disclosure basel iv, crr ii & ecb new disclosure challenges for … · 2019-06-03 · 8...

TRANSCRIPT

DisclosureBasel IV, CRR II & ECBNew disclosure challenges for banks

www.pwc.com/baseliv

We give you an overview of the latest disclosure requirements .

2 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

Contents

Preface ............................................................................................................... 5Foreword .............................................................................................................. 6Disclosure requirements as part of the Basel IV package ....................................... 8Supervisors’ criticism of institutions’ disclosure practices ...................................... 9Revision of disclosure requirements in three stages ............................................. 10Disclosure requirements put on a timeline ...........................................................14

Introducing the new disclosure requirements ..................................................... 17Stage I overview– EBA GL 2016 11 (BCBS 309) ................................................... 18EBA GL on implementing Stage I in the EU ......................................................... 20Reconciliation balance sheet to risk categories – detailed look on the most challenging templates .......................................................................... 24Reconciliation book values to risk positions – detailed look on the most challenging templates .......................................................................... 26Stage II overview – BCBS 400 ............................................................................. 28Frequency and format of disclosure .................................................................... 30Significant challenges of Stage II ........................................................................ 31CRR II on implementing Stage II in the EU .......................................................... 33

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 3

Overview of Articles in draft CRR II .................................................................... 34Stage III –BCBS 432 ............................................................................................ 36Significant challenges of Stage III ....................................................................... 39ECB Guidance – Non Performing Loans .............................................................. 40

Data challenges .................................................................................................. 43Data challenges regarding EBA/GL/2016/11 ...................................................... 44

The solution: PwC’s Tools ................................................................................... 49EBA Synopsis – PwC’s tool to analyse the EBA/GL/2016/11 templates ................ 50Disclosure@ART – PwC’s tool to fill in and/or validate the disclosure templates ........................................................................................... 54Conclusion: Disclosure 2.0 ................................................................................. 60

Our Services ....................................................................................................... 63Contacts ............................................................................................................. 66

4 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

Preface

6 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

Foreword

Disclosure requirements, the pillar III of the Basel framework, are currently undergoing the most tremendous changes since their introduction in 2007. The amount, frequency and granularity of the information required to be disclosed is increased in all topics for which disclosure is required. This creates challenges for institutions with regard to the availability of the information to be disclosed but also in respect to the processes required to produce this information in a timely manner and with the required level of reliability.

When disclosure requirements were introduced as part of Basel II in 2007, they received far less attention than the huge changes introduced in pillars I and II of the framework. And in the ten years that have passed since then, supervisors have time and again criticized the efforts made by institutions to produce transparent and comparable disclosure reports. With the introduction of Basel III, regulators have started a new approach to improve disclosure by requiring institutions to use tables and templates prescribed by the regulators, thereby enforcing comparability between institutions. Also, the topic of frequency of disclosure has been revisited, turning an almost toothless tiger – asking institutions to define for themselves the adequate frequency of reporting – into binding minimum requirements.

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 7

While these efforts were initialy limited to areas such as own funds or the leverage ratio, topics were Basel III brought important changes to pillar I reporting as well, this was only just the beginning. Since then, the Basel Committee but also the EU and EBA applied these ideas – fixed format templates and increased frequency of disclosure – to all disclosure requirements, from RWA calculation to remuneration.

This brochure gives you an oversight over these proposals as well as some insights into the challenges banks face when dealing with them.

Kind regards,

Martin Neisen Stefan RöthGlobal Basel IV Leader National Basel IV Standardised Approach Workstream Leader

8 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

Disclosure requirements as part of the Basel IV package

Banks play a major role in the global economy. Sound risk management is therefore fundamental to ensure their safety and survival. During the recent financial crisis (2007-2009), banks suffered significant losses due to failures in risk management practices, insufficient capital to cover losses and inadequate liquidity reserves. In response to this, many new regulatory requirements were imposed with the objective of addressing these shortfalls. Further, the crisis has shown that the existing Pillar 3 framework failed to enable the identification of material risks or inform market participants in a sufficient manner. Over the last three years, the Basel Committee has continued to publish a number of consultation and discussion papers on how to further improve banking regulation. While not official, the banking sector coined these new capital requirements “Basel IV”.

“Basel IV” fundamentally change the disclosure requirements. In stage I the Pillar 3 framework was revised and extended (BCBS 309). Tables and templates with fixed and flexible formats were introduced to improve transparency for market participants. Stage II further extends disclosure requirements including the unrevised parts of stage I and new areas (BCBS 400) and changes of stage III (BCBS 432), which are not yet finalised at the editorial deadline, are related to finalised reforms of Basel III Framework, respectively Basel IV initiatives, amendments and new disclosure requirements.

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 9

Supervisors’ criticism of institutions’ disclosure practices

In the wake of the 2007–09 financial crisis, it became apparent that the existing Pillar 3 framework […] failed to promote the identification of a bank’s material risks and did not provide sufficient, and sufficiently comparable, information to enable market participants to assess a bank’s overall capital adequacy and to compare it with its peers. BCBS 309, S. 1

10 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

Revision of disclosure requirements in three stages

Basel III – Introduction of mandatory disclosure tables and templates as well as an increased disclosure frequency for those areas revised under the Basel III framework.

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 11

Fig. 1 Pillar 3 disclosure requirements in three stages

Extending the mandatory tables and templates as well as more frequent disclosure

of RWA determination (essentially credit risk)

Further extension of additional topics and

Basel initiatives such as TLAC, IRRBB and FRTB

Additional disclosure requirements arising mainly (but not exclusively) from the finalisation of Basel III in December 2017

Stage II(expected in

2019)

BCBS 400 CRR II

Stage III (01.01-2022)1

BCBS 432 CRR II

Stage I(31.12.2017)

BCBS 309 EBA GL 2016/11

Disclosure

1 ENC. CDC and CC1 templates will be exceptionally applicable earlier than January 2022:

12 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

Fig. 2 Pillar 3 Stage I and Stage II overview

Liquidity risk

G-SIB

Remuneration

Market risk

Accounting and RWA

Counterparty credit risk

Leverage Ratio

Counter- cyclical Buffer

Credit risk

Capital components

Securitisations

Interest rate risk in the

banking book

Stage II (BCBS 400)� a “dashboard” of

Regulatory ratios � Prudent valuation� TLAC (Total loss

absorbing capacity)� Changes in market risk

Stage I (BCBS 309/EBA GL 2016/11) Establishment of five principles for disclosure in the following areas:� Counterparty credit risk� RWA � Market risk� Securitisation (not Part of

EBA GL 2016/11)� Linkages between financial

statements and regulatory exposures

� Credit riskB

CB

S 3

09 (S

tage I)

BC

BS

400 (Stage II)

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 13

Stage II (BCBS 400/CRR II)Harmonisation of disclosure requirements including the unrevised parts of stage I and new areas:• previous BCBS papers which were not included in stage I: IRRBB, LR,

G-SIB, LCR, NSFR, Countercyclical Buffer, Capital, Remuneration • New areas included in stage II: TLAC, regulatory ratios, prudent valuation

and changes to market risk (FRTB)

CRR II: Principle of proportionality by distinguishing between institutions’ size and capital

Stage IIIHarmonisation of disclosure requirements arising from the finalised reforms of the Basel III Framework respectively Basel IV requirements

Credit riskOperational risk

Leverage ratioCVA risk

SA-RWA to bench-mark IM capital requirements

Capital distribution & composition of regulatory capital

Asset encumbrance

14 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

The BCBS revisions to the disclosure requirements are addressing shortcomings in Pillar 3 of the Basel framework. The revised disclosure requirements will enable market participants to better compare banks’ disclosures of risk-weighted assets. They form part of the Committee’s broader agenda to reform regulatory standards for banks in response to the global financial crisis.

The EBA is issuing own-initiative guidelines to ensure the harmonised and timely implementation in the EU. The revision is introducing more specific guidance and formats for disclosures through the use of tables and templates which is a significant step towards enhancing the consistency and comparability of institutions’ regulatory disclosures in accordance with Part Eight of the CRR. The ECB guidance marks an important step in addressing non-performing loans (NPL) across the euro area. It outlines measures, processes and best practices which banks should incorporate when tackling NPLs.

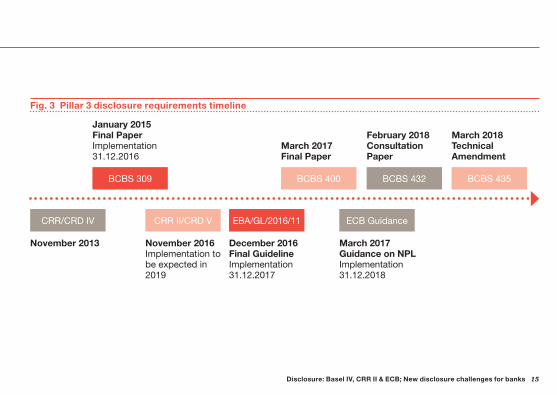

Disclosure requirements put on a timeline

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 15

CRR/CRD IV

BCBS 432

November 2013

February 2018Consultation Paper

CRR II/CRD V

November 2016 Implementation to be expected in 2019

EBA/GL/2016/11

December 2016Final GuidelineImplementation 31.12.2017

ECB Guidance

March 2017Guidance on NPL Implementation 31.12.2018

BCBS 309

January 2015Final PaperImplementation 31.12.2016

BCBS 400 BCBS 435

March 2017Final Paper

March 2018Technical Amendment

Fig. 3 Pillar 3 disclosure requirements timeline

16 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

Introducing the new disclosure requirements

18 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

Stage I overview – EBA GL 2016 11 (BCBS 309)New disclosure requirements at a glance

A key goal of BCBS 309 respectively EBA GL 2016 11 is to ensure consistency and comparability of disclosed information both among banks and over time by specifying standardised formats for disclosure. Disclosure practices following these guidelines shall be complied with for the first time at the end of the financial year 2016 on a top consolidated level. The quality of disclosed information and the internal control procedures used in the disclosure report shall be in line with financial reporting (annual, semi-annual and quarterly financial reports). Banks must establish a board-approved disclosure policy, internal controls and procedures for information subject to disclosure and publish them.

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 19

Fig. 4 Stage I – EBA/GL/2016/11 disclosure requirements

TopicNumber of tables Disclosure frequency Changes to BCBS 309

QuarterlySemi-

annually Yearly New Changed

Risk Management und Governance 4 – – 4 – 3

Groupstructure and scope of application 4 – – 4 1 2

Own funds See Delegated Regulation 1423/2013

Capital requirements 3 1 2 – 1 2

Macroprudential measures See Delegated Regulation 2015/1555 and Delegated Regulation 2014/1030

Credit risk – general 14 – 8 6 9 4

Credit risk – SA approach 3 – 2 1 – 3

Credit risk – IRB approach 5 1 2 2 – 4

Counterparty credit risk 9 1 8 – 2 7

Unencumbered assets See EBA RTS 2017/03

Market risk 6 1 4 1 1 2

Remuneration See EBA GL 2015/22

Leverage Ratio See Delegated Regulation 2016/200

Sum 48 4 26 18 14 27

20 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

EBA GL on implementing Stage I in the EUScope of application, entry into force and frequency

These guidelines apply within all G-SIIs and O-SIIs that are treated under Part 8 CRR, including partial implementation by significant banks (e.g. SSM banks) and significant subsidiaries acc. to Article 13 CRR. Supervisory authorities are able to oblige further banks to comply with the requirements. Banks that are not concerned have to adopt only the requirements with respect to Part 8 CRR. Provided tables and template specify CRR regulations, but they do not substitute them.

Scope of application

Guidelines take effect on 31.12.2017. G-SIIs are recommended to disclose parts of the templates on 31.12.2016, especially OV1, CR5, CR6, CR8, CCR3, CCR4, CCR7, MR1, MR2-A, MR2-B. Supervisory authorities are able to oblige further banks to disclose parts of the guideline. Full revision of the securitisation framework remains to be done (SEC A, SEC 1, SEC 2, SEC 3, SEC 4).

Entry into force

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 21

Frequencies for disclosure are included in BCBS 309. The EBA GL 2014/14 was supplemented and extended with regard to the requirements that should be disclosed more frequently for the institutions covered by the new EBA GL 2016/11. There are no changes of disclosure frequencies for own funds, leverage ratio and other topics outside BCBS 309.

Disclosure frequencies

22 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

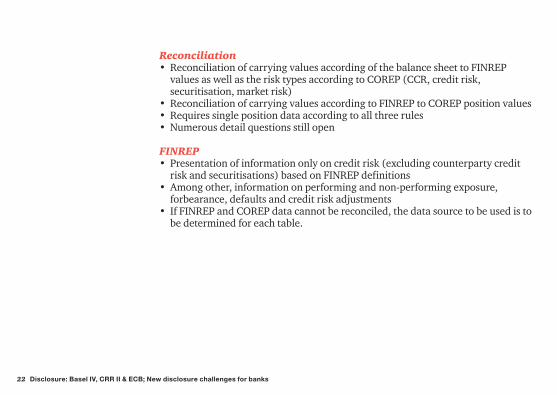

Reconciliation• Reconciliation of carrying values according of the balance sheet to FINREP

values as well as the risk types according to COREP (CCR, credit risk, securitisation, market risk)

• Reconciliation of carrying values according to FINREP to COREP position values• Requires single position data according to all three rules• Numerous detail questions still open

FINREP• Presentation of information only on credit risk (excluding counterparty credit

risk and securitisations) based on FINREP definitions• Among other, information on performing and non-performing exposure,

forbearance, defaults and credit risk adjustments• If FINREP and COREP data cannot be reconciled, the data source to be used is to

be determined for each table.

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 23

RWA flow statement• Presentation of the RWA change within a quarter by banks using internal models• Breakdown by volume and risk effects but also a separate reporting of the effects

of model changes• Allows market participants unprecedented insights into model changes (e.g. for

RWA optimization)

Counterparty Credit Risk• Separate disclosure of credit risk (in the narrower sense ) and counterparty

credit risk.• Multiple new disclosure requirements for counter party risks such as break down

of the EAD components by valuation method, comprehensive presentation of CCP transactions, collateral received and provided and credit derivatives

• SFTs aren’t clearly separable as credit risk or counterparty risk

24 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

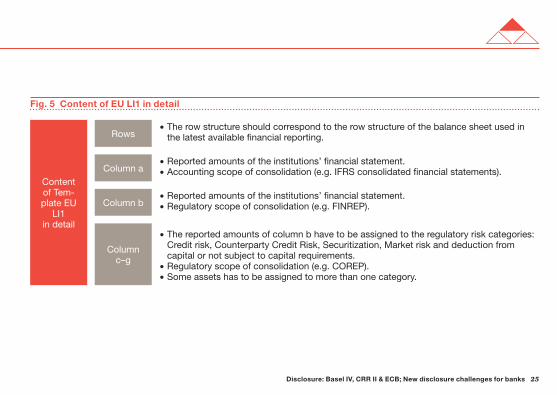

Reconciliation balance sheet to risk categories – detailed look on the most challenging templates

Reconciliation requirements are set to increase the challenge of implementation of EBA GL

Template EU LI1 Institutions should disclose differences between accounting and regulatory scopes of consolidation on group level as well as mapping of each financial statement amount to its corresponding regulatory risk categories.

The template requires consistent accounting and regulatory data warehouses. In case of using a different data basis e.g. one for column a-b and one for column c–g. an institution has to assure data-, outcome- and process-consistency: • Both warehouses should contain the same positions and regulatory data can be

assigned to risk categories (data)• Carrying values should coincide regulatory book or market values (outcome).• Manual adjustments have to be corrected in both data sets etc. (process).

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 25

Fig. 5 Content of EU LI1 in detail

Content of Tem-plate EU

LI1 in detail

Rows� The row structure should correspond to the row structure of the balance sheet used in

the latest available financial reporting.

� Reported amounts of the institutions’ financial statement.� Accounting scope of consolidation (e.g. IFRS consolidated financial statements).Column a

� Reported amounts of the institutions’ financial statement.� Regulatory scope of consolidation (e.g. FINREP).Column b

� The reported amounts of column b have to be assigned to the regulatory risk categories: Credit risk, Counterparty Credit Risk, Securitization, Market risk and deduction from capital or not subject to capital requirements.

� Regulatory scope of consolidation (e.g. COREP).� Some assets has to be assigned to more than one category.

Columnc–g

26 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

Reconciliation book values to risk positions – detailed look on the most challenging templates

Template EU LI2 Institutions should provide information on the main sources of differences (other than those due to different scopes of consolidation, which are shown in Template EU LI1) between the financial statements’ carrying value amounts and the exposure amounts used for regulatory purposes (regulatory scope of consolidation).

• The columns of EU LI2 contain one total and the risk categories corresponding to the ones of EU LI1.

• All differences between carrying values and regulatory exposure amounts have to be analysed, quantified and shown in the template.

• One key issue for example is to define the regulatory exposure amount for market risk positions in case of an implemented internal market risk model.

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 27

Fig. 6 Content of EU LI2 in detail

Content of EU LI2 in detail

Rows 1–2 Correspond to the amounts of columns of EU LI1.

Row 3=Row 1–Row 2.Row 3

Off-balance-sheet original exposures, prior and after the use of a conversion factor. Row 4

Breakdown of reasons for differences between carrying value amounts and exposure amounts considered for regulatory purposes:� Prudent valuation and prudential filters� Provisions� Regulatory netting vs. on-balance-sheet netting� ...

Row 5–x

Exposure amounts considered for regulatory purposes (COREP-reporting).Row x+1

28 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

Stage II overview – BCBS 400New disclosure requirements at a glance

The Basel Committee concentrates and complements the existing requirements for disclosure in an comprehensive framework (BCBS 400).

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 29

Fig. 7 Stage II – BCBS 400 disclosure requirements

Existing papers

Capital

Interest rate risk in the banking book

Remuneration

Stage I (BCBS 309)

Credit risk

G-SIB indicators Counterparty credit risk

Leverage Ratio Securitisation

Stage II (BCBS 400)

LCR Risk Management & RWA Key Metrics

NSFR Reconciliation balance sheet to regulatory Prudent Valuation

TLAC

Countercyclical capital buffer Market risk Market risk

Not part of EBA GL 2016/11, Implementation in Stage II

30 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

Fig. 8 Stage I and Stage II topics of frequency and format of disclosure (Stage I in red)

Tables and templates Format Reporting frequency Content

Fixed Flexible Quarterly Semiannually Annually Quantitative Qualitative

Linkages between financial statements and regulatory exposures

1 3 4 3 1

Credit risk 8 7 1 8 6 10 5

Counterparty credit risk 6 3 1 7 1 8 1

Securitisation 2 3 4 1 4 1

Risk management, Key Metrics & RWA 3 1 3 1 3 1

Market risk 3 4 1 4 2 4 3

Capital and TLAC 4 2 6 5 1

Macroprudential Measures 1 1 1 1 2

Leverage Ratio 2 2 2

Liquidity 2 1 1 1 1 2 1

Interest Rate Risk in the banking book 1 1 2 1 1

Remuneration 4 4 3 1

Total (63) 33 30 9 31 23 47 16

Frequency and format of disclosure

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 31

Significant challenges of Stage II

Key MetricsDisclosure of central regulatory parameters as tables• Own funds and own funds requirements• Total RWA• Capital buffer requirements• Leverage Ratio• LCR• NSFR• MREL requirements

MREL/TLAC• Composition, maturity and main characteristics of MREL-eligible liabilities• Ranking in the creditor hierarchy• Amount of MREL-eligible liabilities• Amount of non-MREL eligible liabilities

32 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

Market risk• New disclosure requirements based on the FRTB.• Granular disclosure of the components of the market risk capital requirements

according to the standard and internal models approach.

IRRBB• Disclosure of six predefined interest rate shock scenarios• Impact on the economic value of equity and net interest income • Qualitative information

Liquidity• Disclosure of LCR, NSFR and liquidity risk management• Details are to be deter mined by the EBA and are expected to follow the Basel

guidelines

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 33

CRR II on implementing Stage II in the EUConsideration of proportionality

The CRR II draft contains references to all the new disclosure requirements contained in the Basel Stage II document but also strengthens the principle of proportionality by distinguishing between institutions’ size and capital market orientation:

Fig. 9 Stage II – CRR II consideration of proportion

Listed Institutions Non listed Institutions

Annual Semiannual Quarterly Annual Semiannual

Large Institutions

Other Institutions

Small Institutions

Full disclosure according to part 8 of CRR

Disclosure of selected information, which cover main requirements of part 8 CRR

Disclosure of selected information, which cover partly requirements of part 8 CRR

Solely disclosure of key metrics template.

34 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

Overview of Articles in draft CRR II

Fig. 10 Stage II – CRR II Overview of Articles

Article Title

Article 430a Definitions new

Article 431 Disclosure requirements and policies changes

Article 432 Non-material, proprietary or confidential information no changes

Article 433 Frequency and scope of disclosures changes

Article 433a Disclosure by large institutions new

Article 433b Disclosure by small institutions new

Article 433c Disclosure by other institutions new

Article 434 Means of disclosures changes

Article 434a Uniform disclosure formats new

Article 435 Disclosure of risk management objectives and policies small changes

Article 436 Disclosure of the scope of application changes

Article 437 Disclosure of own funds small changes

Article 437a Disclosure of on own funds and eligible liabilities requirements new

Article 438 Disclosure of capital own funds requirements and risk weighted exposure amounts changes

Article 439 Disclosure of exposures to counterparty credit risk changes

Article 440 Disclosure of countercyclical capital buffers small changes

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 35

Article Title

Article 441 Disclosure of indicators of global systemic importance no changes

Article 442 Disclosure of exposures to credit risk and dilution risk changes

Article 443 Disclosure of encumbered and unencumbered assets changes

Article 444 Disclosure of use of the standardised approach small changes

Article 445 Disclosure of exposures to market risk under the standardised approach changes

Article 446 Disclosure of operational risk management changes

Article 447 Disclosure of key metrics new

Article 448 Disclosure of exposures to interest rate risk on positions not held in the trading book changes

Article 449 Exposure to securitisation positions changes

Article 450 Disclosure of remuneration policy changes

Article 451 Disclosure of leverage ratio small changes

Article 451a Disclosure of liquidity requirements for credit institutions and systemic investment firms new

Article 452 Disclosure of the use of the IRB Approach to credit risk changes

Article 453 Disclosure of the use of credit risk mitigation techniques changes

Article 454 Disclosure of the use of the Advanced Measurement Approaches to operational risk no changes

Article 455 Use of Internal Market Risk Models changes

36 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

Stage III – BCBS 432Major proposals under consultation

Finalisation of Basel IIIBCBS 432 comprises revisions (revised disclosure requirements for credit risk, operational risk, leverage ratio, CVA and overview templates on risk management, RWA and key prudential metrics) and additions (disclosure requirements to benchmark the internal model RWA according to standardised approaches) as a result of the finalisation of the “Basel IV” initiative, new disclosure requirements on asset encumbrance and capital distribution as well as amendments to the scope of application of disclosure on the composition of regulatory capital.

Asset encumbranceNew disclosure requirement on banks’ encumbered and unencumbered assetsPreliminary overview on the extent to which banks’ assets remain available to creditors in the event of insolvency to be provided this way to market participants

Capital distribution constraints (CDC)New disclosure requirement on the capital ratios of a bank which, if breached, would result in national supervisors imposing CDC In case of G-SIBs the leverage ratio shall be additionally disclosed due to the im-position of a leverage ratio buffer requirement to G-SIBs according to the finalized Basel III

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 37

Composition of regulatory capitalRevised application scope for the disclosures on the composition of regulatory capital so as to additionally capture resolution groupsBetter understanding and benchmarking of the capital positions of resolution groups by the investors

BCBS 432 comprises revisions (revised disclosure requirements for credit risk, operational risk, leverage ratio, CVA and overview templates on risk management, RWA and key prudential metrics) and additions (disclosure requirements to benchmark the internal model RWA according to standardised approaches) as a result of the finalisation of the “Basel IV” initiative, new disclosure requirements on asset encumbrance and capital distribution as well as amendments to the scope of application of disclosure on the composition of regulatory capital.

38 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

Fig. 11 Stage III – Frequency and format of disclosure

Tables and templates Format Reporting frequency Content

Fixed Flexible Quarterly Semiannually Annually Quantitative Qualitative

Credit risk 2 2 0 3 1 3 1

Operational risk 3 1 0 0 4 3 1

Leverage ratio 2 0 2 0 0 2 0

Credit valuation adjustments 4 2 1 3 2 4 2

Benchmarking 2 0 1 1 0 2 0

Overview of risk management, key prudential metrics and RWA

2 0 2 0 0 2 0

Asset encumbrance 1 0 0 1 0 1 0

Capital distribution constraints 0 1 0 0 1 1 0

Composition of capital and TLAC 1 0 0 1 0 1 0

Total (23) 17 6 6 9 8 19 4

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 39

Significant challenges of Stage III

Asset Encumbrance Capital distribution constraints Composition of regulatory capital

� The proposed disclosure of assets encumbered due to the banks’ transaction with central banks could be sensitive

� Such disclosure should not create friction in central banks’ monetary operations or provision of liquidity to banks.

� The proposed disclosure, under certain circumstances, could lead to a bank disclosing its Pillar 2 requirements, which could be deemed by its national supervisor to be sensitive information.

� In this regard, the template would be mandatory for banks only when required by their national supervisor.

� The extended application scope of the pertinent disclosures to resolution groups can be artificial due to the fact that the scope of consolidation of a resolution group may not be the same as that applied to banking groups under the Basel framework (e.g. different treatment of insurance subsidiaries under both frameworks).

� It may also result in a higher disclosure burden for G-SIBs with a Multiple Point of Entry (MPE) resolution strategy compared with those relying on an Single Point of Entry (SPE) resolution strategy.

40 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

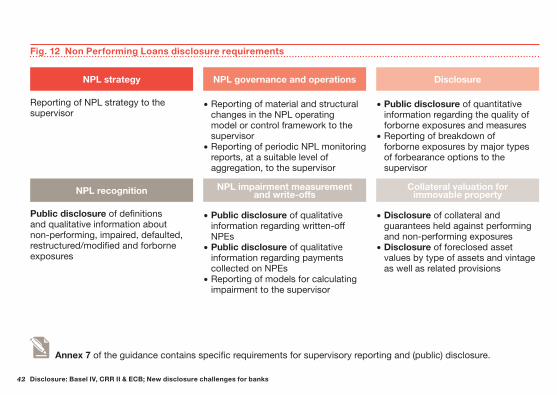

ECB Guidance – Non Performing Loans

Now we’re leaving the world of Basel and Stages I-III and are heading to non performing loans (NPL) as it is coined as a key risk by ECB. We show how to manage new requirements such as transparency of NPLs.

ContextECB banking supervision has high lighted credit risk and heightened levels of non-performing loans as key risks facing euro area banks. The process of balance sheet repairs requires proper identification and management of NPLs.

Transparency is an important building block of this proper management. ECB banking supervision has identified a number of best practices that are set out in this public guidance.

ScopeApplicable to all significant institutions (SI) supervised directly under the SSM including their international subsidiaries Chapters 2 and 3 may be more relevant for “high NPL banks”. It is expected that banks will apply the guidance proportionately and with appropriate urgency, in line with the scale and severity of the NPL challenges they face.

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 41

The NPL guidance is currently non-binding in nature but recommended by the ECB. The guidance is taken into consideration in the SSM regular Supervisory Review and Evaluation Process. Non-compliance may trigger supervisory measures. The guidance does not intend to substitute or supersede any applicable regulatory or accounting requirement.

DisclosureSpecific disclosures should improve stakeholders’ confidence in banks’ balance sheets and ultimately increase the willingness of markets to play a role in the management of NPLs for which high quality information has become available.

In order for banks to convey their risk profiles comprehensively to market participants, the ECB recommends, therefore, that they disclose additional NPL related information to that required under Part 8 CRR (Article 431). In order to ensure consistency and comparability, the expected enhanced disclosures on NPLs should start from 2018 reference dates.

42 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

Fig. 12 Non Performing Loans disclosure requirements

NPL strategy

NPL recognition

NPL governance and operations

NPL impairment measurement and write-offs

Disclosure

Collateral valuation for immovable property

Reporting of NPL strategy to the supervisor

Public disclosure of definitions and qualitative information about non-performing, impaired, defaulted, restructured/modified and forborne exposures

� Reporting of material and structural changes in the NPL operating model or control framework to the supervisor

� Reporting of periodic NPL monitoring reports, at a suitable level of aggregation, to the supervisor

� Public disclosure of qualitative information regarding written-off NPEs

� Public disclosure of qualitative information regarding payments collected on NPEs

� Reporting of models for calculating impairment to the supervisor

� Public disclosure of quantitative information regarding the quality of forborne exposures and measures

� Reporting of breakdown of forborne exposures by major types of forbearance options to the supervisor

� Disclosure of collateral and guarantees held against performing and non-performing exposures

� Disclosure of foreclosed asset values by type of assets and vintage as well as related provisions

Annex 7 of the guidance contains specific requirements for supervisory reporting and (public) disclosure.

Data challenges

Annex 7 of the guidance contains specific requirements for supervisory reporting and (public) disclosure.

44 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

The new disclosure requirements have a significant impact on the topics data and IT. The new requirements demand a high degree of data granularity and volume. The use of different systems and models makes it difficult to gather the required information. One of the major challenges is the required reconciliation of different data sources such as accounting, FINREP and COREP which is demanded by the „Guidelines on disclosure requirements under Part Eight of Regulation (EU) 575/2013“ (EBA GL/2016/11). The transition of balance-sheet positions to regulatory figures is required. Therefore, book values per balance-sheet position need to be reconciled to the corresponding value according to FINREP/regulatory consolidation. Further, the FINREP values need to be assigned to the regulatory risk categories (credit risk, counterparty risk, securitization and market risk). Finally, FINREP information e.g. accumulated depreciation or credit risk adjustments in the respective period need to broken down into the risk categories to get the exposure amounts used for regulatory purposes/COREP.

Another challenge is the required transition of the development of the RWA during the period. Therefore, the additional value adjustments need to be published, separated by the components (e.g. close-out uncertainty, early termination, model risk, operational risk).

Data challenges regarding EBA/GL/2016/11

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 45

Furthermore, the disclosure information published will be used by the institutes as an additional instrument for management and control purposes and therefore will have a greater impact on the internal analytical activities. Besides the impacts mentioned, the disclosure information need to be published more frequently. This requires that historical data is available at a granular level which increases the storage requirements.

The boxes stated here represent only a small selection of challenges of the new disclosure requirements:

Consistency of the regulatory and accounting data is required

Transition of balance-sheet positions to regulatory figures

Change of decentralised and Silo architectures to an integrated financial and risk architecture

Data quality

Historical data increases the storage requirements

Data granularity and volumeDisclosure information as management instrument

Increased frequency of disclosure

46 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

The requirements of the “Guidelines on disclosure requirements under Part Eight of Regulation (EU) 575/2013” (EBA GL 2016/11) lead to the challenge of enhance data harmonisation from various systems with different data models and purposes. Furthermore, the processes need to be adjusted in order to be able to disclosure more information in shorter intervals.

At the moment, disclosure processes are characterised by a high degree of manual data supplies and non-standardised communication steps. These processes are slow, highly resource-intensive and error-prone. In the future, data models need to be harmonised and often extended to ensure that the relevant information is simultaneously available for FINREP, COREP and disclosure.

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 47

Implementation of digitalisation solutions in standardised form

Solutions link data to SmartNotes, so data becomes analysable for management reporting

IT investments are obligatory for regulatory purpose… those improve controllability and ensure competitiveness

Automatisation and IT collaboration assist users’ version control and provide automatical workflows

Working with known documents formats as well as preparation of special formats

Automatically updated figures within texts to ensure consistency with tables published

48 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

To fulfil the upcoming disclosure requirements the banks should implement a standardised data management

Fig. 13 Solution regarding the data challenges due to the new disclosure requirements

� faster and uniform data analysis for business models

� consolidated and harmonised data

Accounting RegulatoryReporting

Riskmanagement

Data Quality

Data Analytics

Data Strategy

� fulfilment of regulatory requirements

� quality regarding the overall bank control

� Stronger use of professional rules

� possibility of faster response to ECB requests

� structured ad-hoc analysis and reporting

� use of regulatory data pools for analytical methods

� better data knowledge � better use of relevant

data� transparency about

the use of modern technologies

� awareness about data responsibility

� clear definition of responsibility

� clear definition of the escalation steps

Data Integration

Data Gover- nance

The solution:PwC’s Tools

50 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

In order to be prepared for the upcoming disclosure data challenges on 31 of December 2017, an efficient analysis regarding the information required and available is the sine qua non. Only if a bank is capable to collect the data for the upcoming supervisory requirements according to the EBA/GL/2016/11, it can better respond to future disclosure challenges. In particular the fact that the disclosure requirements require a large number of information regarding regulatory and accounting data, different departments and systems of a bank are affected.

PwC provides the solution … Meet PwC’s “Synopsis” for analysing the EBA/GL/2016/11.

PwC’s Excel based Synopsis was exclusively developed to cater our clients needs and to support them with regards to the implementation and realisation of supervisory disclosure requirements.

Our Synopsis is flexible and dynamically at use and ensures the analysis of the data required in the EBA/GL/2016/11.

EBA Synopsis – PwC’s tool to analyse the EBA/GL/2016/11 templates

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 51

We would be pleased to introduce you to the Synopsis and to present its variety of useful applications and functions in a personal face – to – face meeting.

Fig. 14 PwC‘s Synopsis to analyse the EBA/GL/2016/11 (Template EU CRB-B)

52 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

The PwC’s Synopsis provides the following applications:• Analysis regarding the required scope• Analysis regarding the mapping of reporting templates (e.g. COREP, FINREP)• Analysis regarding the mapping between the disclosure templates to ensure

consistency• Analysis regarding the resource estimation• Analysis regarding the procurement of information and data• …

The amount of detailed disclosure requirements represents a huge challenge. But identified challenges can be turned into advantages.

Be at the forefront and determine all upcoming challenges for your bank. Use PwC’s Synopsis to analyse the information and data required. This is the first step to estimate the impacts of the EBA/GL/2016/11 requirements on your business.

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 53

Fig. 15 PwC‘s Synopsis to analyse the EBA/GL/2016/11 (Template EU CR8)

54 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

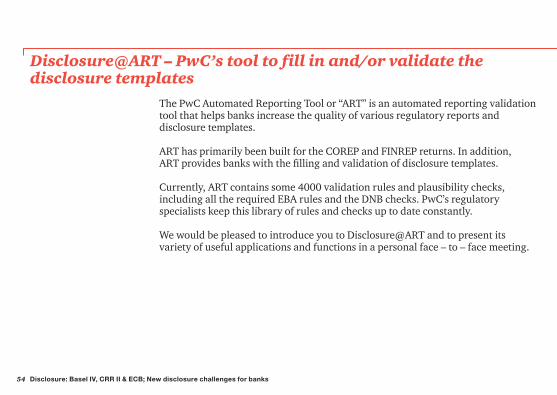

Disclosure@ART – PwC’s tool to fill in and/or validate the disclosure templates

The PwC Automated Reporting Tool or “ART” is an automated reporting validation tool that helps banks increase the quality of various regulatory reports and disclosure templates.

ART has primarily been built for the COREP and FINREP returns. In addition, ART provides banks with the filling and validation of disclosure templates.

Currently, ART contains some 4000 validation rules and plausibility checks, including all the required EBA rules and the DNB checks. PwC’s regulatory specialists keep this library of rules and checks up to date constantly.

We would be pleased to introduce you to Disclosure@ART and to present its variety of useful applications and functions in a personal face – to – face meeting.

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 55

Fig. 16 PwC‘s Automated Reporting Tool (ART)

56 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

Fig. 17 Disclosure@ART: PwC’s tool to fill in and validate the disclosure templates

1. Data 2. Filling 3. Validation 4. Check

Scenario 1Checks 100% passed

Scenario 2Checks <100% passed

Provide .xml, .xls or .xbrl COREP and FINREP

templates

Upload of the file in the ART tool: automatic

filling of the CRR and EBA disclosure

templates

After filling: run of PwC plausibility

checks and validation rules

Analysis of results and update of data

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 57

Fig. 18 Disclosure@ART: PwC’s tool to validate the disclosure templates

1. Data 2. Validation 3. Check 4. Disclosure

Scenario 1Checks 100% passed

Scenario 2Checks <100% passed

Provide .xlsx disclosure templates (CRR and

EBA GL)

Upload of the file in the ART tool: run of PwC

plausibility checks

Disclosure of the templates in the disclosure report

Analysis of results and update of data

58 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

The boxes stated here represent only a small selection of challenging data requirements regarding the EBA/GL/2016/11:

Accumulated write-offs

RWA flow statements of market risk exposures Changes in stock of

general and specific credit risk adjustments

RWA flow statements of CCR exposure

Non-performing and forborne exposures

Effect on RWAs of credit derivatives used as CRM techniques

Differences between accounting and regulatory scopes of consolidation and mapping of financial statement categories with regulatory risk categories

Ageing of past-due exposures

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 59

The figure stated here represent topics, that are mainly affected by the EBA/GL/2016/11 disclosure requirements:

Fig. 19 Interaction of EBA/GL/2016/11 disclosure requirements and other requirements

Solvency

EBA/GL/2016/11

RWA

CR SA IRB

FINREP NPL

CCR …

60 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

Conclusion: Disclosure 2.0

Transparency, comparability and reconciliationBy specifying mandatory sample tables and templates for all areas of banking supervision, transparency and comparability are to be strengthened, both between institutions and over time.

The EU guidelines have largely been aligned to the Basel guidelines and are carefully adapted to EU specifics.

More frequent, more comprehensive and more formalized disclosureThe scope of the information to be disclosed, in particular of the quantitative data, is growing through the use of the mandatory tables and templates.

At the same time, the frequency of disclosure increases as well as the volume of quarterly and, in particular, semi-annual disclosure, also for small and medium-sized institutions.

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 61

A key goal of the revised Pillar 3 disclosures is to improve comparability and consistency of disclosures. To this end, the document introduces harmonised templates.

Data availability and reconcilability between data sources are key challengesThe main challenges of the new disclosure requirements are, on the one hand, the required reconciliation between different data sources, in particular accounting, FINREP and COREP.

Likewise, the increasing scope and frequency of disclosure lead to the need to adapt existing disclosure processes.

62 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

Our Services

64 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

Our ExpertiseWhether regarding the Basel Committee, EU-regulation or national legislation – we use our established know-how of the analysis and implementation of new supervisory regulation to provide our clients with high-quality services. Embedded into the international PwC network, we have access to the extensive knowledge of our experts around the world.

PwC can support you in all aspects of getting compliant with the new Disclosure regulatory requirements.

PwC can draw on long lasting experience of implementing new regulatory requirements by supporting a number of banks in completing quantitative impact studies prior to the implementation of Basel II and Basel III and by the functional and technical implementation of the final regulations.

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 65

About usPwC helps organisations and individuals create the value they’re looking for. We’re a network of firms in 158 countries with more than 236,000 people who are committed to delivering quality in assurance, tax and advisory services. Tell us what matters to you and find out more by visiting us at www.pwc.com. Learn more about PwC by following us online: @PwC_LLP, YouTube, LinkedIn, Facebook andGoogle+.

66 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

Global Basel IV LeaderMartin Neisen PartnerFriedrich-Ebert-Anlage 35–3760327 Frankfurt am MainTel: +49 69 9585-3328Fax: +49 69 [email protected]

AustriaGerald BrandstätterTel: +43 1 501 [email protected]

Australia Katherine Martin Tel: +61 2 8266-3303 [email protected]

BelgiumBirgit SchalkTel: +32 27 104-315 [email protected]

CEEJock NunanTel: +381 [email protected]

CyprusElina ChristofidesTel: +357 22555-718 [email protected]

DenmarkLars NorupTel: +45 [email protected]

Contacts

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 67

EstoniaAgo ViluTel: +372 [email protected]

FinlandMarko LehtoTel: +358 20 [email protected]

FranceMarie-Hélène Sartorius Tel: +33 1 56575-646 [email protected]

GermanyMatthias EisertTel: +49 69 [email protected]

GreeceGeorgios ChormovitisTel: +30 210 [email protected]

HungaryEmöke Szántó-KapornayTel: +36 [email protected]

IrelandCiaran CunnininghamTel: +353 1 [email protected]

IsraelEyal Ben-AviTel: +972 3 [email protected]

68 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

ItalyGabriele GuggiolaTel: +39 346 [email protected]

LatviaTereze LabzovaTel: +371 [email protected]

LithuaniaRimvydas JogelaTel: +370 5 [email protected]

LuxembourgJean-Philippe MaesTel: +352 49 [email protected]

MaltaFabio AxisaTel: +356 [email protected]

Netherlands Abdellah M’barkiTel: +31 88 [email protected]

PolandPiotr BednarskiTel: +48 22 [email protected]

Zdzislaw SuchanTel: +48 22 [email protected]

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 69

PortugalLuís BarbosaTel: +351 213 [email protected]

RussiaNikola [email protected]

SerbiaJock NunanTel: +381 [email protected]

SloveniaPawel PeplinskiTel: +386 1 [email protected]

South AfricaIrwin Lim Ah TockTel: +27 11 [email protected]

Czech RepublikMike JenningsTel: +420 251 [email protected]

Spain/AndorraJose Alberto DominguezTel: +34 915 684-136 [email protected]

70 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

SwedenAndré WallenbergTel: +46 10 [email protected]

SwitzerlandManuel PlattnerTel: +41 58 [email protected]

UkraineLyudmyla PakhuchaTel: +380 44 [email protected]

United Arab EmiratesBurak ZatiturkTel: +971 4 [email protected]

United KingdomNigel WillisTel: +44 20 [email protected]

Agatha PontikiTel: +44 20 7213-3484 [email protected]

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 71

Notes

72 Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks

Disclosure: Basel IV, CRR II & ECB; New disclosure challenges for banks 73

www.pwc.de

PricewaterhouseCoopers GmbH Wirtschaftsprüfungsgesellschaft adheres to the PwC-Ethikgrundsätze/PwC Code of Conduct (available in German at www.pwc.de/de/ethikcode) and to the Ten Principles of the UN Global Compact (available in German and English at www.globalcompact.de).

© April 2018 PricewaterhouseCoopers GmbH Wirtschaftsprüfungsgesellschaft. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers GmbH Wirtschaftsprüfungsgesellschaft, which is a member firm of PricewaterhouseCoopers International Limited (PwCIL). Each member firm of PwCIL is a separate and independent legal entity.