digital payments 2017 - static2.statista.com · well-known providers of mobile wallets are applepay...

TRANSCRIPT

December 2017

FinTech Report 2017 –Digital PaymentsStatista Digital Market Outlook – Segment Report

Market structure, contacts and imprint0402

01 03Segment overview

▪ Market scope

▪ Customer benefit

▪ Future developments, assumptions and sensitivity analysis

KPI comparison

▪ Market KPI comparison by region in the form of charts

▪ Market KPI comparison by region in the form of tables

Deep Dive

▪ Seamless integrated payment features

▪ Biometric authentication

▪ Blockchain

2

Agenda

3

Digital Commerce

Segment overview (1/6)

Mobile POS Payments

FinTech Digital Payments: Products and services

▪ Consumer transactions made via the Internet which are directly related to online shopping for products and services

▪ Transactions can be made via various payment methods (credit cards, direct debit, invoice, or online payment providers, such as PayPal and AliPay)

▪ Transactions at the point-of-sale that are processed via smartphone applications (so-called “mobile wallets”)

▪ Well-known providers of mobile wallets are ApplePay and Samsung Pay. The payment in this case is made by a contactless interaction of the smartphone app with a suitable payment terminal belonging to the merchant.

4

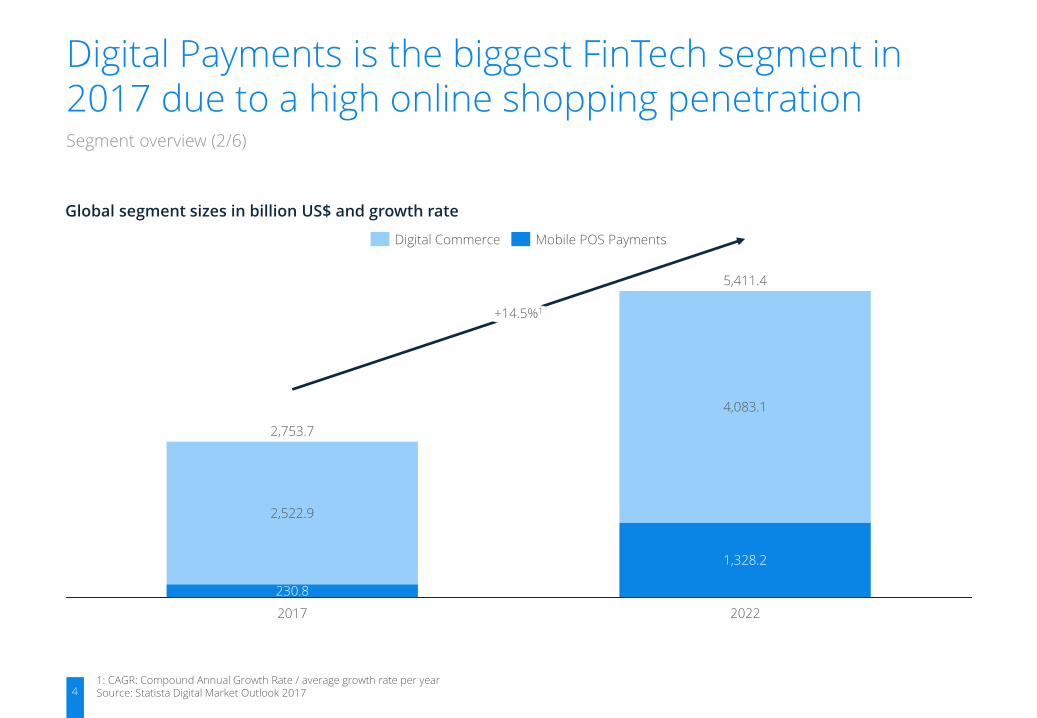

Global segment sizes in billion US$ and growth rate

Segment overview (2/6)

1: CAGR: Compound Annual Growth Rate / average growth rate per yearSource: Statista Digital Market Outlook 2017

Digital Payments is the biggest FinTech segment in 2017 due to a high online shopping penetration

4,083.1

+14.5%1

5,411.4

1,328.2

2022

230.8

2,753.7

2017

2,522.9

Mobile POS PaymentsDigital Commerce

5

Customer benefit

In this report, Digital Payments are defined as non-cash transactions processed through digital channels. This includes:

▪ Digital Commerce: All physical and virtual goods or services purchased online

▪ Mobile Payments: All transactions at the point-of-sale in retail locations processed via personal smart devices.

The digitalization of financial services brings along a disruptive change for the industry when it comes to the checkout process (online purchases) and the payment process at the POS (offline purchases). Digital Payments can hence be considered as the next evolutionary step towards further financial services that might replace classic, old-fashioned payment methods (from cash to credit/debit card to mobile, digital wallets).

Due to the unstoppable rise of smartphones and online (and mobile) shopping, the FinTech revolution is already in full swing, especially in the field of Digital Payments. The key question in this context is: To what extent will Digital Payments substitute cash transactions? The answer to this strongly depends on customer behavior (in terms of the digital commerce development) and customer benefits associated with using digital wallets at the POS.

The most important driving forces for the adoption of digital payment services are the minimal entrance barriers for both consumers and

Segment overview (3/6)

merchants, the simplicity of use, especially for people that are not tech-savvy, the convenience, the broad or ubiquitous acceptance, the reasonable transaction speed, the low cost and high security. The importance of each of the criteria might differ between the aforementioned payment categories and also the cultural mindset of the people in different regions plays an important role in the adoption.

When it comes to user and shop/merchant adoption of a specific FinTech solution, PayPal is probably the most successful player in the Western World today. It offers easy application and payment processes for consumers, which are widely accepted by merchants worldwide.

Source: Statista Digital Market Outlook

Digital Payment solutions are the starting point of the digital revolution in financial services

6

Market size

With a global transaction value of about US$2,754 billion in 2017, the Digital Payments segment made up by far the biggest share of the total FinTech market.

The comparably high transaction value is driven by the vast amount of products and goods purchased online and incorporates all eCommerce transactions or travel bookings. This is why Digital Commerce accounted for about 92% of the total Digital Payment transaction value. Mobile POS payments contributed to the Digital Payments value with about 8% or US$231 billion in 2017.

When it comes to regional distribution, the U.S. and China contributed quite similar shares to the global transaction value, with Europe being considerably less important. The Chinese Digital Payment transaction value amounted to US$820bn (30%) in 2017, followed by the U.S. with US$802bn (29%), and Europe with US$613bn (22%).

Given the high internet coverage and smart device penetration, the adoption of digital payment services in developed countries is mainly a question of convenience and added value to the existing infrastructure.

Nonetheless, there are about 2 billion people worldwide that live outside a financial system or without permanent access to the internet. This means that they do not have instant access to bank accounts or the ability to shop online in a convenient way.

Segment overview (4/6)

Digital Payments transaction value in 2017 in US$ bn

1: Only includes countries listed in the Digital Market OutlookSource: Statista Digital Market Outlook 2017

In 2017, China is the largest global1 Digital Payment market due to its high online shopping volume

729.4

801.7

72.2

699.1

120.9

819.9

591.7

613.9

22.2

United States China Europe

Mobile POS PaymentsDigital Commerce

7

Digital Payments transaction value in 2022 in US$bn

Segment overview (5/6)

Future development

The future of payments: It is obvious that the way we pay for goods and services, online as well as offline, is about to change radically due to emerging digital services.

However, it is still largely uncertain to what extent and at what speed this imminent revolution is going to take place. Hence, the key question will be, can the established players adapt to new technologies fast enough to compete with agile, innovative start-ups? The greatly feared alternative would be that the new market entrants disrupt the existing market structure with innovative business models, an efficient infrastructure and a stronger focus on consumer needs.

Global Digital Payments are expected to double their transaction value by 2022 to reach US$5,411bn. Mobile Payments are expected to grow almost 6-fold between 2017 and 2022 at a compound annual growth rate of 42%. At the same time, Digital Commerce volume is expected to grow at 10%.

Having a look at regional differences, the U.S., Europe and China will account for 83% of the global1 Digital Payment transaction value by 2022. China‘s share of the global transaction volume will increase to US$2,027bn or 37%.

Although growth rates show high double-digit figures in the Western world, relevant market growth is added by mobile-first countries, especially China, in the next couple of years.

1: Only includes countries listed in the Digital Market Outlook2: CAGR: Compound Annual Growth Rate / average growth rate per yearSource: Statista Digital Market Outlook 2017 .

Mobile POS Payments in the U.S. are expected to grow to US$366 billion by 2022

1,412.3

365.5

1,046.8

1,340.7

2,027.1

686.4

1,039.5

166.1

873.4

United States China Europe

Mobile POS PaymentsDigital Commerce

8

Assumptions and sensitivity analysis

We believe that the payment industry is facing three major trends with sustainable long-term impact: seamless commerce, mobile payments & blockchain technology.

Seamless integration of payment processes gains relevance in every context, be it online shopping, in-store purchases or peer-to-peer payments. Usability is the key to high conversion rates and consumer adoption. High security standards throughout the payment process will most likely be ensured by biometrical methods such as fingerprint authentication.

Another important factor is the growing impact of mobile devices, not only for POS shopping but also for mobile checkout processes in the eCommerce world as well as the integration of P2P payments into messengers and social networks. Especially in less developed mobile-first countries, high convenience and usability on mobile devices is inevitable.

A third dimension is blockchain technology, which is closely connected to cryptocurrencies. Here we have a completely new technology without any established players in the market. The technology promises to allow secure direct transactions without intermediaries. However, the impact of blockchain on financial regulation is not yet foreseeable. The European Commission states that “existing regulation will still apply”, but like in other areas of FinTech, regulation can have an unassesableimpact on the future development of the markets.

Segment overview (6/6)

Trends

Large players such as PayPal, Apple, Amazon & Facebook are putting significant amounts of money into online and mobile payment solutions. The ongoing development from separate online shops towards integrated online shopping ecosystems, in particular the merger of shopping and social media / messaging, enables new business models and opportunities for digital payment methods.

In this field, China, as a mobile-first country, sets the standards for mCommerce shopping as well as mobile POS-solutions very high. The strong integration of payment solutions in social messaging services, e.g. WeChat, gave birth to two huge payment systems with an enormous user base, namely Alipay (Ant Financial) and WeChat Pay (Tencent). These two payment providers cover almost the entire Chinese Mobile Payment market. Paying the taxi driver, buying a coffee to go on the way to work, ordering cinema tickets and splitting the bill between friends – it’s all covered by one single payment app. And this is what will probably come to Europe and the U.S. as well (sooner or later).

In Europe we observe an evolving FinTech start-up landscape, especially in Online and Mobile Banking. However, market dynamics and pervasion of innovative FinTech solutions are not comparable to China or the U.S.

Source: Statista Digital Market Outlook 2017

Mobile and seamless: Payments need to become easy and flexible for all consumers

9

United States

KPI comparison (1/5)

China Europe

1: CAGR: Compound Annual Growth Rate / average growth rate per yearSource: Statista Digital Market Outlook 2017

With a CAGR1 of ~20% up to 2022, China will remain the leading economy in terms of Digital Payments

Digital Payment transaction value in billion US$

1,046.8

2017

801.7

72.2

729.4

+12.0%1

2022

1,412.3

365.5

+19.8%1

2022

2,027.1

686.4

1,340.7

2017

819.9

120.9

699.1

+11.1%1

2022

1,039.5

166.1

873.4

2017

613.9

22.2

591.7

Mobile POS PaymentsDigital Commerce

10

KPI comparison (2/5)

1: CAGR: Compound Annual Growth Rate / average growth rate per yearSource: Statista Digital Market Outlook 2017

The average transaction value per user is by far the highest in the U.S., followed by Europe

Average transaction value per user in US$

United States China Europe

1,469

3,914

2017

2022

4,096

5,200

436

1,431

2022

1,049

2017

1,097

630

2017

1,670

1,982

2022

2,160

Mobile POS PaymentsDigital Commerce

11

KPI comparison (3/5)

1: CAGR: Compound Annual Growth Rate / average growth rate per yearSource: Statista Digital Market Outlook 2017

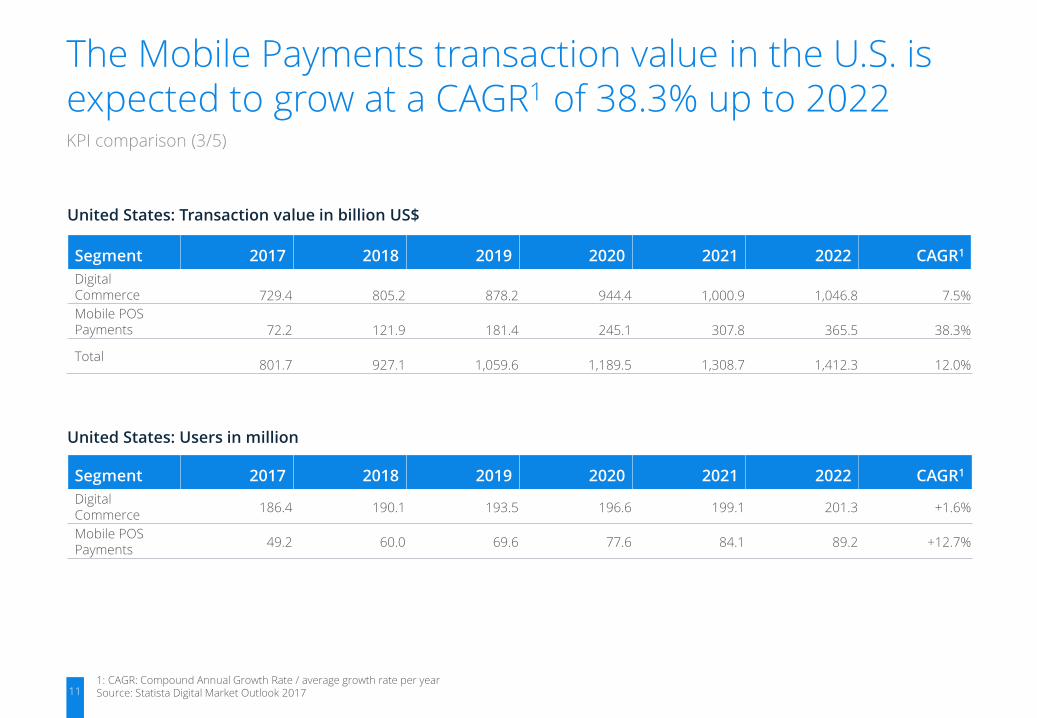

The Mobile Payments transaction value in the U.S. is expected to grow at a CAGR1 of 38.3% up to 2022

Segment 2017 2018 2019 2020 2021 2022 CAGR1

Digital Commerce

186.4 190.1 193.5 196.6 199.1 201.3 +1.6%

Mobile POS Payments

49.2 60.0 69.6 77.6 84.1 89.2 +12.7%

United States: Users in million

United States: Transaction value in billion US$

Segment 2017 2018 2019 2020 2021 2022 CAGR1

Digital Commerce 729.4 805.2 878.2 944.4 1,000.9 1,046.8 7.5%

Mobile POS Payments 72.2 121.9 181.4 245.1 307.8 365.5 38.3%

Total801.7 927.1 1,059.6 1,189.5 1,308.7 1,412.3 12.0%

12

KPI comparison (4/5)

1: CAGR: Compound Annual Growth Rate / average growth rate per yearSource: Statista Digital Market Outlook 2017

The Digital Payments transaction value in China is expected to reach more than US$2 trillion by 2022

China: Users in million

China: Transaction value in billion US$

Segment 2017 2018 2019 2020 2021 2022 CAGR1

Digital Commerce

637.4 695.4 756.7 819.4 880.7 937.2 +8.0%

Mobile POS Payments

277.1 348.9 428.2 508.8 585.4 654.1 +18.7%

Segment 2017 2018 2019 2020 2021 2022 CAGR1

Digital Commerce 699.1 841.9 983.9 1,117.5 1,237.3 1,340.7 13.9%

Mobile POS Payments 120.9 198.2 300.6 422.4 554.3 686.4 41.5%

Total819.9 1,040.1 1,284.5 1,539.9 1,791.7 2,027.1 19.8%

13

KPI comparison (5/5)

1: CAGR: Compound Annual Growth Rate / average growth rate per yearSource: Statista Digital Market Outlook 2017

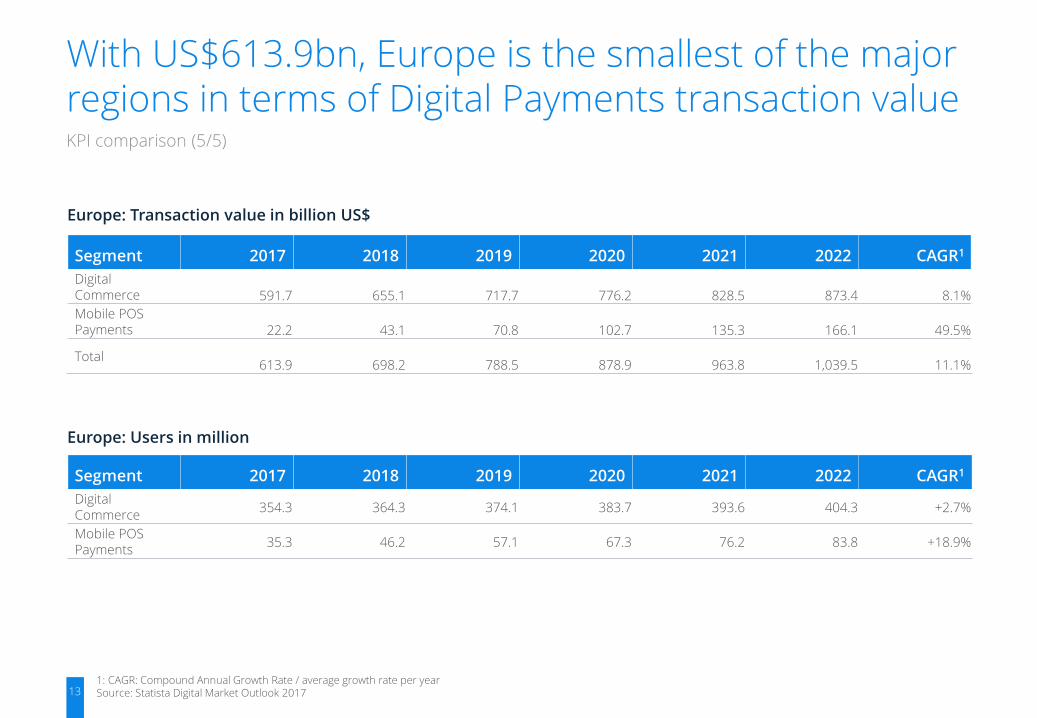

With US$613.9bn, Europe is the smallest of the major regions in terms of Digital Payments transaction value

Europe: Users in million

Europe: Transaction value in billion US$

Segment 2017 2018 2019 2020 2021 2022 CAGR1

Digital Commerce

354.3 364.3 374.1 383.7 393.6 404.3 +2.7%

Mobile POS Payments

35.3 46.2 57.1 67.3 76.2 83.8 +18.9%

Segment 2017 2018 2019 2020 2021 2022 CAGR1

Digital Commerce 591.7 655.1 717.7 776.2 828.5 873.4 8.1%

Mobile POS Payments 22.2 43.1 70.8 102.7 135.3 166.1 49.5%

Total613.9 698.2 788.5 878.9 963.8 1,039.5 11.1%

14

Trend Explanation

In the future, payment features will be integrated into all kinds of everyday objects. From cars to smart TVs – almost every personal object will be able to participate in payment transactions.

This will enable customers to pay even faster and more easily. Physicalcontact is not strictly necessary when money is exchanged digitally. Waiting times will either be reduced to a minimum or disappear completely. When driving out of a car park, the length of stay will be re-corded automatically. The payment will be made directly through the car. Customers will just have to confirm the amount on a display inside.

For security reasons, integrated payment transactions will stay limited. However, future authentication methods could solve this problem. The wearer of an item of clothing with an integrated payment feature could, for example, be recognized by their heartbeat.

Future applications:

▪ Checkout areas will become obsolete. Supermarket customers will pay for their goods using their jackets or coats.

▪ Pay-as-you-go: There is no more need for tickets in public transportation systems. When boarding a bus, payments can be triggered by passengers’ shoes.

▪ Vehicles with integrated payment features enable a contactless payment of refueling and parking charges.

Deep Dive (1/3)

Micro-Trend: MasterCard Key

MasterCard has partnered with the chip manufacturer Qualcomm to work on technologies that add a payment feature to everyday objects. General Motors has been recruited as a partner and will add the payment system to its keys. This system is based on chips which MasterCard has modified and made part of a token.

Micro-Trend: Lyle & Scott Jacket

Scottish fashion brand Lyle & Scott has developed a jacket which allows its wearer to make contactless payments. The sleeve includes a small pocket into which a special payment chip is inserted that supports the Barclays Bank "bPay" payment system. The jacket costs ₤149 and is available in blue and black.

Seamless integration of Payment Solutions is one of the major driving forces in the field of Digital Payment

POWERED BY

15

Trend Explanation

The rapidly growing dangers in the digitalization process have increased the need to protect data and privacy in digital spaces too – this applies to the finance sector in particular.

To guarantee a higher level of security in the future, conventional authentication systems like PINs, passwords and cards will be replaced by biometric methods.

Personal methods will be used, including fingerprint, facial and iris recognition. Highly individual physical features like heartbeat, vein structure and skull echoes will provide even safer ID solutions that are completely resistant to attempted fraud by cyber criminals.

Behavior analysis is yet another approach. The software meticulously monitors keystrokes, mouse movements and touchscreen contacts. Any deviations from these patterns indicate potential identity theft.

Future applications:

▪ Online shopping payments can be verified by selfies

▪ Bank employees can confirm the identity of customers via video chats

▪ Payments via voice command can be accepted by an analysis of voice patterns

▪ The vital signs recorded by a smartwatch enable the wearer to make transactions

Deep Dive (2/3)

The Dutch mobile-only bank Bunq aims to offer customers a secure log-in via mobile devices by using VeridiumID and hand recognition software to authenticate users based on four fingerprints.

The technology can be applied to any modern smartphone with at least a five megapixel camera and flash.

Micro-Trend: NatWest BioCatch

The British bank NatWest is testing BioCatch technology, which uses behavioral biometrics to authenticate visitors to websites.

The system captures more than 500 behavior points, such as hand-eye coordination, pressure, hand tremors, navigation, scrolling and various finger movements.

Biometric authentication is expected to facilitate payment processes and increase security

POWERED BY

Micro-Trend: Bunq 4 Fingers TouchlessID

16

The blockchain is the software basis of the virtual currency Bitcoin. It is used as a secure digital record of transactions. The technology ensures a faster and more efficient exchange of information.

Blockchain technology makes trust an integral component of technology in general. All transactions are stored in a fraud-proof ledger. This ledger is filed decentrally for large numbers of clients and is therefore highly secure.

Trust-building organizations like banks and insurance companies could be gradually replaced by the decentralized network due to the fact that major functions can be performed by the technology itself. Rules, contracts and processes can be programmed on the blockchain and thereby transformed into automated processes.

The revolution will initially run in the background, at the back-end. Customers’ first contact with the blockchain will be via smart contracts or DApps1.

Musicians’ royalties can be automatically paid via the blockchain when people listen to their songs, without a record company being involved. Insurance policies for flight delays will pay out immediately if an airline’s flight data reports a delayed plane. People will no longer have to waste time claiming compensation. The amount of self-generated solar power can be calculated without checks by a utility company and credited to the user’s account via the blockchain.

These services-on-the-blockchain will also give many people access

Deep Dive (3/3)

to global capital markets who previously did not even have a bank account due to structural or political reasons. This also includes the enormous field of micro-transactions that often lack profitability due to relatively high transaction costs..

1: DApps: decentralized applications

Outlook 2025: Blockchain might serve as a future infrastructure for payment transactions

POWERED BY

17

Segment Sub-segments Out of scope

Market structure and definition

Digital Payments revenue streams

Digital Payments

Traditional Bank Transfers

Business-to-Business Payments

Point-of-Sale card payments at mobile card readers (mPOS terminals)

Includes transactions at Point-of-Sale that are processed via smartphone applications (so-called “mobile wallets”). Well-known providers of mobile wallets are ApplePay, and Samsung Pay. The payment in this case is made by a contactless interaction of the smartphone app with a suitable payment terminal belonging to the merchant.

Mobile POS Payments

Consumer transactions made via the Internet which are directly related to online shopping for products and services. Online transactions can be made via various payment methods (credit cards, direct debit, invoice, or online payment providers, such as PayPal and Alipay).

Digital Commerce

18

Details

▪ 50+ countries & regions

▪ Direct access & downloads

▪ 7-Year coverage: 2016 – 2022

▪ Revenue forecasts

▪ User count & penetration

▪ Comparable data

About the Statista Digital Market Outlook

9 markets, 35 segments & 85 sub-segments

Connected Car

Connected Hardware, Vehicle Services, Infotainment Services

eTravel

Online Travel Booking, Mobility Services

eServices

Event Tickets, Fitness, Dating Services, Food Delivery

FinTech

Digital Payments, Alternative Financing, Alternative Lending, Personal Finance

Smart Home

Control and Connectivity, Comfort and Lighting, Security, Home Entertainment, Energy Management, Smart Appliances

eCommerce

Fashion, Electronics & Media, Food & Personal Care, Furniture & Appliances, Toys, Hobby & DIY

Digital Advertising

Banner Ads, Video Ads, Search Ads, Social Media Ads, Classifieds

Digital Media

Video-on-Demand, Digital Music, Video Games, ePublishing

eHealth

Diabetes, Hypertension, Heart Failure

Exclusive part of the Statista Corporate AccountAccess to more than 1,000,000 statistics and all digital markets

more informationmore information

www.statista.com

Felix Wegener

Analyst Digital Markets

Author, Imprint, and Disclaimer

Felix Wegener graduated in Geography and Economics.

He gained comprehensive knowledge of digital technologies and their disruptive character from numerous consulting projects and business transformations in several industries.

ImprintStatista ▪ Johannes-Brahms-Platz 1 ▪ 20355 Hamburg ▪ +49 40 413 49 89 0 ▪ www.statista.com

DisclaimerThis study is based on survey and research data from the previously mentioned sources. The forecasts and market analysis presented were researched and prepared by Statista with great care.

For the presented survey data, estimations, and forecasts Statista cannot assume warranty of any kind. Surveys and forecasts contain information not naturally representing a reliable basis for decisions in individual cases and may require further interpretation. Therefore, Statista is not liable for any damage arising from the use of statistics and data provided in this report.