discussion papers - la trobe university

TRANSCRIPT

School of Business

Estimating a Differentiated Products Model with aDiscrete/Continuous Choice and Limited Data

DISCUSSION PAPERS

David Prentice

Series A 00.16 2000

The copyright associated with this Discussion Paper resides with theauthor(s)

Opinions expressed in this Discussion Paper are those of the author(s),not necessarily those of the School, its Departments or the University

Estimating a Differentiated Products Model with a Discrete/Continuous Choice and Limited Data

David Prentice School of Business La Trobe University

[email protected] December 1, 2000

Abstract:

This paper specifies a vertically differentiated products model for a product with a

discrete/continuous choice. The model is easily estimated with the relatively limited data

used in classical demand equation estimation, supplemented by readily available market

characteristics data. The model, with some modifications, is estimated with a new dataset

(by state and region) for the U.S. Portland cement industry. Plausible patterns of own and

cross price elasticities are obtained. The role of market characteristics is estimated

generalizing the applicability of the results to other markets and periods.

1

1. Introduction

Estimation of differentiated products models, after beginning with the U.S.

automobile industry has flowered into other consumer products (see Davis (2000) for a

recent survey). This work has developed models for particularly visibly differentiated

products, where the consumer makes a discrete choice, which are estimated with readily

available specialized datasets of prices, sales and product characteristics. Even then,

estimation remains demanding. Furthermore, for numerous products for which the

framework is appealing, useful product characteristics data is not available. One of the

implicit assumptions of the new empirical industrial organisation is that though industry

specific models are developed, they are substantially generalisable. However, the focus on

discrete choices and the specialized data and estimation requirements mean the

generalization of structural differentiated products models has been limited to date.

This paper specifies a differentiated products model for a product that features

both a discrete and continuous choice. The model is readily estimated with the type of data

typically used in classical demand equation estimation. The discrete choice component is

based on the vertical differentiation model used in Bresnahan (1987). The model is

estimated with a new dataset on U.S. state and regional Portland cement consumption,

construction, prices of building materials and other market characteristics. This dataset is

typical of data available to researchers in a broad set of products. Furthermore the model

is estimable using just instrumental variables estimation yet it yields estimates of structural

own and cross price elasticities of demand. In addition, elasticities with respect to market

characteristics are estimated.

2

This paper demonstrates how structural models of demand for differentiated

products can be extended to handle products with a discrete and continuous choice. This

case is particularly important for modeling long run demand for products, for example,

with switching costs. It is demonstrates how these models can be applied to broader set of

commodities, with more limited data, than the highly visible differentiated consumer

products considered to date. Finally, a new set of estimates of demand elasticities for

Portland cement is provided – an industry that has rarely been considered for demand

estimation (see Gupta (1975) for the only direct example).

The paper proceeds as follows. In the next section, the cement industry and the

data are introduced. At the end of this section, estimates of a set of linear demand

equations are presented, demonstrating that further structure is required to explain

demand - especially the cross-section variation. Then an estimable version of a generalized

vertical differentiation model is derived - so to handle the mixed discrete/continuous

choice and other features of the commodity and data. In section four, it is discussed how

to handle complements, uncertain substitutes and other econometric issues. Then the

estimated equations and elasticities are presented. Some suggestions for further work are

presented in the conclusion.

3

2. The Demand for Portland cement: Background, Data and Preliminary Estimates

2.1 Background

Portland cement is the powder mixed with water, sand and aggregate that makes

concrete. For a manufactured product, cement is essentially homogeneous, with no

important differences across the types of Portland cement or across the products of

different manufacturers (Prentice (1997)). Up until recently there has been no economic

substitute for cement in making concrete in the United States.

Concrete is primarily used in construction and its importance differs significantly

across different types of construction. The shares of cement in the cost of selected types of

construction are presented in Table One. Streets and Highways feature the largest share,

just over 2.5%.

Table One: Cost Share of Cement in Construction Category Percentage All Construction 0.96 New Construction 1.07 One Family Housing 1.15 Streets and Highways 2.51 Farming 1.30 Calculated by averaging requirements (including in concrete) in the Input-Output Statistics for 1972, 1977 and 1982, (Williams (1981, 1985) and Bureau of Economic Analysis (1991))

Cement differs in importance, in part, because there are several substitutes for

concrete such as asphalt, steel, wood and curtain wall products (U.S Department of

Commerce (1987)). The substitutability of concrete varies considerably with the type of

construction. While there are few substitutes for concrete for foundations and large dams,

the use of concrete varies considerably across buildings and over time. For example, the

Brutalist school, and other modernist architects made prominent and substantial use of

4

concrete in a variety of buildings (Fleming et al (1980), Jencks (1985)). In addition,

concrete houses were built in early 20th century U.S.A and Australia and are common in

developing countries today. Although cement is substantially homogeneous, it is one of a

set of differentiated products in the building materials industry, highlighted by the variety

in the buildings around us.

2.2 Highlights of the Data

In this subsection, the highlights of the data are presented. The sample is

composed of annual data on U.S. states and regions from 1956 to 1992. There are three

sets of data. First, there is the cement and construction data. Second, there is the set of

prices of building materials. Third, there is the set of market characteristics.

The characteristics of the cement and construction data are summarized in Table

Two:

Table Two: Characteristics of the Cement and Construction Data Series Aggregation Availability Sources Cement State 1956-1992 except

Hawaii, Alaska. Bureau of Mines (1956-1992)

Construction State 1967-1992, except Hawaii, Alaska.

FW Dodge

Construction Regions 1956-1966 FW Dodge NB: The components of the FW Dodge regions are listed in a Data Appendix available

from the author.

The construction data is the value of contracted new construction, supplied by

F.W. Dodge Co., which is then deflated using a construction price index constructed in

Prentice (1997). From 1956 – 1966, detailed construction data is provided for eight

regions across the U.S. From 1967 on, state level data is provided. Hence, all other data

was collected for 48 states and Washington DC for 26 years, and eight FW Dodge regions

for 11 years, providing a total of 1362 observations. The coverage of construction is not

5

complete as Preston and Lipsey (1966) suggest rural building is particularly under-

represented. Comparison with the input-output data suggests over 90% of cement

consumption is captured, but just 50-70% of new construction expenditure. However, the

FW Dodge construction data is used commercially, as a base for official statistics and is

the best available measure of detailed regional construction activity.

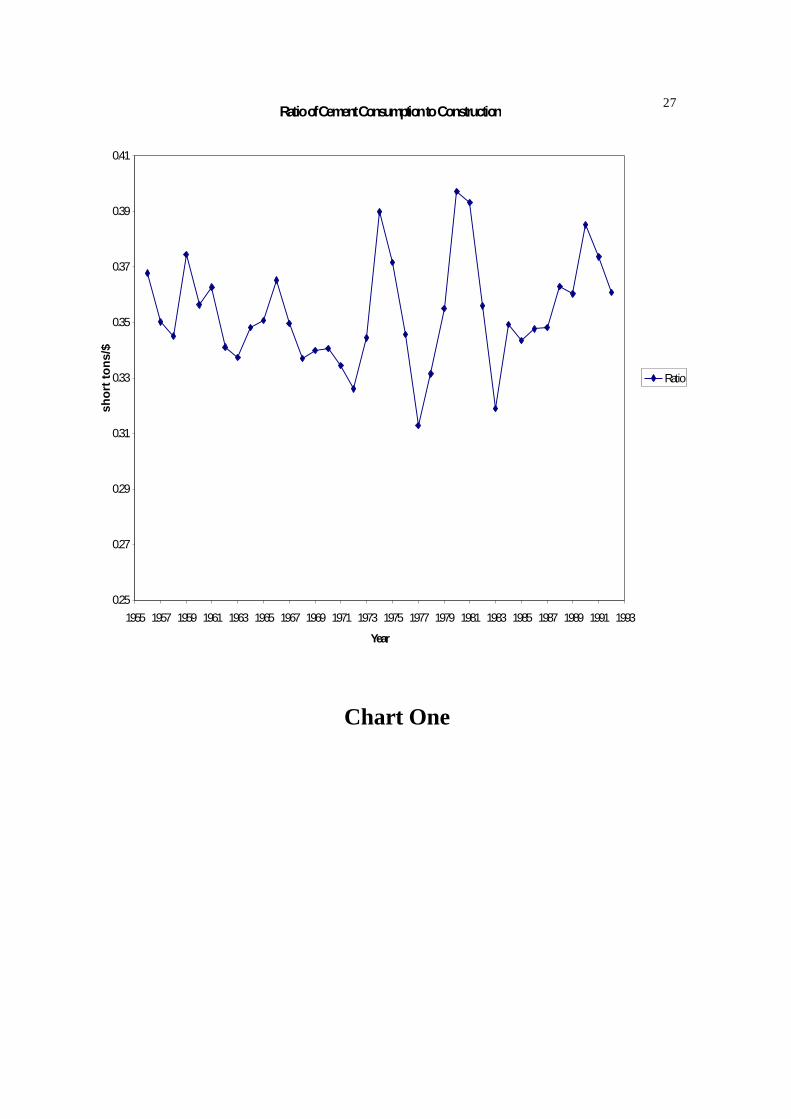

The quantities of construction and cement consumed are highly correlated over

time. The ratio of national cement consumption to construction, presented in Graph One,

demonstrates some cyclical variation without a trend. This is consistent with there being

no evidence of any substantial technological change in cement use in construction over the

period. This ratio is used repeatedly in the paper and is hereafter referred to as the cement-

construction ratio.

There is, though, considerable regional variation as displayed in Map One. The

plains states, and some energy producing states feature higher than average cement-

construction ratios. And the Atlantic states and Washington feature lower than average

cement-construction ratios. These differences may reflect different mixes of construction

or local prices but there is no immediate intuitive explanation for the regional variation.

In Table Three, the definitions and sources of the data on prices and market

characteristics are summarized.

The second set of data is the prices of building materials. For cement and bricks,

average prices are calculated at the source over states or a relatively small number of

states. Where prices are calculated over groups of states, these prices are assigned to all

states in the group. However, for the other substitutes, the Engineering News Record

prices are collected across twenty cities.

6

Table Three: Data Variable Definition Source

Prices of Building Materials Price-Cement Average Annual Mill Price Bureau of Mines Minerals

Yearbook (1956 – 1992) Price-Bricks Average Annual Price of

Building Bricks* Current Industrial Reports: Clay Construction Products (1957 – 1992)

Price-Steel Average – three types of Building Steel*

Engineering News Record (1956 – 1992)

Price-Lumber Average – four types of Lumber*

Engineering News Record (1956 – 1992)

Price-Gravel Average – two types of Gravel*

Engineering News Record (1956 – 1992)

Price-Asphalt Weighted average of three types of Asphalt and Road Oil.

Engineering News Record 1956 – 1969, Dept. of Energy (1970 – 1992)

Market Characteristics Disaster Prone Value of Losses for nine

types of natural disaster, by state for 1970.

Table 5.14, Petak and Atkisson (1982)

Number of Hot Days Statistical Abstract of the United States (denoted SA)

Average Temperature SA Precipitation SA Normal Minimum SA Area SA Annual Growth SA, Bureau of the Census

(1975) (denoted HS) Share of Agriculture Ratio Cash Receipts from

Farm Marketing to State Income

SA

Share of Industries Employment Share of Eight Broad Industry Groups

SA

Catch-up Ratio Ratio of Per Capita State Income to Highest Income State Income in 1950

SA, (HS)

Income Growth Growth 1950-1992 SA, (HS) Other Data

Interest Rate Real Moodys Aaa Corporate Bond Rate

Economic Report of the President. (various years)

7

Where prices are not available for states, prices from neighboring (sometimes averages

across various states) are used. All prices are deflated using the Implicit GDP Deflator,

collected from the Economic Report of the President (various years).

The third set of data is the market characteristics data. There are three sets of

characteristics: physical characteristics, economic structure and stage of development.

First, the physical characteristics of the state, including its exposure to natural disasters,

are likely to influence construction choices. For example, the demand will be lower in

states which feature both high precipitation and extreme cold as this combination of

weather makes concrete failure more likely (Lea (1970)). Demand will be higher in states

which feature short lived strong winds, like tornadoes, as concrete tends to hold well with

short-lived strong winds (Petak and Atkisson (1982)). Second, the economic structure,

and short run demand fluctuations may affect the composition of construction in ways not

captured by the different construction categories. Finally, the stage of economic growth

may also affect the composition of construction. There is no formal theory of the effects of

growth but Hayek (1939), as discussed in Montgomery (1995), suggests one pattern.

Large, basic projects are then followed by smaller more specialized projects to obtain full

value from the initial projects. Roads, dams, aqueducts are examples of basic projects

featuring cement-intensive construction.

2.3 Estimating a Standard Demand Equation

In this section, instrumental variable estimates of standard demand equations are

presented to demonstrate how they fail to adequately control for cross section variation

and to suggest issues important for modeling and estimation in sections three - five.

8

All regressions use the full sample of states and regions. The dependent variable is

the cement-construction ratio. The explanatory variables are the prices of building

materials, shares of construction types and time-varying market characteristics. As the

prices of cement and gravel are locally determined, instruments are constructed.

The first regression (not reported here), with the prices of building materials as the

sole explanatory variables, reveals this data features the heterogeneity associated with unit

record data. Prices explain just 8.6% of the variation. Hence, fixed effects are introduced

(using the within transformation to reduce multicollinearity).

In Table Four, extracts of the results of three regressions with fixed effects are

presented. The first column contains the estimates of an equation with just the prices of

building materials as explanatory variables. The second column contains the estimates of a

second equation with the prices of building materials and the shares of different types of

construction. The third column contains the estimates of a third equation with prices,

construction shares and time varying market characteristics.

Table Four: Extracts from the Demand Equation Results Explanatory Variable

Basic Specification (1)

(1) & Construction Shares

(2)

(2) & Time Varying Market

Characteristics (3)

Price – Cement -0.3706 (-7.812) -0.2286 (-5.756) -0.2180 (-5.408) Price – Brick -0.03419 (-0.361) -0.07376 (-0.947) -0.0861 (-1.112) Price – Asphalt 0.4138 (3.648) 0.5785 (5.114) 0.5938 (4.170) Price – Steel 0.1765 (3.934) 0.1928 (5.173) 0.1863 (4.974) Price – Lumber 0.0394 (1.588) 0.0624 (3.054) 0.0607 (2.947) Price – Gravel 0.2379 (1.723) 0.1347 (1.200) 0.0532 (0.469)

2R 60.04 75.71 77.26 Spearman Rank Correlation Test

23.158 19.121 10.3018

Condition Number 10.9593 1113.1 1817.55 F-Test Result 32.67 (vs. no fixed

effects) 38.19 (vs. column (1))

9.73 (vs. column (2))

9

There are two things to note about these results. First, that the coefficients on

prices have plausible signs and typically are statistically significant from zero. However,

these demand equations fail to pick up the cross sectional variation identified in Map One.

This is demonstrated by testing the relationship between the fixed effects and the

dependant variable. First, the average cement-construction ratios over time for each state

and region are calculated and ranked. Then the sizes of the fixed effects are ranked and the

two sets of ranks used in a Spearman Rank Correlation Test. In all cases the null

hypothesis of no correlation is rejected, suggesting the demand equation has failed to pick

up the cross section variation.

To gain some information on what could be determining the cross sectional

variation, the estimated fixed effects from the third specification are regressed on a set of

non-time varying explanatory variables. Extracts of the results are presented in Table Five

Table Five: Extracts of the Results of the Regression of Fixed Effects on market characteristics.

Variable Coefficient (T-Statistic) Catch-up 0.0621 (5.078) Precipitation -0.2292 (-11.339) Normal Minimum 0.3406 (5.080) Area -0.0193 (-3.516) Flood 1.1686 (13.195) Storm Surge 0.7970 (13.825) Tornado 0.0759 (1.516) Hurricane -0.6746 (-11.018) Strong Winds 11.2428 (4.048) Earthquake -0.1442 (-4.037) Landslide 0.3654 (1.396) Expansive Soil 1.0310 (17.002)

2R 71.4

A substantial proportion of the variation in the fixed effects is accounted for by the

market characteristics. Not surprisingly, weather conditions and physical disaster losses

10

influence the cement-construction ratios. Precipitation has a negative effect and strong

winds a positive effect. The catch-up variable also positively affects cement intensity,

supporting the hypothesis of Hayek (1939).

If the sole purpose of the analysis is to extract current elasticities for the cement

industry then using fixed effects is fine. However, if we want to compare elasticities across

countries or over longer periods of time, estimating the determinants of the cross section

variation is important.

3. A Structural Model of the Demand for Portland cement

In this section, an estimable differentiated products demand model featuring a

discrete and continuous choice is presented. In the first subsection, it is argued that

cement consumption is based on a mixed discrete/continuous choice. Then the discrete

choice component for each construction job is specified following the vertical

differentiation model used by Bresnahan (1987). The quantities consumed for each job are

then aggregated up to a state demand equation. This equation though features variables

unobserved by the econometrician so the equation is manipulated until an estimable

equation is obtained. Because meaningful product characteristics data does not exist,

unlike Bresnahan (1987), the estimated equation is a structural equation. To explain the

cross section variation, market characteristics are introduced as determinants of some

coefficients.

An additional complication, specific to this industry, is to allow for a price inelastic

component of the demand for cement because of building regulations or extreme physical

conditions.

11

3.1 A Model with Discrete/Continuous Product Choice and Inelastic Demand

The demand for building materials has two features that require adapting the

discrete choice framework that is the standard foundation for differentiated products

models.

The first feature is that the demand for building materials is best characterized as

featuring both a discrete choice and a continuous choice. For each component of a

construction job a discrete choice of the building material to be used must be made. For

example, the builder of a driveway could choose gravel, concrete, bricks or asphalt. This

type of choice seems not dissimilar to a choice of model of automobile or other consumer

product. However, a continuous component must be added as rather than buying one

automobile, the quantity of the chosen material varies across consumers with the size of

the construction job. It is assumed the continuous component is a linear function of the

size of the construction job i.e. in effect there is constant returns to scale in construction.

So the total quantity of the ith material consumed on a construction job, j, of type g is:

(1) conjg

ig

ijg QQ ,, β=

where igβ is the per unit requirement coefficient for input i for construction type g.

Different coefficients for different types of construction are assumed because Table One

demonstrates different construction types feature different per unit consumption of

cement. The mixed discrete/continuous specification, though required for building

materials is also applicable to other commodities, particularly those featuring switching

costs such as sunk costs before use.

12

The second modification, though, is more specific to the construction industry. It

is assumed there is a price inelastic component of demand. This is because building codes

or industry practice requires the use of concrete for some jobs because only concrete

provides, for example, sufficient strength or sealant powers. Hence there is a price

inelastic component and a price elastic component of cement consumption. Then, the total

cement consumed for a job j of type g is:

(2) ( )

−+=

otherwise chosen iscement if 1

,,

,,,,, con

jggcem

ig

conjgg

cemeg

conjgg

cemigcem

jg QkQkQk

Qβ

ββ

where kg is the share of construction type g that features a price inelastic component of

cement and cemig,β and cem

eg,β are the input requirement coefficients for the inelastic and

elastic components of cement consumption.

3.2 Modeling the Discrete Choice of a Building Material

The model of a discrete choice of a building material largely follows the adaptation

of the vertical product differentiation model in Bresnahan (1987). This model has the

disadvantage of a relatively restricted pattern of elasticities. While more general models

exist (see Davis (2000) for a survey) for the (even multiple) discrete choice case, there is

no existing model that handles the mixed discrete/continuous case required here and the

Bresnahan (1987) model can be generalized to this case relatively easily.

Therefore, we start with a model of the decision maker and then aggregate up to a

market demand equation. The decisionmaker, hereafter referred to as the client, has

income, Y, to invest and chooses one of a set of construction projects composed of

particular materials, or another investment, commonly referred to as the outside option.

Because construction is substantially an investment good rather than a consumer durable

13

the utility from the outside option is modeled as dependent on the rate of return, r, rather

than as a constant (as in Bresnahan (1987)):

(3) ( )r1YU +=

The utility gained from investing in any one of the construction projects is specified as

follows. Denote a as the taste for quality, xi as the quality of the ith material and Pi as its

price.1 The utility gained from the construction project is:

(4) ( ) ( )( )rQPYQaxQPiaYxU conjg

ig

iconjgi

conf

if

i +−+= 1,,,,,, ,, ββ

When the client chooses between the different materials, two factors are of

concern: price and quality. Quality can be thought of as an index composed of different

factors such as aesthetic appeal, strength, resistance to weather and insulation ability. It is

assumed that, for broad classes of materials, clients, following the advice of their

architects, agree on a ranking, in terms of quality, of the different materials that could be

used. But, the importance of quality is assumed to differ across clients. In particular a is

assumed to be distributed uniformly:

δdensity with ], [~ maxaaUa (Per capita).

Unlike Bresnahan (1987), the density of clients is expressed per capita rather than

absolutely. This is to allow for variations in population across the states and over time.

The taste for quality plays an important role in determining the discrete choices of

whether to invest in construction, and material to be used. For example, assume concrete

is ranked as higher quality than asphalt but of lower quality than bricks. A client is

1 The budget constraint does not enter the problem formally, but, as with Bresnahan (1987), is assumed to be satisfied. Introducing multipliers, etc., to control for the budget constraint would significantly complicate the specification without much gain.

14

indifferent between using concrete, c, or asphalt, b, if their taste for quality, a, equals acb

such that:

(5) ( )r1xxPP

abc

bg

bcg

c

cb +−

β−β=

Denote, Psub, x and subgβ as vectors of the prices, quality ratings and input requirements

coefficients of the relevant materials. Then the indicator function, Ijc(Psub,x, sub

gβ ,a), for

concrete, where the br subscript and superscripts refer to bricks, is defined as follows:

(6) ( ) ( ) ( )

+−−

>>+−−

=otherwise. 0

11 if 1,,, rxx

PPar

xx

PPaxPI

bc

bg

bcg

c

cbr

cg

cbrg

br

subg

subcj

βββββ

The demand for cement for job j of construction type g, of size conjgQ , , is as below:

(7) ( ) conjg

cemg

subg

subcj

cemj QaxPIQ ,,,, ββ=

where ccem

cg

cemg αβ=β where c

cemα is the quantity of cement required per unit of concrete.

3.3 A Model of State Cement Consumption

Because the data is aggregated at the state level the job specific model of the

previous subsection will be aggregated up to the state level. Denote ng as the number of

jobs of construction type g. Each job requires different nonnegative quantities of each type

of construction, conj,gQ .

The total quantity of cement consumed is then obtained by aggregating across all

of the individual decisions represented in equation (7):

(8) ( )∑ ∑ ∑= =

−

==Ι=

G

g

n

j

cemcong

G

g

cemg

conjg

cemg

subg

subcj

cem g

QQaxPQ1 1 1

,,,, βββ

15

where cemcongQ − is the quantity of construction of type g that uses cement. This does not

yield an equation for estimation in terms of observable exogenous variables as cemcongQ − is

not observed. To get around this problem, first denote, congQ as the average quantity of

construction of type g and conj,gε as the deviation from the mean for job j. Then, (8) can be

rewritten as:

(9) ( ) ( )∑ ∑= =

+Ι=G

g

n

j

conjg

cong

cemg

subg

subcj

cem g

QxPQ1 1

,,, εββ

Because, for each construction type, the deviation averages out, (White (1984)), this

leaves us with (10):

(10) ( )∑ ∑= =

Ι=G

g

n

j

cong

cemg

subg

subcj

cem g

QxPQ1 1

,, ββ

Denote ng,cm as the number of projects that use cement. Equation (10) can then be

rewritten as:

(11) ∑=

=G

g

cong

cemgcmg

cem QnQ1

, β

The ng,cm, being unobservable, will now be substituted out. First, multiply and divide (11)

by ng yielding:

(12) ∑=

=

G

g

cong

cemg

g

cmgcem Qn

nQ

1

, β

Note, congQ is observable. However ng,cm and ng are not. Following Bresnahan (1987), ng,cm

for each state s can be replaced as follows:

(13) [ ] ( )

−β−β−

−β−β∗+∗∗δ=−δ=

bc

bb

cc

ca

cc

aa

sbcacscm,g xxPP

xxPP

r1popaa*pop*n

16

Rewriting equation (12) using (13) yields:

(14) [ ]( )raaQpopn

Q bcac

G

g

cong

cemgs

g

cem +−

= ∑

=1

1βδ

This leaves ng to deal with which is neither observable nor can be assumed to be constant.

However, ng can also be replaced. First note all clients with a* as defined below are

indifferent between taking the construction project and just investing the funds in the

outside option:

(15) ( )( )( )

( ) gcgb

cemg

cemgg

bg

b

kxkx

rPkkPa

+−++−

=1

11*

ββ

As long as Pb, the bottom ranked construction material, Pcem and r are negatively

correlated – which is quite likely as the two materials are inputs to investment, a* will be

roughly constant. Assuming a* is constant, ng can be replaced as follows:

(16) ( )∗−= aapopn sg maxδ

Substitution of (16) into (14) yields:

(17) [ ]( )( ) 1max

11

−∗

=−+−= ∑ aaraaQQ bcac

G

g

cong

cemg

cem β

Finally, the price inelastic and price elastic components of cement consumption are added

to yield a differentiated products demand equation for Portland cement:

( ) ( ) ( )∑∑= ∗=

−

−++−+=

G

g

gbcemgcema

cemgba

cemg

gbcem

bbg

gcema

aag

cong

cemgg

G

g

cong

cemgg

cem

aa

xx

Px

x

P

x

P

rQkQkQ1 max

,,,,

,,

,,,,

111 18

βββ

ββ

where xi,j is the difference (xi – xj) in the quality indices and state and time subscripts are

suppressed. This equation is estimated with the same set of variables required for a

17

classical demand equation – the prices of building materials and construction as a defacto

income. The interactive terms arise from the mixed discrete/continuous choice that forms

the foundation of the model.

Cross-section variation is accounted for by making the coefficients a function of

the market characteristics. In the absence of rapid technological change in construction

materials comparable to cement, the values of the quality index are unlikely to change.

However, as argued earlier, the coefficients cemgβ are likely to vary across construction

types and with market characteristics. Hence, the cemgβ can be re-expressed as follows:

(19) Zghgcemg

′+= ,,0 βββ

where Z is a set of market characteristics. Equations (18) and (19) are the theoretical basis

for the estimation in Section 5.

4. Econometric Issues

Before beginning estimation, there are three major econometric issues that must be

dealt with. First, a set of prices of building materials for each type of construction must be

chosen – both substitutes and complements. Second, it is demonstrated that equations (18)

and (19) reduce to a linear form that is relatively simple to estimate with instrumental

variables. Finally, the treatment of market characteristics is discussed.

Strictly replicating Bresnahan (1987, 1981) requires beginning with a set of initial

rankings so to select those to be compared with, in this case, cement. The market

characteristics data available in this case does not permit this. Omitting a relevant material

results in inconsistent estimates, while including an irrelevant variable only reduces

efficiency. Hence we select a set of building materials that could be ranked around cement,

18

and include these in the demand equation, interacting all of them with the relevant

variables as if they were the relevant prices. The model is then supported if two of the

coefficients are significantly positive.

The related problem is that certain materials may be complementary rather than

substitutes for cement e.g. steel for reinforced concrete. Potential complements are treated

the same way as potential substitutes. They are included in the demand equation,

interacting with the relevant variables. Those inputs with coefficients significantly negative

are considered complements. Similarly, if more than two inputs prove to be significant this

suggests they are complementary to the substitutes. Ultimately, as in most estimation of

this type, the industry knowledge and judgment of the researcher will have to be relied on

to decide whether a negative coefficient is evidence of complementarity or

misspecification.

The second issue is choice of estimation technique. The model specified in

equations (18) and (19), though theoretically identified, is highly non-linear. However, the

model reduces to a linear form that retains key features and, importantly, enables

identification of the structural elasticities. The linear form estimated in section five is

summarized below:

( ) ( ) ( ) ∑ ∑∑= ==

++

=+

G

g

I

i

icongig

G

g

cong

gcon

cemg

Psr

s

rQQ

1 1,

1 11 20 θγ

(21) ggchargg Z′+= ,,0 γγγ

where congs is the share of total construction of construction type g, γ and θ are the

reduced form combinations of the structural coefficients in (18) and (19) and Ig and Zg are

19

the set of materials and market characteristics for construction type g. Though the

individual parameters ( matgβ , kg, amax,a*, xij) cannot be identified from this specification,

the structural elasticities can be estimated. The own price, Qcemp,ε , cross price, Q

matp,ε and

characteristics, Qcharε , elasticities are stated below:

( )∑=

+=

G

gcem

cemcongcemgQ

cempQ

rPQ

1

,,

1θε

( )∑=

+=

G

gcem

matcongmatgQ

matpQ

rPQ

1

,,

1θε

∑=

=G

gcem

charcongchargQ

char Q

ZQ

1

,γε

The third issue is the treatment of the market characteristics variables. If the

coefficients γg,char are all equal to zero, then the sign of each reduced form coefficient is

specified unambiguously by the model. The γ’s will all be positive, the θ’s on cement and

any complements will be negative, and the θ’s on the other prices either positive or

insignificantly different from zero. However the evidence from section three suggests

several market characteristics are required to explain the cross section variation. The

market characteristics variables used are Normal Minimum, Precipitation, Catch Up,

Income Growth, Share of Agriculture and Losses due to Tornadoes and Expansive Soil.

While economic theory does not provide signs for the gchar ,γ priors based on industry

literature enable some of them to be evaluated – for the others, their role will be

demonstrated by the results.

20

Finally, the treatment of endogenous explanatory variables and multicollinearity is

discussed. As for the standard demand equations instruments were constructed for the

prices of cement and gravel – the building materials for which the prices were most likely

to be set locally. The other econometric problem is dealing with multicollinearity. The

results from the standard demand equation estimation suggests, suitably transformed, the

price data is not collinear but as construction and other forms of heterogeneity variables

are introduced, the interaction terms are likely to cause problems. Hence the quantity of

cement is divided by the quantity of construction and (1+r). Then all variables are centered

on their means before estimation. Finally the data is scaled to similar levels. This should

reduce problems from multicollinearity.

5. The Results

In this section, three sets of results are discussed. First, the demand equations (20)

and (21) are estimated with the gchar ,γ set equal to zero. Second, a set of elasticities

compiled from estimates of the demand equations (20) and (21) with the gchar ,γ allowed

to differ from zero are discussed. Finally, the coefficients underlying these elasticities and a

more general specification are discussed.

First, equations (20) and (21), without market characteristics, are estimated.

Though potentially inconsistent, the theoretical model provides unambiguous predictions

of the signs of the coefficients, which enables assessing, on their own terms, if the model is

supported in the data. Two versions are presented – the first with one construction type,

and the second with two types: Roads and Rest of Construction. The results are presented

in Table Six:

21

Table Six: Standard Specifications Explanatory Variable One type of Construction Two types of Construction Constant* -10.0717 (-4.7346) Share of Roads 1.7615 (9.4217) Rest of Construction 1.0273 (5.5364) Price-Cement 0.0002 (0.0447) -0.0032 (-0.8235) Price-Brick 0.0266 (3.1914) 0.02714 (3.4059) Price-Asphalt 0.0011 (0.0713) 0.1202 (6.0855) Price-Steel -0.0265 (5.0943) -0.0348 (-6.8504) Price-Lumber 0.0093 (3.2624) 0.0012 (0.4444) Price-Gravel 0.1072 (7.6892) 0.0968 (7.7772) RSS 1501.66 1194.07 Condition Number 533.064 103.999 The constant term is actually the coefficient on (1/1+r). T-statistics are in parentheses.

The first set of estimates is unsatisfactory because the constant term is significantly

less than zero and the price of cement is statistically insignificant. However, when two

types of construction are introduced (only in the “intercept” terms), the coefficients on the

types of construction are significantly positive. The coefficient on the price of cement is

now negative though statistically insignificant. Additional support for the model is gained

from there being at least two prices of substitutes that have significantly positive

coefficients. The price of steel has a significantly negative coefficient suggesting it is a

complement. These results are broadly supportive of the underlying model.

In the next set of regressions, market characteristics variables are included through

equation (21). As is discussed below, results are obtained consistent with the model.

Hence, as the elasticities are identified these are discussed first as presented in Table

Seven:

Table Seven: Elasticities

22

Prices Characteristics Variable Elasticity Variable Elasticity Cement -0.297 Normal Minimum 0.008 Brick 0.137 Precipitation -0.005 Asphalt 0.168 Catch-Up 0.015 Steel -0.122 Agriculture 0.009 Lumber -0.006 Tornado 0.004 Gravel 0.100 Income Growth 0.001 Expansive Soil 0.008

The own-price and cross price elasticities suggest relatively little substitutability

across inputs, but the pattern across inputs is quite plausible. All cross-price elasticities are

smaller than the own price elasticity. Asphalt features the largest cross price elasticity and

steel is again found to be a complement. The coefficient on lumber is statistically

insignificantly different from zero.

Next the characteristics elasticities are considered. First note that all coefficients on

the characteristics are significantly different from zero, except economic growth. But

cement demand is inelastic to small changes in these characteristics. This is not

inconsistent with the map presented earlier as the usage ratios are similar in similar states

but different across substantially different states. Catch-up is the largest, providing some

support for the pattern of growth suggested in Hayek (1939).

Next the coefficients on the two regressions with market characteristics are

presented in Table Eight. The first column (Regression One) allows for different market

characteristics to interact with the different types of construction but not the coefficients

on the prices. These results are quite successful and are used to calculate the elasticities in

Table Seven. The second set (Regression Two) allows for different coefficients on the

prices as well – but these results are less successful.

Table Eight: Coefficients

23

Explanatory Variable Regression One Regression Two Rest 1.1128 (6.8541) 0.9852 (6.805) Roads 1.7640 (10.2046) 1.9949 (2.381) Roads – Normal Minimum 0.0012 (4.4865) 0.0013 (4.7159) Roads – Precipitation -0.0005 (-2.5356) -0.0009 (3.243) Rest – Catch-up 0.0001 (4.6817) 0.0001 (3.7287) Rest – Agriculture 0.0002 (8.6483) 0.0002 (6.5064) Rest – Tornado Damage 0.0004 (5.3423) 0.0004 (5.2137) Rest – Growth 0.0002 (0.6665) -0.0001 (-0.3619) Rest – Expansive Soil 0.0008 (8.6416) 0.0008 (7.936) Cement -0.0195 (-5.083) Brick 0.0321 (3.8457) Asphalt 0.1130 (5.9573) Steel -0.0137 (-2.9321) Lumber -0.0004 (-0.1691) Gravel 0.0410 (3.4361) Rest – Cement 0.00001 (0.0746) Rest – Brick 0.0003 (2.5801) Rest – Steel -0.0001 (-1.8236) Rest – Lumber -0.00002 (-0.5132) Roads – Cement -0.0019 (-1.2965) Roads – Asphalt 0.0089 (4.8599) Roads – Gravel 0.0042 (3.1313) RSS 885.825 885.387 Condition Number 164.801 579.045 T statistics are in parentheses.

First, consider regression one. The signs on the construction and heterogeneity

variables are all plausible. Importantly, there are at least two significantly positive

coefficients on the price variables. The signs on the coefficients on prices have been

discussed further above. The effects of precipitation and tornadoes are consistent with that

suggested in the engineering and disaster literature. It is nice to see roads with a larger

coefficient.

Regression two appears less successful - probably because of multicollinearity. The

residual sum of squares has barely fallen at all. The coefficients on the heterogeneity

variables have not changed very much. For the group of prices based around roads, the

24

results are broadly satisfactory as both asphalt and gravel are positive and significant from

zero. Cement is negative though insignificant. However, the “rest of construction”

coefficients are less satisfactory. Cement is just insignificant but positive. Furthermore,

only brick is positive and significant, though steel remains negative and significant. These

discouraging results could be due to two causes. First, the condition number has crept up

in the second regression so multicollinearity may be starting to create problems. More

seriously, we may be coming up to the limits of what we can get out of the price data.

To summarize, these results suggest we have successfully estimated a

differentiated products model featuring a discrete/continuous choice and using largely

classical demand data. The signs of the coefficients are consistent with the theory - and

departures plausible. The pattern of elasticities is also plausible. Multicollinearity - in part

from the functional form and in part from the limits of the data - appears to be a problem.

5. Conclusions

There are ongoing important advances in estimating differentiated products

models. In general, though, these have focused on visibly differentiated consumer products

best characteristed as requiring a discrete choice. The case of a mixed discrete/continuous

case has not been considered. In this paper we develop a differentiated products model for

a product featuring a discrete and continuous choice and that is readily estimable with the

more limited data typically used in classical demand equation estimation. The model also

handles complementary products and researcher uncertainty about which inputs are

substitutes and complements. This model is estimated with a new dataset on U.S. state and

regional Portland cement consumption, prices and market characteristics. A plausible set

25

of own price and cross price elasticities are obtained. Finally, the model is easily applicable

to a broad range of products - including those with switching costs.

6. References

Bresnahan, T.F. (1981), "Departures from Marginal-cost Pricing in the American

Automobile Industry", Journal of Econometrics, 17, 201 − 227.

Bresnahan, T.F. (1987), "Competition and Collusion in the American Automobile

Industry: The 1955 Price War", Journal of Industrial Economics, 35, 457 − 482.

Bureau of the Census (1975), “Historical Statistics of the United States, colonial times to

1970”, U.S. G.P.O., Washington DC, 1975.

Bureau of Economic Analysis (1991), “The 1982 Benchmark Input-Output Accounts of

the United States”, U.S. G.P.O., Washington DC, 1991.

Bureau of Mines (1957-1992), “Minerals Yearbook” chapter on Cement. U.S Department

of the Interior, G.P.O., Washington DC.

Davis, P., (2000), "Empirical models of demand for differentiated products", European

Economic Review, 44, 993 − 1005.

Department of Energy (various years), “State Energy Price and Expenditure Report”,

Energy Information Administration, U.S. Department of Energy, G.P.O.,

Washington DC.

Fleming J., H. Honour, N. Pevsner (1980), “The Penguin Dictionary of Architecture”,

Third Edition, Penguin, Harmondsworth, 1980.

Gupta, G.S. (1975), “Demand for Cement in India”, Indian Economic Journal, 22(3), 187

− 194.

Hayek, F. (1939), “Profits, Interest and Investment” Routledge & K. Paul, London, 1939.

26

Jencks, C. (1985), “Modern Movements in Architecture”, Second Edition, Penguin,

Harmondsworth, 1985.

Lea, F.M. (1970), “The Chemistry of Cement and Concrete”, Third Edition, Edward

Arnold, London, 1970.

Lipsey, R.E. and D. Preston (1966), “Source Book of Statistics Relating to Construction”,

NBER, New York, 1966.

Montgomery, M.R. (1995), ""Time-to-Build" completion patterns for nonresidential

structures, 1961-1971", Economics Letters, 48(2), 155 − 63.

Petak, W.J. and A.A. Atkisson (1982), “Natural Hazard Risk Assessment and Public

Policy”, Springer Verlag, New York, 1982.

Prentice, D. (1997), "Import Competition in the U.S Portland Cement Industry", Ph.D.

Dissertation, Yale University.

U.S. Department of Commerce (1987), "A Competitive Assessment of the U.S Cement

Industry" U.S. Dept. of Commerce − International Trade Administration. , G.P.O.,

Washington D.C., 1987.

White, H. (1984), “Asymptotic Theory for Econometricans”, Academic Press, Orlando

FL, 1984.

Williams, F.E. (1981), “An Input-Output Profile of the Construction Industry”,

Construction Review, July/August 1981, 4 – 20.

Williams, F.E. (1985), “The 1977 Input-Output Profile of the Construction Industry”,

Construction Review, July/August 1985, 5 – 19.

27

Chart One

Ratio of Cement Consumption to Construction

0.25

0.27

0.29

0.31

0.33

0.35

0.37

0.39

0.41

1955 1957 1959 1961 1963 1965 1967 1969 1971 1973 1975 1977 1979 1981 1983 1985 1987 1989 1991 1993

Year

shor

t ton

s/$

Ratio

28

United States(Alaska and Hawaii excluded)

0.438 to 0.69 (9)0.392 to 0.438 (10)0.346 to 0.392 (10)0.295 to 0.346 (9)0.245 to 0.295 (11)

Map One