figure 4.13 DPS, EPS and DPR of Properties Sector (1998-2007)……………. 59 Figure 4.14 DPS, EPS and DPR of Technology Sector (1998-2007)………….. 60 Figure 4.15 DPS, EPS and DPR of Trading / Services Sector (1998-2007)…… 61

LIST OF TABLES Table 3.1 List of Regression Analysis………………………………………... 35 Table 4.1 No. of dividend paying companies from year 2002 to 2007………. 37 Table 4.2 Percentage of dividend paying companies by sector (Year 2002-

2007)……………………………………………………………….. 39 Table 4.3 Type of dividend changes for dividend paying companies (2002-

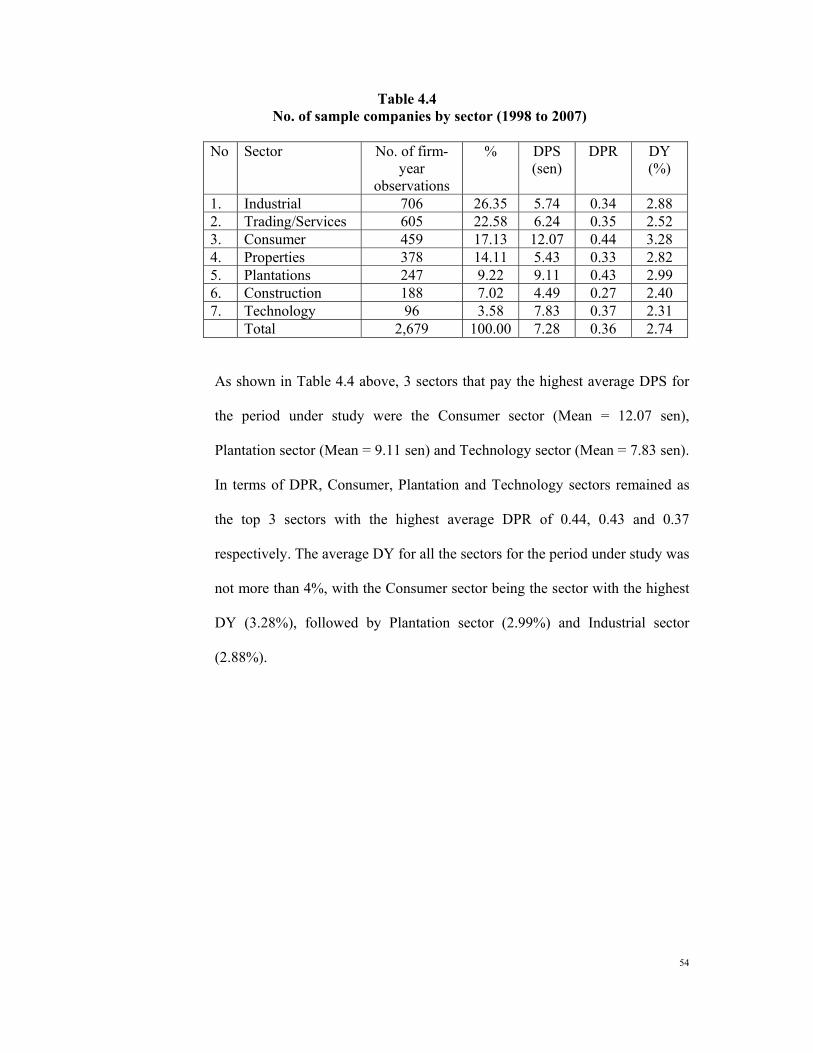

2007)……………………………………………………………….. 41 Table 4.4 No. of sample companies by sector (1998 to 2007)……………….. 54 Table 4.5

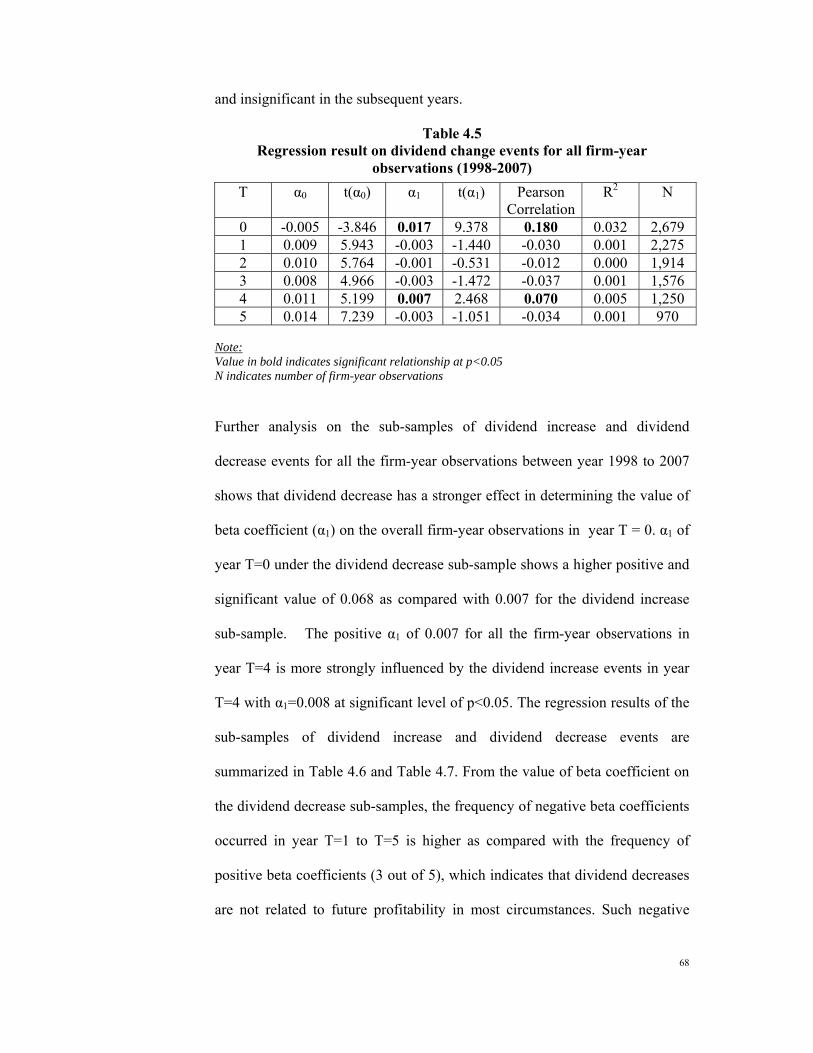

Regression result on dividend change events for all firm-year observations (1998-2007)………………………………………….. 68

Table 4.6

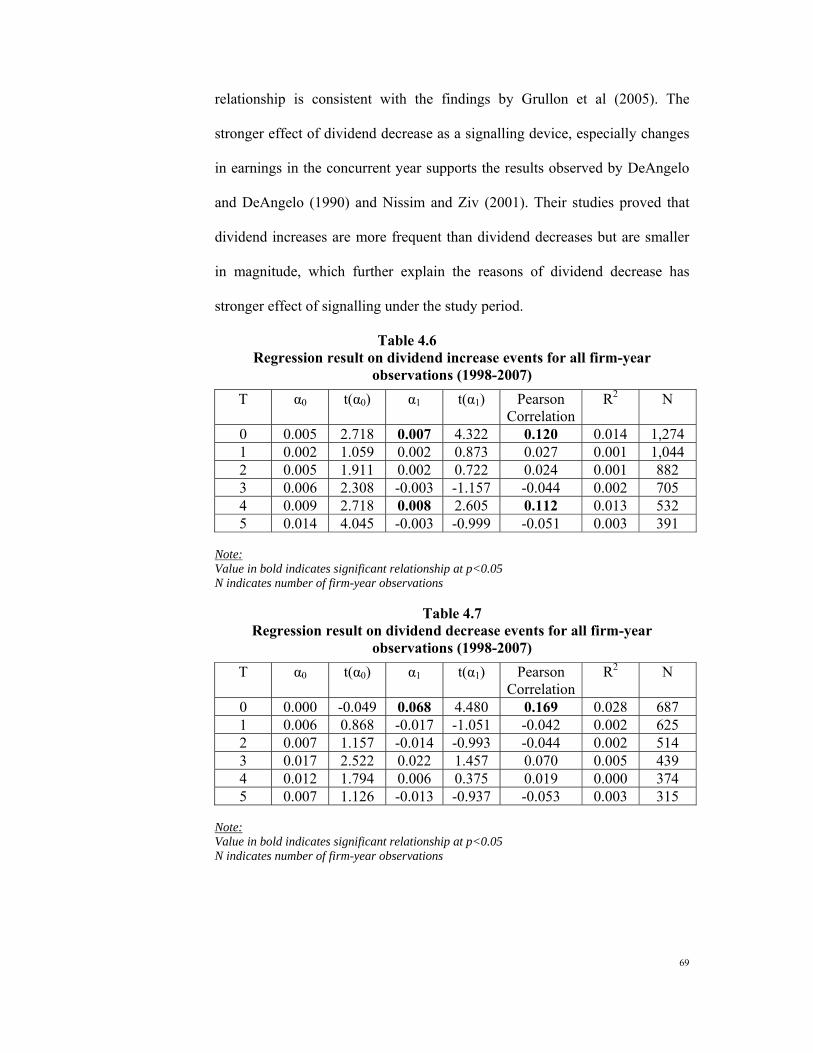

Regression result on dividend increase events for all firm-year observations (1998-2007)………………………………………….. 69

Table 4.7

Regression result on dividend decrease events for all firm-year observations (1998-2007)…………………………………………. 69

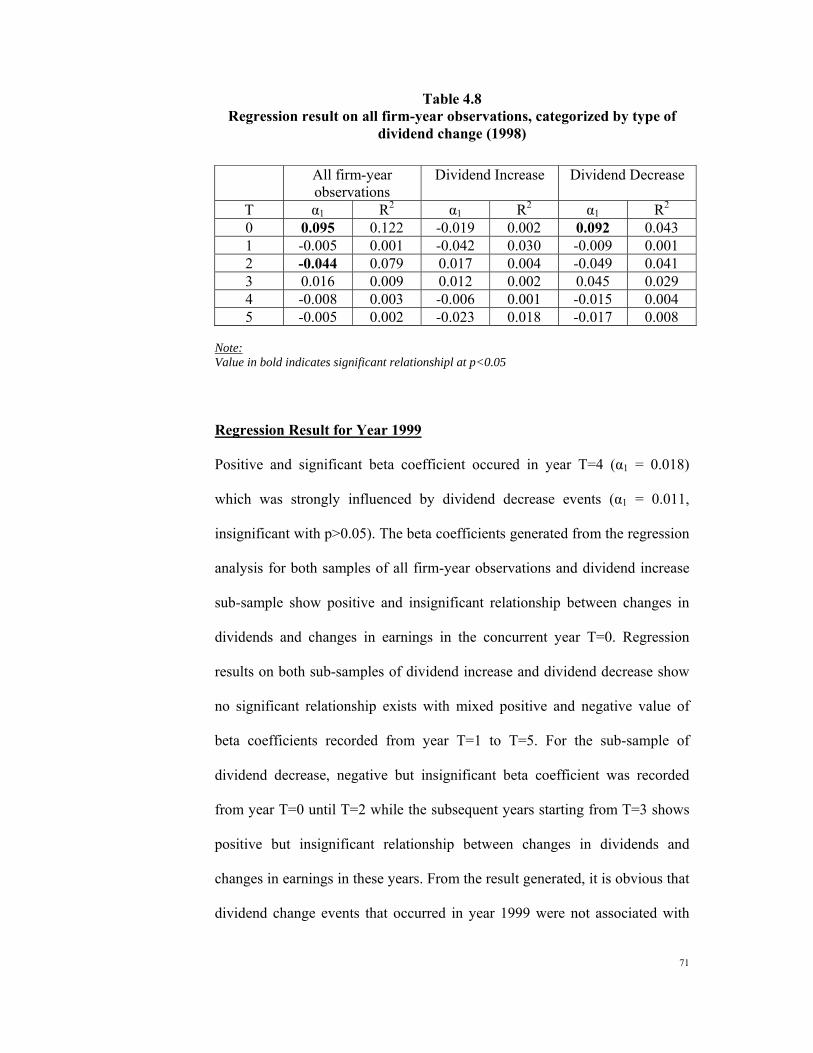

Table 4.8 Regression result on all firm-year observations, categorized by type of dividend change (1998)……………………………………. 71

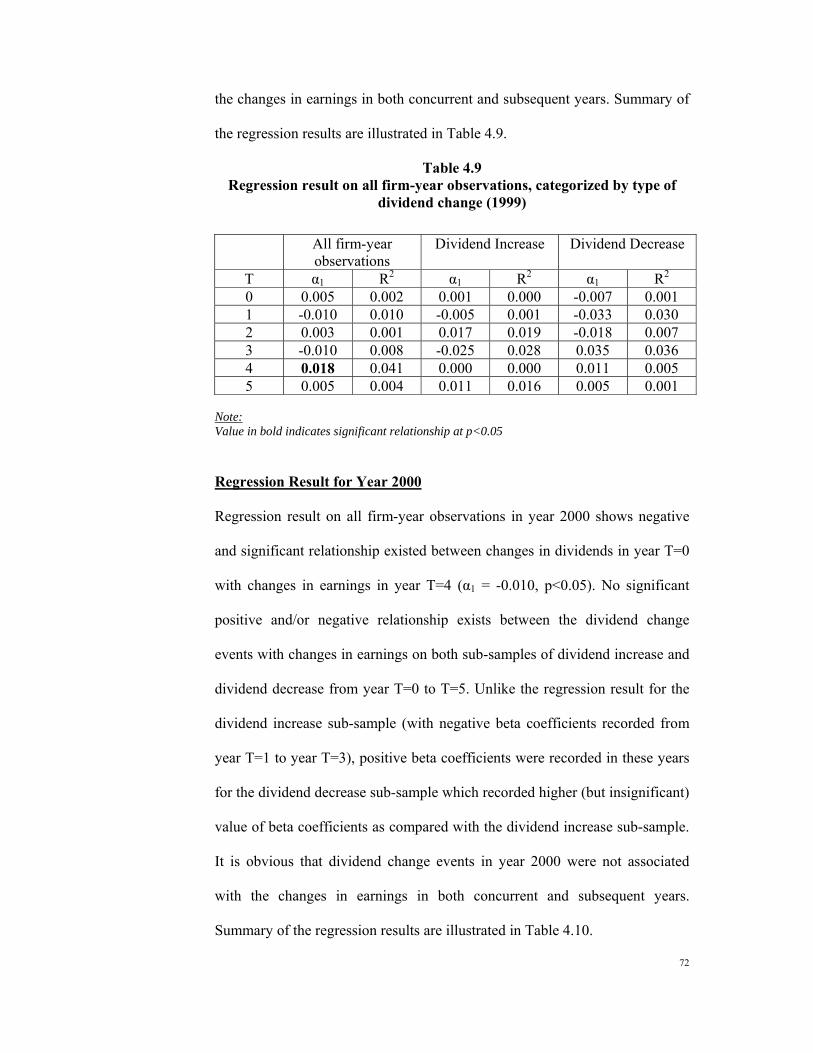

Table 4.9 Regression result on all firm-year observations, categorized by type of dividend change (1999)……………………………………. 72

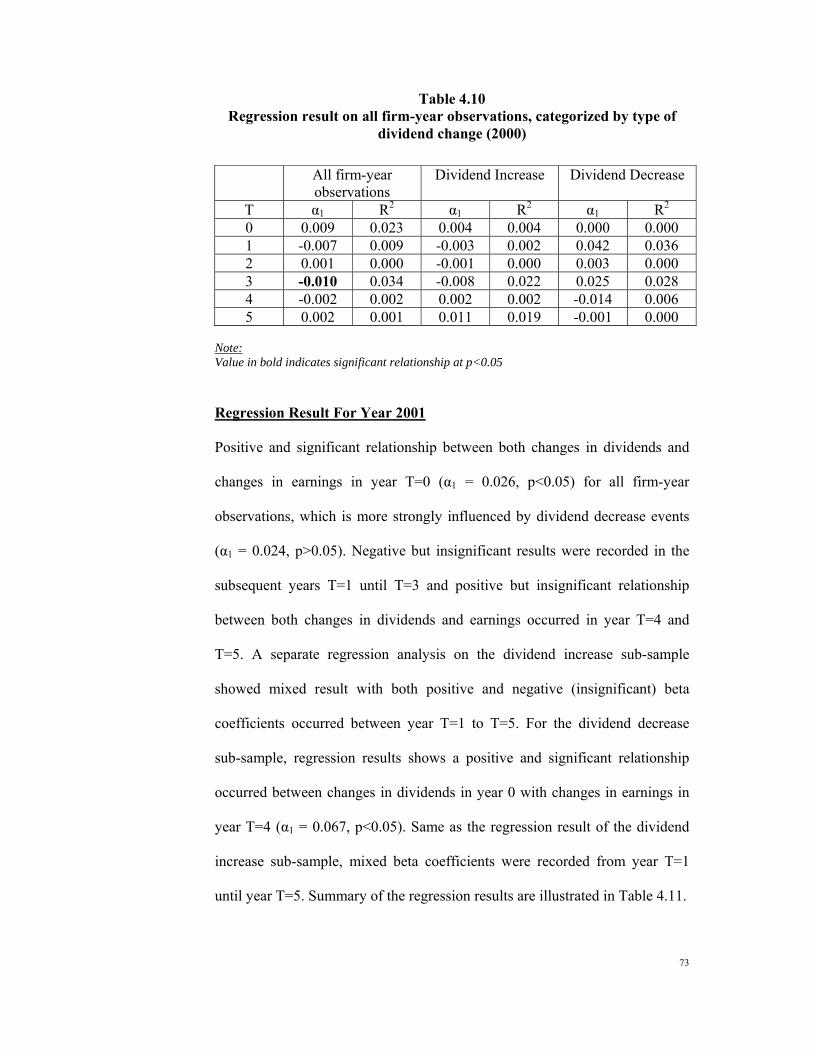

Table 4.10 Regression result on all firm-year observations, categorized by type of dividend change (2000)……………………………………. 73

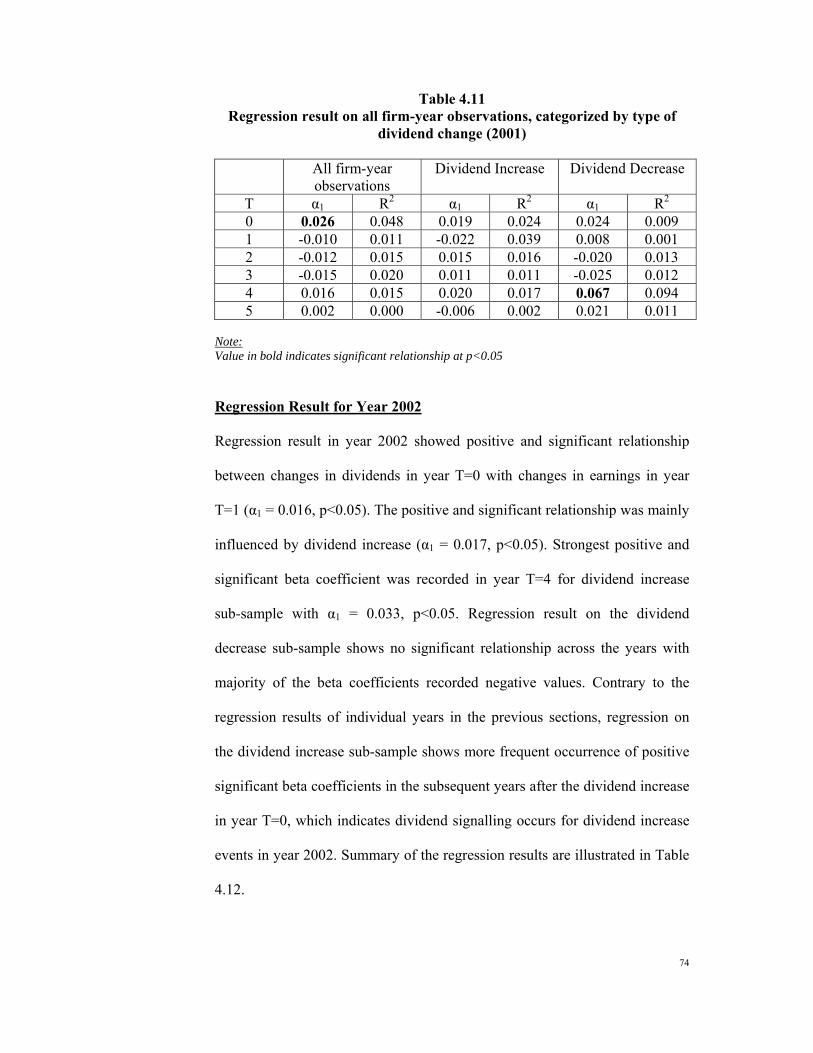

Table 4.11 Regression result on all firm-year observations, categorized by type of dividend change (2001)……………………………………. 74

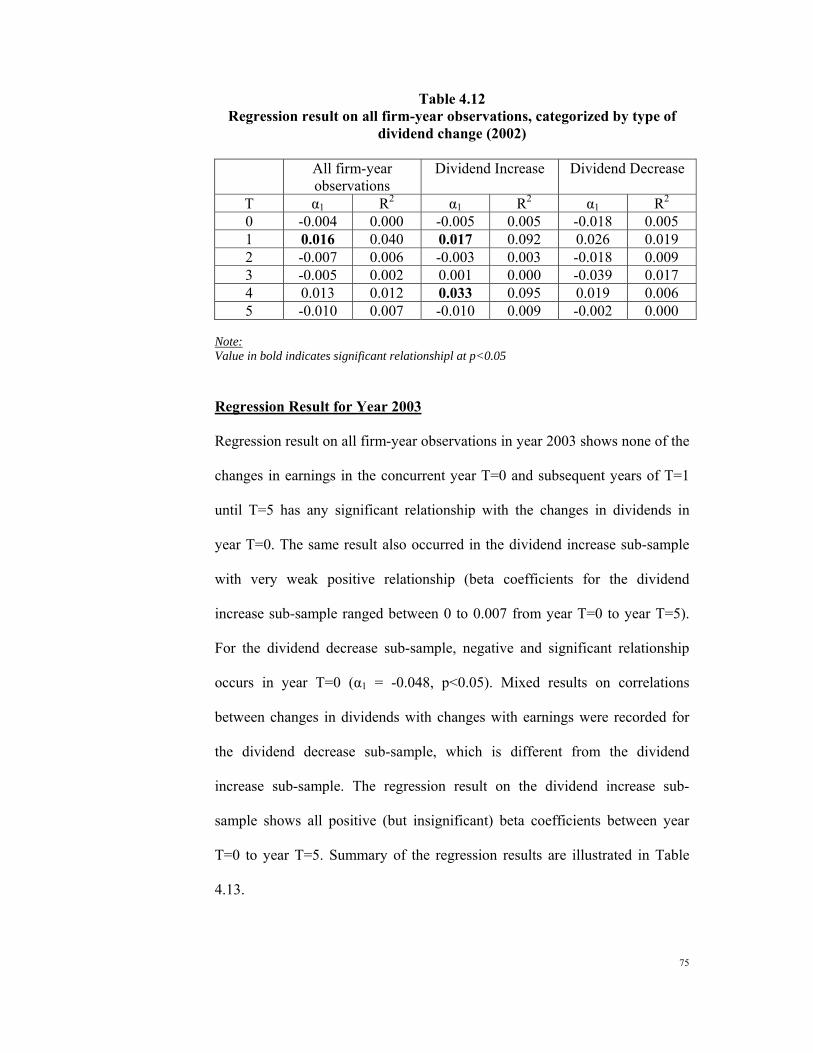

Table 4.12 Regression result on all firm-year observations, categorized by type of dividend change (2002)……………………………………. 75

vii

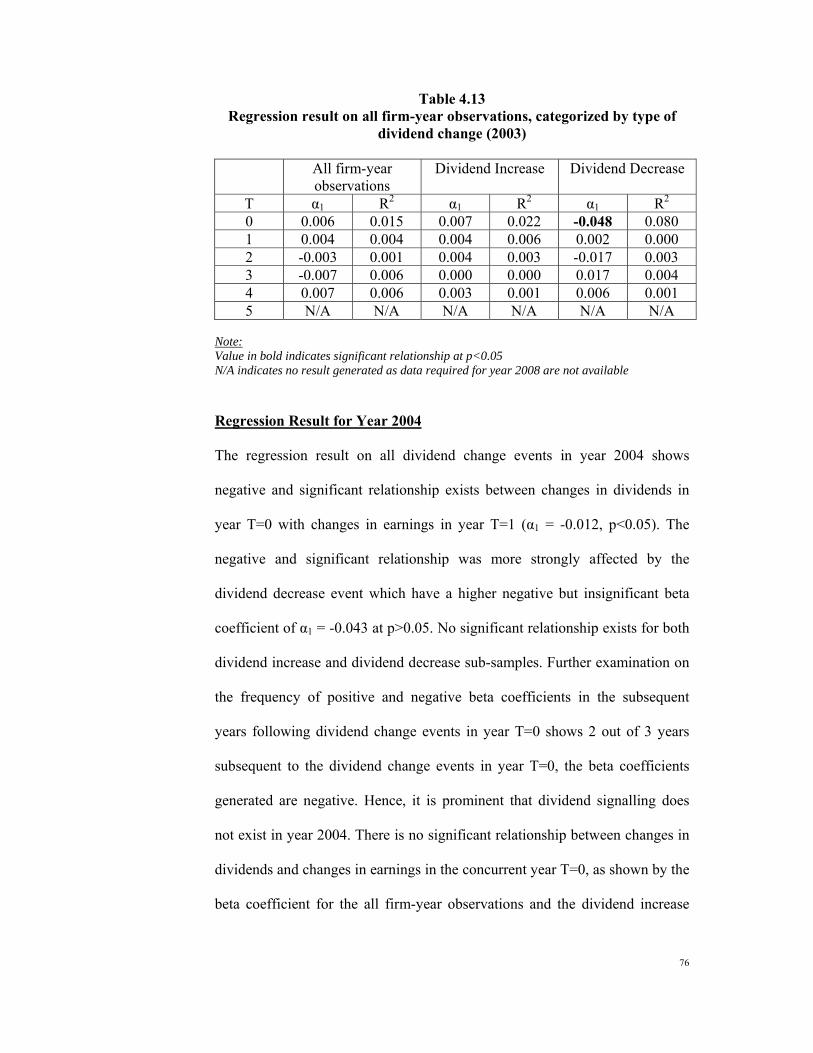

Table 4.13 Regression result on all firm-year observations, categorized by type of dividend change (2003)……………………………………. 76

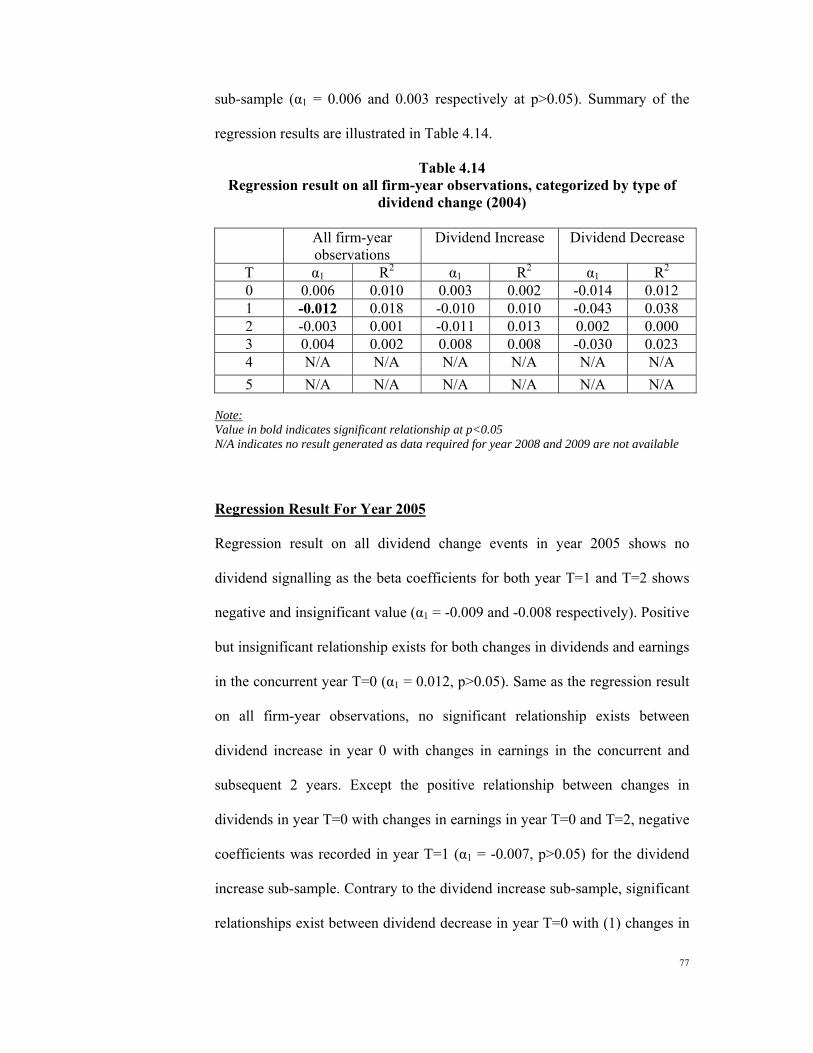

Table 4.14 Regression result on all firm-year observations, categorized by type of dividend change (2004)……………………………………. 77

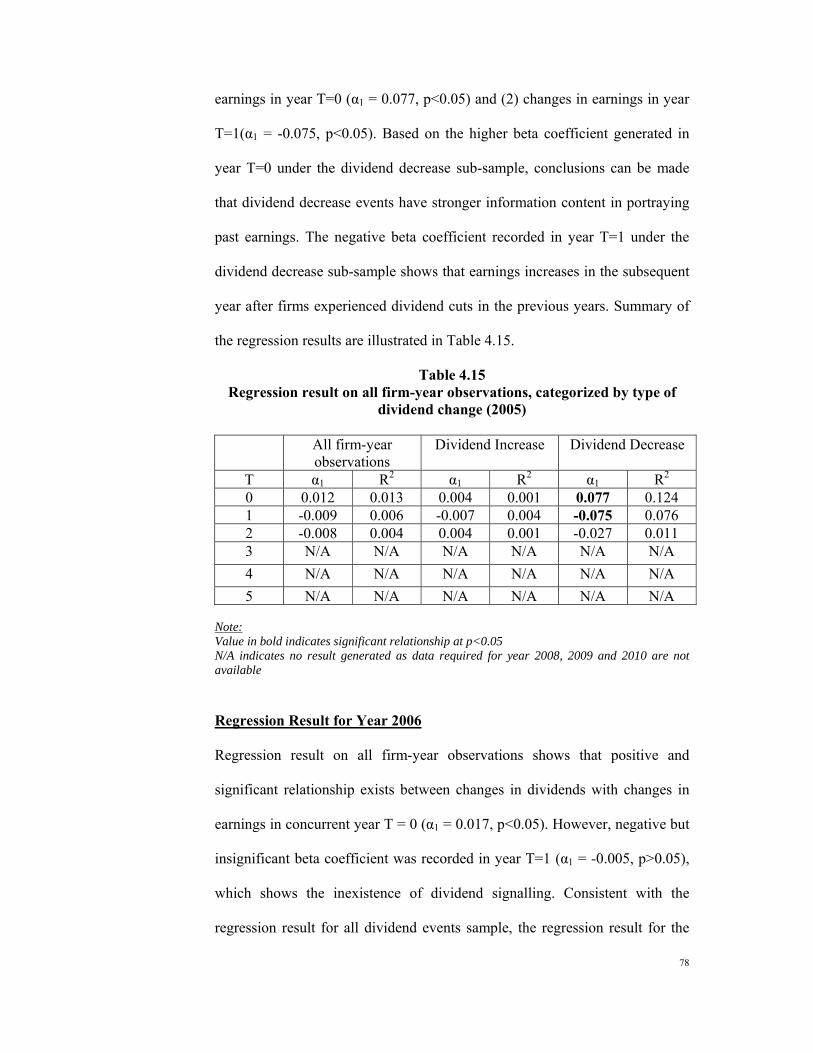

Table 4.15 Regression result on all firm-year observations, categorized by type of dividend change (2005)……………………………………. 78

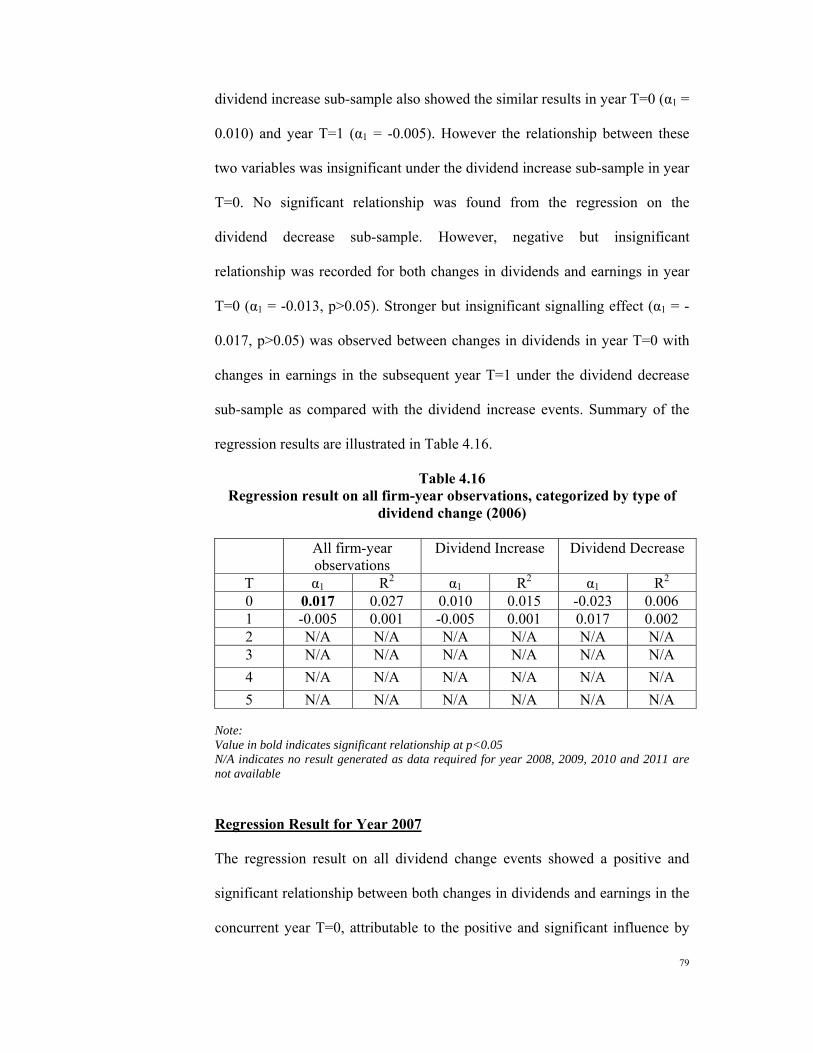

Table 4.16 Regression result on all firm-year observations, categorized by type of dividend change (2006)……………………………………. 79

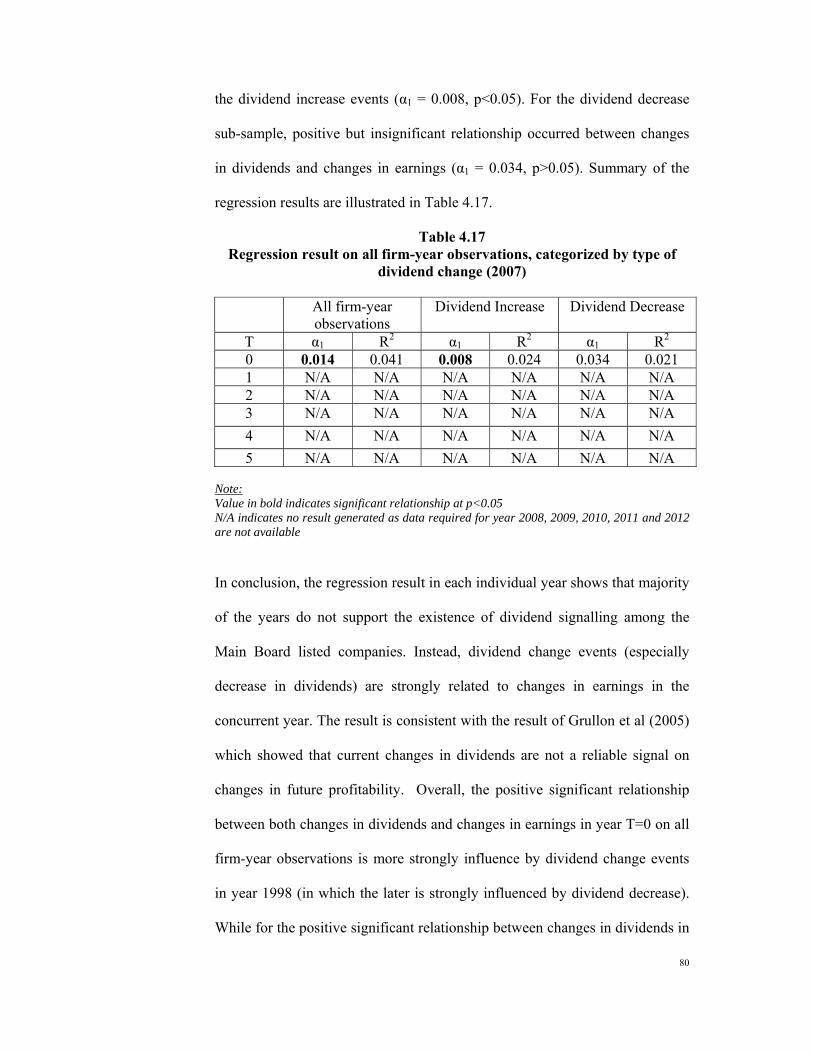

Table 4.17 Regression result on all firm-year observations, categorized by type of dividend change (2007)……………………………………. 80

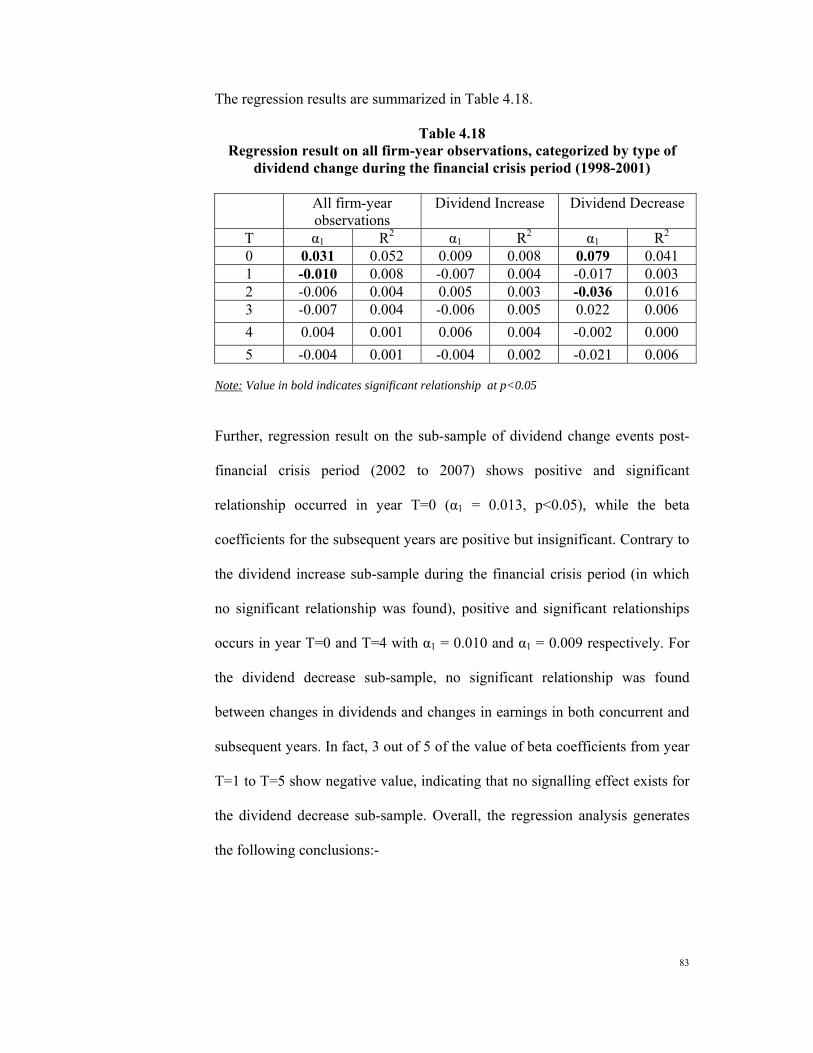

Table 4.18 Regression result on all firm-year observations categorized by type of dividend change during the financial crisis period (1998-2001).. 83

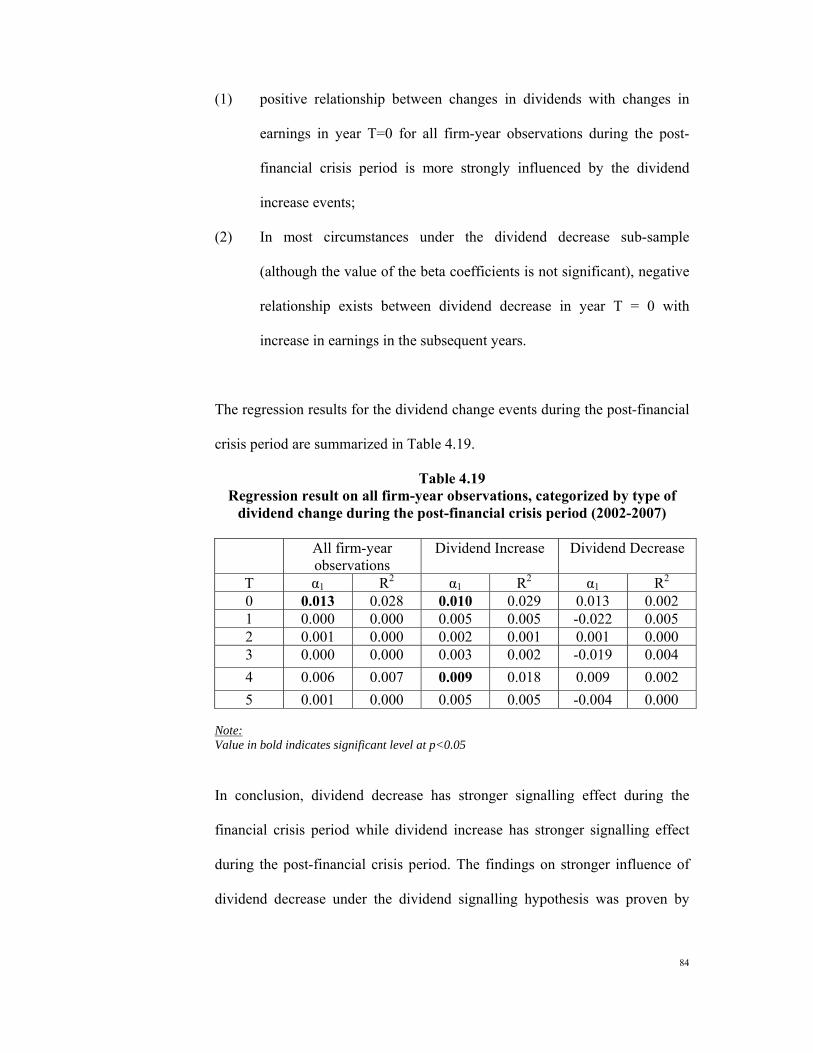

Table 4.19 Regression result on all firm-year observations categorized by type of dividend change during the post- financial crisis period (2002-2007)……………………………………………………………….. 84

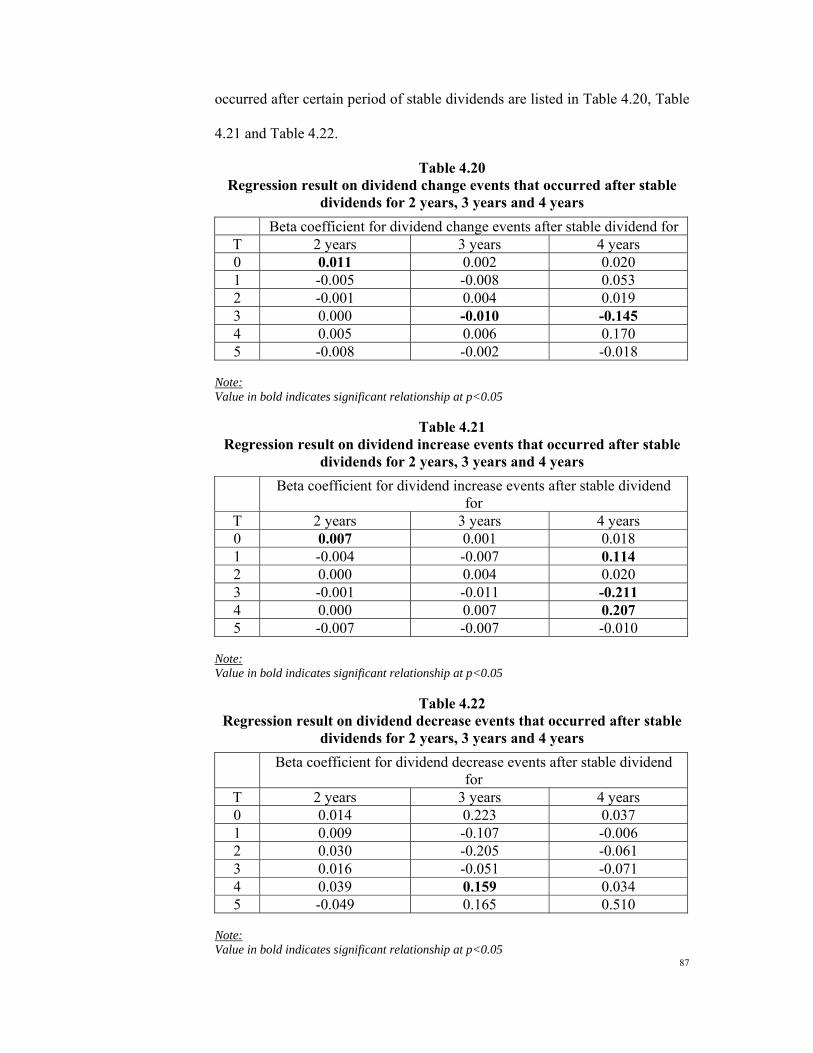

Table 4.20 Regression result on dividend change events that occurred after stable dividends for 2 years, 3 years and 4 years………………….. 87

Table 4.21 Regression result on dividend increase events that occurred after stable dividends for 2 years, 3 years and 4 years………………….. 87

Table 4.22 Regression result on dividend decrease events that occurred after stable dividends for 2 years, 3 years and 4 years………………….. 87

Table 4.23

Summary on the regression result for dividend change events categorized by different sizes of dividend change………………… 88

Table 4.24 Summary on the regression result for dividend change events categorised by different sizes of dividend yield…………………… 90

Table 4.25 Multiple regression on all firm-year observations controlled by industry effect: Industrial sector as base………………………….. 93

Table 4.26 Multiple regression on all firm-year observations controlled by industry effect: Trading / Services sector as base………………… 93

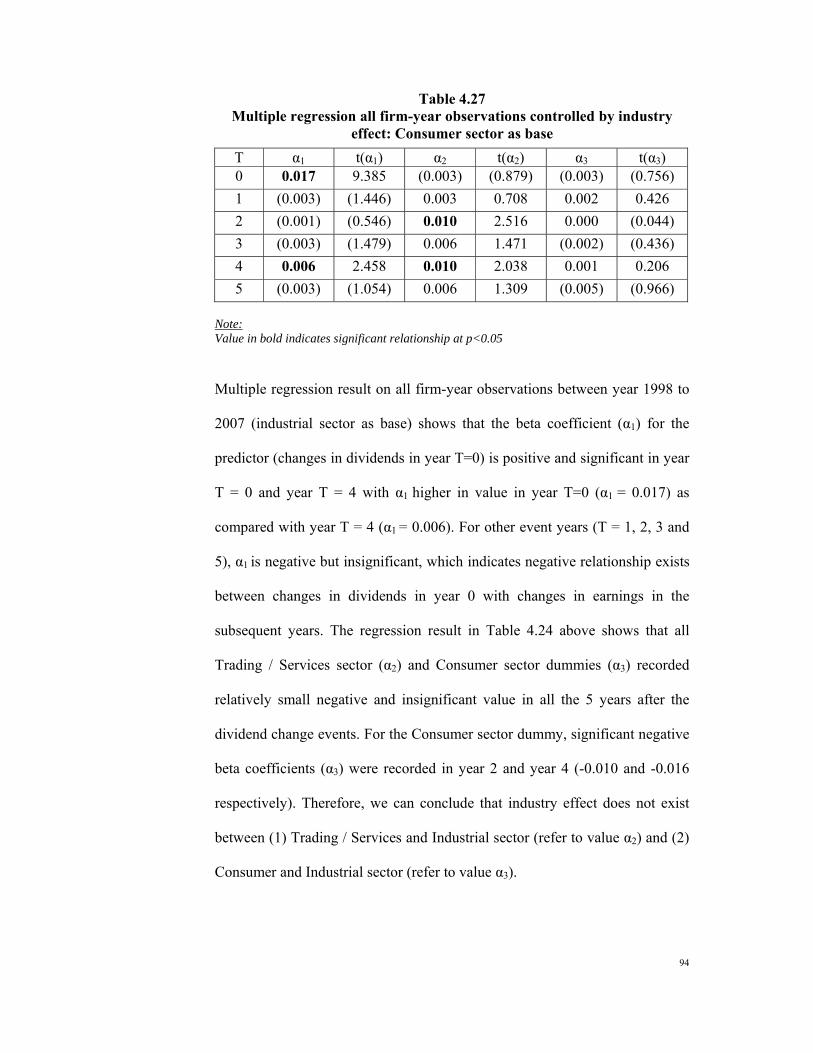

Table 4.27 Multiple regression on all firm-year observations controlled by industry effect: Consumer sector as base………………………….. 94

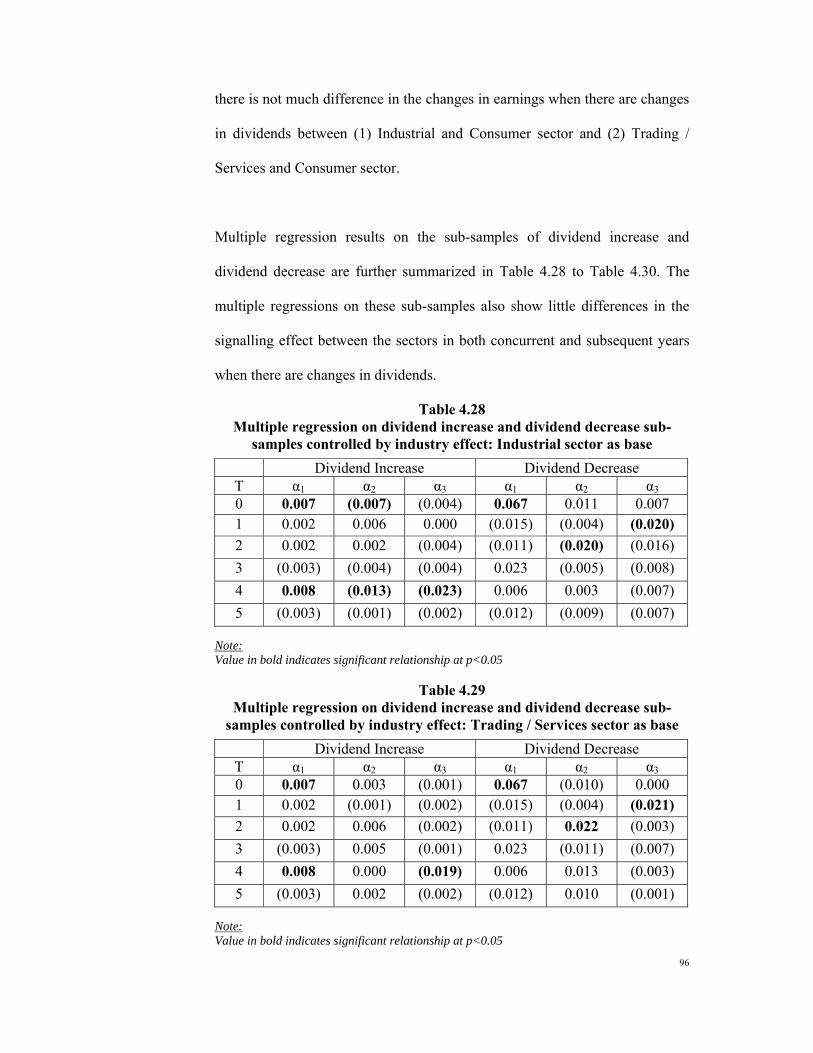

Table 4.28 Multiple regression on dividend increase and dividend decrease sub-samples controlled by industry effect: Industrial sector as base 96

Table 4.29 Multiple regression on dividend increase and dividend decrease sub-samples controlled by industry effect: Trading / Services sector as base………………………………………………………. 96

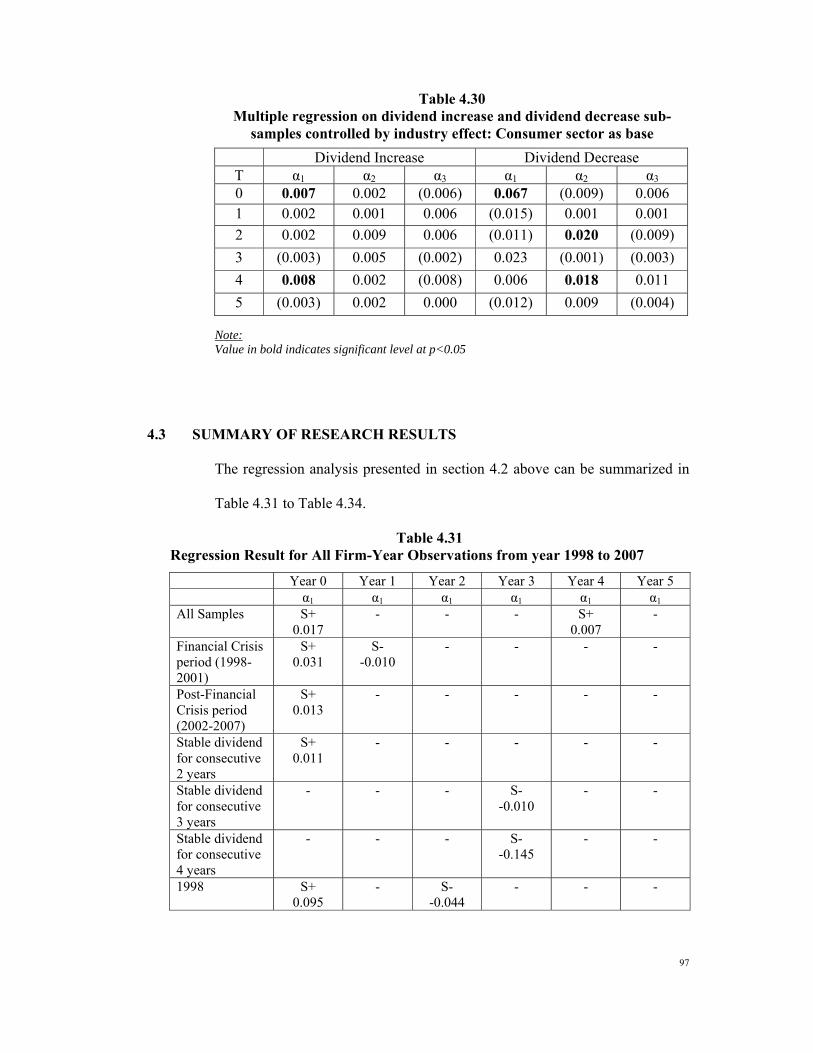

Table 4.30 Multiple regression on dividend increase and dividend decrease sub-samples controlled by industry effect: Consumer sector as base………………………………………………………………… 97

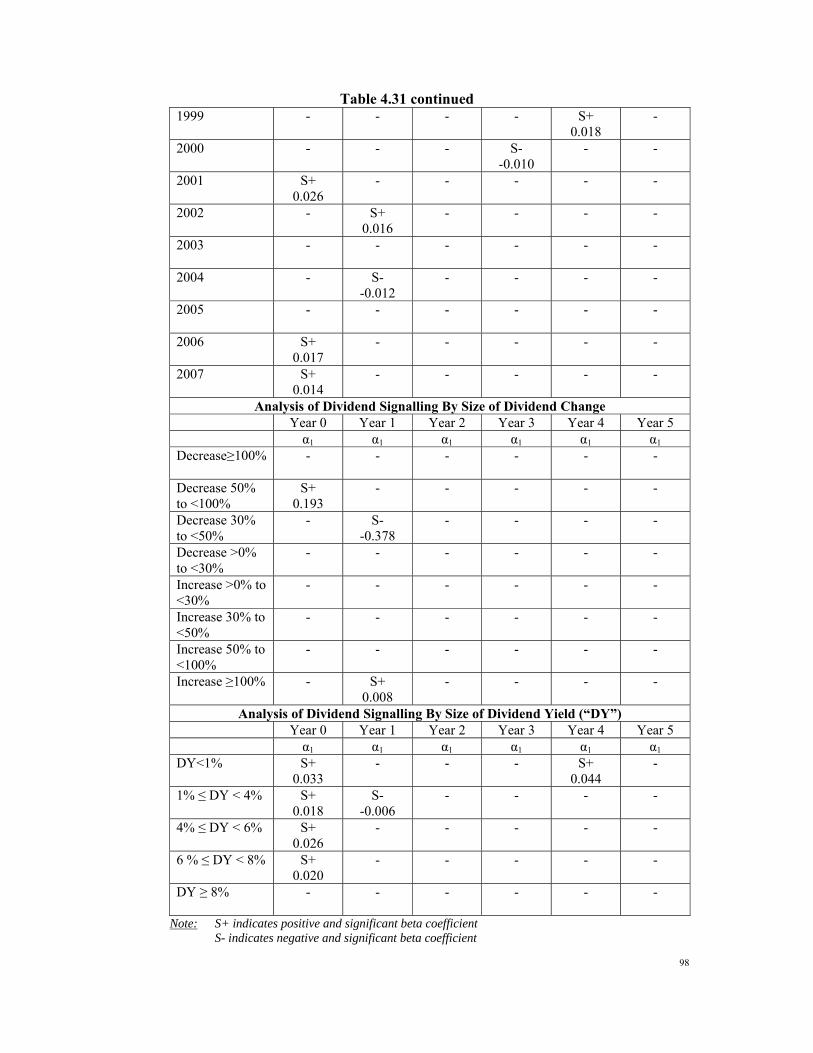

Table 4.31 Regression result for all firm-year observations from year 1998 to 2007………………………………………………………………... 97

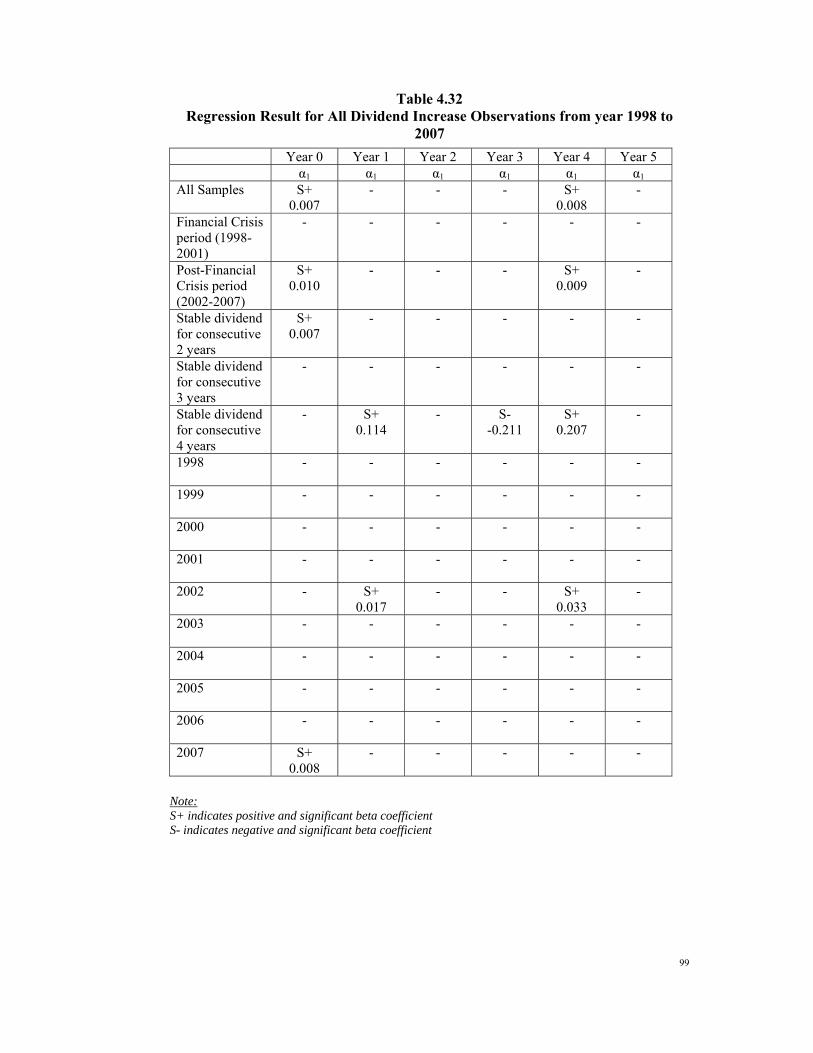

Table 4.32 Regression result for all dividend increase observations from year 1998 to 2007……………………………………………………….. 99

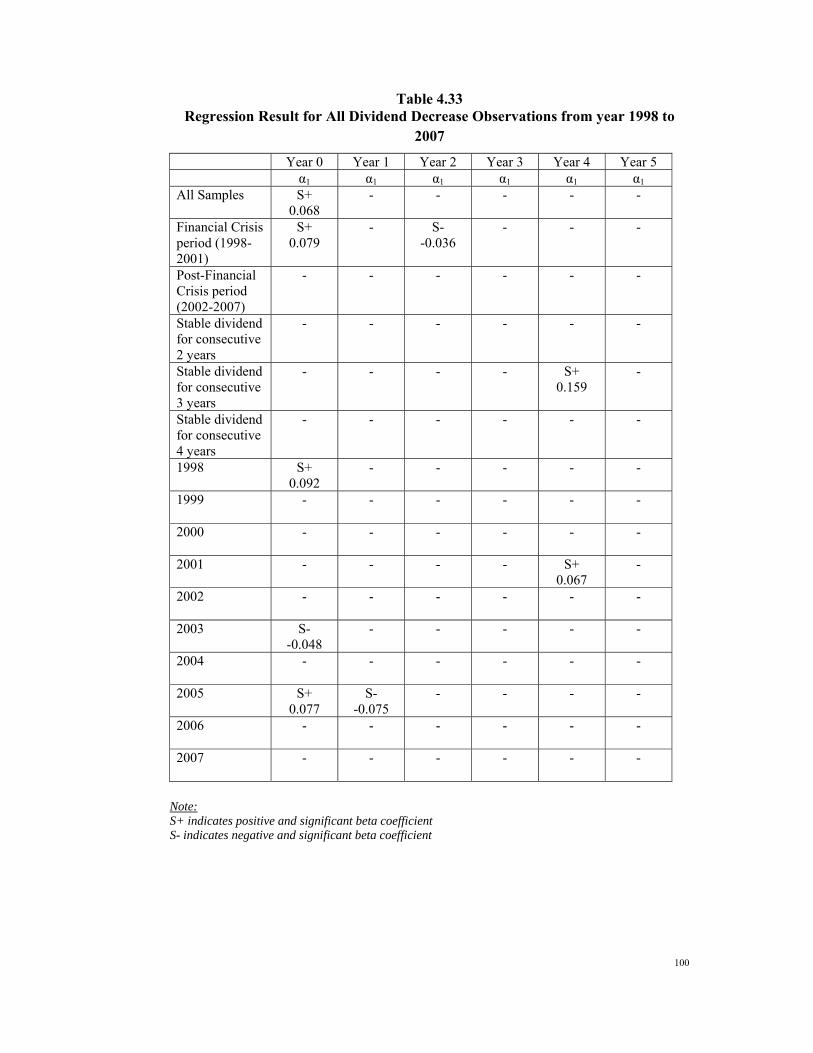

Table 4.33 Regression result for all dividend decrease observations from year 1998 to 2007……………………………………………………….. 100

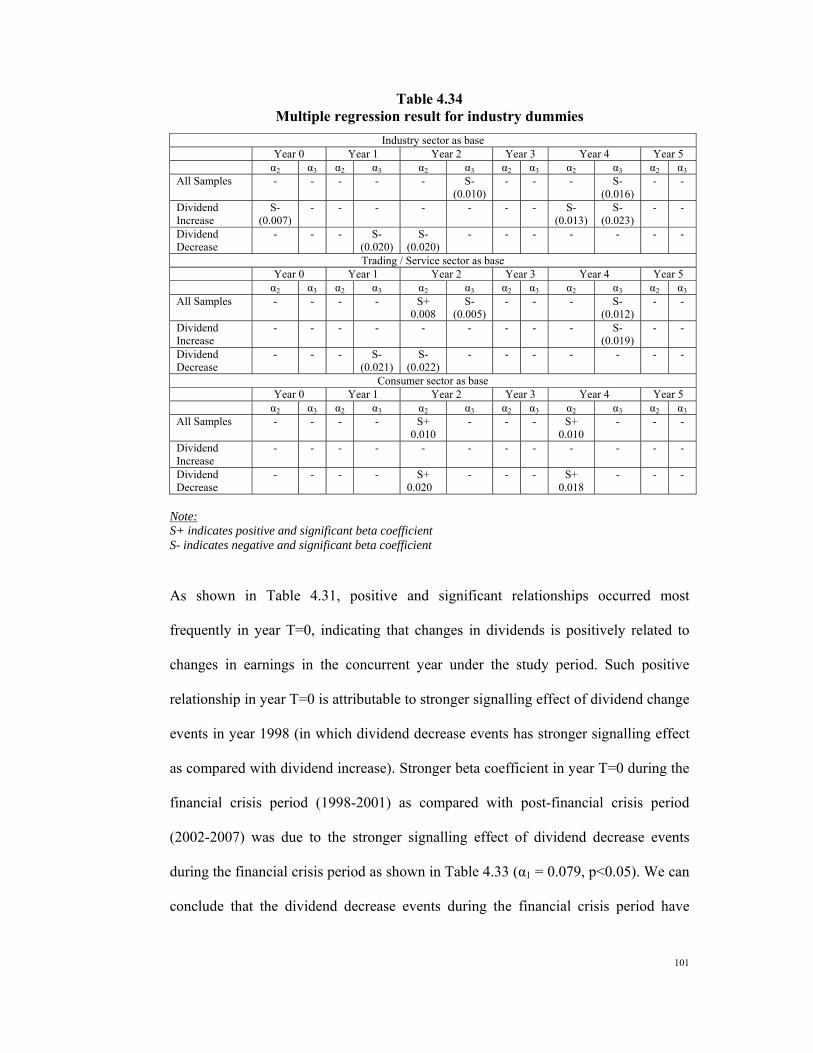

Table 4.34 Multiple regression result for industry dummies………………….. 101

viii

LIST OF SYMBOLS AND ABBREVIATIONS The symbols and abbreviations used in this research paper and the definition of each

are illustrated below:

UE i,t : Unexpected earnings of firm i in year t E i,t : Earnings of firm i in year t MV i,0 : Market value of equity of firm i on the 1st trading day of the

announcement year EPS i,t : Earnings per share of firm i in year t P i,0 : Share price of firm i at the beginning of dividend change year

0. ∆ EPS i,t : Changes in earnings per share of firm i in year t ∆ Div i,t : Changes in dividend per share of firm i in year 0 D i,0 : Dividend per share of firm i in year t REITS : Real Estate Investment Trusts PN4 : Practice Note 4, as per Bursa Malaysia’s published practice

notes for listed companies (repealed and deleted with effect from 3 January 2005). Listed companies categorized under PN4 are companies with financial condition that does not justify continued trading and/or listing.

PN17 : Practice Note 17, as per Bursa Malaysia’s published practice notes for listed companies. Listed companies categorized under PN17 are companies with financial condition and level of operations on a consolidated basis do not warrant continued trading and/or listing as follows:- (a) the shareholders’ equity on a consolidated basis is equal to

or less than 25% of the issued and paid-up capital of the company and such shareholders’ equity is less than the minimum issued and paid-up capital as required under Bursa Malaysia’s Listing Requirements;

(b) receivers and/or managers have been appointed over the asset of the company, its subsidiary or associated company which asset accounts for at least 50% of the total assets employed of the company on a consolidated basis;

ix

(c) a winding up of the company’s subsidiary or associated company which accounts for at least 50% of the total assets employed of the company on a consolidated basis;

(d) the auditors have expressed an adverse or disclaimer opinion in the company’s latest audited accounts;

(e) the auditors have expressed a modified opinion with emphasis on the company’s going concern in the company’s latest audited accounts and the shareholders’ equity on a consolidated basis is equal to or less than 50% of the issued and paid-up capital of the company;

(f) a default in payment by the company, its major subsidiary or major associated company and the company is unable to provide a solvency declaration to Bursa Malaysia.

(g) the company has suspended or ceased:- (i) all of its business or its major business; or (ii) its entire or major operations, for reasons of:- (aa) the cancellation, loss or non-renewal of a licence,

concession or other rights necessary to conduct its business activities;

(bb) the disposal of the company's business or major business; or

(cc) a court order or judgment obtained against the company prohibiting the company from conducting its major operations on grounds of infringement of copyright of products etc; or

(h) the company has an insignificant business or operations IPC : Infrastructure Project Companies α0 : Constant term in the regression equation, represents the

intercept of the regression line on axis Y (dependent variables) when the value of X (independent variable) is equal to zero

α1, α2, α3…. and any other subsequent alpha values

: Beta coefficient for the independent variable and any other subsequent independent variables in the regression equation, measured on the effect of changes in independent variables on the dependent variables

∈T : Error term in the regression DPS : Dividend per share EPS : Earnings per share DPR : Dividend payout ratio which shows how much dividend is

payout from every Ringgit Malaysia of EPS. The formula for dividend payout ratio is DPS / EPS

x

DY : Dividend yield which measures how much cash flow an investor can get for each Ringgit Malaysia invested in the share of a company. The formula for dividend yield is DPS / Price per share.

1

CHAPTER 1: INTRODUCTION

1.1 PURPOSE AND SIGNIFICANCE OF THE STUDY

Dividend policy has become one of the major areas of research amongst the finance

scholars since 1950s. It is obvious from the research results of these scholars that

dividend decision is the most elusive and controversial in financial decision making,

hence remained unsolved with puzzles (Black, 1976). The dividend decision of a

company involves retaining a proportion of net earnings for investment needs in the

future while distributing the rest as dividend to shareholders. A good dividend policy

not only attracts investors and facilitates fund raising from the stock market; it also

caters for the future investment needs of the company. The association between

dividend decision, earnings and future investment needs therefore makes dividend

announcement a source of information to the investors in accessing the future

prospects of a company. In other words, dividend “signals” information to investors.

Majority of the studies on dividend signalling of corporations in developed markets

e.g. United States and Europe concluded with mixed results with some level of

controversial in the theory of dividend signalling. Researchers who support the theory

of dividend signalling claimed that the signalling effect from dividend announcements

help to overcome informational asymmetries between the management of a company

and investors who are less informed about the financial prospects of the company.

Investors may view an increase in dividend payout as a signal that the company has

sufficient future cash flows to meet its debt and dividend payment in the future. Such

positive signal will stimulate positive reaction from investors and further cause an

increase in the share price. (Handjinicolaou and Kalay, 1984). However, there are

2

also findings that showed dividend signalling does not exist, especially in an efficient

market.

The research findings in the developed market may not applicable in Malaysia in view

of different firm characteristics such as ownership structure (Mancinelli and Ozkan,

2006), investment decision of firms (Fama, 1974) as well as the industry and market

`characteristics differentiated by industry classification (Baker, 1998). Therefore, this

research study is to examine whether Malaysian Main Board listed companies use

dividend changes to signal their future financial prospects, i.e. earnings of the

companies to the investors.

1.2 OBJECTIVE AND SCOPE OF THE STUDY

The objective of this research is to test whether dividend signalling applies in

Malaysia, given the fact that most previous studies on dividend signalling were

conducted in developed countries. Given the mixed results on dividend signalling in

developed countries, the study on dividend signalling in the context of Malaysia is

interesting due to different market structure, legal enforcement and ownership

structure in the Malaysian stock market. Hence, the objectives of this study are

generally as follows:-

(1) To study whether Main Board companies in Bursa Malaysia use changes in

dividend to convey earnings prospect of the companies

(2) To examine the effect of dividend signalling in the subsequent 5 years

following the changes in dividend, should dividend signalling is proven to

exist amongst the Main Board companies in Bursa Malaysia. In other words,

3

the research will examine whether the signalling effect becomes stronger

(weaker) in subsequent years following the dividend change events.

(3) To examine whether the dividend signalling effect becomes stronger when

companies change their dividend policy after some period of stable dividend.

(4) The scope of study is further extended to examine whether the larger the

change in dividend, the stronger the signalling effect based on the behavioural

norms of investors who are more concerned with larger changes as compared

with smaller and insignificant changes in dividends,

(5) To examine the clientele effect by creating the linkage between dividend yield

and dividend signalling. Companies with higher dividend yield will place

more emphasis on dividend in their share valuations as compared with

companies with low dividend yield.

(6) To examine the “industry effect” or “peer group effect” in dividend signalling

hypothesis. Under such industry or peer group effect, a firm will adjust their

dividend decisions “to conform with the industry dividend practices” (Baker

and Powell, 2000; Baker, Veit, and Powell, 2001).

This scope of this research paper is generally to examine whether managers use

changes in dividends to signal future prospects to the investing public i.e. increase

(decrease) in earnings in the subsequent years following changes in dividends to the

investing public. The relationship between changes dividends and changes earnings is

tested by focusing the relationship between dividend changes in year 0 with future

earnings changes in the concurrent (year 0) and subsequent 5 years following the

dividend changes (year 1 to year 5) of the companies listed on the Main Board of

Bursa Malaysia.

4

1.3 LIMITATION OF THE STUDY In studying the information content of dividend, changes in future earnings (following

changes in dividends), in some extent may take into account the effect of changes in

earnings in the current year. In Malaysian stock market, the announcements of

dividends and earnings are make simultaneously via the release of annual reports to

the public investors. As highlighted by Aharory and Swary (1980), the major

difficulty in studying the information content of dividend is the synchronization of

dividend and earnings announcement.

The study may not cover adequate width of studies, i.e. the size and pool of the

sample is smaller and may not sufficient for the testing of dividend signalling

hypothesis as compared with the previous studies conducted in more established stock

exchange. The smaller sample with fewer number of dividend paying companies in

each sector is due to the fact that Malaysian stock market is considered as a

developing stock market with smaller number of listed companies. Furthermore, the

number of Main Board listed companies is further eliminate in the filtering process as

(1) some companies did not pay dividends consistently throughout the years; and (2)

companies with incomplete financial information on dividends and earnings are

further eliminated from the study.

The Ordinary Least Square Regression (OLS Regression) adopted in this study has its

limitations in terms of the violation of a host of auxiliary assumptions. For instance,

the error terms in the regression equation might be (1) correlated and may not concern

the effect of outliers or (2) obtained poorly behaved error terms on estimates.

Moreover, the outcome of the OLS Regression might be skewed i.e. when the

5

unexpected earnings distribution has “fat-tails” and is heavily right skewed, the

estimates generated by the OLS Regression will be driven by the data in the tails of

the unexpected earnings distribution.

Signalling theory has limitations in the form of monotonous restriction (Bernhardt,

Douglas and Robertson, 2005) by “averaging” across the changes in dividend signals,

but in fact there are many factors which can influence the result. The problem arises

when there are larger reductions in dividend signal (Bernhardt, et. al, 2005).

1.4 ORGANISATION OF THE STUDY

The study on the dividend signalling of Main Board listed companies in Bursa

Malaysia is presented in the subsequent sections. Chapter 2 summarizes the result of

the studies done by the past scholars and researchers on dividend theories and

dividend signalling. Chapter 3 explains the methodologies adopted in this research

study which include the hypotheses being tested, measurements and formulas of the

variables in the study, sampling design, data collection procedures and data analysis

techniques. Chapter 4 presents the descriptive summaries of the sample and the results

of the analysis. Chapter 5 concludes the research findings and suggests for the

possible area for future research. Chapter 6 lists down all the references in relation to

this research study.

6

CHAPTER 2: LITERATURE REVIEW

2.1 WHAT IS DIVIDEND POLICY

Dividend can be defined as distribution or payment in either cash or shares to the

shareholders of the company out of the firms’ earnings (Ross, Westerfield and Jordan,

2003; Investopedia online). The decision on the amount of net earnings to be paid out

as dividend to the shareholders involves several factors to be considered such as the

firm’s current earnings, future investment needs, cash flow position, shareholders’

preferences (or composition of shareholders), market sentiment as well as dividend

decisions of other companies within the same industry. Due to the complexities

involved in dividend decision, such decision is normally determined by the top

management of the company such as chief financial officers, treasurers and board of

directors.

Dividend policy is a payout matter considered by firms in relation to when, how much

of the net earnings to be payout as dividends and in what forms the dividends to be

paid. In simpler context, dividend policy relates to the time pattern of dividend payout

(Ross et al, 2003) and is determined by the changes in earnings, after taking into

consideration of investment decisions (Lumby and Jones, 1981). We refer such

condition as “residual dividend policy”. High-growth firms will not pay out large

portion of their earnings as dividends, in view of the requirement to sustain higher

than average growth (Investopedia online). In fact, firms that increase dividends are

found to be larger and more profitable than firms that cut or maintain their dividends

(Grullon, Michaely, Benartzi and Thaler, 2005). Although dividend increase is more

frequent than dividend decrease, dividend increase is smaller in magnitude than

7

dividend decrease (DeAngelo and DeAngelo, 1990; Nissim and Ziv, 2001).

There are some studies conducted on the pattern of dividend payout in other countries,

i.e. companies in the United States distribute large part of their earnings as dividends

and try to maintain a stable dividend policy. The establishment of dividend in these

companies is in accordance with the level of current earnings as well as dividends in

previous years (Lintner, 1956). However, dividend policy in emerging markets had

showed some level of differences with developed markets in which the former

pursued less stable dividend policy with lower payout ratio (Glen, Karmokolias,

Miller and Shah, 1995). But there are also cases in which Asian companies in India

and Singapore pursue a stable dividend policy (Pandey and Bhat, 1994; Ariff and

Johnson, 1994).

Many studies were conducted on the dividend policy in Malaysia. Studies in the

1990’s showed that the dividend behavior of Malaysian companies was stable and

confirmed the applicability of the Lintner model in Malaysia (Isa, 1992; Annuar and

Shamser, 1993; Gupta and Lok, 1995; Kester and Isa, 1996). However, subsequent

studies showed that dividend behavior of Malaysin companies was sensitive to

dividend changes (pursued less stable dividend policy) but do not immediately omit

dividends when earnings decreased (Pandey, 2001). Pandey (2001)’s result was

consistent with study done by DeAngelo and DeAngelo (1990), Michaely, Thaler and

Womack (1995), Nissim and Ziv (2001) and Grullon et al (2005) which showed that

dividend cuts are less common than dividend increase and more extreme in magnitude.

Following Pandey’s studies, Al-Twaijry (2007) tested the relationship between DPS

and EPS of listed companies in the Bursa Malaysia and concluded that companies

8

follow dividend policies which are not strongly attached to current earnings and

negative (but insignificant) relationship was found between dividend payout ratio and

future earnings.

The following section elaborates on dividend related theories, namely the (1) dividend

irrelevance theory, (2) agency theory, (3) information asymmetry, (4) Bird-in-Hand

fallacy and (5) clientele effect.

(a) Dividend Irrelevance Theory

According to Miller and Modigliani (1961), the pattern of dividend is

irrelevant and therefore the value and the investment decisions of a firm are

independent from dividend policy in a (1) perfect and efficient market and (2)

a world without taxes and transaction costs. Under the dividend irrelevance

theory, a firm is free to determine any dividend policy in a free of tax

environment without affecting the stream of cash flows or value of the firm in

the following manner:-

(i) Pay dividend in excess of cash flows from operations and issue new

equities to finance for the dividend payment

(ii) Pay dividend less than the cash flows from operations after making

investments and the excess cash flows after paying dividends will be

used to repurchase shares (Copeland and Weston, 1988)

Under the dividend irrelevance theory, the pattern of cash flows provided by a

company through the payment of dividends is irrelevant as shareholders are

free to adjust the dividend patterns to suit their desired consumption patterns

9

through the capital market (Lumby and Jones, 1981). As dividend is irrelevant

in enhancing shareholders’ wealth in a perfect capital market, the only source

to enhance shareholders’ value is through the investment decision alone.

(b) The Bird-in-Hand Fallacy

Under the theory of Bird-in-Hand fallacy, risk-averse investors prefer

dividends as compared to capital gains due to the uncertainties inherent with

capital gains. However, there are a few arguments to this Bird-in-Hand Fallacy

due to the following reasons:-

(i) The choices between current dividends and the current share price

appreciation. When dividend payment is announced by the company,

share price of the company drops slightly lower than the dividend on

the ex-dividend day.

(ii) When firm increases its dividend without changing its investment

policy, dividend payment has to be financed by issuing new shares and

hence the increase in dividend payment is offset by losing an amount

equivalent to the present value of price appreciation (Damodaran,

2001). As the risk of the firm is determined by the risk of the project

cash flow, a decrease in dividend means greater investments and

higher risk and therefore increase in the market rates of return (higher

share price) (Copeland and Weston, 1988).

10

(c) Agency Theory

When there are differences in ownership and control of the company, agency

problem occurs. Managers as agents for shareholders must make their

decisions based on the objective of maximizing shareholders’ wealth. In order

to ensure their decisions are in line with the objective of maximization of

shareholders’ wealth, shareholders will incur nontrivial monitoring costs.

However, pursuing such monitoring action will create “trade-off” issue for

both shareholders and managers. Shareholders will face the trade-off between

monitoring costs and the forms of compensation involved to encourage the

agents to act in the owners’ interest. At the same time, managers also face the

trade-off between maximizing shareholders’ value and its own personal

interests by pursuing non-pecuniary interest. Selfish managers may not pay

out dividends but utilize the funds for personal compensation when the firms

are making profits. Therefore, increase in dividend payout can reduce agency

cost (Rozeff, 1982) as greater dividend payments serves as a mean in

monitoring and bonding the performance of managers. Greater dividend

payout may involve external financing i.e. through fund raising in the capital

markets and hence put the firm under greater scrutiny by the supplier of

capital besides the shareholders of the company. When a company is

controlled by a majority of insiders, there is less need to pay dividends to

reduce agency costs. At the contrary, agency cost will become higher when the

shareholding structure of a company is dispersed and hence higher dividend

payout (Rozeff, 1982).

11

(d) Clientele effect

Contrary with the assumptions of perfect capital market and a tax-free world

under the dividend irrelevance theory, the concept of clientele effect exists due

to imperfection in the capital market (e.g. transaction costs, difference in

interest rates and the presence of absolute capital rationing). The imperfection

in capital market will impose certain costs to shareholders when adjustments

in the dividend patterns are made to fit his preferred consumption pattern. In

such an imperfect capital market, simple wealth maximization may not be a

unique desire for the shareholders and therefore a continuous and stable

supply of dividend is viewed positively as a source of cash inflows to match

the desired consumption pattern of the shareholders (Lumby and Jones, 1981).

The fulfillment of the shareholders’ wealth creates a consequential cost to the

company as the company may leave with insufficient funds to finance for

profitable investments. Alternatively, the company has to finance its

investment needs from external resources which involve issuance cost. As

such, companies start to maintain stable dividend policy with the hope that the

stable dividend policy will not incur heavy cost penalties.

(e) Information asymmetry

The concept of information asymmetry is related to the differences in the

amount of information held by the management and the external shareholders.

The management, being the insiders of the company has more priori

information as compared with external shareholders who have limited access

to the information of the company. Due to such differences in a world of

asymmetry information, any changes in the dividend will be interpreted as a

12

costly signaling tool used by insiders of a company to convey information on

the firm’s future prospects (Bhattacharya, 1979; John and Williams, 1985;

Miller and Rock, 1985). The problem of information asymmetry is mitigated

when the ownership of a company becomes more concentrated, as such the

importance of dividend signalling is reduced (Vieira and Raposo, 2007).

Dividend policy of a firm can be measured using 2 methods: (1) dividend yield and

dividend payout ratio (Damodaran, 2001; Investopedia online). Changes in these 2

measures provide some information in relation to risks and future growth in earnings

of the company. Previous research studies showed that shares with high dividend

yields will result in excess returns, after adjusting for the market performance and risk

(Damodaran, 2001). Dividend payout ratio is used in estimating future dividends and

expected growth in earnings. When dividend payout ratio increases, the amount of

free cash flow decreases and fewer investments can be made from the available cash

flow, therefore the firm is expected to have lower growth in earnings. In other words,

high retention ratio (1-dividend payout ratio) will result in higher growth in earnings

(Damodaran, 2001).

2.2 THE DIVIDEND SIGNALLING THEORY

Dividend signalling theory suggests that dividend announcements convey information

on the firm’s future prospects (Investopedia online) by stimulating changes in share

prices which further generate returns to the shareholders. In other words, we refer this

as the “information content of dividend” as suggested by Miller and Modigliani

(1961). According to Miller and Modigliani, a company’s value is determined by its

13

expected future earnings and not on current earnings. If dividends are dependent on

the permanent component of the earnings, dividends would serve as a surrogate for

expected future earnings. The classic study on dividend signalling suggests that

current dividend is dependant on future as well as current and past earnings (Lintner,

1956). Although changes in dividends do contain some information to the investors,

dividend signalling is not universally applied to all firms (Chin, 2005).

An early study by John Lintner (1956) on dividend signalling showed that changes in

earnings will affect dividend payout and managers rarely change their dividend

payout in order to achieve the target payout ratio. Subsequent study by Fama and

Babiak (1968) also confirmed the findings by Lintner (1956) in which changes in

dividend lagged changes in earnings.

While early scholars suggested that firms use changes in dividends to convey

information on the firms’ financial prospects to the investors, some argued that firms

rarely change their dividends regardless of the earnings of the firm. The reasons of

such sticky dividend can be explained by 2 factors (Damodaran, 2001):-

(a) Concern of firms in maintaining higher dividends in the future; and

(b) Negative views on dividend decrease, which is associated with decrease in

share price

Based on the assertion of firms’ reluctant to change dividends, an increase in dividend

signals a favorable expectation on the firm’s future prospects and vice versa.

14

There are two important hypotheses related to the dividend signalling theory, namely

the free cash flow hypothesis and the maturity hypothesis. The free cash flow

hypothesis suggests that dividend signals information on investment policies of

overinvestment firms (Litzenberger and Ramaswamy, 1979). An increase in dividend

payment signals lack of investment opportunities for the firm and vice versa. The

maturity hypothesis suggests that an increase in dividend conveys information on

decreased investment opportunities, decreased return on assets and future earnings

growth rate as well as decrease in systematic risks. (Grullon, Michaely, Roni and

Swaminathan, 2002).

Using dividend as a mechanism to convey information on the firm’s profitability

involves signalling cost, especially in countries that impose taxation on both dividend

income and capital gains such as United States. When the cost of signalling becomes

higher due to higher tax rate imposed on dividend as compared to capital gains, an

increase in dividends will involve higher cost and therefore a higher return is required

to compensate for the cost of taxation involved (Brennan, 1970; Litzenberger and

Ramaswamy, 1979). In other words, firm value is more sensitive to a more costly

signal under the signalling model (Bernhardt et al, 2005). Contrary with Bernhardt’s

view, subsequent studies showed that market responses more favorably to dividend

increase when the tax rate on dividend is reduced, as experienced after the

implementation of the Tax Reform Act 1986.

The decision whether to use dividend to signal firm’s prospects to the investors may

be determined by the quality and characteristics of the firms. Firms with reputation

may rely on other lower cost communication channel rather than using dividend

15

signalling to convey information to the shareholders.

If changes in dividends signal information to the investors in an efficient capital

market, such changes will be reflected in the share prices of the firms immediately

after the dividend announcements. According to Fama (1970), a market is efficient

when it fully reflects all available information and is characterized by availability of

investment data, large pool of investors and fund managers, active trading, well-

disseminated business and financial information, appropriate degree of market

regulation and reasonably sophisticated communication system. (Lian, 2000)

2.2.1 Previous literatures that support earnings and past dividends determine

current dividends

The signalling effect of dividend has become the major debates amongst the

finance researchers and scholars. The famous dividend-signalling model in

1950s by Lintner (1956) showed that earnings of a company can be sub-

divided into permanent earnings and temporary earnings. He observed that

only changes in permanent earnings affect changes in dividends, while

temporary earnings will not have any influence on a company’s dividend

policy. Due to the nature of dividend which functions as a lagging indicator of

changes in a company’s permanent earnings, dividend payout ratio rises when

a company begins a period of bad times and falls when a company reaches a

period of good times. Further study by Aharony and Swary (1980) supported

Lintner’s model. According to their findings, quarterly dividend

announcements have information content beyond the earnings announcement,

which further supported the semi-strong form of efficient market hypothesis.

16

Lintner (1956) discovered for the first time that firms maintain a target

dividend payout ratio and adjust their dividend policies to such target. His

studies showed that current earnings of the firm and dividend in the previous

years determined the firms’ dividends. Lintner also pointed that managers

believed that investors prefer firms with stable dividend policies. Subsequent

surveys by Baker, Farrelly, and Edelman (1985) on the listed companies in the

New York Stock Exchange supported Lintner’s views with the conclusion that

the major determinants of dividend payments are current earnings and past

dividends.

Empirical evidences had shown that dividends do signal to the market on the

financial position of a company. A research study by Garrett and Priestly

(2000) showed significant evidence of dividend smoothing and dividends

convey information on unexpected positive changes in current permanent

earnings. No evidence was found to support the notion that the dividend

signals future permanent earnings. In the same year, Guay and Harford (2000)

found that relationship exists between dividend distribution with the past and

contemporary cash flow shock. Their studies were further tested by Al-

Sharaks (2005) and his findings supported the previous research done by Guay

and Harford (2000).

17

2.2.2 Previous literatures that support changes in dividends do not provide

signals to the market

A well-known finance theory on irrelevance of dividends without any

influence on the share prices of the company was introduced by Miller and

Modigliani (1961) who supported the market efficiency theory. While some

researchers have different views that the capital market is inefficient and

therefore changes in dividends provide signal to the market, Miller and

Modigliani theory suggests that changes in dividend might have information

content if there exists insider information (managers are better informed than

investors). Further studies by Watts (1973) and Gonedes (1978) showed that

there is no relationship between current dividends and future earnings.

However research done by Watts (1973, 1976a, 1976b) showed that the

hypothesis on the information content of dividend was trivial.

Although Marsh and Merton (1987) briefly considered the dividend signalling

hypothesis, they argued that dividend signalling unlikely to occur as the firm’s

specific information will be washed-out. In other words, the market efficiency

theory exists to support the study by Marsh and Merton (1987). They argued

that the dividend decisions of individual firms are not independent of the

decision of other firms in the same industry. Managers respond to the dividend

announcements of their peers, regardless of the company’s financial position

and future investment requirements. Further study by Healy and Palepu (1988)

and Benartzi et al (1997) proved the earnings reversal phenomena. The results

by Benartzi et al (1997) showed no significant relationship between changes in

dividends and changes in earnings in the subsequent years. However, changes

18

in dividends indicate changes in earnings in current year.

Using Marsh and Merton model, Kao and Wu (1994) discovered marginal

evidence of dividend signalling. Following Kao and Wu’s studies, Fudenberg

and Tirole (1995), and Vieira and Raposo (2007) proved that dividends are

sticky as managers tend to maintain their dividend per share even when the

company faces temporary net losses. Managers cut down their dividend

payment only when they are sure that the earnings will not revive. There are

researchers who viewed a dividend cut as a good news to the investors as it

shows managers’ decision to solve the firms’ financial problems (Abeyratna

and Power, 2002).

The linearity and non-linearity of the mean reversion of earnings are found to

be the elements that distinguish between the effects of dividend signalling.

Earlier study on dividend signalling by Nissim and Ziv (2001) supported for

the dividend signalling theory, however the reverse was found after

considering the non-linearity of earnings (Grullon et al, 2005). Initial test on

the relationship between changes in dividend and changes in future earnings

by assuming the linearity in the changes in earnings and controlling on the

uniform mean reversion and momentum in earnings showed that changes in

dividends convey some information about future earnings. The study by

Grullon et al (2005) showed that changes in dividends are strongly related to

concurrent earnings. His result was consistent with the empirical evidence that

changes in dividend policy occur only when changes in earnings are

substantial (Brav, Graham, Harvey and Michaely, 2003). In other words,

19

changes in dividends are considered as surrogate for non-linearity of earnings

under a uniform mean reversion model. The result by Grullon et al (2005) was

proven earlier by DeAngelo, DeAngelo and Skinner (1992) and Benartzi et al

(1997). The dividend signalling theory holds true for dividend increase based

on the study by Nissim and Ziv (2001) who found the lack of correlation

between dividend decrease and future earnings as the information content of

dividend decrease is already captured by current year earnings. Indeed, they

found that current year earnings and dividend decrease are highly correlated,

which is consistent with the result of DeAngelo et al (1992) and Benartzi, et al

(1997). Study by Benartzi et al (1997) supported the dividend signalling

theory, showing the evidence on changes in dividends provide information on

the current and past level of earnings. According to Nissim and Ziv (2001), the

negative relationship between these two variables is due to accounting

conservatism.

Besides, market characteristics also determine the extent of dividend

signalling. The usage of dividend as a signalling tool is less prominent in less

developed markets as compared with developed markets such as United

Kingdom in which current dividends are determined by lagged dividends

(Vieira and Raposo, 2007). The fact that a developed stock market with larger

pooled of investors is characterised by less concentrated ownership and the

management may use changes in dividends to convey information on firm’s

prospects to the external shareholders. In other words, the pattern of firm

ownership determines the effect of dividend signalling. Firms with

concentrated ownership may not need dividend as signalling tool (Goergen,

20

Renneboog and Silva, 2005) as concentrated ownership reduces information

asymmetries (Vieira and Clara, 2007).

The size of the dividend announcing firms also has some level of influence on

the extent of dividend signalling. According to Bajaj and Vijh (1990),

dividend announcements by large firms will not trigger large market reaction.

2.2.3 Previous literatures that support changes in dividends provide signals to

the market

Some previous studies on dividend behavior found evidence that managers use

changes in dividend as a signalling device to convey information about

unexpected shock in earnings (Bhattacharya, 1979; John and Williams, 1985;

Miller and Rock, 1985; Aharony and Dotan, 1994; Chen and Wu, 1999;

Nissim and Ziv, 2001; Arnott and Asness, 2001 and 2003; Harada and Nguyen,

2005; Baker, Mukherjee and Paskelian, 2006; Staceseu, 2006; Vivian, 2006).

The reason behind changes in dividends as a clear and unambiguous tool to

convey the future prospects of the companies lies on the fact that financial

reports of the firms only reflect past financial performance of the firms and are

manipulated by the management especially when the firms faced financial and

operational difficulties (Kaplan and Roll, 1972).

Research conducted by Yoon and Starks (1995) supported dividend signaling,

which is in turn supported by the evidence of payout asymmetries. In the same

year, Bernheim and Wantz (1995) found evidence in support of signalling

rather than agency explanations on the reasons dividends are paid.

21

Further, two research studies by Fama and French (1998) explained current

dividend payout signals future expected earnings.

Other researchers who used financial models to test the dividend signalling

and dividend behavior in the stock market such as Brickley (1983), Healy and

Palepu (1988) and Aharony and Dotan (1994) found that an increase in

dividend leads to the increase in future earnings. Research done by Aharony

and Dotan (1994) showed that firms that increase (decrease) their dividends

experience greater (smaller) unexpected changes in earnings in the subsequent

years as compared with firms that do not change their dividends. However, the

magnitude of the relationship becomes smaller when the earnings change

events move further away from the event quarter. Differences in the

magnitude of the changes in the unexpected earnings yield are discovered

under different categories of dividend change.

Some researchers tested the relationship between dividends and future

earnings with and without controlling for the effect of past and current

earnings. Nissim and Ziv (2001) proved a positive relationship between

current dividend and changes in earnings in the subsequent 2 years following

the dividend change year by controlling a particular (linear) form of mean

reversion in earnings. However, their results showed that dividend decrease

was not related to future profits. Brickley (1983) found a positive relationship

between dividend increase (decrease) and earnings increase (decrease) without

controlling for the effect of past and current earnings announcements.

22

From the above review on the historical research findings, we can conclude that there

are different views on dividend as signal on the future prospects of the company. The

reasons on the differences in findings are partly due to geographical differences

(different stock exchanges with different market characteristics / sophistication /

market liquidity), differences in companies’ characteristics (different corporate

culture or dividend policies) and industry effect.

Many research studies on dividend signalling have been done in developed countries,

but lack of research studies are conducted in developing countries such as Malaysia.

As such, there is a need to further discover on the dividend signalling of the listed

companies in Bursa Malaysia.

23

CHAPTER 3: RESEARCH METHODOLOGY 3.1 DEVELOPMENT OF THE HYPOTHESES

The information content of dividend with the underlying assumption that earnings

follow a random walk (Benartzi et al, 1997; Nissim and Ziv, 2001) is tested using the

following hypotheses:-

(A) Relationship between changes in dividends in current year with changes in

earnings in the concurrent and subsequent years:

HAo: Companies that change their dividends in year 0 will not experience

any changes in unexpected earnings in the following years, i.e. year 1

to year 5. Instead, there is a positive and significant relationship

between changes in dividends and unexpected earnings in the

concurrent year.

HA1: Companies that change their dividends in year 0 will experience

changes in unexpected earnings in the following years, i.e. year 1 to

year 5 with positive and significant relationship (Dividend signalling

exists).

The above hypothesis is further extended to test the relationship between the type of

dividend change (dividend increase and dividend decrease) with change in unexpected

earnings in the concurrent and subsequent years as follows:-

(B) Relationship between increase in dividend in current year with increase in

earnings in the concurrent and subsequent years:

HBo: There is no relationship between increase in dividends in the

24

concurrent year with increase in the unexpected earnings in the

subsequent years from year 1 to year 5. Instead, there is a positive and

significant relationship between increase in dividends with increase in

unexpected earnings in the concurrent year.

HB1: There is a positive relationship between increases in dividend in the

current year with increases in the unexpected earnings in the

subsequent year 1 to year 5 (Dividend signalling exists for dividend

increase).

(C) Relationship between decrease in dividends in current year with decrease in

earnings in the concurrent and subsequent years

HCo: There is no relationship between decrease in dividends in current year

with decrease in unexpected earnings in subsequent years from year 1

to year 5. Instead, there is a positive and significant relationship

between decrease in dividends with decrease in unexpected earnings in

the concurrent year.

HC1: There is a positive and significant relationship between decreases in

dividends in the current year with decreases in the unexpected earnings

in the subsequent year 1 to year 5 (Dividend signalling exists for

dividend decrease).

The subdivision of the dividend change events into sub-groups of dividend increase

and dividend decrease is to identify the type of dividend change which has a stronger

effect on changes in earnings in the concurrent and / or subsequent 5 years following

the dividend change event, as tested in the hypothesis B and C above.

25

Further to the testing of the above hypotheses A to C, the relationship between

changes in dividends with changes in unexpected earnings was tested by each

category of years as follows:-

(a) Each individual year under the study period from year 1998 to 2007

(b) Sub-period during the financial crisis (1998-2001) and post financial crisis (2002-

2007)

(c) Case by case analysis on dividend change events that occurred after experiencing

stable dividend per share for consecutive 2 years, 3 years and 4 years.

The case by case analysis on changes in dividends that happened after some period of

stable dividends as mentioned in (c) above is tested by using the hypothesis below:-

(D) Relationship between the stability of dividend before changes in dividends

with the extent of dividend signalling

HDo: There is no relationship between the stability of dividend before

changes in dividends with the extent of dividend signalling.

HD1: There is a positive relationship between the stability of dividend before

changes in dividends with the extent of dividend signalling. The more

stable of dividend before the changes in dividend policies, the stronger

the dividend signalling.

Besides testing on the relationship between changes in dividends and changes in

earnings on a combined-year and individual-year basis, more in-depth study was

conducted on the extent of dividend signalling based on the size of changes in

26

dividends and the size of dividend yields of the companies. The rationale behind the

study on the extent of dividend signalling based on the size of changes in dividends is

that investors are more concerned with larger changes in dividends as compared with

smaller and insignificant changes. Hence the hypothesis to test the extent of dividend

signalling based on the size of dividend changes is as follows:-

(E) Relationship between the size of changes in dividends with the extent of

dividend signalling

HEo: There is no relationship between the size of changes in dividends with

the extent of dividend signalling.

HE1: There is a positive relationship between the size of changes in dividend

with the extent of dividend signalling. The larger (smaller) the changes

in dividends, the stronger (weaker) the dividend signalling effect.

In addition to the size effect of changes in dividends, study is further expanded to

examine the clientele effect by testing the relationship between the dividend yield with

the extent of dividend signalling. Naturally, companies with higher dividend yield tend

to place more weight on dividend in share valuation as compared with those companies

with low dividend yield. This is due to investors of those companies with low dividend

yield are more concerned with changes in the share price as a source of investment

gains rather than relying on dividend as investment income. Hence the hypothesis

tested is:-

27

(F) Relationship between dividend yield and the extent of dividend signalling

HF0: There is no relationship between dividend yield and the extent of

dividend signalling.

HF1: There is a positive relationship between dividend yield and the extent

of dividend signalling. The larger (smaller) the dividend yield, the

stronger (weaker) the dividend signalling.

Lastly, industry effect in influencing the extent of dividend signalling is further tested

by incorporating the effect of 3 sectors with the highest number of dividend paying

companies (namely, industrial, trading / services and consumer sector) in the

regression model.

(G) Industry effect in influencing the extend of dividend signalling

HG0: Industry effect does not have any influence on the extent of dividend

signalling of the companies.

HG1: Industry effect does exists to influence the extent of dividend

signalling of the companies

3.2 SELECTION OF MEASURES

The information content of dividends of the listed companies in the Main Board of

Bursa Malaysia is measured by using Pearson correlation and regression analysis on 2

major variables, namely the changes in unexpected earnings and changes in dividends.

The measurement of these 2 variables is shown in the formulas below:-

28

3.2.1 Measure of unexpected earnings

The unexpected earnings are measured by using the following formula as

adopted by Benartzi et al (1997).

∆UE i,t = (E i,t – E i,t-1) / MVi,0

Whereas

∆UE i,t = Changes in unexpected earnings of firm i in year t

E i,t = Earnings of firm i in year t

E i,t-1 = Earnings of firm i in year t-1

MV i,0 = Market value of equity of firm i on the 1st trading day of the

announcement year

In this study, expectation model is adopted for annual changes in earnings in

which we assume earnings follow a random walk with drift (Aharony and

Dotan, 1994).

As the above formula (adopted by the previous studies) uses absolute value,

modification has been made to reflect per share value for dividends and

earnings before extraordinary items as below:-

∆EPS i,t= (EPS i,t – EPS i,t-1) / Pi,0

Whereas

∆EPS i,t = Changes in earnings per share of firm i in year t

EPS i,t = Earnings per share of firm i in year t

EPS i,t-1 = Earnings per share of firm i in year t-1

P i,0 = Share price of firm at the beginning of the dividend

change year 0

29

The EPS of the selected sample companies are adjusted in which extraordinary

items such as gain or loss on sale of investments, land etc and diminution in

the value of investments are excluded from the computation of the bottom line

earnings, except in cases where such extraordinary items are regarded as part

of the ordinary business of the selected sample companies. The adoption of

earnings before extraordinary items is in line with the basis of measurement of

earnings as adopted by Benartzi et al (1997).

3.2.2 Measure of changes in dividends

Annual dividend is adopted in the analysis as dividends are set in response to

annual rather than quarterly earnings (Watts, 1973).

The changes in dividend are measured by the difference of dividend per share

in year t and dividend per share for year t-1, scaled by the dividend per share

in year t-1.

∆ Divi,0 = Di,0 – Di,-1 Di,-1

Whereas

∆ Divi,0 = Changes in dividend per share of firm i in year 0

Di,0 = Dividend per share of firm i in year 0

Di,-1 = Dividend per share of firm i in year -1

The changes in dividends are categorized into two dividend change subgroups,

namely (1) dividend increase and (2) dividend decrease.

30

3.3 SAMPLING DESIGN

The sample for this study consists of listed companies on the Main Board of Bursa

Malaysia, which is derived from the yearly publication of Dynaquest Sdn Bhd titled

“Stock Performance Guide” featuring historical financial and stock performance data

of listed companies on the Main Board of Bursa Malaysia. The selection criteria of

the sample are as follows:-

(i) The selected companies must be listed on the Main Board of Bursa Malaysia

since 1997 onwards with complete financial data of EPS and DPS.

(ii) Companies in the Finance, REITS and Closed-End Funds sectors are excluded

from the study to improve homogeneity of the sample as these companies have

very high leverage with different rules for income measurement. Such

selection criterion follows the selection method adopted by Pandey (2001),

Grullon et al (2003) and Short, Zhang and Keasey (2002).

(iii) Companies that are categorised under PN4 and PN17 will be excluded from

the study. A firm being categorised under PN4 is a company with its assets

consist of 70% or more of cash or short term investments. The inclusion of

these companies in the analysis will jeopardise the result as companies with

abundant of cash may distribute large portion of its retained earnings as

dividends, regardless of the losses experienced by the company. Whereas a

PN17 companies are financially distressed companies in which the possibility

of division omission is very high.

(iv) Companies categorized under the IPC, Hotels and Mining are excluded from

the study due to its relatively small number of companies under each sector.

31

(v) The selected companies must pay at least 2 consecutive years of dividends to

enable calculation of yearly changes in dividends. Dividend initiations and

dividend omissions are excluded from the study.

(vi) The selected companies must have financial information on the changes in

EPS for the current and future five years after the dividend payment year.

(vii) Companies with other distribution events such as stock splits or a stock

dividends declared around the declaration of the current dividend will be

excluded from the study (Grullon et al, 2003; Aharony and Dotan, 1994;

Nissim and Ziv, 2001). The selection criterion is to minimize any

contaminating announcements effect as such distribution events will affect the

per unit share price, which is used as the denominator in measuring changes in

earnings.

3.4 DATA COLLECTION PROCEDURES

The analysis to test the relationship between changes in dividends in year 0 (year 0 is

the dividend change year) and changes in earnings in year 0 and 5 years following the

dividend change year (year 1 to year 5) requires data on EPS and DPS from year 1997

until year 2007 and share price on the beginning of the dividend change year from

year 1998 to 2007. All these data are obtained from the latest yearly publication of

Dynaquest Sdn Bhd - “Stock Performance Guide” which features all the Main Board

listed companies in Bursa Malaysia.

32

3.5 DATA ANALYSIS TECHNIQUES 3.5.1 Data Filtering

The final list of sample companies was obtained by going through 4 stages of

filtering to ensure that the final list of the samples contained only companies

with complete financial data for regression analysis.

1st stage : Filtering of dividend paying and non-dividend paying

companies

Companies that did not pay dividends in each individual year

for the period 1998 to 2007 were excluded from the study.

The process of filtering by excluding companies with DPS=0

on each individual year 0 involves the filtering of dividend

omission events at the same time should DPS is more than 0

in year –1.

2nd stage : Filtering of dividend initiation events

Companies with DPS more than 0 in year 0 but DPS equals

to 0 in year –1 were excluded from the study.

3rd stage : Filtering of companies in the sector of Finance, IPC,

Mining, Hotels, REITS and Closed-End Funds

Companies in the sector of Finance, IPC, Mining, Hotels,

REITS and Closed End Funds were further excluded from

study in view of the different accounting procedures adopted

by Finance companies and the relatively small amount of

companies categorized under the sector of IPC, Mining,

Hotels, REITS and Closed-End Funds.

33

4th stage : Filtering out companies with incomplete financial data

The final stage of the filtering process is to filter out those

companies without complete data on changes in earnings

from year 0 to year 5 due to changes in financial years.

The initial sample of dividend paying companies after the filtering process

consists of 2,679 firm-year observations.

3.5.2 Assumptions adopted in the regression analysis

Prior to regression analysis, the following assumptions must be fulfilled to

ensure reliability of the regression results (Coakes and Steed, 2007)

(1) Minimum number of cases for analysis must be at least five times of

independent variables. The ideal number of cases must be twenty times

more than the number of predictors.

(2) Outliers are deleted or modified to minimize the influence on the result

of the regression.

(3) No multicollinearity and singularity between the independent variables

for multiple regressions.

(4) Variables must fulfill the assumption of normality, linearity,

homoscedasticity and independence of residuals.

All the variables have fulfilled the above assumptions as the number of cases

is large (more than 2,000 cases). The normality on all the variables used in the

regression analysis, namely changes in dividends in year 0 and changes in

34

earnings in the concurrent year and 5 years after the dividend change year

(year 1 to year 5) were tested and identified through the value of skewness,

kurtosis and Kolmogorov-Smirnov test. Outliers were identified through the

generation of boxplots during the normality test by using SPSS.

Initial normality test on all the variables used in the regression analysis

showed some variables were not normally distributed with skewness value

more than 3, high value of kurtosis and Kolmogorov-Smirnov value at

significant level p<0.05. To improve the normality of the variables, outliers

were identified from the boxplots generated from the SPSS program and were

further eliminated from the samples. The elimination of outliers from the

samples has helped in reducing the value of skewness and kurtosis.

Berry and Feldman (1995) pointed out that the most important regression

assumption is related to residuals. A residual plot is used to check the

assumption of independence of error terms in the regression. Examination on

the pattern of the scatter plot of residuals against predicted values for each of

the regression showed random and patternless residuals with no clear

relationship of both variables and hence consistent with assumption (4) above.

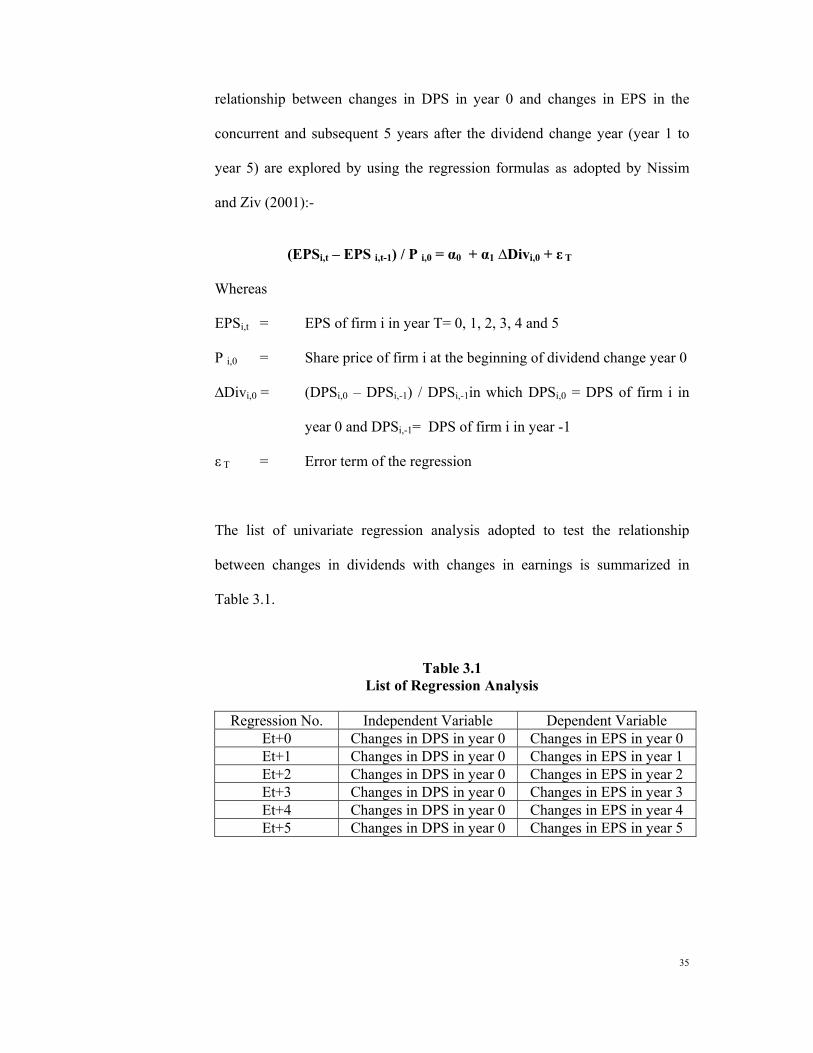

3.5.3 Analysis on the relationship between changes in dividends in year 0 with

changes in earnings in the concurrent year and subsequent 5 years

The analysis technique adopted in this study is regression analysis. In

analyzing the variables using the regression analysis, 2 categories of dividend

changes are identified namely “INCREASE” and “DECREASE”. The

35

relationship between changes in DPS in year 0 and changes in EPS in the

concurrent and subsequent 5 years after the dividend change year (year 1 to

year 5) are explored by using the regression formulas as adopted by Nissim

and Ziv (2001):-

(EPSi,t – EPS i,t-1) / P i,0 = α0 + α1 ∆Divi,0 + ε T

Whereas

EPSi,t = EPS of firm i in year T= 0, 1, 2, 3, 4 and 5

P i,0 = Share price of firm i at the beginning of dividend change year 0

∆Divi,0 = (DPSi,0 – DPSi,-1) / DPSi,-1in which DPSi,0 = DPS of firm i in

year 0 and DPSi,-1= DPS of firm i in year -1

ε T = Error term of the regression

The list of univariate regression analysis adopted to test the relationship

between changes in dividends with changes in earnings is summarized in

Table 3.1.

Table 3.1 List of Regression Analysis

Regression No. Independent Variable Dependent Variable

Et+0 Changes in DPS in year 0 Changes in EPS in year 0 Et+1 Changes in DPS in year 0 Changes in EPS in year 1 Et+2 Changes in DPS in year 0 Changes in EPS in year 2 Et+3 Changes in DPS in year 0 Changes in EPS in year 3 Et+4 Changes in DPS in year 0 Changes in EPS in year 4 Et+5 Changes in DPS in year 0 Changes in EPS in year 5

36

3.5.4 Analysis on the extent of dividend signaling with the influence of industry

effect using multiple regression

In examining whether differences in the changes in earnings exists between

two sectors with the highest number of dividend paying companies when these

2 sectors experienced changes in dividends, multiple regression analysis was

adopted in this study. 2 sector dummies were incorporated to capture any

differences that exist between 2 sectors which were measured by the beta

coefficient of these sector dummies. The multiple regression equation used is

illustrated below:-

(EPSi,t – EPS i,t-1) / P i,0 = α0 + α1 ∆Divi,0 + α2 Dummya + α3 Dummyb + ε T

Whereas

EPSi,t = EPS of firm i in year T= 0, 1, 2, 3, 4 and 5

P i,0 = Share price of firm i at the beginning of dividend change year 0

∆Divi,0 = (DPSi,0 – DPSi,-1) / DPSi,-1in which DPSi,0 = DPS of firm i in

year 0 and DPSi,-1= DPS of firm i in year -1

Dummya = Dummy for sector a

Dummya = Dummy for sector b

ε T = Error term of the regression

All the regression equations above will be tested using the regression function in the

SPSS program.

37

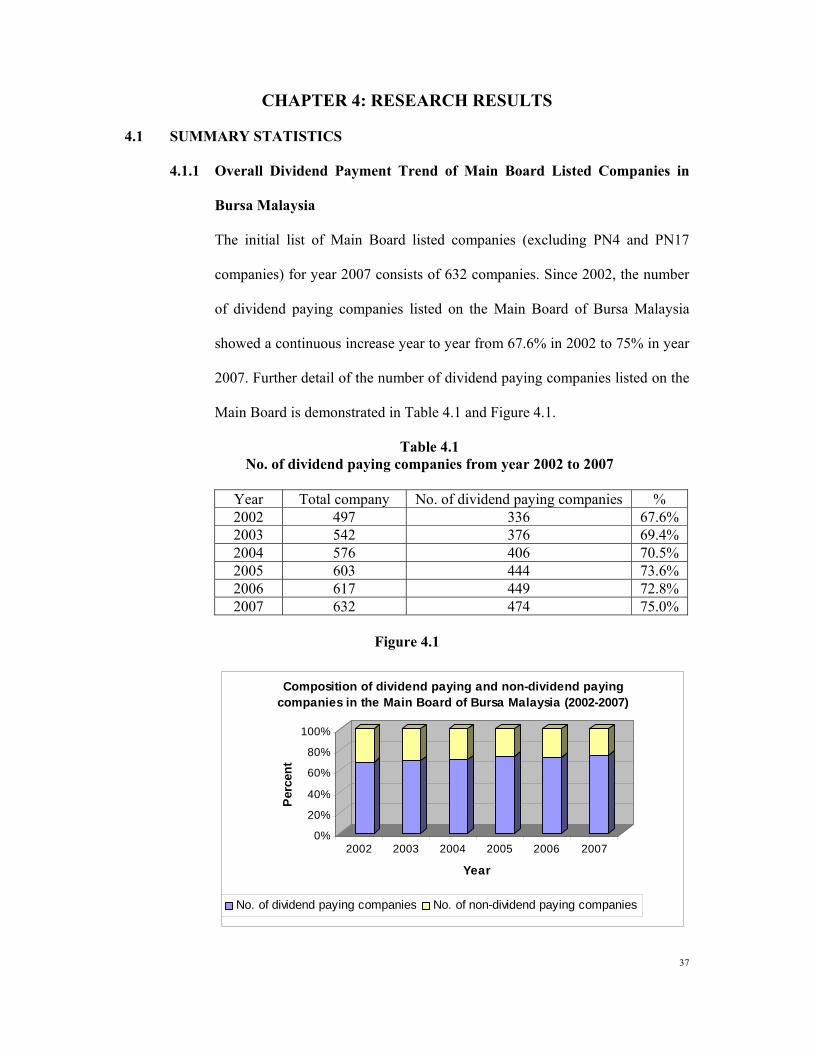

CHAPTER 4: RESEARCH RESULTS 4.1 SUMMARY STATISTICS

4.1.1 Overall Dividend Payment Trend of Main Board Listed Companies in

Bursa Malaysia

The initial list of Main Board listed companies (excluding PN4 and PN17

companies) for year 2007 consists of 632 companies. Since 2002, the number

of dividend paying companies listed on the Main Board of Bursa Malaysia

showed a continuous increase year to year from 67.6% in 2002 to 75% in year

2007. Further detail of the number of dividend paying companies listed on the

Main Board is demonstrated in Table 4.1 and Figure 4.1.

Table 4.1 No. of dividend paying companies from year 2002 to 2007

Year Total company No. of dividend paying companies % 2002 497 336 67.6% 2003 542 376 69.4% 2004 576 406 70.5% 2005 603 444 73.6% 2006 617 449 72.8% 2007 632 474 75.0%

Figure 4.1

0%

20%

40%

60%

80%

100%

Per

cent

2002 2003 2004 2005 2006 2007

Year

Composition of dividend paying and non-dividend paying companies in the Main Board of Bursa Malaysia (2002-2007)

No. of dividend paying companies No. of non-dividend paying companies

38

More than 50% of the dividend paying companies listed on the Main Board

came from 3 major sectors, namely Industrial, Trading / Services and

Consumer sector, with each sector being the first, second and third sector with

the highest number of dividend paying companies in year 2007. The

percentage of the dividend paying companies from the Consumer sector

remained at more than 80% since year 2002, with the highest percentage of

dividend paying companies recorded in year 2005 (88%). As can be seen from

Table 4.2, the Mining sector continued to become a 100% dividend paying

sector in the Main Board of Bursa Malaysia for 5 consecutive years since 2003,

as there is only 1 company listed under this sector. Excluding Mining sector, 3

sectors with the highest percentage of dividend paying companies for the past

2 years since 2006 were the Consumer, Finance and Technology sector with

more than 80% of the companies in these sectors paying dividends. 2 sectors

that experienced continuous increase in the percentage of dividend paying

companies in each sector since year 2002 are the Industrial and IPC sector.

Hotels sector continued to maintain its percentage of dividend paying

companies at 60% across the years since 2002. 3 sectors with the lowest

percentage of dividend paying companies for the part 2 years since 2006 were

the Closed-End Funds, Properties and Hotels sectors. A study on the trend of

percentage of dividend paying companies showed that a total of 5 sectors

(Consumer, Industrial, Construction, Trading / Services, Properties and

Plantations) experienced decrease in the percentage of dividend paying

companies in year 2006, which recorded the highest number of sectors with

reduced dividend paying companies. This may be caused by unfavorable

outlook on the domestic and global economy which is under the threat of

39

recession with the contagion from the United States financial chaos spreading

worldwide. The Malaysian economy was expected to slow down in year 2008

and 2009 due to the faltering economy and the impact of higher commodity

prices. Based on the data extracted from the 23rd National Economic Briefing

2008 of Malaysian Institute of Economic Research, the Real GDP growth rate

in year 2008 and 2009 is forecasted at 4.6% and 5.0%, respectively, as

compared with 6.3% recorded in year 2007. Further information on the

categorization of dividend paying companies by sector is shown in Table 4.2

and Figure 4.2.

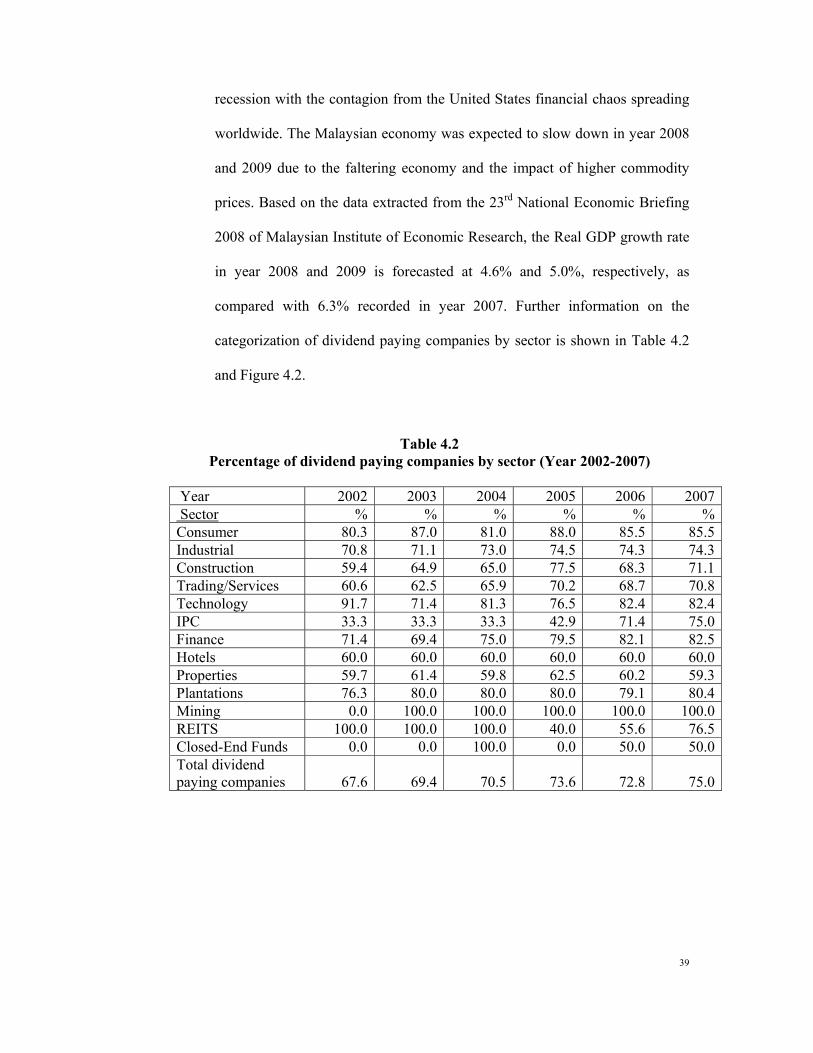

Table 4.2 Percentage of dividend paying companies by sector (Year 2002-2007)

Year 2002 2003 2004 2005 2006 2007 Sector % % % % % %Consumer 80.3 87.0 81.0 88.0 85.5 85.5Industrial 70.8 71.1 73.0 74.5 74.3 74.3Construction 59.4 64.9 65.0 77.5 68.3 71.1Trading/Services 60.6 62.5 65.9 70.2 68.7 70.8Technology 91.7 71.4 81.3 76.5 82.4 82.4IPC 33.3 33.3 33.3 42.9 71.4 75.0Finance 71.4 69.4 75.0 79.5 82.1 82.5Hotels 60.0 60.0 60.0 60.0 60.0 60.0Properties 59.7 61.4 59.8 62.5 60.2 59.3Plantations 76.3 80.0 80.0 80.0 79.1 80.4Mining 0.0 100.0 100.0 100.0 100.0 100.0REITS 100.0 100.0 100.0 40.0 55.6 76.5Closed-End Funds 0.0 0.0 100.0 0.0 50.0 50.0Total dividend paying companies 67.6 69.4 70.5 73.6 72.8 75.0

40

Figure 4.2

0%

20%

40%

60%

80%

100%

P erc