diego de león, 21 28006 madrid land & business registrars’ association of spain beatriz...

TRANSCRIPT

Diego de León, 21 28006 Madrid

Land & Business Registrars’ Association of SpainBeatriz CorredorFrancisco Molina

Pedro Pernas

Amsterdam, September 2012

FORECLOSURE AND SPANISH LAND REGISTRY

LA EJECUCIÓN HIPOTECARIA SOBRE LA VIVIENDA HABITUAL

Haga clic para modificar el estilo de título del patrón

2120918_CINDER Foreclosure and Spanish Land Registry

1. Introduction

2. Mortgage evaluation

3. Foreclosure proceedings: special aspects

4. Efficiency of the foreclosure in Spain.

Haga clic para modificar el estilo de título del patrón

3120918_CINDER Foreclosure and Spanish Land Registry

1. INTRODUCTION

• The Spanish Registry is a title registry.

• Mortgage Act, articles 1, 9.4, 13, 34, 38 y 41.

• Principle of mirror:

– It reflects accurately the rights on real property.

• Principle of curtain:

– It is sufficient to check out the Land Registry to know the title to the property and the charges in force.

• Principle of assurance:

– To publish and to guarantee legality and certainty of what is published.

Haga clic para modificar el estilo de título del patrón

4120918_CINDER Foreclosure and Spanish Land Registry

1. INTRODUCTION

THE SPANISH REGISTRY AS A TITLE REGISTRY: JUSTIFICATION

• Decision of the Constitutional Court of April 24th, 1997

– The Land Registry is a title registry.

– The entry is independent from the title.

– The effects of the registered right derive only from the Registry.

– There is no giving evidence of the document but a certificate of registration that entails assignment of rights.

• Decision of December 18th, 1981

– It states the constitutionality of the summary foreclosure proceedings with grounds on the right registered in the Registry.

Haga clic para modificar el estilo de título del patrón

5120918_CINDER Foreclosure and Spanish Land Registry

1. INTRODUCTION

THE SPANISH REGISTRY AS A TITLE REGISTRY: JUSTIFICATION

• Decisions of the High Court of March 5th and September 7th, 2007

– Legal doctrine on compulsory observance for all Spanish courts.

– Article 34 of the Mortgage Act entails a registry of rights.

• The Registry covers the lack of right to dispose of, thus maintaining the person that relied on the Registry for his/her purchase, even if the preceding contract was null and void but not his/her one.

• Decisions of the Directorate General of Registries and Notaries of May 25th, 2009 and April 19th, 2010

– The evaluation of a Registrar is a statement of the principle of effective judicial protection of art. 24 of the Spanish Constitution.

Haga clic para modificar el estilo de título del patrón

6120918_CINDER Foreclosure and Spanish Land Registry

1. INTRODUCTION

THE SPANISH REGISTRY AS A TITLE REGISTRY: JUSTIFICATION

• Decisions of the High Court of March 5th and September 7th, 2007

– Legal doctrine on compulsory observance for all Spanish courts.

– Article 34 of the Mortgage Act implies a registry of rights.

• The Registry covers the lack of right to dispose of, thus maintaining the person that relied on the Registry for his/her purchase, even if the preceding contract was null and void but not his/her one.

Haga clic para modificar el estilo de título del patrón

7120918_CINDER Foreclosure and Spanish Land Registry

1. Introduction

2. Mortgage evaluation

3. Foreclosure proceedings: special aspects

4. Efficiency of the foreclosure in Spain.

Haga clic para modificar el estilo de título del patrón

8120918_CINDER Foreclosure and Spanish Land Registry

2. MORTGAGE EVALUATION

REGISTRY OF DEEDS REGISTRY OF TITLES (SPANISH SYSTEM)

Registry of Deeds vs. Registry of Titles: efficiency of the registration and authorities of the registry clerk.

The effects of the registration are very limited:

• Mere publicity without presumption of accuracy.

• The registry does not prove title to the right and we can not trust the accuracy of the registrations; the title filed prevails. Registration does only establish priority.

• There is no control of legality by the registrar (passive nature).

Wide effects:• Registration prevails over the deed–Decision of

the Constitution Court of April 24th, 1997-.• Legal attestation: The State guarantees the

contents of the registered right and the legitimacy of the owner: full right to dispose of. Registration as establisher of rights (“security” Fernando Méndez).

• Strict control on formal aspects and on substantial aspects (active nature).

Consequence

• An additional investigation is necessary • No additional investigation is necessary.• It strengthens the legal real property

transactions in eliminating uncertainty.

Haga clic para modificar el estilo de título del patrón

9120918_CINDER Foreclosure and Spanish Land Registry

2. MORTGAGE EVALUATION

EVALUATION IN THE ESTABLISHMENT OF A MORTGAGE• It consists of a notarial deed that is more strictly evaluated than judicial documents (18 of the Mortgage Act and 98 of

the Mortgage Regulations).

• The contents of the right is established through registration; the registrar sets up the right by choosing the terms that shall form part of the entry, and such contents shall be the subject of the certificate on which the foreclosure shall subsequently be based.

• The mortgage loan agreement shall consist of:

– Credit (obligational, inter partes).

– Mortgage (real estate, erga omnes –vis-à-vis third party purchasers and any creditor or subsequent owner of rights).

• Subject of evaluation:

– Clauses with real estate consequence: Set up the mortgage right itself (nature of the obligation and its extension, term of duration, details for the foreclosure...).

– Financial clauses:

• Set up the loan agreement, the fulfilment of which is guaranteed with the mortgage.

• Have access to the registry as the mortgage has had access to it; have erga omnes effects and are the subject of evaluation.

• The advanced maturity clauses must be evaluated because they affect the duration and, hence, third parties (DGRN and High Court Decision 16th November 2009; Directive 92/12-RDLaw 1/2007 Consumers & Users).

Haga clic para modificar el estilo de título del patrón

10120918_CINDER Foreclosure and Spanish Land Registry

2. MORTGAGE EVALUATION

EVALUATION IN THE FORECLOSURE OF THE MORTGAGE

• A judicial document is evaluated –writ of allocation and order of cancellation of charges- (18 of Mortgage Act and 100 of Mortgage Regulations).

• Evaluation is necessary for it has erga omnes effects (the decision has inter partes effects).

• Subject of evaluation:

– Territorial competence.

– Consistency.

– Notifications to the registered owners Importance of the marginal note that informs on the proceedings.

– If credit of the plaintiff is lower than the value of the allocation, the amount in excess must be deposited.

Haga clic para modificar el estilo de título del patrón

11120918_CINDER Foreclosure and Spanish Land Registry

1. Introduction

2. Mortgage evaluation

3. Foreclosure proceedings: special aspects

4. Efficiency of the foreclosure in Spain.

Haga clic para modificar el estilo de título del patrón

12120918_CINDER Foreclosure and Spanish Land Registry

3. FORECLOSURE PROCEEDINGS: SPECIAL ASPECTS

FORECLOSURE PROCEEDINGS

• APPROACH: The mortgage creditor has different possibilities.

• ORDINARY DECLARATORY PROCEEDING

• FORECLOSURE PROCEEDINGS

– Extra-judicial sale proceeding before Notary.

– Ordinary foreclosure proceeding.

– Special foreclosure proceeding (the Decision of the Constitutional Court of December 18th, 1981 recognized its constitutionality).

Haga clic para modificar el estilo de título del patrón

13120918_CINDER Foreclosure and Spanish Land Registry

REGULATION

OBJECT

Special regulations apply and the provisions on ordinary monetary foreclosure apply in a supplementary way

The creditor may only act against the registered property.

LEGITIMACY ACTIVE: creditor with mortgage registered in his favour

REQUIREMENTS Title requirements (public deed):• Registration (the public deed must be registered) It is accredited

with the registration note or registry certificate.• Assessment value and address for injunctions and notifications that

must be stated on the registration.Debt requirements:

• The debt must be certain, liquidated and due and, therefore, payable.• The debt claimed must be within the limits of the registration (which

distinguishes principal, interests and costs).

JURISDICTIONGeneral rule : Courts of First Instance of the place on which property is located.If there are several mortgaged properties: any court with competence at the choice of the petitioner

3. FORECLOSURE PROCEEDINGS: SPECIAL ASPECTS

SPECIAL FORECLOSURE PROCEEDING

Haga clic para modificar el estilo de título del patrón

14120918_CINDER Foreclosure and Spanish Land Registry

3. FORECLOSURE PROCEEDINGS: SPECIAL ASPECTS

PROCEEDING STAGES

PROCEEDING:

1. Foreclosure writ

2. Judicial order on the enforcement of the foreclosure [+ judicial payment summons].

3. Registry certificate of ownership and charges + marginal note of issue of certificate.

4. Notification of proceeding to owners of subsequent charges.

5. Mandatory disposal of the mortgaged property.

6. Payment of credit and application of the exceeding amount.

7. Registration of the property in the name of the person to which it is allotted.

8. Cancellation of the registered mortgage and of subsequent entries.

Haga clic para modificar el estilo de título del patrón

15120918_CINDER Foreclosure and Spanish Land Registry

3. FORECLOSURE PROCEEDINGS: SPECIAL ASPECTS

SPECIAL ASPECTS: PRINCIPLE RESIDENCE

• Approach The foreclosure has several special aspects when it affects a principle residence.

• CASES:

– Consent of both spouses to mortgage the family principle residence.

– Right of use of the mortgaged family residence as a consequence of marriage annulment, separation or divorce proceedings:

• The consent of the spouse who has title to the right is required in order to establish the mortgage.

• In case of foreclosure, it is notified to him if he appears at the moment of issue of the certificate of ownership and charges; but if the property is allotted, the right is extinguished.

– Advanced maturity in case of non-payment of an installment:

• The consent of the creditor is not necessary in order for the debtor to finish the proceedings by paying the capital and interests of the debt.

• He can exercise this authority every five years at the most.

– Insufficiency of what is obtained to fully cover the creditor’s credit.

• The debtor shall only be released if the limit to mortgage liability has been stipulated.

• But… there is a social wave that considers it unfair and also several judicial decisions.

Haga clic para modificar el estilo de título del patrón

16120918_CINDER Foreclosure and Spanish Land Registry

3. FORECLOSURE PROCEEDINGS: SPECIAL ASPECTS

SPECIAL ASPECTS: PRINCIPLE RESIDENCE

– Protection measures of mortgage debtors without resources RD Law 6/2012, of March 9th:

• They apply in cases of adhesion of the credit entity.

• The interest of late-payment is limited.

• The lease of the residence by the debtor is encouraged after the foreclosure.

• The extra-judicial foreclosure proceedings of the debtor’s principle residence is simplified with the celebration of an auction.

• Payment on account:

The payment on account is encouraged, which can be requested if the restructuring of the debt is not feasible.

The debtor can continue as lessee.

» Aids for the renting can be requested

Haga clic para modificar el estilo de título del patrón

17120918_CINDER Foreclosure and Spanish Land Registry

3. FORECLOSURE PROCEEDINGS: SPECIAL ASPECTS

SPECIAL ASPECTS: BANKRUPTCY PROCEEDINGS

• With the bankruptcy proceeding the foreclosure stops

– The competent judicial authority for the bankruptcy proceedings has to settle whether the property is affected or not to the professional or business activity.

• If the real estate is not affected, the creditors can continue with the proceedings or start it.

• If the real estate is affected, the proceedings may start or continue till the voluntary agreement is approved or a year elapses as from the opening of the bankruptcy proceedings.

– Once the term has elapsed, the creditor may continue with the foreclosure before the judge of the bankruptcy proceedings.

Haga clic para modificar el estilo de título del patrón

18120918_CINDER Foreclosure and Spanish Land Registry

3. FORECLOSURE PROCEEDINGS: SPECIAL ASPECTS

SPECIAL ASPECTS: MORTGAGE TITLES

• Mortgage market in Spain:

– General requirements:

• Issuers: Banks, saving funs, Spanish Confederation of Saving Funds (CECA), credit cooperative companies and credit finance establishments.

• Underlying assets:

Mortgage loans or credits with a priority over other mortgages or conditions subsequent.

The relation between the loan or credit and the value of the property must be less than 60%, unless it is used to finance the building, renovating or purchase of a property (it can reach al 80 %). With additional warrantees it can reach 95 %.

– Kinds of titles:

• Loan agreements: 80,6 %

• Bonds: 0 % (not used)

• Mortgage shares: 2,3 % subscribed through Mortgage securitization funds.

• Certificates of mortgage transfer (they are “mortgage shares” in which the underlying assets do not fulfil the requirements): 17,2 % subscribed through Assets securitization funds.

Haga clic para modificar el estilo de título del patrón

19120918_CINDER Foreclosure and Spanish Land Registry

3. FORECLOSURE PROCEEDINGS: SPECIAL ASPECTS

SPECIAL ASPECTS: MORTGAGE TITLES

• Legal system

– In the mortgage loan agreements and bonds, the owner does not take part in the foreclosure.

– In the mortgage shares or in the certificates of transfer of mortgage, the owner may:

• Oblige the issuer to initiate the foreclosure.

• Take a pro rata share in the results of the proceedings.

• Initiate the proceedings, if the issuer does not execute the mortgage 60 days after the summons.

• Continue with the proceedings if it has been suspended.

– The mortgage securitization funds and Assets securitization funds –owners of the shares or of the certificate of transfer of the mortgage- can be owners of the properties obtained from a judicial or extra-judicial proceeding.

Haga clic para modificar el estilo de título del patrón

20120918_CINDER Foreclosure and Spanish Land Registry

1. Introduction

2. Mortgage evaluation

3. Foreclosure proceedings: special aspects

4. Efficiency of the foreclosure in Spain.

Haga clic para modificar el estilo de título del patrón

21120918_CINDER Foreclosure and Spanish Land Registry

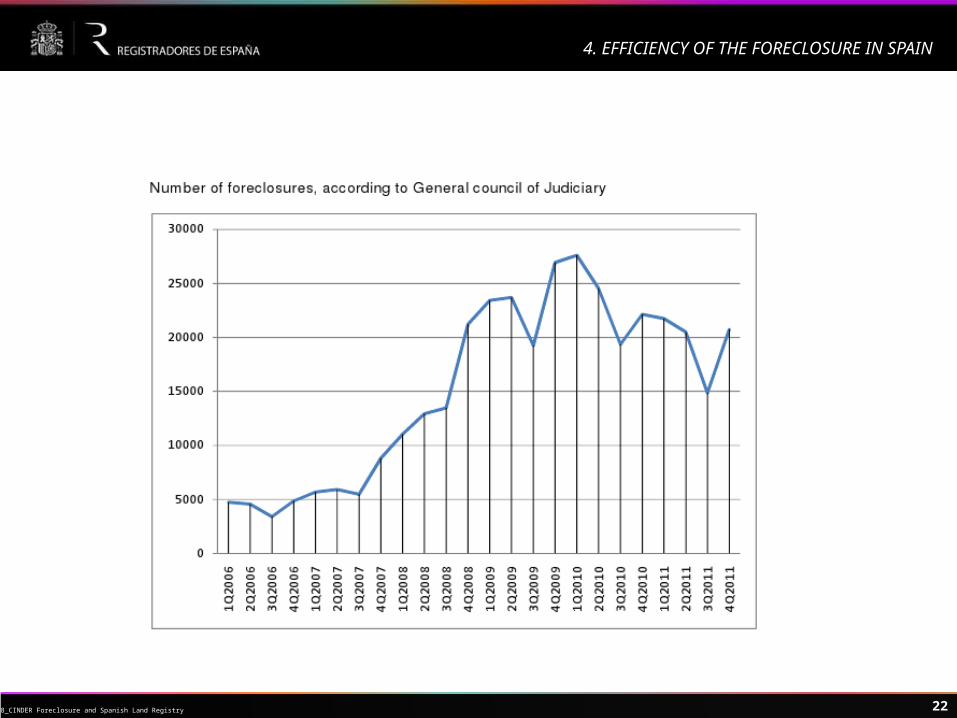

4. EFFICIENCY OF THE FORECLOSURE IN SPAIN

Haga clic para modificar el estilo de título del patrón

22120918_CINDER Foreclosure and Spanish Land Registry

4. EFFICIENCY OF THE FORECLOSURE IN SPAIN

Haga clic para modificar el estilo de título del patrón

23120918_CINDER Foreclosure and Spanish Land Registry

4. EFFICIENCY OF THE FORECLOSURE IN SPAIN

Haga clic para modificar el estilo de título del patrón

24120918_CINDER Foreclosure and Spanish Land Registry

4. EFFICIENCY OF THE FORECLOSURE IN SPAIN

Haga clic para modificar el estilo de título del patrón

25120918_CINDER Foreclosure and Spanish Land Registry

THANK YOU FOR YOUR ATTENTION