discounted cash flow methodology for banks and credit unions

TRANSCRIPT

Sageworksanalyst.com

Discounted Cash Flow (DCF) Modelingfor Credit Loss Reserves and Other Applications

Garver MoorePrincipal - Advisory Services

Sageworksanalyst.com

About the Webinar

• We will address as many questions as we can throughout the presentation or through direct communication via follow-up email

• Ask questions throughout the session using the GoToWebinar control panel

2

Sageworksanalyst.com

Disclaimer

This presentation may include statements that constitute “forward-looking statements” relative to publicly available industry data. Forward-looking statements often contain words such as “believe,” “expect,” “plans,” “project,” “target,” “anticipate,” “will,” “should,” “see,” “guidance,” “confident” and similar terms. There can be no assurance that any of the future events discussed will occur as anticipated, if at all, or that actual results on the industry will be as expected. Sageworks is not responsible for the accuracy or validity of this publicly available industry data, or the outcome of the use of this data relative to business or investment decisions made by the recipients of this data. Sageworks disclaims all representations and warranties, express or implied. Risks and uncertainties include risks related to the effect of economic conditions and financial market conditions; fluctuation in commodity prices, interest rates and foreign currency exchange rates. No Sageworks employee is authorized to make recommendations or give advice as to any course of action that should be made as an outcome of this data. The forward-looking statements and data speak only as of the date of this presentation and we undertake no obligation to update or revise this information as of a later date.

3

Sageworksanalyst.com

Sageworks Solutions

BUSINESS OUTCOMES

Better customer experience

Mitigate risk

Grow profitably

Increase defensibility

Sageworksanalyst.com

Sageworks Uniquely OffersOur Reach Our Client Experience

IMPORTANCE IN MARKET

• Loans Analyzed in our Platform:

» Number of Loans: 9 million loans

» Total Balance: $1.6 trillion dollars

BREADTH

• Number of Clients: 1,000+

• Educated 6,500 bankers in past year

• Nearly 2 million financial statements

of privately held companies in the US

PRODUCT SUPPORT

• Live Support: 99.65% of people who

call in for support get a live person

on the phone

INTEGRATION

• Number of Different Cores

Successfully Integrated: 52

• Number of Successful Integrations: 766

• Average Length of Integration: 42 business

days

Our Leading Technology Proven Value to Clients

SECURE

• Recognized as Critical Vendor

by regulators

• Examined annually by the FFIEC

PRODUCT FEEDBACK

• Focus Groups for Product Innovation:

400–500 annually

• Product Updates: Weekly

EXCLUSIVE

• Patented Technology: Enter and spread

tax returns in seconds using Electronic

Tax Return Reader

• ALLL Benchmarks

• Sageworks Industry Data

• Patented Technology: FIND engine

powering Business Narrative

• Loan Pricing benchmarks

LOAN GROWTH

• Our clients achieve 26% higher loan

growth than other banks

EFFICIENCY

• Our clients saw 3 times the

improvement in Efficiency Ratio

compared to other banks in 2015

YIELD

• Our clients achieved 11 basis points

higher yield on average than other

banks in 2015

RETURN

• Our clients achieved 2 times the ROE

growth over other banks since 2011

Sageworksanalyst.com

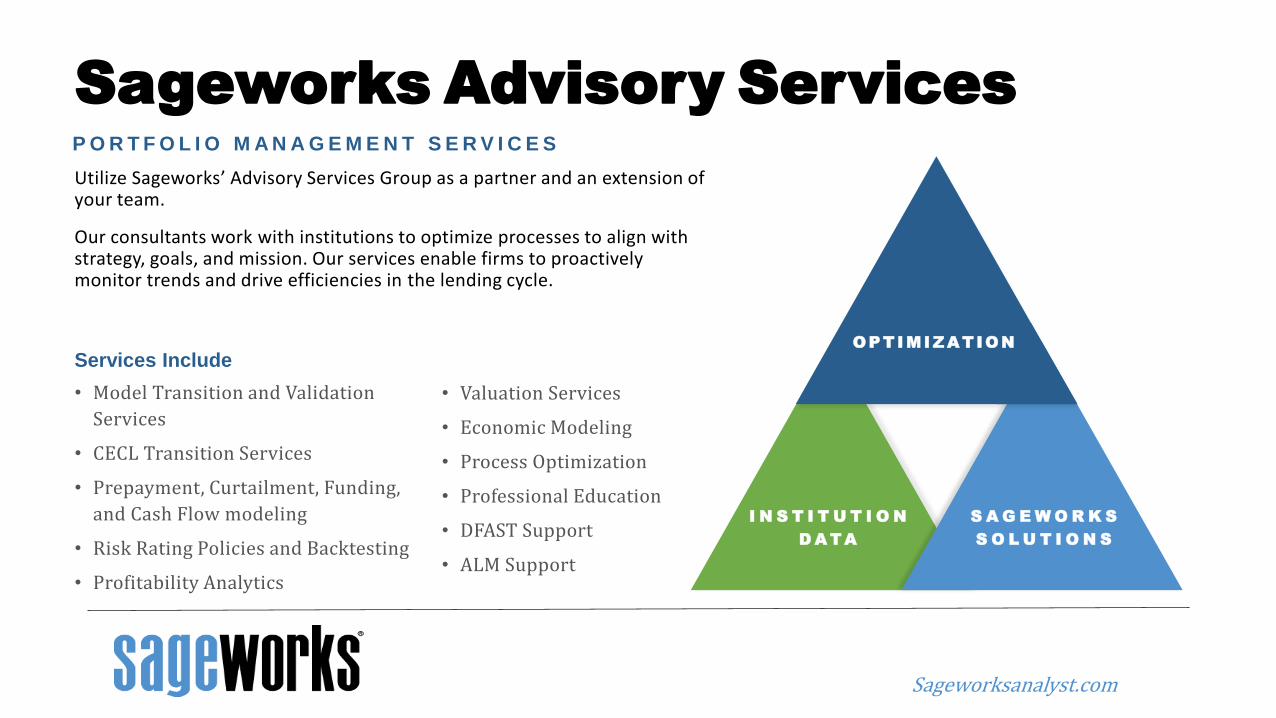

Sageworks Advisory Services

Utilize Sageworks’ Advisory Services Group as a partner and an extension of your team.

Our consultants work with institutions to optimize processes to align with strategy, goals, and mission. Our services enable firms to proactively monitor trends and drive efficiencies in the lending cycle.

P O R T F O L I O M A N A G E M E N T S E R V I C E S

Services Include

• Model Transition and Validation

Services

• CECL Transition Services

• Prepayment, Curtailment, Funding,

and Cash Flow modeling

• Risk Rating Policies and Backtesting

• Profitability Analytics

• Valuation Services

• Economic Modeling

• Process Optimization

• Professional Education

• DFAST Support

• ALM Support

O P T I M I Z A T IO N

I N S T I T U T I O N

D A T A

S A G E W O R K S

S O L U T I O N S

Sageworksanalyst.com

End in Mind

At the conclusion of this discussion, participants should:

• Understand the unique considerations of a discounted cash flow (DCF) analysis

• Understand the limitations of a sampling approach

• Believe DCF can be a solution when life-of-loan data is not available

• Understand the unique timing and component nature of DCF analysis

• Be able to speak to the elections required in a DCF analysis

• Understand the inferential approaches used in producing a DCF analysis

• Understand open areas of uncertainty

• Consider cross-applicability of measurement methodology

Sageworksanalyst.com

Poll Question

Sageworksanalyst.com

Agenda

• “Generative” v. “Look-Back” models

• Discounted cash flow principles

• Sampling vs. Bottom-Up

• Timing and Component Estimations

• Volatility in Measurement

• Current Conditions and Forecasting

• Individual Analysis

• Policy Considerations

• Other Applications

Sageworksanalyst.com

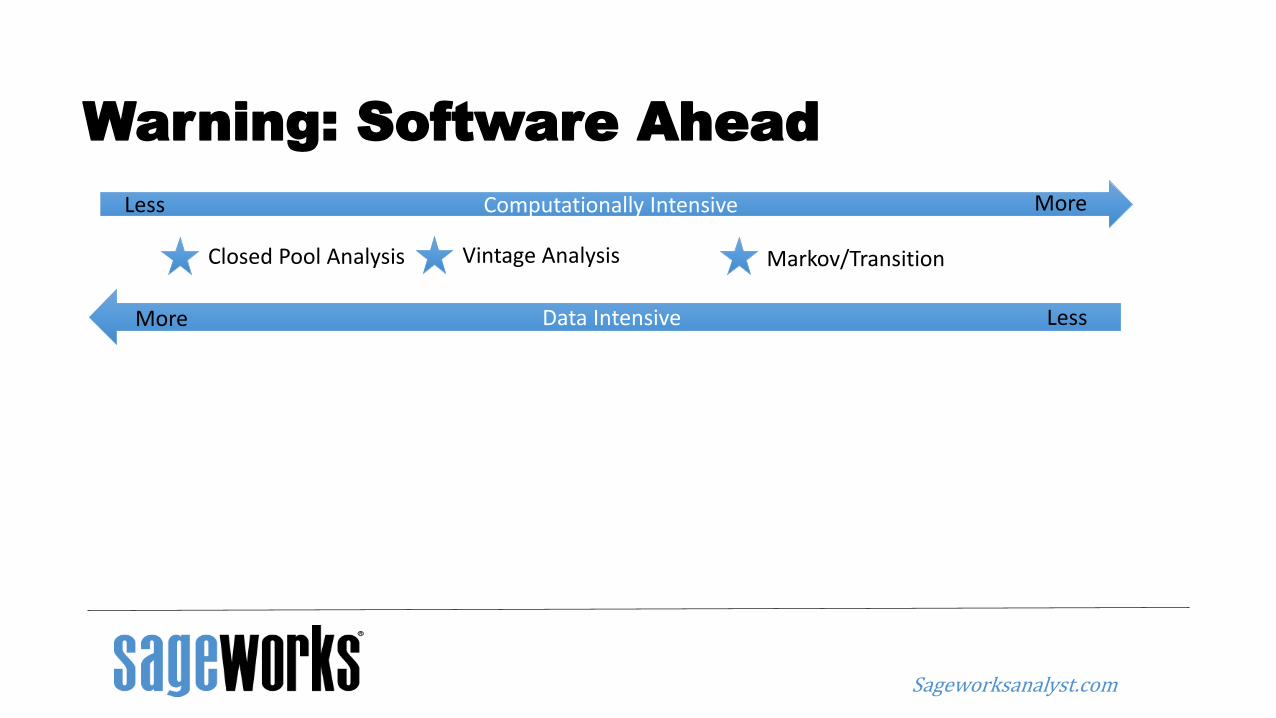

Warning: Software Ahead

Computationally Intensive

Data IntensiveMore Less

MoreLess

Sageworksanalyst.com

Warning: Software Ahead

Computationally Intensive

Data IntensiveMore Less

MoreLess

Closed Pool Analysis

Sageworksanalyst.com

Warning: Software Ahead

Computationally Intensive

Data IntensiveMore Less

MoreLess

Closed Pool Analysis Vintage Analysis

Sageworksanalyst.com

Warning: Software Ahead

Computationally Intensive

Data IntensiveMore Less

MoreLess

Closed Pool Analysis Vintage Analysis Markov/Transition

Sageworksanalyst.com

Warning: Software Ahead

Computationally Intensive

Data IntensiveMore Less

MoreLess

Closed Pool Analysis Vintage Analysis DCFMarkov/Transition

Sageworksanalyst.com

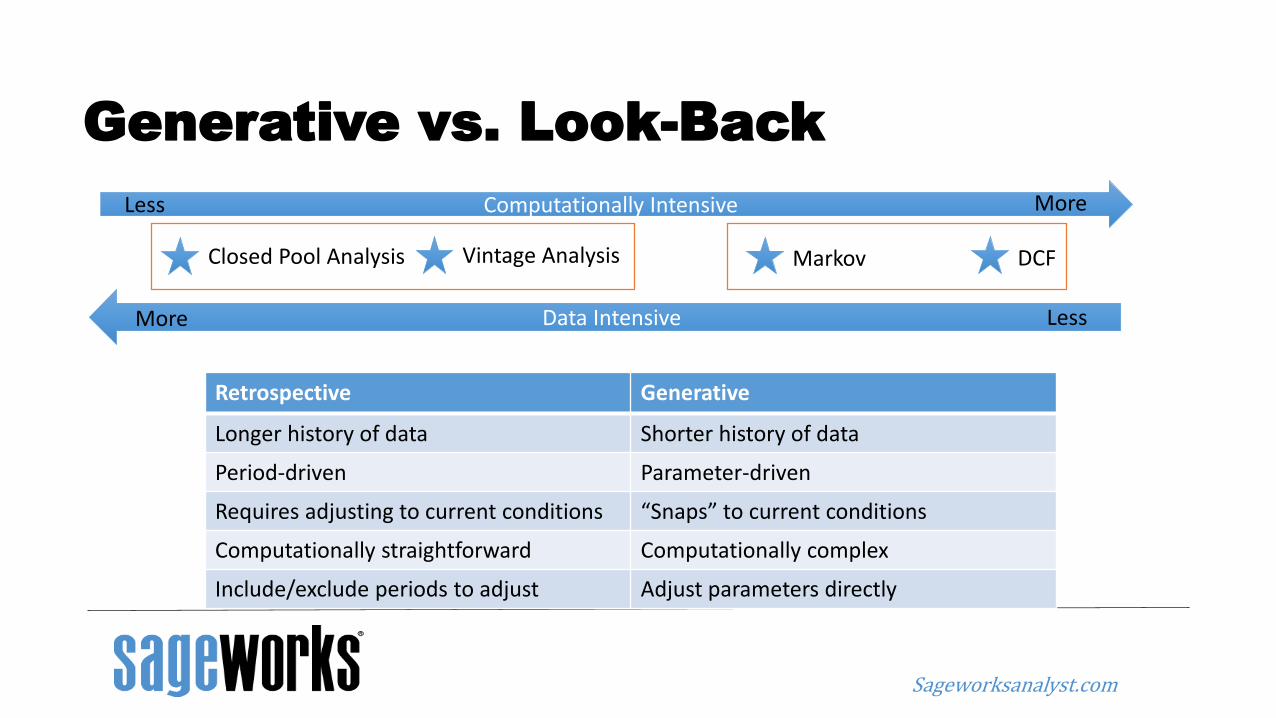

Generative vs. Look-Back

Computationally Intensive

Data IntensiveMore Less

MoreLess

Closed Pool Analysis Vintage Analysis DCFMarkov

Sageworksanalyst.com

Generative vs. Look-Back

Computationally Intensive

Data IntensiveMore Less

MoreLess

Closed Pool Analysis Vintage Analysis DCFMarkov

Retrospective Generative

Longer history of data Shorter history of data

Period-driven Parameter-driven

Requires adjusting to current conditions “Snaps” to current conditions

Computationally straightforward Computationally complex

Include/exclude periods to adjust Adjust parameters directly

Sageworksanalyst.com

DCF Principles I

• Model cashflows in the future on a per-loan (bottom up) basis• Include credit assumptions (defaulted principal, unrecovered principal)• Use periodic, not lifetime parameters in estimation• Parameters can be time-bound

• Vintage/seasoning sensitive• Model date-sensitive

• Key Parameters:• Periodic default tendency• Recovery delay• Loss given default• Prepayment rate (Amortizing)• Curtailment rate (Revolving)

17

Sageworksanalyst.com

DCF Principles I

• Model cashflows in the future on a per-loan (bottom up) basis• Include credit assumptions (defaulted principal, unrecovered principal)• Use periodic, not lifetime parameters in estimation• Parameters can be time-bound

• Vintage/seasoning sensitive• Model date sensitive

• Key Parameters:• Periodic default tendency• Recovery delay• Loss given default• Prepayment rate (Amortizing)• Curtailment rate (Revolving)

18

Sageworksanalyst.com

DCF Principles I

• Model cashflows in the future on a per-loan (bottom up) basis• Include credit assumptions (defaulted principal, unrecovered principal)• Use periodic, not lifetime parameters in estimation• Parameters can be time-bound

• Vintage/seasoning sensitive• Model date sensitive

• Key Parameters:• Periodic default tendency• Recovery delay• Loss given default• Prepayment rate (Amortizing)• Curtailment rate (Revolving)

19

Sageworksanalyst.com

DCF Principles II

• Model takes into account:• Seasoning / blend of loan maturities

• Structure

• Adjustments for current conditions

• Prepayments

• Discount Rate(s):• If available, effective yield

• Coupon rate

• Should not be forecast for variable-rate assets

20

Sageworksanalyst.com

DCF Principles III

21

Parameter Description Lines/Revolvers Amortizing

Curtailment Rate Periodic tendency of an extended principal dollar to be returned to you.

Applicable Not Applicable

Funding Rate Periodic tendency of an undrawn dollar to be drawn

Applicable Not Applicable

Prepayment Speed

Periodic tendency to receive unexpected principal payments

Not Applicable Applicable

Default Rate Periodic tendency of a loan to enter default state.

Applicable Applicable

Loss Given Default

Static loss on a loan, conditional to default event.

Applicable Applicable

Recovery Delay Static time between default event and resolution (recovery or loss)

Applicable Applicable

Sageworksanalyst.com

DCF Principles III

22

Parameter Description Lines/Revolvers Amortizing

Curtailment Rate Periodic tendency of an extended principal dollar to be returned to you.

Applicable Not Applicable

Funding Rate Periodic tendency of an undrawn dollar to be drawn

Applicable Not Applicable

Prepayment Speed

Periodic tendency to receive unexpected principal payments

Not Applicable Applicable

Default Rate Periodic tendency of a loan to enter default state.

Applicable Applicable

Loss Given Default

Static loss on a loan, conditional to default event.

Applicable Applicable

Recovery Delay Static time between default event and resolution (recovery or loss)

Applicable Applicable

Sageworksanalyst.com

Curtailment Rate Measurement Example (or funding)

23

Sageworksanalyst.com

Curtailment Rate Measurement Example

24

Sageworksanalyst.com

Generative vs. Look Back (Redux)

25

We obtain this distribution with 4 quarters of loan detail

Sageworksanalyst.com

Sampling vs. Bottom-Up

26

• Sampling:• Cash-flow some subset (~10%) of randomly sampled loans in a segment

• Churn sample period-to-period

• Arrive at a sampled rate

• Bottom-Up:• Cash-flow portfolio at loan level

• Arrive at population rate

Sageworksanalyst.com

Sampling vs. Bottom-Up

27

• Sampling:• Cash-flow some subset (~10%) of randomly sampled loans in a

segment

• Churn sample period-to-period

• Arrive at a sampled rate

• Bottom-Up:• Cash-flow portfolio at loan level

• Arrive at population rate

Volatility Issues

Sageworksanalyst.com

Sampling vs. Bottom-Up

28

• Sampling:• Cash-flow some subset (~10%) of randomly sampled loans in a segment

• Churn sample period-to-period

• Arrive at a sampled rate

• Bottom-Up:• Cash-flow portfolio at loan level

• Arrive at population rate

Volatility Reflects Portfolio

Sageworksanalyst.com

Timing and Component Estimation

• Cash from Expected Principal• Contract Payments (Amortizing)

• Curtailment (Lines)

• Cash from Interest• Contract Interest (Amortizing and Lines)

• Unexpected Principal (Prepayments)

• Cash from Recovered Defaults (Principal)

• Defaulted Principal• Defaulted Interest Not Received

29

Sageworksanalyst.com 30

Timing and Component Estimation

DCF analysis produces a time-sensitive projection of component

cashflows

Sageworksanalyst.com

Volatility in the Allowance

• Depends on: methodology• Look-back versus Look-forward

• Trivially, look-forward more volatile

• Emergent vs. Intrinsic Volatility:• Emergent: Due to mathematical properties of the model

• Intrinsic: Due to mathematical properties of the subject being modeled (credit loss expectations)

31

Sageworksanalyst.com

Volatility in the Allowance

• Depends on: methodology• Look-back versus Look-forward

• Trivially, look-forward more volatile

• Emergent vs. Intrinsic Volatility:• Emergent: Due to mathematical properties of the model

• Example: High-impact quarter rolls off analysis

• Intrinsic: Due to mathematical properties of the subject being modeled (credit loss expectations)

• Example: Uptick in prepayment activity

32

Sageworksanalyst.com

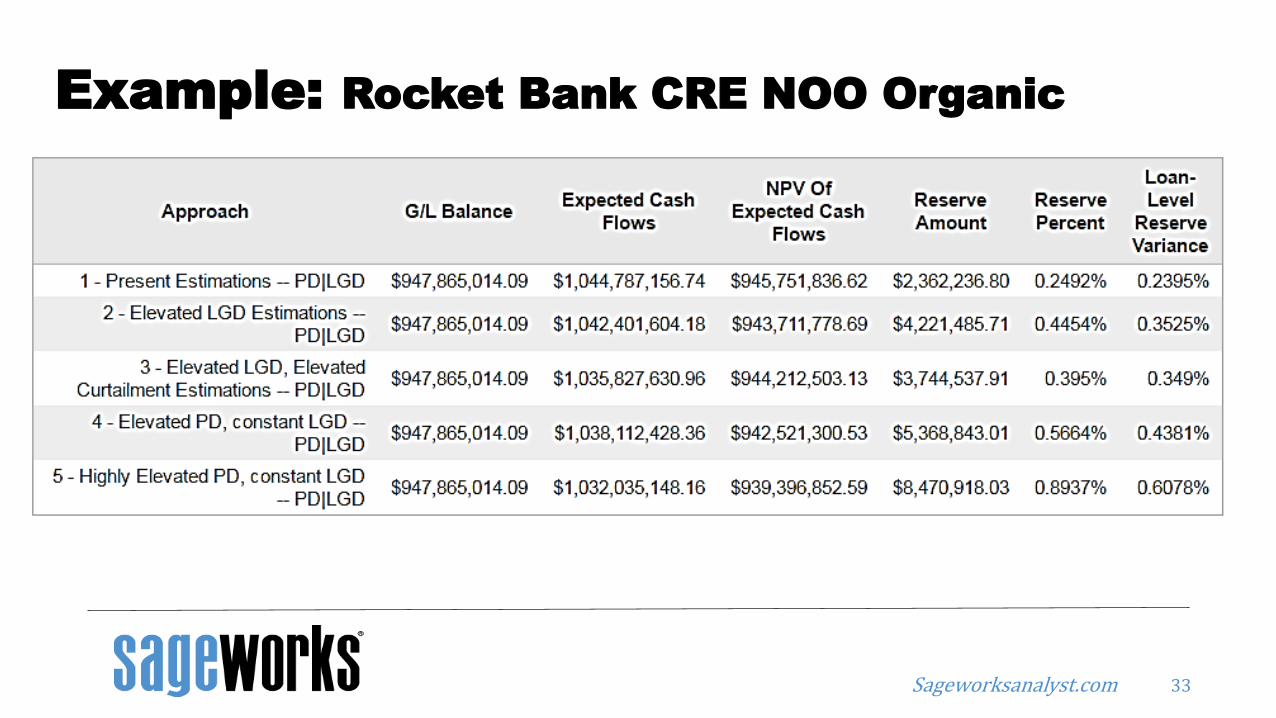

Example: Rocket Bank CRE NOO Organic

33

Sageworksanalyst.com

Example: Present versus elevated LGD

34

Present Conditions

Sageworksanalyst.com

Example: Present versus elevated LGD

35

Present Conditions

Sageworksanalyst.com

Example: Present versus elevated LGD

36

Elevated LGD Conditions

Sageworksanalyst.com

Example: Present versus elevated LGD

37

Sageworksanalyst.com

Example: Present versus elevated LGD

38

Elevated LGD Conditions

Sageworksanalyst.com

Example: Present versus elevated LGD

39

Sageworksanalyst.com

Example: Present versus elevated LGD

40

Sageworksanalyst.com

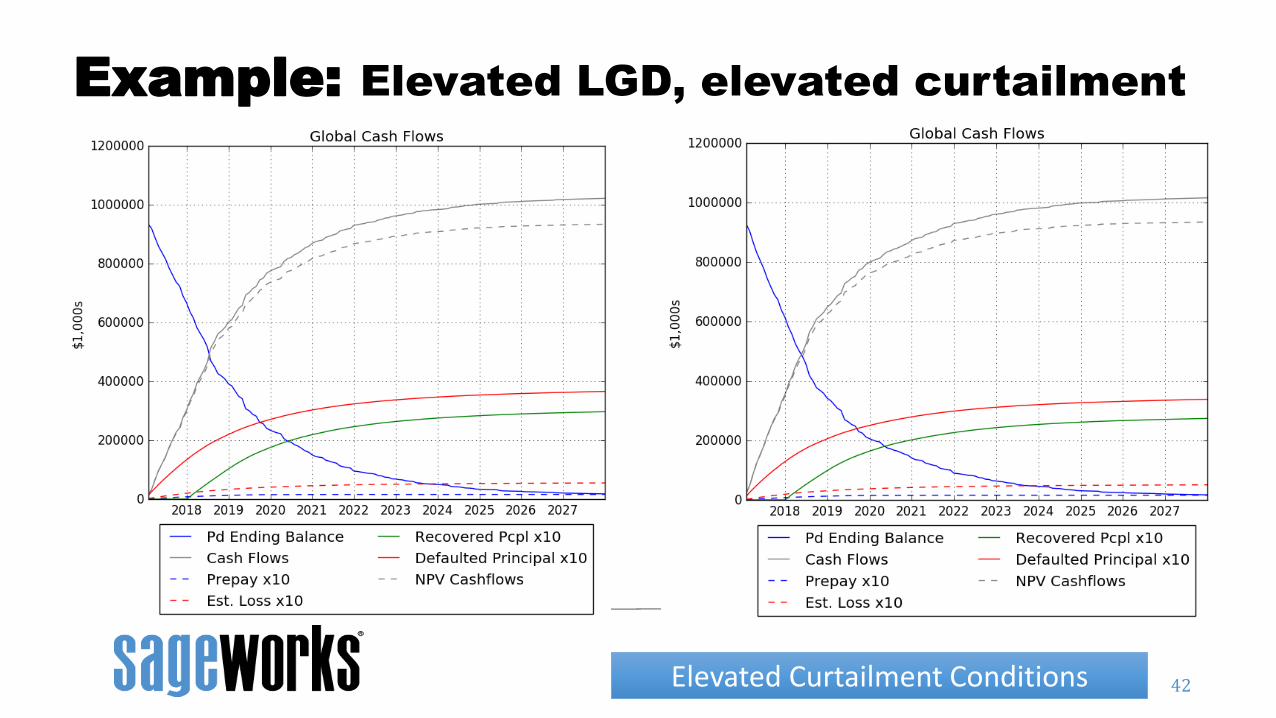

Example: Elevated LGD, elevated curtailment

41

Sageworksanalyst.com

Example: Elevated LGD, elevated curtailment

42Elevated Curtailment Conditions

Sageworksanalyst.com

Example: Elevated LGD, elevated curtailment

43Elevated Curtailment Conditions

Sageworksanalyst.com

Example: Elevated LGD, Elevated Curtailment

44

Elevated Curtailment Conditions

Sageworksanalyst.com

Example: Moderate to Severe PD climb

45

Sageworksanalyst.com

Example: Moderate to Severe PD climb

46

Sageworksanalyst.com

Example: Moderate to Severe PD climb

47

Sageworksanalyst.com

Example: Moderate to Severe PD climb

48

+1 %

Sageworksanalyst.com

Example: Moderate to Severe PD climb

49

+1 % +2 %

Sageworksanalyst.com

Example: Moderate to Severe PD climb

50

Sageworksanalyst.com

Poll Question

51

Sageworksanalyst.com

Q&A

52

Sageworksanalyst.com

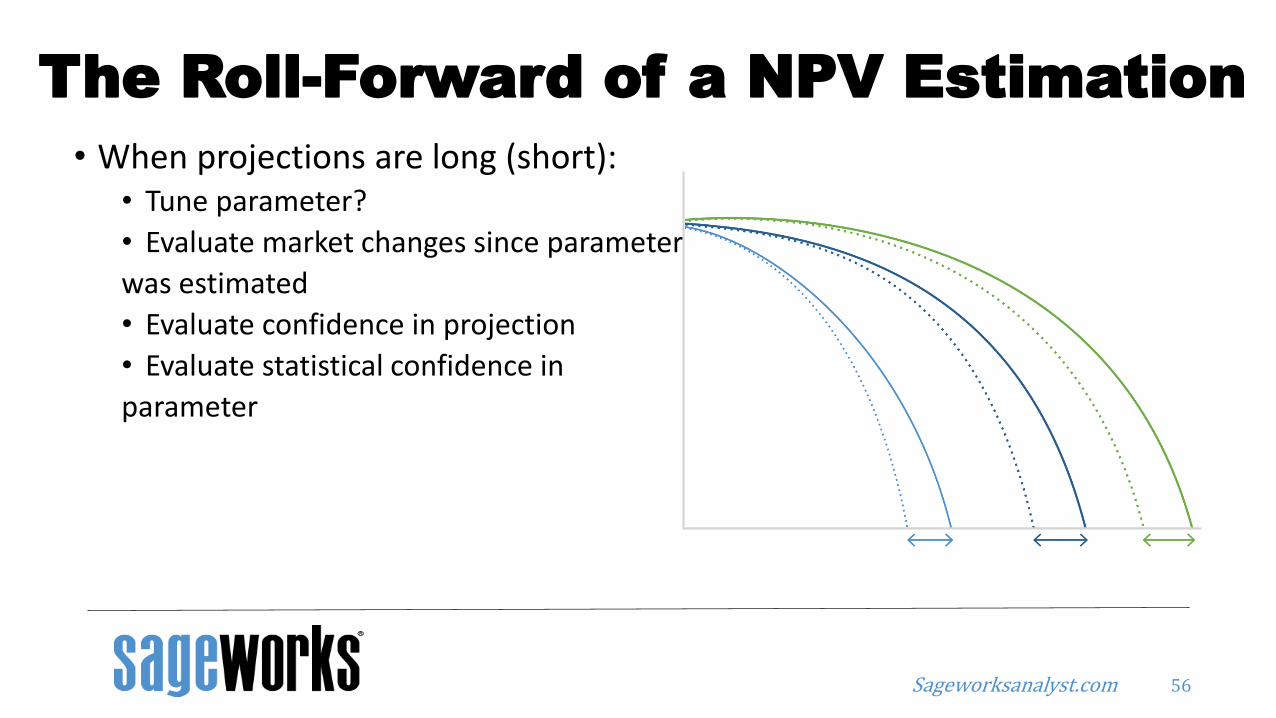

The Roll-Forward of a NPV Estimation

• We have timed, componentized estimations.

• Immediately sensitive to:• Loan maturities/terms

• Parameter estimates

• These are projections

53

Sageworksanalyst.com

The Roll-Forward of a NPV Estimation

• Periodic changes in NPV due to:• Timing

• Credit

• New Loans

54

Sageworksanalyst.com

The Roll-Forward of a NPV Estimation

• Periodic changes in NPV due to:• Timing

• May disclose and recognize as interest

income

• Credit• Provision expense

• New Loans• Provision expense

55

Sageworksanalyst.com

• When projections are long (short):• Tune parameter?

• Evaluate market changes since parameter

was estimated

• Evaluate confidence in projection

• Evaluate statistical confidence in

parameter

56

The Roll-Forward of a NPV Estimation

Sageworksanalyst.com

Time Sensitivity II: Forecasting

• Our projection is time-sensitive

57

Sageworksanalyst.com

Time Sensitivity II: Forecasting

• Our projection is time-sensitive

• Our model inputs can be time-sensitive, too

58

Sageworksanalyst.com

Time Sensitivity II: Forecasting

• Our projection is time-sensitive

• Our model inputs can be time-sensitive, too

• Immediately clarifies how to apply reasonable and supportable forecasts

• Even how to “Revert” for periods beyond our forecastable window

59

Sageworksanalyst.com

Time Sensitivity II: Forecasting

• Our projection is time-sensitive

• Our model inputs can be time-sensitive, too

• Immediately clarifies how to apply reasonable and supportable forecasts

• Even how to “Revert” for periods beyond our forecastable window

• We can also include other time-bound elements in our projection, for example:

60

Sageworksanalyst.com 61

Origination Year 1 2 3 4 5 6 Total Loss Remaining Loss

12/31/2010 0.40% 1.10% 0.60% 0.25% 0.01% 0.03% 2.39% 0.00%

12/31/2011 0.25% 0.85% 1.25% 0.40% 0.06% 0.03% 2.84% 0.03%

12/31/2012 1.25% 0.95% 0.75% 0.06% 0.04% 0.03% 3.08% 0.07%

12/31/2013 0.75% 0.65% 0.40% 0.24% 0.04% 0.03% 2.10% 0.30%

12/31/2014 0.20% 0.60% 0.75% 0.24% 0.04% 0.03% 1.85% 1.05%

12/31/2015 0.30% 0.83% 0.75% 0.24% 0.04% 0.03% 2.18% 1.88%

Average 0.53% 0.83% 0.75% 0.24% 0.04% 0.03% 2.41%

Loss Rate – Year Subsequent to Origination

Loss curve

Vintage Analysis

Sageworksanalyst.com

We can map indicators to losses…

62

5 Factors Unemployment

Sageworksanalyst.com

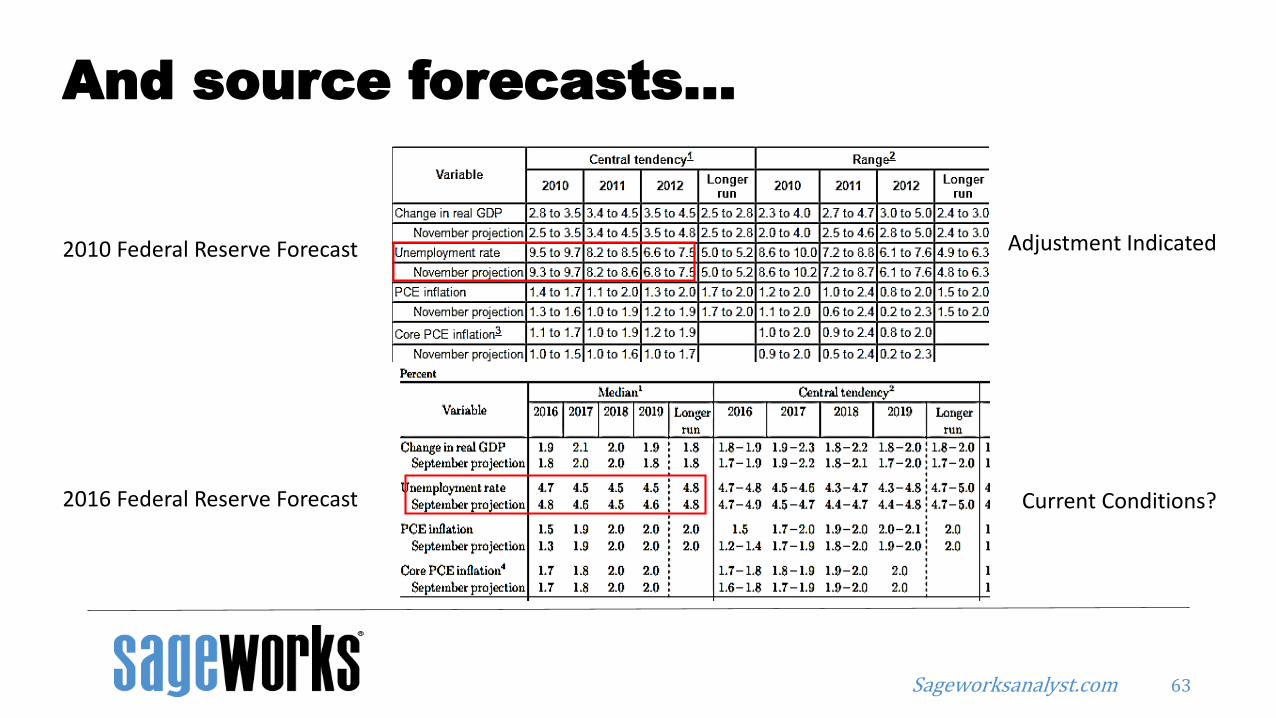

And source forecasts…

63

2010 Federal Reserve Forecast

2016 Federal Reserve Forecast

Adjustment Indicated

Current Conditions?

Sageworksanalyst.com

… and thereby apply them to our parameters

64

Sageworksanalyst.com 65

Individual Analysis

• Standard does not require specific impairment expectation

• Different credit characteristics:• Past Due Mature / Administrative Past Due• Exotic payment streams

Sageworksanalyst.com

Considerations

66

• “Balloon at maturity” assumptions

• Reliability of P&I expectations from reporting systems• Use of inferential systems to model P&I behavior

• Amortization of fees, etc.

Sageworksanalyst.com

Considerations

67

• “Balloon at maturity” assumptions

• Reliability of P&I expectations from reporting systems• Use of inferential systems to model P&I behavior

• Amortization of fees, etc.

• What to do with all that data?

Sageworksanalyst.com

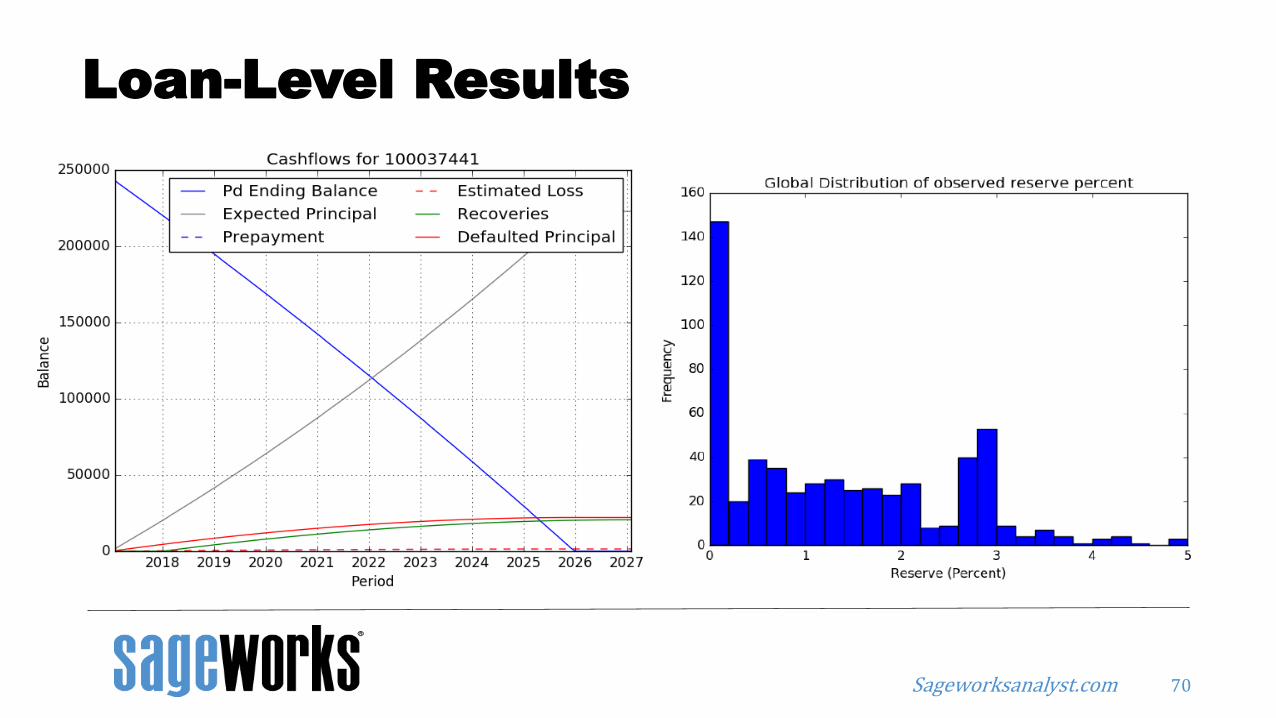

Loan-Level Results

68

Sageworksanalyst.com

Loan-Level Results

69

Sageworksanalyst.com

Loan-Level Results

70

Sageworksanalyst.com

Other Applications

71

• We have a schedule of cashflows, adjusted for credit and timing behavior

• We are discounting by e.g. coupon in our expected loss analysis.

• What if we discount buildup by• Cost of Funds + ROA/ROE Target?• Opportunity cost?

Sageworksanalyst.com

Other Applications

72

Loan Number GL Balance Cash Flow NPV (CECL) NPV (Pricing) NPV (Exit Price) IRR PD LGD

12137713 250,000 281,292 (4,074) (0) (5,679) 3.87% 3.00% 15.00%

Beginning Balance Principal Interest Prepayment Defaulted Principal Estimated Loss Estimated RecoveryEnd of Month

Balance Fees/(Expenses) Cash Flow

250,000 146,631 34,804 79,955 23,414 3,512 19,902 (342) 281,292

(250,000) 1,700.00 (250,000)

250,000 975 942 2,180 634 95 - 246,212 - 4,097

246,212 989 928 2,147 624 94 - 242,452 - 4,064

242,452 1,003 914 2,114 615 92 - 238,720 - 4,031

238,720 1,017 900 2,082 605 91 - 235,016 - 3,998

235,016 1,031 886 2,049 596 89 - 231,340 - 3,966

231,340 1,045 872 2,017 586 88 - 227,691 - 3,934

227,691 1,059 858 1,985 577 87 - 224,070 - 3,902

224,070 1,072 844 1,954 568 85 - 220,476 - 3,871

220,476 1,086 831 1,922 559 84 - 216,908 - 3,839

216,908 1,099 817 1,891 550 82 - 213,368 - 3,808

Sageworksanalyst.com

Other Applications

73

Loan Number GL Balance Cash Flow NPV (CECL) NPV (Pricing) NPV (Exit Price) IRR PD LGD

12137713 250,000 281,292 (4,074) (0) (5,679) 3.87% 3.00% 15.00%

Beginning Balance Principal Interest Prepayment Defaulted Principal Estimated Loss Estimated Recovery End of Month Balance Fees/(Expenses) Cash Flow

250,000 146,631 34,804 79,955 23,414 3,512 19,902 (342) 281,292

(250,000) 1,700.00 (250,000)

250,000 975 942 2,180 634 95 - 246,212 - 4,097

246,212 989 928 2,147 624 94 - 242,452 - 4,064

242,452 1,003 914 2,114 615 92 - 238,720 - 4,031

238,720 1,017 900 2,082 605 91 - 235,016 - 3,998

235,016 1,031 886 2,049 596 89 - 231,340 - 3,966

231,340 1,045 872 2,017 586 88 - 227,691 - 3,934

227,691 1,059 858 1,985 577 87 - 224,070 - 3,902

224,070 1,072 844 1,954 568 85 - 220,476 - 3,871

220,476 1,086 831 1,922 559 84 - 216,908 - 3,839

216,908 1,099 817 1,891 550 82 - 213,368 - 3,808

Sageworksanalyst.com

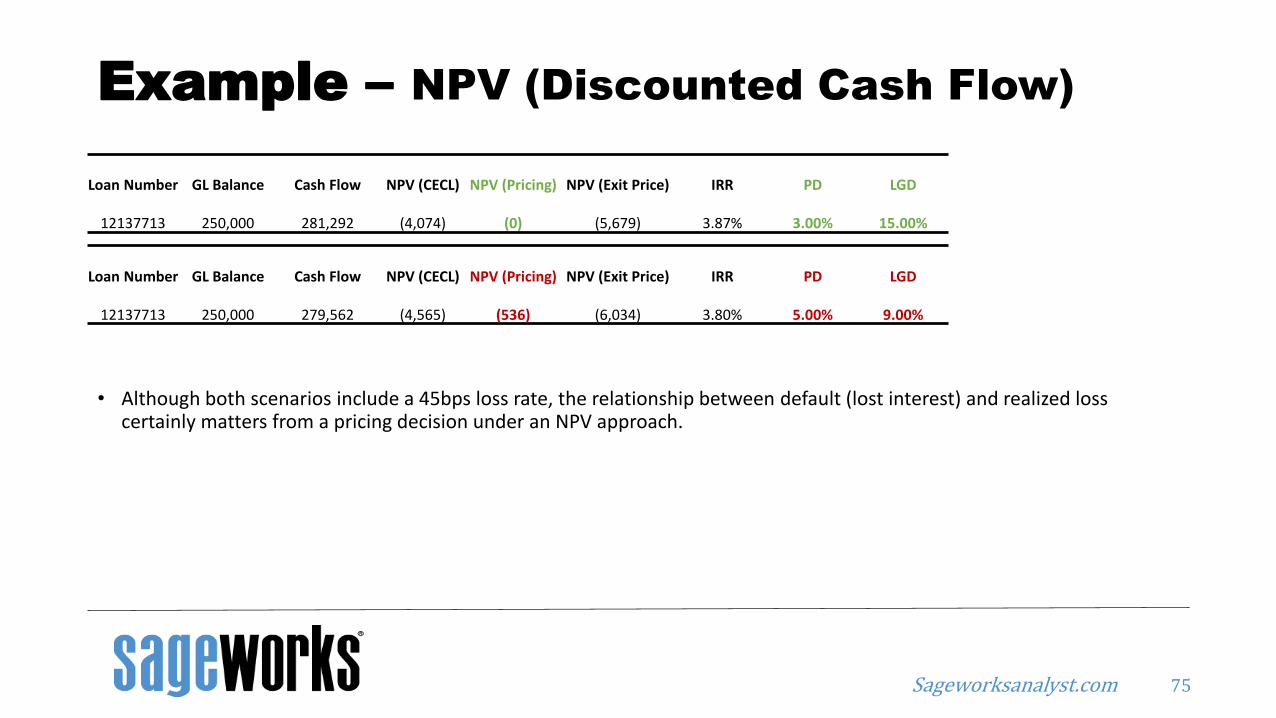

Example – NPV (Discounted Cash Flow)

74

Loan Number GL Balance Cash Flow NPV (CECL) NPV (Pricing) NPV (Exit Price) IRR PD LGD

12137713 250,000 281,292 (4,074) (0) (5,679) 3.87% 3.00% 15.00%

Loan Number GL Balance Cash Flow NPV (CECL) NPV (Pricing) NPV (Exit Price) IRR PD LGD

12137713 250,000 283,118 (4,300) (122) (6,113) 3.86% 3.00% 15.00%

• Prepayment behavior or expectation can have a significant impact on the profitability of a loan

• In the above example, a simple reduction in prepayment behavior from 10% CPR to 8% CPR would result in under-performance relative to institutional targets

• This relationship is not linear. Interest rates exceeding x% will experience an improvement in performance as prepayments slow, while interest rates below x% will experience declining profitability

• There is a certain period of time that is required in order to recover origination costs and overhead allocation

Sageworksanalyst.com

Example – NPV (Discounted Cash Flow)

75

Loan Number GL Balance Cash Flow NPV (CECL) NPV (Pricing) NPV (Exit Price) IRR PD LGD

12137713 250,000 281,292 (4,074) (0) (5,679) 3.87% 3.00% 15.00%

• Although both scenarios include a 45bps loss rate, the relationship between default (lost interest) and realized loss certainly matters from a pricing decision under an NPV approach.

Loan Number GL Balance Cash Flow NPV (CECL) NPV (Pricing) NPV (Exit Price) IRR PD LGD

12137713 250,000 279,562 (4,565) (536) (6,034) 3.80% 5.00% 9.00%

Sageworksanalyst.com

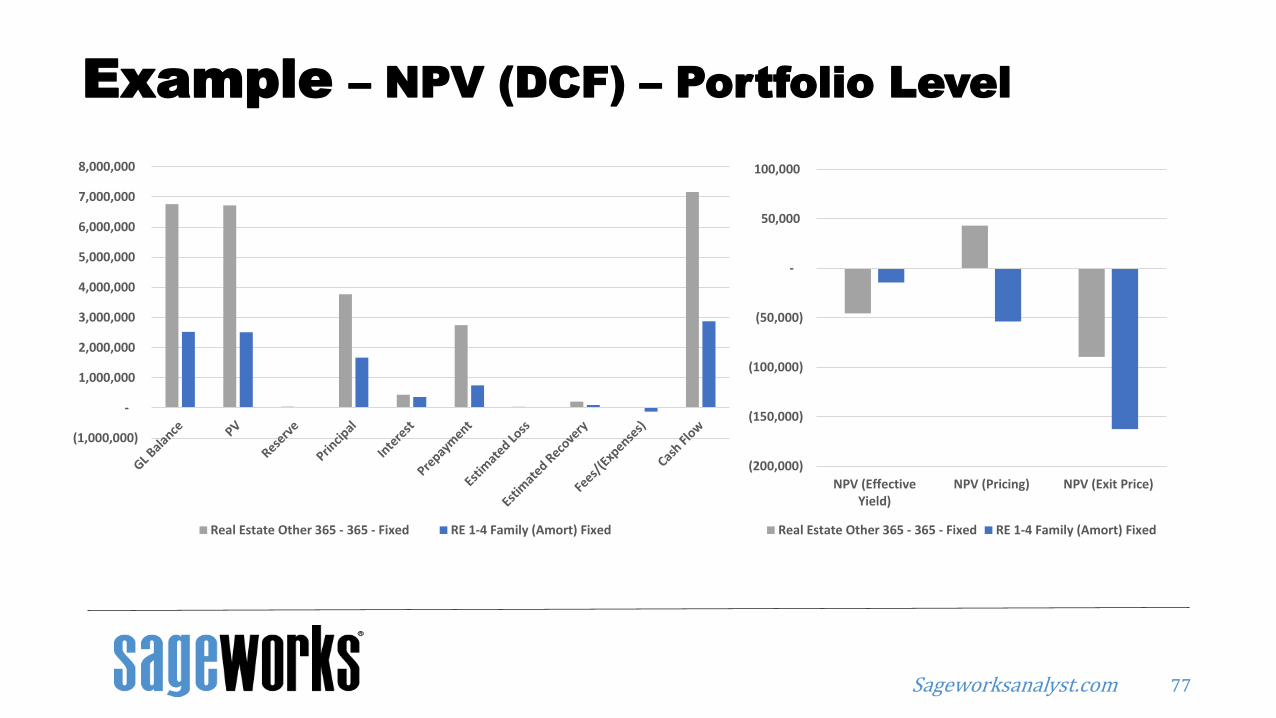

Segment GL Balance PV Reserve Reserve % NPV (Effective Yield) NPV (Pricing) NPV (Exit Price)

Real Estate Other 365 - 365 - Fixed 6,764,709 6,718,898 45,811 0.68% (45,600) 43,155 (89,417)

RE 1-4 Family (Amort) Fixed 2,522,876 2,508,479 14,397 0.57% (14,336) (53,747) (162,600)

TOTAL 9,287,585 9,227,377 60,208 0.65% (59,936) (10,592) (252,017)

Example – NPV (DCF) – Portfolio Level

76

• Portfolio level analysis contains valuable insight into the profitability of various product lines under current market conditions.

• .65% Reserve (CECL)

• -$10M below ROA objective given all assumptions; cost of funds, PD, LGD, CPR, fees, and expenses

• 2% FMV discount

Sageworksanalyst.com

(1,000,000)

-

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

Real Estate Other 365 - 365 - Fixed RE 1-4 Family (Amort) Fixed

(200,000)

(150,000)

(100,000)

(50,000)

-

50,000

100,000

NPV (EffectiveYield)

NPV (Pricing) NPV (Exit Price)

Real Estate Other 365 - 365 - Fixed RE 1-4 Family (Amort) Fixed

Example – NPV (DCF) – Portfolio Level

77

Sageworksanalyst.com

NPV (DCF): Cross Application + CECL

78

CECL

CECL

SEC Filer

Non-SEC Filer

Sageworksanalyst.com

IMP

LEM

ENT

NPV (DCF): Cross Application + CECL + Exit Price

79

Classification and Measurement

IMP

LEM

ENT

Classification and Measurement

CECL

CECL

SEC Filer

Non-SEC Filer

Sageworksanalyst.com

IMP

LEM

ENT

NPV (DCF): Cross Application + CECL + Exit Price + Pricing

80

Classification and Measurement

IMP

LEM

ENT

Classification and Measurement

CECL

CECL

IMP

LEM

ENT

IMP

LEM

ENT

Valuation, Day 2, and Pricing

Valuation, Day 2, and Pricing

SEC Filer

Non-SEC Filer

Sageworksanalyst.com

Poll Question

Sageworksanalyst.com

Poll Question

Sageworksanalyst.com

Sageworks ALLLCECL Demonstration – DCF Modeling

• Learn: » See how software can make

running a DCF manageable for all sizes of institutions

» Gain understanding on how DCF can be leveraged by other areas within the institution

» See benefits of incorporating discounting into the CECL measurement

Thursday, May 25th from 11:00am to 12:00pm ET

Sageworksanalyst.com

2017 Risk Management SummitThe premier conference for lending and risk

• Learn: » Sessions dedicated to lending, credit risk and

portfolio risk» Led by industry experts to address your

challenges around growth and risk• Network:

» More than 200 bankers from 130 institutions attend

• Apply:» 98% of attendees recommend the RMS to

community bankers» Offers actionable insights to help banks grow

profitably and mitigate risk

Denver, Colorado | September 25-27

Sageworksanalyst.com

Question & Answer

85

Upcoming Webinar

• DCF Demonstration - web.sageworks.com/dcf-demo/

Resources

• ALLL.com – join to network, discuss and learn about the ALLL

• SageworksAnalyst.com – access whitepapers and the webinar archive

• Risk Management Summit 2017 – September 25-27 in Denver, CO

Garver MoorePrincipal - Advisory Services

Contact Us:

David KistlerMarketing Manager