digital finance plus readiness in tanzania: summary

TRANSCRIPT

WORKING DRAFT

Last Modified 7/24/2014 4:21 PM Eastern Standard Time

Printed 6/27/2014 8:10 PM Eastern Standard Time

Digital Finance +

Readiness

Tanzania

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

1

We assessed the digital finance plus readiness along

6 dimensions

SOURCE: Client Survey (Oct 2011); McKinsey Quarterly Survey (Jul 2011)

Digital finance plus enabling environmentSector-level digital finance plus assessment

4.1 Sector description

4.2 Sector impact on low-income households

5.1 Financial service needs along the value chain

5.2 Financial gap analysis along the value chain

5.3 Barriers to provision of financial products

4.3 Sector-specific actors and regulation

6.1 Potential applications of DF+ to address barriers

6.2 Viability of observed and potential business models

6.3 Scaling and execution capabilities

4.4 Sector challenges

6

5

4 3

2

1

Readiness

1.1 Technical infra-structure readiness

1.2 Telecom industry readiness

1.3 Level of adoption

3.1 Relevant financial andtelco regulation

3.2 Government support

3.3 Use of DF+ by the government

2.2 Digital finance readiness

2.3 Level of digital finance adoption

2.1 Overall financial sector readiness

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

2

Sector readiness dimension

Sector-rele-

vant mobile

infrastructure

reach and

adoption

Readiness of

financial and

digital

financial

infrastructure

65

4 32

1

65

4 32

1

Role of

government

and

regulation

6

54 3

2

1

Severity of

sector

challenges

65

4 32

1

Financial gap

in sector

65

4 32

1

DF+ business

models and

scaling

65

4 32

1

Reach

Reach of mobile

infrastructure

Adoption of mobile

technology

Financial product

offering to sector

Availability of

DF+ solutions

Sector-specific

regulation

Role of

government

Stakeholder

complexity

Non-financial chal-

lenges in sector

Execution and

scalling ability

Depth of financial

gap

Availability of DF+

business models

Sub-dimensions

Applicability of

DF+ solutions

DF+ readiness assessment – DF+ implementation in the

agriculture sector faces varying levels of constraints

▪ 85% of the country are covered by a 2G network, with some concern around the quality of service in the most rural areas

▪ High penetration, at ~60% of households, with some concern around ownership of handsets and proficient usage by poorest farmers

▪ Traditional financial institutions offer limited credit to farmers without value chain actor guarantees or crop deposit collateral; MFIs lend at annual rates of up to 100%

▪ Present but not scaled – WRS-based post-harvest credit provision, input credit in closed-loop ecosystems, and value chain payment facilitation

▪ No regulatory barriers – regulations on formation of producer associations and export controls have been relaxed

▪ Policy priority for the government; but public spending on the sector is below the target of the 10% of national budget

▪ Moderate complexity – several actors involved along value chain, but roles and interaction are relatively well-defined

▪ Severe non-financial challenges related to quality farmer education, organization, enterprise, and supply/demand dynamics

▪ The majority of farmers cannot access credit support for critical steps of input acquisition and post-harvest liquidity

▪ DF+ solutions can play a significant role by facilitating value chain actors’ market linkages, reducing transaction costs and financial transparency

▪ Value chain actors collaborate to share risk and create “closed loop” ecosystems to provide of DF+ enabled financial products in controlled circumstances

▪ Value chain actors have proven that they can successfully execute, but solutions still apply to small niche of “emerging farmers” meetings a set of selective criteria

6.2 AGRICULTURE – VIABILITY OF OBSERVED AND POTENTIAL BUSINESS MODELS

1

Binding constraint Readiness for scaling

2 3 54 Explanation

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

3

DF+ implementation in the health sector faces varying levels of

constraints

• 85% of the country is covered by 2G networks, though selected rural areas remain a problem

Sector readiness dimension

Sector-rele-

vant mobile

infrastructure

reach and

adoption

Readiness of

financial and

digital

financial

infrastructure

65

4 32

1

65

4 32

1

Role of

government

and

regulation

6

54 3

2

1

Severity of

sector

challenges

65

4 32

1

Financial gap

in sector

65

4 32

1

DF+ business

models and

scaling

65

4 32

1

• High penetration at ~60% of households, with some concern over female access to mobile phone within HH as they seek most child care

• Low level of private lending, savings, or insurance products for low-income HHs, with low-utilized government-subsidized insurance as the exception

• Donor organizations adopting technology for limited pilots, but there is a lack of pilots with business models or providing financial products

• Free care creates low willingness to pay for necessary services and low supervision leads to sub-optimal care practice

• The government has played a neutral role in DF+ implementation; donors are driving development

• Complex stakeholder landscape with a mix of public, private (incl. faith-based) providers and active donors

• Severe non-financial challenges related to the quality of care, availability of medical staff, and awareness of illnesses among population

• The majority of low-income households do not use any form of finance products in health; access to financing for providers is limited

• DF+ solutions can address selected issues within the health sector though major change will require comprehensive reform

• Most pilots and solutions are subsidy-based, though a few potential unexplored business models exist

• No clear sign of scaling – given large government role, scaling will require its explicit support

Reach

Reach of mobile

infrastructure

Adoption of mobile

technology

Financial product

offering to sector

Availability of

DF+ solutions

Sector-specific

regulation

Role of

government

Stakeholder

complexity

Non-financial chal-

lenges in sector

Execution and

scalling ability

Depth of financial

gap

Availability of DF+

business models

Sub-dimensions

Applicability of

DF+ solutions

1

Binding constraint Readiness for scaling

2 3 54 Explanation

6.2 HEALTH – VIABILITY OF OBSERVED AND POTENTIAL BUSINESS MODELS

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

4

▪ 85% of the country is covered by a 2G network, with some concern

about the quality of service in the most rural areas

▪ High penetration, at ~60% of households, with some concern about

the ownership of handsets and proficient usage by poorest

households

▪ Lending to consumers and enterprises by banks and MFIs is minimal.

Robust equity financing for enterprises by VC actors and other

investors

▪ Several innovative energy enterprises are using DF+ to deploy

different financing solutions to consumers

▪ Highly conducive – existing solar enterprises are almost entirely

unregulated given their capacity is less than 100kw capacity

▪ The government is involved through two agencies n/a EWURA

regulates and REA facilitates – both are conducive to off-grid energy

development

▪ Little complexity – primary actors are energy enterprises and

households with demand for electricity access

▪ Moderate – a poor rural infrastructure inhibiting “last mile” reach and

lack of consumer knowledge of off-grid benefits are most notable

▪ Somewhat deep – almost all energy enterprises provide financing

support to consumers, but their own access to working capital is

limiting

▪ Highly applicable – allows enterprises to cut transaction costs,

enhance contract enforcement, and provide additional services

▪ Successful enterprises have identified winning technologies, built low-

cost, effective distribution networks, and established a loyal base of

customers

▪ Currently, SHS reach is 50,000-100,000 households. “True scale” of

1million + will be reached with the introduction of commercial lending,

consumer education and the expansion of distribution networks

DF+ implementation in the energy sector faces varying levels of

constraints

6.2 ENERGY – VIABILITY OF OBSERVED AND POTENTIAL BUSINESS MODELS

Sector readiness dimension

Sector-rele-

vant mobile

infrastructure

reach and

adoption

Readiness of

financial and

digital

financial

infrastructure

65

4 32

1

65

4 32

1

Role of

government

and

regulation

6

54 3

2

1

Severity of

sector

challenges

65

4 32

1

Financial gap

in sector

65

4 32

1

DF+ business

models and

scaling

65

4 32

1

Reach

Reach of mobile

infrastructure

Adoption of mobile

technology

Financial product

offering to sector

Availability of

DF+ solutions

Sector-specific

regulation

Role of

government

Stakeholder

complexity

Non-financial chal-

lenges in sector

Execution and

scalling ability

Depth of financial

gap

Availability of DF+

business models

Sub-dimensions

Applicability of

DF+ solutions

1

Binding constraint Readiness for scaling

2 3 54 Explanation

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

5

DF+ implementation in the education sector faces varying levels

of constraints

▪ 85% of the country is covered by a 2G network; selected rural areas remain a problem

▪ High penetration at ~60% of households, with some concern about female access to mobile phone within the household

▪ Low level of private lending and savings for education as BoP consumers are considered unattractive

▪ The government drives reform in the sector and is currently not focused on DF+

▪ Regulation neither helps nor hinders growth of DF+

▪ The government is a major player in the sector and has not adopted technologies

▪ Government adoption would affect 95% of the students in public schools

▪ Severe non-financial challenges are related to absenteeism, quality of instruction, pupil:teacherratio

▪ The majority of low-income households do not use any form of finance products for education

▪ DF+ solutions can play a part in improving attendance, increasing the ability to pay for school and access textbooks

▪ While models are impactful, they largely have unclear business models

▪ Execution and scaling would need to be undertaken largely by government actors

6.2 EDUCATION – VIABILITY OF OBSERVED AND POTENTIAL BUSINESS MODELS

Sector readiness dimension

Sector-rele-

vant mobile

infrastructure

reach and

adoption

Readiness of

financial and

digital

financial

infrastructure

65

4 32

1

65

4 32

1

Role of

government

and

regulation

6

54 3

2

1

Severity of

sector

challenges

65

4 32

1

Financial gap

in sector

65

4 32

1

DF+ business

models and

scaling

65

4 32

1

Reach

Reach of mobile

infrastructure

Adoption of mobile

technology

Financial product

offering to sector

Availability of

DF+ solutions

Sector-specific

regulation

Role of

government

Stakeholder

complexity

Non-financial chal-

lenges in sector

Execution and

scalling ability

Depth of financial

gap

Availability of DF+

business models

Sub-dimensions

Applicability of

DF+ solutions

1

Binding constraint Readiness for scaling

2 3 54 Explanation

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

6

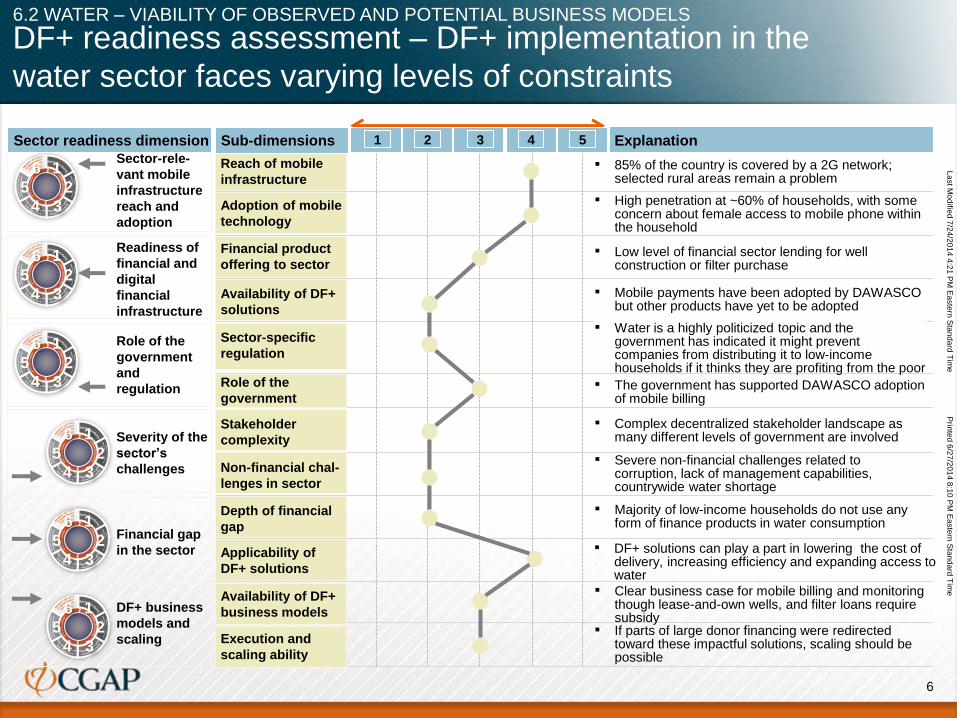

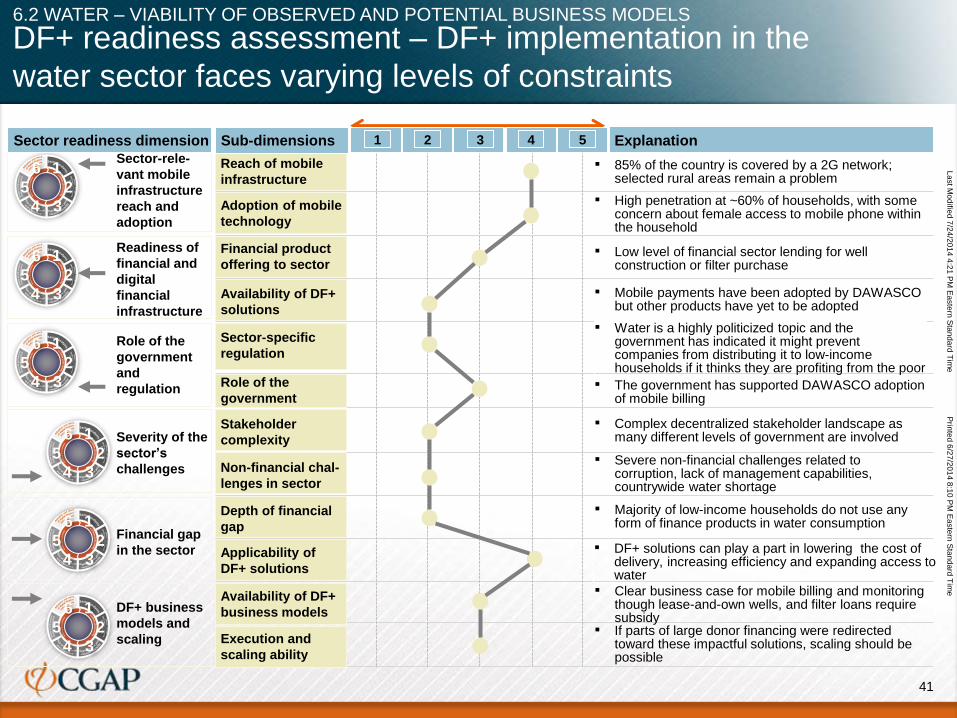

DF+ readiness assessment – DF+ implementation in the

water sector faces varying levels of constraints

Sector-rele-

vant mobile

infrastructure

reach and

adoption

Readiness of

financial and

digital

financial

infrastructure

6

5

4 3

2

1

6

5

4 3

2

1

Role of the

government

and

regulation

6

5

4 3

2

1

Severity of the

sector’s

challenges

6

5

4 3

2

1

Financial gap

in the sector

6

5

4 3

2

1

DF+ business

models and

scaling

6

5

4 3

2

1

Reach

Reach of mobile

infrastructure

Adoption of mobile

technology

Financial product

offering to sector

Availability of DF+

solutions

Sector-specific

regulation

Role of the

government

Stakeholder

complexity

Non-financial chal-

lenges in sector

Execution and

scaling ability

Depth of financial

gap

Availability of DF+

business models

Applicability of

DF+ solutions

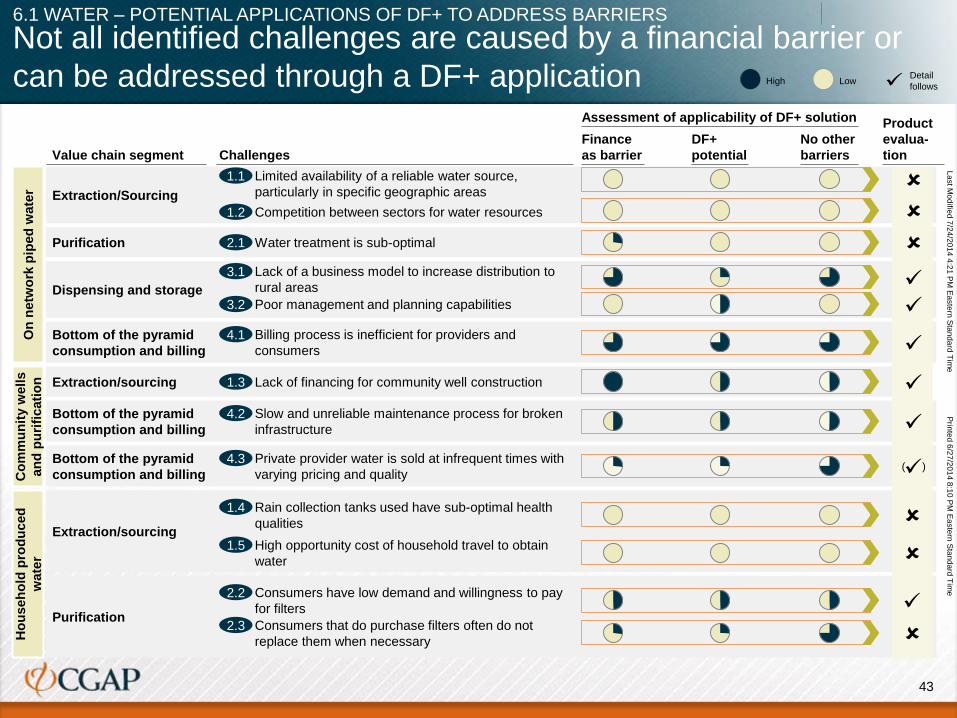

▪ 85% of the country is covered by a 2G network; selected rural areas remain a problem

▪ High penetration at ~60% of households, with some concern about female access to mobile phone within the household

▪ Low level of financial sector lending for well construction or filter purchase

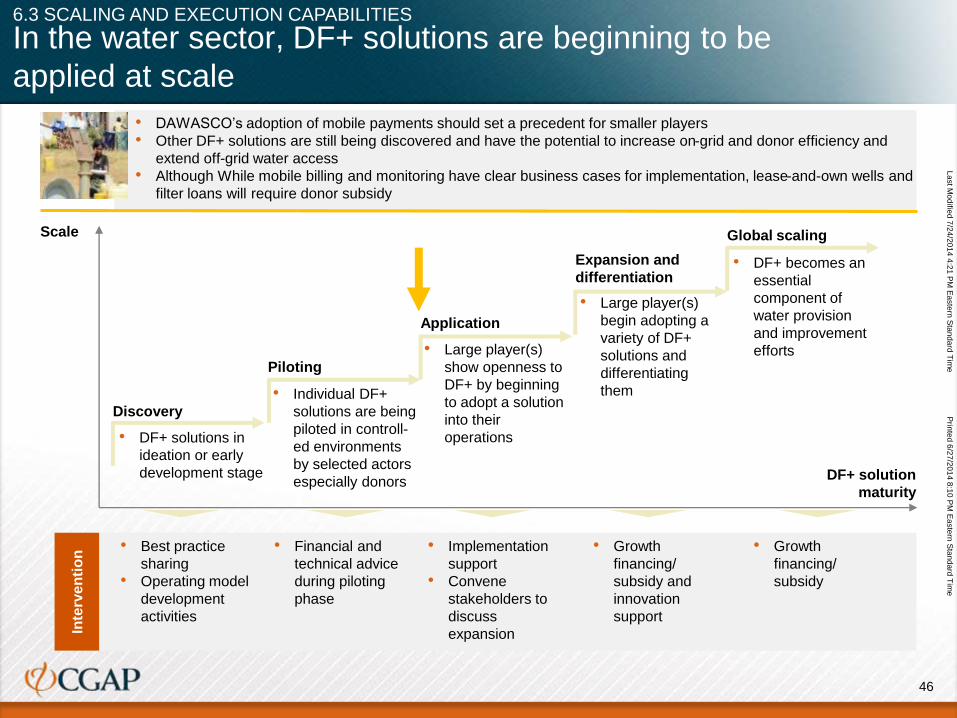

▪ Mobile payments have been adopted by DAWASCObut other products have yet to be adopted

▪ The government has supported DAWASCO adoption of mobile billing

▪ Complex decentralized stakeholder landscape as many different levels of government are involved

▪ Severe non-financial challenges related to corruption, lack of management capabilities, countrywide water shortage

▪ Majority of low-income households do not use any form of finance products in water consumption

▪ DF+ solutions can play a part in lowering the cost of delivery, increasing efficiency and expanding access to water

▪ Clear business case for mobile billing and monitoring though lease-and-own wells, and filter loans require subsidy

▪ If parts of large donor financing were redirected toward these impactful solutions, scaling should be possible

▪ Water is a highly politicized topic and the government has indicated it might prevent companies from distributing it to low-income households if it thinks they are profiting from the poor

6.2 WATER – VIABILITY OF OBSERVED AND POTENTIAL BUSINESS MODELS

Sector readiness dimension Sub-dimensions 1 2 3 54 Explanation

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

7

Agenda

Overall assessment framework

Sector analysis agriculture

Sector analysis and challenge identification

Assessment of financial service needs and gap analysis

Digital finance plus feasibility assessment

Sector analysis energy

Sector analysis water

Sector analysis health

Sector analysis education

SOURCE: Source

Access to and reach of mobile infrastructure

Adoption and reach of digital finance infrastructure

Role of the government and regulation

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

8

Sector readiness dimension

Sector-rele-

vant mobile

infrastructure

reach and

adoption

Readiness of

financial and

digital

financial

infrastructure

65

4 32

1

65

4 32

1

Role of

government

and

regulation

6

54 3

2

1

Severity of

sector

challenges

65

4 32

1

Financial gap

in sector

65

4 32

1

DF+ business

models and

scaling

65

4 32

1

Reach

Reach of mobile

infrastructure

Adoption of mobile

technology

Financial product

offering to sector

Availability of

DF+ solutions

Sector-specific

regulation

Role of

government

Stakeholder

complexity

Non-financial chal-

lenges in sector

Execution and

scalling ability

Depth of financial

gap

Availability of DF+

business models

Sub-dimensions

Applicability of

DF+ solutions

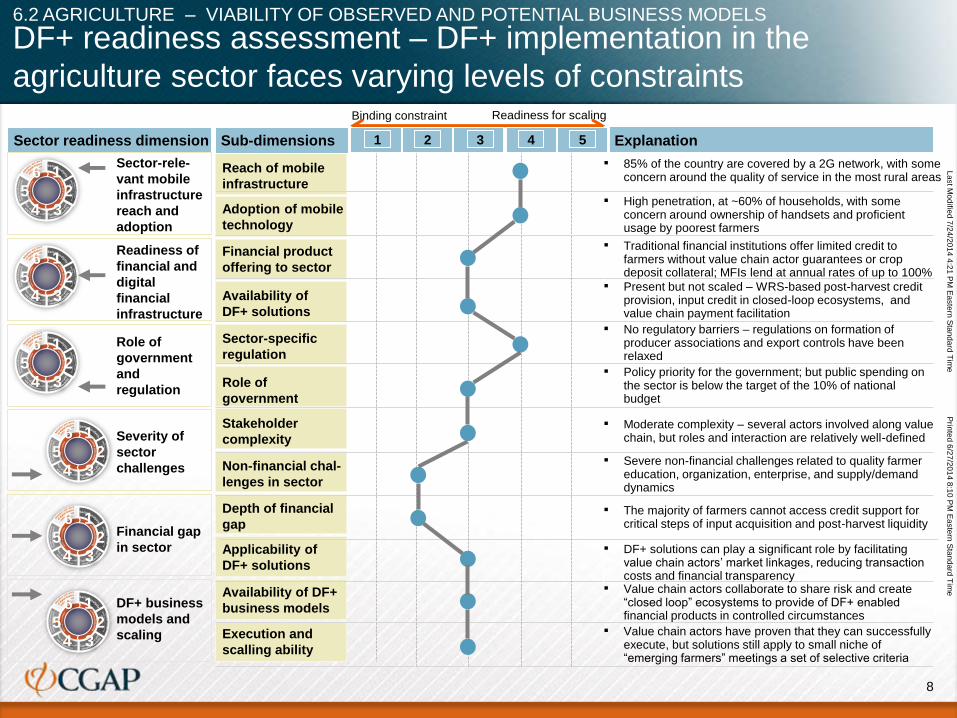

DF+ readiness assessment – DF+ implementation in the

agriculture sector faces varying levels of constraints

▪ 85% of the country are covered by a 2G network, with some concern around the quality of service in the most rural areas

▪ High penetration, at ~60% of households, with some concern around ownership of handsets and proficient usage by poorest farmers

▪ Traditional financial institutions offer limited credit to farmers without value chain actor guarantees or crop deposit collateral; MFIs lend at annual rates of up to 100%

▪ Present but not scaled – WRS-based post-harvest credit provision, input credit in closed-loop ecosystems, and value chain payment facilitation

▪ No regulatory barriers – regulations on formation of producer associations and export controls have been relaxed

▪ Policy priority for the government; but public spending on the sector is below the target of the 10% of national budget

▪ Moderate complexity – several actors involved along value chain, but roles and interaction are relatively well-defined

▪ Severe non-financial challenges related to quality farmer education, organization, enterprise, and supply/demand dynamics

▪ The majority of farmers cannot access credit support for critical steps of input acquisition and post-harvest liquidity

▪ DF+ solutions can play a significant role by facilitating value chain actors’ market linkages, reducing transaction costs and financial transparency

▪ Value chain actors collaborate to share risk and create “closed loop” ecosystems to provide of DF+ enabled financial products in controlled circumstances

▪ Value chain actors have proven that they can successfully execute, but solutions still apply to small niche of “emerging farmers” meetings a set of selective criteria

6.2 AGRICULTURE – VIABILITY OF OBSERVED AND POTENTIAL BUSINESS MODELS

1

Binding constraint Readiness for scaling

2 3 54 Explanation

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

9

Key takeaways: Agriculture sector Digital Finance Plus solutions

feasibility

AGRICULTURE – DIGITAL FINANCE PLUS SOLUTION FEASIBILITY

6.1 Potential applications of DF+ to address barriers

6.3 Scaling and execution capabilities

6.2 Viability of observed and potential business models

• DF+ can play a positive role in helping to address several of the financing gaps faced by smallholders in

agriculture by facilitating financial linkages between value chain actors, decreasing transaction costs, promoting

transparency in the flow of commodities and financial products, powering the aggregation and analytics of

data (behavioral, agronomic, and market), and enhancing contract enforceability

• Consequently, several value chain actors are partnering to provide innovative applications that enhance farmer

access to financing and increase farmer incomes. The most noteworthy products already in operation and/or

under development for the near term include: i) Warehouse Receipt System based post-harvest credit provision; ii)

input loans through closed-loop agriculture ecosystems; iii) information portals for agronomic, weather, and market

data; iv) e-wallets for input subsidy administration; and v) weather-indexed crop insurance to protect against extreme

weather conditions

• The current landscape of DF+ solutions is mostly driven by value chain actors, including seed and fertilizer

companies (e.g., Monsanto, Yara) and agro-processors (e.g., ETG), with the notable exception of the most

successful agronomic information portal, which is primarily driven by Tigo, a telco company

• Financial institutions lend directly to producers or producer associations in extremely rare cases –

however, banks like NMB and Barclays are extending credit with heavy collateralization/security guarantee through

value chain actors

• Scaling of DF+ solutions is hampered by several non-finance-related challenges, including

– Producer organization and entrepreneurship: many farmers are not encompassed in market-based

associations and lack the business knowledge to self-organize and form enterprising collectives

– Supply/demand market dynamics: the provision of financing is closely linked with robust markets for

particular crops, consequently favoring producers of high-value crops with market for agro-processing and

export (e.g., white maize, sunflower, coffee)

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

10SOURCE: Organization websites; press search; expert interviews; team analysis

A number of players meet the sector’s financing

needs to a very limited extent

Number/reach of existing initiatives

Minimal Moderate

LimitedN/A

Minimal but efforts underway

1 432 65

Information

Short term

Long term

Product/receive-ables finance

Credit

Value chain lending

Physical asset collateralization

Insurance

Credit guarantees

Savings

Payments

5.2 AGRICULTURE – FINANCIAL GAP ANALYSIS ALONG THE VALUE CHAIN

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

11

DF+ can help in addressing some of the gaps

in the Agriculture value chain

6.1 AGRICULTURE – POTENTIAL APPLICATIONS OF DF+ TO ADDRESS BARRIERS

Detail

follows

Value chain segment ChallengesProduct

evaluation

Finance

as barrier

DF+

potential

No other

barriers

Assessment of applicability of DF+ solution

1.1 Small arable land utilization

1.2 Limited average plot size

2.1 Inadequate fertilizer application

2.2 Weak demand for improved seeds

2.3 Underdeveloped capacity of agro-dealers

2.4 Inefficient government input subsidies

3.1 Farmer information constraints

3.2 Weak extension services

3.3 Low levels of mechanization

3.4 Heavy exposure to weather variability

4.1 Unavailability of storage warehouses

4.2 Post-harvest need for liquidity

4.3 Underdeveloped rural infrastructure

5.1 Low levels of commercialization

5.2 Non-consolidated aggregation/off-take

5.3 Poor access to market information

5.4 Weak market linkages

6.1 Low level of private investment

Land

Input provision

Production

Storage & Distribution

Marketing

Processing

high low

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

12

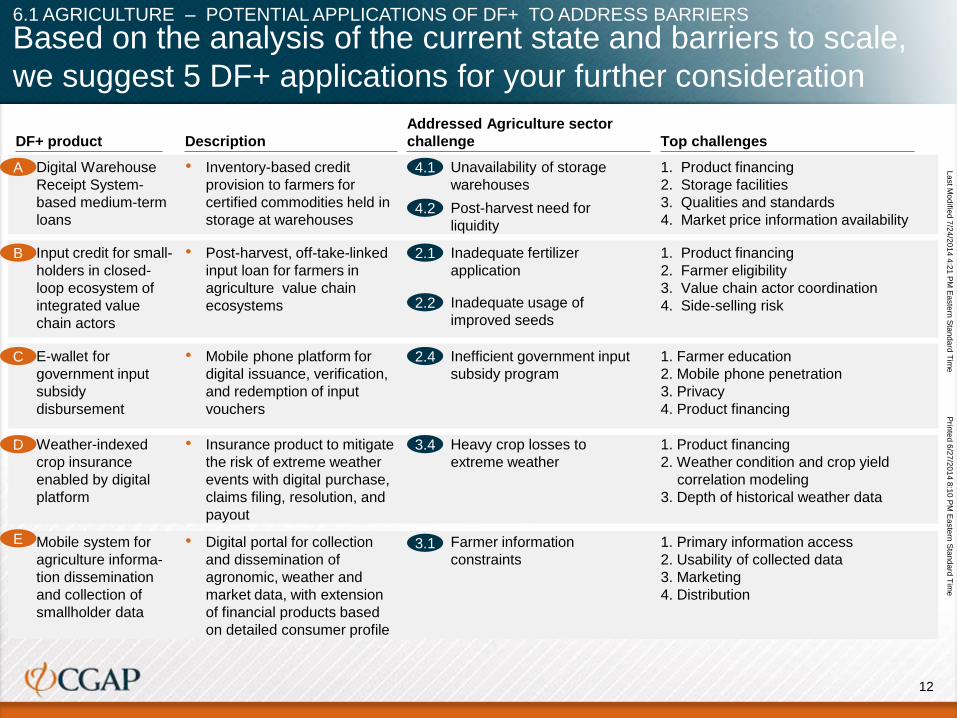

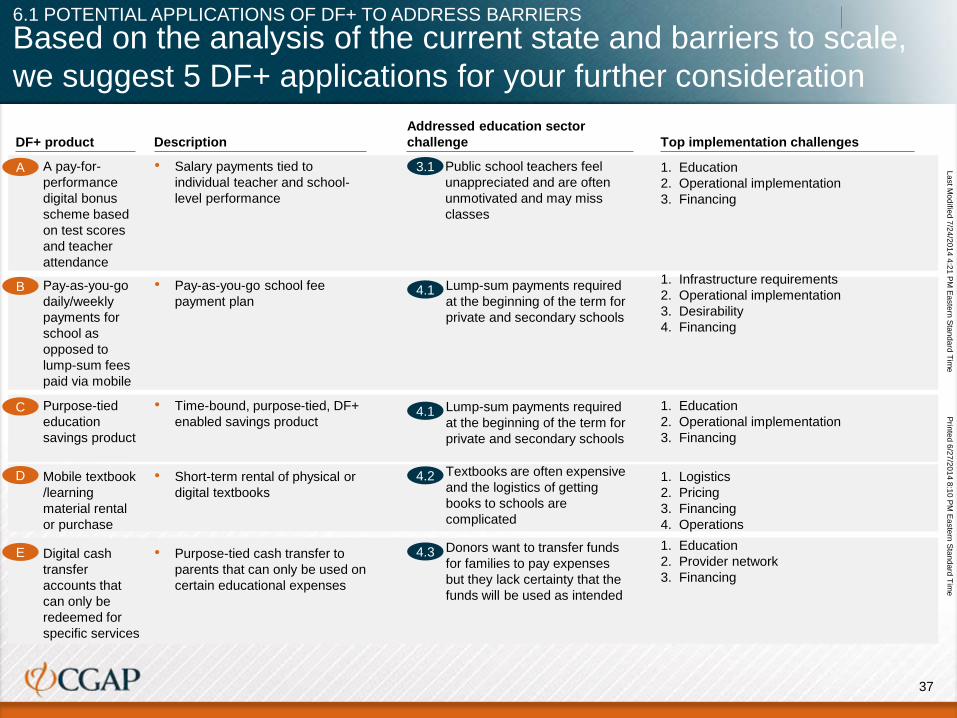

Based on the analysis of the current state and barriers to scale,

we suggest 5 DF+ applications for your further consideration

Top challengesDescriptionDF+ product

Unavailability of storage

warehouses

4.1 1. Product financing

2. Storage facilities

3. Qualities and standards

4. Market price information availability

• Inventory-based credit

provision to farmers for

certified commodities held in

storage at warehouses

• Digital Warehouse

Receipt System-

based medium-term

loans

Addressed Agriculture sector

challenge

A

Post-harvest need for

liquidity

4.2

Inadequate fertilizer

application

2.1 1. Product financing

2. Farmer eligibility

3. Value chain actor coordination

4. Side-selling risk

• Post-harvest, off-take-linked

input loan for farmers in

agriculture value chain

ecosystems

• Input credit for small-

holders in closed-

loop ecosystem of

integrated value

chain actors

B

Inadequate usage of

improved seeds

2.2

Inefficient government input

subsidy program

2.4 1. Farmer education

2. Mobile phone penetration

3. Privacy

4. Product financing

• Mobile phone platform for

digital issuance, verification,

and redemption of input

vouchers

• E-wallet for

government input

subsidy

disbursement

C

D Heavy crop losses to

extreme weather

3.4• Insurance product to mitigate

the risk of extreme weather

events with digital purchase,

claims filing, resolution, and

payout

• Weather-indexed

crop insurance

enabled by digital

platform

1. Product financing

2. Weather condition and crop yield

correlation modeling

3. Depth of historical weather data

Farmer information

constraints 3.1• Digital portal for collection

and dissemination of

agronomic, weather and

market data, with extension

of financial products based

on detailed consumer profile

• Mobile system for

agriculture informa-

tion dissemination

and collection of

smallholder data

E 1. Primary information access

2. Usability of collected data

3. Marketing

4. Distribution

6.1 AGRICULTURE – POTENTIAL APPLICATIONS OF DF+ TO ADDRESS BARRIERS

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

13

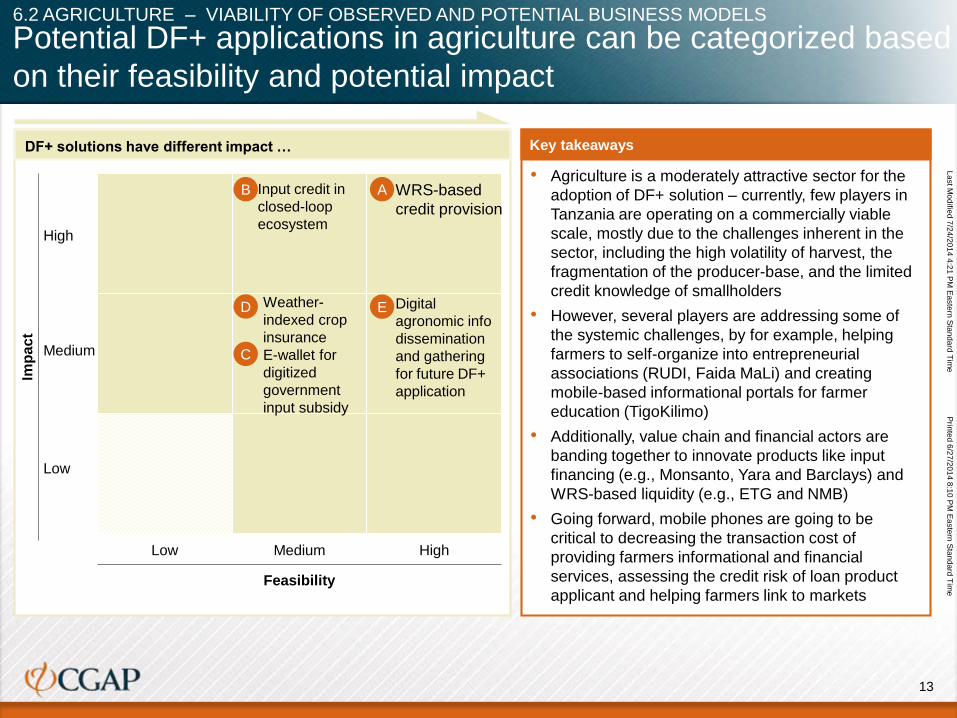

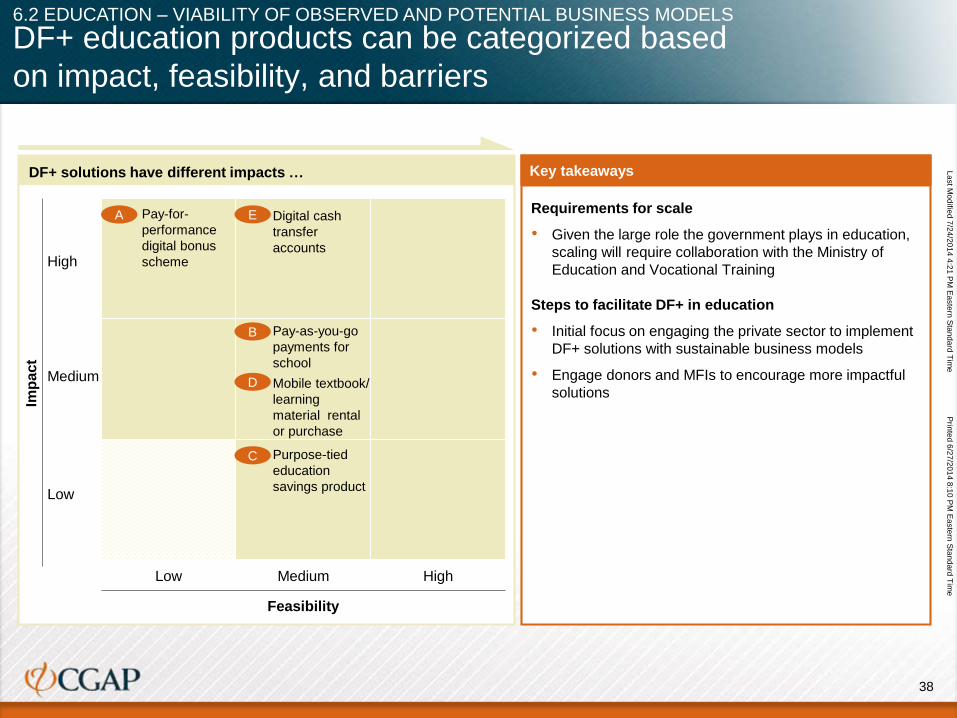

DF+ solutions have different impact … Key takeaways

Imp

act

High

Medium

Low

Low Medium High

Feasibility

• Agriculture is a moderately attractive sector for the

adoption of DF+ solution – currently, few players in

Tanzania are operating on a commercially viable

scale, mostly due to the challenges inherent in the

sector, including the high volatility of harvest, the

fragmentation of the producer-base, and the limited

credit knowledge of smallholders

• However, several players are addressing some of

the systemic challenges, by for example, helping

farmers to self-organize into entrepreneurial

associations (RUDI, Faida MaLi) and creating

mobile-based informational portals for farmer

education (TigoKilimo)

• Additionally, value chain and financial actors are

banding together to innovate products like input

financing (e.g., Monsanto, Yara and Barclays) and

WRS-based liquidity (e.g., ETG and NMB)

• Going forward, mobile phones are going to be

critical to decreasing the transaction cost of

providing farmers informational and financial

services, assessing the credit risk of loan product

applicant and helping farmers link to markets

• WRS-based

credit provision

• Input credit in

closed-loop

ecosystem

• Weather-

indexed crop

insurance

• E-wallet for

digitized

government

input subsidy

• Digital

agronomic info

dissemination

and gathering

for future DF+

application

AB

C

D E

Potential DF+ applications in agriculture can be categorized based

on their feasibility and potential impact

6.2 AGRICULTURE – VIABILITY OF OBSERVED AND POTENTIAL BUSINESS MODELS

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

14

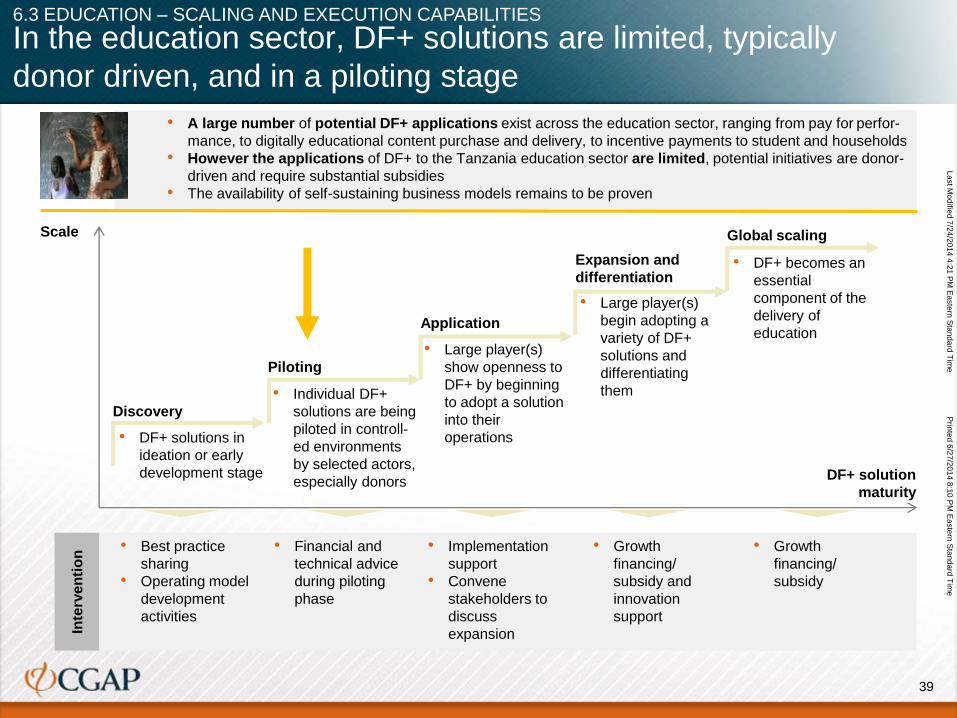

In the agriculture sector, DF+ solutions have been applied to

enable financing solutions with some success In

terv

en

tio

n

Discovery

Piloting

Scale

Application

Expansion &

differentiation

Global scaling

DF+ solution

maturity

• Growth financing/

subsidy

• Growth financing/

subsidy and

innovation

support

• Implementation

support

• Convene

stakeholders to

discuss

expansion

• Financial and

technical advice

during piloting

phase

• Best practice

sharing

• Operating model

development

activities

• DF+ has helped to address a number of the financing gaps faced by smallholders in agriculture, including by facilitating

virtual market linkages, decreasing transaction costs, and increasing the transparency of financial flows

• Value chain actors acting in concert, as well as a few telcos, have been the main drivers of DF+ solutions, with products

like WRS-based credit provision and off-take-linked input loans enabled by closed-loop ecosystems and risk-sharing

• Scaling and full commercial viability require more active financial institution involvement in the space, as well as improved

organization and entrepreneurship of producers, with development of market demand for more crop types

DF+ business

model in ideation

or early develop-

ment stage

Individual DF+

business models

are being piloted

in controlled

environments

DF+ business

models are rolled

out under market

conditions

Existing DF+

business models

are being

innovated and

differentiated

Successful DF+

business models

are scaling

nationally

6.3 AGRICULTURE – SCALING AND EXECUTION CAPABILITIES

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

15

Agenda

Sector analysis agriculture

Sector analysis health

Sector analysis and challenge identification

Assessment of financial service needs and gap analysis

Digital finance plus feasibility assessment

Overall assessment framework

Access to and reach of mobile infrastructure

Adoption and reach of digital finance infrastructure

Role of the government and regulation

Sector analysis energy

Sector analysis water

Sector analysis education

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

16

DF+ implementation in the health sector faces varying levels of

constraints

• 85% of the country is covered by 2G networks, though selected rural areas remain a problem

Sector readiness dimension

Sector-rele-

vant mobile

infrastructure

reach and

adoption

Readiness of

financial and

digital

financial

infrastructure

65

4 32

1

65

4 32

1

Role of

government

and

regulation

6

54 3

2

1

Severity of

sector

challenges

65

4 32

1

Financial gap

in sector

65

4 32

1

DF+ business

models and

scaling

65

4 32

1

• High penetration at ~60% of households, with some concern over female access to mobile phone within HH as they seek most child care

• Low level of private lending, savings, or insurance products for low-income HHs, with low-utilized government-subsidized insurance as the exception

• Donor organizations adopting technology for limited pilots, but there is a lack of pilots with business models or providing financial products

• Free care creates low willingness to pay for necessary services and low supervision leads to sub-optimal care practice

• The government has played a neutral role in DF+ implementation; donors are driving development

• Complex stakeholder landscape with a mix of public, private (incl. faith-based) providers and active donors

• Severe non-financial challenges related to the quality of care, availability of medical staff, and awareness of illnesses among population

• The majority of low-income households do not use any form of finance products in health; access to financing for providers is limited

• DF+ solutions can address selected issues within the health sector though major change will require comprehensive reform

• Most pilots and solutions are subsidy-based, though a few potential unexplored business models exist

• No clear sign of scaling – given large government role, scaling will require its explicit support

Reach

Reach of mobile

infrastructure

Adoption of mobile

technology

Financial product

offering to sector

Availability of

DF+ solutions

Sector-specific

regulation

Role of

government

Stakeholder

complexity

Non-financial chal-

lenges in sector

Execution and

scalling ability

Depth of financial

gap

Availability of DF+

business models

Sub-dimensions

Applicability of

DF+ solutions

1

Binding constraint Readiness for scaling

2 3 54 Explanation

6.2 HEALTH – VIABILITY OF OBSERVED AND POTENTIAL BUSINESS MODELS

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

17

Key takeaways: Health sector digital finance plus solutions

feasibility

HEALTH – DIGITAL FINANCE PLUS SOLUTION FEASIBILITY

6.1 Potential applications of DF+ to address barriers

6.3 Scaling and execution capabilities

6.2 Viability of observed and potential business models

• In Tanzanian health, DF+ is limited to small pilot projects at different stages of the value chain

• These pilots both enhance previously offered payments and financial products through DF+ or offer newly enabled products

• Based on the finance gaps and the ability of DF+ to overcome different barriers, we have identified 6 DF+ products that have the

potential to deliver significant impact e.g.:

– DF+ can enable a more effective system of financial flows through supporting a payment system that incentivizes

community ambassadors to generate demand for health services and a payment system that enables subsidy

transfers to target segments for targeted health interventions

– DF+ can enable an effective new type of payment through a system that ties doctors’ salaries to performance

– DF+ can also aid in the provision of finance products as its use makes existing private insurance and lease-and-own

equipment models more effective while also making a novel maternity savings product possible

• Current DF+ efforts in Tanzania have been implemented only for a limited number of providers but lessons for viability have emerged

• The success of enhancing payments through DF+ (demand generation schemes and subsidy distribution) in various NGO pilots

for single conditions/products suggests a broader applicability to other conditions

• DF+-enabled pay for performance and maternity savings products have shown encouraging results in limited pilots

• The viability of digital private provider insurance and lease-and-own equipment remains to be tested

• Major scaling barriers exist in Tanzania given low system performance, the large role the government plays, patient’s lacking

understanding of financial products (especially insurance), and the lack of management capabilities

• Individual DF+ solutions are unlikely to have a compelling value proposition as a comprehensive reform package is necessary to

address the sector’s core problems

• Scaling of any DF+ solution will require government buy-in given that it directly controls and funds the vast majority of facilities and

medical personnel; limited pilots could be rolled-out in cooperation with the faith-based providers

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

18

There are low levels of finance provision in

the Tanzanian health sectorMinimal ModerateLimitedN/A

Number/reach of existing financial products

Minimal but efforts underway

Finance for

country's

purchase of Rx

and equipment

Finance for

medical students

Finance for

facilities to hire,

pay, and

incentivize labor

Finance for facility

infrastructure

improvement and

expansion

Finance for

purchasing of

Rx/equipment by

facility

Finance for patients

to pay for desired

health services

Financing for health

education and

demand generation

High

Ability to

access

Build desire

to accessLabor

Provision of care

Infra-

structure

Rx/

equipment

Input production/distribution

Rx and

equipmentMedical training

1 2 3 4

Patient

Dir

ect

len

din

gIn

su

ran

ce

Sav

ing

s

Payment

Routine

expenses

Catastro-

phic

expenses

Short term

Long term

Specific

type of

expenses

All health

expenses

Donor

financing

Facilities outside referral hospitals are unable to get credit from traditional providers

CHF and TIKA cover basic

medical expenses and are

available to all Tanzanians for low

subsidized prices; though overall

insurance covers <15% of

population

Traditional bank

administration

of small

accounts Is

unprofitable

and end

consumer travel

to make small

deposits has

high opportunity

cost

Donor focus on communicable diseases – HIV, etc.

Lump-sum payments required for treatment as no way exists to enforce payment post-treatment

Under current model

economics do not

justify banks

determining credit-

worthiness of

patients

CCBRTtransfers funds to ambassadors who provide information about maternity complications and facilitate proper care

Flexible payment plans allowed by teaching facilities

Some NGOs build and operate their own care facilities

CHF does not cover most secondary or tertiary care while National Health Insurance Fund is accepted at most secondary and tertiary providers

5.2 HEALTH – FINANCIAL GAP ANALYSIS ALONG THE VALUE CHAIN

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

19

Product

evaluation

Not all identified challenges are caused by a financial barrier or

can be addressed through a DF+ application

6.1 HEALTH – POTENTIAL APPLICATIONS OF DF+ TO ADDRESS BARRIERS

Finance as barrier DF+ potential No other barriers

Medical training2.1 System has health worker shortage

Rx and equipment

1.1 Temporary and systematic shortfall of drug supplies in

public facilities

Counterfeit drugs enter supply chain1.2

Supply chain deficiencies compromise certain Rx1.3

Labor2.2 Inconsistent application of best practices across facil-

ities, especially in lower level care settings

Low staff motivation leading to attendance and

retention problems

2.3

Infrastructure

Inability to follow up with patients and tracking them

through a unified system

2.4

2.5 Facilities lack basic access to utilities

2.6 Hospital shortage creates large distances to seek care

Rx and equipment2.7 Facilities lack ability to acquire and maintain

appropriate equipment

Ability to access

Inability of low-income households to effectively

access health expenditure financing products (savings

and insurance)

3.1

Households are unwilling or unable to pay for im-

portant health services

3.2

3.3 Transport constitutes a significant barrier to care

Desire to access4.1 Households do not seek treatment in appropriate

health facilities when condition warrants it

Inp

ut

pro

du

cti

on

Pro

vis

ion

of

care

Dem

an

d f

or

care

Detail

follows

Value chain segment Challenges

)(

Assessment of applicability of DF+ solution

High Low

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

20

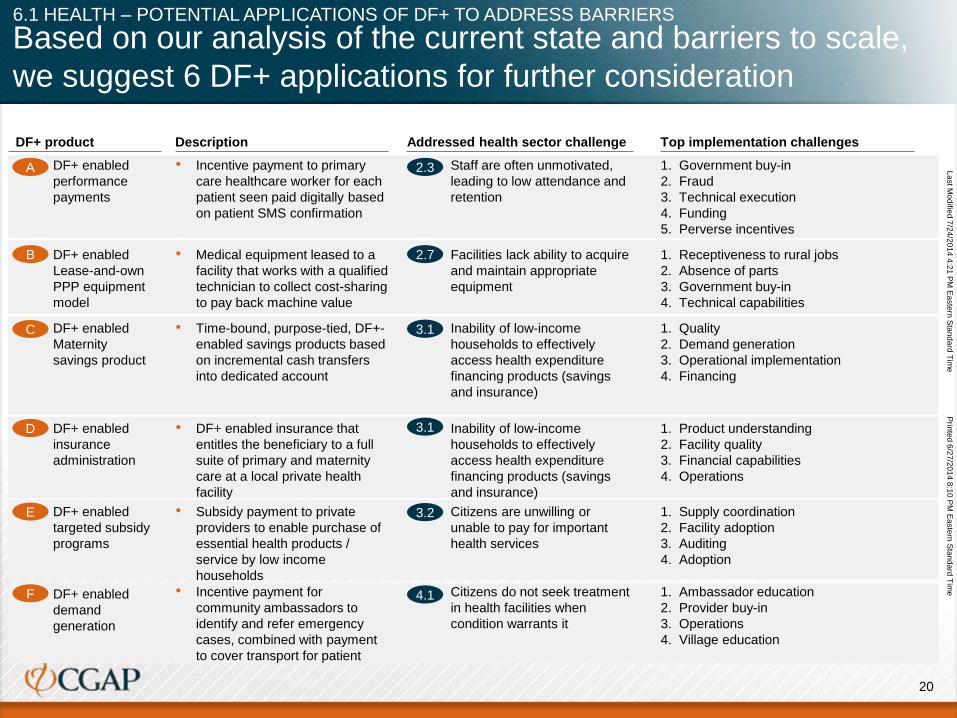

Top implementation challengesDescriptionDF+ product

Staff are often unmotivated,

leading to low attendance and

retention

2.3 1. Government buy-in

2. Fraud

3. Technical execution

4. Funding

5. Perverse incentives

• Incentive payment to primary

care healthcare worker for each

patient seen paid digitally based

on patient SMS confirmation

• DF+ enabled

performance

payments

2.7 Facilities lack ability to acquire

and maintain appropriate

equipment

1. Receptiveness to rural jobs

2. Absence of parts

3. Government buy-in

4. Technical capabilities

• Medical equipment leased to a

facility that works with a qualified

technician to collect cost-sharing

to pay back machine value

• DF+ enabled

Lease-and-own

PPP equipment

model

4.1 Citizens do not seek treatment

in health facilities when

condition warrants it

1. Ambassador education

2. Provider buy-in

3. Operations

4. Village education

• Incentive payment for

community ambassadors to

identify and refer emergency

cases, combined with payment

to cover transport for patient

• DF+ enabled

demand

generation

Inability of low-income

households to effectively

access health expenditure

financing products (savings

and insurance)

3.1 1. Quality

2. Demand generation

3. Operational implementation

4. Financing

• Time-bound, purpose-tied, DF+-

enabled savings products based

on incremental cash transfers

into dedicated account

• DF+ enabled

Maternity

savings product

Inability of low-income

households to effectively

access health expenditure

financing products (savings

and insurance)

3.1 1. Product understanding

2. Facility quality

3. Financial capabilities

4. Operations

• DF+ enabled insurance that

entitles the beneficiary to a full

suite of primary and maternity

care at a local private health

facility

• DF+ enabled

insurance

administration

3.2 Citizens are unwilling or

unable to pay for important

health services

1. Supply coordination

2. Facility adoption

3. Auditing

4. Adoption

• Subsidy payment to private

providers to enable purchase of

essential health products /

service by low income

households

• DF+ enabled

targeted subsidy

programs

Addressed health sector challenge

A

B

C

D

E

F

Based on our analysis of the current state and barriers to scale,

we suggest 6 DF+ applications for further consideration

6.1 HEALTH – POTENTIAL APPLICATIONS OF DF+ TO ADDRESS BARRIERS

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

21

DF+ solutions have different impacts … Key takeaways

Imp

act

High

Medium

Low

Low Medium High

Feasibility

A

B

D

C

F Demand

generation

E Subsidy

delivery

Pay for

performance

Lease-and-own

equipment

Insurance

product admin-

istrative tool

Maternity

savings

product

Requirements for scale

• Government buy-in is necessary given its role as a

funder of the majority of doctors and facilities

• Facility buy-in is necessary given that most mobile

solutions require doctor and administrator data input

• Improved health system quality to increase patient

system use; increased use will improve business model

feasibility and subsidy redemption rates

• Thus a government-led reform effort focused on quality

improvement is necessary to maximize DF+ impact

Steps to facilitate DF+ in health

• Focus initially on engaging the private sector to

implement DF+ solutions with sustainable business

models (lease-and-own equipment, maternity savings,

insurance administrative tool)

• Engage donor organizations to encourage the

implementation of more demand generation and subsidy

delivery efforts

• Encourage collaboration among stakeholders to

implement the solutions that will have the most impact at

scale

Potential DF+ applications in health can be categorized based on

their feasibility and potential impact

6.2 HEALTH – VIABILITY OF OBSERVED AND POTENTIAL BUSINESS MODELS

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

22

In the Health sector, DF+ solutions are nascent but growing

Discovery

Piloting

Scale

Application

Expansion and

differentiation

Global scaling

DF+ solution

maturity

• DF+ solutions in

ideation or early

development stage

• Individual DF+

solutions are being

piloted in controll-

ed environments

by selected actors,

especially donors

• Smaller players

have implemented

DF+ into

operations across

conditions

• Some DF+

solutions begin to

be used by large

health system

players (e.g.,

MSD, MOH public

facilities, large

private providers)

• DF+ becomes an

essential

component of the

provision of care

and proposed

health system

reform

• Growth

financing/

subsidy

• Growth

financing/

subsidy and

innovation

support

• Implementation

support

• Convene

stakeholders to

discuss

expansion

• Financial and

technical advice

during piloting

phase

• Best practice

sharing

• Operating model

development

activities

• The health sector lags other sectors in the adoption of mobile payments

• Donor organizations are piloting subsidy-based demand and access generation for a limited set of products

• The use of DF+ is unlikely to be a tipping point in financial product availability to facilities or BoP consumers

• However, unexplored business models do exist for maternity savings, insurance, and lease-and-own equipment

• The scaling of DF+ solutions will depend on government incorporation into comprehensive reform

6.3 HEALTH – SCALING AND EXECUTION CAPABILITIES

Inte

rve

nti

on

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

23

Agenda

Sector analysis – energy

Sector analysis and challenge identification

Assessment of financial service needs and gap analysis

Digital finance plus solution feasibility assessment

Overall assessment framework

Sector analysis – agriculture

Sector analysis – health

Role of the government and regulation

Access to and reach of mobile infrastructure

Sector analysis water

Sector analysis education

Adoption and reach of digital payment infrastructure

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

24

▪ 85% of the country is covered by a 2G network, with some concern

about the quality of service in the most rural areas

▪ High penetration, at ~60% of households, with some concern about

the ownership of handsets and proficient usage by poorest

households

▪ Lending to consumers and enterprises by banks and MFIs is minimal.

Robust equity financing for enterprises by VC actors and other

investors

▪ Several innovative energy enterprises are using DF+ to deploy

different financing solutions to consumers

▪ Highly conducive – existing solar enterprises are almost entirely

unregulated given their capacity is less than 100kw capacity

▪ The government is involved through two agencies n/a EWURA

regulates and REA facilitates – both are conducive to off-grid energy

development

▪ Little complexity – primary actors are energy enterprises and

households with demand for electricity access

▪ Moderate – a poor rural infrastructure inhibiting “last mile” reach and

lack of consumer knowledge of off-grid benefits are most notable

▪ Somewhat deep – almost all energy enterprises provide financing

support to consumers, but their own access to working capital is

limiting

▪ Highly applicable – allows enterprises to cut transaction costs,

enhance contract enforcement, and provide additional services

▪ Successful enterprises have identified winning technologies, built low-

cost, effective distribution networks, and established a loyal base of

customers

▪ Currently, SHS reach is 50,000-100,000 households. “True scale” of

1million + will be reached with the introduction of commercial lending,

consumer education and the expansion of distribution networks

DF+ implementation in the energy sector faces varying levels of

constraints

6.2 ENERGY – VIABILITY OF OBSERVED AND POTENTIAL BUSINESS MODELS

Sector readiness dimension

Sector-rele-

vant mobile

infrastructure

reach and

adoption

Readiness of

financial and

digital

financial

infrastructure

65

4 32

1

65

4 32

1

Role of

government

and

regulation

6

54 3

2

1

Severity of

sector

challenges

65

4 32

1

Financial gap

in sector

65

4 32

1

DF+ business

models and

scaling

65

4 32

1

Reach

Reach of mobile

infrastructure

Adoption of mobile

technology

Financial product

offering to sector

Availability of

DF+ solutions

Sector-specific

regulation

Role of

government

Stakeholder

complexity

Non-financial chal-

lenges in sector

Execution and

scalling ability

Depth of financial

gap

Availability of DF+

business models

Sub-dimensions

Applicability of

DF+ solutions

1

Binding constraint Readiness for scaling

2 3 54 Explanation

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

25

6.1 Potential applications of DF+ to address barriers

Key takeaways: Energy sector – Digital finance plus solution

feasibility

ENERGY – DIGITAL FINANCE PLUS SOLUTION FEASIBILITY

6.3 Scaling and execution capabilities

• The off-grid energy space in Tanzania includes several players (6-8 notables companies, including Mobisol, Off.Grid :Electric, Devergy and EGG-energy), many of whom have integrated DF+ as an essential enabler of their business models. The se energy enterprises have modest scale, with each player serving ~1,000 to ~20,000 households today

• For the majority of these players, DF+ facilitates mobile payments (pre-paid, pay-as-you-go, and post-paid schemes for energy services and/or energy hardware leasing and/or ownership), allows remote regulation (enabling/disabling energy provision through a control box, providing network maintenance), and enables two-way communication with customers (SMS alerts for payments, maintenance, consumption modulation).

• Thus, DF+ encourages energy enterprises to offer products and financing by enabling contract enforcement, cutting the cost of customer service, driving scale, and providing scope for additional services

• The successful solar enterprises have identified winning technologies, built low-cost and effective distribution networks with “last mile” reach, and deployed capital productively by acquiring creditworthy customers and providing them with financing, thereby fortifying a loyal and growing customer base, as well as establishing credibility with investors

• With payback periods of up to 2 years by customer, many of the nascent players, mostly having entered the market around 2010, are beginning to turn profits on their first wave of customers

• Given the solar enterprises are proving commercial viability, investors are expressing enthusiasm to fundraising new equity, with many rounds being oversubscribed; however, securing commercial loans without donor support continues to be a challenge

• Today, there are estimated to be 50,000-100,000 total off-grid connections in Tanzania. Depending on the business model, “true scale” (profitable including over-head) for a single energy enterprise can range from 20,000 customers (household solar systems) to 80,000 connections (solar micro-grids); for nation-wide operations “true scale” number of off-grid customers to be closer 1 million households

• For the off-grid sector and individual businesses to attain scale, there are a few key areas of focus, including financing through commercial lending, awareness-creation in rural populaces about the benefits of OG solutions, and the establishment of wide, efficient, and cost-effective networks for sales and user support

6.2 Viability of observed and potential business models

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

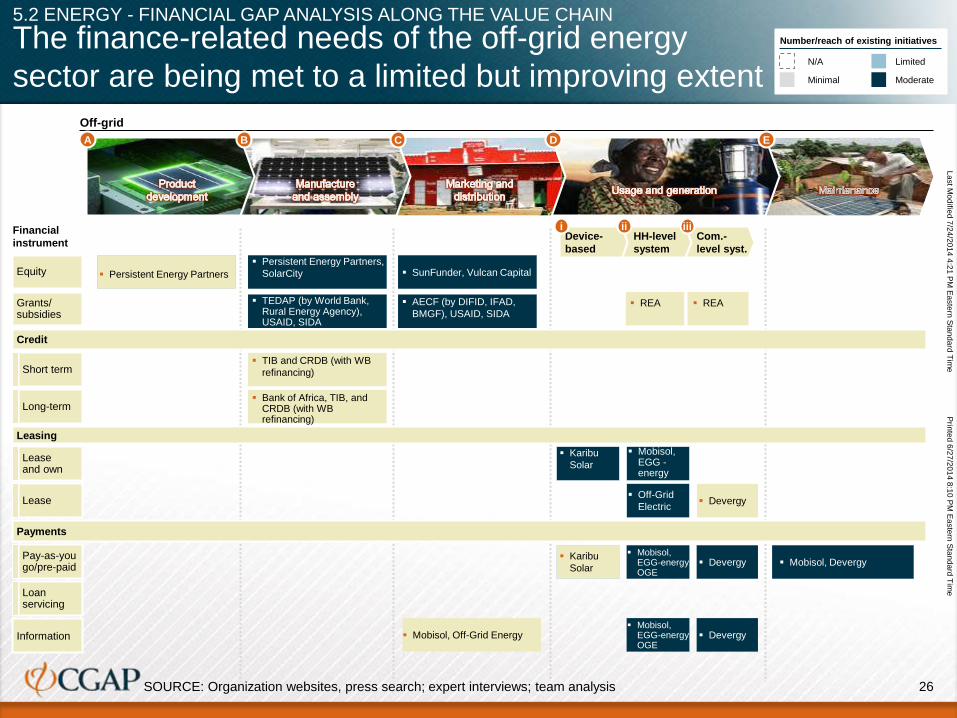

26SOURCE: Organization websites, press search; expert interviews; team analysis

The finance-related needs of the off-grid energy

sector are being met to a limited but improving extent Minimal Moderate

LimitedN/A

Number/reach of existing initiatives

Financial

instrument

Payments

Credit

Grants/subsidies

Information

Short term

Long-term

Lease and own

Lease

Loan servicing

Pay-as-yougo/pre-paid

Equity

Leasing

Persistent Energy Partners,

SolarCity SunFunder, Vulcan Capital

TEDAP (by World Bank, Rural Energy Agency), USAID, SIDA

AECF (by DIFID, IFAD,

BMGF), USAID, SIDA

TIB and CRDB (with WB

refinancing)

Bank of Africa, TIB, and CRDB (with WB refinancing)

REA REA

Karibu

Solar

Mobisol, EGG -energy

Off-Grid

Electric Devergy

Karibu

Solar

Mobisol, EGG-energy, OGE

Devergy

Devergy Mobisol, Off-Grid Energy

Mobisol, Devergy

Persistent Energy Partners

Off-grid

D EA B C

Device-

based

HH-level

system

Com.-

level syst.

i ii iii

Mobisol, EGG-energy, OGE

5.2 ENERGY - FINANCIAL GAP ANALYSIS ALONG THE VALUE CHAIN

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

27

DF+ can help in addressing some of the gaps

in the off-grid energy value chain

Value chain segment ChallengesProduct

evaluation

Finance

as barrier

DF+

potential

No other

barriers

Assessment of applicability of DF+ solution

)(

)(

A2

B1

C1

C2

C3

C4

D1/2

D3

D4

E1

E2

E3

A1 Insufficient business development financing

Insufficient local research and development capacity

Insufficient product financing

Insufficient working capital finance

Insufficient consumer awareness

Insufficient distribution reach

Insufficient consumer risk management experience and tools

Insufficient consumer lending to low-income households

Complex payment administration

Unavailability of liquidity facility

Lack of effective maintenance

Insufficient upgrade financing

Unavailability of protection against theft or destruction of equipment

)(

)(

DF+ solution

Add-on to core

DF+ solution)(

6.1 ENERGY – POTENTIAL APPLICATIONS OF DF+ to ADDRESS BARRIERS

Product

development

Manufacture and

Assembly

Marketing and

Distribution

Usage and

Generation

Maintenance

High Low

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

28

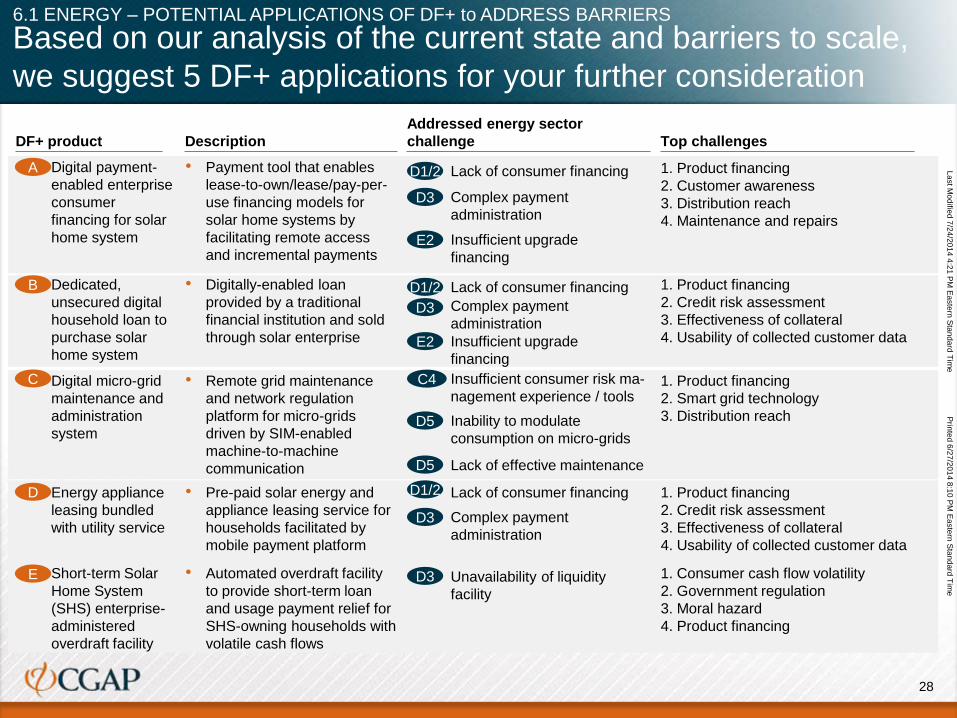

Top challengesDescriptionDF+ product

Lack of consumer financingD1/2 1. Product financing

2. Customer awareness

3. Distribution reach

4. Maintenance and repairs

• Payment tool that enables

lease-to-own/lease/pay-per-

use financing models for

solar home systems by

facilitating remote access

and incremental payments

• Digital payment-

enabled enterprise

consumer

financing for solar

home system

Addressed energy sector

challenge

A

1. Product financing

2. Credit risk assessment

3. Effectiveness of collateral

4. Usability of collected customer data

• Digitally-enabled loan

provided by a traditional

financial institution and sold

through solar enterprise

• Dedicated,

unsecured digital

household loan to

purchase solar

home system

B

1. Product financing

2. Smart grid technology

3. Distribution reach

• Remote grid maintenance

and network regulation

platform for micro-grids

driven by SIM-enabled

machine-to-machine

communication

• Digital micro-grid

maintenance and

administration

system

C

Lack of consumer financing 1. Product financing

2. Credit risk assessment

3. Effectiveness of collateral

4. Usability of collected customer data

• Pre-paid solar energy and

appliance leasing service for

households facilitated by

mobile payment platform

• Energy appliance

leasing bundled

with utility service

D

Insufficient consumer risk ma-

nagement experience / tools

C4

Insufficient upgrade

financing

E2

Complex payment

administration

D3

1. Consumer cash flow volatility

2. Government regulation

3. Moral hazard

4. Product financing

• Automated overdraft facility

to provide short-term loan

and usage payment relief for

SHS-owning households with

volatile cash flows

• Short-term Solar

Home System

(SHS) enterprise-

administered

overdraft facility

E

Based on our analysis of the current state and barriers to scale,

we suggest 5 DF+ applications for your further consideration

6.1 ENERGY – POTENTIAL APPLICATIONS OF DF+ to ADDRESS BARRIERS

D1/2

Lack of consumer financingD1/2

Insufficient upgrade

financing

E2

Complex payment

administrationD3

Inability to modulate

consumption on micro-grids

D5

D5 Lack of effective maintenance

Complex payment

administration

D3

D3 Unavailability of liquidity

facility

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

29

Potential DF+ applications in energy can be categorized based on

their feasibility and potential impact

DF+ solutions have different impacts Key takeaways

Imp

act

High

Medium

Low

Low Medium High

Feasibility

• The off-grid energy space in Tanzania is beginning to witness

several innovative players

• Companies provide solutions that focus on mobile energy

generators for individual devices, household-based generation

systems for multi-purpose usage as well as mini- and micro-

grid services with solar, biomass, and hydro distributed

generation

• Further opportunities exist in providing services, such as

distribution, salesforce management and maintenance, for the

solar energy enterprises

• Many of the innovations integrate mobile technology and end-

consumer financing as fundamental enablers of their business

models (e.g., Off-Grid Energy, Mobisol)

• Although the innovative players have enjoyed success on

relatively localized levels, scaling to regional and national levels

has been a challenge given limited capital, weak distribution,

and lack of customer awareness

• To spur further innovation and scaling, the focus of enabling

stakeholders should be on providing debt and equity financing

to promising enterprises, creating awareness of off-grid

solutions in rural areas, educating the financial sector, and

providing financing to households

• Digital payment

enabled

consumer

financing for SHS

• Remote micro-

grid admin. and

regulation

• Short-term

overdraft facility

for SHS

customers

• Energy appliance

leasing bundled

with utility service

• Unsecured

digital

consumer bank

loan for SHS

6.2 ENERGY – VIABILITY OF OBSERVED AND POTENTIAL BUSINESS MODELS

AB

C

D

E

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

30

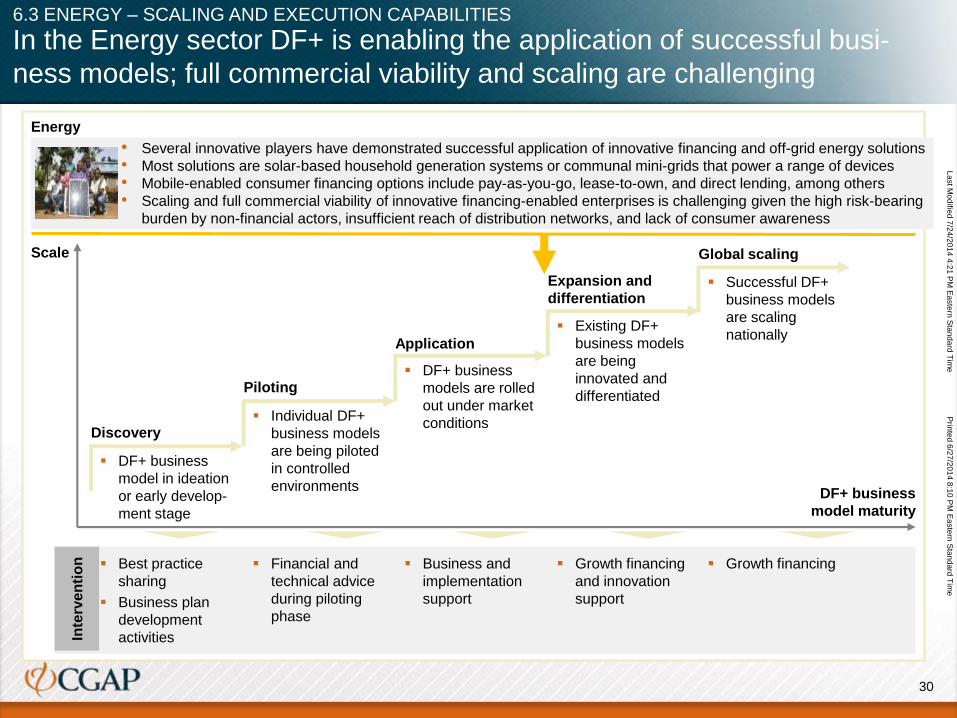

In the Energy sector DF+ is enabling the application of successful busi-

ness models; full commercial viability and scaling are challenging

Discovery

Piloting

Scale

Application

Expansion and

differentiation

Global scaling

DF+ business

model maturity

DF+ business

model in ideation

or early develop-

ment stage

Individual DF+

business models

are being piloted

in controlled

environments

DF+ business

models are rolled

out under market

conditions

Existing DF+

business models

are being

innovated and

differentiated

Successful DF+

business models

are scaling

nationally

Energy

Best practice

sharing

Business plan

development

activities

Financial and

technical advice

during piloting

phase

Business and

implementation

support

Growth financing

and innovation

support

Growth financing

• Several innovative players have demonstrated successful application of innovative financing and off-grid energy solutions

• Most solutions are solar-based household generation systems or communal mini-grids that power a range of devices

• Mobile-enabled consumer financing options include pay-as-you-go, lease-to-own, and direct lending, among others

• Scaling and full commercial viability of innovative financing-enabled enterprises is challenging given the high risk-bearing

burden by non-financial actors, insufficient reach of distribution networks, and lack of consumer awareness

6.3 ENERGY – SCALING AND EXECUTION CAPABILITIES

Inte

rve

nti

on

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

31

Agenda

Sector analysis energy

Sector analysis education

Sector analysis and challenge identification

Assessment of financial service needs and gap analysis

Digital finance plus feasibility assessment

Sector analysis health

Sector analysis agriculture

Overall assessment framework

Access to and reach of mobile infrastructure

Adoption and reach of digital payment infrastructure

Role of the government and regulation

Sector analysis water

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

32

DF+ implementation in the education sector faces varying levels

of constraints

▪ 85% of the country is covered by a 2G network; selected rural areas remain a problem

▪ High penetration at ~60% of households, with some concern about female access to mobile phone within the household

▪ Low level of private lending and savings for education as BoP consumers are considered unattractive

▪ The government drives reform in the sector and is currently not focused on DF+

▪ Regulation neither helps nor hinders growth of DF+

▪ The government is a major player in the sector and has not adopted technologies

▪ Government adoption would affect 95% of the students in public schools

▪ Severe non-financial challenges are related to absenteeism, quality of instruction, pupil:teacherratio

▪ The majority of low-income households do not use any form of finance products for education

▪ DF+ solutions can play a part in improving attendance, increasing the ability to pay for school and access textbooks

▪ While models are impactful, they largely have unclear business models

▪ Execution and scaling would need to be undertaken largely by government actors

6.2 EDUCATION – VIABILITY OF OBSERVED AND POTENTIAL BUSINESS MODELS

Sector readiness dimension

Sector-rele-

vant mobile

infrastructure

reach and

adoption

Readiness of

financial and

digital

financial

infrastructure

65

4 32

1

65

4 32

1

Role of

government

and

regulation

6

54 3

2

1

Severity of

sector

challenges

65

4 32

1

Financial gap

in sector

65

4 32

1

DF+ business

models and

scaling

65

4 32

1

Reach

Reach of mobile

infrastructure

Adoption of mobile

technology

Financial product

offering to sector

Availability of

DF+ solutions

Sector-specific

regulation

Role of

government

Stakeholder

complexity

Non-financial chal-

lenges in sector

Execution and

scalling ability

Depth of financial

gap

Availability of DF+

business models

Sub-dimensions

Applicability of

DF+ solutions

1

Binding constraint Readiness for scaling

2 3 54 Explanation

La

st M

od

ified

7/2

4/2

01

4 4

:21

PM

Ea

ste

rn S

tan

da

rd T

ime

Prin

ted

6/2

7/2

01

4 8

:10

PM

Ea

ste

rn S

tan

da

rd T

ime

33

Key Takeaways

6.2 Viability of observed and potential business models

• With the majority of identified products and business models in the pilot phase, their viability is yet to be seen

• However, some of the major challenges to implementation include educating consumers on how the products work and ensuring

that schools, parents, and teachers have the requisite equipment to access the product

• Additionally, several of these products have the potential for fraud; as such, it will be critical to implement appropriate checks and

balances and refine the business models over time

6.3 Scaling and execution capabilities

• Major scaling barriers in Tanzania are due to the large role the government has in the education systems and the lack of

understanding of financial products among low-income consumers

• To scale many of these products, entrepreneurs and donors will have to work with the Ministry of Education and Vocational

Training, which is already spread thin with its current responsibilities

• Given the lack of financial products for low-income consumers, a high-touch approach will be required to educate parents and

schools on the products’ usage